1. Introduction

The COVID-19 pandemic was first identified in late 2019. In 2020, it spread around the globe, with the World Health Organization (WHO) identifying the first case on 31 December 2019 in Wuhan, China. Shortly after, on 11 March 2020, the WHO classified the COVID-19 virus outbreak as a global pandemic. As the pandemic has spread across the globe, the number of deaths and confirmed cases has soared. As such, nearly all the countries of Earth have implemented various containment measures, such as social distancing and lockdowns, in an effort to mitigate the pandemic’s lethal impact. The top 10 countries based on GDP (the U.S., China, Japan, Germany, India, the U.K., France, Italy, Brazil, and Canada) have accounted for 60% of total cases as of 15 August 2020, which in turn halted many economic and financial activities across the globe (

Chaudhry et al. 2020). The stock market indices in the U.S., U.K., and China decreased by 14.9%, 21.4%, and 12.1% respectively (

Shehzad et al. 2020).

In Australia, and as of 30 December 2020, 28,350 confirmed cases of COVID-19 were reported, with 25,751 recovered and 909 deaths. In response, the federal government introduced social distance and sanitary measures to alleviate the spread of the COVID-19 virus, followed by a nationwide lockdown on 13 March 2020, when the government announced that all mass gatherings or events with more than 500 participants were to be cancelled. More restrictions were imposed over the following days (

IMF 2020). These restrictions caused 3.8% and 3.2% declines in GDP and household savings respectively over 2020, interrupting 26 years of economic growth (

OECD 2020). By the end of 2020, the S&P/ASX 200 index fell by nearly 5.84%. The Australian federal government announced a fiscal stimulus scheme of AUD 164 billion to mitigate the economic and financial effects of COVID-19. The bailout package encompassed households’ support and health system aids, and commercial banks were permitted to use more of their capital buffer by deferring the scheduled implementation of Basel III reforms (

IMF 2020). The Australian Prudential Regulation Authority (APRA) also allowed temporary relief from its capital requirements to commercial banks in order to facilitate ongoing lending activities.

These developments in the Australian market remind us of the function of information arrival and its effect on asset prices, especially within equity markets, which are useful barometers to gauge tension in financial markets. From this point of view, in this study, we attempted to test the impact of COVID-19 on various sectoral indices of the Australian equity market. Although the influence of the pandemic on the entire economy was inevitable due to the heightened systematic risks associated with lockdowns, social distancing, curfews, and uncertainness, theoretically, we expected that the exposure of the sectors would vary depending on the extent of market integration and type of goods and services generated. For instance, whereas some sectors such as tourism, entertainment, and hospitality were the most negatively impacted by the pandemic, opportunities were created for certain industries such as online payment, e-commerce, chemists, online gaming, and remote learning. Therefore, following

Gunay and Kurtulmuş (

2020), we employed eleven sector indices to reveal the pros and cons of the pandemic in the Australian economy. In this investigation, stock market sectoral indices were used as a proxy to represent different components of aggregate economic activity. This approach is based on the proposition of the Efficient Market Hypothesis (EMH). The EMH states that all public information should be captured by asset prices. The extent of the reflection illustrates the level of market efficiency. The current stock prices also contain the present value of the future expectations of different market participants. Therefore, following the developments in stock indices, we evaluated the anticipations of various markets and projected productive policies.

Given this information, in the empirical analysis section of the study, we investigated the financial contagion between the Chinese stock market and Australian Stock market, examined the structural breaks in each sector indices’ volatilities, and tested the influence of the pandemic on these indices. Our findings contribute to the existing literature by providing evidence from different sectors regarding the incorporation of information arrivals. Additionally, as China is the largest trade partner of Australia, we provide evidence from the domain of financial contagion. Thus, we were able to observe the reaction of various sectors unlike the current literature studies (

Vo and Tran 2020;

Hung 2020;

Bouri et al. 2020;

Belaid et al. 2021) that investigated the overall market interactions and not the sectors. Similarly, instead of examining structural breaks in aggregate equity market, we explored this exposure with a sectorial framework. Consideration of our findings will allow investors to adjust their portfolios in accordance with the extent of the effect in different sectors. Our empirical findings may serve policymakers in terms of the actions that need to be taken in the most-impacted sectors. Implementation of necessary polices and measures in corresponding sectors would enhance the stability of the economy and offer less volatile equity markets.

The remainder of the paper is organized as follows:

Section 2 provides a review of the relevant literature;

Section 3 describes the research methodology,

Section 4 contains data description and the analysis of the results, and

Section 5 summarizes the conclusions derived from this study.

2. Review of the Literature

Significant external shocks tend to have striking impacts on macroeconomic and financial variables. Over the last decades, economic, financial, political, environmental, and health crises have spurred financial researchers to quantify their impacts on stock market returns.

