Modelling Systemically Important Banks vis-à-vis the Basel Prudential Guidelines

Abstract

:1. Introduction

2. Literature Review

2.1. Theoretical Approaches on Systemically Important Banks

2.2. Standards Guideline

3. Data and Methodology

3.1. Source of Data

3.2. Model Estimation

- Conditional Value at Risk (CoVaR)

- 2.

- Marginal Expected Shortfall (MES)

- 3.

- Systemic Risk Measure (SRISK)

- Wi,t = market value of equity;

- Di,t = book value of debt;

- Ai,t = book value of assets;

- k = prudential capital fraction, which is set to 8%.

- 4.

- Basel-Indicator-Based Approach

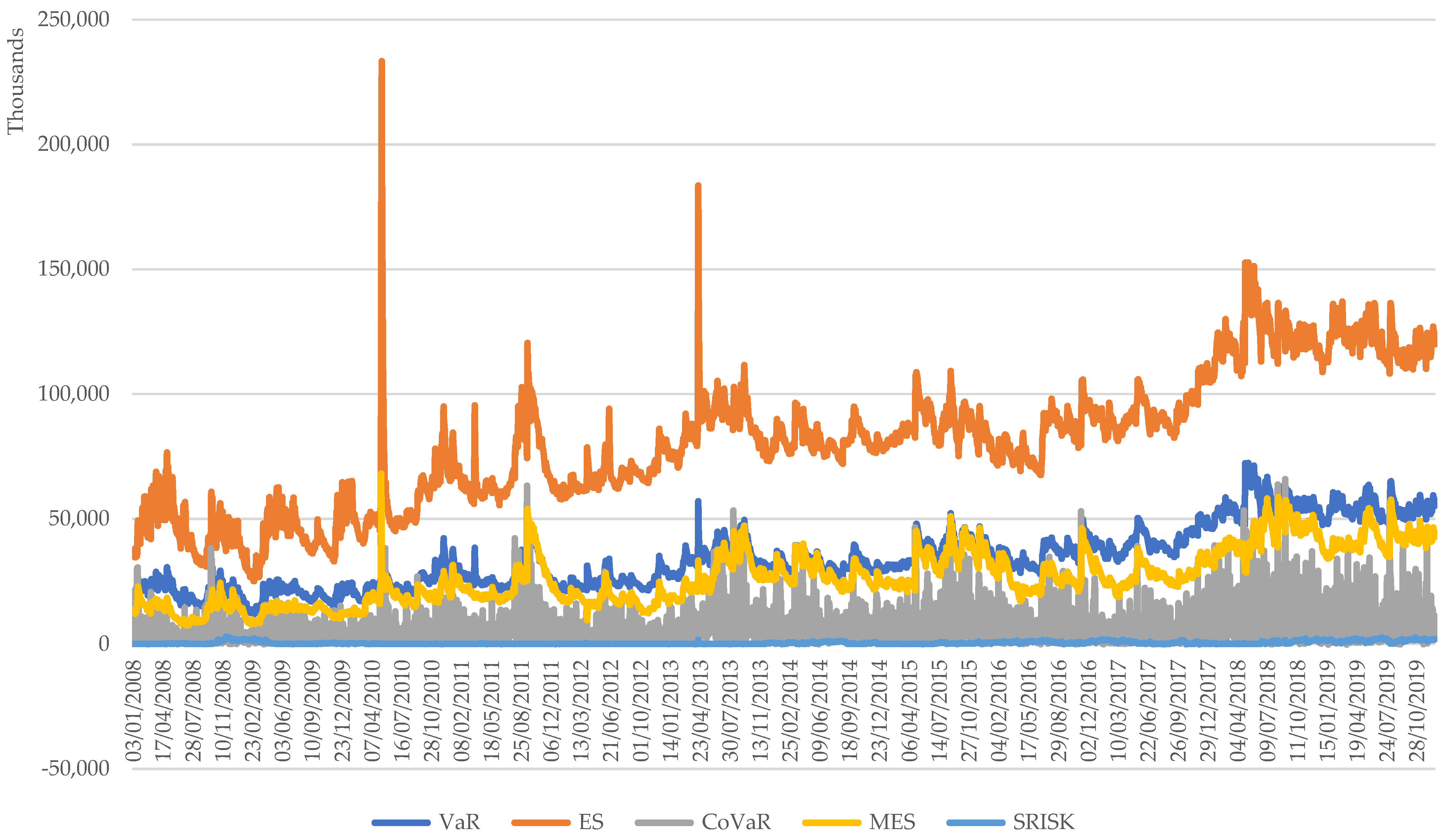

4. Results

4.1. CoVaR

4.2. Marginal Expected Shortfall (MES)

4.2.1. Systemic Risk Measure (SRISK)

4.2.2. Basel-Indicator-Based Approach

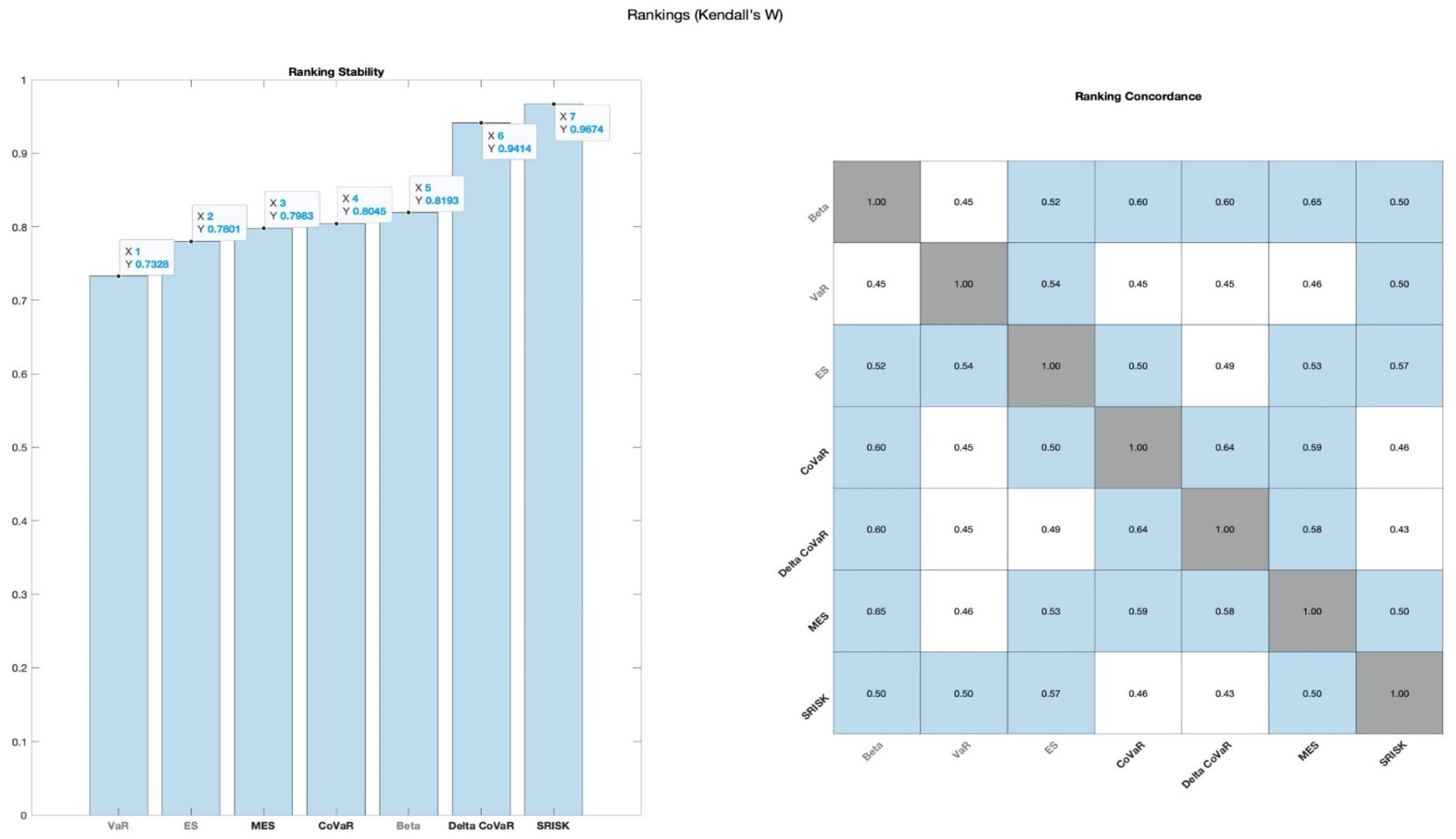

4.2.3. Strengths and Weaknesses

5. Conclusions and Policy Recommendation

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Robustness Test

- 1.

- Impute 3-month T-bill data

| Variable | Obs | Mean | Std. Dev. | Min | Max |

| Date | 2971 | 19,749.43 | 1269.313 | 17,533 | 21913 |

| MOLIBOR | 2971 | 1.024651 | 0.9536291 | 0.22285 | 4.81875 |

| MOTBILL | 2302 | 6.084313 | 1.474008 | 3.721 | 11.55471 |

| YRTBOND | 2971 | 8.188854 | 2.028928 | 5.047 | 20.955 |

| INDOJIBON | 2971 | 5.608955 | 1.373478 | 3.20861 | 11.97222 |

| JIBOR1W | 2971 | 5.944626 | 1.349811 | 3.8044 | 10.50028 |

| JIBOR1MO | 2971 | 6.590463 | 1.443273 | 3.9716 | 11.79167 |

| JIBOR3MO | 2971 | 6.986121 | 1.470088 | 4.19 | 12.59722 |

| JIBOR6MO | 2971 | 7.291413 | 1.503186 | 4.4196 | 13.44444 |

| JIBOR12MO | 2971 | 7.53949 | 1.530414 | 4.82 | 14.25 |

| Obs<. | ||||||

| Variable | Obs=. | Obs>. | Obs<. | Unique Values | Min | Max |

| Date | 2971 | >500 | 17,533 | 21,913 | ||

