COVID-19 Outbreak and CO2 Emissions: Macro-Financial Linkages

Abstract

:1. Introduction

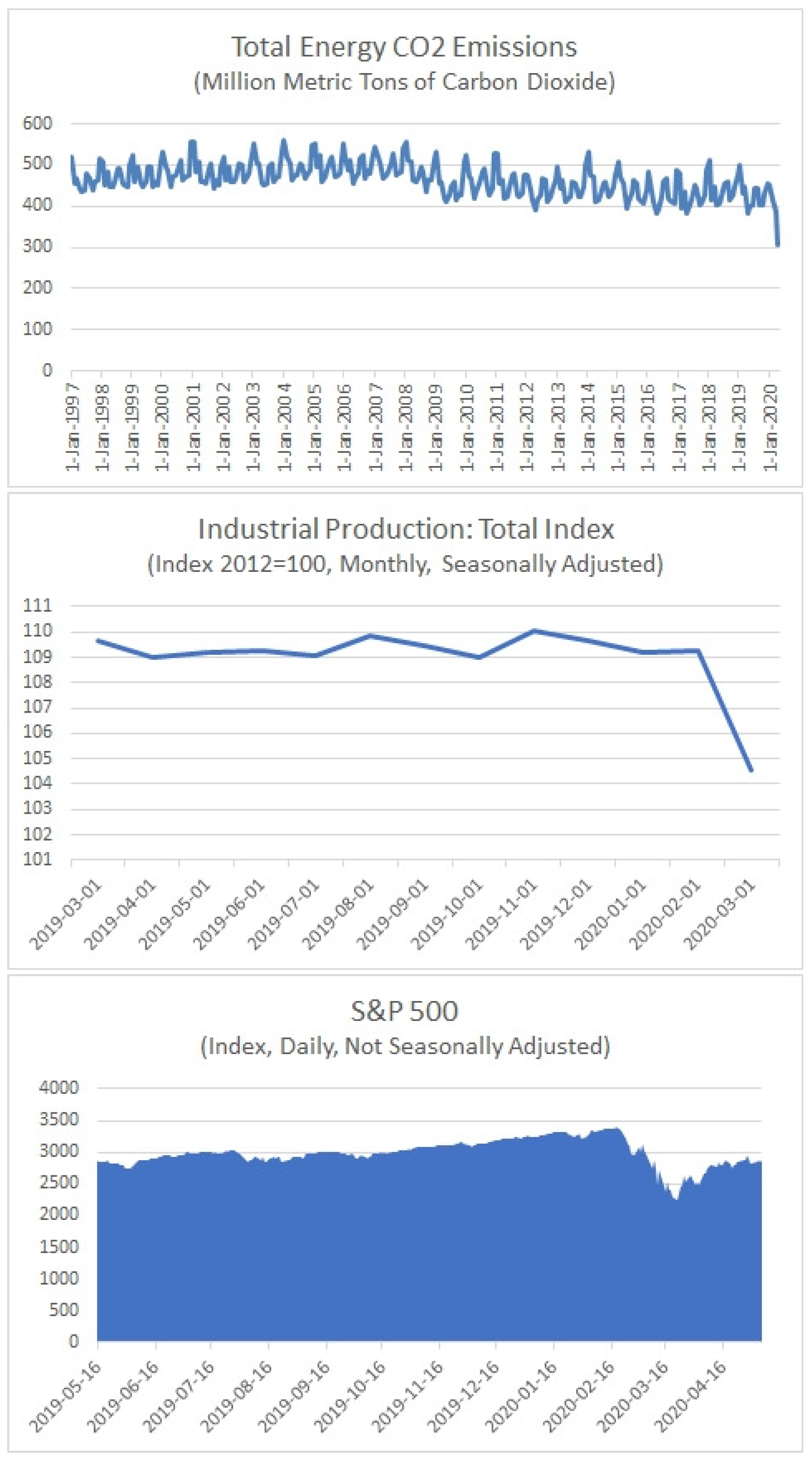

2. Data

2.1. U.S. COVID-19 Cases

- confirmed cases,

- deaths, and

- recovered cases.

