Transfer Entropy Approach for Portfolio Optimization: An Empirical Approach for CESEE Markets

Abstract

:1. Introduction

2. Methodology and Data

3. Results

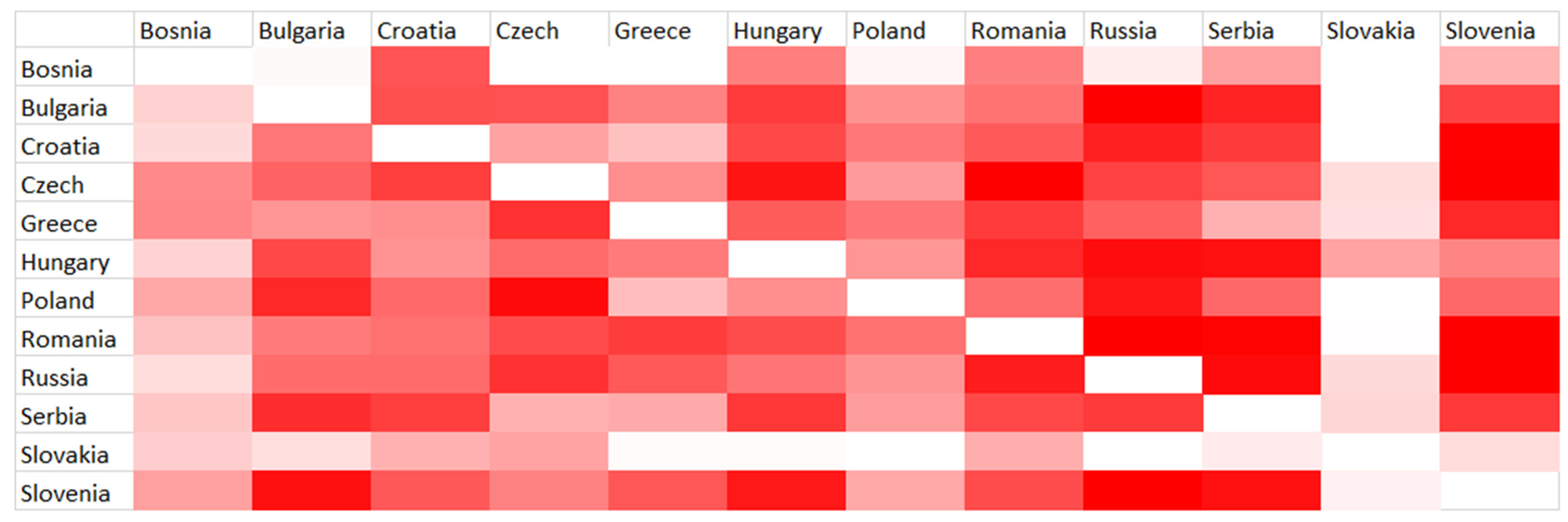

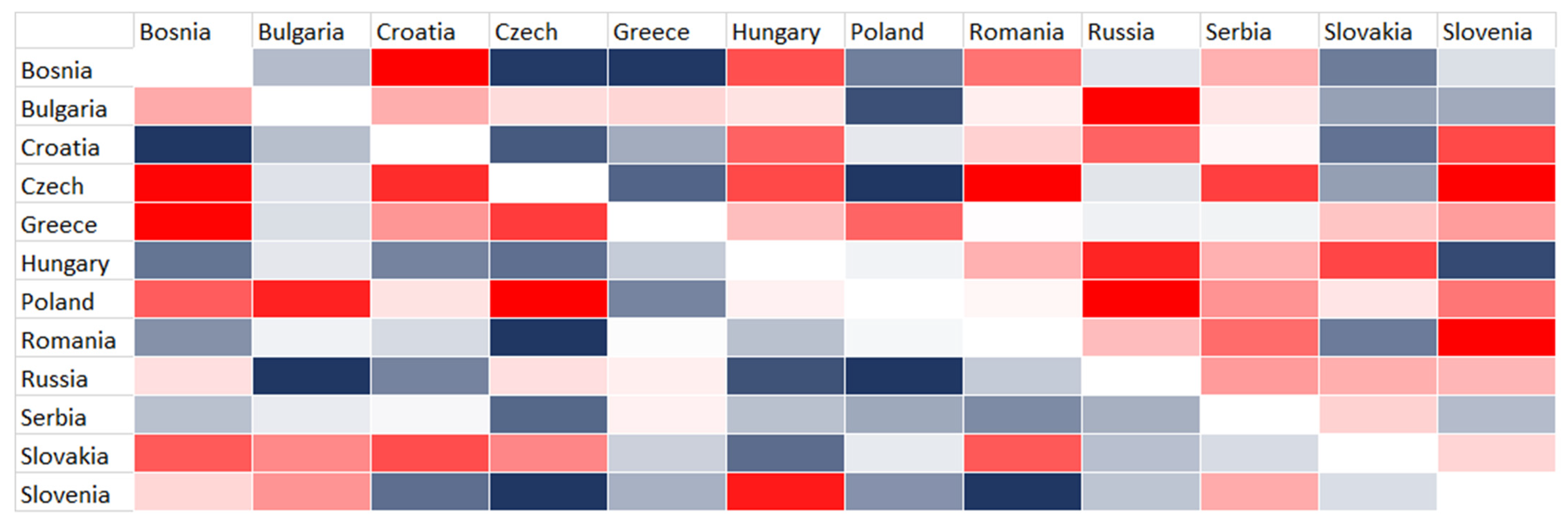

3.1. Preliminary Results

3.2. Description of Simulated Strategies

