Bitcoin and Portfolio Diversification: A Portfolio Optimization Approach

Abstract

:1. Introduction

2. Literature Review

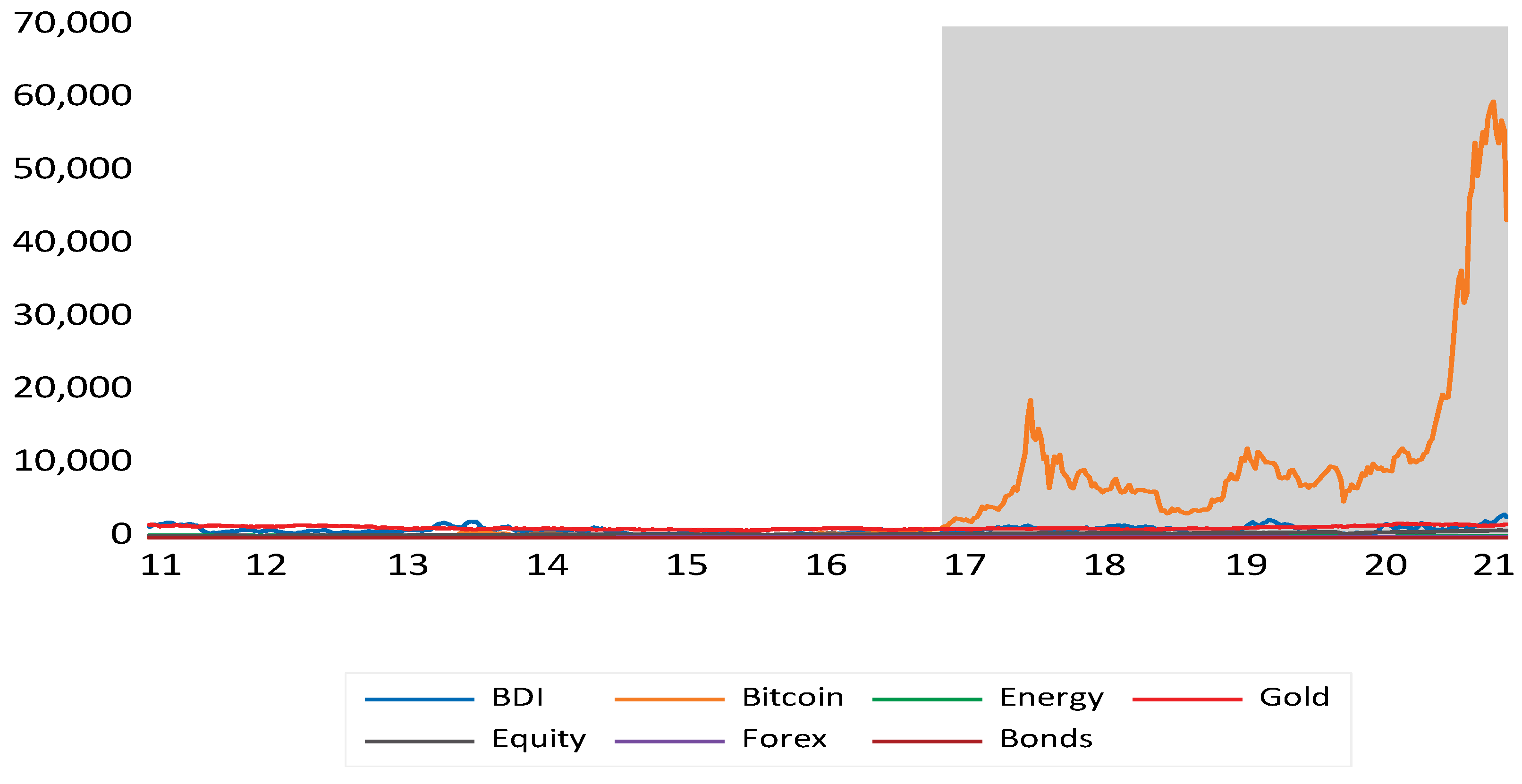

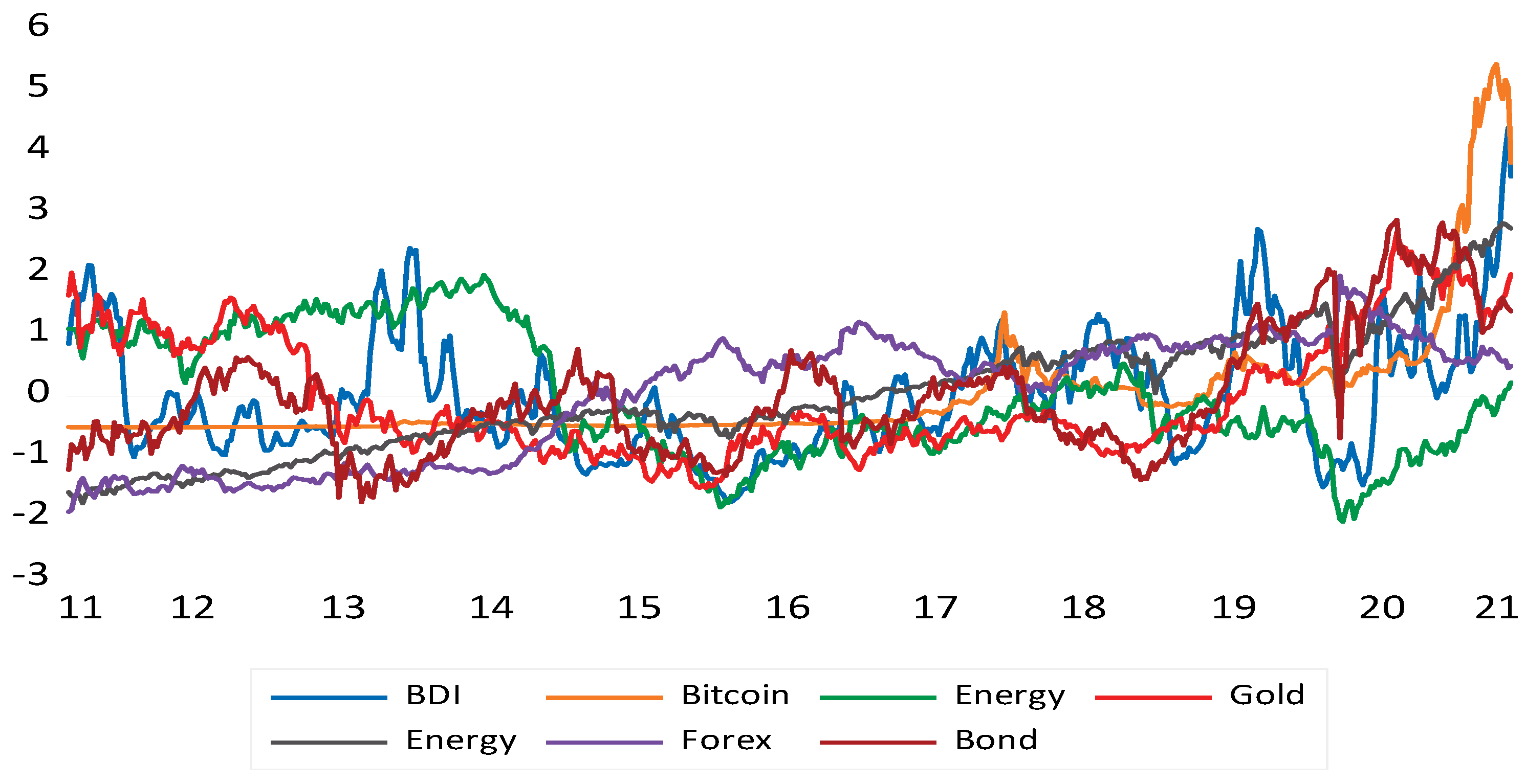

3. Data Description and Research Methodology

3.1. Mean-Variance Optimization

3.1.1. Scenario 1: Equal-Weighted or Naïve Portfolio ()

3.1.2. Scenario 2: Semi-Constrained Max-Long Portfolio (

3.1.3. Scenario 3: Semi-Constrained Min-Long Portfolio (

3.1.4. Scenario 4: Constrained Portfolio 1 (

3.1.5. Scenario 5: Risk Parity (Long Only) Portfolio (

3.1.6. Scenario 6: Risk Parity Unconstrained Portfolio (

