1. Introduction

Many developing nations such as India, Brazil, Argentina, Indonesia and many south east Asian countries are vulnerable to external economic crisis due to over dependency on foreign soil for their capital need (

De 2020). It has been seen that, when the major economies in the world trembles, the nations depending on the major economies start shattering. The world crisis has affected the major developing nations and its growing economy. Due to openness in the economy, India’s economy is susceptible to world economic crises. The Latin American debt crisis in 2002, the great depression in 2007 and the European crisis in 2010 have shown the devastating impact of world crises on the Indian economy. (

Srinivas 2011). The world has also seen many financial crises arising out of pandemicsandepidemics such as SARS, swine flu, H1N1 virus, COVID-19, etc. (

Bluedorn et al. 2020;

Peckham 2013). These world financial crises have negative effectsin the short term, and in some cases, this can extend to long-term unconstructive consequences (

Merle 2018). The financial crises in the globalised era are not just limited to the extent of the country of origin but also affect many countries connected with international support systems and international trade. The crises in one country lead to the crises with other dependent nations. Many a time, the Indian economy has shaken due to the devastation that happened in connected countries’trade and business. The fall of the economy in one country leads to withdrawal of capital provided by that country in the form of foreign direct investment (FDI) and foreign portfolio investment (FPI). Just not India but many developing nations in the subcontinent region and the south east Asian region are affected by the withdrawal of FDI and FPI due to world economic crises, in spite of having good domestic parameters (

Caycedo 2018).

India’s liberal foreign direct investment (FDI) and foreign portfolio investment (FPI) policies, similar to many other developing economies, have been proved as a gain for the economic growth for many years, but it has also made the Indian economy penetrable to external unforeseen situations. In recent years, big world economic crises such as the great crisis of the United States of America in 2008 (

Razack and Thimmaiah 2014), the Japan crisis in 2011 (

Lakshman 2011), the Euro debt crisis in 2011–2012 (

Mukherjee 2012) and the COVID-19 crisis in 2020 (

Ramakrishnan 2020) have shown the negative facet of open economic policies. Even if the fundamentals of the Indian economy were strong in some of these situations, the impact of global crises made it fall. Therefore, we need to be capital adequate from the domestic resources especially through domestic retail investors.

The participation of Indian domestic retailer investors, such as many other developing nations, is very discouraging for their domestic economy (

IBRD 2017). The contribution towards investment is less than 3% in India, which seems insignificant as compared to the United States of America (55%) (

Agrawal 2020). Only 40.8 million people in India have a dematerialisation of share (DEMAT) account in a population of more than 1.36 billion (

Sultana 2020). The Indian investors, investing in mutual funds and systematic investment plans relating to the equity market, hold up to only 2.37 and 85% of the total investors in mutual funds coming from top 30 cities of India, which shows that India’s financial system is just concentrating on the major cities and has failed significantly to significantly draw the attention of rural retail investors (

Nair 2020). The above statistics show how India’s financial intermediaries failed to encourage and understand the behaviour of Indian investors.

Domestic investments from domestic investors or the retail investors are very much important for filling the capital and financial need of any nation by utilising the disposable income from the public and depending less on the external financing from other countries.

Bakari (

2017) stated that domestic investments are very important for the economic development of any nation.

Bal et al. (

2016) also supported the fact that domestic investment lead to the growth of GDP, as it promotes capital formation. The increase in capital formation through the disposable income from domestic investment could be pathway for economic investment, and for this purpose, we need to encourage domestic investors (

Pegkas and Tsamadias 2016). Therefore, to encourage more and more domestic-based investment, we need to encourage the domestic individual investors. So, it has been essential to study the characteristics of domestic investors and their intention to invest.

Investments are subjected to a knowledge-driven scenario. Brain processing through various forces is needed for understanding, imitating and investing in different investment platforms. Therefore, the different sources by which the mental processing could be done are needed to be studied for a better understanding of the investment mechanisms of the investors. The investment dynamics are also driven by the risk-tolerance character of the investors. On stimulating the risk-taking potential, we can aggravate the investors to go for purchasing the investment. Therefore, we also need to study the factors affecting the risk-taking potential of the investors along with knowing their present risk-taking ability. Therefore, this paper has been focused to find out the different dimension of cognitions, which can help to build decision-making potential for investment in the domestic capital market as different dimensions of cognition are different potential sources to drive one’s attitude and intent. Along with cognition, this study also concentrated on finding out different traits that can be inculcated in the investors, so that they can take firmand better financial product investment decisions.