Recently, a group of studies has measured the impact of the COVID-19 pandemic on stock market performance in different countries. For instance,

Chaudhry et al. (

2020) measured the effect of COVID-19 on the daily return volatilities of stock markets in the top ten countries based on GDP (the U.S., China, Japan, Germany, India, the U.K., France, Italy, Brazil, and Canada) between January 2019 and June 2020. They found a daily negative mean return for the aforementioned index between January 2020 and June 2020, which was characterized by its high volatility compared with normal periods. These markets have experienced a higher degree of interconnectedness in the wake of COVID-19.

Gunay (

2020) examined the financial contagion in various stock markets. The results indicated that while the time-varying correlations of Chinese and Turkish stock markets weakened between 2005 and 2019, due to the pandemic, it rose by 20% in 2020.

Alber (

2020) studied the impact of COVID-19 on stock market returns in the U.S, China, France, Italy, Spain, and Germany, revealing that daily confirmed COVID-19 cases had a larger negative effect on stock returns in China, France, Spain, and Germany compared with U.S and Italian markets. In a similar work,

He et al. (

2020) used daily data to assess the impact of the COVID-19 pandemic on Asian and developed-countries stock markets. They concluded that the COVID-19 pandemic has negatively affected the stock markets in China, Italy, South Korea, Spain, France, Germany, Japan, and the U.S. However, this negative impact was not isolated to these groups of markets, but also affected global financial markets. Likewise,

Sansa (

2020) studied the impact of COVID-19 on the stock markets in the U.S. and China and found that the number of confirmed COVID-19 cases affected both stock markets.

Shehzad et al. (

2020) compared the behaviour of U.S, EU, and Asian stock markets during the Global Financial Crisis and COVID-19 pandemic. They found that the Global Financial Crisis had a more severe impact on stock market volatility in Japan and China compared with COVID-19; in addition, they concluded that the stock markets in the U.S. and selected E.U. countries were more affected by the COVID-19 pandemic than their counterparts in Asia.

Al-Awadhi et al. (

2020) found a profound negative impact of daily growth by total confirmed cases and in total cases of death caused by COVID-19 on stock returns in the Chinese market.

Gunay et al. (

2021) investigated the impact of the pandemic on the economic growth of China. Their predictions showed a recovery in the third quarter of 2020 in the Chinese economy. The authors found that the Midas regression model outperformed the Markov regime-switching analysis in economic forecasts. A number of studies, such as

Fahlenbrach et al. (

2020),

Ramelli and Wagner (

2020),

Alfaro et al. (

2020), and

Hassan et al. (

2020), found that, in general, nonfinancial firms have been less affected by the repercussions of COVID-19. Conversely,

Albuquerque et al. (

2020) found that during COVID-19, the shares of U.S. firms with high environmental and social ratings experienced higher returns and less volatility compared with their counterparts with lower ratings.

In Australia, the impact of the COVID-19 pandemic was most pronounced within the education and tourism sectors, in addition to cafes, restaurants, and accommodation services (

RBA 2020a). The pandemic has considerably impacted the total Australian university revenue due to the substantial decrease in the number of international students continuing their studies in Australia during the pandemic (

Thatcher et al. 2020). However, the effects of the COVID-19 outbreak have been mitigated by the good financial health of Australian households and businesses prior to the outbreak, and by the swift and unprecedented actions of policymakers to bail out the Australian financial system (

RBA 2020b).

O’Sullivan et al. (

2020) provided a theoretical detection and explanation of the impact of COVID-19 pandemic on Australia from economic and social perspectives. The study found that with respect to the noticeable impact of COVID-19 on trade, education, and tourism sectors, Australia’s stable economic and political systems, alongside early-imposed sanitary and social distancing measures, have helped mitigate the impact of the pandemic on Australia.

Downey and Myers (

2020), who compared the governmental responses to COVID-19 between the United States and Australia, supported these findings. They also claimed that unlike the conflicting and inconsistent responses exhibited by different U.S. authorities, Australian authorities have been working collaboratively and at the same pace as the World Health Organization (WHO) to overcome and face the repercussions of the pandemic. However, only a few studies provided analytical measures of the impact of the COVID-19 outbreak on the Australian stock market. For instance,

Brueckner and Vespignani (

2020) tested the response of the ASX-200 index to an increase in the number of COVID-19 infections. They found that the ASX-200 exhibited 0.2% growth (next day) for each 1% increase in the daily number of COVID-19 cases and 0.5% growth on the second day. A plausible interpretation for such outcomes, as claimed by

Sedlacek and Sterk (

2020), is that the large firms (listed on ASX-200) might have indirectly benefited from the economic circumstances during COVID-19, as start-up businesses were more negatively effective, which in turn reduced competition in the market.

Despite the considerable efforts to prognosticate and measure the impact of various, economic, financial, environmental, and non-environmental shocks on the Australian stock market, at present, there is a dearth of empirical evidence of the impact of the COVID-19 pandemic on the sector returns in the Australian stock market. We closely inspected the scope of the impact of the first wave of the COVID-19 pandemic on different Australian sectors. This study is thought to be one of the earliest attempts to provide a comprehensive sectoral analysis of the impact of this dire event on the Australian stock market.