3.1.7. Scenario 7: Unconstrained Portfolio (

3.1.8. Scenario 8: Long Only Portfolio ()

3.1.9. Scenario 9: Minimum Variance ()

3.1.10. Scenario 10: Semi-Constrained Portfolio 2 (

4. Results and Analysis

4.1. Descriptive Statistics

4.2. Portfolio Optimization and Monte Carlo Simulation

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

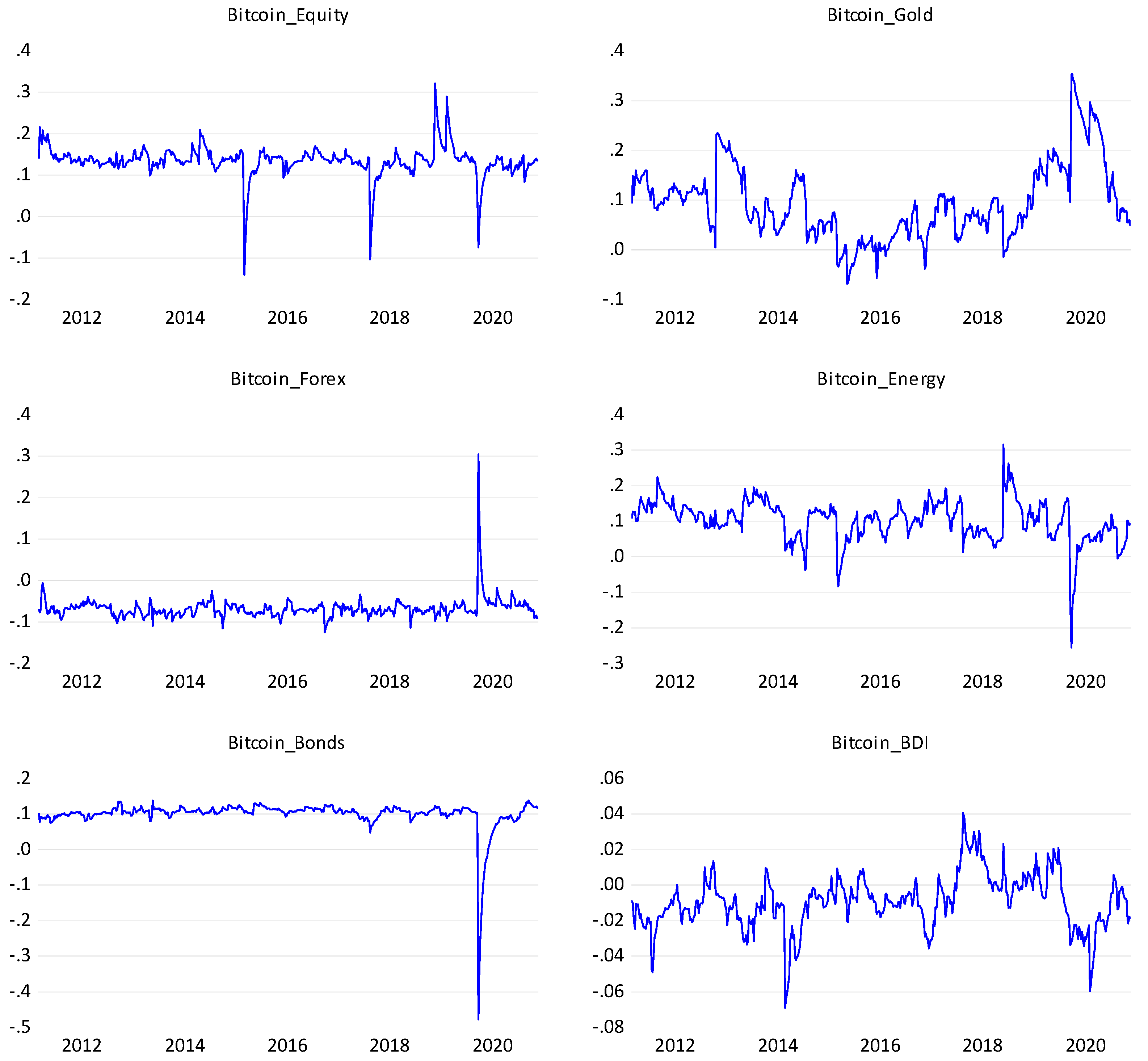

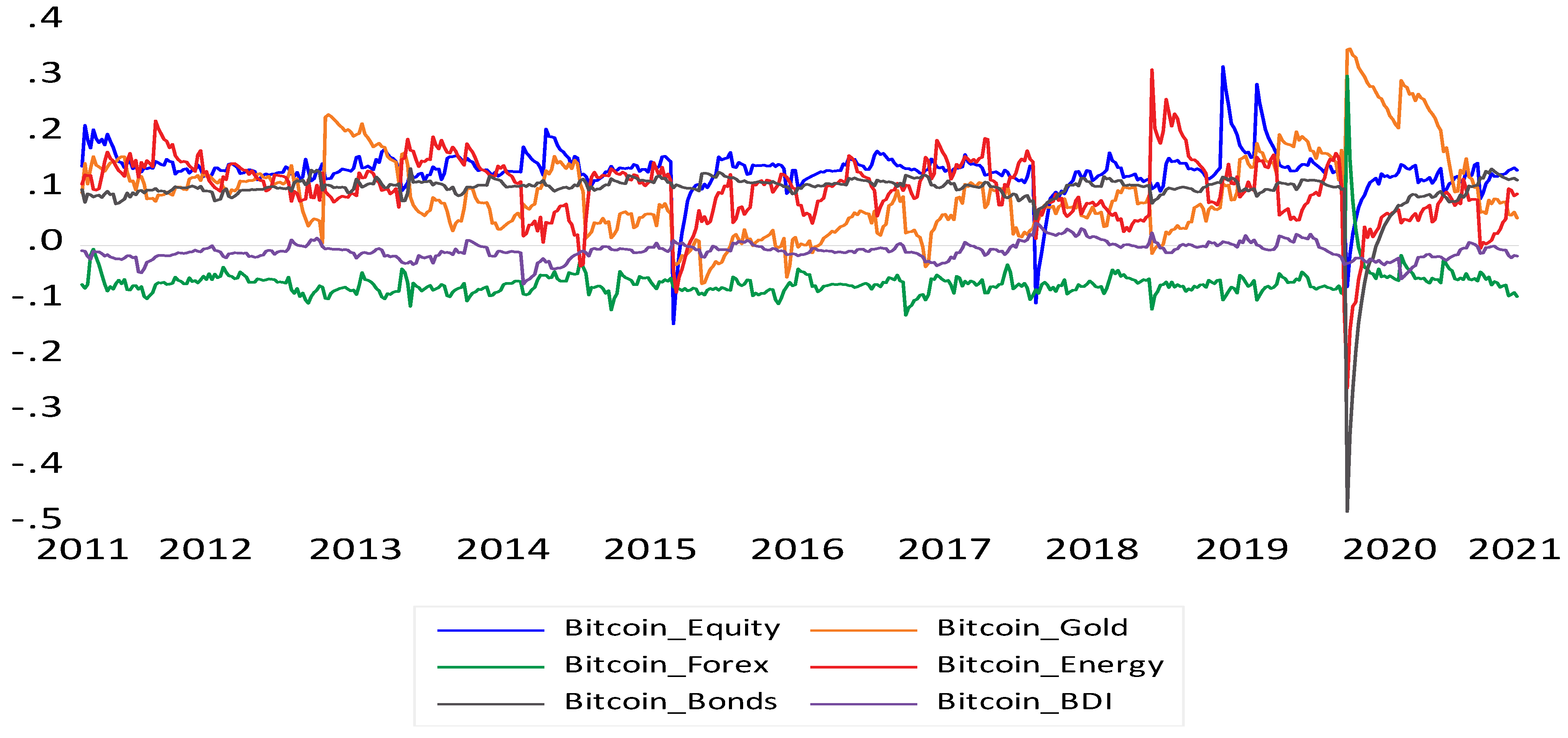

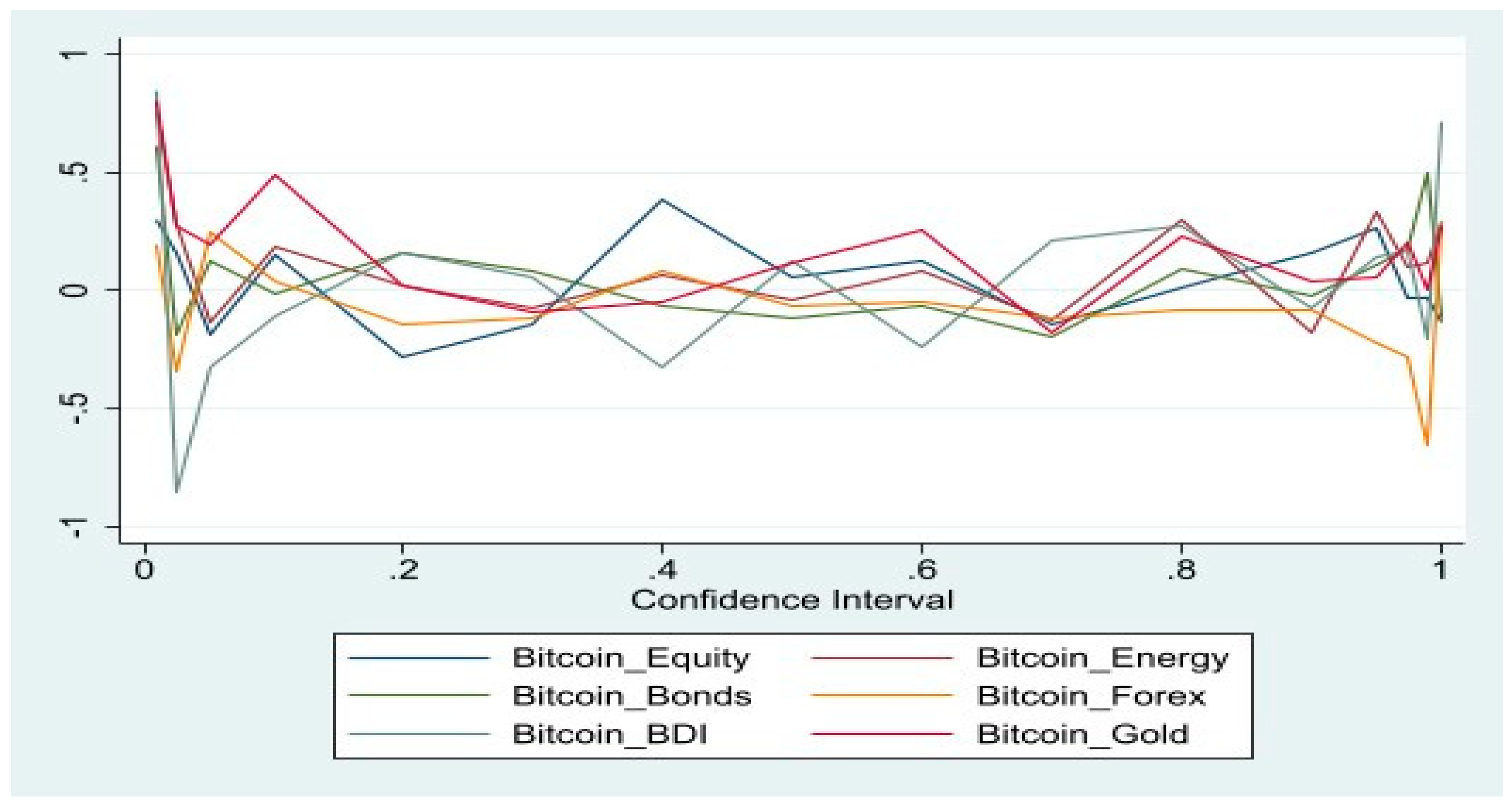

Appendix A. Supplemental Dynamic Conditional Correlation Graphs

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Constraining Framework | Scenario 1 Naïve Portfolio | Scenario 2 Semi-Constrained Max-Long Portfolio | Scenario 3 Semi-Constrained Min-Long Portfolio | Scenario 4 Constrained Portfolio | ||||

| Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | |

| Asset/Index | ||||||||

| Forex | 16.67% | 14.29% | 25.00% | 25.00% | 10.00% | 10.00% | 25.00% | 25.00% |

| Bitcoin | - | 14.29% | - | 2.95% | - | 10.00% | - | 2.95% |

| Baltic Dry Index | 16.67% | 14.29% | 2.65% | 10.31% | 10.00% | 17.66% | 2.65% | 10.31% |

| Equities | 16.67% | 14.29% | 25.00% | 25.00% | 50.00% | 32.34% | 25.00% | 25.00% |

