Modelling the Impact of Different COVID-19 Pandemic Waves on Real Estate Stock Returns and Their Volatility Using a GJR-GARCHX Approach: An International Perspective

Abstract

:1. Introduction

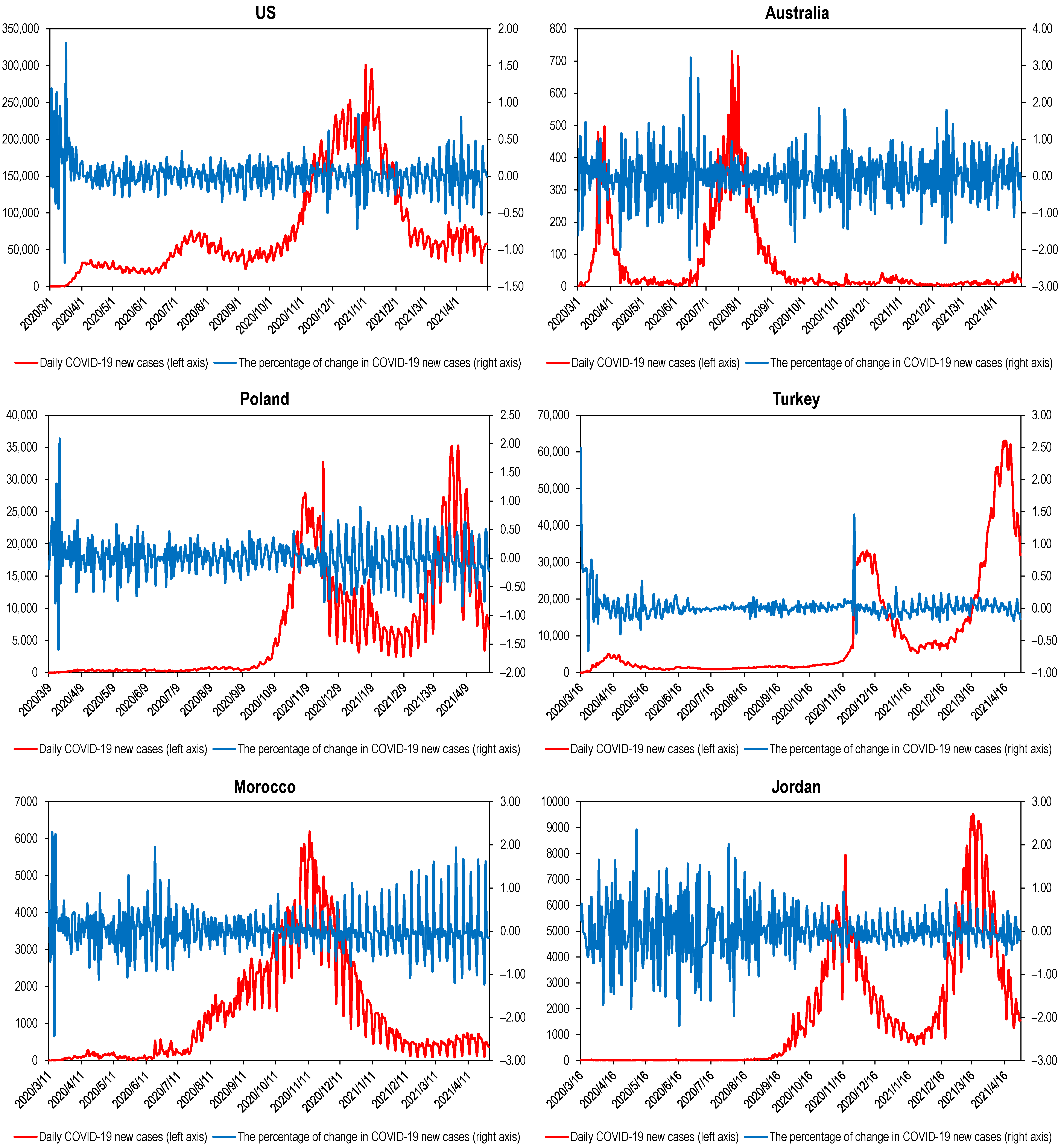

2. Data and Software

3. Methodology

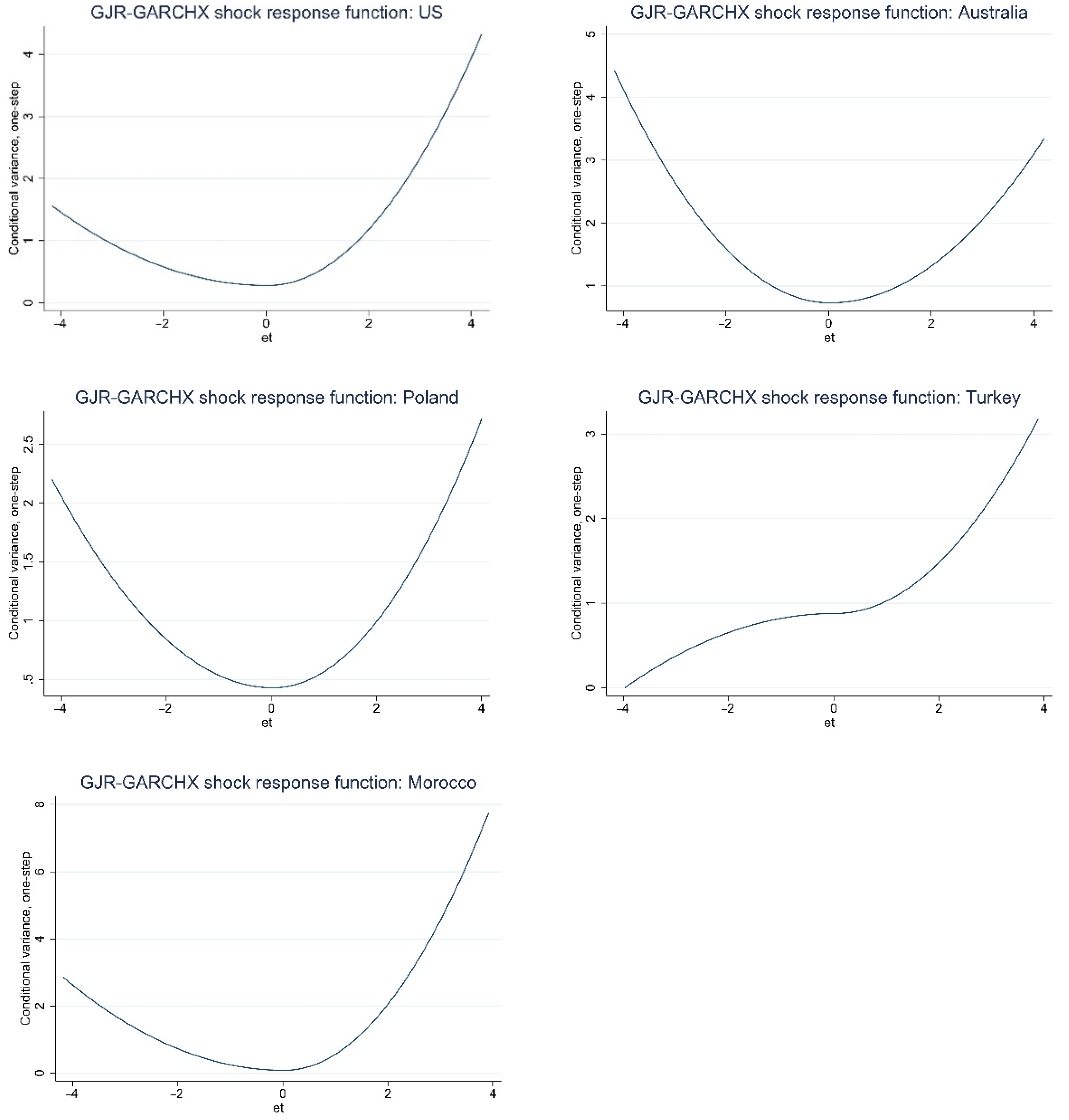

4. Results and Discussion

5. Robustness Checks

6. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ahsan, Md Moynul, and Cihan Sadak. 2021. Exploring housing market and urban densification during COVID-19 in Turkey. Journal of Urban Management. [Google Scholar] [CrossRef]