1.1. Literature Review

Human psychology plays an important part in the everyday life of human beings in taking various decisions of life. Investment being a matter of necessity in today’s lifestyle, there is a concern about an investor’s psychology with regard to what drives him for investment. Investors’ informative view point and the processing of information help make the investment decision and develop the risk-taking capacities. Therefore, in this literature review, we have concentrated on the cognitive factors relating to an investor’s psychology and the risk-bearing capabilities of the investors.

1.1.1. Risk-Taking Abilities

Risk-taking capabilities have been a major aspect when it comes to investing your hard-earned money in the scenario of return uncertainties. Risk-taking aptitude is different from investor to investor. Generally, the investors are categorised into three on the basis of their risk-taking abilities (

Harris and Wu 2014). They can be risk averse, risk neutral and risk seeking. The risk averse investors always ceases to take any risk and avoid risk to the maximum extent. The risk neutral investors are basically those investors who intend to take limited risk in the investment and do not extend their current investment to a greater number of years. The risk seekers are the investorswhoaim to obtain more return out of a risky investment and continue to do so for a more extended time (

Dev 2014). Financial risk tolerance is the maximum amount of risk or uncertainty that someone is willing to bear or accept, while making a financial decision, considering the economic and social factors relating an individual (

Grable 2000). Risk tolerance is measured by five factors such as traditional risk factor, reflective risk factor, allocation risk factor, capacity risk factor and knowledge risk factor.

This ability of taking risk and risk averse thoughts creates a likelihood towards investment or creates resiliency in the mind of the investors to make an investment decision (

Feldman and Lepori 2016). On the other hand,

Dickason and Ferreira (

2018) have found that the perceived environmental security relating risky investment affects their decision-making process and the behaviour of risk aversion comes into play.

Saurabh and Nandan (

2018) supported his arguments and stated that the financial risk attitude affects the financial satisfaction or else leads to dissatisfaction towards an investment.

Broihanne et al. (

2014) also found that the risk perception and the risk-taking behaviour amplify or reduce the tenacity of investment decision.

Factors Affecting Risk Tolerance

There are many elements affecting the risk-tolerance behaviour of the investors and their risk-bearing capacity. These factors are the emotional intelligence and locus of control, which have a positive effect on financial risk taking.

Aydemir and Aren (

2017) also stated the fact that the emotional intellect among the investor is the major factor behind the risk-tolerance conduct of the individual.

Sweet (

2013) explained that income and education have an individual impact and effect in combination.

Anderson (

2016) also showed that factors such as family profile and financial literacy impact financial risk at the individual level.

Mohan and Singh (

2017) supported the information that financial risk tolerance enhances with an increase in the level of education of investors.

Anbar and Eker (

2010) and

Chattopadhyay and Dasgupta (

2015) have shown from their studies that married persons are more risk unenthusiastic than unmarried persons. Risk-tolerance capacity fluctuates from male and female and personality of conscientiousness (

Wong and Carducci 2013). To support his arguments,

Saurabh and Nandan (

2018) assert that the internal consistencies and satisfactory reliabilities are able to construct and enhance the risk handling and increase risk-tolerance level.

Reddy and Mahapatra (

2017) explained from their study that personal fiscal knowledge and the demographic variables such as age and educational level affects the risk-tolerance level.

Wasiuzzaman and Edalat (

2016) found from his learning that social network use can convey the information and relevant data concerned with the investment, which will increase the risk-tolerance level.

Effect of Risk-Absorption Capacity (RA) on Level/Degree of Interest in Investment (LII)

Risk and return have two equivalent aspects of investment theory. The higherrisk investment would result in more return. The risk-tolerance ability has been the important constraint behind the investment decision.

Khan (

2017) found that people with more financial risk-tolerance behaviour possess more interest in investment.

