1. Introduction

Consumption within the U.S. is reduced significantly due to the coronavirus disease 2019 (COVID-19). As shown by studies such as by

Baker et al. (

2020b) or

Relihan et al. (

2020), this reduction is evident widely across sectors (except for grocery) and especially for products purchased through offline (rather than online) shopping. However, these observations based on nationwide data can easily suppress valuable information on consumption patterns coming from more disaggregated areas as their effects may cancel each other out during the aggregation process. For example, when zip codes are considered, spending on a particular sector may increase in one zip code, whereas it may decrease in another, resulting in no significant impact at the aggregate level. Therefore, using data from more disaggregated areas is important to understand the changes in consumption patterns amid COVID-19.

Based on this motivation, this paper investigates sector-level as well as online versus offline consumption patterns within the U.S. by using monthly zip-code level data from the early COVID-19 era (covering 16 U.S. cities) on credit card transactions for local commercial purchases. The main strategy is to identify common factors across zip codes representing sector-level or online versus offline consumption patterns at the U.S. national level that do not suffer from an aggregation problem. This is achieved by estimating sector-time fixed effects or shopping channel-time fixed effects in the monthly zip-code level data, where factors that are zip-code and time specific as well as those that are zip-code and sector specific are controlled for.

The results based on the sector-level data show that relative consumption of products and services that can be consumed at home (e.g., grocery, pharmacy, home maintenance) has increased by up to 56% amid COVID-19, whereas relative consumption of products and services that cannot be consumed at home (e.g., fuel, transportation, personal care services, restaurant) has decreased by up to 51%. This result is analogous to the one that has been used to explain the reduction in economic activity, unemployment or social distancing experience by workers’ ability of working from home as in studies such as by

Dingel and Neiman (

2020);

Bick et al. (

2020) or

Yilmazkuday (

2020). The difference in this paper is that it is consuming at home that can be connected to the sectoral heterogeneity in consumption changes amid COVID-19.

With respect to the existing literature, the sector-level results are consistent with other studies focusing on the U.S. such as by

Coibion et al. (

2020) who have documented largest drops in spending on travel and clothing or by

Baker et al. (

2020b) who have shown that greater levels of social distancing are associated with drops in spending on restaurants or by

Grashuis et al. (

2020) who have shown that consumer spending on groceries has increased amid COVID-19. Nevertheless, different from these studies that focus on aggregate-level data in the U.S., this paper has shown that, after controlling for factors that are zip-code and time specific as well as those that are zip-code and sector specific, common factors across zip codes representing relative spending on general goods, home maintenance, pharmacy and professional services have increased over time amid COVID-19. This difference can be attributed to estimating common factor across zip codes in this paper as opposed to using aggregate-level data.

The results based on online versus offline shopping show that online shopping has increased by up to 21%, while its expenditure share has increased by up to 16% compared to the pre-COVID-19 period. These results are consistent with those in

Relihan et al. (

2020) who have used an earlier version of the dataset used in this paper and shown that the increase in online shopping has been only about 1.5% in March 2020 (with respect to March 2019). Nevertheless, different from

Relihan et al. (

2020) who have focused on aggregate-level data in the U.S. to obtain this measure, this paper has shown that, after controlling for factors that are zip-code and time specific as well as those that are zip-code and sector specific, the common factor across zip codes representing online spending within the U.S. has increased by about 7.4% in March 2020 (with respect to March 2019). This difference can again be attributed to estimating common factor across zip codes in this paper as opposed to using aggregate-level data.

2. Literature Review

Regarding the sector-level consumption, studies such as by

Baker et al. (

2020b) have shown that consumption on retail (food) products have initially increased, followed by a significant reduction in overall spending; they have also shown that greater levels of social distancing are associated with drops in spending on restaurants. Similarly,

Coibion et al. (

2020) have documented largest drops in spending on travel and clothing, whereas

Grashuis et al. (

2020) have documented increases in spending on groceries. Different from these studies focusing on the (geographically) aggregate level data covering different sectors, this paper focuses on common factors across zip codes to avoid any aggregation bias.