| MOLIBOR | 2971 | >500 | 22,285 | 4.8187 | ||

| MOTBILL | 669 | 2302 | >500 | 3.721 | 11.5547 | |

| YRTBOND | 2971 | >500 | 5047 | 20.955 | ||

| INDOJIBON | 2971 | >500 | 3.2086 | 11.9722 | ||

| JIBOR1W | 2971 | >500 | 3.8044 | 10.5002 | ||

| JIBOR1MO | 2971 | >500 | 3.9716 | 11.7916 | ||

| JIBOR3MO | 2971 | >500 | 4.19 | 12.5972 | ||

| JIBOR6MO | 2971 | >500 | 4.4196 | 13.4444 | ||

| JIBOR12MO | 2971 | >500 | 4.82 | 14.25 |

| Univariate imputation | Imputations = | 660 |

| Linear regression | added = | 660 |

| Imputed: m = 1 through m = 660 | updated = | 0 |

{kind=link}

{kind=link}

| Variable | Observations per m | |||

|---|---|---|---|---|

| Complete | Incomplete | Imputed | Total | |

| MOTBILL | 2302 | 669 | 669 | 2971 |

- 2.

- Basel-indicator-based approach

| Bank | Size | Interconnectedness | Complexity | Total Systemic Score |

| 33.3% | 33.3% | 33.3% | ||

| A | 1732 | 937 | 705 | 1125 |

| B | 1030 | 341 | 273 | 548 |

| ….. | ….. | ….. | ….. | ….. |

| ….. | ….. | ….. | ….. | ….. |

| Z | 217 | 53 | 23 | 98 |

| Total system | 10,000 | 10,000 | 10,000 | 10,000 |

- 3.

- Spearman rho correlation

| CoVaR15 | CoVaR16 | CoVaR17 | CoVaR18 | Mes15 | Mes16 | Mes17 | Mes18 | Srisk15 | Srisk16 | Srisk17 | Srisk18 | Bsl15 | Bsl16 | Bsl17 | Bsl18 | |

| CoVaR15 | 1.0000 | |||||||||||||||

| CoVaR16 | −0.0857 | 1.0000 | ||||||||||||||

| CoVaR17 | 0.7714 | −0.2000 | 1.0000 | |||||||||||||

| CoVaR18 | 0.8286 | 0.0857 | 0.9429 | 1.0000 | ||||||||||||

| Mes15 | −1.0000 | −1.0000 | −0.8000 | −0.8000 | 1.0000 | |||||||||||

| Mes16 | −0.6000 | −0.7000 | −0.2000 | −0.6000 | 0.4000 | 1.0000 | ||||||||||

| Mes17 | −0.8000 | −0.8000 | −0.6000 | −0.6000 | −0.1000 | 0.8000 | 1.0000 | |||||||||

| Mes18 | −0.5000 | −0.5000 | −0.6000 | 0.5000 | 0.7000 | 0.6571 | 0.5000 | 1.0000 | ||||||||