4. Data and Empirical Analysis

In this study, we examined the impact of the COVID-19 pandemic on different Australian sectors. Lockdowns, travel restrictions, quarantines, and extreme forms of physical distancing across the country have affected different sectors of the Australian economy. Using firms included in the S&P/ASX 200 index, we sorted them into sectors based on the Global Industry Classification Standard (GICS) with a total of 11 sectors (

Table 1). Afterward, the sectors’ return indices were generated using two weights: market capitalization weights and equal weights for each sector. Using market capitalization weights might produce biased results due to firms included in each sector having different sizes or market capitalization. Equality in the weights allowed us to overcome the size effects of the constituents included in each sector.

In empirical analysis, we employed various econometric models including the DCC-FIGARCH model (to display the time-varying behaviour of correlations between the Shanghai Composite Index and each of the Australian sector indices), the M-ICSS test (to examine if the Black Summer Bushfires and the first wave of the COVID-19 pandemic led to structural breaks in the volatilities of these indices), and the MRSR analysis (to model the recent financial downturn and capture the impact of the COVID-19 pandemic on the Australian sectors). Econometric tests were conducted through OxMetrics, R, Gauss, and E-Views.

The data used in this study were the daily closing stock prices for all firms included in the S&P/ASX 200, and the daily closing prices for the Shanghai Composite Index (SHE). Each variable contained 1416 daily observations. The data were obtained from the Refinitiv Eikon database. The continuously compounded daily returns were calculated for each firm by taking the difference in the logarithms of the two consecutive prices of a series, which were then used to produce each sector’s return indices. This study examined the time period of 1 January 2015 to 5 June 2020, which includes the events of the Black Summer Bushfires and the COVID-19 pandemic (Wave 1). The time horizon was deemed to be long enough to appropriately capture the departures in the cyclic patterns of index return series that might have been caused by the pandemic. Financial and economic time series show cycles over time, and the duration and amplitude of these cycles may vary in expansion and contraction periods. The trend formed in time series behaviour may be distorted due to shocks such as wars, civil conflicts, natural disasters, industrial disputes, or financial crises.

Zarnowitz and Ozyildirim (

2006) stated that business cycles are mostly formed between two and eight years. In a recent study,

Hiebert et al. (

2018) stated that financial cycles may be even longer than business cycles. Using relatively shorter periods may produce artificial findings as they may contain rapidly varying seasonal and irregular components.

Figure 1 illustrates the effect of the first wave of the pandemic during the first two quarters of 2020. The general S&P/ASX 200 index dropped to an unprecedented level during Quarter One (Q1) 2020 and gained back almost half of this loss during Quarter Two (Q2) 2020. Similarly, most Australian sectors exhibited similar patterns to the general index, with all sectors experiencing a substantial drop in their price indices during the first quarter of 2020 and partially regaining it back in the second quarter. However, the impact of the first wave of the pandemic was moderate for the ConSi, HCi, ITi, Mati, and Utili, since these sectors benefited from the increase in demand for their products and services during the first wave of the pandemic (for example, increase in the demand for food and beverage products, healthcare, and various IT services).

In general, both market capitalization and equally weighted sectoral indices exhibited similar price movements over the period of the study. However, equally weighted sectoral indices showed a lower price level compared with the market capitalization indices. This occurred due to lowering the weight of the larger market capitalization firms, which mainly exhibited higher price per share compared with smaller size firms, while the weight of smaller market capitalization firms increased. ConSi equally weighted index shows a higher price level, mainly around end of 2015 and for the first three quarters of 2016 compared with the use of market capitalization weights. This is mainly due to Blackmores Limited, which is a relatively small size firm in that sector. The price per share for this firm has increased from AUD 35 in January 2015 reaching its highest value of AUD 220.90 during early January 2016.

