Impact of COVID-19 on the Stock Market by Industrial Sector in Chile: An Adverse Overreaction

Abstract

:1. Introduction

2. Materials and Methods

2.1. Used Data

2.2. COVID-19 Pandemic Timetable

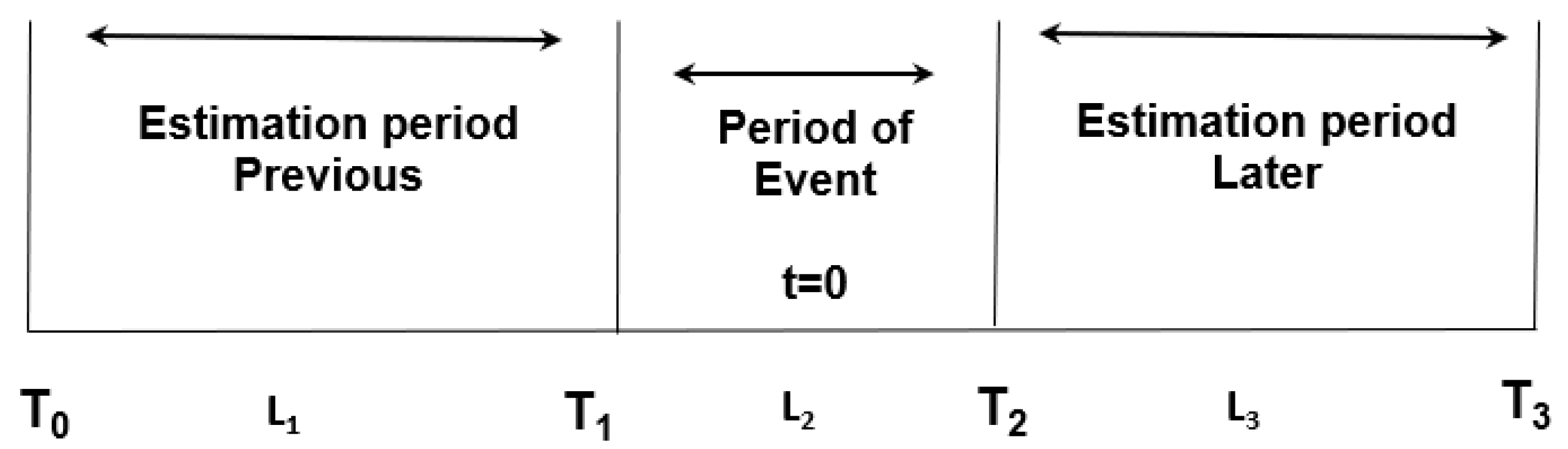

2.3. Methodology Event Study

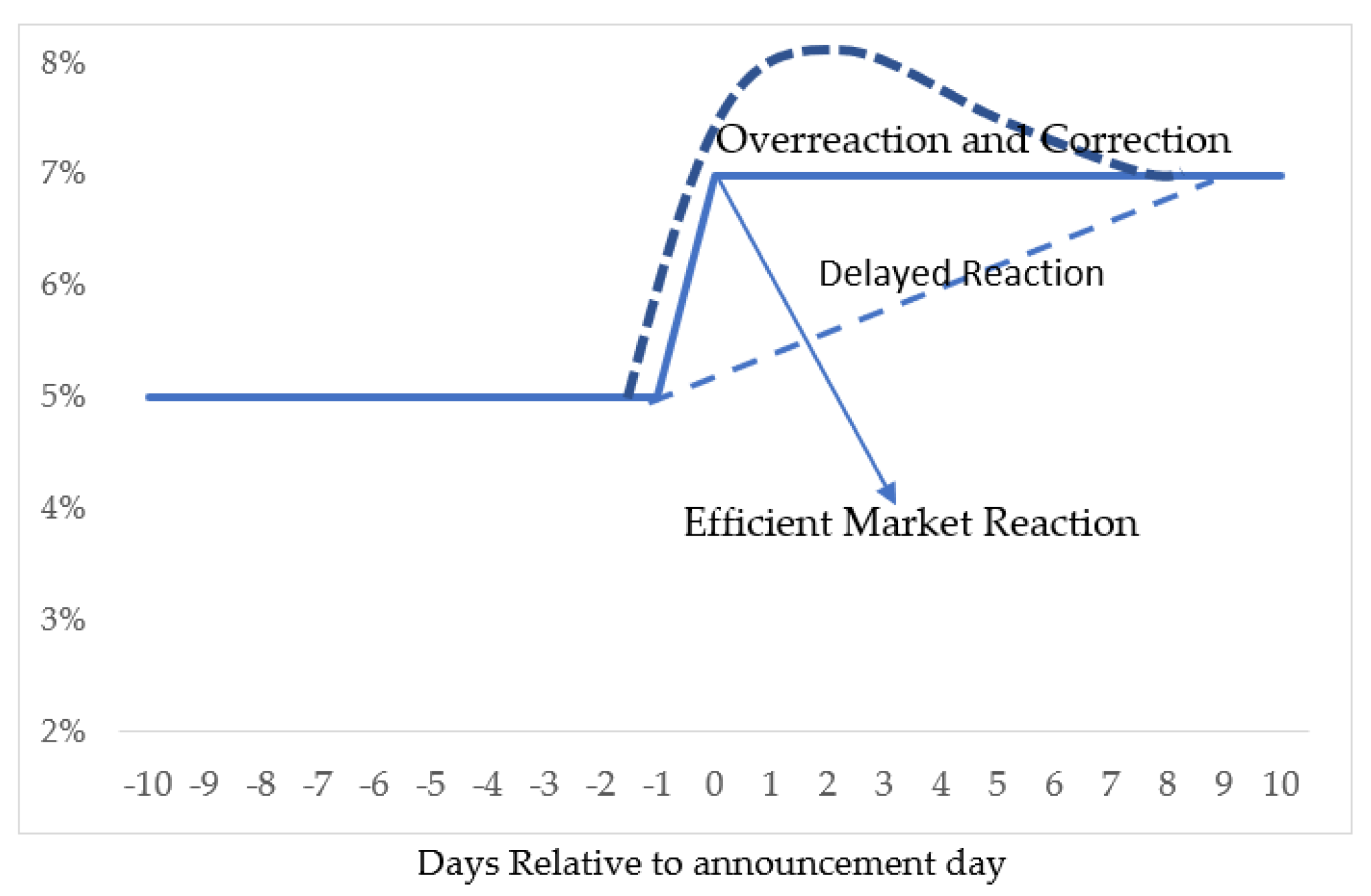

2.4. Analysis of Reaction to New Information in the Market

- The incorporation of the new information at time t = 0 and the implementation of a proper correction.

