Dynamic Impact of Unconventional Monetary Policy on International REITs

Abstract

:1. Introduction

2. Methodology and Data

2.1. Methodology

2.2. Data

3. Empirical Results

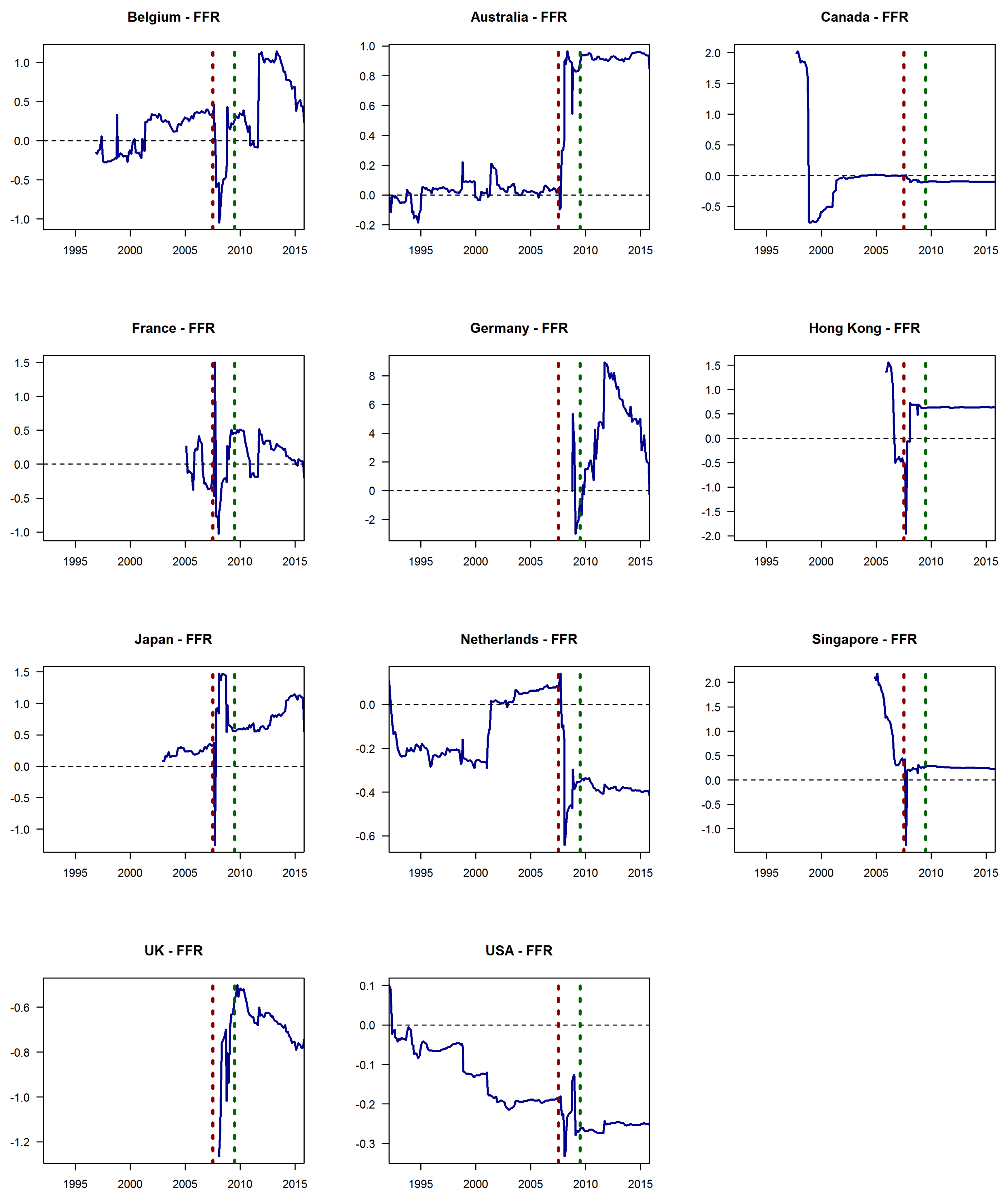

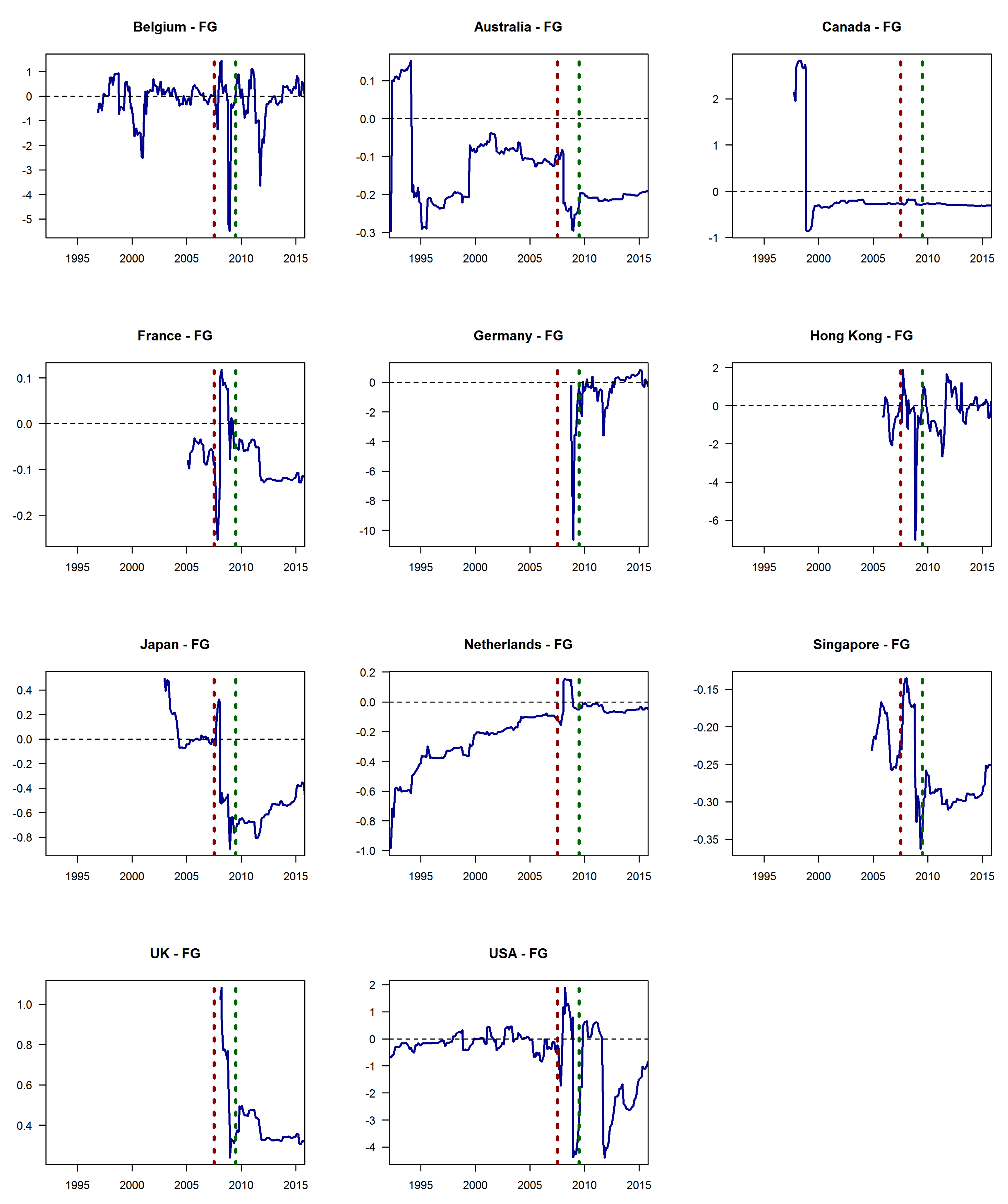

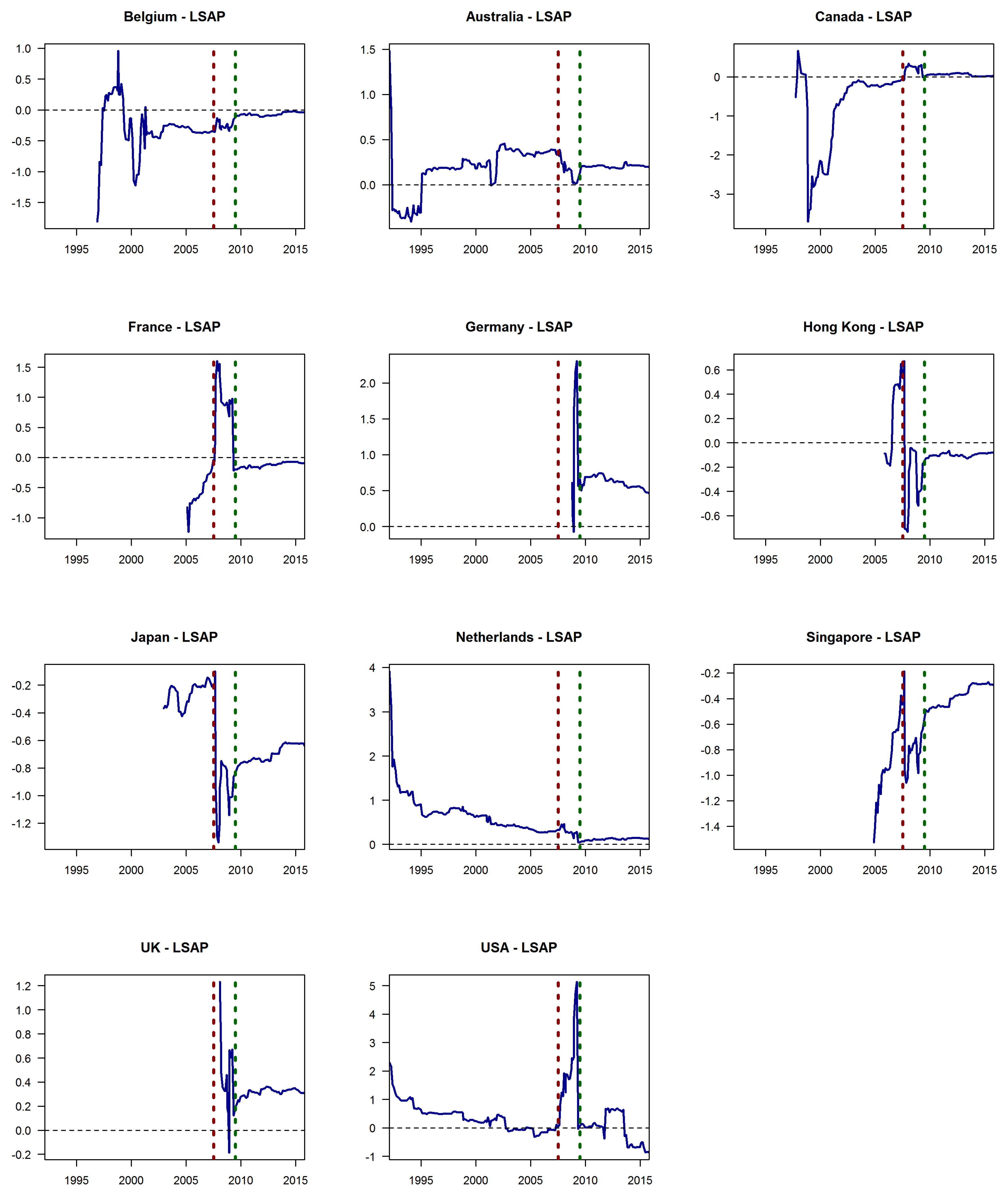

3.1. Dynamic Impact of Unconventional Monetary Policy

3.2. Dynamic Impact, Gold Prices, Exchange Rates, Financial Conditions, and Market-Based Uncertainty

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | The event study approach is one of the most superior approaches because it addresses the two most challenging problems in assessing monetary policy impact, namely, identification and endogeneity. Several studies use this approach including, Cook and Hahn (1989), Kuttner (2001), Bernanke and Kuttner (2005), and Hausman and Wongswan (2011), Marfatia (2014, 2015), Nyakabawo et al. (2018), and Gupta et al. (2019). |

| 2 | An overview of key developments can be found in publications of the European Public Real Estate Association. |

References

- Akinsomi, Omokolade, Goodness C. Aye, Vassilios Babalos, Fotini Economou, and Rangan Gupta. 2016. Real estate returns predictability revisited: Novel evidence from the US REITs market. Empirical Economics 51: 1165–90. [Google Scholar] [CrossRef] [Green Version]

- Batrancea, Ioan, Larissa Batrancea, Malar Maran Rathnaswamy, Horia Tulai, Gheorghe Fatacean, and Mircea-Iosif Rus. 2020. Greening the Financial System in USA, Canada and Brazil: A Panel Data Analysis. Mathematics 8: 2217. [Google Scholar] [CrossRef]