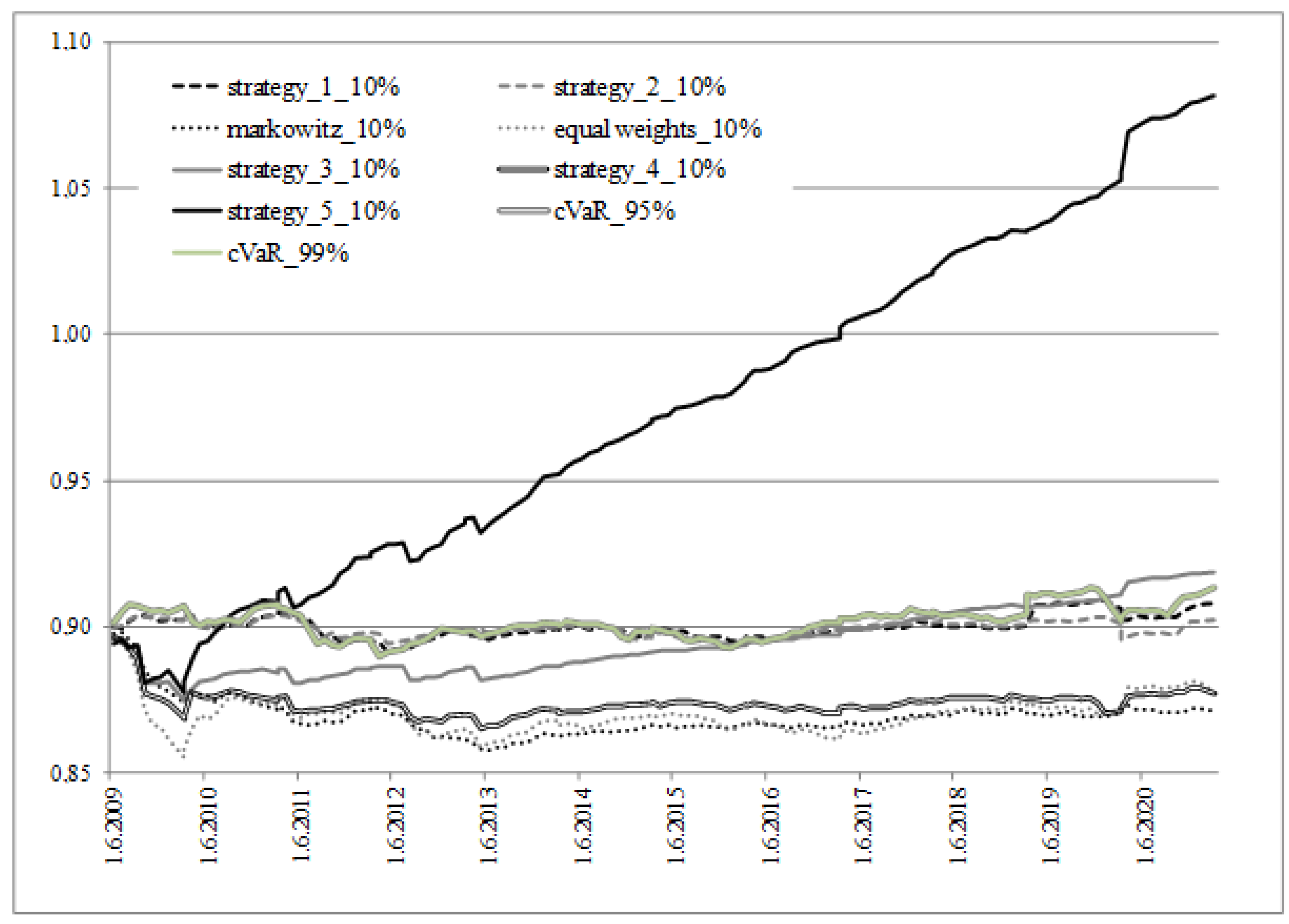

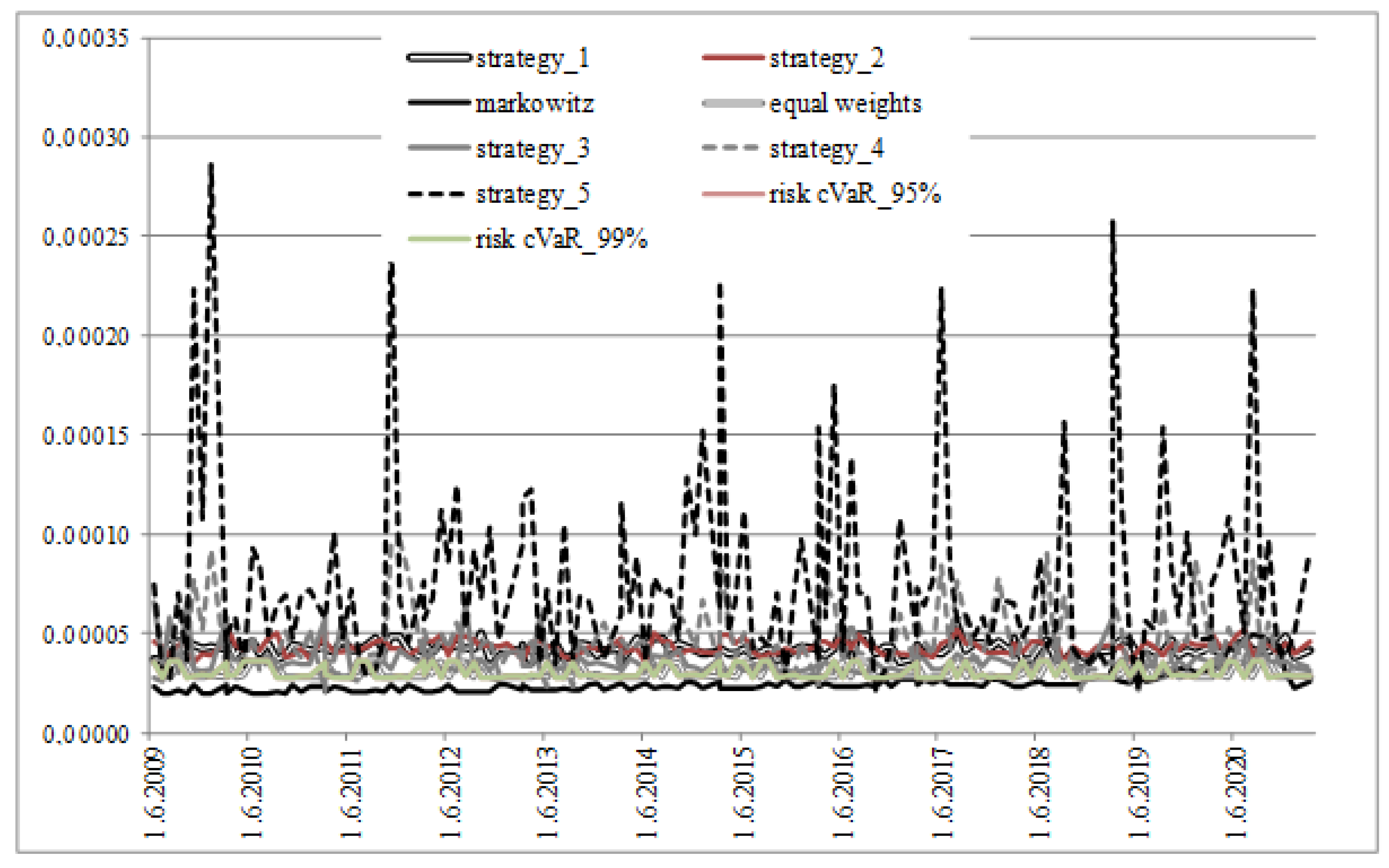

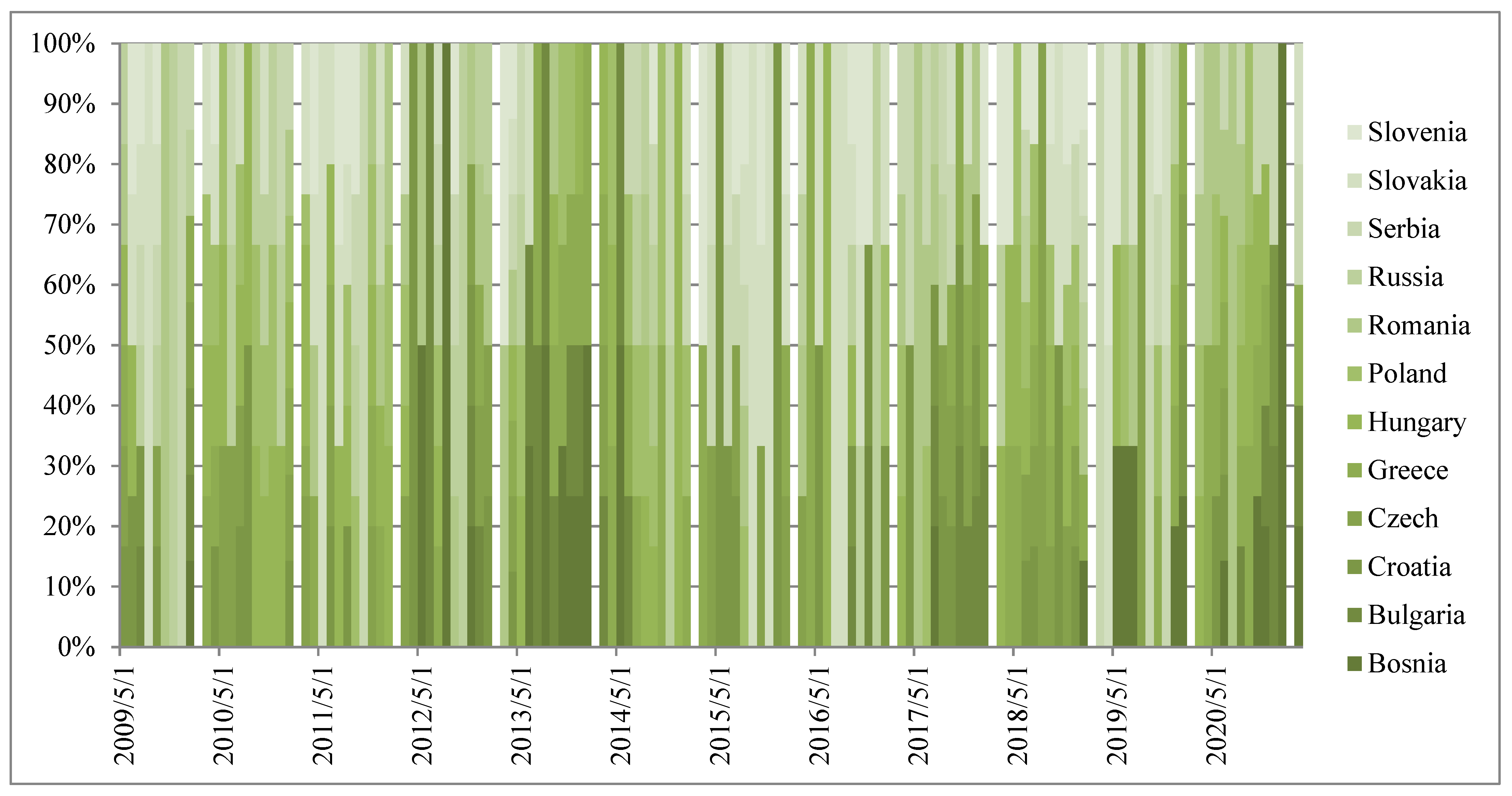

3.3. Results of Trading Simulations

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | Median | Maximum | Minimum | Standard Deviation | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|---|