2.2. U.S. Macroeconomic Indicators and CO Emissions

2.3. U.S. Stock Markets

2.4. Series’ Transformation

3. Model

4. Results

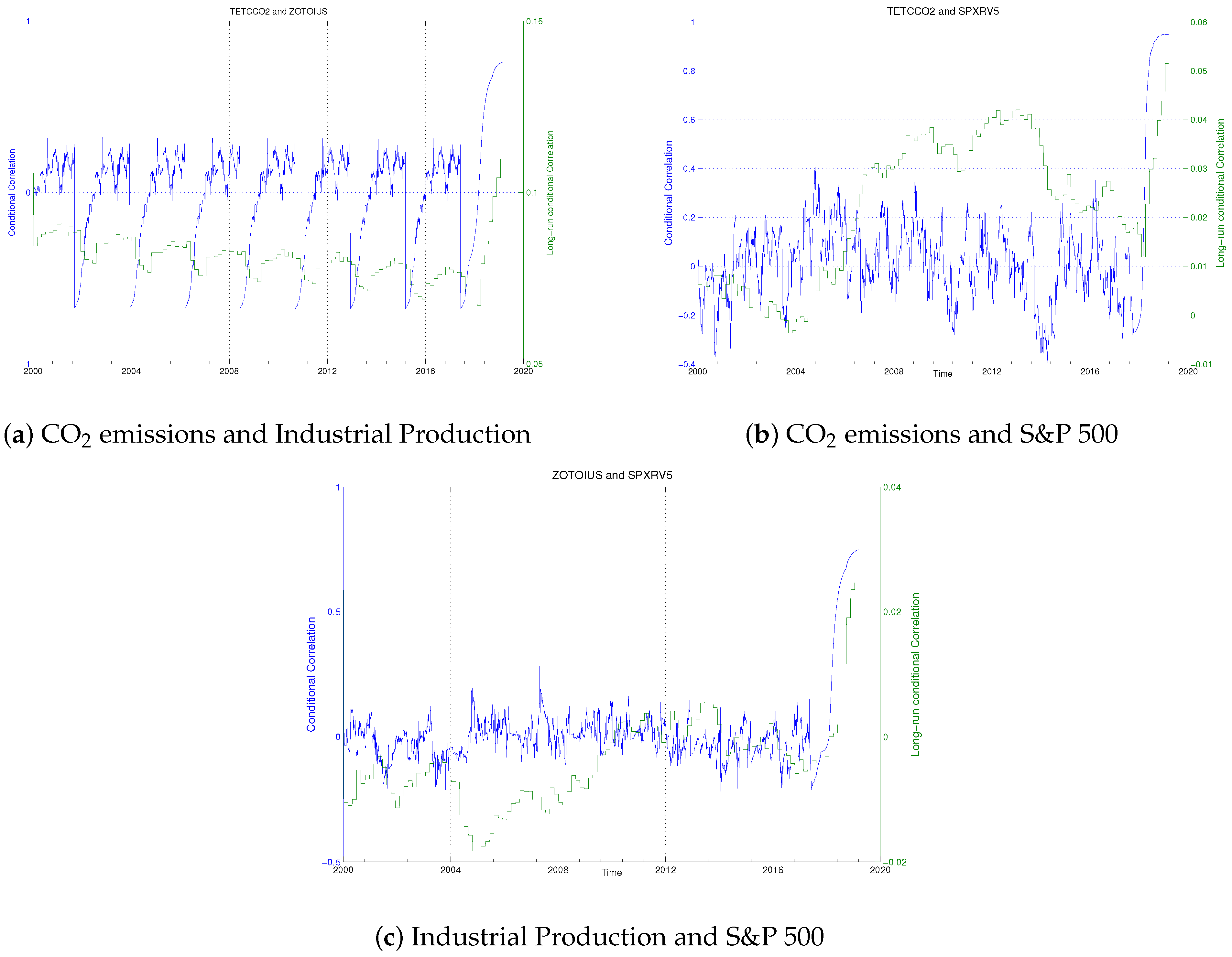

4.1. Baseline Correlations (without COVID-19 Cases)

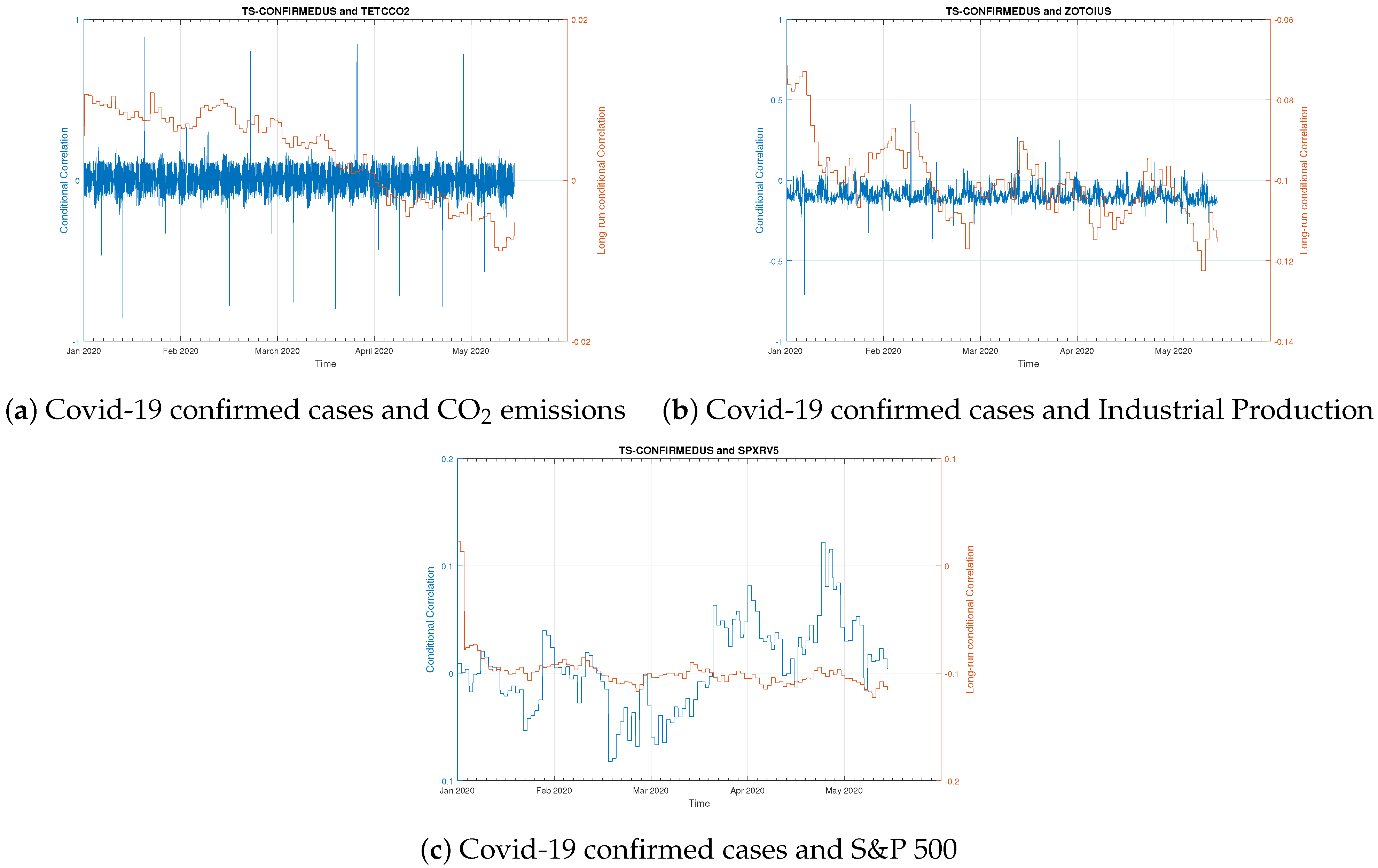

4.2. Introducing COVID-19 Confirmed Cases

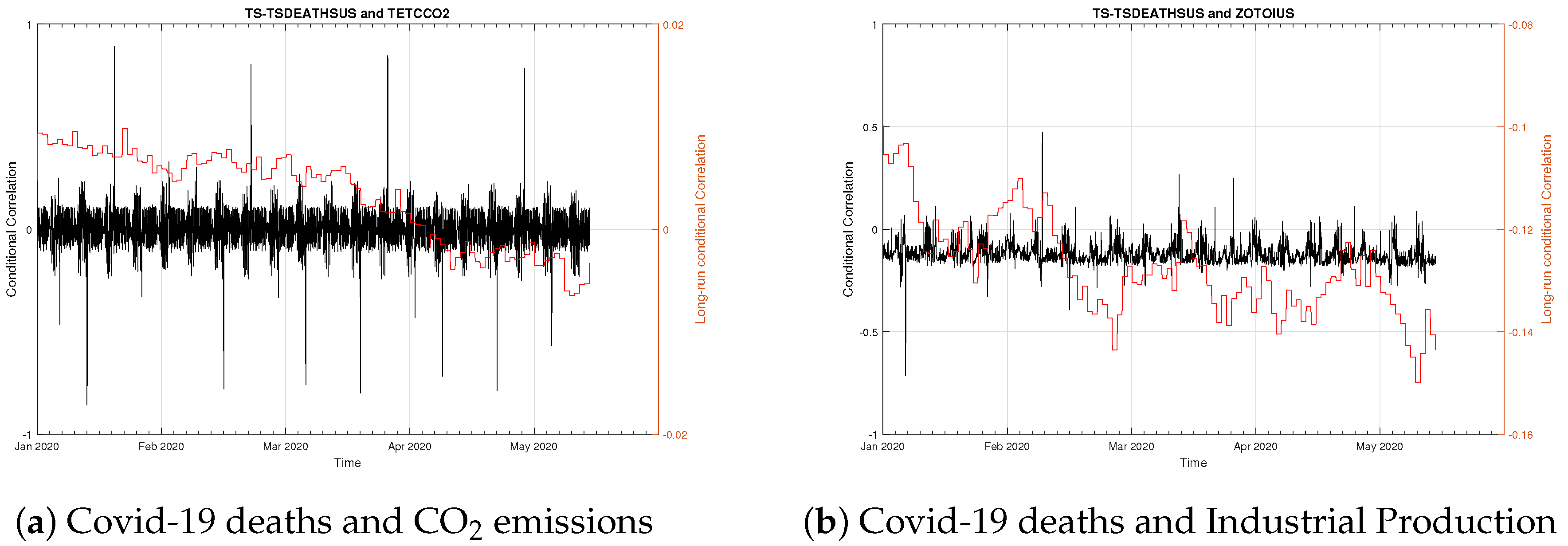

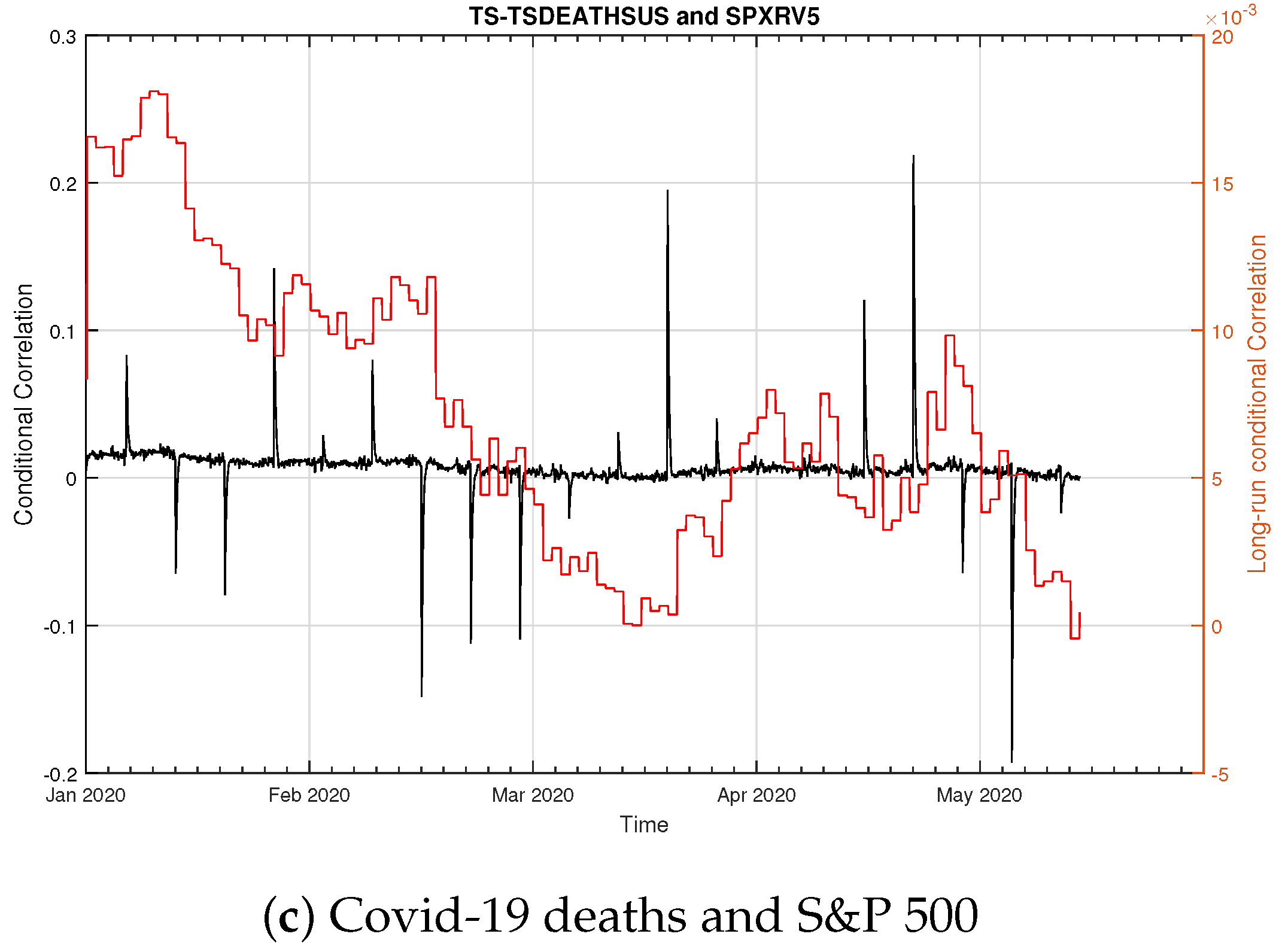

4.3. Introducing COVID-19 Deaths

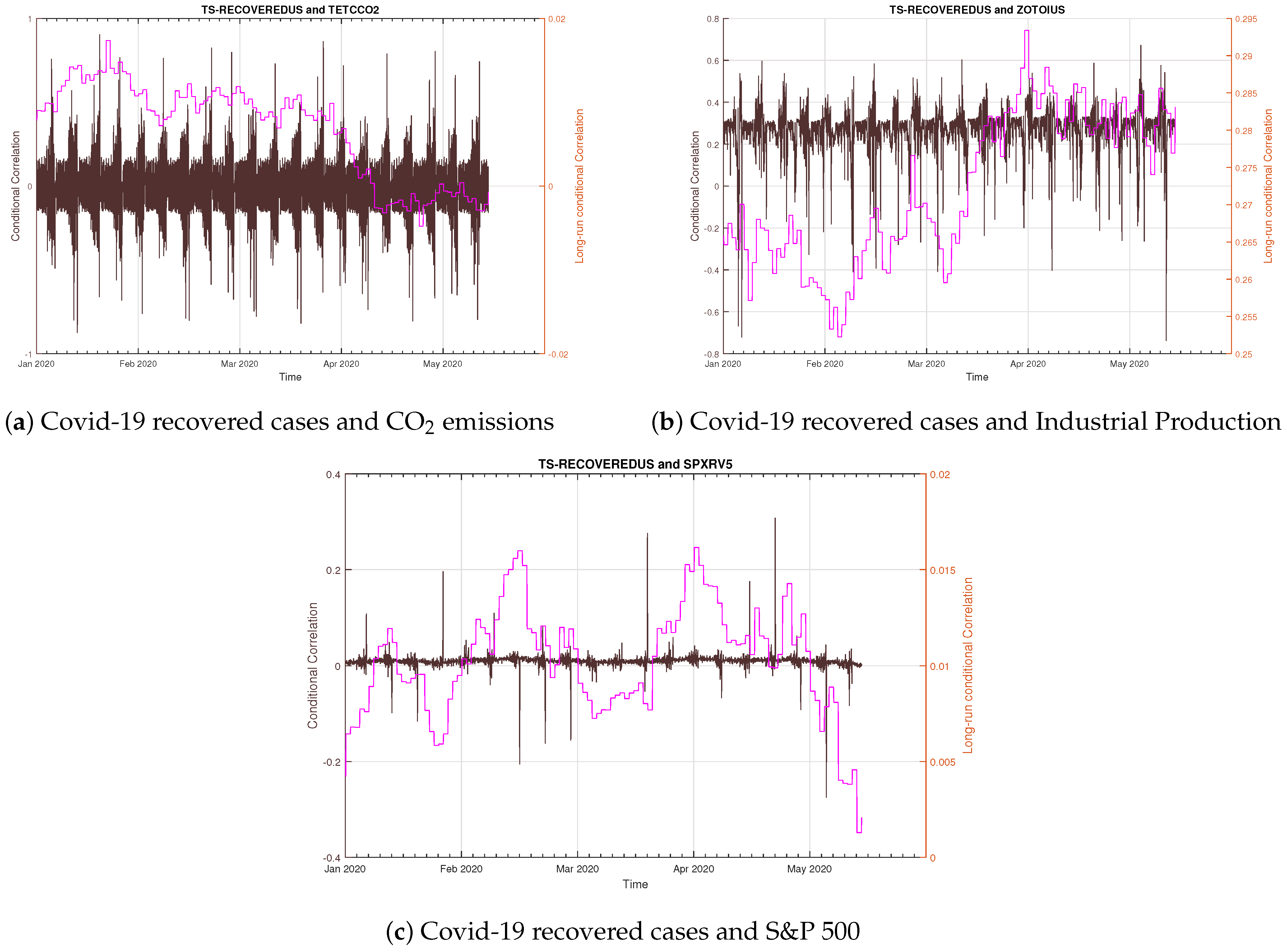

4.4. Introducing COVID-19 Recovered Cases

4.5. Sensitivity

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

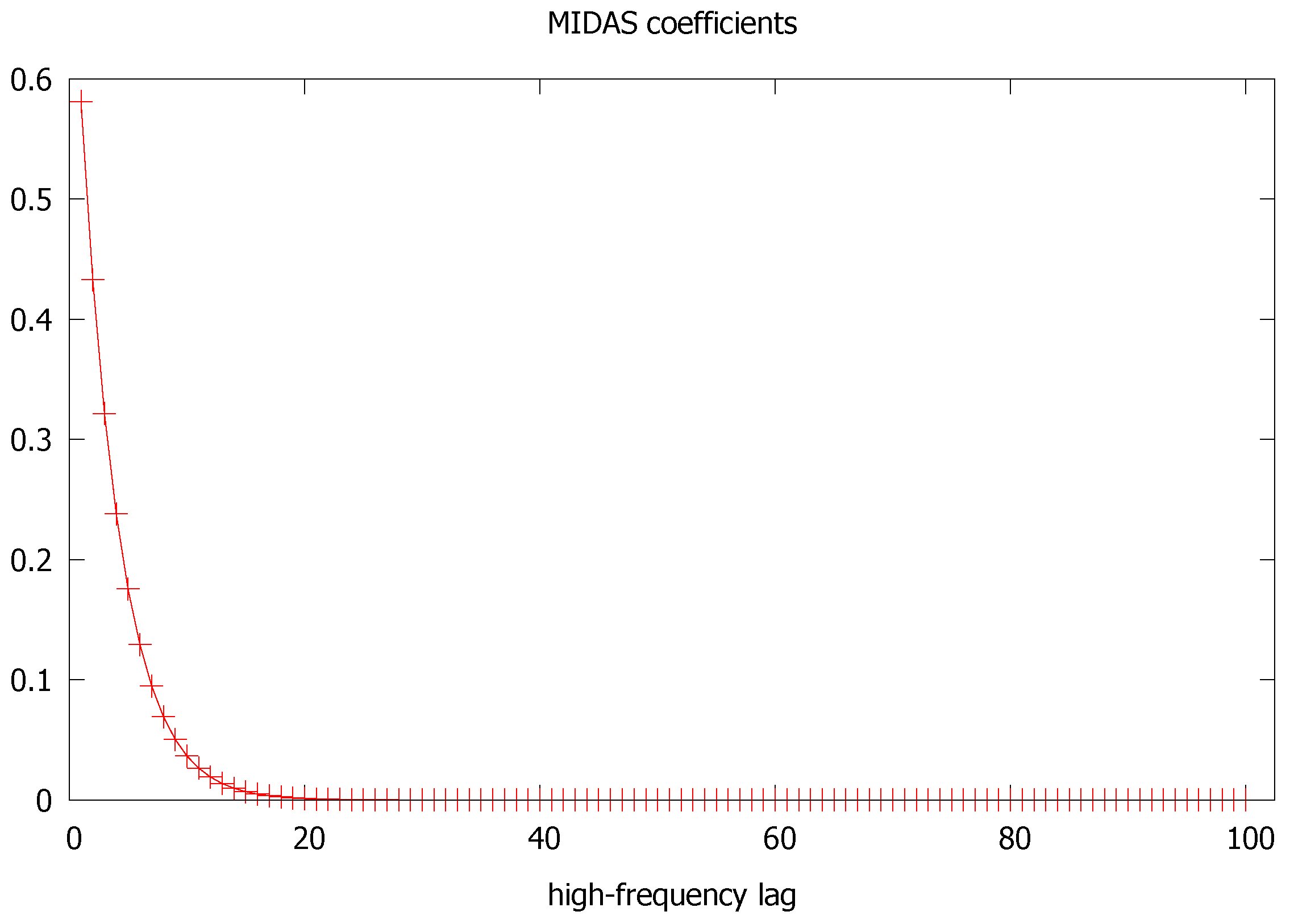

Setting the MIDAS Lags

References

- Aatola, Piia, Markku Ollikainen, and Anne Toppinen. 2013. Price determination in the eu ets market: Theory and econometric analysis with market fundamentals. Energy Economics 36: 380–95. [Google Scholar] [CrossRef]