- Bauer, Michael, and Glenn D. Rudebusch. 2014. The Signaling Channel for Federal Reserve Bond Purchases. International Journal of Central Banking 10: 233–89. [Google Scholar] [CrossRef] [Green Version]

- Bauer, Michael D., and Christopher J. Neely. 2014. International channels of the Fed’s unconventional monetary policy. Journal of International Money and Finance 44: 24–46. [Google Scholar] [CrossRef] [Green Version]

- Bernanke, Ben S., and Kenneth N. Kuttner. 2005. What explains the stock market’s reaction to Federal Reserve policy? The Journal of Finance 60: 1221–257. [Google Scholar] [CrossRef] [Green Version]

- Bredemeier, Christian, Christoph Kaufmann, and Andreas Schabert. 2018. Interest Rate Spreads and Forward Guidance. Working Paper Series 2186; Frankfurt: European Central Bank. [Google Scholar]

- Bredin, Don, Gerard O’Reilly, and Simon Stevenson. 2010. Monetary policy transmission and real estate investment trusts. International Journal of Finance & Economics 16: 92–102. [Google Scholar]

- Caraiani, Petre, Rangan Gupta, Chi Keung Marco Lau, and Hardik Arvind Marfatia. 2019. Effects of Conventional and Unconventional Monetary Policy Shocks on Housing Prices in the United States: The Role of Sentiment. Working No. 201953. Pretoria: Department of Economics, University of Pretoria. [Google Scholar]

- Chan, Su Han, Wai-Kin Leung, and Ko Wang. 2005. Changes in REIT Structure and Stock Performance, Evidence from the Monday Stock Anomaly. Real Estate Economics 33: 89–120. [Google Scholar] [CrossRef]