| BOSNIA | −0.00064 | 0.00000 | 0.05370 | −0.41365 | 0.01152 | −14.78 | 524.10 |

| BULGARIA | −0.00038 | 0.00000 | 0.07292 | −0.17374 | 0.01147 | −2.44 | 34.22 |

| CROATIA | −0.00022 | 0.00000 | 0.14779 | −0.10764 | 0.01100 | −0.49 | 31.95 |

| CZECH | −0.00017 | 0.00004 | 0.12364 | −0.16186 | 0.01372 | −0.71 | 21.88 |

| GREECE | −0.00050 | 0.00000 | 0.13431 | −0.17713 | 0.02129 | −0.44 | 9.44 |

| HUNGARY | 0.00016 | 0.00024 | 0.13178 | −0.12649 | 0.01533 | −0.33 | 12.52 |

| POLAND | −0.00015 | 0.00000 | 0.08155 | −0.14246 | 0.01450 | −0.53 | 9.52 |

| ROMANIA | 0.00006 | 0.00038 | 0.10565 | −0.13117 | 0.01442 | −0.99 | 17.08 |

| RUSSIA | 0.00017 | 0.00003 | 0.70829 | −0.21199 | 0.02431 | 7.53 | 234.83 |

| SERBIA | −0.00015 | 0.00000 | 0.84108 | −0.16388 | 0.02140 | 18.92 | 756.05 |

| SLOVAKIA | −0.00007 | 0.00000 | 0.11880 | −0.14810 | 0.01169 | −1.03 | 23.67 |

| SLOVENIA | −0.00021 | 0.00000 | 0.40474 | −0.40354 | 0.01439 | −0.24 | 394.33 |

References

- Ahmed, Abdullahi Dahir, and Rui Huo. 2018. China–Africa financial markets linkages: Volatility and interdependence. Journal of Policy Modeling 40: 1140–64. [Google Scholar] [CrossRef]

- Baele, Lieven, Geert Bekaert, and Larissa Schäfer. 2015. An Anatomy of Central and Eastern European Equity Markets. Working Paper No. 181. London: European Bank for Reconstruction and Development. [Google Scholar]

- Behrendt, Simon, Thomas Dimpfl, Franziska Julia Peter, and David Zimmermann. 2019. RTransferEntropy—Quantifying information flow between different time series using effective transfer entropy. SoftwareX 10: 100265. [Google Scholar] [CrossRef]

- Beshkooh, Mandi, and Mohammad Ali Afshari. 2012. Selection of the Optimal Portfolio Investment in Stock Market with a Hybrid Approach of Hierarchical Analysis (AHP) and Grey Theory Analysis (GRA). Journal of Basic and Applied Scientific Research 2: 11218–25. [Google Scholar]

- Biglova, Almira, Sergio Ortobelli, Svetlozar Rachev, and Stoyan Stoyanov. 2004. Different approaches to risk estimation in portfolio theory. The Journal of Portfolio Management 31: 103–12. [Google Scholar] [CrossRef] [Green Version]

- Bossomaier, Terry, Lionel Barnett, Michael Harré, and Joseph Lizier. 2016. Miscellaneous Applications of Transfer Entropy. In An Introduction to Transfer Entropy. Cham: Springer. [Google Scholar] [CrossRef]

- Bricco, Jana, and Teng-Teng Xu. 2019. Interconnectedness and Contagion Analysis: A Practical Framework. IMF Working Paper WP/19/220. Washington, DC: IMF. [Google Scholar]

- Cevik, Emrah Ismail, Turhan Korkmaz, and Emre Cevik. 2017. Testing causal relation among central and eastern European equity markets: Evidence from asymmetric causality test. Economic Research-Ekonomska Istraživanja 30: 381–93. [Google Scholar] [CrossRef] [Green Version]

- Chen, Mei-Ping, Pei-Fen Chen, and Chien-Chiang Lee. 2014. Frontier stock market integration and the global financial crisis. North American Journal of Economics and Finance 29: 84–103. [Google Scholar] [CrossRef]

- Cheng, Chao. 2006. Improving the Markowitz Model Using the Notion of Entropy. Available online: http://divaportal.org/smash/get/diva2:304730/FULLTEXT01.pdf (accessed on 8 August 2021).

- Cheridito, Patrick, and Eduard Kromer. 2013. Risk-reward ratios. Journal of Investment Strategies 3: 3–18. [Google Scholar] [CrossRef]

- Delcea, Camelia. 2015. Grey systems theory in economics—A historical applications review. Grey Systems: Theory and Application 5: 263–76. [Google Scholar] [CrossRef]

- Dimpfl, Thomas, and Franziska Julia Peter. 2013. Using transfer entropy to measure information flows between financial markets. Studies in Nonlinear Dynamics and Econometrics 17: 85–102. [Google Scholar] [CrossRef] [Green Version]

- Favre, Laurent, and Jose Antonio Galeano. 2002. Mean-modified Value-at-Risk optimization with hedge funds. The Journal of Alternative Investments 5: 21–25. [Google Scholar] [CrossRef]

- Ferreira, Paulo. 2018. What guides Central and Eastern European stock markets? A view from detrended methodologies. Post-Communist Economies 30: 805–19. [Google Scholar] [CrossRef]