- A positive overreaction to the news, where prices react earlier and slowly correct themselves. It can also be a negative overreaction in the case that the news negatively affects the price of the asset.

- A delayed reaction; the price of the asset does not react at t = 0 before the news release but does react after the news that affects the market.

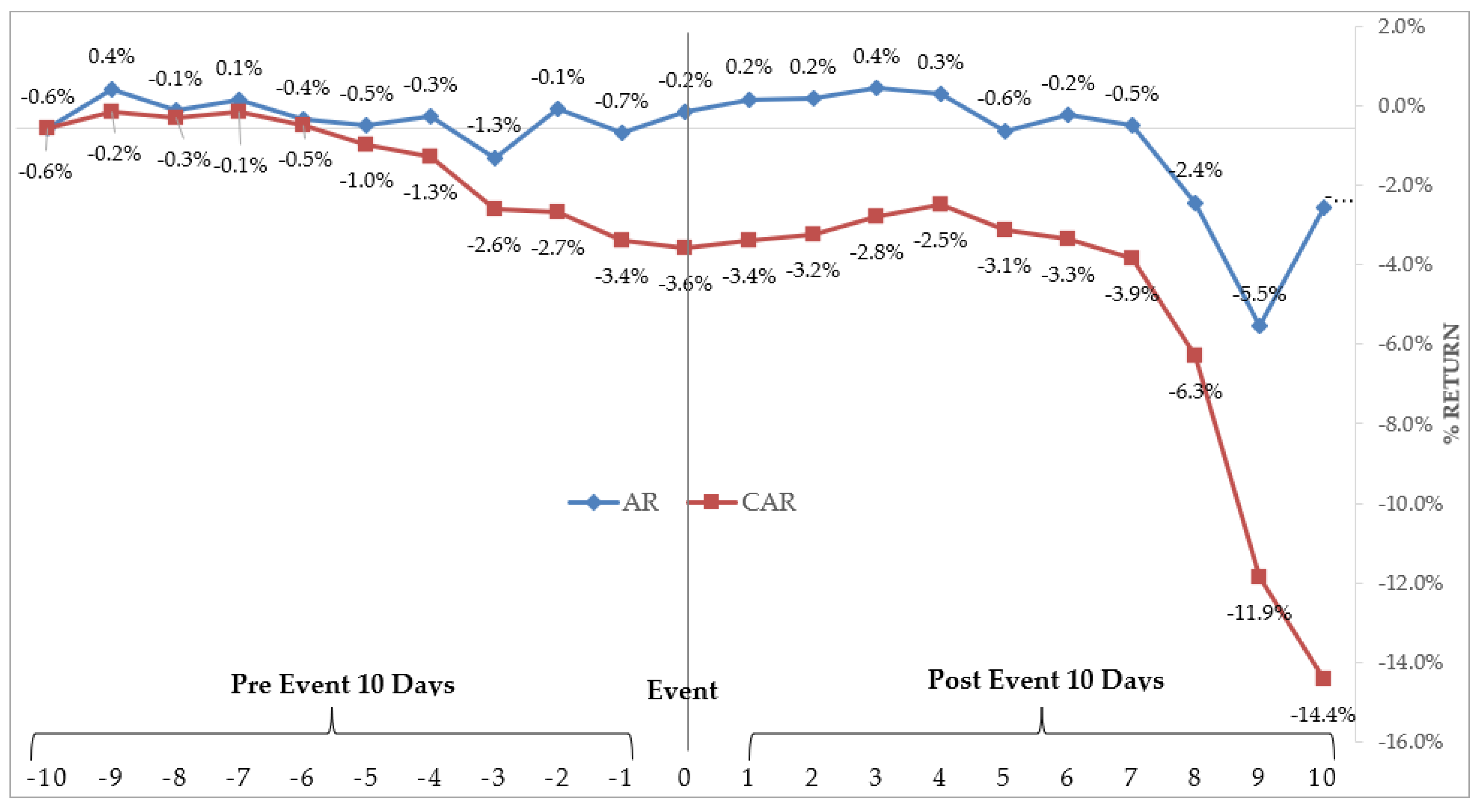

3. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abuzayed, Bana, Elie Bouri, Nedal Al-Fayoumi, and Naji Jalkh. 2021. Systemic risk spillover across global and country stock markets during the COVID-19 pandemic. Economic Analysis and Policy 71: 180–97. [Google Scholar] [CrossRef]

- Adnan, Abu Taleb Mohammad, Mohammad Mahadi Hasan, and Ezaz Ahmed. 2020. Capital Market Reactions to the Arrival of COVID-19: A Developing Market Perspective. The Economic Research Guardian 10: 97–121. [Google Scholar]

- Ahmed, Fakrul. 2021. Assessment of Capital Market Efficiency in COVID-19. European Journal of Business and Management Research 6: 42–6. [Google Scholar] [CrossRef]

- Albulescu, Claudiu Tiberiu. 2021. COVID-19 and the United States financial markets’ volatility. Finance Research Letters 38: 1–5. [Google Scholar] [CrossRef]

- Banco Central de Chile. 2020. Informe de Política Monetaria. Santiago de Chile: Banco Central de Chile. [Google Scholar]

- Binder, John J. 1998. The Event Study Methodology Since 1969. Review of Quantitative Finance and Accounting 11: 111–37. [Google Scholar] [CrossRef]

- Bolsa de Santiago de Chile. 2021. Bolsa de Santiago. October 6. Available online: https://www.bolsadesantiago.com/ (accessed on 10 July 2021).