| Energy | 16.67% | 14.29% | 0.36% | −1.99% | 10.00% | 10.00% | 0.36% | −1.99% |

| Corporate Bond | 16.67% | 14.29% | 25.00% | 25.00% | 10.00% | 10.00% | 25.00% | 25.00% |

| Gold | 16.67% | 14.29% | 21.98% | 13.74% | 10.00% | 10.00% | 21.98% | 13.74% |

| Average Returns ( | 0.071% | 0.292% | 0.087% | 0.255% | 0.146% | 0.386% | 0.087% | 0.255% |

| Standard Deviation | 1.97% | 2.58% | 0.90% | 1.64% | 1.76% | 2.81% | 0.90% | 1.64% |

| Sharpe Ratio | 3.58% | 11.29% | 9.68% | 15.57% | 8.28% | 13.74% | 9.68% | 15.57% |

| Constraining Framework | Scenario 5 Risk Parity (Long Only) Portfolio | Scenario 6 Risk Parity (Unconstrained) Portfolio | Scenario 7 Long Only Portfolio | Scenario 8 Unconstrained Portfolio | ||||

| Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | |

| Asset/Index | ||||||||

| Forex | 0.00% | 6.04% | −118.94% | −28.69% | 66.64% | 66.60% | 67.08% | 67.18% |

| Bitcoin | - | 4.90% | - | 8.84% | - | 0.29% | - | 0.44% |

| Baltic Dry Index | 5.84% | 3.14% | 14.60% | 5.53% | 0.28% | 2.40% | 0.39% | 2.61% |

| Equities | 19.76% | 22.75% | 43.20% | 23.08% | 20.59% | 20.25% | 22.62% | 22.96% |

| Energy | 13.00% | 9.95% | 28.62% | 15.21% | 0.00% | 0.00% | −2.34% | −3.16% |

| Corporate Bond | 37.00% | 27.22% | 79.94% | 48.96% | 5.05% | 5.60% | 4.56% | 4.99% |

| Gold | 24.41% | 25.99% | 52.59% | 27.07% | 7.44% | 4.86% | 7.68% | 4.98% |

| Average Returns ( | 0.064% | 0.123% | 0.084% | 0.155% | 0.087% | 0.125% | 0.093% | 0.137% |

| Standard Deviation | 1.37% | 1.36% | 3.61% | 2.06% | 0.48% | 0.60% | 0.51% | 0.65% |

| Sharpe Ratio | 4.67% | 9.03% | 2.34% | 7.49% | 18.11% | 20.83% | 18.35% | 21.14% |

| 1 | Data is available online: https://www.coindesk.com/price/Bitcoin (accessed on 10 June 2021). |

| 2 | Data is available online: https://www.coindesk.com/price/Bitcoin (accessed on 10 June 2021). |

| 3 | Data is available online: https://www.bloomberg.com/quote/BDIY:IND (accessed on 10 May 2020). |

| 4 | Data is available online: https://www.coindesk.com/price/Bitcoin (accessed on 10 June 2021). |

References

- Aggarwal, Shivani, Mayank Santosh, and Prateek Bedi. 2018. Bitcoin and Portfolio Diversification: Evidence from India. In Digital India. Cham: Springer, pp. 99–115. [Google Scholar]

- Andrianto, Yanuar, and Diputra Yoda. 2017. The effect of cryptocurrency on investment portfolio effectiveness. Journal of Finance and Accounting 5: 229–38. [Google Scholar] [CrossRef] [Green Version]

- Baek, Chung, and Matt Elbeck. 2015. Bitcoins as an investment or speculative vehicle? A first look. Applied Economics Letters 22: 30–4. [Google Scholar] [CrossRef]

- Baumöhl, Eduard. 2019. Are cryptocurrencies connected to forex? A quantile cross-spectral approach. Finance Research Letters 29: 363–72. [Google Scholar] [CrossRef]

- Baur, Dirk, and Brian Lucey. 2010. Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. Financial Review 45: 217–29. [Google Scholar] [CrossRef]

- Baur, Dirk, Kihoon Hong, and Adrian Lee. 2018. Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets, Institutions and Money 54: 177–89. [Google Scholar] [CrossRef]

- Beckmann, Joscha, Theo Berger, and Robert Czudaj. 2015. Does gold act as a hedge or a safe haven for stocks? A smooth transition approach. Economic Modelling 48: 16–24. [Google Scholar] [CrossRef] [Green Version]

- Blau, Benjamin. 2017. Price dynamics and speculative trading in Bitcoin. Research in International Business and Finance 41: 493–99. [Google Scholar] [CrossRef]

- Boiko, Viktor, Yelizaveta Tymoshenko, Anna Kononenko, and Dmitrii Goncharov. 2021. The optimization of the cryptocurrency portfolio in view of the risks. Journal of Management Information and Decision Sciences 24: 1–9. [Google Scholar]

- Bouoiyour, Jamal, and Refk Selmi. 2017. The Bitcoin price formation: Beyond the fundamental sources. arXiv arXiv:1707.01284. [Google Scholar]

- Bouoiyour, Jamal, Refk Selmi, Aviral Tiwari, and Olaolu Olayeni. 2016. What drives Bitcoin price. Economics Bulletin 36: 843–50. [Google Scholar]

- Bouri, Elie, Naji Jalkh, Peter Molnár, and David Roubaud. 2017a. Bitcoin for energy commodities before and after the December 2013 crash: Diversifier, hedge or safe haven? Applied Economics 49: 5063–73. [Google Scholar] [CrossRef]

- Bouri, Elie, Peter Molnár, Georges Azzi, David Roubaud, and Lars Hagfors. 2017b. On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters 20: 192–98. [Google Scholar] [CrossRef]

- Bouri, Elie, Rangan Gupta, Aviral Tiwari, and David Roubaud. 2017c. Does Bitcoin hedge global uncertainty? Evidence from wavelet-based quantile-in-quantile regressions. Finance Research Letters 23: 87–95. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Rangan Gupta, Chi Lau, David Roubaud, and Shixuan Wang. 2018. Bitcoin and global financial stress: A copula-based approach to dependence and causality in the quantiles. The Quarterly Review of Economics and Finance 69: 297–307. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Rangan Gupta, and David Roubaud. 2019. Herding behaviour in cryptocurrencies. Finance Research Letters 29: 216–21. [Google Scholar] [CrossRef]

- Bouri, Elie, Syed Shahzad, David Roubaud, Ladislav Kristoufek, and Brian Lucey. 2020. Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis. The Quarterly Review of Economics and Finance 77: 156–64. [Google Scholar] [CrossRef]

- Brauneis, Alexander, and Roland Mestel. 2018. Price discovery of cryptocurrencies: Bitcoin and beyond. Economics Letters 165: 58–61. [Google Scholar] [CrossRef]

- Brian, Domitrovic. 2008. The Dollar—Euro Exchange Rate Sure Is the Most Imporant Price in the World. Forbes. Available online: https://www.forbes.com/sites/briandomitrovic/2018/02/06/the-dollar-euro-exchange-rate-sure-is-the-most-important-price-in-the-world/?sh=171921a2412b (accessed on 10 May 2020).