- Figueira, Joao, Salvatore Greco, and Matthias Ehrgott. 2005. Multiple Criteria Decision Analysis: State of the Art Surveys. New York: Springer, vol. 78. [Google Scholar]

- Gilmore, Claire, and Ginette McManus. 2003. Bilateral and multilateral cointegration properties between the German and central European equity markets. Studies in Economics and Finance 21: 40–53. [Google Scholar] [CrossRef]

- Golab, Anna, David Edmund Allen, and Robert Powell. 2015. Aspects of Volatility and Correlations in European Emerging Economies. In Emerging Markets and Sovereign Risk. Edited by Nigel Finch. London: Palgrave Macmillan. [Google Scholar]

- Granger, Clive. 1969. Investigating Causal Relations by Econometric Models and Cross-spectral Methods. Econometrica 37: 424–38. [Google Scholar] [CrossRef]

- Guidolin, Massimo, and Alen Timmermann. 2007. Asset allocation under multivariate regime switching. Journal of Economic Dynamics and Control 31: 3503–44. [Google Scholar] [CrossRef] [Green Version]

- Guidolin, Massimo, and Alen Timmermann. 2008. International Asset allocation under Regime Switching, Skew, and Kurtosis Preferences. The Review of Financial Studies 21: 889–935. [Google Scholar] [CrossRef]

- Huang, Xiaoxia. 2007. Portfolio Selection with Fuzzy Returns. Journal of Intelligent & Fuzzy Systems 18: 383–90. [Google Scholar]

- Huang, Xiaoxia. 2008. Mean-Semivariance Models for Fuzzy Portfolio Selection. Journal of Computational and Applied Mathematics 217: 1–9. [Google Scholar] [CrossRef] [Green Version]

- Huang, Xiaoxia. 2012. An Entropy Method for Diversified Fuzzy Portfolio Selection. International Journal of Fuzzy Systems 14: 161–65. [Google Scholar]

- Hurson, Christian, and Constantin Zopounidis. 1995. On the use of multicriteria decision aid methods to portfolio selection. In Multicriteria Analysis. Edited by J. Clímaco. Berlin and Heidelberg: Springer. [Google Scholar]

- Ilhan, Usta, and Yeliz Mert Kantar. 2007. Portfolio Optimization with Entropy Measure. Available online: https://www.researchgate.net/publication/261859605_Portfolio_optimization_with_entropy_measure (accessed on 8 August 2021).

- Investing. 2021. Available online: https://www.investing.com (accessed on 8 June 2021).

- Jizba, Petr, Hagen Kleinert, and Mohammad Shefaat. 2012. Rényi’s information transfer between financial time series. Physica A 391: 2971–89. [Google Scholar] [CrossRef] [Green Version]

- Kamisli, Melik, Seraf Kamisli, and Mustafa Ozer. 2015. Are volatility transmissions between stock market returns of Central and Eastern European countries constant or dynamic? Evidence from MGARCH models. Paper presented at the Conference Proceedings of 10th MIBES Conference, Larisa, Greece, October 15–17; pp. 190–203. [Google Scholar]

- Kim, Sondo, Seugmo Ku, Woojin Chang, and Jae Wook Song. 2020. Predicting the Direction of US Stock Prices Using Effective Transfer Entropy and Machine Learning Techniques. IEEE Access 8: 111660–82. [Google Scholar] [CrossRef]

- Knight, John, and Stephen Satchell. 2002. Performance Measurement in Finance. Oxford: Elsevier. [Google Scholar]

- Krokhmal, Pavlo, Jonas Palmquist, and Stanislav Uryasev. 2001. Portfolio Optimization with Conditional Value-at-Risk Objective and Constraints. Research Report. Available online: https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.205.3769&rep=rep1&type=pdf (accessed on 8 August 2021).