Regarding online versus offline consumption, studies such as by

Carvalho et al. (

2020) have shown that offline shopping has declined much more than online shipping, whereas studies such as by

Chen et al. (

2021) have shown that offline shopping has reduced by about 70% following COVID-19. Similarly,

Relihan et al. (

2020) have shown that the increase in online shopping has been only about 1.5% in March 2020 (with respect to March 2019). Different from these studies focusing on the (geographically) aggregate level data covering online versus offline shopping or the corresponding heterogeneity, this paper focuses on common factors across zip codes to avoid any aggregation bias.

3. Data Set

Monthly zip-code level dataset on consumption covering 3674 zip codes from 16 U.S. cities is borrowed from

Relihan et al. (

2020). This dataset has been constructed by aggregating approximately 450 million credit card transactions (at the zip-code level based on consumer residence) per month made by a rolling sample of 11 million JPMorgan Chase customer accounts. Focusing on purchases from local commercial places, the dataset distinguishes between consumption across different sectors as well as between online and offline shopping as we detail in the following subsections.

The dataset includes information on percentage changes (with respect to the previous year) in spending on products of 11 sectors as well as corresponding the expenditure shares over the period between October 2019 and May 2020. The list of these 11 sectors can be found in

Table 1. Although most of these sector names are self-explanatory, some may require further clarification.

Specifically, general goods include department stores, discount stores, large non-specific online retailers, and other miscellaneous retailers such as florists and books stores that sell everyday goods. Home maintenance includes both goods and services. Leisure goods and services include those related to arts and sporting activities. Personal care services include salons and dry cleaners. Professional consumer services examples include veterinary, legal, and childcare services.

The dataset also includes information of shopping channels, namely online versus offline shopping, at the aggregate level (for all rather than individual sectors). Due to the heterogeneity across zip codes, in the following sections, we focus on formal investigations to estimate sector-level consumption patterns, as well as those through online versus offline shopping, in the U.S. by focusing on the common factors across zip codes to avoid any aggregation bias as discussed above.

4. Sector-Level Analysis

This section achieves formal investigations on the sector-level data as described above.

4.1. Empirical Methodology

We are interested in estimating common factors across zip codes representing sector-level consumption patterns within the U.S., where the dataset described above is controlled for factors that are zip-code and time specific as well as those that are zip-code and sector specific. We focus on both percentage changes in sector-level spending and sector-level expenditure shares, below.

The formal investigation based on the sector-level spending is achieved according to the following expression:

where

is the percentage change (with respect to the previous year) in spending on sector-s products in zip-code

z at time

t. In this expression, we are interested in sector-time fixed effects represented by

’s as they are common factors across zip codes representing relative sector-level percentage changes in spending within the U.S. after controlling for other factors. These factors include zip-code-time fixed effects represented by

’s as they control for the effects of zip-code specific developments over time, such as a certain zip code being affected by COVID-19 more than others in general over time. Similarly, sector-zip-code fixed effects represented by

’s control for factors such as consumer preferences in certain zip codes that are constant over time.

Similarly, the formal investigation based on sector-level expenditure shares is achieved according to the following expression:

where

is the expenditure share on sector-s products in zip-code

z at time

t. Here, we are interested in sector-time fixed effects represented by

’s, this time as they are common factors across zip codes representing relative sector-level expenditure shares within the U.S. after controlling for other factors as they are described above.

4.2. Empirical Results Based on Spending

The estimation of Equation (1) is achieved by using 249,698 observations that results in estimates of