- Brière, Marie, Kim Oosterlinck, and Ariane Szafarz. 2015. Virtual Currency, Tangible Return: Portfolio Diversification with Bitcoin. Journal of Asset Management 16: 365–73. [Google Scholar] [CrossRef]

- Burnie, Andrew. 2018. Exploring the interconnectedness of cryptocurrencies using correlation networks. arXiv arXiv:1806.06632. [Google Scholar]

- Cai, Xiaoqiang, Kok-Lay Teo, Xiaoqi Yang, and Xun Yu Zhou. 2000. Portfolio optimization under a minimax rule. Management Science 46: 957–72. [Google Scholar] [CrossRef]

- Carrick, Jon. 2016. Bitcoin as a complement to emerging market currencies. Emerging Markets Finance and Trade 52: 2321–34. [Google Scholar] [CrossRef]

- Chan, Wing Hong, Minh Le, and Yan Wendy Wu. 2019. Holding Bitcoin longer: The dynamic hedging abilities of Bitcoin. The Quarterly Review of Economics and Finance 71: 107–13. [Google Scholar] [CrossRef]

- Cheah, Eng-Tuck, and John Fry. 2015. Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of the Bitcoin. Economics Letters 130: 32–36. [Google Scholar] [CrossRef] [Green Version]

- Chung, Pin J., and Donald. J. Liu. 1994. Common stochastic trends in Pacific Rim stock markets. The Quarterly Review of Economics and Finance 34: 241–59. [Google Scholar] [CrossRef]

- Ciaian, Pavel, Miroslava Rajcaniova, and d’Artis Kancs. 2016. The economics of Bitcoin price formation. Applied Economics 48: 1799–815. [Google Scholar] [CrossRef] [Green Version]

- Ciner, Cetin. 2001. On the long run relationship between gold and silver prices A note. Global Finance Journal 12: 299–303. [Google Scholar] [CrossRef]

- Ciner, Cetin, Constantin Gurdgiev, and Brian Lucey. 2013. Hedges and safe havens: An examination of stocks, bonds, gold, oil and exchange rates. International Review of Financial Analysis 29: 202–11. [Google Scholar] [CrossRef]

- Click, Reid, and Michael Plummer. 2005. Stock market integration in ASEAN after the Asian financial crisis. Journal of Asian Economics 16: 5–28. [Google Scholar] [CrossRef]

- Colombo, Jefferson, Fernando Cruz, Luis Paese, and Renan Cortes. 2021. The Diversification Benefits of Cryptocurrencies in Multi-Asset Portfolios: Cross-Country Evidence. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3776260 (accessed on 12 June 2021).

- Conrad, Christian, Anessa Custovic, and Eric Ghysels. 2018. Long-and short-term cryptocurrency volatility components: A GARCH-MIDAS analysis. Journal of Risk and Financial Management 11: 23. [Google Scholar] [CrossRef]

- DeFusco, Richard, John Geppert, and George Tsetsekos. 1996. Long-run diversification potential in emerging stock markets. Financial Review 31: 343–63. [Google Scholar] [CrossRef]

- DeMiguel, Victor, Lorenzo Garlappi, Francisco Nogales, and Raman Uppal. 2009. A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms. Management Science 55: 798–812. [Google Scholar] [CrossRef] [Green Version]

- Deng, Guang-Feng, Woo-Tsong Lin, and Chih-Chung Lo. 2012. Markowitz-based portfolio selection with cardinality constraints using improved particle swarm optimization. Expert Systems with Applications 39: 4558–66. [Google Scholar] [CrossRef]

- Dwyer, Gerald P. 2015. The economics of Bitcoin and similar private digital currencies. Journal of Financial Stability 17: 81–91. [Google Scholar] [CrossRef] [Green Version]

- Dyhrberg, Anne Haubo. 2016a. Hedging capabilities of bitcoin. Is it the virtual gold? Finance Research Letters 16: 139–44. [Google Scholar] [CrossRef] [Green Version]

- Dyhrberg, Anne Haubo. 2016b. Bitcoin, gold and the dollar—A GARCH volatility analysis. Finance Research Letters 16: 85–92. [Google Scholar] [CrossRef] [Green Version]

- Dyhrberg, Anne Haubo, Sean Foley, and Jiri Svec. 2018. How investible is Bitcoin? Analyzing the liquidity and transaction costs of Bitcoin markets. Economics Letters 171: 140–43. [Google Scholar] [CrossRef]

- Ehrgott, Matthias, Kathrin Klamroth, and Christian Schwehm. 2004. An MCDM approach to portfolio optimization. European Journal of Operational Research 155: 752–70. [Google Scholar] [CrossRef]

- Eisl, Alexander, Stephan Gasser, and Stephan Weinmayer. 2015. Caveat Emptor: Does Bitcoin Improve Portfolio Diversification? Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2408997 (accessed on 8 June 2021).

- Ferson, Wayne, Suresh Nallareddy, and Biqin Xie. 2013. The “out-of-sample” performance of long run risk models. Journal of Financial Economics 107: 537–56. [Google Scholar] [CrossRef]

- Gaivoronski, Alexei, and Georg Pflug. 2005. Value-at-risk in portfolio optimization: Properties and computational approach. The Journal of Risk 7: 1–31. [Google Scholar] [CrossRef] [Green Version]

- Gangwal, Shashwat. 2017. Analyzing the effects of adding Bitcoin to portfolio. International Journal of Economics and Management Engineering 10: 3519–32. [Google Scholar]

- Garcia, David, Claudio Tessone, Pavlin Mavrodiev, and Nicolas Perony. 2014. The digital trace of bubbles: Feedback cycles between socio-economic signals in the Bitcoin economy. Journal of the Royal Society Interface 11: 623–31. [Google Scholar] [CrossRef] [PubMed]

- Garcia-Jorcano, Laura, and Sonia Benito. 2020. Studying the properties of the Bitcoin as a diversifying and hedging asset through a copula analysis: Constant and time-varying. Research in International Business and Finance 54: 1–24. [Google Scholar] [CrossRef]

- Glaser, Florian, Kai Zimmermann, Martin Haferkorn, Moritz Christian Weber, and Michael Siering. 2014. Bitcoin-Asset or Currency? Revealing Users’ Hidden Intentions. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2425247 (accessed on 25 May 2020).

- Guesmi, Khaled, Samir Saadi, Ilyes Abid, and Zied Ftiti. 2019. Portfolio diversification with virtual currency: Evidence from bitcoin. International Review of Financial Analysis 63: 431–37. [Google Scholar] [CrossRef]

- Ivanova, Miroslava, and Lilko Dospatliev. 2017. Application of Markowitz portfolio optimization on Bulgarian stock market from 2013 to 2016. International Journal of Pure and Applied Mathematics 117: 291–307. [Google Scholar] [CrossRef] [Green Version]

- Jagannathan, Ravi, and Tongshu Ma. 2003. Risk reduction in large portfolios: Why imposing the wrong constraints helps. The Journal of Finance 58: 1651–83. [Google Scholar] [CrossRef] [Green Version]

- Jeribi, Ahmed, and Mohamed Fakhfekh. 2021. Portfolio management and dependence structure between cryptocurrencies and traditional assets: Evidence from FIEGARCH-EVT-Copula. Journal of Asset Management 22: 224–39. [Google Scholar] [CrossRef]

- Ji, Qiang, Elie Bouri, Rangan Gupta, and David Roubaud. 2018. Network causality structures among Bitcoin and other financial assets: A directed acyclic graph approach. The Quarterly Review of Economics and Finance 70: 203–13. [Google Scholar] [CrossRef] [Green Version]

- Kajtazi, Anton, and Andrea Moro. 2017. Bitcoin, portfolio diversification and Chinese financial Markets. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3062064 (accessed on 15 May 2020).