- Chian, Thomas Chinan. 2020. Global Stock Market Prices Response to Uncertainty Changes in US Monetary and Fiscal Policies. In Emerging Market Finance: New Challenges and Opportunities (International Finance Review, Vol. 21). Edited by Bang Nam Jeon and Ji Wu. Bingley: Emerald Publishing Limited, pp. 131–47. [Google Scholar]

- Chou, Yu-Hsi, and Yi-Chi Chen. 2014. Is the Response of REIT Returns to Monetary Policy Asymmetric? Journal of Real Estate Research, American Real Estate Society 36: 109–36. [Google Scholar] [CrossRef]

- Claus, Edda, Iris Claus, and Leo Krippner. 2014. Asset Markets and Monetary Policy Shocks at the Zero Lower Bound. Technical Report. Canberra: Centre for Applied Macroeconomic Analysis, Crawford School of Public Policy, The Australian National University. [Google Scholar]

- Cook, Timothy, and Thomas Hahn. 1989. The effect of changes in the federal funds rate target on market interest rates in the 1970s. Journal of Monetary Economics 24: 331–51. [Google Scholar] [CrossRef] [Green Version]

- Cooley, Thomas F., and Edward C. Prescott. 1976. Estimation in the presence of stochastic parameter variation. Econometrica: Journal of the Econometric Society 44: 167–84. [Google Scholar] [CrossRef]

- European Public Real Estate Associaion (EPRA). 2016. Global REIT Survey 2016. Brussels: European Public Real Estate Associaion. [Google Scholar]

- Feldkircher, Martin, and Florian Huber. 2018. Unconventional U.S. Monetary Policy: New Tools, Same Channels? Journal of Risk and Financial Management 11: 71. [Google Scholar] [CrossRef] [Green Version]

- Gabriel, Stuart A., and Chandler Lutz. 2017. The Impact of Unconventional Monetary Policy on Real Estate Markets. SSRN. 2493873. Available online: https://ssrn.com/abstract=2493873 (accessed on 30 June 2020).