| Srisk15 | −1.0000 | −1.0000 | 0.5000 | −1.0000 | 0.0000 | 0.8000 | 1.0000 | 1.0000 | 1.0000 | |||||||

| Srisk16 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.5000 | 1.0000 | 0.5000 | −0.4000 | 1.0000 | ||||||

| Srisk17 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | −1.0000 | −1.0000 | −1.0000 | −1.0000 | −1.000 | 1.0000 | |||||

| Srisk18 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 1.0000 | 1.0000 | 1.0000 | −0.2000 | 0.8000 | −1.0000 | 1.0000 | ||||

| Bsl15 | 0.4000 | 0.4000 | 0.0000 | 0.0000 | 0.6000 | −0.8000 | −0.3714 | 0.5000 | −1.0000 | 1.0000 | 0.0000 | 1.0000 | 1.0000 | |||

| Bsl16 | 0.4000 | 0.4000 | 0.0000 | 0.0000 | 0.6000 | −0.7000 | −0.9000 | 0.0286 | 0.5000 | −0.5000 | 0.0000 | 0.5000 | 0.9833 | 1.0000 | ||

| Bsl17 | 0.4000 | 0.4000 | 0.0000 | 0.0000 | 0.6000 | −0.7000 | −0.9000 | 0.2571 | 0.5000 | −0.5000 | 0.0000 | 0.5000 | 0.9500 | 0.9515 | 1.0000 | |

| Bsl18 | 0.4000 | 0.4000 | 0.0000 | 0.0000 | 0.6000 | −0.7000 | −0.9000 | 0.2571 | 0.5000 | −0.5000 | 0.0000 | 0.5000 | 0.9500 | 0.9515 | 1.0000 | 1.0000 |

| 1 | The Basel Committee on Banking Supervision agreed to review the framework every 3 years. As a result, the standard was revised in July 2013, and the latest update was issued in July 2018. |

References

- Acharya, Viral, Robert Engle, and Matthew Richardson. 2012. Capital Shortfall: A New Approach to Ranking and Regulating Systemic Risks. American Economic Review 102: 59–64. [Google Scholar] [CrossRef] [Green Version]

- Acharya, Viral V., Lasse H. Pedersen, Thomas Philippon, and Matthew Richardson. 2017. Measuring Systemic Risk. Review of Financial Studies 30: 2–47. [Google Scholar] [CrossRef]

- Adrian, Tobias, and Markus K. Brunnermeier. 2016. CoVaR. American Economic Review 106: 1705–41. [Google Scholar] [CrossRef]

- Akhter, Selim, and Kevin Daly. 2017. Contagion risk for Australian banks from global systemically important banks: Evidence from extreme events. Economic Modelling 63: 191–205. [Google Scholar] [CrossRef]

- Allen, Franklin, and Douglas Gale. 2000. Financial Contagion. Journal of Political Economy 108: 1–33. [Google Scholar] [CrossRef]

- Ayomi, Sri, and Bambang Hermanto. 2013. Systemic Risk and Financial Linkages Measurement in the Indonesian Banking. Bulletin of Monetary Economics and Banking 16: 91–114. [Google Scholar] [CrossRef]

- Bank Indonesia. 2014. PBI No.16/11/PBI/2014 Tentang Pengaturan dan Pengawasan Makroprudensial. Jakarta: Bank Indonesia. [Google Scholar]

- BCBS. 2010. An Assessment of the Long-Term Economic Impact of Stronger Capital and Liquidity Requirement. Basel: Bank for International Settlements. [Google Scholar]

- BCBS. 2011. Global Systemically Important Banks: Assessment Methodology and the Additional Loss Absorbency Requirement. Basel: Bank for International Settlements. [Google Scholar]

- BCBS. 2012. A Framework for Dealing with Domestic Systemically Important Banks. Basel: Bank for International Settlements. [Google Scholar]

- BCBS. 2013. Global Systemically Important Banks: Updated Assessment Methodology and the Higher Loss Absorbency Requirement. Basel: Bank for International Settlements. [Google Scholar]

- BCBS. 2014. The G-SIB Assessment Methodology—Score Calculation. Basel: Bank for International Settlements. [Google Scholar]

- BCBS. 2018. Global Systemically Important Banks: Revised Assessment Methodology and the Higher Loss Absorbency Requirement. Basel: Bank for International Settlements. [Google Scholar]

- Belluzzo, Tommaso. 2020. Systemic Risk. Available online: https://github.com/TommasoBelluzzo/SystemicRisk/releases/tag/v3.0.0 (accessed on 5 November 2020).

- Bengtsson, Elias, Ulf Holmberg, and Kristian Jonsson. 2013. Identifying Systemically Important Banks in Sweden—What do Quantitative Indicators Tell Us? Stockholm: Sveriges Riksbank. [Google Scholar]

- Benoit, Sylvain, Gilbert Colletaz, and Christophe Hurlin. 2011. A Theoretical and Empirical Comparison of Systemic Risk Measures: MES versus CoVaR. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Billio, Monica, Mila Getmansky, Andrew W. Lo, and Loriana Pelizzon. 2012. Econometric measures of connectedness and systemic risk in the finance and insurance sectors. Journal of Financial Economics 104: 535–59. [Google Scholar] [CrossRef]

- Bisias, Dimitrios, Mark Flood, Andrew W. Lo, and Stavros Valavanis. 2012. A Survey of Systemic Risk Analytics. Annual Review of Financial Economics 4: 255–96. [Google Scholar] [CrossRef] [Green Version]

- Brämer, Patrick, and Horst Gischer. 2013. An Assessment Methodology for Domestic Systemically Important Banks in Australia. The Australian Economic Review 46: 140–59. [Google Scholar] [CrossRef]

- Brownlees, Christian, and Robert F. Engle. 2017. SRISK: A Conditional Capital Shortfall Measure of Systemic Risk. Review of Financial Studies 30: 48–79. [Google Scholar] [CrossRef]

- Caballero, Ricardo. 2010. The “Other” Imbalance and The Financial Crisis. Cambridge, MA: National Bureau of Economic Research. [Google Scholar]

- Daly, Kevin, Jonathan A. Batten, Anil V. Mishra, and Tonmoy Choudhury. 2019. Contagion risk in global banking sector. Journal of International Financial Markets, Institutions and Money. [Google Scholar] [CrossRef]

- De Bandt, Olivier, and Philipp Hartmann. 2000. Systemic Risk: A Survey. St. Louis: Federal Reserve Bank of St Louis. [Google Scholar]

- Dias, Alexandra. 2014. Semiparametric estimation of multi-asset portfolio tail risk. Journal of Banking & Finance 49: 398–408. [Google Scholar] [CrossRef] [Green Version]

