1. Background

As the world is getting ready for a new year, health authorities in Wuhan, China has reported to the World Health Organization (WHO) the outbreak of an unknown cluster of viral pneumonia cases on the last day of December 2019. After a formal investigation of these cases by the beginning of 2020, the world witnessed the birth of the SARS‑CoV‑2 (COVID 19) virus. As of 15 December, more than 73 million infection cases and more than 1,600,000 deaths have been globally declared to be associated with COVID 19 pandemic (World Health Organization (

WHO 2020). COVID 19 is the fifth in the 21st-century list of pandemics, after Influenza H1N1, Coronavirus (Bats), and Ebolavirus, Coronavirus (Camels). H1N1 is the furriest among the list as it was associated with 151,700 to 575,400 deaths worldwide (Center for Disease Control and Prevention (

CDC 2019).

While the exact global economic impacts of COVID 19 are not yet clear, it is considered deadlier than the other two Coronaviruses and has affected a massively larger number of people over a shorter period. SARS and MERS have affected respectively, 8437 and 2499 cases, and with 813 and 816 associated deaths (

WHO 2012;

CDC 2004). This study contributes to the newly developed COVID 19 empirical research by examining the impact of the COVID 19 contamination rate on returns of stock market indices and prices of selected globally trade commodities, namely gold, platinum, silver, WTI, and Brent oil. We utilize daily data of selected stock markets from the firstly affected countries, China, the USA, Spain, Italy, South Korea, and Japan. The methodology adopted is a k-variate panel VAR of order

based on (

Abrigo and Love 2016).

The overall panel least squares VAR estimation indicates a negative short termed impact of 2.3% in the performances of the stock markets when the spread rate of coronavirus increases by 1% across countries in time ceteris paribu. The coronavirus contamination rate is not statistically significant to explain the changes in the exchange rate and the growth of the prices of gold in the countries of analysis, regardless of this result, the virus spread rate is significant at the 90% confidence level to explain changes related to the prices of platinum, silver, WTI, and Brent crude oil. According to the Driscoll–Kraay approach, we found that the fluctuations of the exchange rate, platinum, and gold prices are the main drivers for stock market movements.

Global stock markets reacted strongly and wildly to the outbreak of COVID 19. In March 2020, the US stock market hit the circuit breaker mechanism four times in ten days. Since its inception in 1987, the breaker has only ever been triggered once, in 1997. Stock markets in Europe and Asia have also dramatically reacted. FTSE of the UK has dropped on the 12th of March more than 10% on its worst day since 1987 and the stock market in Japan has lost more than 20% from its highest position at the end of 2019 (

Zhang et al. 2020).

Gormsen and Koijen (

2020) showed that stock markets have dropped in response to COVID 19 as much as the global financial crises of 2008, yet the markets during the pandemic have recovered quicker especially in Europe.

The pandemic severity varies across countries hence begetting non-uniform individual stock markets reactions,

Capelle-Blancard and Desroziers (

2020) have accounted for such heterogeneity across 74 countries and found that the number of infected people in each country was the primary driver for stock market reactions, and volatility heaved as concerns about the pandemic grew. Their results also showed that the number of COVID 19 infection cases in wealthy neighboring countries has affected investors’ decisions.

He et al. (

2020) used conventional t-tests and non-parametric Mann–Whitney tests to analyze the impact of COVID 19 on selected stock markets in Asia and Europe. They found that COVID 19 has a negative, bidirectional, and short-termed impact on stock markets between Asian, American, and European stock markets, yet the impact tends to intensify as the virus spreads.

Examining a different perspective of heterogeneity,

Albuquerque et al. (

2020) argued that COVID 19 have triggered unparalleled shocks to stocks, those with higher Environmental, Social, and Governance activities (ESG) rating have shown more resilience, maintained higher returns and higher operating profit margins relative to their counterparts during the first quarter of 2020. The logic here follows

Albuquerque et al. (

2019) model that investing in ESG policies feeds into the firms’ customer loyalty and reduces the price elasticity of demand for their products.

2. Literature Review

Studies of the macroeconomic impact of past pandemics have mainly aimed to quantify the effects in terms of lost output and growth, however firm conclusions about the pandemics’ long-run economic effects have not been well researched (

Bell and Lewis 2004). Studies of such a scope usually study the short-term economic effects of pandemics through their impact on supply and demand, stock market, fertility rate, trade, labor inputs, and tourism (

Jonung and Roeger 2006).

One of the few studies on the economic effects of Spanish influenza between 1918–1919, suggested that this pandemic has stimulated the growth of the US economy post the pandemic years in the 1920s (

Brainerd and Siegler 2003), contrary to

Correia et al. (

2020) who showed that a sharp decline in economic activity has persisted until at least 1923. Comparing the Spanish flu effects across 43 countries between 1918 and 1920,

Barro et al. (

2020) concluded that the flu-associated death rates caused declines in GDP and consumption of about 6%.

Karlsson et al. (

2014) found no discernible effect of the 1918 influenza pandemic on earnings in Sweden. The state of the economy during a pandemic defines extensively the speed and severity of the ensued economic effects.

Benmelech and Frydman (

2020) argued that the increase in the government’s demand for World War I-related products during the 1918 influenza pandemic has made up for the contraction in consumer spending and private investment, leaving only modest and short-termed effects on US and European economies. It is generally perceived also that during pandemics, regions with a higher degree of global exposure and economic integration are affected more sturdily than less integrated regions (

Verikios et al. 2012).

May 2009 witnessed the emergence of a new H1N1 commonly known as “swine flu” due to its close association with North American and Eurasian pig influenza.