Corter and Chen (

2006) explain from their study that the investor with the larger risk-handling capability emerges to be the most enthusiastic for investment. Risk-absorption capacity (RA) reflects the risk-tolerance nature of the investors; those who are investing for a greater duration of time, repeating such an investment, suggesting investment plans with others and waiting for the market to rise rather than selling in the falling market. This risk-absorption capacity induces the investor to take calculative and more risk in investments. Supporting the finding

Kannadhasan (

2015) also found that the investor with the greater risk-tolerance behaviour is likely to invest more in risky assets. Risk perception holdsa lot of sway in the investment decision (

Sindhu and Kumar 2014). The risk associated with investment frequently makes the investor use their cognitive ability to make the decision (

Shafi and Fatima 2016).

1.1.2. Cognition

Being one of the constituents among the tri-component of attitude formation, cognition has taken a prior component in developing purchase attitudes towards investment among the investor. Investment is a subject matter of examination and understanding, so cognition plays a vital role. Starting from resolving the matter of investors to a confirmed investment decision, cognition is the distinguished focus objective. It provides a better psychological processing environment for understanding relating to the financial product, which ultimately helps the investors to make an improved investment decision. The cognition is non-emotional, emotional and social. The different magnitude of cognition affects the attitude of investors in the direction of investment individually, and also, the combined effect brings a greater positivity towards investment.

Niznikiewicz (

2013) explained that the dimensions of cognition can be cold cognition (non-emotional), hot cognition (emotional), social cognition (current social environment) and meta cognition (learning process).

1.1.3. Cold Cognition (CC)

Cognition is the mental process involving gaining knowledge through thinking knowing, remembering, reviewing and problem solving (

Cherry 2019). This knowing process could engage emotional sources of information and can be non-emotional as well. Cold cognition involves the mental process in which memories, working memory, attention level, sensory processing, phonology and the non-emotional semantics play a key role by which a person acquires knowledge about a particular subject (

Sahakian 2017). Further (

Bhushan 2014;

Dhingra et al. 2017), the information relating to investment guidesthe investors’ awareness through continuous and conscious education, which helps in decision making. In addition of the above facts, (

Mane 2016;

Saravanakumar et al. 2011) we must also give weight to the news and awareness about liquidity, diversification and the fine-framed regulation relating to investment scenarios, which ultimately have an impact on their decision. An investor uses their intelligence to evaluate the current and past performance of the investment (

Jagongo and Mutswenje 2014). The analysis of macro-economic factors and risk and return factors affect the investment propensity (

Shinde and Zanvar 2014).

1.1.4. Hot Cognition (HC)

Investors, being social animals, are influenced by their emotional surroundings. Their activities and decisions reflect the emotional behaviour around them. “Hot cognition” is said to be the emotional way of psychological processing. It is developed through emotional processing, emotional semantics, emotional prosody, conversing intentions of self and understanding emotions and empathy (

Niznikiewicz 2013). Many investors pursue information or follow the knowledge of related people or sources with whom they are emotionally associated.

Blackwell et al. (

2011) and

Cabosky (

2016) established from their study that hot cognition is the emotional-based cognition through emotional resilience, and social interaction influences the speed and accuracy of the decision of the people.

Redlawsk (

2002) holds the facts and concluded that hot cognition conveys an emotional belongingness in decision making and affects the degree of potency of the decision. Emotional affection is from the family and peer group, which influences their purchasing intention (

Kshetri and Jha 2016;

Massa 2003).

1.1.5. Social Cognition (SC)

Social cognition is the mental process by which one person perceives, thinks and attends to another person in our social world (

Cherry 2019;

Currás-Pérez et al. 2013). Social cognition controls social interaction, and social interaction helps a person or affects decision making.

Fiske (

1993) and

Yuksel et al. (

2016) found that society or an acquaintance can guide investors to a general agreement or consensus. This shows that the known information and known people leads to social cognition, which helps to seize a relatively confirmatory decision. Two studies (

Ferreira et al. 2014;

Ickes et al. 1990) also added that if the intensity of colleague and social cognition is raised (

Sahoo et al. 2020), then the degree of acceptability of the theory of those within the social environment will be more (

Bounkhong 2017;

He et al. 2015). Social media are the platform for information creation and circulation regarding investment patterns (

Islamoğlu et al. 2015;

Pang and Lee 2008). Facebook, Twitter, etc., havebeen efficient in the buying decisions among different age groups especially in millennials (

Boateng and Okoe 2015;

Duffett 2015). Often social media creates brand awareness, which ultimately helps in purchasing decisions (

Bruhn et al. 2012;

Cocosila and Igonor 2015).