- ECB. 2009. Financial Stability Review. Frankfurt: European Central Bank, pp. 134–42. [Google Scholar]

- Eisenberg, Larry, and Thomas H. Noe. 2001. Systemic Risk in Financial Systems. Management Science 47: 236–49. [Google Scholar] [CrossRef]

- Elsinger, Helmut, Alfred Lehar, and Martin Summer. 2006a. Risk Assessment for Banking Systems. Management Science 52: 1301–14. [Google Scholar] [CrossRef] [Green Version]

- Elsinger, Helmut, Alfred Lehar, and Martin Summer. 2006b. Using Market Information for Banking System Risk Assessment. International Journal of Central Banking 2. [Google Scholar] [CrossRef] [Green Version]

- Fadhlan, Kandrika P. 2015. Risiko Sistemik Perbankan Indonesia: Kausalitas Granger dan Analisis Sentralitas. Yogyakarta: Skripsi, Universitas Gadjah Mada. [Google Scholar]

- FSB, IMF, and BIS. 2009. Guidance to Assess the Systemic Importance of Financial Institutions, Markets and Instruments: Initial Considerations. Washington, DC: International Monetary Fund, Basel: Bank for International Settlements and Financial Stability Board. [Google Scholar]

- Gai, Prasanna, and Sujit Kapadia. 2010. Contagion in financial networks. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences 466: 2401–23. [Google Scholar] [CrossRef] [Green Version]

- Gai, Prasanna, Andrew Haldane, and Sujit Kapadia. 2011. Complexity, concentration and contagion. Journal of Monetary Economics 58: 453–70. [Google Scholar] [CrossRef]

- Huang, Xin, Hao Zhou, and Haibin Zhu. 2009. A framework for assessing the systemic risk of major financial institutions. Journal of Banking & Finance 33: 2036–49. [Google Scholar] [CrossRef] [Green Version]

- Jobst, Andreas A. 2014. Measuring systemic risk-adjusted liquidity (SRL)—A model approach. Journal of Banking & Finance 45: 270–87. [Google Scholar] [CrossRef]

- Jobst, Andreas, and Dale Gray. 2013. Systemic Contingent Claims Analysis—Estimating Market-Implied Systemic Risk. Washington, DC: International Monetary Fund. [Google Scholar]

- Jorion, Philippe. 2007. Value at Risk: The New Benchmark for Managing Financial Risk, 3rd ed. New York: Mc-Graw-Hill. [Google Scholar]

- Krause, Andreas, and Simone Giansante. 2012. Interbank lending and the spread of bank failures: A network model of systemic risk. Journal of Economic Behavior & Organization 83: 583–608. [Google Scholar] [CrossRef] [Green Version]

- Laeven, Luc, and Fabián Valencia. 2013. Systemic Banking Crises Database. IMF Economic Review 61: 225–70. [Google Scholar] [CrossRef] [Green Version]

- Muharam, Harjum, and Erwin Erwin. 2017. Measuring Systemic Risk of Banking in Indonesia: Conditional Value at Risk Model Application. Signifikan: Jurnal Ilmu Ekonomi 6. [Google Scholar] [CrossRef]

- OJK. 2015. Determination of Systemically Important Banks and Capital Surcharges; POJK No. 46/POJK.03/2015; Edited by Otoritas Jasa Keuangan. Jakarta: Otoritas Jasa Keuangan.

- OJK. 2016a. Business Activities and Network of Commercial Banks based on Core Capital; POJK No. 6/POJK.03/2016; Edited by Otoritas Jasa Keuangan. Jakarta: Otoritas Jasa Keuangan.

- OJK. 2016b. Minimum Capital Requirement for Commercial Banks; POJK No. 11/POJK.03/2016; Edited by Otoritas Jasa Keuangan. Jakarta: Otoritas Jasa Keuangan.

- OJK. 2018. Systemic Bank and Capital Surcharge; POJK No. 2/POJK.03/2018; Edited by Otoritas Jasa Keuangan. Jakarta: Otoritas Jasa Keuangan.

- Reinhart, Carmen, and Kenneth Rogoff. 2008. Banking Crises: An Equal Opportunity Menace. Washington, DC: CEPR Centre for Economic Policy Research. [Google Scholar]

- Rizwan, Muhammad Suhail, Ghufran Ahmad, and Dawood Ashraf. 2020. Systemic risk: The impact of COVID-19. Finance Research Letters 36: 101682. [Google Scholar] [CrossRef]

- Rocco, Marco. 2014. Extreme Value Theory in Finance: A Survey. Journal of Economic Surveys 28: 82–108. [Google Scholar] [CrossRef] [Green Version]

- Segoviano, Miguel A., and Charles Goodhart. 2009. Banking Stability Measures. St. Louis: IMF. [Google Scholar]

- Wibowo, Buddi. 2017. Systemic risk, bank’s capital buffer, and leverage. Economic Journal of Emerging Markets 9: 150–58. [Google Scholar] [CrossRef] [Green Version]

- Zebua, Alfredo. 2011. Analisis Risiko Sistemik Perbankan Indonesia. Bogor: Institut Pertanian Bogor. [Google Scholar]

| Category and Weighting | BCBS G-SIB | Indicator Weighting | Category Weighting | Adjusted Indicators D-SIB | Indicator Weighting |

|---|---|---|---|---|---|

| Size (20%) | Total exposures | 20% | Size (33.3%) | Total exposures | 100% |

| Interconnectedness (20%) | Intrafinancial system assets | 6.67% | Interconnectedness (33.3%) | Intrafinancial system assets | 33.3% |

| Intrafinancial system liabilities | 6.67% | Intrafinancial system liabilities | 33.3% | ||

| Securities outstanding | 6.67% | Securities outstanding | 33.3% | ||

| Complexity (20%) | Notional amount of over-the-counter (OTC) derivatives | 6.67% | Complexity (33.3%) | Notional amount of over-the-counter (OTC) derivatives | 25% |

| Level 3 assets | 6.67% | Trading and available-for-sale securities | 25% | ||

| Trading and available-for-sale securities | 6.67% | Domestic indicators | 25% | ||