- Gagnon, Joseph, Matthew Raskin, Julie Remache, and Brian Sack. 2011. The Financial Market Effects of the Federal Reserve’s Large-Scale Asset Purchases. International Journal of Central Banking 7: 3–43. [Google Scholar]

- Ghysels, Eric, Alberto Plazzi, Rossen Valkanov, and Walter Torous. 2013. Forecasting Real Estate Prices. In Handbook of Economic Forecasting. Amsterdam: Elsevier, vol. 2, pp. 509–80. [Google Scholar]

- Giliberto, Michael, and David Shulman. 2017. On the Interest Rate Sensitivity of REITs: Evidence from Twenty Years of Daily Data. Journal of Real Estate Portfolio Management 23: 7–20. [Google Scholar] [CrossRef]

- Gray, Colin. 2013. Responding to a Monetary Superpower: Investigating the Behavioral Spillovers of U.S. Monetary Policy. Atlantic Economic Journal 41: 173–84. [Google Scholar] [CrossRef]

- Gupta, Rangan, and Hardik A. Marfatia. 2018. The impact of unconventional monetary policy shocks in the US on emerging market REITs. Journal of Real Estate Literature 26: 175–88. [Google Scholar] [CrossRef]

- Gupta, Rangan, Chi Keng Marco Lau, Ruipeng Liu, and Hardik A. Marfatia. 2019. Price jumps in developed stock markets: The role of monetary policy committee meetings. Journal of Economics and Finance 43: 298–312. [Google Scholar] [CrossRef] [Green Version]

- Gürkaynak, Refet S., Brian Sack, and Eric T. Swanson. 2005. Do Actions Speak Louder Than Words? The Response of Asset Prices to Monetary Policy Actions and Statements. International Journal of Central Banking 1: 55–93. [Google Scholar]

- Haldane, Andrew, Matt Roberts-Sklar, Tomasz Wieladek, and Chris Young. 2016. QE: The Story So Far. Bank of England Working Papers 624. London: Bank of England. [Google Scholar]

- Hausman, Joshua, and Jon Wongswan. 2011. Global asset prices and FOMC announcements. Journal of International Money and Finance 30: 547–71. [Google Scholar] [CrossRef] [Green Version]

- Hesse, Henning, Boris Hofmann, and James Michael Weber. 2018. The macroeconomic effects of asset purchases revisited. Journal of Macroeconomics 58: 115–38. [Google Scholar] [CrossRef] [Green Version]

- Huber, Florian, and Maria Teresa Punzi. 2018. International Housing Markets, Unconventional Monetary Policy and the Zero Lower Bound. Macroeconomic Dynamics 24: 774–806. [Google Scholar] [CrossRef] [Green Version]

- Kishor, N. Kundan, and Hardik A. Marfatia. 2013. The time-varying response of foreign stock markets to US monetary policy surprises: Evidence from the Federal funds futures market. Journal of International Financial Markets, Institutions and Money 24: 1–24. [Google Scholar] [CrossRef]

- Krippner, Leo. 2013. Measuring the stance of monetary policy in zero lower bound environmentst. Economics Letters 118: 135–38. [Google Scholar] [CrossRef] [Green Version]

- Kuttner, Kenneth N. 2001. Monetary policy surprises and interest rates: Evidence from the Fed funds futures market. Journal of Monetary Economics 47: 523–44. [Google Scholar] [CrossRef]

- Lubik, Thomas A., and Christian Matthes. 2015. Time-varying parameter vector autoregressions: Specification, estimation, and an application. Economic Quarterly-Federal Reserve Bank of Richmond 101: 323. [Google Scholar] [CrossRef] [Green Version]

- Lucas, Robert E. 1973. Some International Evidence on Output-Inflation Tradeoff. The American Economic Review 63: 326–34. [Google Scholar]

- Marfatia, Hardik A. 2014. Impact of uncertainty on high frequency response of the US stock markets to the Fed’s policy surprises. The Quarterly Review of Economics and Finance 54: 382–92. [Google Scholar] [CrossRef]

- Marfatia, Hardik A. 2015. Monetary policy’s time-varying impact on the US bond markets: Role of financial stress and risks. The North American Journal of Economics and Finance 34: 103–23. [Google Scholar] [CrossRef]

- Marfatia, Hardik A., Rangan Gupta, and Esin Cakan. 2017. The international REIT’s time-varying response to the US monetary policy and macroeconomic surprises. The North American Journal of Economics and Finance 42: 640–53. [Google Scholar] [CrossRef] [Green Version]

- Miranda-Agrippino, Silvia, and Hélène Rey. 2020. US Monetary Policy and the Global Financial Cycle. Review of Economic Studies 86: 2754–76. [Google Scholar] [CrossRef]

- Nakamura, Emi, and Jón Steinsson. 2018. High-frequency identification of monetary non-neutrality: The information effect. The Quarterly Journal of Economics 133: 1283–330. [Google Scholar] [CrossRef]

- Ngo, Thanh. 2017. Exchange rate exposure of REITs. The Quarterly Review of Economics and Finance 64: 249–58. [Google Scholar] [CrossRef]

- Nyakabawo, Wendy, Rangan Gupta, and Hardik A. Marfatia. 2018. High frequency impact of monetary policy and macroeconomic surprises on US MSAs, aggregate US housing returns and asymmetric volatility. Advances in Decision Sciences 22: 1–25. [Google Scholar]

- Refinitiv. 2020. Datastream International. Available online: https://www.refinitiv.com/ (accessed on 30 June 2020).