- Kwon, Okyu, and Jae Suk Yang. 2008. Information flow between stock indices. Europhysics Letters 82: 1–4. [Google Scholar] [CrossRef] [Green Version]

- Lim, Sungmook, Kwang Wuk Oh, and Joe Zhu. 2013. Use of DEA cross-efficiency evaluation in portfolio selection: An application to Korean Stock Market. European Journal of Operational Research 236: 361–68. [Google Scholar] [CrossRef]

- Martínez-Vega, Daniel, Laura Cruz-Reyes, Claudia Guadalupe Gomez-Santillan, Fausto Balderas-Jaramillo, and Marco Antonio Aguirre-Lam. 2020. The Dynamic Portfolio Selection Problem: Complexity, Algorithms and Empirical Analysis. In Intuitionistic and Type-2 Fuzzy Logic Enhancements in Neural and Optimization Algorithms: Theory and Applications. Studies in Computational Intelligence. Edited by Oscar Castillo, Patricia Melin and Januzs Kacprzyk. Cham: Springer, vol. 862. [Google Scholar] [CrossRef]

- Özer, Mustafa, Sandra Kamenković, and Zoran Grubišić. 2020. Frequency domain causality analysis of intra- and inter-regional return and volatility spillovers of South-East European (SEE) stock markets. Economic Research-Ekonomska Istraživanja 33: 1–25. [Google Scholar] [CrossRef]

- Palo, Gianni. 2016. On Entropy and Portfolio Diversification. Journal of Asset Management 17: 218–28. [Google Scholar]

- Pop, Corneila, Dragozs Bozdog, and Adina Calugaru. 2013. The Bucharest Stock Exchange case: Is BET-FI an index leader for the oldest indices BET and BET-C? International Business: Research, Teaching and Practice 7: 35–56. [Google Scholar]

- Rozlucki, Wiselaw. 2010. The creation of exchanges in countries with communist histories. In Regulated Exchanges, Dynamic Agents of Economic Growth. Edited by Larry Harris. Oxford: Oxford University Press. [Google Scholar]

- Salardini, Firoozeh. 2013. An AHP-GRA method for asset allocation: A case study of investment firms on Tehran Stock Exchange. Decision Science Letters 2: 275–80. [Google Scholar] [CrossRef]

- Schreiber, Thomas. 2000. Measuring Information Theory. Physical Review Letters 85: 461. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Sensoy, Ahmet, Cihat Sobaci, Sadri Sensoy, and Fatih Alali. 2014. Effective transfer entropy approach to information flow between exchange rates and stock markets. Chaos, Solitons and Fractals 68: 180–85. [Google Scholar] [CrossRef]

- Shannon, Claude. 1949. Communication Theory of Secrecy Systems. Bell System Technical Journal 28: 656–715. [Google Scholar] [CrossRef]

- Skaf, Jöelle, and Stephen Boyd. 2008. Multi-Period Portfolio Optimization with Constraints and Transaction Costs. Working Paper. Stanford: Stanford University. [Google Scholar]

- Škrinjarić, Tihana. 2014. Investment Strategy on the Zagreb Stock Exchange Based on Dynamic DEA. Croatian Economic Survey 16: 129–60. [Google Scholar] [CrossRef]

- Škrinjarić, Tihana. 2020a. CEE and SEE equity market return spillovers: Creating profitable investment strategies. Borsa Istanbul Review 20 S1: S62–S80. [Google Scholar] [CrossRef]

- Škrinjarić, Tihana. 2020b. Dynamic Portfolio Optimization Based on Grey Relational Analysis Approach. Expert Systems with Applications 147: 1–15. [Google Scholar] [CrossRef]

- Sortino, Frank, and Stephen Satchell. 2001. Managing Downside Risk in Financial Markets. Oxford: Butterworth–Heinemann. [Google Scholar]

- Taylor, Mark, and Hellen Allen. 1992. The use of technical analysis in the foreign exchange market. Journal of International Money and Finance 11: 304–14. [Google Scholar] [CrossRef]

- Wallis, Kenneth. 2011. Combining forecasts—Forty years later. Applied Financial Economics 21: 33–41. [Google Scholar] [CrossRef] [Green Version]

| Strategy_1 | Strategy_2 | Markowitz | Equal Weights | Strategy_3 | Strategy_4 | Strategy_5 | cVAR 95% | cVaR 99% | |

|---|---|---|---|---|---|---|---|---|---|

| Mean return | 0.06462 | 0.02003 | −0.22930 | −0.17344 | 0.14615 | −0.17815 | 1.30851 | 0.106 | 0.106 |

| SD (volatility) | 0.04224 | 0.04313 | 0.02485 | 0.03057 | 0.03641 | 0.04461 | 0.07663 | 0.03052 | 0.03051 |

| CE 1 | 0.06462 | 0.02003 | −0.22930 | −0.17344 | 0.14615 | −0.17816 | 1.30850 | 0.10588 | 0.10591 |

| CE 2 | 0.06462 | 0.02003 | −0.22930 | −0.17344 | 0.14615 | −0.17816 | 1.30849 | 0.10588 | 0.10591 |

| CE 10 | 0.06460 | 0.02001 | −0.22931 | −0.17345 | 0.14614 | −0.17818 | 1.30842 | 0.10587 | 0.10588 |

| Total return | 0.0091 | 0.0028 | −0.0323 | −0.0245 | 0.0206 | −0.0251 | 0.1845 | 0.01493 | 0.01493 |