| Substitutability (payment system and custodian) | 25% | ||||

| Substitutability (20%) | Assets under custody | 6.67% | |||

| Payment activity | 6.67% | ||||

| Underwritten transactions in debt and equity markets | 3.33% | ||||

| Trading volume | 3.33% | ||||

| Cross-jurisdictional activity (20%) | Cross-jurisdictional claims | 10% | |||

| Cross-jurisdictional liabilities | 10% |

| No. | TICKER | BANK | BUKU |

|---|---|---|---|

| 1 | BBCA | PT. Bank Central Asia Tbk. | 4 |

| 2 | BBRI | PT. Bank Rakyat Indonesia (Persero) Tbk. | 4 |

| 3 | BMRI | PT. Bank Mandiri (Persero) Tbk. | 4 |

| 4 | BBNI | PT. Bank Negara Indonesia (Persero) Tbk. | 4 |

| 5 | MEGA | PT. Bank Mega Tbk. | 3 |

| 6 | MAYA | PT. Bank Mayapada Internasional Tbk. | 3 |

| 7 | BNLI | PT. Bank Permata Tbk. | 3 |

| 8 | BDMN | PT. Bank Danamon Indonesia Tbk. | 3 |

| 9 | PNBN | PT. Bank Pan Indonesia Tbk. | 3 |

| 10 | NISP | PT. Bank OCBC NISP Tbk. | 3 |

| 11 | BNGA | PT. Bank CIMB Niaga Tbk. | 4 |

| 12 | BTPN | PT. Bank BTPN Tbk. | 3 |

| 13 | BNII | PT. Bank Maybank Indonesia Tbk. | 3 |

| 14 | BJBR | PT. Bank Pembangunan Daerah Jawa Barat Tbk. | 3 |

| 15 | BBTN | PT. Bank Tabungan Negara (Persero) Tbk. | 3 |

| 16 | BSIM | PT. Bank Sinarmas Tbk. | 2 |

| 17 | BJTM | PT. Bank Pembangunan Daerah Jawa Timur Tbk. | 3 |

| 18 | SDRA | PT. Bank Woori Saudara Indonesia Tbk. | 2 |

| 19 | BACA | PT. Bank Capital Indonesia Tbk. | 2 |

| 20 | AGRO | PT. BRI Agroniaga Tbk. | 2 |

| 21 | CCBI | PT. Bank China Construction Indonesia Tbk. | 2 |

| 22 | BBKP | PT. Bank Bukopin Tbk. | 3 |

| 23 | BABP | PT. Bank MNC Internasional Tbk. | 2 |

| 24 | BKSW | PT. Bank QNB Indonesia Tbk. | 2 |

| 25 | INPC | PT. Bank Artha Graha Internasional Tbk. | 2 |

| 26 | BNBA | PT. Bank Bumi Arta Tbk. | 2 |

| 27 | BVIC | PT. Bank Victoria Internasional Tbk. | 2 |

| Stats | Beta | VaR | ES | CoVaR | ΔCoVaR | MES | SRISK |

|---|---|---|---|---|---|---|---|

| mean | 1.129854 | 3.45 × 107 | 8.06 × 107 | 7,689,775 | 948.8452 | 2.67 × 107 | 459,073.1 |

| max | 1.68771 | 7.60 × 107 | 2.33 × 108 | 6.73 × 107 | 2200.084 | 6.82 × 107 | 2,894,598 |

| min | 0.4221394 | 1.18 × 107 | 2.51 × 107 | −195,820 | 260.8946 | 7,327,341 | 0 |

| sd | 0.1931884 | 1.24 × 107 | 2.65 × 107 | 7,948,986 | 409.0613 | 1.10 × 107 | 585,642.8 |

| variance | 0.0373217 | 1.54 × 1014 | 7.04 × 1014 | 6.32 × 1013 | 167,331.2 | 1.20 × 1014 | 3.43 × 1011 |

| se(mean) | 0.0035461 | 227,512.5 | 486,926.4 | 145,908.2 | 7.508557 | 201,388.5 | 10,749.81 |

| cv | 0.1709853 | 0.3594899 | 0.3290485 | 1.033709 | 0.4311149 | 0.4114864 | 1.275707 |

| skewness | −0.6543876 | 0.5895252 | 0.2660278 | 2.260526 | 0.5894564 | 0.5057055 | 1.402021 |

