Sectoral Performance and the Government Interventions during COVID-19 Pandemic: Australian Evidence

Abstract

:1. Introduction

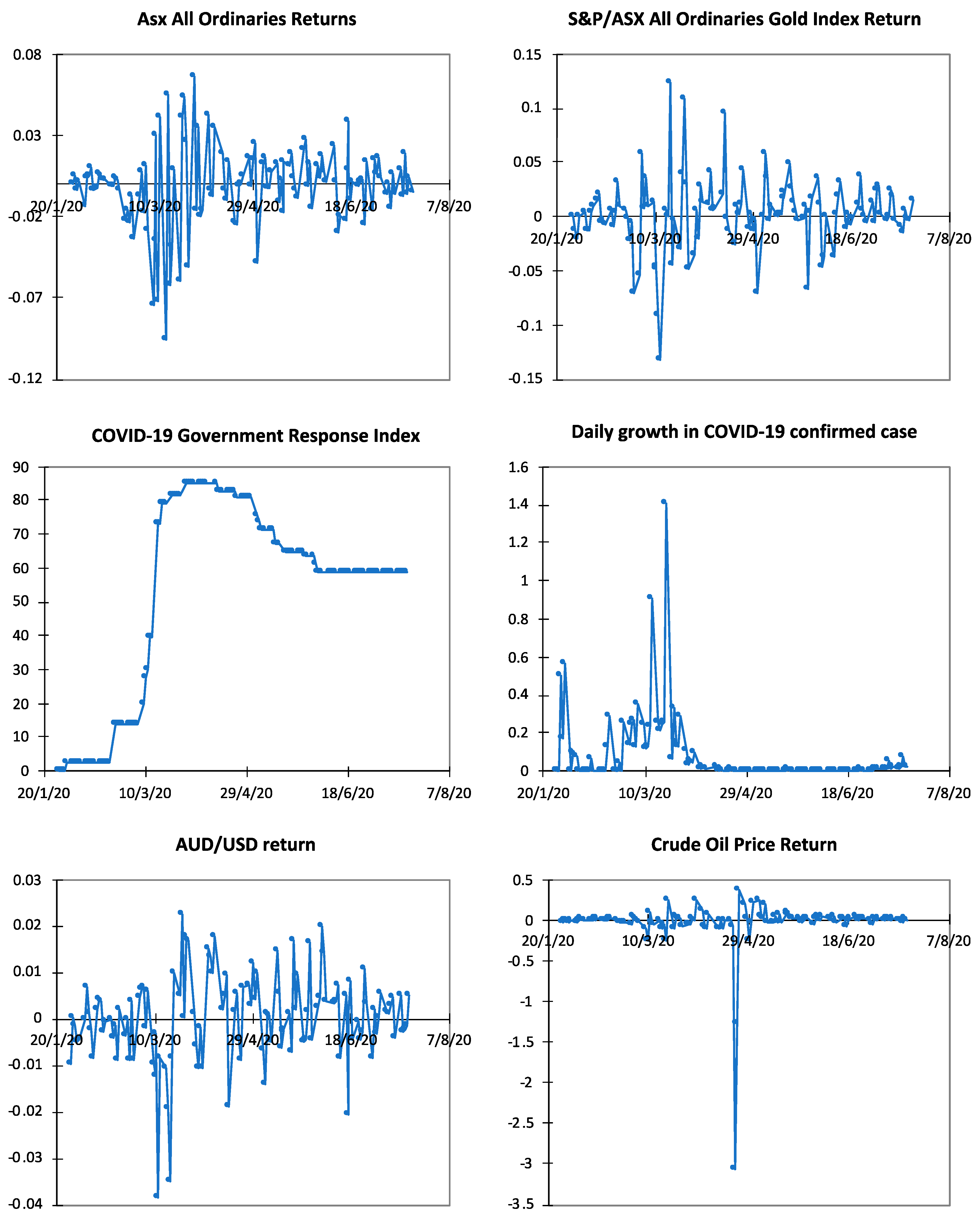

2. Data and Methodology

3. Results and Discussion

3.1. Empirical Results

3.2. Result Summary and Discussion

4. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Variables

| Dependent Variable | ||

| Market-Cap Index | Description | Source |

| ASX ALL ORDINARIES | The index represents the 500 largest companies in the Australian equities market. Index constituents are drawn from eligible companies listed on the Australian Securities Exchange. Liquidity is not considered as criteria for inclusion, except for foreign domiciled companies. | S&P Dow Jones Indices Database |