1.1.6. Meta Cognition (MC)

Meta cognition is the intellectual process originates from the person’s own learning. It develops the learning from their own thoughts. It starts with its own desire to find out and evaluate the strengths and weaknesses, preparing the strategies and learning from the action (

Spencer 2018). It is cognition developed through self-directed goals and experience. Meta cognition shapes the future-oriented decision that was previously experienced. (

Bennet et al. 2012;

Lee et al. 2012) stated that the person, experience or self-analysed learning and cognition assist them in analysing prospective situations and change their attitude to make a better decision.

Guo (

2012) and

Sukanya and Thimmarayappa (

2015) also found that the learners’ independent awareness of the mental processing ability to reflect, assess its actions and control its own cognitive process helps to make good strategies and could lead to a better decision.

Effect of Investors’ Cognition (IC) on Level/Degree of Interest in Investment (LII)

Pothos and Busemeyer (

2013) concluded from their study that the various dimensions of cognition become the rationality in decision making. The relevance of cognition and cognitive abilities will create a positive intention to invest.

Yang (

2015) explains that cognition or cognitive ability helps to change the dynamism of strategies and helps to implement the strategic transform. It leads to a change in the propensity of decision making and helps to make confirmed decisions.

Tidwell et al. (

2000) explained that there is necessitate for cognition in every decision made. The strength and weakness of the decision rely upon the relevance of cognition in a particular field. The different types of cognition support an individual to take a firmed purchase decision (

Akhter and Ahmed 2013;

Kim 2012).

1.2. Problem Statement

Human decisions relating to the purchase of any product depends on the psychological characteristics, which can be driven by many components such as the cognitive, conative and the affective components (