Verikios et al. (

2012) is one of the few studies that investigated the economic effects of the H1N1 epidemic, by applying on Australia, their MONASH. Health model simulation results showed that the epidemic is associated with significant short-termed adverse macroeconomic effects that extend only within two or four quarters then the economy reverts to normal rates. The preceded contractionary effect would reduce tourism, household demands for international travel and industries would face increased costs via absenteeism and loss of labor force (

Verikios et al. 2012).

As we move forward in time and from north to south on the map,

Young (

2005) projected an increasing trend in per capita consumption post the AIDS epidemic in South Africa. The widespread community infection measures during the epidemic have lowered national fertility rates, both directly, through a reduction in the willingness to engage in unprotected sexual activity and increasing the scarcity of labor and the value of a woman’s time. On contrary, the World

Bank (

2016) postulated that the recent Ebola epidemic in West Africa during 2014–2015 has had severe and adverse shocks to the private sector as well as has posed threats to national food security due to the decline in agricultural production.

Regarding the impact of the current COVID 19 pandemic on the global financial markets,

Baker et al. (

2020) stated that the US stock market has reacted more forcefully to the current pandemic than any other pandemic in the US history.

Albulesco (

2020) showed that the news about the new infection cases has enhanced the volatility of the United States S&P 500. Similar findings were portrayed by

Zhang et al. (

2020) on a global sample.

Ashraf (

2020b) studied the impact of COVID 19 on stock market returns using a global sample of 64 countries and found that stock market returns declined as the number of confirmed cases increased.

Bakas and Triantafyllou (

2020) analyzed the impact of the pandemic on global commodity markets, they showed that the pandemic uncertainty has decreased the volatility of commodity markets, especially on the crude oil market, while the effect on the gold market is positive but less significant.

Following a similar approach to our paper, but by applying to Africa,

Takyi and Bentum-Ennin (

2020) estimated the negative impact of COVID 19 on stock market performance to between 2.7% and 21% across their sample of 13 countries. Markets react un-uniformly to COVID 19 shocks, one possible reason according to

Ashraf (

2020a) is the level of cultural uncertainty avoidance, meaning that investors in countries with a higher level of uncertainty aversion are more likely to engage in panic selling to avoid uncertainty causing this market to be more vulnerable to COVID 19 shock relative to their counterparts.

Engelhardt et al. (

2020) suggest that high- trust levels between fellow citizens as well as for the government, contribute largely to reducing market volatility in response to the COVID 19 announcements. This paper contributes to the growing literature on the stock market effects of the COVID 19 pandemic. Using a sample of the 6 first affected countries, we use panel K VAR methodology to capture the interdependencies and homogeneity between COVID 19 contamination rate, stock market return, and selected global market commodities across countries and time.

3. Stylized Facts

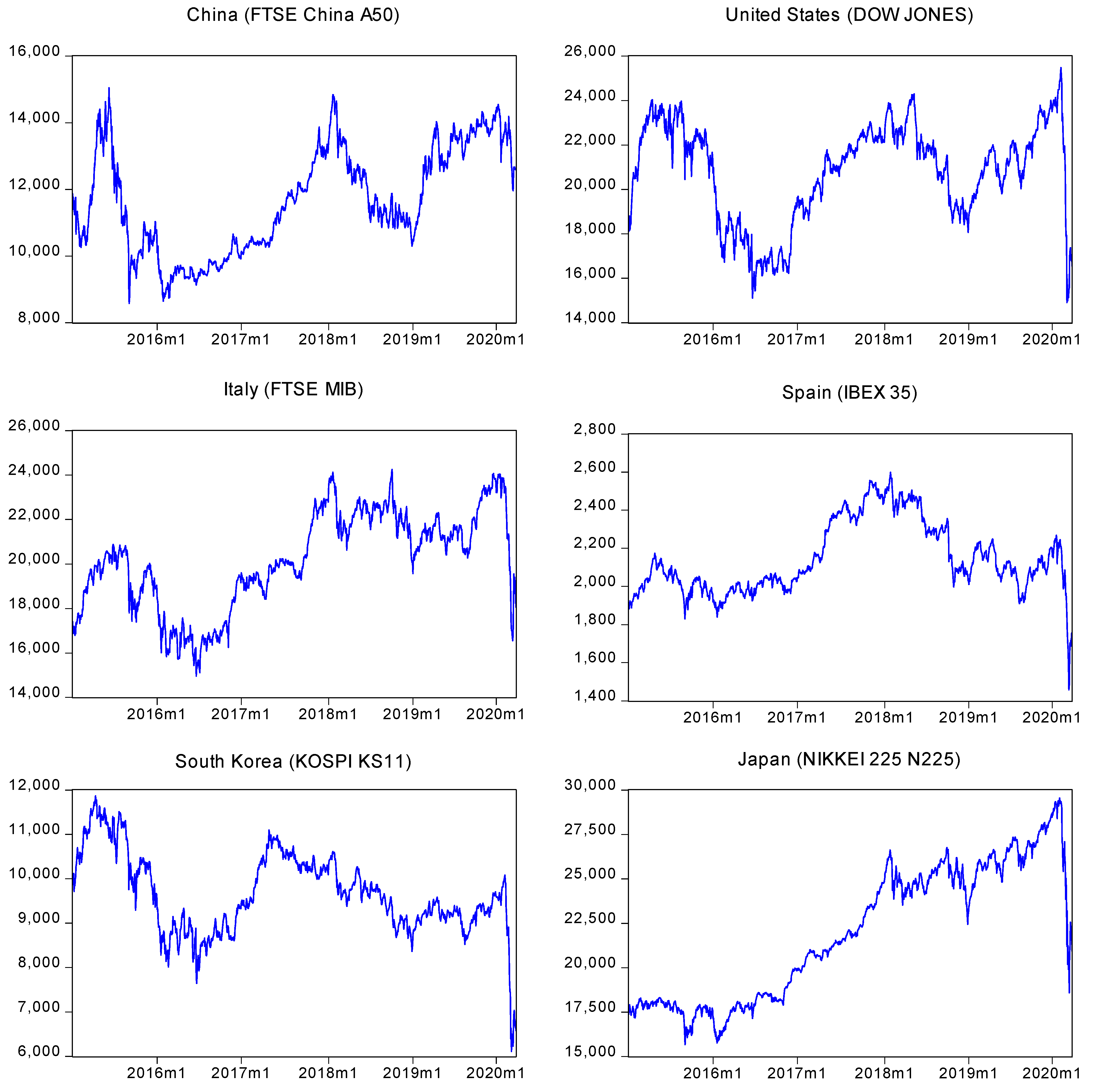

Since the outbreak of the COVID 19 in January 2020 and on, a persistent decrease in stock market returns is observed in

Figure 1 in the first affected countries.