| S&P/ASX 50 | The S&P/ASX 50 is Australia’s most prominent large-cap equity index and is designed to represent 50 of the largest and most liquid stocks listed on the ASX by float-adjusted market capitalization. | S&P Dow Jones Indices Database |

| S&P/ASX 300 | The S&P/ASX 300 is designed to provide investors with broader exposure to the Australian equity market. The index is liquid and float-adjusted, and it measures up to 300 of Australia’s largest securities by float-adjusted market capitalization. The S&P/ASX 300 index covers the large-cap, mid-cap, and small-cap components of the S&P/ASX Index Series. This index is designed to address investment managers’ needs to benchmark against a broad opportunity set characterized by sufficient size and liquidity. | S&P Dow Jones Indices Database |

| Sectoral Index | ||

| S&P/ASX All Ordinaries Gold Index | S&P/ASX All Ordinaries Gold Index includes companies in the gold sub-industry of the All Ordinaries Index. The index includes a wide range of companies within the GICS® gold sub-industry, and therefore, serves as an ideal broad market indicator for the gold industry. | S&P Dow Jones Indices Database |

| S&P/ASX All Technology Index | The S&P/ASX All Technology Index is designed to be a comprehensive measure of technology-oriented companies listed on the ASX that meet certain investability constraints. It includes companies classified under the GICS® Information Technology sector, as well as additional relevant sub-industries in other sectors. | S&P Dow Jones Indices Database |

| S&P/ASX 300 A-REIT | A sector subindex of the S&P/ASX 300, this index tracks the performance of Australian real estate investment trusts (A-REITs) and mortgage REITs. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Consumer Discretionary | The S&P/ASX 300 Consumer Discretionary provides investors with a sector benchmark that reflects those companies included in the S&P/ASX 300 that are classified as members of the GICS® consumer discretionary sector and sub-industries. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Consumer Staples | The S&P/ASX 300 Consumer Staples provides investors with a sector benchmark that reflects those companies included in the S&P/ASX 300 that are classified as members of the GICS® consumer staples sector and sub-industries. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Energy | The S&P/ASX 300 Energy provides investors with a sector benchmark that reflects those companies included in the S&P/ASX 300 that are classified as members of the GICS® energy sector and sub-industries. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Financials excluding A-REITs Index | A sector sub-index of the S&P/ASX 300, this index contains companies involved in activities such as banking, mortgage finance, consumer finance, specialized finance, investment banking and brokerage, asset management and custody, corporate lending, insurance, and financial investment, excluding Australian real estate investments trusts (A-REITs), mortgage REITs, equity REITs, and real estate management & development companies. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Health Care | The S&P/ASX 300 Health Care provides investors with benchmark that reflects those companies included in the S&P/ASX 300 that are classified as members of the GICS® health care sector and sub-industries | S&P Dow Jones Indices Database |

| S&P/ASX 300 Industrials | The S&P/ASX 300 Industrials provides investors with sector benchmark that reflects those companies included in the S&P/ASX 300 that are classified as members of the GICS® industrials sector and sub-industries. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Information Technology | The S&P/ASX 300 Information Technology provides investors with a sector benchmark that reflects those companies included in the S&P/ASX 300 that are classified as members of the GICS® information technology sector and sub-industries. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Materials | The S&P/ASX 300 Materials provides investors with a sector benchmark that reflects those companies included in the S&P/ASX 300 that are classified as members of the GICS® materials sector and sub-industries. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Metals and Mining | The S&P/ASX 300 Metals and Mining Index is based on the S&P/ASX 300 Index, and is comprised of companies that are classified as being in the Metals and Mining industry1. It includes producers of aluminium, gold, steel, precious metals and minerals and also diversified metals and minerals. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Real Estate | The S&P/ASX 300 Real Estate comprises stocks included in the S&P/ASX 300 that are classified as members of the GICS® real estate sector. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Resources | A sector sub-index of the S&P/ASX 300 Index, this index provides investors with a sector exposure to the Resources sector of the Australian equity market as classified as members of the GICS® resources sector. Resources are defined as companies classified in the Energy sector (GICS® Tier 1), as well as companies classified in the Metals and Mining Industry (GICS® Tier 3) | S&P Dow Jones Indices Database |

| S&P/ASX 300 Communication Services | The S&P/ASX 300 Communication Services provides investors with a sector benchmark that reflects those companies included in the S&P/ASX 300 that are classified as members of the GICS® communication services sector and sub-industries. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Utilities | The S&P/ASX 300 Utilities provides investors with a sector benchmark that reflects those companies included in the S&P/ASX 300 that are classified as members of the GICS® utilities sector and sub-industries. | S&P Dow Jones Indices Database |