- Bouri, Elie, Oguzhan Cepni, David Gabauer, and Rangan Gupta. 2020. Return connectedness across asset classes around the COVID-19 outbreak. International Review of Financial Analysis 73: 1–11. [Google Scholar] [CrossRef]

- Bouri, Elie, Riza Demirer, Rangan Gupta, and Jacobus Nel. 2021. COVID-19 Pandemic and Investor Herding in International Stock Markets. Herding in International Stock Risks 9: 168. [Google Scholar] [CrossRef]

- Brown, Stephen J., and Jerold B. Warner. 1985. Using Daily Stock Returns: The Case of Event Studies*. Journal of Financial Economics 14: 3–31. [Google Scholar] [CrossRef]

- Campbell, Cynthia J., Arnold R. Cowan, and Valentina Salotti. 2010. Multi-Country Event Study Methods. Journal of Banking & Finance 34: 3078–90. [Google Scholar]

- Campbell, Cynthia, and Charles Wasley. 1992. Measuring security price performance using daily NASDAQ returns. Journal of Financial Economics 33: 73–92. [Google Scholar] [CrossRef]

- Chen, Ming-Hsiang, SooCheong (Shawn) Jang, and Woo Gon Kim. 2007. The impact of the SARS outbreak on Taiwanese hotel stock performance: An event-study approach. Hospitality Management 26: 200–12. [Google Scholar] [CrossRef]

- CNN Chile. 2020. Cnnchile. May 5. Available online: https://www.cnnchile.com/coronavirus/hitos-claves-covid-19-chile-mundo-cronologia_20200505/ (accessed on 10 July 2021).

- Corrado, Charles J. 1989. A nomparametric test for abnormal securiy-price performance in event studies. Journal of Financial Economics 23: 385–95. [Google Scholar] [CrossRef]

- Corrado, Charles J., and Terry L. Zivney. 1992. The Specification and Power of the Sign Test in Event Study Hypothesis Tests Using Daily Stock. The Journal of Financial and Quantitative Analysis 27: 465–78. [Google Scholar] [CrossRef]

- Doria, Carlos Fernando, and William Niebles Nuñez. 2020. El mercado integrado latinoamericano-MILA-en tiempo de Covid-19. Revista Aglala 11: 17–37. [Google Scholar]

- Duarte, Juan Juan Benjamín, and Juan Manuel Mascareñas. 2014. Comprobación de la eficiencia débil en los principales mercados. Estudios Gerenciales 30: 365–75. [Google Scholar] [CrossRef] [Green Version]

- Evangelos, Vasileiou. 2020. Efficient Markets Hypothesis in the Time of COVID-19. Review of Economic Analysis 13: 45–62. [Google Scholar]

- Fama, Eugene. 1969. Efficient Capital Markets II. The Journal of Finance 46: 1575–617. [Google Scholar] [CrossRef]

- Fama, Eugene. 1965. Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance 25: 28–30. [Google Scholar] [CrossRef]

- Fama, Eugene F., Lawrence Fisher, Michael C. Jensen, and Richard Roll. 1970. The Adjustment of Stock Prices to New Information. International Economic Review 10: 1–21. [Google Scholar] [CrossRef]

- Fama, Eugene. 1991. The Behavior of Stock-Market Prices. The Journal of Business, 34–105. [Google Scholar] [CrossRef]

- Funakoshi, Minami, and Travis Hartman. 2020. Mad March: How the Stock Market Is Being Hit by COVID-19. March 23, Available online: https://www.weforum.org/agenda/2020/03/stock-market-volatility-coronavirus/ (accessed on 20 May 2021).

- Hassan, Hashibul, and Shahidullah Kayser. 2019. Ramadan effect on stock market return and trade volume: Evidence from Dhaka Stock Exchange (DSE). Cogent Economics & Finance 7: 1605105. [Google Scholar]

- Kendall, M. G., and A. Bradford Hill. 1953. The Analysis of Economic Time-Series-Part I: Prices. Journal of the Royal Statistical Society. Series A (General) 116: 11–34. [Google Scholar] [CrossRef]

- MacKinlay, A. Craig. 1997. Event Studies in Economics and Finance. Journal of Economic Literature 35: 13–39. [Google Scholar]

- Malkiel, Burton G. 2003. The Eficcient Market Hypothesis and Its Critics. Journal of Economic Perspectives 17: 59–82. [Google Scholar] [CrossRef] [Green Version]

- Martín Ugedo, Juan Francisco. 2003. Metodología de los Estudios de Sucesos: Una Revisión. España: Investigaciones Europeas de Dirección y Economía de la Empresa. [Google Scholar]

- Navratil, Robert, Stephen Taylor, and Jan Vecer. 2021. On equity market inefficiency during the COVID-19 pandemic. International Review of Financial Analysis, 1–9. [Google Scholar] [CrossRef]

- Nippani, Srinivas, and Kenneth M. Washer. 2004. SARS: A non-event for affected countries’ stock. Applied Financial Economics 14: 1105–10. [Google Scholar] [CrossRef]

- Pandey, Dharen Kumar, and Vineeta Kumari. 2020. Event study on the reaction of the developed and emerging stock markets to the 2019-nCoV outbreak. International Review of Economics and Finance, 467–83. [Google Scholar] [CrossRef]

- Peterson, Pamela P. 1989. Event Studies: A Review of Issues and Methodology. Quarterly Journal of Business and Economics 28: 36–66. [Google Scholar]

- Phan, Dinh Hoang, and Paresh Kumar Narayan. 2020. Country Responses and the Reaction of the Stock Market to COVID-19. Emerging Markets Finance and Trade 2020 56: 2138–50. [Google Scholar] [CrossRef]

- Ramírez, Laura Bibiana, Aura María Valencia, and Diana Marcela Villalba. 2017. Evaluación de la eficiencia en nivel débil de la información en los mercados de renta variable de los países pertenecientes al MILA 2011–2016: Una estimación a partir del modelo de Tres Factores de Fama y French. Colombia: Facultad de Ciencias Económicas y Sociales–Universidad de la Salle. [Google Scholar]

- Sepúlveda, Jorge, Pablo Tapia, and Boris Pastén. 2021. Analyzing Stock Market Signals for H1N1 and COVID-19: The BRIC Case. Santiago: Munich Personal RePEc Archive. [Google Scholar]

- Shahzad, Syed Jawad, Muhammad Abubakr Naeem, Zhe Peng, and Elie Bouri. 2021. Asymmetric volatility spillover among Chinese sectors during COVID-19. International Review of Financial Analysis 75: 1–9. [Google Scholar] [CrossRef]