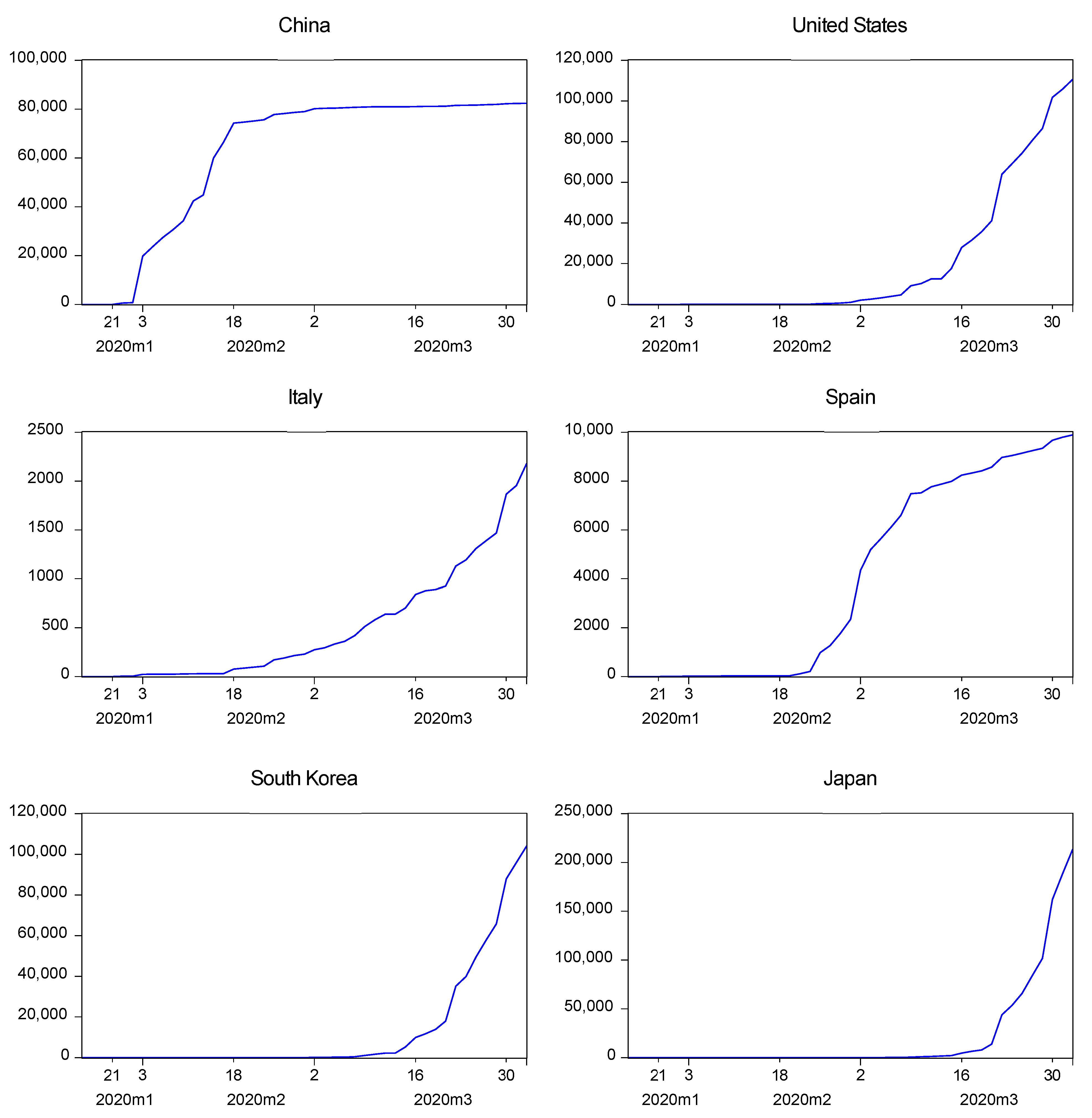

The decrease in the stock market prices corresponds with the surge in the overall number of people contaminated per day in each country (see

Figure 2), where the first transmission pattern is appointed to the factor of close contact with infected individuals. The behavior of the absolute number of people infected per day in these countries suggests an inverse correlation with the stock market returns.

The number of people contaminated per day is shown ahead, and the increasing trend is evident. China is considered the best performer to control the virus spread rate. The rest of the countries are struggling to keep the curve plane; however, Japan and United States have the largest contamination speed considering that the outbreak on a large scale started in February (even when the first case was detected earlier).