- Albulescu, Claudiu Tiberiu. 2020. COVID-19 and the united states financial markets’ volatility. Finance Research Letters, 101699. [Google Scholar] [CrossRef] [PubMed]

- Asgharian, Hossein, Charlotte Christiansen, and Ai Jun Hou. 2016. Macro-finance determinants of the long-run stock–bond correlation: The dcc-midas specification. Journal of Financial Econometrics 14: 617–42. [Google Scholar] [CrossRef]

- Azimli, Asil. 2020. The impact of covid-19 on the degree of dependence and structure of risk-return relationship: A quantile regression approach. Finance Research Letters 36: 101648. [Google Scholar] [CrossRef]

- Bai, Lan, Yu Wei, Guiwu Wei, Xiafei Li, and Songyun Zhang. 2020. Infectious disease pandemic and permanent volatility of international stock markets: A long-term perspective. Finance Research Letters, 101709. [Google Scholar] [CrossRef]

- Baig, Ahmed, Hassan A Butt, Omair Haroon, and Syed Aun R Rizvi. 2020. Deaths, panic, lockdowns and us equity markets: The case of covid-19 pandemic. Finance Research Letters, 101701. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, Kyle Kost, Marco Sammon, and Tasaneeya Viratyosin. 2020. The unprecedented stock market reaction to covid-19. The Review of Asset Pricing Studies 10: 742–58. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, Ole E, Peter Reinhard Hansen, Asger Lunde, and Neil Shephard. 2008. Designing realized kernels to measure the ex post variation of equity prices in the presence of noise. Econometrica 76: 1481–536. [Google Scholar]

- Carlsson-Szlezak, Philipp, Martin Reeves, and Paul Swartz. 2020. What coronavirus could mean for the global economy. Harvard Business Review 3: 1–10. [Google Scholar]

- Chevallier, Julien. 2011a. Evaluating the carbon-macroeconomy relationship: Evidence from threshold vector error-correction and markov-switching var models. Economic Modelling 28: 2634–56. [Google Scholar] [CrossRef]

- Chevallier, Julien. 2011b. A model of carbon price interactions with macroeconomic and energy dynamics. Energy Economics 33: 1295–1312. [Google Scholar] [CrossRef]

- Chevallier, Julien. 2012. Time-varying correlations in oil, gas and co2 prices: An application using bekk, ccc and dcc-mgarch models. Applied Economics 44: 4257–74. [Google Scholar] [CrossRef] [Green Version]