| Banks | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | ||||||

| % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | |

| BCA | 30.0% | 2 | 25.4% | 1 | 26.6% | 1 | 21.7% | 2 | 30.9% | 1 | 25.1% | 1 |

| BRI | 15.8% | 3 | 9.0% | 4 | 9.7% | 4 | 10.1% | 5 | 6.4% | 6 | 10.7% | 3 |

| BMRI | 30.9% | 1 | 17.0% | 2 | 19.7% | 2 | 22.4% | 1 | 16.9% | 2 | 22.5% | 2 |

| BNI | 6.1% | 4 | 9.2% | 3 | 8.5% | 5 | 10.2% | 4 | 8.1% | 4 | 8.7% | 4 |

| MEGA | 1.1% | 8.0% | 5 | 1.8% | 2.0% | 2.1% | 1.7% | |||||

| BDMN | 1.5% | 1.6% | 2.0% | 1.7% | 1.4% | 2.1% | ||||||

| PNBN | 0.9% | 1.2% | 1.0% | 1.5% | 1.1% | 1.1% | ||||||

| BJBR | 3.5% | 5.7% | 6 | 10.5% | 3 | 10.3% | 3 | 11.4% | 3 | 7.3% | 5 | |

| BTN | 0.0% | 1.2% | 3.0% | 2.2% | 2.3% | 3.1% | ||||||

| BSIM | 0.4% | 0.6% | 5.0% | 6 | 3.2% | 1.2% | 0.8% | |||||

| BJTM | 0.1% | 0.1% | 0.1% | 0.2% | 7.1% | 5 | 6.2% | 6 | ||||

| SDRA | 1.4% | 2.9% | 2.1% | 2.9% | 2.4% | 2.3% | ||||||

| BACA | 2.1% | 3.6% | 3.5% | 4.1% | 2.6% | 2.5% | ||||||

| AGRO | 0.2% | 1.1% | 0.5% | 0.5% | 0.5% | 0.6% | ||||||

| CCBI | 1.5% | 4.4% | 0.7% | 0.4% | 0.3% | 0.7% | ||||||

| BBKP | 1.7% | 2.2% | 2.1% | 3.2% | 2.0% | 2.2% | ||||||

| MNC | 1.2% | 4.3% | 1.7% | 2.1% | 1.8% | 1.0% | ||||||

| Others—10 banks | 1.5% | 2.5% | 1.3% | 1.3% | 1.3% | 1.5% | ||||||

| Banks | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | ||||||

| % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | |

| BCA | 19.0% | 2 | 24.7% | 1 | 14.9% | 3 | 20.1% | 1 | 20.6% | 1 | 19.7% | 1 |

| BRI | 9.9% | 4 | 11.3% | 3 | 7.0% | 5 | 9.3% | 5 | 7.9% | 5 | 7.5% | 5 |

| BMRI | 19.4% | 1 | 20.9% | 2 | 14.0% | 4 | 16.9% | 2 | 18.9% | 2 | 15.2% | 3 |

| BNI | 11.4% | 3 | 8.6% | 5 | 6.7% | 6 | 10.5% | 3 | 10.2% | 4 | 9.6% | 4 |

| MEGA | 2.2% | 1.6% | 1.3% | 3.2% | 2.4% | 1.9% | ||||||

| BDMN | 2.0% | 1.9% | 1.3% | 3.7% | 1.8% | 1.8% | ||||||

| PNBN | 1.4% | 1.1% | 0.9% | 1.3% | 1.6% | 1.4% | ||||||

| BJBR | 9.7% | 5 | 8.9% | 4 | 23.5% | 1 | 9.4% | 4 | 11.9% | 3 | 16.9% | 2 |

| BTN | 2.9% | 1.4% | 2.6% | 2.2% | 3.2% | 2.5% | ||||||

| BSIM | 1.5% | 1.4% | 0.8% | 5.0% | 2.5% | 2.6% | ||||||

| BJTM | 7.9% | 6 | 6.3% | 6 | 17.2% | 2 | 6.5% | 6 | 7.0% | 6 | 6.0% | 6 |

| SDRA | 2.8% | 2.2% | 1.7% | 2.6% | 3.3% | 5.7% | 7 | |||||

| BACA | 3.4% | 3.2% | 1.9% | 2.8% | 3.4% | 2.5% | ||||||

| BBKP | 2.3% | 1.8% | 2.3% | 2.6% | 2.5% | 2.7% | ||||||

| MNC | 1.3% | 1.2% | 1.1% | 1.0% | 0.8% | 0.8% | ||||||

| Others—12 banks | 2.9% | 3.5% | 2.6% | 2.8% | 2.2% | 3.1% | ||||||

| Banks | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | ||||||

| % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | |

| BCA | 10.77% | 3 | 8.00% | 4 | 7.12% | 5 | 5.29% | 8 | 9.79% | 1 | 6.77% | 6 |

| BRI | 16.51% | 1 | 6.99% | 6 | 8.00% | 2 | 6.52% | 6 | 5.62% | 7 | 8.45% | 2 |

| BMRI | 15.55% | 2 | 7.50% | 5 | 8.33% | 1 | 7.06% | 5 | 7.76% | 3 | 7.75% | 3 |

| BNI | 9.88% | 4 | 13.02% | 1 | 6.89% | 6 | 10.18% | 1 | 1.20% | 10.51% | 1 | |

| BDMN | 6.67% | 6 | 6.77% | 7 | 7.75% | 3 | 4.56% | 6.50% | 5 | 6.93% | 4 | |

| PNBN | 8.37% | 5 | 6.60% | 9 | 6.74% | 7 | 8.01% | 2 | 9.74% | 2 | 6.91% | 5 |

| BTPN | 1.20% | 5.10% | 11 | 3.31% | 5.77% | 7 | 4.05% | 4.23% | ||||

| Maybank | 1.38% | 5.01% | 12 | 3.61% | 4.16% | 3.34% | 2.56% | |||||

| BJBR | 0.64% | 0.95% | 6.42% | 8 | 4.99% | 5.80% | 6 | 3.14% | ||||

| BTN | 0.09% | 2.92% | 7.63% | 4 | 4.65% | 4.28% | 5.77% | 7 | ||||

| BSIM | 0.19% | 0.28% | −0.45% | 7.63% | 3 | 2.57% | 0.71% | |||||

| SDRA | 4.41% | 5.81% | 10 | 4.56% | 5.28% | 9 | 3.80% | 3.89% | ||||

| AGRO | 2.83% | 6.79% | 7 | 3.41% | 2.41% | 3.92% | 2.18% | |||||

| BBKP | 5.66% | 7 | 6.77% | 8 | 5.32% | 9 | 7.17% | 4 | 7.00% | 4 | 5.22% | 8 |

| MNC | 2.44% | 9.24% | 2 | 1.19% | 0.07% | 3.45% | 3.78% | |||||

| BAG | 0.98% | 4.98% | 3.59% | 5.16% | 10 | 1.78% | 2.08% | |||||

| BNBA | 3.94% | 3.47% | 2.11% | 2.27% | 2.25% | 1.65% | ||||||

| BVIC | 3.47% | 8.75% | 3 | 3.38% | 3.88% | 4.45% | 4.00% | |||||

| Others—9 banks | 8.92% | −5.51% | 13.17% | 7.22% | 13.43% | 12.30% | ||||||

| Banks | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | ||||||

| % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | |

| BCA | 5.27% | 7 | 7.49% | 4 | 4.07% | 6.27% | 4 | 4.45% | 5.21% | 9 | ||

| BRI | 7.90% | 2 | 9.89% | 2 | 6.01% | 6 | 8.14% | 3 | 6.36% | 6 | 5.77% | 7 |

| BMRI | 7.02% | 3 | 8.72% | 3 | 5.58% | 8 | 5.83% | 6 | 7.33% | 3 | 5.50% | 8 |

| BNI | 12.10% | 1 | 10.80% | 1 | 8.33% | 1 | 12.23% | 2 | 11.22% | 1 | 10.36% | 2 |

| MEGA | 1.93% | 1.39% | 0.48% | 6.16% | 5 | 3.07% | 2.04% | |||||

| BDMN | 6.75% | 4 | 6.69% | 5 | 6.03% | 5 | 17.08% | 1 | 6.83% | 5 | 6.05% | 5 |