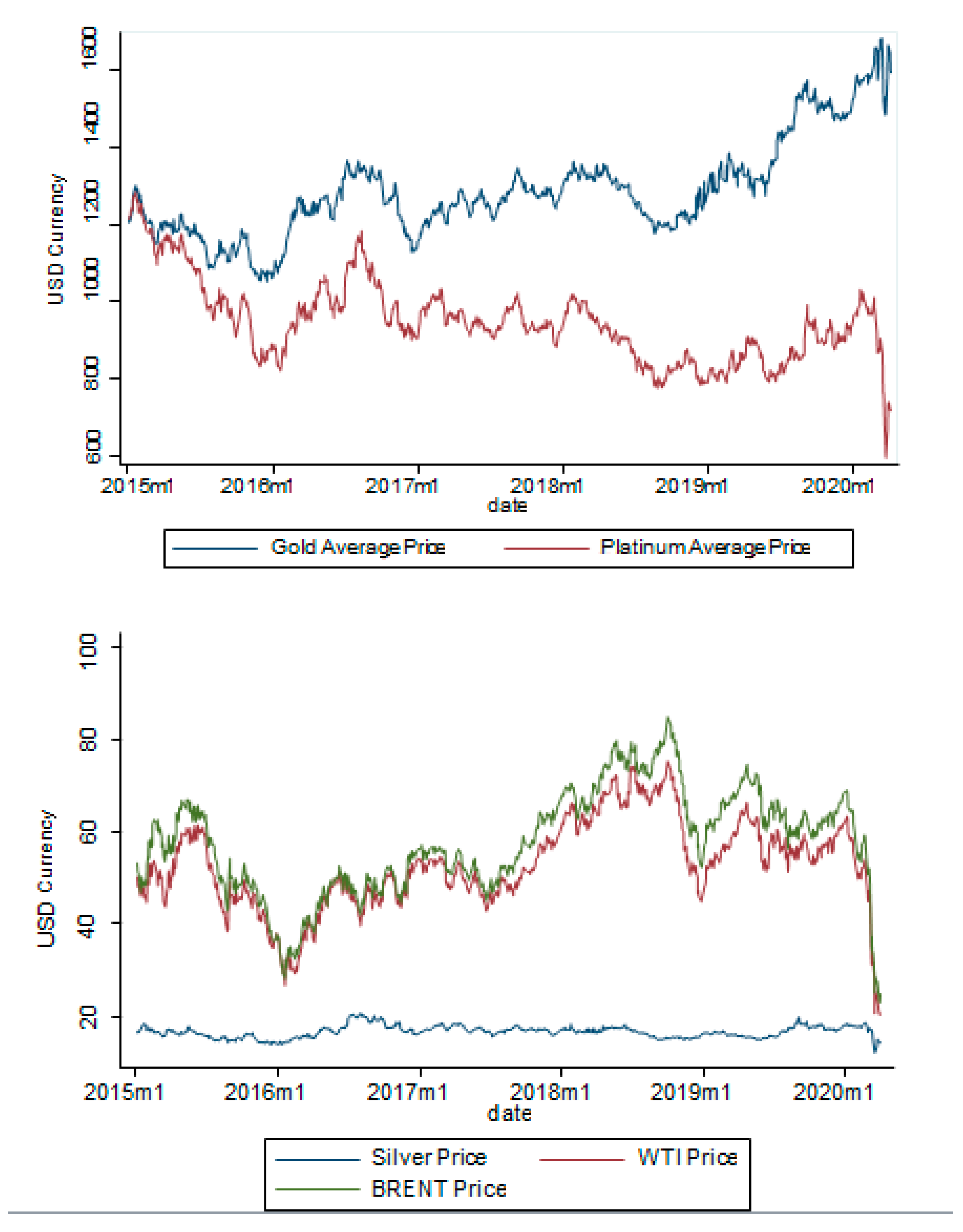

Since the financial market is closely linked with the commodity market and the overall economic production, the prices (as a measure of value) of the commodities are also influenced by COVID 19. In January 2020, it can be seen from

Figure 3, that a significant prices’ drop-down started to appear with the outbreak of coronavirus across countries and it was more intense for the commodities of Gold, Platinum (measured in 1 troy ounce for each), Brent and WTI crude oil (measured in 1 barrel of oil).

A correlation analysis (see

Table 1) measuring growth as percentage change using log-differences of these variables suggest that the contamination growth rate of Covid-19 is statistically significant and negatively correlated with the performance of the stock markets and the commodity prices, except for exchange rate and gold prices

1. The highest negative correlation coefficients of the contamination growth rate of Covid-19 are with the price of the Brent oil barrel and the stock market performance.

Average positive returns from the stock markets of Japan, the United States, China, South Korea, Spain, and Italy are reported in

Table 2 during the period between 2015 and 2020. The average number of people contaminated per day is 21,002 for all of these countries. The prices of gold and silver have an average growth of 0.016% and 0.129%, respectively. The prices of platinum, WTI, and Brent oil are decreasing during the same period. The price of the oil Brent barrel has the highest volatility, while the exchange rate has the lowest volatility. The selected stock markets for each of these countries exhibit positive returns except for Spain (see

Table 3). China (FTSE China A50) has a higher return on average than the United States (Dow Jones) from 2015 to 2020.

4. Methodology

We utilize a

k-variate panel VAR of order

to empirically investigate the impact of the contamination rate of COVID 19 on stock market returns of first-affected countries. Following the description of

Abrigo and Love (

2016), the general model specification is expressed as follows:

where

is a (1 ×

k) vector of the dependent stationary variables, which includes the performance of the stock market of country

i at time

t as the variable of interest, and later a set of endogenous regressors which includes the growth rate of the current exchange rates of country

i at time

t, the growth rate of the prices of commodities of gold, platinum, silver, WTI & BRENT oil. We assume parameter homogeneity for

and

which is a matrix of

of parameters.

is the (1 ×

l) vector of exogenous covariates, which includes the growth rate of contagious per day of COVID 19

2, among this exogenous variable, the fixed effects are captured in

.

From (1) by defining as the vector of k endogenous dependent variables with , which contains the autoregressive lag orders of the endogenous and exogenous variables. The matrix of coefficients is defined by and the least-squares estimator from this panel data structure is given by which is the result of minimizing the sums of squares of the vector . We use the log-returns and log growth rates of all the variables to provide better economic inferences.