- Sharpe, William F. 1963. A Simplified Model for Portfolio Analysis. Management Science 9: 277–93. [Google Scholar] [CrossRef] [Green Version]

- Singh, Bhanwar, Rosy Dhall, Sahil Narang, and Savita Rawat. 2020. The Outbreak of COVID-19 and Stock Market Responses: An Event Study and Panel Data Analysis for G-20 Countries. Global Business Review 1: 1–26. [Google Scholar] [CrossRef]

- Sin-Yi, Cindy Tsai. 2011. The Real World is Not Normal. Chicago: Morningstar Alternative Investments Observer. [Google Scholar]

- Vasileiou, Evangelos, Aristeidis Samitas, Maria Karagiannaki, and Jagadish Dandu. 2021. Health risk and the efficient market hypothesis in the time of COVID-19. International Review of Applied Economics 35: 210–23. [Google Scholar] [CrossRef]

- Xiong, James X., and Thomas M. Idzorek. 2011. The Impact of Skewness and Fat Tails on the Asset Allocation Decision. Financial Analysts Journal 67: 23–35. [Google Scholar] [CrossRef] [Green Version]

- Yan, Heather, Andy Tu, Logan Stuart, and Qingquan Zhang. 2020. Analysis of the Effect of COVID-19 On the Stock Market and Potential Investing Strategies. Illinois: Gies School of Business, University of Illinois Urbana-Champaign. [Google Scholar]

- Yousaf, Imran, Elie Bouri, Shoaib Ali, and Nehme Azoury. 2021. Gold against Asian Stock Markets during the COVID-19 Outbreak. Journal of Risk and Financial Management 14: 186. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Asset | Industry | Asset | Industry | Asset | Industry | Asset | Industry |

|---|---|---|---|---|---|---|---|

| BCI | Banking | SM-CHILE B | Holding | PARAUCO | Const. & real estate | SONDA | IT |

| BSANTANDER | Banking | MASISA | Industrial | SALFACORP | Const. & real estate. | ENTEL | Commu-nication |

| CHILE | Banking | SK | Industrial | ANDINA_B | Consumption | LTM | Air travel |

| ITAUCORP | Banking | SMSAAM | Industrial | CCU | Consumption | AESGENER | Utilities |

| SECURITY | Banking | VAPORES | Industrial | CONCHATORO | Consumption | AGUAS_A | Utilities |

| CAP | Commodities | CENCOSUD | Retail | EMBONOR-B | Consumption | COLBUN | Utilities |

| CMPC | Commodities | FALABELLA | Retail | ANTARCHILE | Holding | ECL | Utilities |

| COPEC | Commodities | FORUS | Retail | IAM | Holding | ENELAM | Utilities |

| SQMB | Commodities | NUEVAPO-LAR | Retail | ILC | Holding | ENELCHILE | Utilities |

| BESALCO | Const. & real estate | RIPLEY | Retail | OROBLANCO | Holding | ENELGXCH | Utilities |

| Event Date | News |

|---|---|

| 31 December 2019 | First case The World Health Organization first reports that between 12 and 29 December, certain people who had been around an animal market in Wuhan became infected with an unknown virus. A type of pneumonia is talked about. |

| 1 January 2020 | Wuhan market becomes shut down Chinese health authorities shut down the market, right after speculations stated that the source of the virus could be the wild and exotic species commercialized there. |

| 7 January 2020 | Virus identification Wuhan authorities announce the virus has been identified as a new coronavirus strain. |

| 11 January 2020 | First death The municipal health commissioner from Wuhan announces the first death caused by the coronavirus. A 61-year-old man passed away due to respiratory insufficiency. |

| 21 January 2020 | First reported case in the United States Washington authorities confirm their first COVID-19 patient, a 30-year-old man, who stays under observation. Days before, Thailand and Japan also announced their first cases. |

| 30 January 2020 | The World Health Organization declares a health emergency Hours after the announcement of the first cases where transmission between infected humans outside of China was confirmed, the WHO declares the virus outbreak to be a public health emergency of international concern. At this point, there are already 7800 confirmed cases in 20 countries around the world. |

| 4 February 2020 | The virus reaches cruise ships The Japan health ministry states that 10 people on board a cruise ship are confirmed to be positive for coronavirus. A total of 3711 passengers are put in quarantine for over 2 weeks. Days later, another 700 people get infected. |

| 11 February 2020 | Virus name changed to COVID-19 and over 1000 deaths are registered The International Committee on Taxonomy of Viruses announces the new name for the present coronavirus will be severe acute respiratory syndrome coronavirus type 2 (SARS-CoV-2), which was chosen since it is genetically related to the SARS outbreak in 2003. The WHO director Dr Tedros Adhanom announces the new virus name will be COVID-19. |

| 14 February 2020 | Africa’s first cases A case presents in Egypt, according to given information from authorities in the country, representing the first confirmed case within the African continent. |

| 14 February 2020 | The crisis in Italy starts In Europe, to prevent a major virus outbreak, several towns and cities in Italy enter lockdown. Circulation restrictions affect 100,000 people. |

| 25 February 2020 | First Latin American case The Brazilian health ministry confirms its first infected person. A 60-year-old man living in Sao Paulo who, due to work matters, had to travel to Italy. Days later, the virus spreads to Mexico, Ecuador, and Argentina, amongst other Latin American countries. |

| 3 March 2020 | First COVID-19 case in Chile Confirmed in Talca. A 33-year-old doctor who had travelled to Southeast Asia; the ministry points out that he will quarantine at his home address under epidemiological surveillance. |

| 7 March 2020 | Infection cases skyrocket Worldwide COVID-19 cases exceed 100,000 and deaths above 3400. The five countries with the most confirmed cases are China, South Korea, Iran, Italy, and Japan. |

| 11 March 2020 | Pandemic is declared The World Health Organization officially declares the COVID-19 outbreak as a pandemic. In response, President Donald Trump announces travel restrictions from Europe to the United States. |

| 14 March 2020 | Chile enters Stage 3 The lack of infection traceability leads the ministry to proceed into the third stage of the pandemic, including the cancellation of large events for over 500 people, while day-to-day activities are still available, such as shopping malls. Additionally, mandatory quarantine is applied to travelers coming from the peak countries, including Japan, China, Korea, France, Germany, Spain, and Italy. |