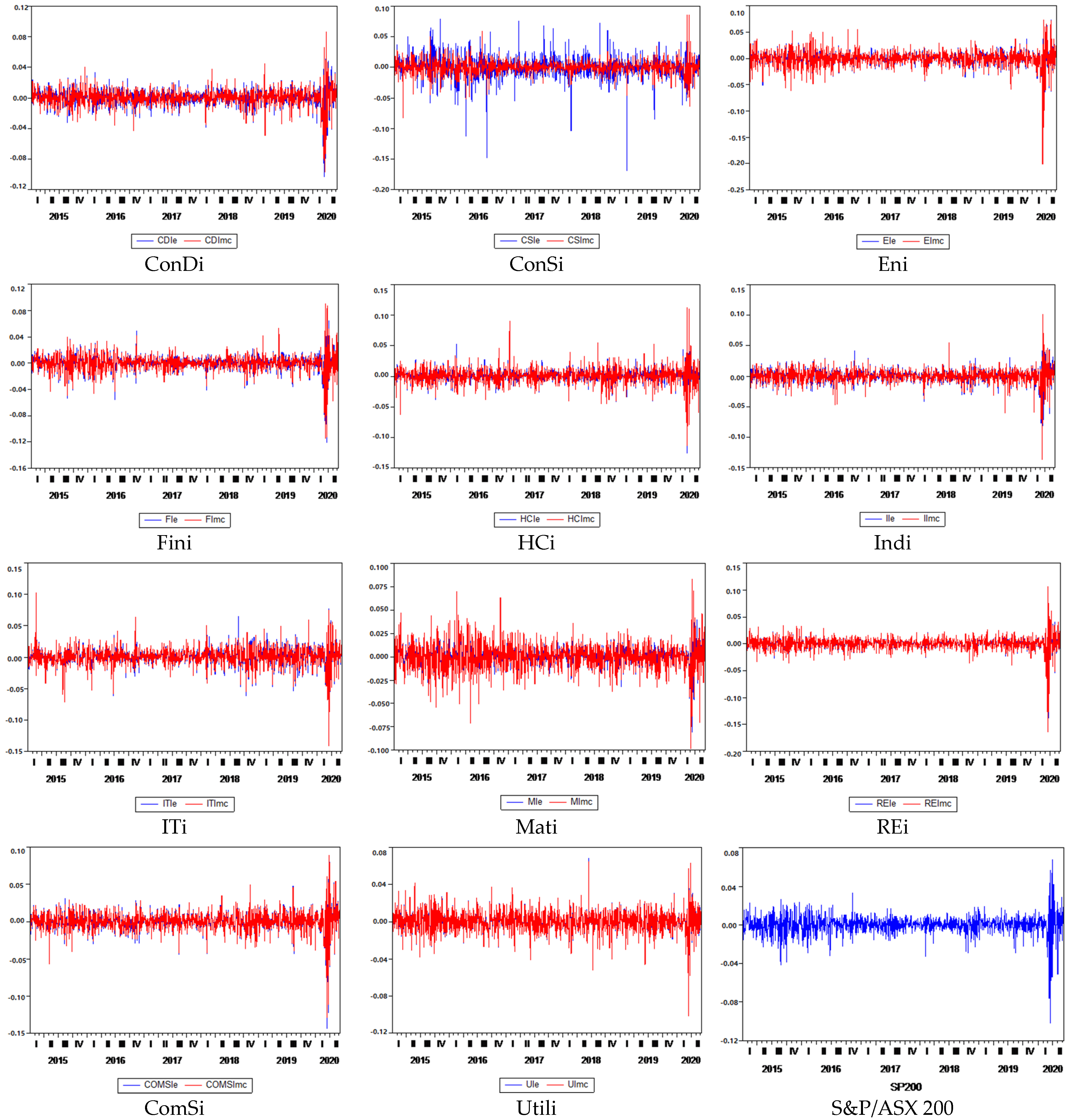

In

Appendix A, we present the returns of each variables. As shown, sector return indices series exhibited different fluctuations in terms of their scale and timing ranges, from low fluctuations, as in the REi, to extreme fluctuations such as that in the ConSi, Mati, or Utili. The variability in returns for all sectors was extremely high during the COVID-19 pandemic period, larger than in any other year. Looking at the variability of returns in the S&P/ASX 200 index, we concluded that this was also the case for the whole Australian market.

Figure 1 shows that the variability in return indices changed when we used equal weights in the creation of indices. By lowering the weights of the larger market capitalization firms, the variability in returns in ConDi and ConSi increased. This implies that smaller companies exhibited larger changes in returns for these two sectors. For the remaining sectors, the variability in returns decreased when equal weights were used in the creation of the return indices, implying that large companies in these sectors experienced greater fluctuations in their return series.

Table 2 provides descriptive statistics for each index series. The results revealed that for market capitalization weighted indices, the highest average returns occurred for the HCi and ITi, while the Eni and Fini exhibited the lowest. However, most sectors (except for HCi, REi, and Utili) displayed higher returns for the indices generated with the equally weighted method. This implies that smaller companies in these sectors experienced higher average returns. Regarding the volatility in the return series (as measured by the standard deviation), the highest variability in the market capitalization indices occurred in the returns of the Eni, ITi, and Mati; and in ConSi, ITi, and Eni for equally weighted indices. Contrary to the average return results, the variability in the returns in most sectors (except for ConDi and ConSi) decreased with the change in weights. The skewness and kurtosis test statistics as well as the Jarque–Bera test for normality indicated that the return indices for all sectors were more asymmetric, fat-tailed, and high-peaked than the Gaussian distribution. Except for health care in market-cap weighted indices, all sectors in both groups displayed negative skewness. This means that the frequency of higher returns was greater in these sectors.

Before proceeding to the main analysis, we examined the stationarity of the variables. Non-stationary time series might lead to spurious results in the empirical analysis.