The performance (or returns) of the stock market which is the main variable of interest is given as

where for country

i at day

t the closing stock price is represented in

, and it would be assumed as the growth rate of the last price registered of the stock market, equivalent to the difference in natural logarithms. Similarly, the same idea is used for the growth rates of the current exchange rate for the countries of analysis and the prices of the commodities. We use daily stock market data from China, the United States, Italy, Spain, South Korea, and Japan during the period from the 1st of January of 2015 to the 1st of April of 2020 (

Datastream 2020).

Table 4 presents the stock markets used in the analysis. They are selected based on having the highest index value by each country:

The information regarding the number of people infected per day in each of these countries was collected from the Center for Systems Science and Engineering (CSSE) of the John Hopkins Whiting School of Engineering (

CSSE 2020). CSSE provides well-documented data on the positive cases in absolute values of the population contaminated

3 for all of the countries of the world.

As we are working with financial data, problems of highly persistent serial correlation and heteroskedasticity are possible. To account for these issues and to provide robustness checks for the estimations, the following methodologies are utilized

4: (1) The overall panel VAR will be estimated using the panel least squares method and then compared with the Maximum Likelihood approach using the standard normal density function. (2) White–Arellano estimator (

White 1980,

1984;

Arellano 1987) with cross-section weights and

Driscoll and Kraay (

2006) robust standard errors both are used to account for heteroskedasticity and serially correlated errors

5. These robust standard errors are proper in the context of our data structure that has a longer time dimension relative to panel groups (

T > N) and considering the heteroskedastic, cross-sectionally dependent, and autocorrelated error structure (

Hoechle 2007)

6. As a VAR model is, in essence, a Seemly Unrelated Regression (SUR) model (

Triacca 2014), we can follow

Woolridge’s (

2002) recommendation to use the generalized least square method to estimate (1). By doing this, we improve the efficiency of the results unlike using conventional OLS.

The advantage of the SUR estimation is that the correlation between the errors of the equations in (1) can be examined with the Breusch and Pagan Lagrange Multiplier (

Breusch and Pagan 1980) test. De

Hoyos and Sarafidis (

2006) recommend this test to confirm the presence of cross-sectional dependence in the context of large panels (

T >

N). Based on the test results, we can confirm if Driscoll–Kraay’s robust standard errors outperform the other estimations, resulting in consistent results that account for serial correlation, heteroskedasticity, and cross-sectional dependence (

Hoechle 2007).

The methodology involves confirming the property of stationarity among the variables with the first generation of panel unit-roots, considering the test of

Levin et al. (

2002). The second-generation tests are also performed using the ones proposed by

Im et al. (

2003) and the Fisher-type unit-root test (

Choi 2001). For Equation (1) panel VAR with the generalized method of moments (GMM) becomes unfeasible

7 for the scale of T. Nevertheless, the approximation in (1) has the same structure compared with the original panel VAR model proposed by

Abrigo and Love (

2016) where the model accounts for the effects with fixed individual effects, but with the explicit difference that we are working with a large scale of T in comparison to N units.

The lag selection for

in Equation (1) is a problematic issue since the available literature cannot provide a proper guide for the same type of application, threatening the feasibility to perform the optimal moment and model selection criteria (MMSC) of