| 15 March 2020 | Schools get shut down and other actions are taken After officially entering the third stage, the government restricts entry to elderly homes and also proposes a law to review prisoners’ situations to avoid the spread of infection inside jails; quarantine is declared inside SENAME homes (National Service for Children), sanitary customs are established at all borders, and cruise ship entry to the country is prohibited. One of the most weighted and controversial guidelines was to suspend kindergarten for two-week periods, as well as private and public schools. |

| 16 March 2020 | Stage 4 is declared and borders close all over the country After registering 155 confirmed cases, the government initiates stage 4 of lockdown and closes sea, land, and air borders all along Chile effective from March 18. This resolution was considered after other countries took the same action, including Peru and Argentina, the neighboring countries. |

| 21 March 2020 | First death in Chile An 82-year-old woman living in the Renca commune becomes the first fatality of the virus in Chile. According to information provided by the health minister, Jaime Mañalich, the woman suffered from multiple pathologies and physically collapsed, which explains the compassionate management. |

| 22 March 2020 | Curfew in Chile With over 600 active COVID-19 cases, the government orders restrictions for free circulation from 22:00 until 05:00 in the morning the following day. Chileans can only leave their homes with an appropriate permit. |

| March 2020 | Several sectors declare quarantine In order to flatten the infection curve, authorities enforce a total lockdown in the following communes: Independencia, Las Condes, Lo Barnechea, Vitacura, Ñuñoa, Providencia, and Santiago. Weeks after, several other communes join the quarantine. |

| 30 March 2020 | Death records in Italy By this date, the country has already surpassed 10,000 registered deaths. In Spain, the number of fatal victims surpasses 7300. Lockdowns across Europe continue. |

| 2 April 2020 | Over one million infected COVID-19 has already infected over a million people worldwide and has caused 54,000 deaths to this date. Experts argue that the only way to stop the spread of the virus is to socially distance. |

| 19 April 2020 | Chile’s new normal Through nationwide broadcast, President Sebastian Piñera makes a call to reactivate the economy and for the public workforce to gradually return to face-to-face work. |

| 23 April 2020 | Education Ministry suspends going back to school The Education Minister, Raul Figueroa, announces that a date for going back to school is impossible to nail down due to COVID-19. Face-to-face classes become suspended until sanitary conditions allow a gradual return. |

| 29 April 2020 | First Chilean sanitary officer dead Government authorities regret the death of Lorena Duran, administrative from Cesfam Lastarria in the region La Araucania, due to the virus; she was the first official within the health system to pass away. |

| 2 May 2020 | The worst day to date in Chile Almost 1500 newly infected people are registered along with 13 deaths in just a day. This figure was confirmed by the health ministry who declared the strongest outbreak. Among the dead, there is another health officer. |

| 5 May 2020 | More than twenty thousand active cases in Chile Following the last official report launched by the health ministry on Tuesday, 1373 new COVID-19 cases are confirmed, of which 56 are asymptomatic, and the country reaches 22,016 cases. |

| Industry | Average | Median | Variance | Standard Deviation | Skewness | Kurtosis |