| S&P/ASX 300 Banks | The S&P/ASX 300 Banks (Industry) provides investors with a benchmark that is designed to measure constituents in the S&P/ASX 200 that are classified as members of the GICS® Banks industry and sub-industries. | S&P Dow Jones Indices Database |

| Independent Variable | ||

| Daily growth in COVID-19 confirmed cases | The growth rate in coronavirus-related data is calculated from the Coronavirus Pandemic (COVID-19) data on daily basic. | Our World in Data: https://ourworldindata.org/coronavirus-data |

| COVID-19 Government Response Index | Oxford COVID-19 Government Response Tracker (OxCGRT), systematically collects information on several different common policy responses that governments have taken to respond to the pandemic on 17 indicators such as school closures and travel restrictions. The higher value, the more references to levels of pandemic in the country. | Blavatnik School of Government database, University of Oxford |

| Control Variables | ||

| AUD/USD exchange rate | Daily exchange rate between Australian dollar and U.S dollar on daily basic. | Investing Database |

| Brent crude oil prices per barrel (USD) | Brent crude oil prices in USD per barrel on daily basic. | Investing Database |

Appendix B. Graphical Correlation Matrix

| 1 | The data was retrieved on 27th March 2021 from the World Health Organization (WHO): https://covid19.who.int/ (accessed on 27 March 2021). |

| 2 | The data was retrieved from the Mar 2020 Issue—Australian National Accounts: National Income, Expenditure and Product on the Australian Bureau of Statistics (ABS) website. |

| 3 | The data for GRI is not stationary as the index increases overtime during the pandemic and gradually falls according to the updated government policies. |

References

- Akhtaruzzaman, Md, Sabri Boubaker, Mardy Chiah, and Angel Zhong. 2020. COVID−19 and Oil Price Risk Exposure. Finance Research Letters, 101882. [Google Scholar] [CrossRef]

- Akhtaruzzaman, Md, Sabri Boubaker, and Ahmet Sensoy. 2021. Financial Contagion during COVID–19 Crisis. Finance Research Letters 38: 101604. [Google Scholar] [CrossRef] [PubMed]

- Banerji, Gunjan. 2020. Why Did Stock Markets Rebound From Covid in Record Time? Here Are Five Reasons. Wall Street Journal. September 15, sec. Markets. Available online: https://www.wsj.com/articles/why-did-stock-markets-rebound-from-covid-in-record-time-here-are-five-reasons-11600182704 (accessed on 20 January 2021).

- Chen, Mei-Ping, Chien-Chiang Lee, Yu-Hui Lin, and Wen-Yi Chen. 2018. Did the S.A.R.S. Epidemic Weaken the Integration of Asian Stock Markets? Evidence from Smooth Time-Varying Cointegration Analysis. Economic Research-Ekonomska Istraživanja 31: 908–26. [Google Scholar] [CrossRef] [Green Version]

- Choudhry, Taufiq. 2005. September 11 and Time-Varying Beta of United States Companies. Applied Financial Economics 15: 1227–42. [Google Scholar] [CrossRef]

- Corbet, Shaen, Constantin Gurdgiev, and Andrew Meegan. 2018. Long-Term Stock Market Volatility and the Influence of Terrorist Attacks in Europe. The Quarterly Review of Economics and Finance 68: 118–31. [Google Scholar] [CrossRef]

- Del Giudice, Alfonso, and Andrea Paltrinieri. 2017. The Impact of the Arab Spring and the Ebola Outbreak on African Equity Mutual Fund Investor Decisions. Research in International Business and Finance 41: 600–12. [Google Scholar] [CrossRef]

- Elyasiani, Elyas, Iqbal Mansur, and Babatunde Odusami. 2011. Oil Price Shocks and Industry Stock Returns. Energy Economics 33: 966–74. [Google Scholar] [CrossRef]

- Guo, Mengmeng, Yicheng Kuai, and Xiaoyan Liu. 2020. Stock Market Response to Environmental Policies: Evidence from Heavily Polluting Firms in China. Economic Modelling 86: 306–16. [Google Scholar] [CrossRef]

- Hiang Liow, Kim, Muhammad Faishal Ibrahim, and Qiong Huang. 2006. Macroeconomic Risk Influences on the Property Stock Market. ” Journal of Property Investment & Finance 24: 295–323. [Google Scholar] [CrossRef]

- Ichev, Riste, and Matej Marinč. 2018. Stock Prices and Geographic Proximity of Information: Evidence from the Ebola Outbreak. International Review of Financial Analysis 56: 153–66. [Google Scholar] [CrossRef]