’s,

’s and

’s with an adjusted R-squared value of 0.73. The corresponding estimates of

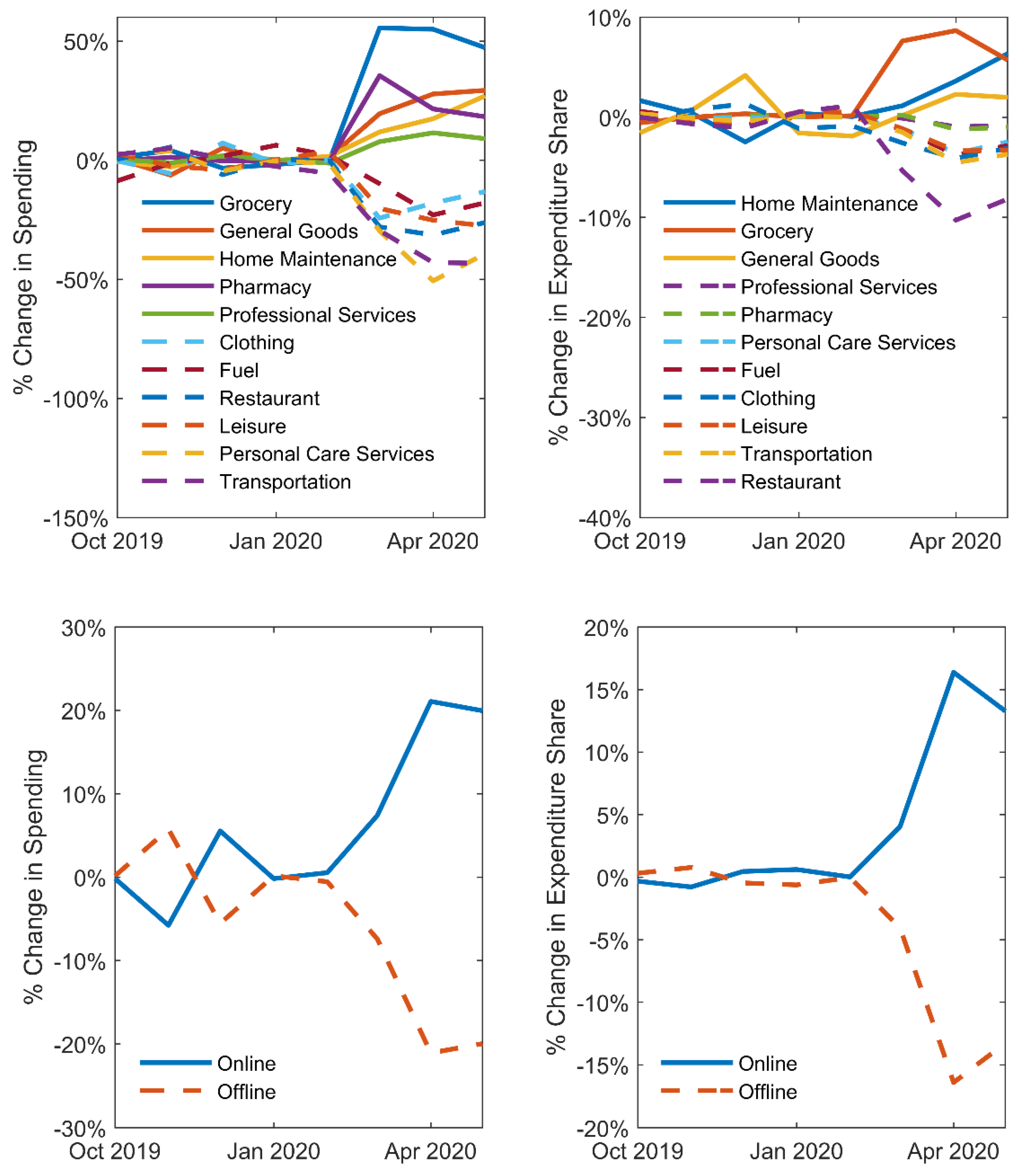

’s representing common factors across zip codes for individual sectors are depicted in

Figure 1 for individual sectors, where their average values between October 2019 and February 2020 are also shown for comparison purposes. As is evident, there is evidence for sectoral heterogeneity in consumption changes amid COVID-19. In particular, relative spending on sectors of clothing, fuel, leisure, personal care services, restaurant services and transportation has decreased amid COVID-19, whereas relative spending in other sectors of general goods, grocery, home maintenance, pharmacy or professional services has increased.