| PNBN | 6.54% | 5 | 5.14% | 8 | 4.94% | 1.81% | 5.99% | 7 | 6.88% | 4 | ||

| BTPN | 3.84% | 2.63% | 1.97% | 3.96% | 3.70% | 3.91% | ||||||

| BJBR | 4.68% | 4.75% | 5.10% | 9 | −0.61% | 2.61% | −0.28% | |||||

| BTN | 6.43% | 6 | 3.10% | 7.27% | 3 | 3.04% | 8.08% | 2 | 5.21% | 10 | ||

| BJTM | 2.57% | 3.19% | 7.01% | 4 | 0.73% | 1.91% | 1.79% | |||||

| SDRA | 4.12% | 2.65% | 2.03% | 2.79% | 1.97% | 3.92% | ||||||

| BACA | 1.62% | 5.18% | 7 | 4.12% | 2.38% | 2.55% | 2.17% | |||||

| BNGA | 2.55% | 1.67% | 3.20% | 2.26% | 3.69% | 3.95% | ||||||

| AGRO | 3.25% | 3.16% | 7.94% | 2 | 3.85% | 3.46% | 8.88% | 3 | ||||

| BBKP | 4.96% | 4.13% | 5.78% | 7 | 5.06% | 7 | 5.95% | 8 | 5.82% | 6 | ||

| MNC | 3.73% | 5.65% | 6 | 4.15% | 2.55% | 1.31% | 1.35% | |||||

| BVIC | 2.10% | 4.04% | 2.92% | 3.89% | 6.96% | 4 | 12.75% | 1 | ||||

| Others—9 banks | 12.64% | 9.71% | 13.06% | 12.60% | 12.56% | 8.70% | ||||||

| Banks | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | ||||||

| % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | |

| BMRI | 31.14% | 1 | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |||||

| BNI | 29.17% | 2 | 16.13% | 3 | 0.00% | 7.43% | 3 | 0.00% | 39.87% | 1 | ||

| BNLI | 11.30% | 4 | 24.24% | 2 | 31.85% | 2 | 27.93% | 2 | 0.00% | 0.00% | ||

| PNBN | 0.00% | 0.00% | 0.00% | 2.47% | 70.17% | 1 | 22.02% | 3 | ||||

| BNGA | 24.61% | 3 | 44.70% | 1 | 67.64% | 1 | 49.54% | 1 | 0.00% | 0.00% | ||

| BJBR | 0.00% | 13.67% | 4 | 0.00% | 0.00% | 3.83% | 0.00% | |||||

| BTN | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 26.72% | 2 | |||||

| BJTM | 0.00% | 0.00% | 0.00% | 5.75% | 4 | 0.00% | 0.00% | |||||

| BBKP | 2.81% | 0.00% | 0.00% | 4.04% | 18.48% | 2 | 4.55% | |||||

| BAG | 0.88% | 1.26% | 0.51% | 2.45% | 1.95% | 2.56% | ||||||

| BVIC | 0.00% | 0.00% | 0.00% | 0.39% | 5.57% | 3 | 4.29% | |||||

| OTHERS—16 BANKS | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | ||||||

| Banks | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | ||||||

| % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | % to sys | Rank | |

| BNI | 0.00% | 23.91% | 2 | 26.65% | 2 | 26.11% | 2 | 40.78% | 1 | 49.14% | 1 | |

| BNGA | 19.62% | 2 | 26.94% | 1 | 12.77% | 4 | 0.00% | 11.45% | 4 | 10.52% | 4 | |

| BTPN | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 1.97% | ||||||

| Maybank | 0.00% | 7.52% | 5 | 0.00% | 0.00% | 0.26% | 1.44% | |||||

| BJBR | 16.16% | 3 | 10.77% | 4 | 0.00% | 0.00% | 0.00% | 0.00% | ||||

| BTN | 43.27% | 1 | 13.48% | 3 | 28.09% | 1 | 0.00% | 28.55% | 2 | 20.15% | 2 | |

| BBKP | 1.84% | 6.62% | 6 | 13.36% | 3 | 52.75% | 1 | 13.36% | 3 | 10.94% | 3 | |

| BAG | 9.18% | 4 | 5.30% | 7 | 3.81% | 14.51% | 3 | 2.38% | 1.79% | |||

| BNBA | 0.93% | 0.32% | 0.46% | 0.00% | 0.00% | 0.00% | ||||||

| BVIC | 8.19% | 5 | 5.13% | 8 | 4.37% | 6.63% | 4 | 3.22% | 3.35% | |||

| BACA | 0.81% | 0.00% | 0.58% | 0.00% | 0.00% | 0.00% | ||||||

| AGRO | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.70% | ||||||

| PNBN | 0.00% | 0.00% | 9.90% | 0.00% | 0.00% | 0.00% | ||||||

| OTHERS—14 BANKS | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | ||||||

| Jun-15 | Dec-15 | Jun-16 | Dec-16 | Jun-17 | Dec-17 | Jun-18 | Dec-18 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Name | Systemic Score | Name | Systemic Score | Name | Systemic Score | Name | Systemic Score | Name | Systemic Score | Name | Systemic Score | Name | Systemic Score | Name | Systemic Score |

| BANK 2 | 1408 | BANK 2 | 1321 | BANK 2 | 1242 | BANK 2 | 1248 | BANK 2 | 1224 | BANK 2 | 1219 | BANK 2 | 1222 | BANK 2 | 1219 |

| BANK 1 | 1100 | BANK 1 | 1155 | BANK 1 | 1158 | BANK 1 | 1115 | BANK 1 | 1126 | BANK 1 | 1158 | BANK 1 | 1153 | BANK 1 | 1158 |

| BANK 6 | 957 | BANK 6 | 960 | BANK 6 | 1040 | BANK 6 | 1084 | BANK 6 | 1105 | BANK 6 | 1079 | BANK 6 | 1116 | BANK 6 | 1079 |

| BANK 3 | 564 | BANK 3 | 670 | BANK 3 | 694 | BANK 3 | 750 | BANK 3 | 733 | BANK 3 | 759 | BANK 3 | 798 | BANK 3 | 759 |

| BANK 9 | 376 | BANK 9 | 399 | BANK 9 | 379 | BANK 9 | 355 | BANK 9 | 347 | BANK 9 | 372 | BANK 9 | 364 | BANK 9 | 372 |

| BANK 4 | 309 | BANK 19 | 327 | BANK 19 | 316 | BANK 19 | 333 | BANK 19 | 328 | BANK 19 | 316 | BANK 19 | 330 | BANK 19 | 316 |

| BANK 18 | 301 | BANK 24 | 279 | BANK 24 | 279 | BANK 4 | 267 | BANK 73 | 268 | BANK 4 | 266 | BANK 73 | 274 | BANK 4 | 266 |

| BANK 24 | 296 | BANK 4 | 274 | BANK 4 | 275 | BANK 24 | 261 | BANK 4 | 255 | BANK 73 | 266 | BANK 4 | 248 | BANK 73 | 266 |

| BANK 19 | 285 | BANK 8 | 268 | BANK 8 | 274 | BANK 8 | 250 | BANK 8 | 254 | BANK 8 | 247 | BANK 32 | 232 | BANK 8 | 247 |

| BANK 5 | 273 | BANK 18 | 252 | BANK 5 | 242 | BANK 73 | 236 | BANK 24 | 250 | BANK 24 | 219 | BANK 11 | 230 | BANK 24 | 219 |