- Chevallier, Julien. 2020. COVID-19 pandemic and financial contagion. Journal of Risk and Financial Management 13: 309. [Google Scholar] [CrossRef]

- Colacito, Riccardo, Robert F Engle, and Eric Ghysels. 2011. A component model for dynamic correlations. Journal of Econometrics 164: 45–59. [Google Scholar] [CrossRef] [Green Version]

- Conrad, Christian, Karin Loch, and Daniel Rittler. 2014. On the macroeconomic determinants of long-term volatilities and correlations in us stock and crude oil markets. Journal of Empirical Finance 29: 26–40. [Google Scholar] [CrossRef]

- Diebold, Francis X. 2020. Real Time Economic Activity: Exiting the Great Recession and Entering the Pandemic Recession. IAAE Webinar Series; New York: International Association for Applied Econometrics. [Google Scholar]

- Engle, Robert F, Eric Ghysels, and Bumjean Sohn. 2013. Stock market volatility and macroeconomic fundamentals. Review of Economics and Statistics 95: 776–97. [Google Scholar] [CrossRef]

- Engle, Robert F, and Kevin Sheppard. 2001. Theoretical and empirical properties of dynamic conditional correlation multivariate garch. In National Bureau of Economic Research. Technical Report. Cambridge: NBER. [Google Scholar]

- Fell, Harrison. 2010. Eu-ets and nordic electricity: A cvar analysis. The Energy Journal 31: 1–17. [Google Scholar] [CrossRef]

- Gharib, Cheima, Salma Mefteh-Wali, and Sami Ben Jabeur. 2020. The bubble contagion effect of covid-19 outbreak: Evidence from crude oil and gold markets. Finance Research Letters, 101703. [Google Scholar] [CrossRef]

- Ghysels, Eric, Pedro Santa-Clara, and Rossen Valkanov. 2004. The Midas Touch: Mixed Data Sampling Regressions. Chapel Hill: University of North Carolina and UCLA. [Google Scholar]

- Ghysels, Eric, Arthur Sinko, and Rossen Valkanov. 2007. Midas regressions: Further results and new directions. Econometric Reviews 26: 53–90. [Google Scholar] [CrossRef]

- Gómez-Puig, Marta, and Simón Sosvilla-Rivero. 2016. Causes and hazards of the euro area sovereign debt crisis: Pure and fundamentals-based contagion. Economic Modelling 56: 133–47. [Google Scholar] [CrossRef] [Green Version]

- Gruppe, Mario, Tobias Basse, Meik Friedrich, and Carsten Lange. 2017. Interest rate convergence, sovereign credit risk and the european debt crisis: A survey. The Journal of Risk Finance 18: 432–42. [Google Scholar] [CrossRef]

- Hintermann, Beat. 2010. Allowance price drivers in the first phase of the eu ets. Journal of Environmental Economics and Management 59: 43–56. [Google Scholar] [CrossRef] [Green Version]

- Kamin, Steven B, and Laurie Pounder DeMarco. 2012. How did a domestic housing slump turn into a global financial crisis? Journal of International Money and Finance 31: 10–41. [Google Scholar] [CrossRef] [Green Version]

- Le Quéré, Corinne, Robert B. Jackson, Matthew W. Jones, Adam J. P. Smith, Sam Abernethy, Robbie M. Andrew, Anthony J. De-Gol, David R. Willis, Yuli Shan, Josep G. Canadell, and et al. 2020. Temporary reduction in daily global co2 emissions during the covid-19 forced confinement. Nature Climate Change 10: 1–7. [Google Scholar] [CrossRef]

- Liu, Zhu, Philippe Ciais, Zhu Deng, Ruixue Lei, Steven J. Davis, Sha Feng, Bo Zheng, Duo Cui, Zhu Xinyu, Guo Biqing, and et al. 2020. Near-real-time monitoring of global co2 emissions reveals the effects of the covid-19 pandemic. Nature Communications 11: 1–12. [Google Scholar] [CrossRef]

- Lutz, Benjamin Johannes, Uta Pigorsch, and Waldemar Rotfuß. 2013. Nonlinearity in cap-and-trade systems: The eua price and its fundamentals. Energy Economics 40: 222–32. [Google Scholar] [CrossRef] [Green Version]

- Lyócsa, Štefan, and Peter Molnár. 2020. Stock market oscillations during the corona crash: The role of fear and uncertainty. Finance Research Letters 36: 101707. [Google Scholar] [CrossRef]

- Mazur, Mieszko, Man Dang, and Miguel Vega. 2020. COVID-19 and the march 2020 stock market crash. evidence from s&p1500. Finance Research Letters, 101690. [Google Scholar] [CrossRef]

- Melvin, Michael, and Mark P Taylor. 2009. The global financial crisis: Causes, threats and opportunities. introduction and overview. Journal of International Money and Finance 28: 1243–1245. [Google Scholar] [CrossRef]

- Moro, Beniamino. 2014. Lessons from the european economic and financial great crisis: A survey. European Journal of Political Economy 34: S9–S24. [Google Scholar] [CrossRef]

- National Academies of Sciences, Engineering, Medicine. 2020. Framework for Equitable Allocation of COVID-19 Vaccine. Washington: National Academies Press. [Google Scholar]

- Papadamou, Stephanos, Athanasios P. Fassas, Dimitris Kenourgios, and Dimitrios Dimitriou. 2020. Flight-to-quality between global stock and bond markets in the covid era. Finance Research Letters, 101852. [Google Scholar] [CrossRef]

- Rizwan, Muhammad Suhail, Ghufran Ahmad, and Dawood Ashraf. 2020. Systemic risk: The impact of covid-19. Finance Research Letters, 101682. [Google Scholar] [CrossRef] [PubMed]