Andrews and Lu (

2001). The number of lags in

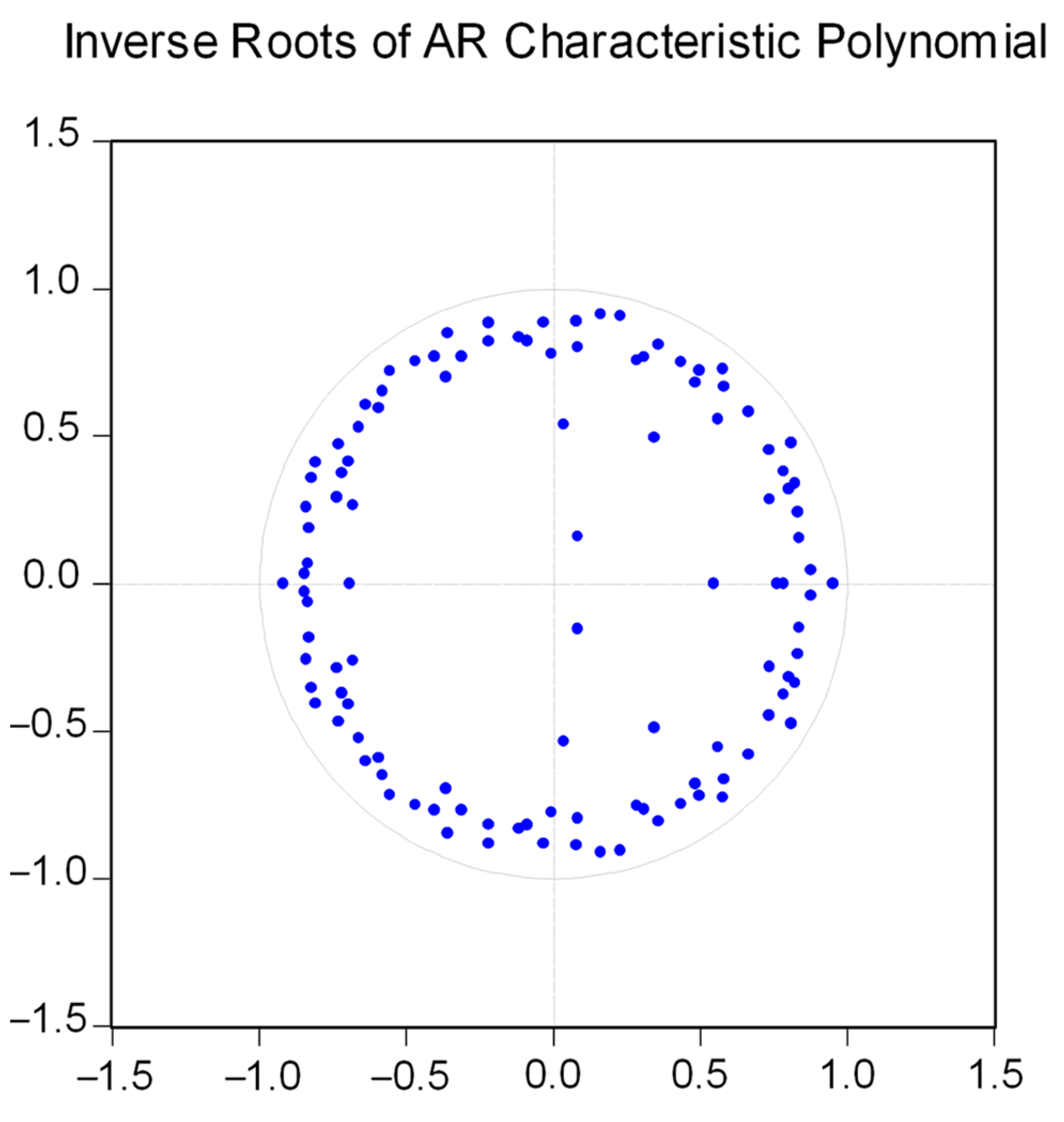

is selected based on two criteria: (1) using sufficient lags to capture the persistent serial correlation in time and (2) fulfilling the condition of stability of the model regarding the autoregressive coefficients. This is considered since with too many lags, the inverse roots of the AR characteristic polynomial can shift outside the unit circle and become unstable, the concept of parsimony is imperative in this selection.

An advantage with the current structure of the data is that endogeneity bias which emerges due to the correlation of the unobserved heterogeneity and the lagged values of the dependent variable can be corrected with the fixed effects approach. Wherein as

, the average error term becomes close to zero, therefore the bias induced in the dynamic panel data models can be avoided as recommended by

Beck and Katz (

1995).

5. Results

The first and second generation of panel unit-root tests confirmed the stationarity of the stock market performance, the growth rates of the exchange rate, the growth in the commodity prices of gold, platinum, silver, WTI, and Brent (see

Appendix A). An ideal number of lags were selected based on the error criteria of AIC, BIC, FPS, and Hannan–Quinn of the VAR model

8.

The overall panel least squares VAR estimation and the Maximum Likelihood approach yield identical results, which indicates a negative impact of 2.3% on the performance of the stock markets when the virus contamination rate increases by 1% across countries at the 99% confidence level. The model’s stability test is satisfactory but the Breush–Pagan Lagrange Multiplier test results report the presence of autocorrelation in the residuals. To account for this problem, the White–Arellano period estimator with cross-sectional weights, SUR, and the Driscoll–Kraay approaches were utilized. The results however remain robust, a decrease of around 2.3% of the performance of the stock markets is explained by the Corona Virus contamination. A slight reduction in the magnitude of the stock market performance variable to 2.1% is observed with the White–Arellano estimator (see

Appendix B for all the regression outputs).

According to the SUR model, the Breusch–Pagan test of independence is rejected, indicating the presence of cross-sectional dependence in the model of Equation (1), therefore, the Driscoll–Kraay approach provides the most accurate results as it accounts for the problems of serial correlation, heteroskedasticity, and cross-sectional dependence. The results from this approach are consistent with the rest of the estimations, yielding an empirical finding of a negative impact of 2.3% in the stock market performance across countries in time, significant at the 99% confidence level ceteris paribus.

The coronavirus is not statistically significant to explain the changes in the exchange rate and the growth of the prices of gold in the countries of analysis, regardless of this result, it is significant at the 90% confidence level to explain changes related to the prices of platinum, silver, WTI, and Brent crude oil. By a 1% increase of the coronavirus contamination rate, a significant reduction of 1.1%, 1.6%, 3.26%, and 4.08% in the prices of platinum, silver, WTI, and Brent occur. It can be noted that the biggest drop is associated with the Brent oil price, similar to

Bakas and Triantafyllou (

2020) results.

Empirical findings regarding the Granger-causality tests derived from the Driscoll–Kraay approach are located in

Appendix C. Considering the transformation of all of the variables in growth rates related to the closing prices, these tests allow to enhance the understanding of the model inner dynamics, and permits a differential view of the propensities among the correlations between the variables. The results are as follows: (1) Exchange rate, platinum, and gold granger cause the stock market performance. (2) Stock market performance, platinum, and gold granger cause exchange rate. (3) WTI, exchange rate, and oil granger cause gold. (4) Brent, WTI, and gold and silver granger cause platinum. (5) Exchange rate, Brent, WTI, Gold, and platinum granger cause silver. (6) Silver is the only variable that granger causes WTI, and Brent is granger-caused by the exchange rate. It is important to note that these dynamics are observed only during the period from January of 2015 to April of 2020, therefore, possible market deviations or new intercorrelations might arise in the future as the coronavirus endure.