Pippenger and Goering (

2000) showed that standard unit root tests, Augmented Dickey Fuller (ADF) and Phillips-Perron (PP), do not have sufficient power against the nonlinear alternatives. Considering the potential nonlinear dynamics of the variables, the multiple regime self-exciting threshold autoregressive (SETAR) model (hereafter BBC model) of

Bec et al. (

2010) was employed. The empirical critical values of the test are 16.18, 18.4, and 23.01 at 90%, 95%, and 99% confidence levels, respectively. In both market-cap and equally weighted indices, we allowed the middle regime to follow a random walk process, and the null of a unit root was jointly tested in lower and upper regimes. In

Table 3, we present the Wald statistic results for the joint significance of the autoregressive parameters in the outer regimes. The BBC test results suggested the rejection of the null hypothesis of a unit root at the 1% level for each variable in both market-cap and equally weighted indices when considering the nonlinear dynamics. Under the consideration of regime shifts, in the final section of the study, we utilized another nonlinear model, Markov regime-switching regression analysis, in the examination of the influence of COVID-19 on these sectors.

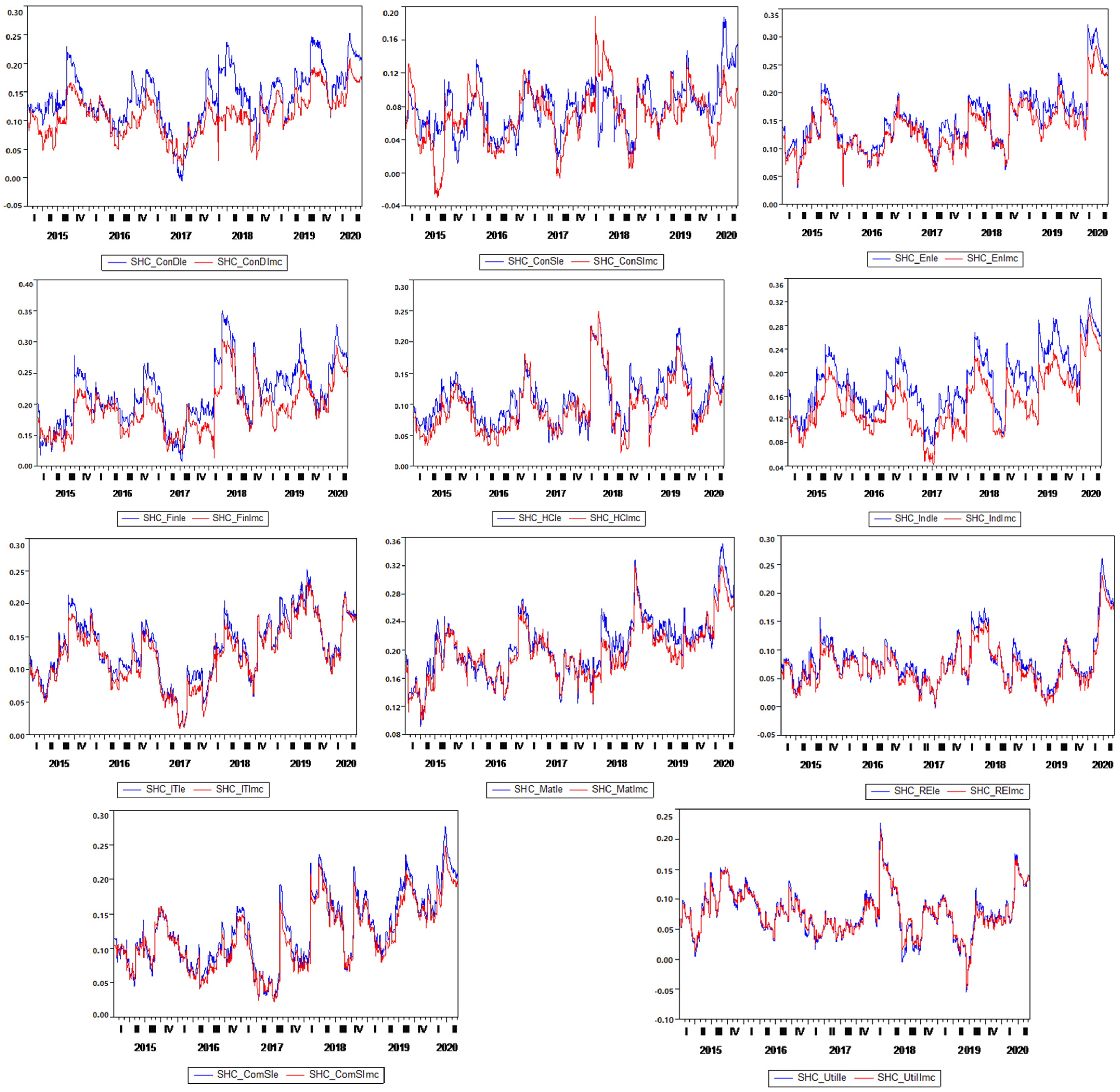

To reveal the pandemic’s effects on the Australian stock market, the time-varying correlations between the Shanghai Composite Index (SHC) and the constructed sector indices of the Australian equity market were examined. The objective of the investigation of the stock market co-movements of China and Australia was twofold: First, as the pandemic emerged in China and spread to other countries, we considered this in the return spillovers and examined the time-varying correlations between Chinese stock market and various Australian sector indices. The second reason is also based on objective criteria. Economic statistics exhibit very-high connectedness between these two countries. China is Australia’s largest two-way trading partner in goods and services, accounting for 29% of Australia’s trade with the world. Chinese–Australian trade has escalated to AUD 251 billion in 2019–2020 (up 7% year on year). Additionally, China remained the biggest services export market of Australian goods and services, particularly in education and tourism. On 20 December 2020, The China–Australia Free Trade Agreement (ChAFTA) entered into force. The agreement aims at enhancing the Australian competitive position in the Chinese market, boosting economic growth, and creating jobs. It has also brought comparative advantages to Australian businesses in terms of lower tariffs (

Australian Government, Department of Foreign Affairs and Trade 2021).

Since this study covers the period from 2015 to 2020, it was possible to explore the long-term behavior of conditional correlations and their behavior during important social and economic events. These events can directly or indirectly be linked to the Australian economy. For example, as the largest trade partner of Australia, the Chinese stock market experienced a bubble and plunge in 2015 and 2016, respectively. The high integration of the Chinese and Australian stock markets suggests that risk transmission between the two is highly possible. Secondly, November 2016 was another important year for the global financial markets due to the U.S. election and its potential effects on financial markets. The imposition of tariffs on Chinese products in 2017 by the U.S. was another significant event to consider. Finally, the Black Summer Bushfires in 2019 and the COVID-19 pandemic in 2020 have severely shocked domestic and international financial markets, and Australia was inevitably affected by these experiences. As dynamic conditional correlations illustrate the co-movement of variable pairs over time, they allowed us to examine pre-, during, and post-turmoil periods of financial contagion.