| Annualized return | 0.0238 | 0.0073 | −0.0816 | −0.0621 | 0.0542 | −0.0637 | 0.5501 | 0.0391 | 0.0391 |

| HPM_1_rtilda = 0 | 0.0008 | 0.0007 | 0.0009 | 0.0014 | 0.0005 | 0.0008 | 0.0018 | 0.0013 | 0.0012 |

| LPM_1 | −0.0008 | −0.0008 | −0.0011 | −0.0019 | −0.0054 | −0.0014 | −0.0059 | −0.00138 | −0.00138 |

| std return | 1.5139 | 0.6138 | −11.1637 | −5.3775 | 7.8609 | −4.9223 | 19.1374 | 4.93052 | 4.9305 |

| Information ratio (compared to equal weights) | 0.284237 | 0.238609 | - | - | 0.714288 | −0.009597 | 3.26210 | - | - |

| Information ratio (compared to Markowitz) | 0.490959 | 0.445967 | - | - | 1.059740 | 0.143827 | 2.77281 | - | - |

| Information ratio (compared to cVaR 95%) | −0.06631 | −0.1446 | 0.051898 | −0.347746 | 1.24413 | - | - | ||

| Information ratio (compared to cVaR 99%) | −0.06630 | −0.14461 | 0.05189 | −0.34775 | 1.24412 | - | - | ||

| Sortino–Satchell ratio | 0.073741 | 0.0220332 | −0.173492 | −0.08302 | 0.088883 | −0.10514 | 0.718279 | 0.07601 | 0.07606 |

| Rachev ratio, lower and upper tail 5% | 0.9724844 | 0.7698989 | 0.5515859 | 0.6509754 | 0.5344477 | 0.5878211 | 1.3656363 | 0.87731 | 0.8773 |

| RoVar ratio | 0.040629 | 0.004908 | −0.038348 | −0.016579 | 0.026266 | −0.015628 | 0.106897 | 0.01766 | 0.01765 |

| Index | % Months Entering the Portfolio | Max Weight % | Average Weight % | Mode % | No Times Only One in Portfolio | Min Weight % |

|---|---|---|---|---|---|---|

| Bosnia | 17 | 100 | 35 | 33 | 2 | 14 |

| Bulgaria | 18 | 100 | 33 | 20 | 2 | 14 |

| Croatia | 29 | 100 | 30 | 25 | 3 | 13 |

| Czech | 27 | 100 | 29 | 20 | 3 | 13 |

| Greece | 36 | 100 | 28 | 25 | 2 | 13 |

| Hungary | 37 | 100 | 27 | 25 | 2 | 13 |

| Poland | 32 | 50 | 26 | 25 | 0 | 14 |

| Romania | 25 | 100 | 32 | 25 | 3 | 13 |

| Russia | 24 | 100 | 32 | 25 | 3 | 14 |

| Serbia | 31 | 100 | 31 | 25 | 3 | 13 |

| Slovakia | 33 | 100 | 36 | 20 | 6 | 13 |

| Slovenia | 23 | 50 | 26 | 17 | 0 | 13 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Škrinjarić, T.; Quintino, D.; Ferreira, P. Transfer Entropy Approach for Portfolio Optimization: An Empirical Approach for CESEE Markets. J. Risk Financial Manag. 2021, 14, 369. https://doi.org/10.3390/jrfm14080369

Škrinjarić T, Quintino D, Ferreira P. Transfer Entropy Approach for Portfolio Optimization: An Empirical Approach for CESEE Markets. Journal of Risk and Financial Management. 2021; 14(8):369. https://doi.org/10.3390/jrfm14080369

Chicago/Turabian StyleŠkrinjarić, Tihana, Derick Quintino, and Paulo Ferreira. 2021. "Transfer Entropy Approach for Portfolio Optimization: An Empirical Approach for CESEE Markets" Journal of Risk and Financial Management 14, no. 8: 369. https://doi.org/10.3390/jrfm14080369

APA StyleŠkrinjarić, T., Quintino, D., & Ferreira, P. (2021). Transfer Entropy Approach for Portfolio Optimization: An Empirical Approach for CESEE Markets. Journal of Risk and Financial Management, 14(8), 369. https://doi.org/10.3390/jrfm14080369