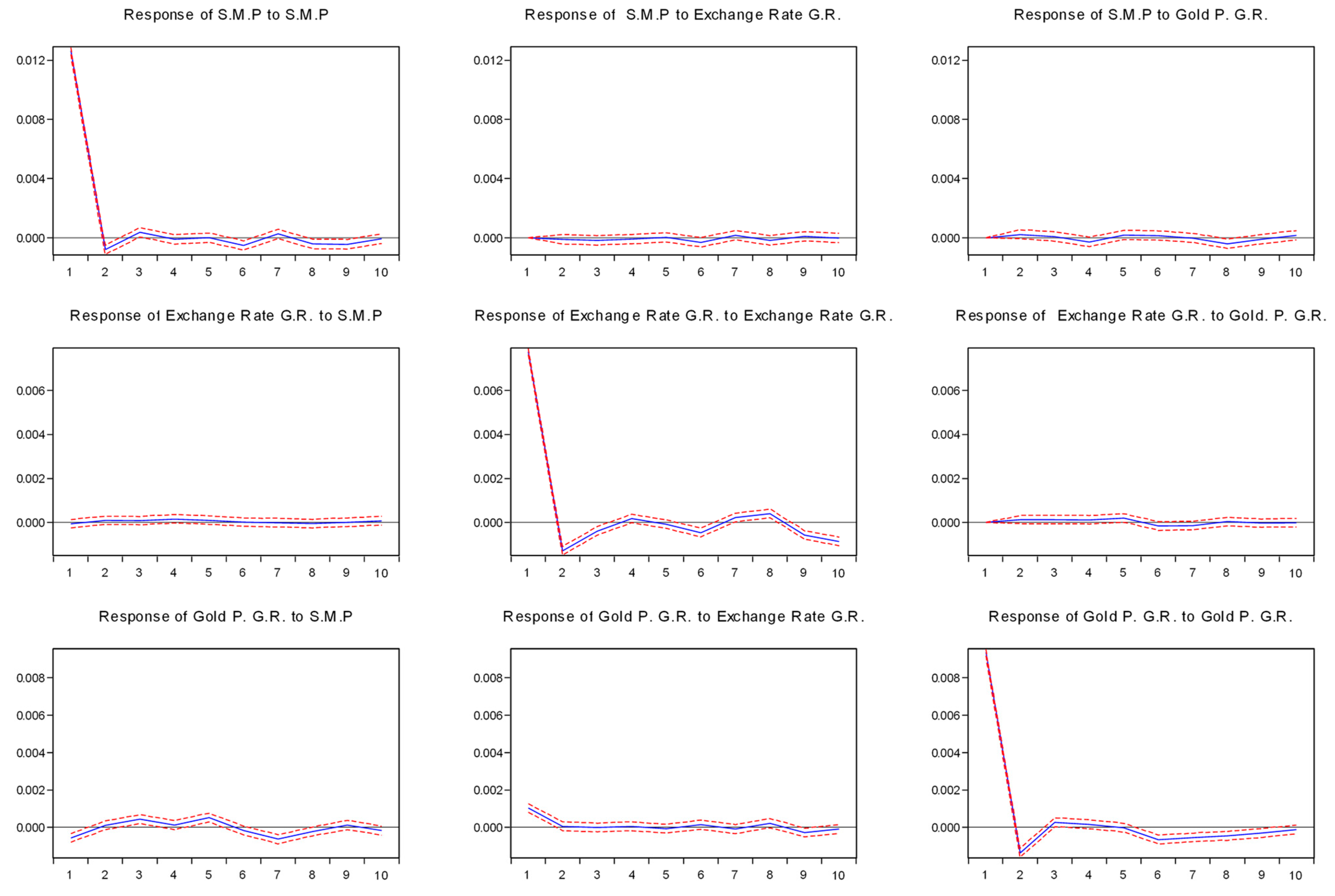

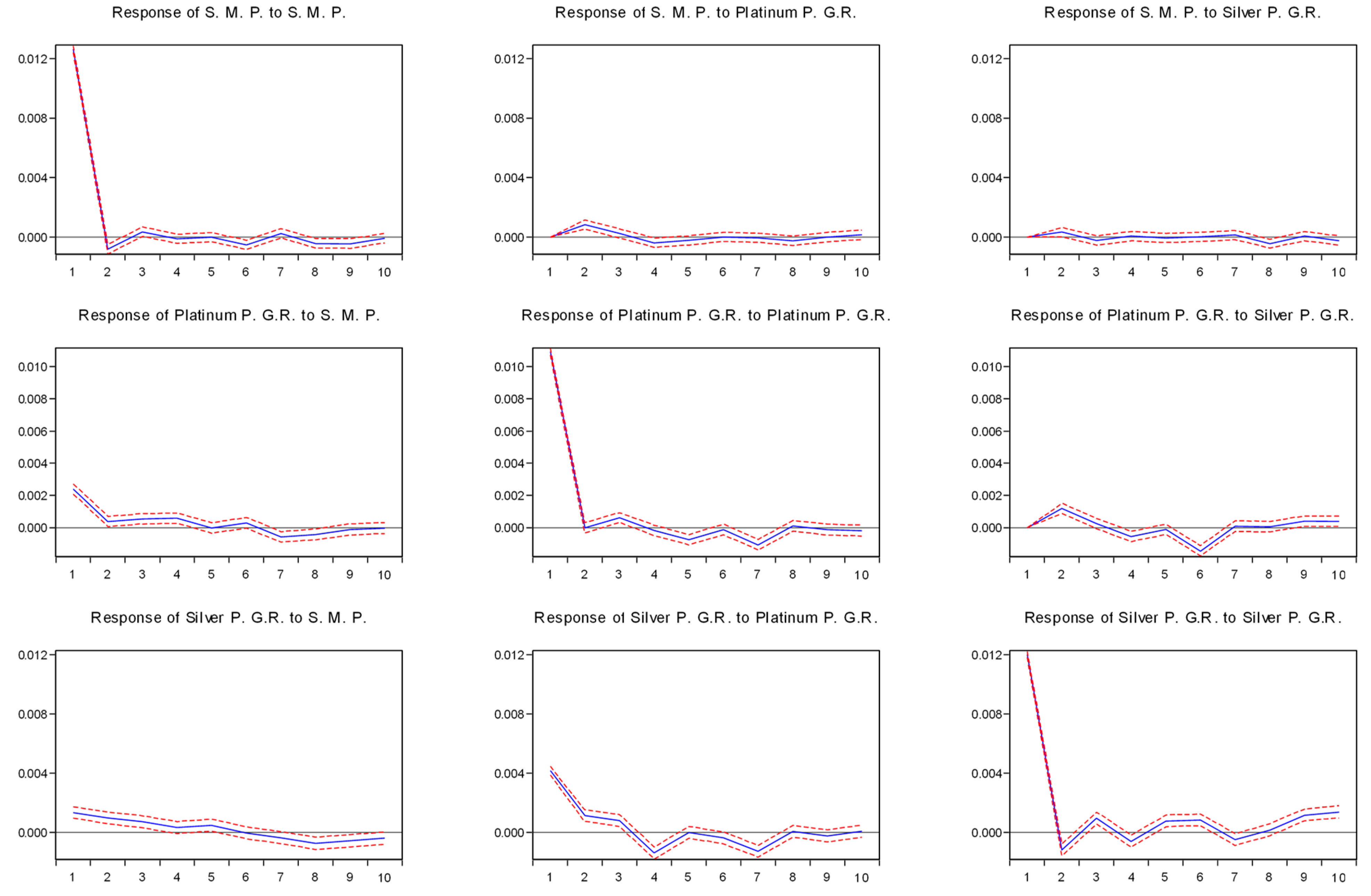

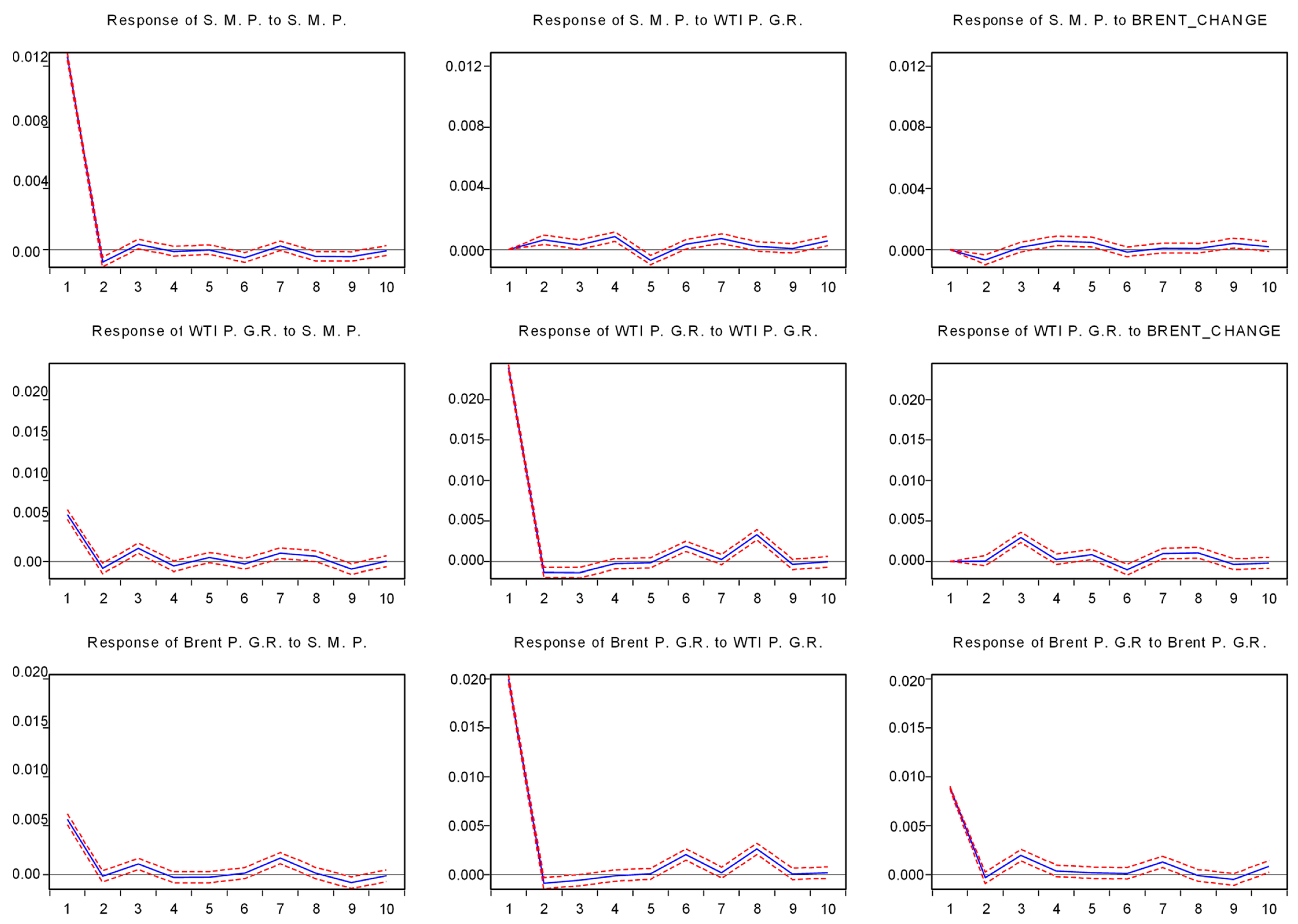

The impulse response function of the panel VAR model is presented in

Appendix D, and it indicates that within an initial shock, for each variable considering the response for its own, there’s a decreasing but significant effect, which tends to disappear in 8–10 days. A positive shock in stock market performance causes a short-termed positive shock in gold, WTI, and Brent oil. Platinum and silver commodities tend to behave similarly yet for a relatively long period, around 4 days after initial shock in the stock market performance. A positive shock in Brent tends to increase WTI prices. Silver reacts positively to stock market performance for a short time, then the effect reverts after the fifth day and becomes negative.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}