Figure 2 displays the time-varying behavior of correlations between SHC and various Australian sector indices. As discussed earlier, two types of indices were constructed: the first one utilizes market capitalization weights; the second employs equal weights. This methodology allowed us to incorporate the influence of firm size in the relationships. According to the results, except for the ConDi, Fini and Indi, all other indices illustrated a tiny spread in the path of correlations for market capitalization weighted and equally weighted indices. However, equally weighted indices depicted a higher correlation with the Chinese stock market for these three sectors. Since equally weighted indices used a relatively lower weight for large companies and a higher weight for small companies, smaller firms in these sectors had higher co-movements with the Chinese stock market. This finding for these sectors may be related to, although having one or two extremely large companies, being dominated by smaller size firms. When we examined the period of the pandemic’s first wave, it is evident that in addition to these three sectors, ConSi, Eni, and Mati sectors showed a significant difference in equally weighted market indices. In each variable, we observed that smaller companies substantially contributed to the extent of co-movements with the Chinese stock market. Conversely, when we examined the behavior of correlations across the years, the Fini, HCi, ITi, and Utili sectors showed lower correlations with the Chinese stock market during the pandemic than their historical averages. For the remaining sectors, co-movements with the Chinese stock market during the COVID-19 period exhibited record high values. For all sectors, the correlation with the Chinese stock market showed an increase during Q1 2020 followed by a decline during Q2 2020. This might be related to the start of COVID-19 in China during Q1, followed by the virus reaching Australia during Q2, which led to the lockdown and slowdown of financial and economic activities during this period.

To examine the impact of aforementioned events on the volatilities of sector indices, the M-ICSS algorithm of

Sansó et al. (

2004) was applied. The results in

Table 4 show that almost all variables showing a break during the pandemic, either on 18 or 21 February 2020, except for the market capitalization weighted ConSi, Indi, ITi, and REi. This date corresponds to a major decline in global financial markets due to COVID-19 (also known as the Coronavirus Crash), which started on 20 February 2020. As for the equally weighted indices, similar results were found with the exception of Fini and HCi, which did not show any breaks during the COVID-19 period. The difference in these two index forms’ results can be attributed to their nature, that is, the size of the firms in these indices. When we lower the weight of the large firms and increase the weight of small firms, the break in the volatility of Fini and HCi fades, meaning that the break in these indices is mainly due to the volatility in large firms’ stock returns. Surprisingly, the M-ICSS test suggested that ConSi, Indi, ITi, and REi did not experience any break in their volatilities, in neither the market-cap-weighted nor equally weighted indices.