- Apergis, Nicholas, and Emmanuel Apergis. 2020. The role of Covid-19 for Chinese stock returns: Evidence from a GARCHX model. Asia-Pacific Journal of Accounting & Economics, 1–9. [Google Scholar] [CrossRef]

- Baker, Scott, Nicholas Bloom, Steven Davis, Kyle Kost, Marco Sammon, and Tasaneeya Viratyosin. 2020. The Unprecedented Stock Market Reaction to COVID-19. The Review of Asset Pricing Studies 10: 742–58. [Google Scholar] [CrossRef]

- Buszko, Michał, Witold Orzeszko, and Marcin Stawarz. 2021. COVID-19 pandemic and stability of stock market—A sectoral approach. PLoS ONE 16: e0250938. [Google Scholar] [CrossRef] [PubMed]

- Charles, Amélie, and Olivier Darné. 2019. The accuracy of asymmetric GARCH model estimation. International Economics 157: 179–202. [Google Scholar] [CrossRef]

- Dong, Ensheng, Hongru Du, and Lauren Gardner. 2020. An interactive web-based dashboard to track COVID-19 in real time. The Lancet Infectious Diseases 20: 533–34. [Google Scholar] [CrossRef]

- Duca, John, Martin Hoesli, and Joaquim Montezuma. 2021. The resilience and realignment of house prices in the era of Covid-19. Journal of European Real Estate Research. [Google Scholar] [CrossRef]

- Engle, Robert. 1990. Stock volatility and the crash of’87: Discussion. The Review of Financial Studies 3: 103–6. [Google Scholar] [CrossRef]

- Glosten, Lawrence, Ravi Jagannathan, and David Runkle. 1993. On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks. The Journal of Finance 48: 1779–801. [Google Scholar] [CrossRef]

- Huynh, Nhan, Dat Nguyen, and Anh Dao. 2021. Sectoral Performance and the Government Interventions during COVID-19 Pandemic: Australian Evidence. Journal of Risk and Financial Management 14: 178. [Google Scholar] [CrossRef]

- Janndi, Widad, and Abdelhak Moussamir. 2021. Stock market reactions to COVID-19: Evidence from Morocco. International Journal of Management Sciences 4: 579–93. [Google Scholar]

- Jiang, Wei. 2012. Using the GARCH Model to Analyse and Predict the Different Stock Markets. Masters’ dissertation, Department of Statistics, Uppsala University, Uppsala, Sweden. [Google Scholar]

- Jindřichovská, Irena, and Erginbay Uğurlu. 2021. EU and China trends in trade in challenging times. Journal of Risk and Financial Management 14: 71. [Google Scholar] [CrossRef]

- Khalil, Nait. 2021. The COVID-19′s Spillover Effects on Industry Indices Returns: Evidence from Casablanca Stock Exchange. African Scientific Journal 3: 505–24. [Google Scholar]

- Lombardi, Marco, and Giampiero Gallo. 2002. Analytic Hessian matrices and the computation of FIGARCH estimates. Statistical Methods and Applications 11: 247–64. [Google Scholar] [CrossRef]

- Mazur, Mieszko, Man Dang, and Miguel Vega. 2021. COVID-19 and the march 2020 stock market crash. Evidence from S&P1500. Finance Research Letters 38: 101690. [Google Scholar] [CrossRef] [PubMed]

- Milcheva, Stanimira. 2021. Volatility and the Cross-Section of Real Estate Equity Returns during Covid-19. The Journal of Real Estate Finance and Economics, 1–28. [Google Scholar] [CrossRef]

- Narayan, Paresh, Qiang Gong, and Huson Ahmed. 2021. Is there a pattern in how COVID-19 has affected Australia’s stock returns? Applied Economics Letters. [Google Scholar] [CrossRef]

- Nelson, Daniel. 1991. Conditional heteroskedasticity in asset returns: A new approach. Econometrica: Journal of the Econometric Society 59: 347–70. [Google Scholar] [CrossRef]

- Öztürk, Özkan, Muhammet Şişman, Hakan Uslu, and Ferhat Çıtak. 2020. Effect of COVID-19 outbreak on Turkish stock market: A sectoral-level analysis. Hitit University Journal of Social Sciences Institute 13: 56–68. [Google Scholar]

- Prevost, Lisa. 2021. House Hunting in Morocco: A Marrakesh Riad for Under $500,000. The New York Times. Available online: https://www.nytimes.com/2021/05/12/realestate/house-hunting-in-morocco-a-marrakesh-riad-for-under-500000.html (accessed on 5 August 2021).