- Ilzetzki, Ethan, Carmen Reinhart, and Kenneth Rogoff. 2020. Will the Secular Decline In Exchange Rate and Inflation Volatility Survive COVID-19? w28108. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Ji, Qiang, Dayong Zhang, and Yuqian Zhao. 2020. Searching for Safe-Haven Assets during the COVID-19 Pandemic. International Review of Financial Analysis 71: 101526. [Google Scholar] [CrossRef]

- Karolyi, George Andrew, and Rodolfo Martell. 2006. Terrorism and the Stock Market. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Kim, Harold Y, and Jianping P Mei. 2001. What Makes the Stock Market Jump? An Analysis of Political Risk on Hong Kong Stock Returns. Journal of International Money and Finance 20: 1003–16. [Google Scholar] [CrossRef]

- Kowalewski, Oskar, and Piotr Śpiewanowski. 2020. Stock Market Response to Potash Mine Disasters. Journal of Commodity Markets 20: 100124. [Google Scholar] [CrossRef] [Green Version]

- Liu, Xiaohui, and Peter Sinclair. 2008. Does the Linkage between Stock Market Performance and Economic Growth Vary across Greater China? Applied Economics Letters 15: 505–8. [Google Scholar] [CrossRef]

- Ngo, Thanh. 2017. “Exchange Rate Exposure of REITs”. The Quarterly Review of Economics and Finance 64: 249–58. [Google Scholar] [CrossRef]

- Okorie, David Iheke, and Boqiang Lin. 2021. Stock Markets and the COVID-19 Fractal Contagion Effects. Finance Research Letters 38: 101640. [Google Scholar] [CrossRef] [PubMed]

- Peckham, Robert. 2013. Economies of Contagion: Financial Crisis and Pandemic. Economy and Society 42: 226–48. [Google Scholar] [CrossRef]

- Shanaev, Savva, and Binam Ghimire. 2019. Is All Politics Local? Regional Political Risk in Russia and the Panel of Stock Returns. Journal of Behavioral and Experimental Finance 21: 70–82. [Google Scholar] [CrossRef]

- Vuchelen, Jef. 2003. Electoral Systems and the Effects of Political Events on the Stock Market: The Belgian Case. Economics & Politics 15: 85–102. [Google Scholar] [CrossRef]

- Wachter, Jessica A. 2013. Can Time-Varying Risk of Rare Disasters Explain Aggregate Stock Market Volatility? The Journal of Finance 68: 987–1035. [Google Scholar] [CrossRef] [Green Version]

- Wang, Lin, and Ali M Kutan. 2013. The Impact of Natural Disasters on Stock Markets: Evidence from Japan and the US. Comparative Economic Studies 55: 672–86. [Google Scholar] [CrossRef]

- Zhang, Dayong, Min Hu, and Qiang Ji. 2020. Financial Markets under the Global Pandemic of COVID-19. Finance Research Letters 36: 101528. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

| Market-Cap Index | Abbreviation | Source |

|---|---|---|

| ASX ALL ORDINARIES | ASX | S&P Dow Jones Indices Database |

| S&P/ASX 50 | ASX50 | S&P Dow Jones Indices Database |

| S&P/ASX 300 | ASX300 | S&P Dow Jones Indices Database |

| Sectoral Index | ||

| S&P/ASX All Ordinaries Gold Index | Gold | S&P Dow Jones Indices Database |

| S&P/ASX All Technology Index | Technology | S&P Dow Jones Indices Database |

| S&P/ASX 300 Real estate investment trusts (A-REITs) and mortgage REITs | REIT | S&P Dow Jones Indices Database |

| S&P/ASX 300 Consumer Discretionary | Con-discretionary | S&P Dow Jones Indices Database |

| S&P/ASX 300 Consumer Staples | Consumer Staples | S&P Dow Jones Indices Database |

| S&P/ASX 300 Energy | Energy | S&P Dow Jones Indices Database |

| S&P/ASX 300 Financials excluding A-REITs | Fin Ex | S&P Dow Jones Indices Database |

| S&P/ASX 300 Health Care | Health Care | S&P Dow Jones Indices Database |

| S&P/ASX 300 Industrials | Industrials | S&P Dow Jones Indices Database |

| S&P/ASX 300 Information Technology | IT | S&P Dow Jones Indices Database |

| S&P/ASX 300 Materials | Materials | S&P Dow Jones Indices Database |

| S&P/ASX 300 Metals and Mining | Metals and Mining | S&P Dow Jones Indices Database |