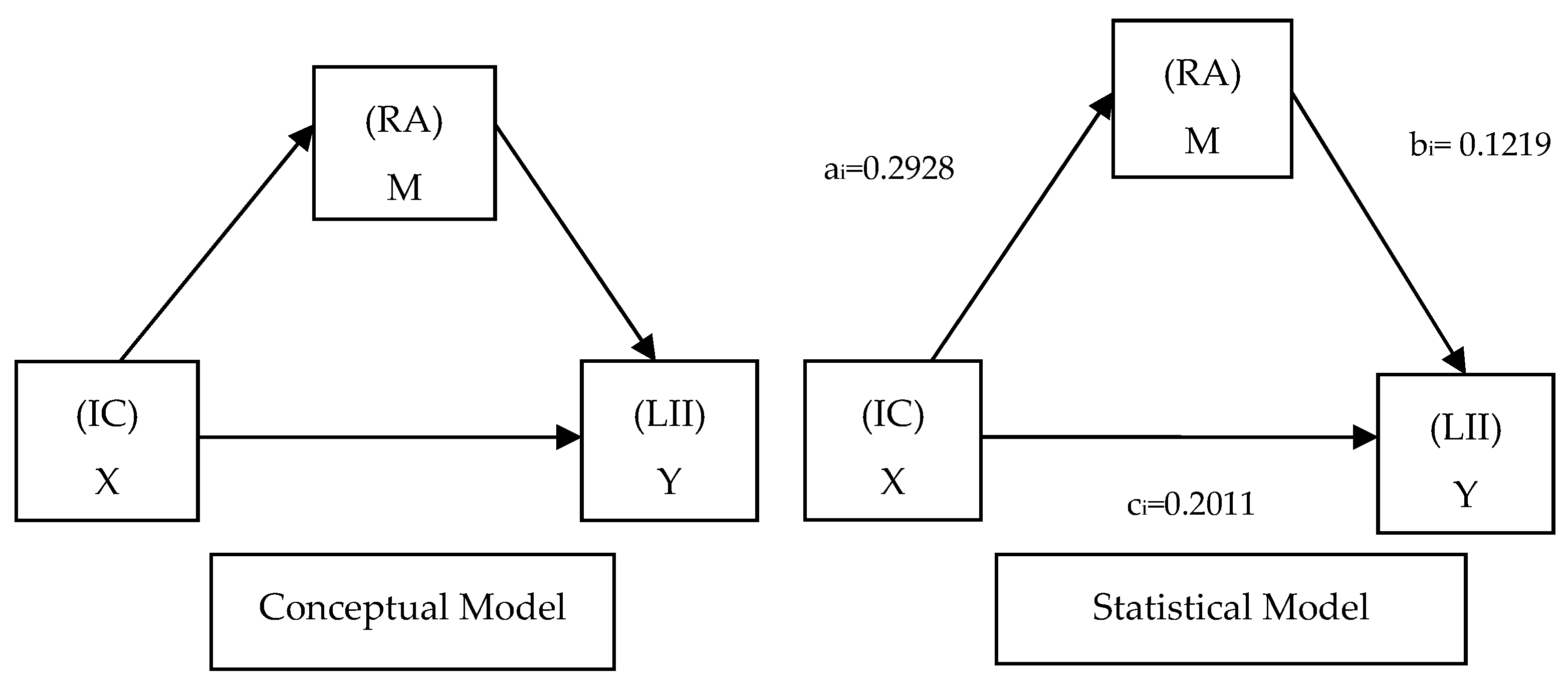

Wengrzyn 2013). However, the financial product is just like any other necessity product for the investors, which are determined by the psychological characteristics and attitude of the investor, but this character and attitude are mostly influenced by the mental processing or the cognitive element. As investments are subjected to risk of loss, the risk-taking ability of the investors also plays a major role in the purchase decision of the financial products. Cognition affects both the level of interest in the investors towards investment as well as developing the qualities of the investor having risk absorption. The development of this risk-absorption quality again leads to changes in the level of interest in investment. In this regard, the research question is “can risk-absorption potential among investors play a mediating role in the impact relationship of investors’ cognition on the level of interest in investment?”

1.3. Objective of the Study

To find the different dimension of investors’ cognition.

To explore different characteristics of the investor having risk absorption.

To analyse the direct impact of the dimension of investors’ cognition on the level of interest in investment.

To study the mediating effect of risk-absorption factors on the relationship between the investors’ cognition and the level of interest in investment.

1.4. Hypothesis of the Study

Hypothesis 1 (H1). There is a significant direct impact of the dimension of investors’ cognition on the level of interest in investment.

Hypothesis 2 (H2). There is a significant mediating effect of risk-absorption factors on the relationship between the investors’ cognition and the level of interest in investment.

1.5. Scope of the Study

The is based on knowing the cognition effect on both risk-tolerance capacity of the investors as well as helping in enhancing investors’ interest level towards financial products such as systematic investment plans (SIP) and mutual funds linked with the stock market. It can help the managers of a broking firm as well as asset management companies to set specific targets for investors and can form suitable strategies to develop their risk-taking ability and can also help in developing their information processing abilities relating to investment. A better informative possessed client is always been a long-term asset for these companies, as they tend to invest for a longer duration of time without panicking because of market fluctuation.

4. Discussion

The study focused on investors’ psychological behaviour with regard to investment scenarios. It was found from the study that investment decisions are always in a need of information processing abilities along with the intention of taking valuable risks for better return. The study found that the mental processing of information has different dimensions of information processing from various sources. They are hot cognition, cold cognition, social cognition and meta cognition. Along with that, the past investment experience and success leads to better knowledge processing capabilities, which indirectly resulted in better investment strategies. The studies found that the dimension of investors’ cognition along with risk-absorption character have a significant impact on the level of interest in investment. The study elaborated different ways of mental processing, which can be used by the financial product marketer to understand and provide relevant information as per the investors’ mental processing capabilities, so they can form an intent to invest in the domestic capital market through their sense of information processing.

The study also showed the characteristics of investors having risk absorption and found that the investor having risk absorption possesses five characteristics, which are risk seeking attitude, strategic investment planner, recurrence in investment, risk tolerance or tolerance behaviour and protracted or longer duration of investment. The study also found that the risk-absorption nature mediates the relationship of the investors’ cognition and level of interest in the investment. The study shows that the mediating impacts of investors’ cognition along with risk-absorption characteristics have a greater impact than the direct relationship between the investors’ cognition and level of interest in investment. The marketer can classify investors on the basis of risk-absorption capacity and could make strategies, which could motivate them to take a steady and firmed decision. The study can also help the mutual fund companies to formulate strategies to build the risk-absorption capacity through effective advertising and informative strategies.