- Kajtazi, Anton, and Andrea Moro. 2019. The role of bitcoin in well diversified portfolios: A comparative global study. International Review of Financial Analysis 61: 143–57. [Google Scholar] [CrossRef] [Green Version]

- Kandel, Shmuel, and Robert Stambaugh. 1987. On correlations and inferences about mean-variance efficiency. Journal of Financial Economics 18: 61–90. [Google Scholar] [CrossRef]

- Karalevicius, Vytautas, Niels Degrande, and Jochen De Weerdt. 2018. Using sentiment analysis to predict interday Bitcoin price movements. The Journal of Risk Finance 19: 56–7. [Google Scholar] [CrossRef]

- Kaul, Aditya, and Sapp Stephen. 2006. Y2K fears and safe haven trading of the US dollar. Journal of International Money and Finance 25: 760–79. [Google Scholar] [CrossRef]

- Khaki, Audil, Somar Al-Mohamad, Walid Bakry, and Samet Gunay. 2020. Can Cryptocurrencies Be the Future Safe-Haven for Investors? A Case Study of Bitcoin. Working Paper. SSRN-ID 3593508. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3593508 (accessed on 30 October 2020).

- Koutmos, Dimitrios. 2018. Bitcoin returns and transaction activity. Economics Letters 167: 81–85. [Google Scholar] [CrossRef]

- Kristoufek, Ladislav. 2015. What are the main drivers of the Bitcoin price? Evidence from wavelet coherence analysis. PLoS ONE 10: e0123923. [Google Scholar] [CrossRef]

- Krokhmal, Pavlo, Palmquist Jonas, and Uryasev Stanislav. 2002. Portfolio optimization with conditional value-at-risk objective and constraints. Journal of Risk 4: 43–68. [Google Scholar] [CrossRef] [Green Version]

- Lee, Wai. 2011. Risk-based asset allocation: A new answer to an old question? The Journal of Portfolio Management 37: 11–28. [Google Scholar] [CrossRef]

- Luther, William, and Alexander Salter. 2017. Bitcoin and the bailout. The Quarterly Review of Economics and Finance 66: 50–56. [Google Scholar] [CrossRef]

- Ma, Yechi, Ferhana Ahmad, Miao Liu, and Zilong Wang. 2020. Portfolio optimization in the era of digital financialization using cryptocurrencies. Technological Forecasting and Social Change 161: 1–11. [Google Scholar] [CrossRef]

- Markowitz, Harry. 1952. Portfolio Selection. Journal of Finance 7: 77–91. [Google Scholar]

- Markowitz, Harry. 1958. Portfolio Selection: Efficient Diversification of Investments. New York: John Wiley & Sons. [Google Scholar]

- Mazanec, Jaroslav. 2021. Portfolio Optimalization on Digital Currency Market. Journal of Risk and Financial Management 14: 160. [Google Scholar] [CrossRef]

- Mendes, R. R. A., A. P. Paiva, Rogério Santana Peruchi, Pedro Paulo Balestrassi, Rafael Coradi Leme, and M. B. Silva. 2016. Multiobjective portfolio optimization of ARMA–GARCH time series based on experimental designs. Computers & Operations Research 66: 434–44. [Google Scholar]

- Miyazaki, Takashi, and Shigeyuki Hamori. 2014. Cointegration with regime shift between gold and financial variables. International Journal of Financial Research 5: 90–7. [Google Scholar] [CrossRef] [Green Version]

- Nadarajah, Saralees, and Jeffrey Chu. 2017. On the inefficiency of Bitcoin. Economics Letters 150: 6–9. [Google Scholar] [CrossRef] [Green Version]

- Nakamoto, Satoshi. 2008. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://nakamotoinstitute.org/bitcoin (accessed on 12 June 2021).

- Ngene, Geoffrey, Jordin Post, and Ann Mungai. 2018. Volatility and shock interactions and risk management implications: Evidence from the US and frontier markets. Emerging Markets Review 37: 181–98. [Google Scholar] [CrossRef]

- Nguyen, Sang Phu, and Toan Luu Duc Huynh. 2019. Portfolio optimization from a Copulas-GJRGARCH-EVT-CVAR model: Empirical evidence from ASEAN stock indexes. Quantitative Finance and Economics 3: 562–85. [Google Scholar] [CrossRef]

- Ozturk, Serda Selin. 2020. Dynamic Connectedness between Bitcoin, Gold, and Crude Oil Volatilities and Returns. Journal of Risk and Financial Management 13: 275. [Google Scholar] [CrossRef]

- Pal, Debdatta, and Subrata Mitra. 2019. Hedging bitcoin with other financial assets. Finance Research Letters 30: 30–36. [Google Scholar] [CrossRef]

- Pho, Kim Hung, Sel Ly, Richard Lu, Thi Hong Van Hoang, and Wing-Keung Wong. 2021. Is Bitcoin a better portfolio diversifier than gold? A copula and sectoral analysis for China. International Review of Financial Analysis 74: 1–30. [Google Scholar] [CrossRef]

- Platanakis, Emmanouil, and Andrew Urquhart. 2019. Portfolio management with cryptocurrencies: The role of estimation risk. Economics Letters 177: 76–80. [Google Scholar] [CrossRef] [Green Version]

- Platanakis, Emmanouil, and Andrew Urquhart. 2020. Should investors include bitcoin in their portfolios? A portfolio theory approach. The British Accounting Review 52: 1–19. [Google Scholar] [CrossRef]

- Pooter, Michiel de, Martin Martens, and Dick Van Dijk. 2008. Predicting the daily covariance matrix for S&P 100 stocks using intraday data—But which frequency to use? Econometric Reviews 27: 199–229. [Google Scholar]

- Reboredo, Juan. 2013. Is gold a hedge or safe haven against oil price movements? Resources Policy 38: 130–37. [Google Scholar] [CrossRef]

- Selmi, Refik, Walid Mensi, Shawkat Hammoudeh, and Jamal Bouoiyour. 2018. Is Bitcoin a hedge, a safe haven or a diversifier for oil price movements? A comparison with gold. Energy Economics 74: 787–801. [Google Scholar] [CrossRef]

- Shahzad, Syed Jawad Hussain, Elie Bouri, David Roubaud, Ladislav Kristoufek, and Brian Lucey. 2019. Is Bitcoin a better safe-haven investment than gold and commodities? International Review of Financial Analysis 63: 322–30. [Google Scholar] [CrossRef]