| S&P/ASX 300 Real Estate | Real Estate | S&P Dow Jones Indices Database |

| S&P/ASX 300 Resources | Resources | S&P Dow Jones Indices Database |

| S&P/ASX 300 Communication Services | Communication | S&P Dow Jones Indices Database |

| S&P/ASX 300 Utilities | Utilities | S&P Dow Jones Indices Database |

| S&P/ASX 300 Banks | Bank | S&P Dow Jones Indices Database |

| Independent Variable | ||

| Daily growth in COVID-19 confirmed cases | CASE | Our World in Data |

| COVID-19 Government Response Index | GRI | Blavatnik School of Government database, University of Oxford |

| Control Variable | ||

| Daily AUD/USD exchange rate return | FX | Investing Database |

| Daily Brent crude oil prices return | OIL | Investing Database |

| Market-Cap Index | Obs | Mean | S.D. | Jarque–Bera Test | ADF Test | PP Test |

|---|---|---|---|---|---|---|

| ASX | 122 | −0.001 | 0.025 | 41.51 * | −3.734 * | −13.942 * |

| ASX50 | 122 | −0.001 | 0.025 | 40.69 * | −3.947 * | −14.676 * |

| ASX300 | 122 | −0.001 | 0.025 | 42.18 * | −3.776 * | −14.151 * |

| Sectoral Index | ||||||

| Gold | 122 | 0.002 | 0.033 | 90.78 * | −5.446 * | −8.223 * |

| Technology | 122 | 0.001 | 0.031 | 27.23 * | −3.627 * | −12.466 * |

| REIT | 122 | −0.002 | 0.034 | 99.35 * | −4.120 * | −11.250 * |

| Con-Discretionary | 122 | −0.001 | 0.028 | 41.33 * | −3.837 * | −12.303 * |

| Consumer Staples | 122 | 0.000 | 0.020 | 112.13 * | −6.948 * | −16.417 * |

| Energy | 122 | −0.003 | 0.039 | 205.67 * | −3.848 * | −12.009 * |

| Fin Ex | 122 | −0.001 | 0.032 | 23.80 * | −3.932 * | −13.456 * |

| Health Care | 122 | 0.000 | 0.029 | 71.45 * | −4.839 * | −20.482 * |

| Industrials | 122 | −0.002 | 0.027 | 143.41 * | −3.904 * | −11.603 * |

| IT | 122 | 0.001 | 0.031 | 18.57 * | −3.607 * | −12.181 * |

| Materials | 122 | 0.000 | 0.026 | 43.31 * | −4.173 * | −13.378 * |

| Metals and Mining | 122 | 0.001 | 0.027 | 53.78 * | −4.438 * | −13.303 * |

| Real Estate | 122 | −0.002 | 0.034 | 107.10 * | −4.084 * | −11.417 * |

| Resources | 122 | 0.000 | 0.028 | 78.16 * | −4.088 * | −13.356 * |

| Communication | 122 | −0.001 | 0.020 | 49.08 * | −5.036 * | −14.518 * |

| Utilities | 122 | 0.000 | 0.019 | 157.42 * | −5.189 * | −12.171 * |

| Bank | 122 | −0.002 | 0.035 | 19.41 * | −4.045 * | −13.201 * |

| Independent Variable | ||||||

| CASE | 122 | 0.077 | 0.179 | 4363.54 * | −1.929 | −7.374 * |

| GRI | 122 | 52.525 | 29.255 | 15.70 * | −1.421 | 0.188 |

| Control Variable | ||||||

| FX | 122 | 0.000 | 0.009 | 55.17 * | −4.726 * | −8.680 * |

| OIL | 122 | −0.030 | 0.311 | 294.59 * | −4.336 * | −7.675 * |

| Variable | ASX | ASX50 | ASX300 | GOLD | CASE | GRI | FX | OIL |

|---|---|---|---|---|---|---|---|---|

| ASX | 1.000 | |||||||

| ASX50 | 0.993 * | 1.000 | ||||||

| ASX300 | 0.999 * | 0.996 | 1.000 | |||||

| GOLD | 0.106 | 0.074 | 0.100 | 1.000 | ||||

| CASE | −0.327 * | −0.277 * | −0.314 * | −0.084 | 1.000 | |||