As a final test, we employed MRSR analysis. The MRSR model is helpful when the parameters of a data-generating process vary over a set of different observed states. The model characterizes the relationships of variables under two regimes and is therefore applicable to economic cycles (depression and expansion), financial markets (low and high volatility), etc. Therefore, the MRSR model analyzes the asymmetric relationship between the regime-dependent variables. Accordingly, the MRSR results are presented in two panels: regime one and regime two. In theory, both regimes are generated by multiple equilibria in aggregate economic activity; therefore, each regime reflects the possible behavior of different periods, such as bullish and bearish or expansion and contradiction periods. However, in order to examine the impact of the Black Summer Bushfires and the COVID-19 pandemic on the Australian sectors, our main focus was the coefficient of the dummy variables rather than the characterization of both regimes. As independent variables, we used the Australian S&P/ASX 200 index returns and dummy variables to gauge the impact of the COVID-19 pandemic and the Black Summer Bushfires. For the Black Summer Bushfires, the dummy variable took the value of 0 before 1 August 2019 and 1 until 24 January 2020. For the COVID-19 pandemic, the dummy variable took the value of 0 before 27 January 2020 (when the first COVID-19 case was confirmed by the Australian Department of Health on 25 January 2020) and 1 until the last observation. The S&P/ASX 200 index is considered as an investable benchmark for the Australian equity market that reflects local and foreign investors’ risk and return preferences. By employing the S&P/ASX 200 index in our model, we were able to explain the changes in the dependent variable, which are highly linked to the general market trend. Compared with tranquil periods, the bushfires and the pandemic periods might exhibit higher volatility and therefore lower predictability. We used the sector index returns series as dependent variables.

Table 5 demonstrates the outcomes of the Markov regime-switching regression. The results indicated that under the market capitalization weighted model, the ConSi, Eni, Indi, and REi exhibited statistically and economically significant coefficients for the COVID-19 dummy variable, with Indi and REi sectors being the most impacted sectors with coefficients (Regime Two) of 0.138 and −0.077, respectively. Although the ConDi, Fini, and HCi showed statistically significant coefficients for the COVID-19 dummy variable, the values for these coefficients were very close to zero, indicating that the COVID-19 pandemic had very little impact on these sectors. The coefficients for the ConSi and Indi sectors switched from negative (under the one-tranquil-period regime) to positive (under the two-crisis-period regime) signs, indicating that the COVID-19 pandemic had a positive impact on these two sectors. The Eni and REi were negatively impacted by the COVID-19 pandemic. The results for the consumer staples sector can be explained by the general panic-buying and stockpiling behavior, which led to an extraordinary increase in household expenditure on non-discretionary products such as food, beverage, household, and personal care: products that usually have a low-income elasticity of demand (

Funck and Gutierrez 2016;

Nicola et al. 2020). For the industrial sector, although the aviation and industrial transportation industries were negatively impacted by the COVID-19 pandemic, the Australian government announced AUD 715 million of unconditional Australian airline relief through the Coronavirus Economic Response Package, in which a range of fees were waived in order to mitigate the negative impact of COVID-19 on this industry (

Australian Government Fact Sheet 2020). The aerospace and defense, construction and materials, and electronic and equipment industries maintained a good position during the COVID-19 lockdown. Most high market capitalization shares in the industrial sector (such as Qantas Airways Limited and Transurban Group) maintained a healthy liquidity position via debt raising, while others (such as Aurizon Holdings Limited, Brambles Limited, and CIMIC Group Limited) increased their on-market share buy-back activities during the pandemic (see ASX announcements for more details. Available at

https://www.asx.com.au/asx/statistics/announcements.do, accessed on 18 December 2020). Finally, the real estate sector results can be explained by almost all stocks in that sector being real estate investment trusts (REITs), which mainly have commercial properties in their portfolios, such as offices, industrial retails, and hospitality spaces. The lockdown restrictions in Australia had a negative effect on rent, earning distributions, and the ability of these REITs to serve their debts, which in turn negatively affected investor perception of the future prospects of this industry. As such, the real estate sector experienced a drastic fall in its returns during the COVID-19 pandemic (

Akinsomi 2020). The results also showed that the COVID-19 pandemic period had no substantial impact on Eni, Mati, ITi, ComSi and Utili.

The effect of the Black Summer Bushfires on the Australian sectors was limited to the ConSi and Indi, with signs of a positive impact on the former and a negative impact on the latter. The positive impact on the ConSi might be explained by the panic-buying of food and beverage products due to the increase in air pollution levels all over Australia and citizens remaining indoors more to avoid the pollution. The negative effect on the Indi was mainly due to the negative impact of the bushfires on the transportation and capital goods industries. Other than these two sectors, it seems that the Black Summer Bushfires did not have a substantial impact on Australia’s sectors. A possible explanation for this is that bushfires mainly occur in forested lands; thus, the negative effect of bushfires on different sectors of the Australian economy might be limited. These findings are consistent with those of

Ulubaşoğlu et al. (

2019).