|---|---|---|---|---|---|---|

| Banking | −0.26% | −0.12% | 0.0005 | 0.02 | −0.75 * | 9.79 ** |

| Commodities | −0.08% | −0.22% | 0.0008 | 0.03 | −1.48 * | 10.46 ** |

| Const. & real estate | −0.25% | −0.30% | 0.0008 | 0.03 | −0.46 * | 9.00 ** |

| Consumption | −0.13% | −0.10% | 0.0003 | 0.02 | −1.06 * | 6.27 ** |

| Holding | −0.25% | −0.05% | 0.0005 | 0.02 | −0.45 * | 13.26 ** |

| Industrial | −0.24% | −0.05% | 0.0003 | 0.02 | −3.69 * | 33.39 ** |

| Retail | −0.32% | −0.20% | 0.0008 | 0.03 | −1.23 * | 13.73 ** |

| IT | −0.28% | −0.26% | 0.0008 | 0.03 | −0.56 * | 7.45 ** |

| Communication | −0.14% | −0.07% | 0.0010 | 0.03 | −0.38 * | 4.92 ** |

| Air travel | −0.70% | −0.16% | 0.0066 | 0.08 | −3.57 * | 27.17 ** |

| Utilities | −0.11% | −0.09% | 0.0004 | 0.02 | −1.41 * | 13.80 ** |

| Normality Tests | ||||||

|---|---|---|---|---|---|---|

| Industry | Kolmogorov-Smirnov ** | Shapiro-Wilk | ||||

| Statistical | gl | Sig. | Statistical | gl | Sig. | |

| Banking | 0.149 | 228.000 | 0.000 * | 0.843 | 228.000 | 0.000 * |

| Commodities | 0.086 | 228.000 | 0.000 * | 0.876 | 228.000 | 0.000 * |

| Const. & real estate | 0.122 | 228.000 | 0.000 * | 0.866 | 228.000 | 0.000 * |

| Consumption | 0.132 | 228.000 | 0.000 * | 0.903 | 228.000 | 0.000 * |

| Holding | 0.131 | 228.000 | 0.000 * | 0.826 | 228.000 | 0.000 * |

| Industrial | 0.165 | 228.000 | 0.000 * | 0.717 | 228.000 | 0.000 * |

| Retail | 0.143 | 228.000 | 0.000 * | 0.808 | 228.000 | 0.000 * |

| IT | 0.095 | 228.000 | 0.000 * | 0.912 | 228.000 | 0.000 * |

| Communication | 0.084 | 228.000 | 0.001 * | 0.937 | 228.000 | 0.000 * |

| Air travel | 0.218 | 228.000 | 0.000 * | 0.589 | 228.000 | 0.000 * |

| Utilities | 0.145 | 228.000 | 0.000 * | 0.811 | 228.000 | 0.000 * |

| Method | Day | Z | p-Value | Day | Z | p-Value |

|---|---|---|---|---|---|---|

| MRMA | Day −10 | −1.29 * | 0.20 ** | Day 1 | 0.49 * | 0.62 ** |

| MRMA | Day −9 | −0.04 * | 0.96 ** | Day 2 | 0.58 * | 0.56 ** |

| MRMA | Day −8 | −0.40 * | 0.69 ** | Day 3 | 0.93 * | 0.35 ** |

| MRMA | Day −7 | 0.93 * | 0.35 ** | Day 4 | 1.29 * | 0.20 ** |

| MRMA | Day −6 | −0.04 * | 0.96 ** | Day 5 | 0.13 * | 0.89 ** |

| MRMA | Day −5 | −1.64 * | 0.10 ** | Day 6 | −0.04 * | 0.96 ** |

| MRMA | Day −4 | −0.22 * | 0.82 ** | Day 7 | 0.22 * | 0.82 ** |

| MRMA | Day −3 | −1.56 * | 0.12 ** | Day 8 | −1.73 * | 0.08 ** |

| MRMA | Day −2 | 0.22 * | 0.82 ** | Day 9 | −1.56 * | 0.12 ** |

| MRMA | Day −1 | −1.73 * | 0.08 ** | Day 10 | −2.00 * | 0.05 ** |

| MRMA | Day 0 | −0.49 * | 0.62 ** |

| Method | Day | Z | p-Value | Day | Z | p-Value |

|---|---|---|---|---|---|---|

| MRPA | Day −10 | −1.11 * | 0.27 ** | Day 1 | 0.67 * | 0.50 ** |

| MRPA | Day −9 | 0.49 * | 0.62 ** | Day 2 | 0.58 * | 0.56 ** |

| MRPA | Day −8 | 0.04 * | 0.96 ** | Day 3 | 1.29 * | 0.20 ** |

| MRPA | Day −7 | 1.02 * | 0.31 ** | Day 4 | 1.64 * | 0.10 ** |

| MRPA | Day −6 | 0.31 * | 0.76 ** | Day 5 | 0.84 * | 0.40 ** |

| MRPA | Day −5 | −1.38 * | 0.17 ** | Day 6 | 0.04 * | 0.96 ** |

| MRPA | Day −4 | −0.13 * | 0.89 ** | Day 7 | 1.38 * | 0.17 ** |

| MRPA | Day −3 | −2.36 * | 0.02 ** | Day 8 | −1.64 * | 0.10 ** |

| MRPA | Day −2 | 0.49 * | 0.62 ** | Day 9 | −0.84 * | 0.40 ** |

| MRPA | Day −1 | −1.82 * | 0.07 ** | Day 10 | −2.00 * | 0.05 ** |

| MRPA | Day 0 | 0.04 * | 0.96 ** |

| Method | Day | Z | p-Value | Day | Z | p-Value |

|---|---|---|---|---|---|---|

| MM | Day −10 | −0.04 * | 0.96 ** | Day 1 | −2.89 | 0.00 |

| MM | Day −9 | 0.49 * | 0.62 ** | Day 2 | −2.89 | 0.00 |

| MM | Day −8 | −2.89 | 0.00 | Day 3 | 2.53 | 0.01 |

| MM | Day −7 | −2.18 | 0.03 | Day 4 | −2.71 | 0.01 |

| MM | Day −6 | −2.89 | 0.00 | Day 5 | −2.89 | 0.00 |

| MM | Day −5 | −2.71 | 0.01 | Day 6 | 1.64 * | 0.10 ** |

| MM | Day −4 | −2.89 | 0.00 | Day 7 | −2.89 | 0.00 |

| MM | Day −3 | 2.80 | 0.01 | Day 8 | −1.02 * | 0.31 ** |

| MM | Day −2 | 0.67 * | 0.50 ** | Day 9 | −2.89 | 0.00 |

| MM | Day −1 | 2.36 | 0.02 | Day 10 | 2.62 | 0.01 |

| MM | Day 0 | −2.80 | 0.01 |

| Method MRPA | Method MRMA | Method MM | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Median | Median | Median | ||||||||||

| Industry | pre (10 Days) | Post (10 Days) | t-Value | p-Value | pre (10 Days) | Post (10 Days) | t-Value | p-Value | pre (10 Days) | Post (10 Days) | t-Value | p-Value |

| Banking | 0.004 | 0.008 | −1.00 | 0.22 ** | 0.002 | 0.005 | −0.60 | 0.22 ** | 0.001 | −0.024 * | 1.31 | 0.22 ** |

| Commodities | −0.004 * | −0.042 * | 1.83 | 0.34 ** | −0.004 * | −0.042 * | 1.83 | 0.56 ** | −0.004 * | −0.042 * | 1.83 | 0.12 ** |

| Const. & real estate | −0.002 * | 0.000 * | −0.14 | 0.89 ** | −0.005 * | −0.012 * | 0.68 | 0.51 ** | −0.005 * | −0.041 * | 1.66 | 0.13 ** |

| Consumption | −0.001 * | −0.002 * | 0.29 | 0.78 ** | −0.001 * | 0.009 | −1.31 | 0.22 ** | −0.003 * | −0.021 * | 1.44 | 0.18 ** |

| Holding | 0.001 | −0.003 * | 0.47 | 0.65 ** | 0.000 | −0.008 * | 0.88 | 0.40 ** | −0.002 * | −0.038 * | 2.15 | 0.06 ** |

| Industrial | −0.005 * | −0.015 * | 0.97 | 0.36 ** | −0.004 * | 0.000 | −0.44 | 0.67 ** | −0.006 * | −0.030 * | 1.42 | 0.19 ** |

| Retail | 0.001 | −0.013 * | 1.33 | 0.22 ** | −0.001 * | −0.021 * | 1.85 | 0.10 ** | −0.002 * | −0.050 * | 2.07 | 0.07 ** |

| IT | −0.001 | 0.002 | 1.83 | 0.64 ** | −0.003 * | −0.004 * | 1.83 | 0.90 ** | −0.003 * | −0.032 * | 1.35 | 0.21 ** |

| Communication | −0.004 | 0.004 | −0.71 | 0.50 ** | −0.006 * | −0.007 * | 0.04 | 0.97 ** | −0.007 * | −0.036 * | 1.90 | 0.09 ** |

| Air travel | −0.016 | −0.086 * | 1.47 | 0.18 ** | −0.015 * | −0.082 * | 1.46 | 0.18 ** | −0.019 * | −0.114 * | 1.53 | 0.16 ** |