- Sharpe, William. 1963. A simplified model for portfolio analysis. Management Science 9: 277–93. [Google Scholar] [CrossRef] [Green Version]

- Symitsi, Efthymia, and Konstantinos Chalvatzis. 2019. The economic value of Bitcoin: A portfolio analysis of currencies, gold, oil and stocks. Research in International Business and Finance 48: 97–110. [Google Scholar] [CrossRef] [Green Version]

- Tan, Boon Seng, and Kin Yew Low. 2017. Bitcoin—Its economics for financial reporting. Australian Accounting Review 27: 220–27. [Google Scholar] [CrossRef]

- Wang, Jinghua, and Geoffrey Ngene. 2020. Does Bitcoin still own the dominant power? An intraday analysis. International Review of Financial Analysis 71: 1–12. [Google Scholar] [CrossRef]

- Wątorek, Marcin, Stanislaw Drożdż, Jaroslaw Kwapień, Ludovico Minati, Pawel Oświęcimka, and Marek Stanuszek. 2021. Multiscale characteristics of the emerging global cryptocurrency market. Physics Reports 901: 1–82. [Google Scholar] [CrossRef]

- Wei, Wang Chun. 2018. The impact of Tether grants on Bitcoin. Economics Letters 171: 19–22. [Google Scholar] [CrossRef]

- Williamson, Stephen. 2018. Is Bitcoin a Waste of Resources? Rev. Federal Reserve Bank St.Louis 100: 107–15. [Google Scholar] [CrossRef]

- Wu, Chen, and Vivek Pandey. 2014. The value of Bitcoin in enhancing the efficiency of an investor’s portfolio. Journal of Financial Planning 27: 44–52. [Google Scholar]

- Yi, Shuyue, Zishuang Xu, and Gang-Jin Wang. 2018. Volatility connectedness in the cryptocurrency market: Is Bitcoin a dominant cryptocurrency? International Review of Financial Analysis 60: 98–114. [Google Scholar] [CrossRef]

| Variable/Index/Asset | Mnemonics | Indices and Definition |

|---|---|---|

| Exchange Rate/Forex | US $CWBN | US Nominal Dollar Broad Index, representing the number of US dollars for 1 Euro. The USD–Euro exchange rate is considered the most important indicator of Forex markets in the world. The importance of the USD–Euro exchange rate is due to the investment and trade of these two large economic areas with one another. The trade and investment among the two regions is such that the prices in these economic regions are arbitraged against the exchange rate (Brian 2008). |

| Economic Activity | BALTICF | Baltic Exchange Dry Index (BDI). The BDI provides insights into global supply and demand trends and is considered an indicator of global economic activity. The Index was first started in January 1985 by the London-based Baltic Exchange. The BDI is a composite of the Capesize, Panamax, Handysize, and Supramax subindices.3 It measures the changes in the cost of transporting raw materials across more than 20 different sea routes. |

| Bitcoin | BTCTOU$ | USD to Bitcoin (Bitstamp). Bitcoin is a special kind of asset called cryptocurrency and has the highest market capitalization of all cryptocurrencies. The market capitalization of Bitcoin currently sits at USD 690 billion as of 10 June 2021.4 |

| Stock Market | SBBUSD$ | Standard and Poor’s United States Broad Market Index (BMI). The S&P 500 is considered the best representation of the US stock market. The S&P 500 Index is one of the most used proxies for the stock market and captures the performance of 500 large companies listed on the US stock exchanges. |

| Energy Market | DJUBENS | Formerly known as the Dow Jones–UBS Energy Spot Subindex (DJUBENS), this index measures the price movements of energy included in the Bloomberg CI and select subindexes. |

| Corporate Bond | U:IGLB | iShares Long-Term Corporate Bond ETF. The iShares Long-Term Corporate Bond ETF seeks to track the investment results of an index composed of US dollar-denominated, investment-grade corporate bonds with remaining maturities greater than ten years. |

| Gold | NGCC.01 | CMX-Gold 100 Ounce TRC1. This index quotes the price of 100 ounces of 0.995 fine (24-karat) gold in US dollars. |

| BDI | Bitcoin | Bonds | Energy | Equity | Forex | Gold | |

|---|---|---|---|---|---|---|---|

| Mean | 0.001248 | 0.016187 | 0.000290 | −0.000354 | 0.002588 | 0.000483 | −0.000022 |

| Median | 0.001340 | 0.009284 | 0.001238 | 0.000430 | 0.003559 | 0.000300 | 0.000526 |

| Maximum | 0.470774 | 0.665419 | 0.083595 | 0.158034 | 0.160962 | 0.042156 | 0.061457 |

| Minimum | −0.335448 | −0.919529 | −0.110510 | −0.236569 | −0.153451 | −0.022924 | −0.144423 |

| Std. Dev. | 0.099 | 0.127 | 0.014 | 0.038 | 0.023 | 0.007 | 0.022 |

| Sharpe Ratio | 1.26% | 12.71% | 2.05% | −0.91% | 10.88% | 6.62% | −0.10% |

| Skewness | 0.138 | −0.426 | −1.079 | −0.558 | −0.550 | 0.634 | −1.071 |

| Kurtosis | 4.491 | 11.502 | 15.517 | 6.341 | 12.781 | 6.194 | 8.567 |

| Jarque–Bera | 48.674 | 1545.651 | 3415.117 | 262.738 | 2050.655 | 250.075 | 753.402 |

| Probability | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Forex | BDI | Bitcoin | Equity | Energy | Bonds | Gold | |

|---|---|---|---|---|---|---|---|

| Forex | 1.000 | ||||||

| BDI | 0.000 | 1.000 | |||||

| Bitcoin | −0.029 | −0.004 | 1.000 | ||||

| Equity | −0.447 | 0.044 | 0.107 | 1.000 | |||

| Energy | −0.287 | 0.129 | 0.082 | 0.367 | 1.000 | ||

| Bonds | −0.325 | −0.050 | 0.058 | 0.177 | −0.006 | 1.000 | |

| Gold | −0.410 | −0.076 | 0.179 | 0.018 | 0.023 | 0.335 | 1.000 |

| Constraining Framework | Scenario 1 Naïve Portfolio | Scenario 2 Semi-Constrained Max-Long Portfolio | Scenario 3 Semi-Constrained Min-Long Portfolio | Scenario 4 Constrained Portfolio | ||||

|---|---|---|---|---|---|---|---|---|

| Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | |

| Bitcoin Weight | - | 14.29% | - | 2.95% | - | 10.00% | - | 2.95% |

| Average Returns ( | 0.071% | 0.292% | 0.087% | 0.255% | 0.146% | 0.386% | 0.087% | 0.255% |

| Standard Deviation | 1.97% | 2.58% | 0.90% | 1.64% | 1.76% | 2.81% | 0.90% | 1.64% |

| Sharpe Ratio | 3.58% | 11.29% | 9.68% | 15.57% | 8.28% | 13.74% | 9.68% | 15.57% |