Regarding the magnitudes, the estimation results in

Figure 1 are further given with more details in

Table 1, where the estimates are again normalized with respect to their pre-COVID-19 period. As is evident, spending on grocery products has increased by about 56%, whereas spending on personal care services or transportation has decreased about 30%, all in March 2020 with respect to the pre-COVID-19 period. Similarly, spending on grocery products has increased by about 55%, whereas spending on personal care services has decreased about 51%, both in April 2020 with respect to the pre-COVID-19 period. Similar values are observed for May 2020, when home maintenance has increased about 27% with respect to the pre-COVID-19 period.

4.3. Empirical Results Based on Expenditure Shares

The estimation of Equation (2) is achieved by using 249,698 observations that results in estimates of

’s,

’s and

’s with an adjusted

R-squared value of 0.97. The corresponding estimates of

’s representing sector-time fixed effects are depicted in

Figure 1 for individual sectors with equal pre-COVID-19 values for comparison purposes. As is evident, the results based on expenditure shares highly mimic those based on spending, except for sectors of pharmacy and professional services of which expenditure shares have decreased, and spending on these sectors have increased.

Regarding the magnitudes, the estimation results in

Figure 1 are further given with more details in

Table 2, where the estimates are again normalized with respect to their pre-COVID-19 period. As is evident, expenditure share has increased up to 9% (for grocery products), whereas it has decreased up to 10% (for restaurant services), both in April 2020.

4.4. Discussion on Estimation Results

The results based on the sector-level data are consistent with other studies focusing on the U.S. such as by

Coibion et al. (

2020) who have documented largest drops in spending on travel and clothing or by

Baker et al. (

2020b) who have shown that greater levels of social distancing are associated with drops in spending on restaurants or by

Grashuis et al. (

2020) who have shown that consumer spending on groceries has increased amid COVID-19. Nevertheless, different from these studies that focus on aggregate-level data in the U.S., this paper has shown that, after controlling for factors that are zip-code and time specific as well as those that are zip-code and sector specific, common factors across zip codes representing relative spending on general goods, home maintenance, pharmacy and professional services have increased over time amid COVID-19.

Regarding economic intuition behind the results, it is evident that consumption of products and services that can be consumed at home (e.g., grocery, pharmacy, home maintenance) have increased amid COVID-19, whereas consumption of products and services that cannot be consumed at home (e.g., fuel, transportation, personal care services, restaurant) have decreased. This approach is similar to the one that has been used to explain the reduction in economic activity, unemployment or social distancing experience by workers’ ability of working from home as in studies such as by

Dingel and Neiman (

2020);

Bick et al. (

2020) or

Yilmazkuday (

2020). The only difference is that it is consuming at home that can be connected to the sectoral heterogeneity in consumption changes amid COVID-19 as in this paper.

5. Online versus Offline Shopping

This section achieves formal investigations using data on online versus offline shopping as described above.

5.1. Empirical Methodology

We are interested in estimating common factors across zip codes representing online versus offline shopping patterns within the U.S., where the dataset described above is controlling for factors that are zip-code and time specific as well as those that are zip-code and sector specific. As in the case of sector-level investigation, we focus on both percentage changes in spending and expenditure shares, below.

The formal investigation based on online versus offline shopping is achieved according to the following expression:

where

is the percentage change (with respect to the previous year) in spending through shopping channel n (representing either online or offline shopping) in zip-code

z at time

t. In this expression, we are interested in shopping channel-time fixed effects represented by

’s as they are common factors across zip codes representing relative percentage changes in spending through online versus offline shopping within the U.S. after controlling for other factors as they are described above.

Likewise, the formal investigation based on online versus offline expenditure shares is achieved according to the following expression:

where

is the expenditure share on products through shopping channel n (representing either online or offline shopping) in zip-code

z at time

t. Here, we are again interested in shopping channel-time fixed effects represented by

’s, this time as they are common factors across zip codes representing relative expenditure shares on products purchased through online versus offline shopping within the U.S. after controlling for other factors as they are described above.

5.2. Empirical Results Based on Spending

The estimation of Equation (3) is achieved by using 56,220 observations that results in estimates of

’s,

’s and

’s with an adjusted

R-squared value of 0.73. The corresponding estimates of

’s representing shopping channel-time fixed effects are depicted in

Figure 1 with equal pre-COVID-19 values for comparison purposes. As is evident, relative spending through online shopping has increased amid COVID-19, whereas relative spending through offline shopping has decreased.