- Sohrabi, Catrin, Zaid Alsafi, Niamh O’Neill, Mehdi Khan, Ahmed Kerwan, Ahmed Al-Jabir, Christos Iosifidis, and Riaz Agha. 2020. World health organization declares global emergency: A review of the 2019 novel coronavirus (covid-19). International Journal of Surgery. [Google Scholar] [CrossRef]

- Topcu, Mert, and Omer Serkan Gulal. 2020. The impact of covid-19 on emerging stock markets. Finance Research Letters 36: 101691. [Google Scholar] [CrossRef]

- Wegener, Christoph, Robinson Kruse, and Tobias Basse. 2019. The walking debt crisis. Journal of Economic Behavior & Organization 157: 382–402. [Google Scholar]

- Xu, Qifa, Lu Chen, Cuixia Jiang, and Jing Yuan. 2018. Measuring systemic risk of the banking industry in china: A dcc-midas-t approach. Pacific-Basin Finance Journal 51: 13–31. [Google Scholar] [CrossRef]

- Zheng, Bo, Guannan Geng, Philippe Ciais, Steven J. Davis, Randall V. Martin, Jun Meng, Nana Wu, Frederic Chevallier, Gregoire Broquet, Folkert Boersma, and et al. 2020. Satellite-based estimates of decline and rebound in china’s co2 emissions during covid-19 pandemic. Science Advances, 6. [Google Scholar] [CrossRef]

| 1 | Academically, it is interesting to investigate whether the two crisis events are connected to each other. As argued by Gómez-Puig and Sosvilla-Rivero (2016), the European sovereign debt crisis is preceded by contagion episodes with causal links that stem from the Global Financial Crisis’s outburst. Wegener et al. (2019) challenge the view that the arising sovereign credit risk in the EMU has been triggered by the U.S. subprime crunch. On the contrary, they conclude that the severe fiscal problems in peripheral countries are homemade, rather than imported from the U.S. Thus, no definitive conclusion seems to be reached based on quantitative analysis. |

| 2 | Such as the excessive dependence on short-term funding; or vicious cycles of mark-to-market losses driving fire sales of mortgage-backed securities. |

| 3 | |

| 4 | |

| 5 | |

| 6 | Precisely, the EIA’s Table 9a accessed from https://www.eia.gov/totalenergy/data/browser/. |

| 7 | See Barndorff-Nielsen et al. (2008) for the theory. |

| 8 | Upon reasonable request, we can transmit (unformatted) unit root tests in order to show that, thus transformed, the series are indeed . |

| 9 | To save space, conditional variances not shown here and they can be transmitted upon request to the interested reader. |

| 10 | Upon a reasonable request, we can transmit (unformatted) logs of DCC-MIDAS estimates. The computational burden induced by the loop (e.g., combinations) can create memory usage bottlenecks on lower-end computers. |

| 11 | |

| 12 | Upon request, a similar analysis can be produced for the 144 lag settings of the conditional correlation. It is not shown for brevity. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Macroeconomic | |