When the constituents inside each sector’s indices were equally weighted, meaning that the weight of larger market capitalization firms was lowered while the weight of smaller market capitalization firms was increased, ConDi, Eni, HCi, Indi, REi, and ComSi exhibited statistically and economically significant coefficients for the COVID-19 dummy variable. Moreover, the Eni and HCi showed higher and significant negative coefficients compared with the market capitalization weighting coefficient. This might indicate that the gradual deterioration in these sectors started in comparatively small firms’ stock returns. Finally, and interestingly, the ConDi sector showed a large, positive, and significant coefficient compared with a negative, small, but significant coefficient under the market capitalization method. This finding indicated that small firms were positively impacted by the pandemic. This was confirmed upon examining the data of sectors dominated by relatively small- and medium-sized firms. It is evident that these firms displayed a better performance during the pandemic compared with their large-sized counterparts. The results for Eni, Indi, and REi are consistent with the findings obtained under the market capitalization weighted index model.

With respect to the effect of the Black Summer Bushfires on the Australian sectors under the equally weighted index model, only Eni exhibited a statistically significant and positive coefficient, implying that smaller firms in the energy sector, constituting half the sample, performed better than larger ones during Australia’s devastating bushfires in 2019. ConSi and Indi did not show any significant coefficient under the equally weighted method as they did with the market capitalization method. This implies that the impact of the Black Summer Bushfires was mainly felt by large firms in these two sectors. We did not observe any influence in any other sector caused by the Black Summer Bushfires.

As the findings showed, the response of different service sector indices to the COVID-19 pandemic varied in the Australian equity market. As asset prices are expected to incorporate the incoming information and future predictions, the extent of the shocks to stock returns can indicate the expected deterioration in future cash flows for the companies that form these industries. Therefore, the pandemic’s revealed influence can be of use for portfolio managers who want to adjust their portfolio weights for better diversification and for policymakers who need to take corresponding actions. The bottom line is, depending on the extent of efficiency, stock markets can serve as an early warning system for economies, and since our study provides evidence on a sector basis, the results allow different market participants to adjust their investment and expenditure strategies. The results suggest that the regulatory authorities should expeditiously undertake the required actions to support specific sectors, such as real estate, whose recovery depends more on the effectiveness of the domestic policy responses to controlling the pandemic. The recovery of other sectors important for capital investment, such as industry, is more dependent on global financial system’s resilience and the ability to absorb the negative and adverse spillovers of the pandemic.

5. Conclusions

In addition to resulting in severe illness and health risks for humans, the first wave of COVID-19 pandemic has disrupted the functioning of the Australian and global economies. The main purpose of this study was to examine the reactions of various Australian sector indices to the first wave of COVID-19. Empirical analyses were conducted using the stock return series of 200 firms from eleven sectors included in the ASX/S&P 200 index. These firms were classified per their relative sectors over the period from 1 January 2015 to 5 June 2020. The indices were created with market capitalization weights and equal weights to control for the firm size effect. Empirical analyses were conducted through the DCC-FIGARCH model, M-ICSS, and MRSR analysis.

Time-varying conditional correlations showed that across the years, smaller companies have significantly contributed the co-movements between consumer discretionary, financial, and industrial sectors, and the Chinese stock market. During the pandemic, we observed that smaller companies in the consumer staples, energy, and materials sectors also strengthened their correlations with the Chinese equity market. However, when we examined the historical development in correlations, we observed that the co-movements of financial, health care, information technology, and utilities sectors with the Chinese stock market declined during the pandemic, while others displayed record high values. To examine the potential structural breaks in the volatilities of these sector indices, we also employed the M-ICSS test. The results showed that in both group of indices, consumer staples, industrial, information technology, and real estate sectors did not display a break during the coronavirus crash of 18–21 February 2020.

The MRSR analysis results indicated that among eleven sectors, the most significant findings were found in the consumer staples, industrial, and real estate sectors. While the industrial and consumer staples sectors were positively impacted by the pandemic with coefficients of 0.13 and 0.03, respectively, this effect was negative for the real estate sector with a coefficient of −0.08. The highest positive impact seen in consumer staples index can be accounted for by the general panic-buying and stockpiling behaviour of households during the pandemic. Although aviation and transportation industries were negatively affected by the pandemic from a global perspective, the positive coefficient can be explained by the mitigating influence of Australian government’s AUD 715 million unconditional airline relief package. Thus, this aid indicates the effectiveness of economic relief programs employed in crisis periods. For the real estate sector, disruptions in rental incomes and earning distributions distorted their cash flows, which was incorporated in their index performance. When we increased the weight of smaller companies in the formation indices (equally weighted indices), the energy sector experienced a larger negative effect of the pandemic due to the deterioration in the performance of these smaller companies. More interestingly, changing the weight showed that smaller companies in consumer discretionary sector experienced the largest positive effect from the pandemic.

Aligning with the propositions of the efficient market hypothesis, we concluded that when sector indices reflect the information disseminated in the market, asset price developments can provide useful information for the investors and policymakers to adjust their portfolio weights and take necessary actions. Thus, sector indices might be used as a barometer for all market participants to gauge the stress and tension in the different segments of the economy, as revealed in this study.

{kind=link}

{kind=link}

{kind=link}