| BANK 29 | 246 | BANK 79 | 251 | BANK 7 | 226 | BANK 7 | 229 | BANK 7 | 226 | BANK 7 | 218 | BANK 12 | 219 | BANK 7 | 218 |

| BANK 8 | 243 | BANK 5 | 239 | BANK 73 | 224 | BANK 11 | 214 | BANK 32 | 224 | BANK 11 | 218 | BANK 7 | 213 | BANK 11 | 218 |

| BANK 11 | 224 | BANK 29 | 216 | BANK 29 | 221 | BANK 12 | 207 | BANK 12 | 215 | BANK 32 | 209 | BANK 24 | 211 | BANK 32 | 209 |

| BANK 12 | 223 | BANK 12 | 209 | BANK 18 | 215 | BANK 18 | 203 | BANK 11 | 213 | BANK 12 | 205 | BANK 8 | 200 | BANK 12 | 205 |

| BANK 73 | 207 | BANK 11 | 205 | BANK 11 | 210 | BANK 5 | 200 | BANK 29 | 194 | BANK 29 | 185 | BANK 5 | 187 | BANK 29 | 185 |

| BANK 7 | 193 | BANK 7 | 201 | BANK 12 | 193 | BANK 29 | 185 | BANK 5 | 173 | BANK 5 | 180 | BANK 29 | 184 | BANK 5 | 180 |

| BANK 79 | 171 | BANK 73 | 194 | BANK 79 | 186 | BANK 79 | 185 | BANK 81 | 165 | BANK 79 | 172 | BANK 20 | 165 | BANK 79 | 172 |

| BANK 37 | 146 | BANK 37 | 144 | BANK 21 | 142 | BANK 37 | 162 | BANK 79 | 158 | BANK 37 | 171 | BANK 21 | 161 | BANK 37 | 171 |

| BANK 21 | 132 | BANK 21 | 134 | BANK 37 | 142 | BANK 20 | 152 | BANK 20 | 153 | BANK 20 | 165 | BANK 79 | 150 | BANK 20 | 165 |

| BANK 81 | 129 | BANK 20 | 123 | BANK 20 | 127 | BANK 81 | 147 | BANK 37 | 151 | BANK 21 | 146 | BANK 37 | 147 | BANK 21 | 146 |

| BANK 10 | 113 | BANK 10 | 110 | BANK 10 | 109 | BANK 21 | 138 | BANK 21 | 140 | BANK 81 | 144 | BANK 10 | 105 | BANK 81 | 144 |

| BANK 20 | 113 | BANK 13 | 105 | BANK 13 | 107 | BANK 10 | 106 | BANK 10 | 103 | BANK 10 | 105 | BANK 75 | 100 | BANK 10 | 105 |

| CoVaR15 | CoVaR16 | CoVaR17 | CoVaR18 | Mes15 | Mes16 | Mes17 | Mes18 | Srisk15 | Srisk16 | Srisk17 | Srisk18 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CoVaR15 | 1.0000 | |||||||||||

| CoVaR16 | 0.0667 | 1.0000 | ||||||||||

| CoVaR17 | 0.6000 | −0.0667 | 1.0000 | |||||||||

| CoVaR18 | 0.7333 | 0.0667 | 0.8667 | 1.0000 | ||||||||

| Mes15 | −1.0000 | −1.0000 | −0.6667 | −0.6667 | 1.0000 | |||||||

| Mes16 | −0.4000 | −0.6000 | −0.2000 | −0.4000 | 0.3333 | 1.0000 | ||||||

| Mes17 | −0.6667 | −0.6667 | −0.3333 | −0.3333 | 0.0000 | 0.6000 | 1.0000 | |||||

| Mes18 | −0.3333 | −0.3333 | 0.3333 | 0.3333 | 0.6000 | 0.6000 | 0.4000 | 1.0000 | ||||

| Srisk15 | . | . | . | . | . | 0.6667 | . | 1.0000 | 1.0000 | |||

| Srisk16 | . | . | . | . | . | 0.3333 | . | 0.3333 | −0.3333 | 1.0000 | ||

| Srisk17 | . | . | . | . | . | . | . | . | . | . | 1.0000 | |

| Srisk18 | . | . | . | . | . | 1.0000 | . | 1.0000 | 0.0000 | 0.6667 | . | 1.0000 |

| Bsl15 | 0.3333 | 0.3333 | 0.0000 | 0.0000 | 0.4667 | −0.6667 | −0.3333 | 0.4000 | . | . | . | . |

| Bsl16 | 0.3333 | 0.3333 | 0.0000 | 0.0000 | 0.4667 | −0.6000 | −0.8000 | 0.0667 | 0.3333 | −0.3333 | . | 0.3333 |

| Bsl17 | 0.3333 | 0.3333 | 0.0000 | 0.0000 | 0.4667 | −0.6000 | −0.8000 | 0.2000 | 0.3333 | −0.3333 | . | 0.3333 |

| Bsl18 | 0.3333 | 0.3333 | 0.0000 | 0.0000 | 0.4667 | −0.6000 | −0.8000 | 0.2000 | 0.3333 | −0.3333 | . | 0.3333 |

| Bsl15 | Bsl16 | Bsl17 | Bsl18 | |||||||||

| Bsl15 | 1.0000 | |||||||||||

| Bsl16 | 0.9444 | 1.0000 | ||||||||||

| Bsl17 | 0.8889 | 0.8667 | 1.0000 | |||||||||

| Bsl18 | 0.8889 | 0.8667 | 1.0000 | 1.0000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Salim, M.Z.; Daly, K. Modelling Systemically Important Banks vis-à-vis the Basel Prudential Guidelines. J. Risk Financial Manag. 2021, 14, 295. https://doi.org/10.3390/jrfm14070295

Salim MZ, Daly K. Modelling Systemically Important Banks vis-à-vis the Basel Prudential Guidelines. Journal of Risk and Financial Management. 2021; 14(7):295. https://doi.org/10.3390/jrfm14070295

Chicago/Turabian StyleSalim, M. Zulkifli, and Kevin Daly. 2021. "Modelling Systemically Important Banks vis-à-vis the Basel Prudential Guidelines" Journal of Risk and Financial Management 14, no. 7: 295. https://doi.org/10.3390/jrfm14070295

APA StyleSalim, M. Z., & Daly, K. (2021). Modelling Systemically Important Banks vis-à-vis the Basel Prudential Guidelines. Journal of Risk and Financial Management, 14(7), 295. https://doi.org/10.3390/jrfm14070295