| Real Gross Domestic Product | |

| Real Personal Consumption Expenditures | |

| Real Private Fixed Investment | |

| Business Inventory Change | |

| Real Government Expenditures | |

| Real Exports of Goods & Services | |

| Real Imports of Goods & Services | |

| Real Disposable Personal Income | |

| Non-Farm Employment | |

| Civilian Unemployment Rate | |

| Housing Starts | |

| Manufacturing Production Indices | |

| Total Industrial Production Index | |

| Manufacturing Production Index | |

| Food Production Index (NAICS 311) | |

| Paper Production Index (NAICS 322) | |

| Petroleum and Coal Products Production Index (NAICS 324) | |

| Chemicals Production Index (NAICS 325) | |

| Resins and Synthetic Products Production Index (NAICS 3252) | |

| Agricultural Chemicals Production Index | |

| Nonmetallic Mineral Products Production Index | |

| Primary Metals Production Index (NAICS 311) | |

| Coal-weighted Manufacturing Production Index | |

| Distillate-weighted Manufacturing Production Index | |

| Electricity-weighted Manufacturing Production Index | |

| Natural Gas-weighted Manufacturing Production Index | |

| Price Indexes | |

| Consumer Price Index (all urban consumers) | |

| Producer Price Index: All Commodities | |

| Producer Price Index: Petroleum | |

| GDP Implicit Price Deflator | |

| Miscellaneous | |

| Vehicle Miles Traveled | |

| Air Travel Capacity | |

| Aircraft Utilization | |

| Airline Ticket Price Index | |

| Raw Steel Production | |

| Carbon Dioxide (CO) Emissions | |

| Petroleum CO Emissions | |

| Natural Gas CO Emissions | |

| Coal CO Emissions | |

| Total Fossil Fuels CO Emissions |

| Symbol | Name | Earliest Available | Latest Available |

|---|---|---|---|

| .DJI | Dow Jones Industrial Average | 3 January 2000 | 8 May 2020 |

| .IXIC | Nasdaq 100 | 3 January 2000 | 8 May 2020 |

| .SPX | S&P 500 Index | 3 January 2000 | 8 May 2020 |

| m | ||||||

|---|---|---|---|---|---|---|

| TETCCO2 | 0.2797 *** | 0.0469 *** | 0.5986 *** | 0.1000 *** | 5.7068 *** | 7.7439 *** |

| (0.0001) | (0.0002) | (0.0013) | (0.0003) | (0.0005) | (0.0001) | |

| ZOTOIUS | −0.1181 | 0.0142 *** | 0.9858 *** | 0.1368 | 1.001 0 | 32.3250 *** |

| (0.1101) | (0.0004) | (0.0004) | (9.9118 ) | (13.4850) | (3.6880) | |

| SPX-RV5 | 0.0015 | 0.2344 *** | 0.0556 | 0.1939 *** | 6.4697 *** | 0.3568 *** |

| (0.0090) | (0.0245) | (0.0574) | (0.0142) | (2.0287) | (0.0678) | |

| a | b | |||||

| DCC-MIDAS | 0.0171 | 0.8000 | 1.001 *** | |||

| (0.0204) | (0.6090 ) | (0.2088) | ||||

| Logarithmic likelihood: | −6430.57 | |||||

| Akaike info criterion: | 12,867.1 | |||||

| Bayesian info criterion: | 12,886.7 | |||||

| Sample size: | 5103 |

| m | ||||||

|---|---|---|---|---|---|---|

| TS-CONFIRMED-US | 12969.7920 | 0.9999 *** | 0.0001 *** | −28.4962 *** | 1.0830 *** | 0.0100 *** |

| (12085) | (0.3189) | (0.0001) | (6.8426) | (0.1688) | (0.0005) | |

| TETCCO2 | 0.2796 *** | 0.0468 *** | 0.5980 *** | 0.1000 *** | 5.7067 *** | 7.7438 *** |

| (0.0001) | (0.0001) | (0.0001) | (0.0001) | (0.0001) | (0.0001) | |

| ZOTOIUS | −0.1180 | 0.0141*** | 0.9857 *** | 0.1368 | 1.001 | 32.3246 *** |

| (0.1103) | (0.0004) | (0.0004) | (9.9118) | (13.4850) | (3.688) | |

| SPX-RV5 | 0.0015 | 0.2344 *** | 0.0556 | 0.1938 *** | 6.4696 *** | 0.3567 *** |

| (0.0090) | (0.0245) | (0.0574) | (0.0142) | (2.0287) | (0.0678) | |

| a | b | |||||

| DCC-MIDAS | 0.0178 | 0.6012 | 1.001 *** | |||

| (0.0291) | (0.8847) | (0.4317) | ||||

| Logarithmic likelihood: | −6334.08 | |||||

| Akaike info criterion: | 12,674.2 | |||||

| Bayesian info criterion: | 12,693.8 | |||||

| Adjusted sample size: | 1503 |

| m | ||||||

|---|---|---|---|---|---|---|

| TS-DEATHS-US | 760.71748 | 0.9999 *** | 0.0001 *** | −46.2930 *** | 1.0836 *** | 0.0100 *** |

| (633.73) | (0.3178) | (0.0001) | (2.9142) | (0.1697) | (0.0005) | |

| TETCCO2 | 0.2799 *** | 0.0468 *** | 0.5986 *** | 0.1000 *** | 5.7068 *** | 7.7439 *** |

| (0.0001) | (0.0001) | (0.0001) | (0.0001) | (0.0001) | (0.0001) | |

| ZOTOIUS | −0.1181 | 0.0146 *** | 0.9859 *** | 0.1366 | 1.0010 | 32.3250 *** |

| (0.1137) | (0.0004) | (0.0004) | (9.9118) | (13.4850) | (3.6880) | |

| SPX-RV5 | 0.0016 | 0.2343 *** | 0.0557 | 0.1939 *** | 6.4697 *** | 0.3577 *** |

| (0.0091) | (0.0246) | (0.0577) | (0.0141) | (2.0287) | (0.0688) | |

| a | b | |||||

| DCC-MIDAS | 0.0163 | 0.6430 | 1.001 *** | |||

| (0.0272) | (0.8376) | (0.4335) | ||||

| Logarithmic likelihood: | −6334.93 | |||||

| Akaike info criterion: | 12,677 | |||||

| Bayesian info criterion: | 12,696.6 | |||||

| Adjusted sample size: | 1503 |

| m | ||||||

|---|---|---|---|---|---|---|

| TS-RECOVERED-US | −2567.0739 ** | 0.6144 *** | 0.3778 *** | 1.8502 *** | 1.0876 *** | 0.0100 |

| (1041.40) | (0.0354) | (0.0328) | (0.1576) | (0.2205) | (0.0006) | |

| TETCCO2 | 0.2769 *** | 0.0488 *** | 0.5980 *** | 0.1000 *** | 5.7068 *** | 7.7439 *** |

| (0.0001) | (0.0001) | (0.0001) | (0.0001) | (0.0001) | (0.0001) | |

| ZOTOIUS | −0.1189 | 0.0147 *** | 0.9857 *** | 0.1368 | 1.0010 | 32.3250 *** |

| (0.1137) | (0.0004) | (0.0004) | (9.9118) | (13.4850) | (3.6880) | |

| SPX-RV5 | 0.0015 | 0.2344 *** | 0.0557 | 0.1938 *** | 6.4697 *** | 0.3568 *** |

| (0.0090) | (0.0245) | (0.0574) | (0.0142) | (2.0287) | (0.0675) | |

| a | b | |||||

| DCC-MIDAS | 0.0278 | 0.6170 *** | 1.001 *** | |||

| (0.0383) | (0.0813 | (0.3917) | ||||

| Logarithmic likelihood: | −6492.48 | |||||

| Akaike info criterion: | 12,991 | |||||

| Bayesian info criterion: | 13,010.6 | |||||

| Adjusted sample size: | 1503 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chevallier, J. COVID-19 Outbreak and CO2 Emissions: Macro-Financial Linkages. J. Risk Financial Manag. 2021, 14, 12. https://doi.org/10.3390/jrfm14010012

Chevallier J. COVID-19 Outbreak and CO2 Emissions: Macro-Financial Linkages. Journal of Risk and Financial Management. 2021; 14(1):12. https://doi.org/10.3390/jrfm14010012

Chicago/Turabian StyleChevallier, Julien. 2021. "COVID-19 Outbreak and CO2 Emissions: Macro-Financial Linkages" Journal of Risk and Financial Management 14, no. 1: 12. https://doi.org/10.3390/jrfm14010012

APA StyleChevallier, J. (2021). COVID-19 Outbreak and CO2 Emissions: Macro-Financial Linkages. Journal of Risk and Financial Management, 14(1), 12. https://doi.org/10.3390/jrfm14010012