| GRI | 0.163 | 0.146 | 0.159 | 0.161 | −0.122 | 1.000 | ||

| FX | 0.098 | 0.079 | 0.096 | 0.164 | −0.066 | 0.157 | 1.000 | |

| OIL | 0.000 | 0.006 | 0.002 | −0.044 | 0.061 | −0.086 | 0.117 | 1.000 |

| Model | Variable | Market-Cap Index | |||||

|---|---|---|---|---|---|---|---|

| ASX | ASX50 | ASX300 | |||||

| Coefficient | t-Stat | Coefficient | t-Stat | Coefficient | t-Stat | ||

| (1) | Constant | 0.003 | (1.10) | 0.002 | (0.80) | 0.002 | (1.03) |

| −0.045 | (−3.79) ** | −0.039 | (−3.16) ** | −0.044 | (−3.63) ** | ||

| F-stat | 14.33 ** | 9.97 ** | 13.17 ** | ||||

| R-square | 0.107 | 0.077 | 0.099 | ||||

| (2) | Constant | 0.003 | (1.25) | 0.002 | (0.97) | 0.003 | (1.19) |

| −0.071 | (−3.15) ** | −0.069 | (−2.93) ** | −0.071 | (−3.10) ** | ||

| 0.000 | (1.35) | 0.001 | (1.48) | 0.000 | (1.39) | ||

| F-stat | 8.13 ** | 6.14 ** | 7.60 ** | ||||

| R-square | 0.120 | 0.094 | 0.113 | ||||

| (3) | Constant | 0.003 | (1.20) | 0.002 | (0.94) | 0.003 | (1.15) |

| −0.068 | (−3.00) ** | −0.067 | (−2.81) ** | −0.068 | (−2.95) ** | ||

| 0.000 | (1.24) | 0.001 | (1.40) | 0.000 | (1.29) | ||

| 0.001 | (0.11) | 0.001 | (0.16) | 0.001 | (1.12) | ||

| 0.164 | (0.71) | 0.119 | (0.62) | 0.159 | (68) | ||

| F-stat | 4.15 ** | 3.10 ** | 3.88 ** | ||||

| R-square | 0.124 | 0.096 | 0.117 | ||||

| Sector | Model 1 | Model 2 | Model 3 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Constant | F-Stat | R-Square | Constant | F-Stat | R-Square | Constant | F-Stat | R-Square | ||||||||

| Gold | 0.003 | −0.015 | 0.85 | 0.007 | 0.004 | −0.033 | 0.000 | 0.64 | 0.011 | 0.003 | −0.025 | 0.000 | −0.006 | 0.056 | 1.13 | 0.037 |

| (1.03) | (−0.92) | (1.09) | (−1.04) | (0.66) | (0.91) | (−0.79) | (0.46) | (−0.65) | (1.74) | |||||||

| Technology | 0.006 | −0.063 | 18.35 ** | 0.133 | 0.006 | −0.091 | 0.001 | 9.95 ** | 0.143 | 0.006 | −0.086 | 0.000 | 0.001 | 0.381 | 5.45 ** | 0.157 |

| (1.99) | (−4.28) ** | (2.13) * | (−3.29) ** | (1.21) | (2.04) * | (−3.07) ** | (1.03) | (0.16) | (1.35) | |||||||

| A-REIT | 0.004 | −0.072 | 20.44 ** | 0.146 | 0.003 | −0.057 | 0.000 | 10.31 ** | 0.148 | 0.003 | −0.046 | 0.000 | 0.000 | 0.882 | 7.29 ** | 0.200 |

| (1.16) | (−4.52) ** | (1.08) | (−1.90) | (−0.55) | (0.93) | (−1.54) | (−0.90) | (0.00) | (2.73) ** | |||||||

| Consumer Discretionary | 0.004 | −0.058 | 18.57 ** | 0.134 | 0.004 | −0.071 | 0.000 | 9.44 ** | 0.137 | 0.004 | −0.068 | 0.000 | 0.002 | 0.283 | 5.02 ** | 0.147 |

| (1.45) | (−4.31) ** | (1.51) | (−2.79) ** | (0.63) | (1.46) | (−2.61) ** | (0.48) | (0.26) | (1.08) | |||||||

| Consumer Staples | 0.001 | −0.016 | 2.74 | 0.022 | 0.001 | −0.022 | 0.000 | 1.43 | 0.023 | 0.002 | −0.026 | 0.000 | 0.005 | −0.221 | 1.17 | 0.038 |

| (0.59) | (−1.66) | (0.62) | (−1.18) | (0.37) | (0.78) | (−1.34) | (0.49) | (0.84) | (−1.15) | |||||||

| Energy | 0.003 | −0.075 | 16.10 ** | 0.118 | 0.003 | −0.129 | 0.001 | 9.88 ** | 0.142 | 0.003 | −0.128 | 0.001 | −0.008 | 0.038 | 5.00 ** | 0.146 |