- Thorbecke, Willem. 2020. The impact of the COVID-19 pandemic on the US Economy: Evidence from the stock market. Journal of Risk and Financial Management 13: 233. [Google Scholar] [CrossRef]

- Tomal, Mateusz, and Bartłomiej Marona. 2021. The Impact of the COVID-19 Pandemic on the Private Rental Housing Market in Poland: What Do Experts Say and What Do Actual Data Show? Critical Housing Analysis 8: 24–35. [Google Scholar] [CrossRef]

- Zakoian, Jean-Michel. 1994. Threshold heteroskedastic models. Journal of Economic Dynamics and Control 18: 931–55. [Google Scholar] [CrossRef]

- Zivot, Eric. 2009. Practical issues in the analysis of univariate GARCH models. In Handbook of Financial Time Series. Berlin and Heidelberg: Springer, pp. 113–55. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Country | Dependent Variable | Control Variable | Period Analyzed | N | |||

|---|---|---|---|---|---|---|---|

| Index | S | K | Shapiro–Wilk Test | ||||

| US | S&P 500 Real Estate returns | −1.45 | 12.90 | S&P 500 returns | 2 March 2020–30 April 2021 | 295 | |

| Australia | S&P/ASX 200 Real Estate returns | −1.52 | 10.31 | S&P/ASX 200 returns | 2 March 2020–30 April 2021 | 293 | |

| Poland | WIG Real Estate returns | −0.65 | 4.25 | WIG returns | 9 March 2020–30 April 2021 | 288 | |

| Turkey | BIST Real Estate Invest Trusts returns | −0.73 | 3.40 | BIST 100 returns | 16 March 2020–30 April 2021 | 284 | |

| Morocco | Real Estate (IMMOB) returns | −0.32 | 2.35 | FTSE CSE Morocco 15 returns | 11 March 2020–30 April 2021 | 285 | |

| Jordan | Real Estate (AMREX) returns | 0.26 | 0.70 | Amman SE All Share returns | 10 May 2020–29 April 2021 | 237 | |

| Variable | US | Australia | Poland | Turkey | Morocco | Jordan |

|---|---|---|---|---|---|---|

| Mean equation | ||||||

| Constant | 0.000144 | −0.000108 | −0.001248 | 0.001766 | 0.001815 | 0.000765 |

| Control | 1.031600 *** | 1.112680 *** | 0.512053 ** | 1.034670 *** | 0.951915 *** | 0.270696 *** |

| COVID19 | −0.015908 *** | −0.000398 | 0.002723 | 0.004504 | 0.001545 | 0.000430 |

| CWave23 | 0.000260 | −0.000237 | 0.002930 ** | −0.002585 | 0.001285 | −0.000099 |

| COVID19 × CWave23 | 0.009304 | 0.001947 | −0.007845 ** | 0.000040 | −0.001064 | −0.003241 * |

| Diagnostics | ||||||

| q | 2 | 3 | 2 | 3 | 2 | 1 |

| p | 3 | 3 | 2 | 2 | 1 | 0 |

| Joint significance † | ||||||

| ARCH effect | ||||||

| Conditional volatility equation | ||||||

| Constant | −9.544025 *** | −11.174630 *** | −10.019260 *** | −12.093360 *** | −8.776888 *** | NA |

| COVID19 | 0.999685 | 1.020167 | 2.187499 *** | 0.793015 | 0.007589 | NA |

| CWave23 | −0.410830 | −0.741840 | −0.256941 | 0.884779* | −0.473977 ** | NA |

| COVID19 × CWave23 | −4.289059 * | −2.223724 | −2.434554 * | −0.408110 | 0.172183 | NA |