| Utilities | −0.004 | 0.009 | −1.70 | 0.12 ** | −0.003 * | 0.011 | −1.85 | 0.10 ** | −0.006 * | −0.019 * | 0.85 | 0.42 ** |

| Industry | Banking | Commodities | Const. & Real Estate | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Method | MRPA | MRMA | MM | MRPA | MRMA | MM | MRPA | MRMA | MM |

| Return (CAR) | |||||||||

| Event | −0.8% | −0.1% | 0.1% | −1.9% | −0.9% | −0.7% | −1.4% | −0.7% | −0.2% |

| Pre−Event | 0.7% | 1.8% | 3.5% | −3.6% | −0.8% | −0.2% | −5.3% | −4.6% | −1.8% |

| Post Event | −24.4% | 4.7% | 8.5% | −41.7% | −10.9% | −2.7% | −40.6% | −11.8% | −0.2% |

| Total | −24.5% | 6.4% | 12.1% | −47.2% | −12.6% | −3.6% | −47.3% | −17.1% | −2.3% |

| p-value (CAR) | |||||||||

| Event | 0.59 | 0.90 | 0.85 | 0.35 | 0.40 | 0.51 | 0.51 | 0.61 | 0.87 |

| Pre-Event | 0.88 | 0.43 | 0.11 | 0.57 | 0.82 | 0.94 | 0.44 | 0.28 | 0.65 |

| Post Event | 0.00 * | 0.03 * | 0.00 * | 0.00 * | 0.00 * | 0.43 | 0.00 * | 0.01 * | 0.96 |

| Total | 0.00 * | 0.05 * | 0.00 * | 0.00 * | 0.02 * | 0.46 | 0.00 * | 0.01 * | 0.70 |

| Industry | Consumption | Holding | Industrial | ||||||

| Method | MRPA | MRMA | MM | MRPA | MRMA | MM | MRPA | MRMA | MM |

| Return (CAR) | |||||||||

| Event | −0.6% | 0.3% | 0.0% | −2.4% | −1.6% | −1.4% | −0.2% | 0.6% | 0.2% |

| Pre-Event | −2.6% | −0.5% | −1.0% | −1.6% | −0.3% | 1.4% | −6.0% | −4.1% | −4.7% |

| Post Event | −21.3% | 8.9% | −2.4% | −37.7% | −8.3% | −3.4% | −29.9% | 0.1% | −14.8% |

| Total | −24.5% | 8.6% | −3.3% | −41.7% | −10.3% | −3.4% | −36.1% | −3.4% | −19.3% |

| p-value (CAR) | |||||||||

| Event | 0.61 | 0.74 | 1.00 | 0.19 | 0.15 | 0.21 | 0.79 | 0.53 | 0.76 |

| Pre-Event | 0.45 | 0.85 | 0.67 | 0.79 | 0.93 | 0.70 | 0.04 * | 0.17 | 0.03 * |

| Post Event | 0.00 * | 0.00 * | 0.31 | 0.00 * | 0.02 * | 0.34 | 0.00 * | 0.97 | 0.00 * |

| Total | 0.00 * | 0.03 * | 0.32 | 0.00 * | 0.05 * | 0.51 | 0.00 * | 0.43 | 0.00 * |

| Industry | Retail | IT | Communication | ||||||

| Method | MRPA | MRMA | MM | MRPA | MRMA | MM | MRPA | MRMA | MM |

| Return (CAR) | |||||||||

| Event | −0.8% | −0.1% | 0.3% | −0.6% | 0.1% | 0.4% | −0.3% | 0.5% | 0.9% |

| Pre-Event | −2.1% | −1.2% | 1.0% | −3.5% | −3.0% | −0.5% | −7.4% | −6.3% | −4.1% |

| Post Event | −50.0% | −21.0% | −12.7% | −32.4% | −3.8% | 2.4% | −35.8% | −6.6% | 3.8% |

| Total | −53.0% | −22.3% | −11.5% | −36.5% | −6.8% | 2.3% | −43.6% | −12.5% | 0.6% |

| p-value (CAR) | |||||||||

| Event | 0.65 | 0.91 | 0.78 | 0.77 | 0.95 | 0.76 | 0.90 | 0.80 | 0.61 |

| Pre-Event | 0.71 | 0.68 | 0.72 | 0.59 | 0.50 | 0.90 | 0.33 | 0.25 | 0.45 |

| Post Event | 0.00 * | 0.00 * | 0.00 * | 0.00 * | 0.39 | 0.59 | 0.00 * | 0.23 | 0.49 |

| Total | 0.00 * | 0.00 * | 0.01 * | 0.00 * | 0.30 | 0.72 | 0.00 * | 0.12 | 0.94 |

| Industry | Air Travel | Utilities | |||||||

| Method | MRPA | MRMA | MM | MRPA | MRMA | MM | |||

| Return (CAR) | |||||||||

| Event | −2.0% | −1.0% | −1.2% | 0.2% | 1.1% | 1.0% | |||

| Pre-Event | −18.6% | −14.9% | −16.3% | −5.9% | −3.3% | −3.5% | |||

| Post Event | −113.7% | −81.9% | −86.2% | −19.3% | 11.4% | 9.1% | |||

| Total | −134.3% | −97.8% | −103.6% | −25.0% | 9.2% | 6.6% | |||

| p-value (CAR) | |||||||||

| Event | 0.49 | 0.71 | 0.65 | 0.89 | 0.08 | 0.09 | |||

| Pre-Event | 0.04 * | 0.07 | 0.05 | 0.17 | 0.09 | 0.07 | |||

| Post Event | 0.00 * | 0.00 * | 0.00 * | 0.00 * | 0.00 * | 0.00 * | |||

| Total | 0.00 * | 0.00 * | 0.00 * | 0.00 * | 0.00 * | 0.02 * | |||

| Industry | Banking | Commodities | Const. & Real Estate | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Method | MRPA | MRMA | MM | MRPA | MRMA | MM | MRPA | MRMA | MM |

| Return (BHAR) | |||||||||

| Event | −0.8% | −0.1% | 0.1% | −1.9% | −0.9% | −0.7% | −1.4% | −0.7% | −0.2% |

| Pre-Event | 0.4% | 1.7% | 3.5% | −3.8% | −0.8% | −0.3% | −5.3% | −4.6% | −2.0% |