- Rosa, Carlo. 2012. How ‘Unconventional’ Are Large-Scale Asset Purchases? The Impact of Monetary Policy on Asset Prices. FRB of New York Staff Report 560. Available online: https://ssrn.com/abstract=2053640 (accessed on 30 June 2020).

- Sahoo, Satyananda, Shiv Shanker, and Jessica M. Anthony. 2020. US Monetary Policy and Spillovers to Select EMEs: An Episodic Analysis. In Financial Issues in Emerging Economies: Special Issue Including Selected Papers from II International Conference on Economics and Finance, 2019, Bengaluru, India (Research in Finance, Vol. 36). Edited by Rita Biswas and Michael Michaelides. Bingley: Emerald Publishing Limited, pp. 67–97. [Google Scholar]

- Smith, A. Lee, and Thealexa Becker. 2015. Has Forward Guidance been Effective? In Economic Review. Kansas City: Federal Reserve Bank of Kansas City, p. 57. [Google Scholar]

- Swanson, Eric T. 2021. Measuring the Effects of Federal Reserve Forward Guidance and Asset Purchases on Financial Markets. Journal of Monetary Economics 118: 32–53. [Google Scholar] [CrossRef]

- Xu, Pisun, and Jian Yang. 2011. US monetary policy surprises and international securitized real estate markets. The Journal of Real Estate Finance and Economics 43: 459–90. [Google Scholar] [CrossRef]

- Yunus, Nafeesa. 2009. Increasing convergence between US and international securitized property market: Evidence based on cointegration tests. Real Estate Economics 37: 383–411. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Country | Code | Mean | Median | Max. | Min. | S.D. | Obs |

|---|---|---|---|---|---|---|---|

| Australia | AU | −0.080 | 0.000 | 4.419 | −11.097 | 1.454 | 213 |

| Belgium | BE | 0.173 | 0.157 | 6.403 | −7.574 | 1.383 | 172 |

| Canada | CA | 0.196 | 0.127 | 6.867 | −8.487 | 1.532 | 165 |

| Germany | DE | 0.202 | 0.401 | 7.387 | −16.128 | 3.619 | 69 |

| France | FR | 0.507 | 0.392 | 4.684 | −4.922 | 1.731 | 103 |

| Hong Kong | HK | −0.220 | 0.000 | 3.122 | −10.061 | 1.502 | 97 |

| Japan | JP | −0.308 | −0.116 | 7.892 | −8.506 | 2.073 | 120 |

| Netherlands | NL | 0.270 | 0.251 | 8.621 | −7.539 | 1.485 | 213 |

| Singapore | SG | 0.063 | 0.089 | 5.710 | −7.869 | 1.575 | 105 |

| UK | UK | 0.509 | 0.457 | 7.696 | −9.179 | 2.550 | 76 |

| USA | US | 0.216 | 0.079 | 13.347 | −21.945 | 2.441 | 213 |

| Australia | Belgium | Canada | |||||||

| FFR | FG | LSAP | FFR | FG | LSAP | FFR | FG | LSAP | |

| FFR | 1.00 | 1.00 | 1.00 | ||||||

| FG | 0.52 | 1.00 | −0.04 | 1.00 | 0.05 | 1.00 | |||

| LSAP | 0.62 | 0.91 | 1.00 | 0.28 | 0.71 | 1.00 | −0.06 | 0.43 | 1.00 |

| Germany | France | Hong Kong | |||||||

| FFR | FG | LSAP | FFR | FG | LSAP | FFR | FG | LSAP | |

| FFR | 1.00 | 1.00 | 1.00 | ||||||

| FG | 0.09 | 1.00 | −0.06 | 1.00 | −0.45 | 1.00 | |||

| LSAP | −0.33 | −0.30 | 1.00 | −0.06 | 0.52 | 1.00 | −0.17 | 0.67 | 1.00 |

| Japan | Netherlands | Singapore | |||||||

| FFR | FG | LSAP | FFR | FG | LSAP | FFR | FG | LSAP | |

| FFR | 1.00 | 1.00 | 1.00 | ||||||

| FG | 0.73 | 1.00 | −0.07 | 1.00 | −0.47 | 1.00 | |||

| LSAP | 0.56 | 0.63 | 1.00 | −0.27 | 0.30 | 1.00 | −0.28 | 0.07 | 1.00 |

| UK | USA | ||||||||

| FFR | FG | LSAP | FFR | FG | LSAP | ||||

| FFR | 1.00 | 1.00 | |||||||

| FG | −0.01 | 1.00 | −0.01 | 1.00 | |||||

| LSAP | 0.03 | −0.38 | 1.00 | 0.45 | −0.23 | 1.00 | |||

| Gold | Exchange Rate | Tr. Spread: 10 Year–3 Month | ||||||||||

| Country | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R |

| Australia | 0.105 | 0.045 | 0.02 | 0.97 | −0.082 | 0.085 | 0.34 | 0.97 | −0.002 | 0.004 | 0.65 | 0.97 |

| Belgium | 0.003 | 0.075 | 0.96 | 0.86 | −0.582 | 0.213 | 0.01 | 0.86 | 0.013 | 0.011 | 0.24 | 0.86 |

| Canada | −0.066 | 0.059 | 0.26 | 0.91 | −0.015 | 0.198 | 0.94 | 0.91 | 0.009 | 0.010 | 0.37 | 0.91 |

| Germany | 3.045 | 2.123 | 0.16 | 0.74 | −8.947 | 3.466 | 0.01 | 0.76 | −0.035 | 0.444 | 0.94 | 0.74 |

| France | −0.331 | 0.322 | 0.31 | 0.26 | −0.474 | 0.486 | 0.33 | 0.26 | 0.056 | 0.030 | 0.07 | 0.30 |