| (0.73) | (−4.01) ** | (0.94) | (−3.69) ** | (1.83) | (0.85) | (−3.60) ** | (1.81) | (−0.70) | (0.11) | |||||||

| Financial excluding REIT | 0.003 | −0.059 | 14.34 ** | 0.107 | 0.003 | −0.074 | 0.000 | 7.32 ** | 0.109 | 0.003 | −0.070 | 0.000 | 0.002 | 0.308 | 3.91 ** | 0.118 |

| (1.01) | (−3.79) ** | (1.07) | (−2.50) * | (0.60) | (1.01) | (−2.32) * | (0.47) | (0.17) | (1.01) | |||||||

| Health Care | 0.001 | −0.010 | 0.48 | 0.004 | 0.001 | −0.061 | 0.001 | 2.65 | 0.043 | 0.002 | −0.065 | 0.001 | 0.007 | −0.305 | 1.74 | 0.056 |

| (0.18) | (−0.69) | (0.44) | (−2.24) * | (2.19) * | (0.59) | (−2.37) * | (2.29) * | (0.81) | (−1.09) | |||||||

| Industrials | 0.002 | −0.048 | 14.14 ** | 0.105 | 0.003 | −0.092 | 0.001 | 9.54 ** | 0.138 | 0.002 | −0.086 | 0.001 | 0.001 | 0.429 | 5.62 ** | 0.161 |

| (0.84) | (−3.76) ** | (1.09) | (−3.82) ** | (2.13) * | (0.99) | (−3.55) ** | (1.90) * | (0.09) | (1.76) | |||||||

| Information Technology | 0.005 | −0.057 | 14.90 ** | 0.110 | 0.005 | −0.088 | −0.001 | 8.37 ** | 0.123 | 0.006 | −0.083 | 0.000 | 0.001 | 0.404 | 4.72 ** | 0.139 |

| (1.88) | (−3.86) ** | (2.03) * | (−3.16) ** | (1.32) | (1.94) | (−2.93) ** | (1.13) | (0.14) | (1.42) | |||||||

| Materials | 0.003 | −0.032 | 6.11 * | 0.048 | 0.003 | −0.078 | 0.001 | 5.75 ** | 0.088 | 0.003 | −0.077 | 0.001 | −0.005 | 0.028 | 2.95 * | 0.092 |

| (1.14) | (−2.47) * | (1.41) | (−3.26) ** | (2.27) * | (1.31) | (−3.18) ** | (2.25) * | (−0.67) | (0.12) | |||||||

| Metals and Mining | 0.003 | −0.028 | 4.42 * | 0.035 | 0.004 | −0.079 | 0.001 | 5.03 ** | 0.078 | 0.003 | −0.079 | 0.001 | −0.006 | −0.012 | 2.63 * | 0.083 |

| (1.13) | (−2.10) * | (1.42) | (−3.12) ** | (2.34) * | (1.32) | (−3.07) ** | (2.33) * | (−0.75) | (−0.05) | |||||||

| Real Estate | 0.004 | −0.073 | 21.38 ** | 0.151 | 0.003 | −0.060 | 0.000 | 10.76 ** | 0.153 | 0.003 | −0.048 | 0.000 | 0.000 | 0.802 | 7.43 ** | 0.203 |

| (1.17) | (−4.62) ** | (1.10) | (−1.98) * | (−0.52) | (0.95) | (−1.63) | (−0.86) | (0.02) | (2.67) ** | |||||||

| Resources | 0.003 | −0.038 | 7.65 ** | 0.060 | 0.004 | −0.091 | 0.001 | 6.86 ** | 0.103 | 0.003 | −0.091 | 0.001 | −0.006 | −0.009 | 3.54 ** | 0.108 |

| (1.05) | (−2.77) ** | (1.34) | (−3.53) ** | (2.40) * | (1.24) | (−3.47) ** | (2.39) * | (−0.77) | (−0.04) | |||||||

| Communication Services | 0.001 | −0.020 | 3.73 | 0.030 | 0.001 | −0.023 | 0.000 | 1.87 | 0.031 | 0.001 | −0.023 | 0.000 | 0.002 | 0.057 | 0.99 | 0.033 |

| (0.41) | (−1.93) | (0.43) | (−1.18) | (0.20) | (0.45) | (−1.13) | (0.15) | (0.40) | (0.28) | |||||||

| Utilities | 0.003 | −0.037 | 15.90 ** | 0.117 | 0.003 | −0.056 | 0.000 | 8.91 ** | 0.130 | 0.003 | −0.058 | 0.000 | 0.003 | −0.095 | 4.51 ** | 0.134 |