| 0.072690 | 0.212285 ** | 0.100403 | −0.054744 | 0.156881 | NA | |

| 0.159656 | −0.064464 | 0.044493 | 0.209003 ** | 0.351020 | NA | |

| 0.278839 | 0.732480 *** | 0.428604 *** | 0.878622 *** | 0.080777 | NA | |

| Diagnostics | ||||||

| Joint significance † | NA | |||||

| Joint significance ‡ | NA | |||||

| GED shape parameter | 2.003883 | 1.723155 | 1.530436 | 1.633107 | 1.571219 | NA |

| 0.431358 | 0.912532 | 0.551254 | 0.928379 | 0.413168 | NA | |

| Log–likelihood | 945.4581 | 905.1113 | 917.9927 | 867.1617 | 820.9228 | NA |

| N | 295 | 293 | 288 | 284 | 285 | 237 |

| Variable | US | Australia | Poland | Turkey | Morocco | Jordan |

|---|---|---|---|---|---|---|

| Conditional volatility equation (EGARCHX) | ||||||

| Constant | −4.055683 * | −0.576225 | −6.666113 | −13.101910 *** | −4.837369 ** | NA |

| COVID19 | 0.701977 | 0.395548 * | 0.200734 | 0.501505 | −0.237770 | NA |

| CWave23 | −0.115050 | −0.059870 | −0.484480 | −0.343260 | −0.012890 | NA |

| COVID19 × CWave23 | −2.463610 ** | −0.480260 | −0.410610 | −0.791810 | −0.047360 | NA |

| Joint significance † | NA | |||||

| Log–likelihood | 945.9369 | 905.5441 | 915.6624 | 863.0055 | 820.4674 | NA |

| Conditional volatility equation (SAARCHX) | ||||||

| Constant | −9.553358 *** | −11.198190 *** | −9.994610 *** | Not enough observations to estimate the model | −8.851563 *** | NA |

| COVID19 | 1.013982 | 1.024124 | 2.162423 *** | 0.041785 | NA | |

| CWave23 | −0.445330 * | −0.738190 | −0.261250 | −0.424921 * | NA | |

| COVID19 × CWave23 | −3.858470 * | −2.235790 | −2.380910 * | 0.080146 | NA | |

| Joint significance † | NA | |||||

| Log–likelihood | 945.767 | 905.0433 | 917.945 | 821.1242 | NA | |

| Conditional volatility equation (TARCHX) | ||||||

| Constant | −9.234961 *** | −11.165170 *** | −10.04424 *** | −9.478187 *** | −8.845685 *** | NA |

| COVID19 | 0.983270 | 1.033758 | 2.203767 *** | 0.497031 | 0.013858 | NA |

| CWave23 | −0.521980 ** | −0.762210 | −0.267080 | 0.323462 | −0.445720 * | NA |

| COVID19 × CWave23 | −2.537060 * | −2.365700 | −2.538890 * | 0.963047 | 0.175666 | NA |

| Joint significance † | NA | |||||

| Log–likelihood | 945.845 | 904.2689 | 918.9061 | 864.776 | 821.3933 | NA |

| N | 295 | 293 | 288 | 284 | 285 | 237 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tomal, M. Modelling the Impact of Different COVID-19 Pandemic Waves on Real Estate Stock Returns and Their Volatility Using a GJR-GARCHX Approach: An International Perspective. J. Risk Financial Manag. 2021, 14, 374. https://doi.org/10.3390/jrfm14080374

Tomal M. Modelling the Impact of Different COVID-19 Pandemic Waves on Real Estate Stock Returns and Their Volatility Using a GJR-GARCHX Approach: An International Perspective. Journal of Risk and Financial Management. 2021; 14(8):374. https://doi.org/10.3390/jrfm14080374

Chicago/Turabian StyleTomal, Mateusz. 2021. "Modelling the Impact of Different COVID-19 Pandemic Waves on Real Estate Stock Returns and Their Volatility Using a GJR-GARCHX Approach: An International Perspective" Journal of Risk and Financial Management 14, no. 8: 374. https://doi.org/10.3390/jrfm14080374

APA StyleTomal, M. (2021). Modelling the Impact of Different COVID-19 Pandemic Waves on Real Estate Stock Returns and Their Volatility Using a GJR-GARCHX Approach: An International Perspective. Journal of Risk and Financial Management, 14(8), 374. https://doi.org/10.3390/jrfm14080374