Regarding the magnitudes, the corresponding estimates between March 2020 and May 2020 are further given in

Table 3, where they are mirror images of each other (representing relative changes) as they add up to zero. As is evident, relative online (offline) spending has increased (decreased) significantly amid COVID-19 by up to 21% in April 2020 and 20% in May 2020, both with respect to the pre-COVID-19 period.

5.3. Empirical Results Based on Expenditure Shares

The estimation of Equation (4) is achieved by using 56,220 observations that results in estimates of

’s,

’s and

’s with an adjusted R-squared value of 0.79. The corresponding estimates of

’s representing shopping channel-time fixed effects are depicted in

Figure 1 for online versus offline shopping with equal pre-COVID-19 values for comparison purposes. As is evident, relative expenditure share through online shopping has increased amid COVID-19, whereas relative expenditure share through offline shopping has decreased.

Regarding the magnitudes, the corresponding estimates between March 2020 and May 2020 are further given in

Table 4, where they are mirror images of each other (representing relative changes) as they add up to zero. As is evident, relative expenditure share of online (offline) shopping has increased (decreased) significantly amid COVID-19 by up to 16% in April 2020 and 13% in May 2020, both with respect to the pre-COVID-19 period.

5.4. Discussion on Estimation Results

The results based on online versus offline shopping are consistent with those in

Relihan et al. (

2020) who have used an earlier version of the dataset used in this paper and shown that the increase in online shopping has been only about 1.5% in March 2020 (with respect to March 2019). Nevertheless, different from this study that has focused on aggregate-level data in the U.S., this paper has shown that, after controlling for factors that are zip-code and time specific as well as those that are zip-code and sector specific, the common factor across zip codes representing online spending within the U.S. has increased by about 7.4% in March 2020 (with respect to March 2019).

Regarding economic intuition behind the results, the increase in online shopping during COVID-19 can be observed as a reducing factor on the negative consumption effects as in studies such as by

Bounie et al. (

2020). Hence, it can be claimed that resilience of the U.S. economy has improved due to online shopping. However, as shown by studies such as by

Watanabe and Omori (

2020), online consumption has increased mostly due to consumers who were already familiar with online consumption before COVID-19. It is implied that encouraging online shopping can easily reduce the severity of economic recessions caused by similar reasons in the future.

6. Conclusions

Using monthly zip-code level data on credit card transactions covering 16 U.S. cities, this paper has investigated the changes in consumption at local commercial places in the early COVID-19 era. Different from earlier studies focusing on aggregate-level data that can suppress valuable information coming from more disaggregated areas, this paper has identified common factors across zip codes so that the estimated sector-level or online versus offline consumption patterns at the U.S. national level do not suffer from an aggregation bias.

The results based on the sector-level data show that relative consumption of products and services that can be consumed at home (e.g., grocery, pharmacy, home maintenance) has increased by up to 56% amid COVID-19, whereas relative consumption of products and services that cannot be consumed at home (e.g., fuel, transportation, personal care services, restaurant) has decreased by up to 51%. Therefore, similar to the working-from-home approach in the literature used to explain the reduction in economic activity, unemployment or social distancing, consuming-at-home that can be connected to the sectoral heterogeneity in consumption changes amid COVID-19 as in this paper.

The results based on online versus offline shopping show that online shopping has increased by up to 21%, while its expenditure share has increased by up to 16% compared to the pre-COVID-19 period. This increase in online shopping can be observed as a reducing factor on the negative consumption effects, and thus, it can be claimed that resilience of the U.S. economy has improved due to online shopping. Since online consumption has increased mostly due to consumers who were already familiar with online consumption before COVID-19, it is implied that encouraging online shopping can reduce the severity of economic recessions caused by similar reasons in the future.

The results are not without caveats, though. Specifically, although the monthly dataset on consumption cover 3674 zip codes from 16 U.S. cities for the early COVID-19 period, a better geographical coverage with a longer sample period within the U.S. or across countries may improve the results. As such data were not available at the time this paper as written, we leave this extension as a topic of future research.

{kind=link}