| (1.47) | (−3.99) ** | (1.62) | (−3.24) ** | (1.34) | (1.68) | (−3.27) ** | (1.38) | (0.47) | (−0.53) | |||||||

| Banks | 0.003 | −0.059 | 12.24 ** | 0.093 | 0.003 | −0.075 | 0.000 | 6.27 ** | 0.095 | 0.003 | −0.071 | 0.000 | 0.001 | 0.293 | 3.31 * | 0.102 |

| (0.88) | (−3.50) ** | (0.95) | (−2.34) ** | (0.59) | (0.89) | (−2.81) * | (0.47) | (0.10) | (0.89) | |||||||

| Significantly Negative Impact | Negative Impact | No Significant Impact | |

|---|---|---|---|

| All market-cap indices | Materials a | Health Care a | Gold |

| Technology | Metals and Mining a | Financial excluding REIT | Consumer Staples |

| A-REIT b | Resources a | Banks | Communication services |

| Consumer Discretionary | Utilities | Real Estate b | |

| Industrials a | Energy | ||

| Information Technology | |||

| a Sectors are affected by the government interventions (using the GRI index). b Sectors are exposed to the AUD/USD rate fluctuations. | |||

| Scheme | Description | Date | Sectors |

|---|---|---|---|

| First Home Loan Deposit Scheme | The package allows first home buyer to purchase a home with a deposit as small as 5% without needing to pay lender mortgage insurance. It guarantees to a participating lender up to 15 percent of the value of the property purchased that is financed by an eligible first home buyer’s home loan. Source: www.nhfic.gov.au/what-we-do/fhlds/ (accessed on 15 January 2021) | 1 January 2020 | Real Estate, Financial ex-REIT, Banks |

| Home Builder Grant | It is tax-free grant program to help the residential construction market to get through the Coronavirus pandemic. It will provide eligible owner-occupiers (including first home buyers) with a grant of $25,000 to build a new home or substantially renovate an existing home. Source: www.sro.vic.gov.au/homebuilder-grant-guidelines (accessed on 15 January 2021) | 4 June 2020 | Real Estate, Financial ex-REIT, Banks |

| COVID-19: Land tax relief for landowners | States and territory governments have announced a range of land tax measures:

| 13 April 2020 | Real Estate |

| Coronavirus Small and Medium Enterprises (SME) Guarantee Scheme | This package provides up to $40 billions of lending to SMEs by guaranteeing 50 per cent of new loans issued by participating lenders. It also supports lenders’ ability to provide credit and ensure that SMEs benefit from low interest rates. Source: treasury.gov.au/coronavirus/coronavirus-sme-guarantee-scheme (accessed on 15 January 2021) | 23 March 2020 to 30 September 2020 | Financial ex-REIT, Banks |

| Relief for commercial tenants | It includes temporary hold on evictions and a mandatory code of conduct for commercial tenancies to support small and medium sized enterprises (SMEs) affected by coronavirus. Source: www.business.gov.au/risk-management/emergency-management/coronavirus-information-and-support-for-business/relief-for-commercial-tenancies (accessed on 15 January 2021) | 29 March 2020 | Real Estate |

| Coronavirus (COVID-19): National Health Plan resources | The $2.4 billion package provides unprecedented support across primary care, aged care, hospitals, research and the national medical stockpile. It also includes $30 million for the Communication sector to support a national communications campaign across all media. Source: www.health.gov.au/resources/collections/coronavirus-covid-19-national-health-plan-resources (accessed on 15 January 2021) | 11 March 2020 | Healthcare, Communication |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Huynh, N.; Nguyen, D.; Dao, A. Sectoral Performance and the Government Interventions during COVID-19 Pandemic: Australian Evidence. J. Risk Financial Manag. 2021, 14, 178. https://doi.org/10.3390/jrfm14040178

Huynh N, Nguyen D, Dao A. Sectoral Performance and the Government Interventions during COVID-19 Pandemic: Australian Evidence. Journal of Risk and Financial Management. 2021; 14(4):178. https://doi.org/10.3390/jrfm14040178

Chicago/Turabian StyleHuynh, Nhan, Dat Nguyen, and Anh Dao. 2021. "Sectoral Performance and the Government Interventions during COVID-19 Pandemic: Australian Evidence" Journal of Risk and Financial Management 14, no. 4: 178. https://doi.org/10.3390/jrfm14040178

APA StyleHuynh, N., Nguyen, D., & Dao, A. (2021). Sectoral Performance and the Government Interventions during COVID-19 Pandemic: Australian Evidence. Journal of Risk and Financial Management, 14(4), 178. https://doi.org/10.3390/jrfm14040178