The study, however, is limited to a state of one developing nation. Further study can be made in this regard in other developing nations to set policies in many countries to face and revive from any anticipated financial crisis.

4.1. Theoretical Contribution

Just like India, most of the South Asian countries face unsustainable capital inadequacy, as these countries have significantly failed to understand theirown investors, who are basically risk averse in nature. Clearly, the strategies made to bring about the trust of the investors on the domestic capital market have been futile. The study reflects sources that could change the investment behaviours of the investors, which are basically cognitive in nature. The different dimensions of cognition create different investment perception towards the financial products. The better and more trustworthy is the cognitive elements, the greater the success in developing investment behaviour for a strong investment scenario. The study also took another step in categorising the investor on the basis of risk-taking abilities (previously, risk averse, risk neutral and risk taker). A new term, i.e., “risk-absorbed”, has been coined to portray an elite class of investors, those have been using those entire cognitive dimensions for their ultimate investment decision making. These categories of investors are proven to be potential investors.

4.2. Practical Contribution

The study will be proven as a helping hand for the asset management companies and financial services providers for strategizing the concepts derived in the study to understandthe domestic investors and encourage them to invest in the domestic market and in the relevant products. The different dimensions can be used to understand the brain mechanism of the investors and can set respective plans to manoeuvre their investor behaviour. The four dimensions can lead to four alternative patterns for providing trustworthy information, which could bring a sense of trust in the minds of the investor, and they could feel secure in the investment. The study can help the strategy makers of different financial service providers to categorise and follow those specific elite groups of risk-absorbed investors with specific characters, as discussed earlier in the study, to draw investment for a longer duration of time. These investments with long duration end in sustainable capital adequacy in an economy.

4.3. Limitation of the Study

The study is based on 392 responses. Had it been of more responses, more reliable inferences could have been drawn. This study is based on the Odisha prospective. With a larger geographical base like other states of India as well as other parts of developing countries, a better result could have been extracted. The study focused only on the cognitive part of the investors, ignoring the affective, conative and psychomotor component. The combination of the tri-components can bring a healthy result in this section of study.

4.4. Scope for Future Research

Further research can be done in this field, where different dimensions of cognition can be studied to amplify investment brain mechanism towards investment scenarios. The other components of attitude formation such asthe conative, affective and psychomotor can be studied along with different dimensions of cognitions and can provide better and more reliable results. More focuses could be given to understand other different traits of risk-absorbed investors to categorise them in the elite group. Different other researchers from different developing countries can make collaborative research to come to new and common conclusions for inspiring investor to invest in the domestic economy and market.

5. Conclusions

Failure in the past investment and domestic economic crisis because of foreign economic break down has scared the domestic investors away frominvesting in the capital market. For the procurement of steady capital for the financial need of the nation, the participation of the domestic investors is very much necessary. Encouraging domestic investors has been a major necessity for “Atmanirbhar Bharat” (self-reliant India) with regard to capital adequacy from domestic sources. For this purpose, understanding, informing, strengthening and influencing the modern day investors has never been imperative as it has become in this digital era. Therefore, better strategies must be evolved to make people aware and understand all the information relating investment, so that persons with risk-absorption capacity can process that information and can develop good investment strategies and will enhance their level of interest in investment. Strategy makers can use the different dimensions of cognition to become knowledgeableabout the sources of information that investors adhere to and can use those sources for educating and developing investors’ sentiments towards investment. Marketers of financial products such assystematic investment plans (SIP) and mutual funds can use the different dimensions of cognition as different sources motivating the investor according to their information processing level and can set strategies accordingly. With the use of technology, it has been very easy to provide information through a different channel, which could build risk-absorption capacity, which can result in a better firmed decision. In the hands of marketers, the study has proven to be of greater importance, as it can use both the dimensions of cognition as well as traits of risk absorption for providing available systematic information to the investors for better understanding of the investment scenario and to take greater risk in investment, which can solve the problem of lack of domestic investment from domestic investors. The strategies also help the nation to procure better, trustworthy and steady sources of capital for economic development and sustainability.

,

,

{kind=link}