| Hong Kong | −5.045 | 1.508 | 0.00 | 0.75 | 0.250 | 0.431 | 0.56 | 0.71 | 0.067 | 0.028 | 0.02 | 0.74 |

| Japan | −0.001 | 0.002 | 0.47 | 0.59 | −0.667 | 0.389 | 0.09 | 0.60 | 0.013 | 0.024 | 0.58 | 0.60 |

| Netherlands | −0.058 | 0.025 | 0.02 | 0.94 | −0.135 | 0.059 | 0.02 | 0.93 | −0.001 | 0.003 | 0.65 | 0.93 |

| Singapore | 0.079 | 0.202 | 0.70 | 0.84 | −0.039 | 0.321 | 0.90 | 0.84 | 0.004 | 0.020 | 0.85 | 0.84 |

| UK | −0.030 | 0.077 | 0.70 | 0.69 | −0.402 | 0.127 | 0.00 | 0.73 | 0.013 | 0.015 | 0.39 | 0.71 |

| USA | 0.016 | 0.044 | 0.73 | 0.69 | −0.023 | 0.022 | 0.30 | 0.96 | 0.000 | 0.001 | 0.75 | 0.96 |

| TED Spread | Corp Spread: AAA10Y | Corp Spread: BAA10Y | ||||||||||

| Country | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R |

| Australia | 0.000 | 0.010 | 0.96 | 0.97 | 0.011 | 0.012 | 0.38 | 0.97 | 0.008 | 0.007 | 0.27 | 0.97 |

| Belgium | −0.001 | 0.029 | 0.99 | 0.86 | 0.057 | 0.028 | 0.04 | 0.86 | 0.027 | 0.015 | 0.08 | 0.86 |

| Canada | −0.028 | 0.022 | 0.21 | 0.91 | −0.020 | 0.027 | 0.45 | 0.91 | −0.009 | 0.015 | 0.56 | 0.91 |

| Germany | 0.329 | 0.431 | 0.45 | 0.74 | −0.056 | 0.684 | 0.94 | 0.74 | −0.200 | 0.224 | 0.38 | 0.74 |

| France | −0.053 | 0.055 | 0.34 | 0.28 | 0.119 | 0.064 | 0.07 | 0.30 | 0.055 | 0.033 | 0.11 | 0.29 |

| Hong Kong | −0.045 | 0.046 | 0.33 | 0.72 | 0.126 | 0.062 | 0.05 | 0.73 | 0.043 | 0.031 | 0.17 | 0.72 |

| Japan | −0.043 | 0.042 | 0.31 | 0.60 | 0.068 | 0.060 | 0.26 | 0.60 | 0.014 | 0.029 | 0.63 | 0.60 |

| Netherlands | −0.002 | 0.007 | 0.82 | 0.93 | 0.003 | 0.008 | 0.72 | 0.93 | 0.001 | 0.004 | 0.90 | 0.93 |

| Singapore | −0.044 | 0.034 | 0.19 | 0.84 | −0.020 | 0.048 | 0.69 | 0.84 | −0.007 | 0.024 | 0.78 | 0.84 |

| UK | −0.043 | 0.013 | 0.00 | 0.75 | −0.028 | 0.029 | 0.35 | 0.71 | −0.003 | 0.010 | 0.75 | 0.70 |

| USA | 0.005 | 0.003 | 0.04 | 0.96 | −0.005 | 0.003 | 0.11 | 0.96 | −0.004 | 0.002 | 0.03 | 0.96 |

| VIX | ||||||||||||

| Country | Esti. | SE | P-Val | R | ||||||||

| Australia | 0.010 | 0.013 | 0.43 | 0.97 | ||||||||

| Belgium | 0.048 | 0.039 | 0.22 | 0.86 | ||||||||

| Canada | −0.030 | 0.032 | 0.36 | 0.91 | ||||||||

| Germany | 0.241 | 0.530 | 0.65 | 0.74 | ||||||||

| France | 0.071 | 0.078 | 0.36 | 0.28 | ||||||||

| Hong Kong | 0.038 | 0.070 | 0.59 | 0.72 | ||||||||

| Japan | −0.008 | 0.064 | 0.91 | 0.59 | ||||||||

| Netherlands | 0.001 | 0.009 | 0.95 | 0.93 | ||||||||

| Singapore | −0.053 | 0.054 | 0.33 | 0.84 | ||||||||

| UK | −0.010 | 0.020 | 0.62 | 0.70 | ||||||||

| USA | −0.002 | 0.003 | 0.55 | 0.96 | ||||||||

| Gold | Exchange Rate | Spread: 10 Year–3 Month | ||||||||||

| Country | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R |

| Australia | −0.034 | 0.022 | 0.13 | 0.83 | 0.031 | 0.052 | 0.56 | 0.83 | 0.001 | 0.002 | 0.79 | 0.83 |

| Belgium | 0.100 | 0.338 | 0.77 | 0.51 | 1.878 | 0.910 | 0.04 | 0.52 | 0.003 | 0.048 | 0.96 | 0.52 |

| Canada | −0.027 | 0.114 | 0.81 | 0.84 | −0.100 | 0.371 | 0.79 | 0.84 | −0.001 | 0.019 | 0.95 | 0.84 |

| Germany | −0.448 | 2.123 | 0.83 | 0.47 | 6.435 | 3.554 | 0.08 | 0.50 | −0.193 | 0.326 | 0.56 | 0.49 |

| France | 0.064 | 0.034 | 0.06 | 0.78 | 0.078 | 0.049 | 0.12 | 0.78 | 0.001 | 0.003 | 0.83 | 0.78 |