| HS VaR (95%) | 3.03% | 3.77% | 1.12% | 2.09% | 2.70% | 3.93% | 1.12% | 2.09% |

| HS VaR (99%) | 4.69% | 6.71% | 2.39% | 4.23% | 4.69% | 7.07% | 2.39% | 4.23% |

| VCV VaR (95%) | 3.17% | 3.96% | 1.39% | 2.44% | 2.75% | 4.23% | 1.39% | 2.44% |

| VCV VaR (99%) | 4.51% | 5.72% | 2.00% | 3.55% | 3.95% | 6.15% | 2.00% | 3.55% |

| HS CVaR (95%) | 4.25% | 5.88% | 1.98% | 3.66% | 3.97% | 6.37% | 1.98% | 3.66% |

| HS CVaR (99%) | 5.61% | 10.22% | 3.89% | 7.85% | 6.91% | 12.28% | 3.89% | 7.85% |

| VCV CVaR (95%) | 3.96% | 4.99% | 1.74% | 3.09% | 3.45% | 5.35% | 1.74% | 3.09% |

| VCV CVaR (99%) | 5.06% | 6.43% | 2.24% | 4.00% | 4.44% | 6.92% | 2.24% | 4.00% |

| Probability of Loss (HS) | 48.82% | 41.34% | 41.93% | 39.37% | 43.31% | 39.76% | 41.93% | 39.37% |

| Portfolio Framework | Scenario 1 Naïve Portfolio | Scenario 2 Semi-Constrained Max-Long Portfolio | Scenario 3 Semi-Constrained Min-Long Portfolio | Scenario 4 Constrained Portfolio | ||||

|---|---|---|---|---|---|---|---|---|

| Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | |

| Average Returns ( | 0.065% | 0.28% | 0.083% | 0.23% | 0.138% | 0.37% | 0.087% | 0.26% |

| Standard Deviation | 1.98% | 2.57% | 0.89% | 1.64% | 1.77% | 2.82% | 0.90% | 1.65% |

| Sharpe Ratio | 3.28% | 10.90% | 9.30% | 13.94% | 7.79% | 13.29% | 9.67% | 15.52% |

| MC CVaR (95%) | 3.97% | 4.97% | 1.74% | 3.12% | 3.48% | 5.38% | 1.75% | 3.12% |

| MC CVaR (99%) | 5.08% | 6.41% | 2.24% | 4.03% | 4.47% | 6.95% | 2.26% | 4.04% |

| Probability of Loss (MC) | 48.72% | 45.45% | 46.06% | 44.21% | 47.26% | 44.26% | 46.17% | 43.68% |

| Constraining Framework | Scenario 5 Risk Parity (Long Only) Portfolio | Scenario 6 Risk Parity (Unconstrained) Portfolio | Scenario 7 Long Only Portfolio | Scenario 8 Unconstrained Portfolio | ||||

|---|---|---|---|---|---|---|---|---|

| Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | |

| Bitcoin Weight | - | 4.90% | - | 8.84% | - | 0.29% | - | 0.44% |

| Average Returns ( | 0.064% | 0.123% | 0.084% | 0.155% | 0.087% | 0.125% | 0.093% | 0.137% |

| Standard Deviation | 1.37% | 1.36% | 3.61% | 2.06% | 0.48% | 0.60% | 0.51% | 0.65% |

| Sharpe Ratio | 4.67% | 9.03% | 2.34% | 7.49% | 18.11% | 20.83% | 18.35% | 21.14% |

| HS VaR (95%) | 1.89% | 1.68% | 5.37% | 2.90% | 0.58% | 0.76% | 0.65% | 0.48% |

| HS VaR (99%) | 3.44% | 3.78% | 8.39% | 5.31% | 1.52% | 2.14% | 1.48% | 1.75% |

| VCV VaR (95%) | 2.19% | 2.11% | 5.85% | 3.24% | 0.70% | 0.86% | 0.74% | 0.93% |

| VCV VaR (99%) | 3.12% | 3.04% | 8.31% | 4.65% | 1.03% | 1.27% | 1.09% | 1.37% |

| HS CVaR (95%) | 3.10% | 3.09% | 8.13% | 4.62% | 1.03% | 1.33% | 1.07% | 1.39% |

| HS CVaR (99%) | 5.23% | 6.08% | 14.10% | 8.63% | 1.93% | 2.79% | 1.86% | 2.82% |

| VCV CVaR (95%) | 2.74% | 2.65% | 7.28% | 4.06% | 0.90% | 1.10% | 0.95% | 1.19% |

| VCV CVaR (99%) | 3.50% | 3.41% | 9.30% | 5.21% | 1.16% | 1.44% | 1.23% | 1.55% |

| Probability of Loss (HS) | 48.82% | 43.11% | 48.03% | 45.87% | 41.54% | 39.37% | 41.73% | 37.99% |

| Portfolio Framework | Scenario 5 Risk Parity (Long Only) Portfolio | Scenario 6 Risk Parity (Unconstrained) Portfolio | Scenario 7 Long Only Portfolio | Scenario 8 Unconstrained Portfolio | ||||

|---|---|---|---|---|---|---|---|---|

| Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | Without Bitcoin | With Bitcoin | |

| Average Returns ( | 0.043% | 0.12% | 0.070% | 0.14% | 0.084% | 0.13% | 0.094% | 0.15% |

| Standard Deviation | 1.35% | 1.33% | 3.65% | 2.06% | 0.48% | 0.60% | 0.51% | 0.65% |

| Sharpe Ratio | 3.21% | 9.33% | 1.92% | 7.02% | 17.53% | 20.99% | 18.60% | 22.38% |

| MC CVaR (95%) | 2.72% | 2.60% | 7.38% | 4.07% | 0.89% | 1.10% | 0.94% | 1.19% |

| MC CVaR (99%) | 3.48% | 3.34% | 9.42% | 5.22% | 1.16% | 1.44% | 1.22% | 1.55% |

| Probability of Loss (MC) | 48.82% | 46.18% | 49.99% | 47.43% | 42.67% | 44.27% | 42.31% | 41.62% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bakry, W.; Rashid, A.; Al-Mohamad, S.; El-Kanj, N. Bitcoin and Portfolio Diversification: A Portfolio Optimization Approach. J. Risk Financial Manag. 2021, 14, 282. https://doi.org/10.3390/jrfm14070282

Bakry W, Rashid A, Al-Mohamad S, El-Kanj N. Bitcoin and Portfolio Diversification: A Portfolio Optimization Approach. Journal of Risk and Financial Management. 2021; 14(7):282. https://doi.org/10.3390/jrfm14070282

Chicago/Turabian StyleBakry, Walid, Audil Rashid, Somar Al-Mohamad, and Nasser El-Kanj. 2021. "Bitcoin and Portfolio Diversification: A Portfolio Optimization Approach" Journal of Risk and Financial Management 14, no. 7: 282. https://doi.org/10.3390/jrfm14070282

APA StyleBakry, W., Rashid, A., Al-Mohamad, S., & El-Kanj, N. (2021). Bitcoin and Portfolio Diversification: A Portfolio Optimization Approach. Journal of Risk and Financial Management, 14(7), 282. https://doi.org/10.3390/jrfm14070282