| Post Event | −23.5% | 4.8% | 8.7% | −36.6% | −10.5% | −2.7% | −35.1% | −11.8% | −1.3% |

| Total | −23.8% | 6.5% | 12.7% | −40.2% | −12.0% | −3.7% | −39.5% | −16.4% | −3.4% |

| p-value (BHAR) | |||||||||

| Event | 0.59 | 0.90 | 0.85 | 0.35 | 0.40 | 0.51 | 0.51 | 0.61 | 0.87 |

| Pre-Event | 0.93 | 0.43 | 0.11 | 0.54 | 0.82 | 0.94 | 0.43 | 0.28 | 0.62 |

| Post Event | 0.00 * | 0.03 * | 0.00 * | 0.00 * | 0.00 * | 0.42 | 0.00 * | 0.01 * | 0.75 |

| Total | 0.00 * | 0.04 * | 0.00 * | 0.00 * | 0.02 * | 0.45 | 0.00 * | 0.01 * | 0.55 |

| Industry | Consumption | Holding | Industrial | ||||||

| Method | MRPA | MRMA | MM | MRPA | MRMA | MM | MRPA | MRMA | MM |

| Return (BHAR) | |||||||||

| Event | −0.6% | 0.3% | 0.0% | −2.4% | −1.6% | −1.4% | −0.2% | 0.6% | 0.2% |

| Pre-Event | −2.6% | −0.6% | −1.0% | −1.7% | −0.4% | 1.2% | −5.9% | −4.1% | −4.6% |

| Post Event | −20.1% | 8.9% | −2.4% | −32.9% | −8.3% | −3.7% | −27.3% | −0.4% | −14.3% |

| Total | −22.6% | 8.6% | −3.4% | −35.6% | −10.2% | −3.9% | −31.7% | −3.9% | −18.1% |

| p-value (BHAR) | |||||||||

| Event | 0.61 | 0.74 | 1.00 | 0.19 | 0.15 | 0.21 | 0.79 | 0.53 | 0.76 |

| Pre-Event | 0.44 | 0.84 | 0.66 | 0.77 | 0.90 | 0.73 | 0.05 * | 0.17 | 0.03 * |

| Post Event | 0.00 * | 0.00 * | 0.30 | 0.00 * | 0.02 * | 0.30 | 0.00 * | 0.90 | 0.00 * |

| Total | 0.00 * | 0.03 * | 0.31 | 0.00 * | 0.05 | 0.45 | 0.00 * | 0.36 | 0.00 * |

| Industry | Retail | IT | Communication | ||||||

| Method | MRPA | MRMA | MM | MRPA | MRMA | MM | MRPA | MRMA | MM |

| Return (BHAR) | |||||||||

| Event | −0.8% | −0.1% | 0.3% | −0.6% | 0.1% | 0.4% | −0.3% | 0.5% | 0.9% |

| Pre-Event | −2.3% | −1.3% | 1.0% | −3.5% | −3.1% | −0.7% | −7.7% | −6.3% | −4.2% |

| Post Event | −41.7% | −19.5% | −12.5% | −29.7% | −4.2% | 1.9% | −31.9% | −6.7% | 3.3% |

| Total | −43.5% | −20.6% | −11.4% | −32.5% | −7.1% | 1.6% | −37.3% | −12.2% | −0.2% |

| p-value (BHAR) | |||||||||

| Event | 0.65 | 0.91 | 0.78 | 0.77 | 0.95 | 0.76 | 0.90 | 0.80 | 0.61 |

| Pre-Event | 0.69 | 0.68 | 0.73 | 0.59 | 0.48 | 0.87 | 0.31 | 0.25 | 0.44 |

| Post Event | 0.00 * | 0.00 * | 0.00 * | 0.00 * | 0.35 | 0.66 | 0.00 * | 0.23 | 0.54 |

| Total | 0.00 * | 0.00 * | 0.01 * | 0.00 * | 0.28 | 0.80 | 0.00 * | 0.13 | 0.98 |

| Industry | Air Travel | Utilities | |||||||

| Method | MRPA | MRMA | MM | MRPA | MRMA | MM | |||

| Return (BHAR) | |||||||||

| Event | −2.0% | −1.0% | −1.2% | 0.2% | 1.1% | 1.0% | |||

| Pre-Event | −17.6% | −14.1% | −15.3% | −5.9% | −3.3% | −3.5% | |||

| Post Event | −78.3% | −63.5% | −65.6% | −19.1% | 11.9% | 9.3% | |||

| Total | −82.4% | −68.9% | −71.2% | −23.7% | 9.4% | 6.6% | |||

| p-value (BHAR) | |||||||||

| Event | 0.49 | 0.71 | 0.65 | 0.89 | 0.08 | 0.09 | |||

| Pre-Event | 0.05 | 0.09 | 0.07 | 0.17 | 0.09 | 0.07 | |||

| Post Event | 0.00 * | 0.00 * | 0.00 * | 0.00 * | 0.00 * | 0.00 * | |||

| Total | 0.00 * | 0.00 * | 0.00 * | 0.00 * | 0.00 * | 0.02 * | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

González, P.A.; Gallizo, J.L. Impact of COVID-19 on the Stock Market by Industrial Sector in Chile: An Adverse Overreaction. J. Risk Financial Manag. 2021, 14, 548. https://doi.org/10.3390/jrfm14110548

González PA, Gallizo JL. Impact of COVID-19 on the Stock Market by Industrial Sector in Chile: An Adverse Overreaction. Journal of Risk and Financial Management. 2021; 14(11):548. https://doi.org/10.3390/jrfm14110548

Chicago/Turabian StyleGonzález, Pedro Antonio, and José Luis Gallizo. 2021. "Impact of COVID-19 on the Stock Market by Industrial Sector in Chile: An Adverse Overreaction" Journal of Risk and Financial Management 14, no. 11: 548. https://doi.org/10.3390/jrfm14110548

APA StyleGonzález, P. A., & Gallizo, J. L. (2021). Impact of COVID-19 on the Stock Market by Industrial Sector in Chile: An Adverse Overreaction. Journal of Risk and Financial Management, 14(11), 548. https://doi.org/10.3390/jrfm14110548