| Hong Kong | 3.003 | 5.085 | 0.56 | 0.40 | 4.886 | 1.493 | 0.00 | 0.47 | −0.108 | 0.096 | 0.26 | 0.42 |

| Japan | 0.002 | 0.001 | 0.11 | 0.92 | 0.076 | 0.143 | 0.60 | 0.92 | −0.019 | 0.009 | 0.04 | 0.93 |

| Netherlands | 0.053 | 0.016 | 0.00 | 0.95 | 0.022 | 0.039 | 0.58 | 0.98 | 0.002 | 0.002 | 0.29 | 0.98 |

| Singapore | 0.015 | 0.016 | 0.36 | 0.89 | 0.084 | 0.026 | 0.00 | 0.90 | −0.004 | 0.002 | 0.05 | 0.89 |

| UK | 0.209 | 0.073 | 0.01 | 0.92 | 0.237 | 0.092 | 0.01 | 0.92 | 0.010 | 0.010 | 0.34 | 0.91 |

| USA | −0.813 | 1.632 | 0.62 | 0.73 | 0.343 | 0.687 | 0.62 | 0.78 | 0.002 | 0.033 | 0.96 | 0.78 |

| TED Spread | AAA10Y | BAA10Y | ||||||||||

| Country | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R |

| Australia | −0.008 | 0.006 | 0.19 | 0.84 | −0.002 | 0.006 | 0.73 | 0.83 | −0.002 | 0.003 | 0.50 | 0.83 |

| Belgium | −0.345 | 0.105 | 0.00 | 0.55 | −0.232 | 0.122 | 0.06 | 0.53 | −0.175 | 0.070 | 0.01 | 0.53 |

| Canada | −0.019 | 0.042 | 0.65 | 0.84 | −0.043 | 0.050 | 0.39 | 0.84 | −0.025 | 0.028 | 0.36 | 0.84 |

| Germany | −3.113 | 0.304 | 0.00 | 0.82 | −3.678 | 0.741 | 0.00 | 0.64 | −1.711 | 0.256 | 0.00 | 0.72 |

| France | 0.002 | 0.006 | 0.77 | 0.78 | 0.001 | 0.007 | 0.92 | 0.77 | 0.000 | 0.004 | 0.99 | 0.77 |

| Hong Kong | −0.384 | 0.161 | 0.02 | 0.45 | −0.176 | 0.226 | 0.44 | 0.42 | −0.209 | 0.119 | 0.08 | 0.43 |

| Japan | −0.015 | 0.015 | 0.33 | 0.93 | −0.068 | 0.023 | 0.00 | 0.93 | −0.032 | 0.011 | 0.00 | 0.93 |

| Netherlands | −0.002 | 0.005 | 0.65 | 0.98 | −0.001 | 0.005 | 0.79 | 0.98 | −0.002 | 0.003 | 0.53 | 0.98 |

| Singapore | −0.007 | 0.003 | 0.05 | 0.89 | −0.012 | 0.004 | 0.00 | 0.90 | −0.008 | 0.002 | 0.00 | 0.91 |

| UK | −0.022 | 0.011 | 0.05 | 0.92 | −0.050 | 0.019 | 0.01 | 0.92 | −0.019 | 0.006 | 0.00 | 0.92 |

| USA | −0.073 | 0.082 | 0.37 | 0.78 | −0.194 | 0.081 | 0.02 | 0.79 | −0.148 | 0.046 | 0.00 | 0.79 |

| VIX | ||||||||||||

| Country | Esti. | SE | P-Val | R | ||||||||

| Australia | −0.008 | 0.008 | 0.30 | 0.84 | ||||||||

| Belgium | −0.442 | 0.155 | 0.01 | 0.54 | ||||||||

| Canada | −0.010 | 0.061 | 0.87 | 0.84 | ||||||||

| Germany | −3.049 | 0.503 | 0.00 | 0.69 | ||||||||

| France | 0.001 | 0.009 | 0.89 | 0.77 | ||||||||

| Hong Kong | −0.418 | 0.265 | 0.12 | 0.43 | ||||||||

| Japan | −0.053 | 0.023 | 0.03 | 0.93 | ||||||||

| Netherlands | −0.004 | 0.006 | 0.50 | 0.98 | ||||||||

| Singapore | −0.012 | 0.004 | 0.01 | 0.90 | ||||||||

| UK | −0.027 | 0.015 | 0.08 | 0.92 | ||||||||

| USA | −0.172 | 0.104 | 0.10 | 0.78 | ||||||||

| Gold | Exchange Rate | Spread: 10 Year–3 Month | ||||||||||

| Country | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R |

| Australia | −0.001 | 0.048 | 0.98 | 0.79 | 0.017 | 0.121 | 0.89 | 0.79 | −0.017 | 0.006 | 0.00 | 0.80 |

| Belgium | 0.130 | 0.063 | 0.04 | 0.67 | −0.215 | 0.211 | 0.31 | 0.70 | 0.000 | 0.011 | 0.99 | 0.70 |

| Canada | −0.215 | 0.134 | 0.11 | 0.90 | −0.164 | 0.365 | 0.65 | 0.90 | 0.016 | 0.021 | 0.43 | 0.90 |

| Germany | 0.443 | 0.417 | 0.29 | 0.28 | 1.408 | 0.683 | 0.04 | 0.31 | −0.043 | 0.065 | 0.52 | 0.29 |

| France | 0.216 | 0.225 | 0.34 | 0.88 | 0.298 | 0.299 | 0.32 | 0.88 | −0.038 | 0.018 | 0.04 | 0.88 |

| Hong Kong | 1.688 | 0.919 | 0.07 | 0.65 | −0.225 | 0.253 | 0.38 | 0.63 | −0.025 | 0.017 | 0.15 | 0.65 |

| Japan | 0.000 | 0.001 | 0.90 | 0.87 | −0.162 | 0.148 | 0.28 | 0.87 | 0.003 | 0.010 | 0.74 | 0.88 |

| Netherlands | −0.020 | 0.023 | 0.39 | 0.96 | 0.008 | 0.127 | 0.95 | 0.95 | −0.013 | 0.006 | 0.03 | 0.95 |

| Singapore | −0.242 | 0.113 | 0.03 | 0.88 | −0.194 | 0.156 | 0.22 | 0.87 | 0.006 | 0.010 | 0.52 | 0.87 |

| UK | 0.015 | 0.115 | 0.89 | 0.08 | −0.048 | 0.218 | 0.83 | 0.08 | −0.050 | 0.023 | 0.03 | 0.17 |

| USA | −1.206 | 1.203 | 0.32 | 0.71 | 0.532 | 0.507 | 0.30 | 0.75 | −0.014 | 0.025 | 0.57 | 0.75 |

| TED Spread | AAA10Y | BAA10Y | ||||||||||

| Country | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R | Esti. | SE | P-Val | R |

| Australia | −0.010 | 0.014 | 0.49 | 0.79 | 0.012 | 0.014 | 0.39 | 0.79 | 0.006 | 0.008 | 0.47 | 0.79 |

| Belgium | 0.009 | 0.024 | 0.71 | 0.70 | −0.001 | 0.027 | 0.96 | 0.70 | −0.006 | 0.015 | 0.68 | 0.70 |

| Canada | −0.036 | 0.041 | 0.39 | 0.90 | 0.004 | 0.048 | 0.94 | 0.90 | 0.003 | 0.027 | 0.90 | 0.90 |

| Germany | 0.057 | 0.083 | 0.50 | 0.29 | 0.409 | 0.132 | 0.00 | 0.39 | 0.104 | 0.043 | 0.02 | 0.35 |

| France | 0.097 | 0.041 | 0.02 | 0.89 | −0.059 | 0.047 | 0.21 | 0.88 | −0.042 | 0.025 | 0.10 | 0.88 |

| Hong Kong | −0.061 | 0.026 | 0.02 | 0.66 | −0.094 | 0.043 | 0.03 | 0.66 | −0.037 | 0.021 | 0.08 | 0.65 |

| Japan | −0.048 | 0.016 | 0.00 | 0.89 | −0.026 | 0.031 | 0.41 | 0.88 | −0.012 | 0.015 | 0.41 | 0.88 |

| Netherlands | 0.009 | 0.015 | 0.53 | 0.95 | −0.031 | 0.016 | 0.05 | 0.95 | −0.024 | 0.009 | 0.01 | 0.95 |

| Singapore | −0.045 | 0.016 | 0.01 | 0.88 | 0.010 | 0.022 | 0.63 | 0.87 | −0.001 | 0.011 | 0.94 | 0.87 |

| UK | −0.017 | 0.020 | 0.40 | 0.12 | 0.050 | 0.045 | 0.28 | 0.12 | 0.004 | 0.015 | 0.80 | 0.11 |

| USA | 0.281 | 0.065 | 0.00 | 0.77 | 0.037 | 0.061 | 0.54 | 0.75 | 0.044 | 0.037 | 0.24 | 0.76 |

| VIX | ||||||||||||

| Country | Esti. | SE | P-Val | R | ||||||||

| Australia | 0.021 | 0.018 | 0.25 | 0.80 | ||||||||

| Belgium | 0.006 | 0.035 | 0.86 | 0.70 | ||||||||

| Canada | −0.032 | 0.060 | 0.59 | 0.90 | ||||||||

| Germany | 0.125 | 0.097 | 0.20 | 0.31 | ||||||||

| France | −0.005 | 0.061 | 0.93 | 0.88 | ||||||||

| Hong Kong | −0.072 | 0.044 | 0.11 | 0.65 | ||||||||

| Japan | −0.041 | 0.029 | 0.16 | 0.88 | ||||||||

| Netherlands | −0.010 | 0.019 | 0.61 | 0.95 | ||||||||

| Singapore | −0.018 | 0.025 | 0.46 | 0.87 | ||||||||

| UK | −0.033 | 0.032 | 0.31 | 0.12 | ||||||||

| USA | 0.161 | 0.081 | 0.05 | 0.76 | ||||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Marfatia, H.A.; Gupta, R.; Lesame, K. Dynamic Impact of Unconventional Monetary Policy on International REITs. J. Risk Financial Manag. 2021, 14, 429. https://doi.org/10.3390/jrfm14090429

Marfatia HA, Gupta R, Lesame K. Dynamic Impact of Unconventional Monetary Policy on International REITs. Journal of Risk and Financial Management. 2021; 14(9):429. https://doi.org/10.3390/jrfm14090429

Chicago/Turabian StyleMarfatia, Hardik A., Rangan Gupta, and Keagile Lesame. 2021. "Dynamic Impact of Unconventional Monetary Policy on International REITs" Journal of Risk and Financial Management 14, no. 9: 429. https://doi.org/10.3390/jrfm14090429

APA StyleMarfatia, H. A., Gupta, R., & Lesame, K. (2021). Dynamic Impact of Unconventional Monetary Policy on International REITs. Journal of Risk and Financial Management, 14(9), 429. https://doi.org/10.3390/jrfm14090429