Do the Underlying Portfolios Matter? A Comparative Study of Equity-Linked Pay-at-Maturity Principal Protected Notes in Canada and the UK

Abstract

:1. Introduction

2. Industry Background

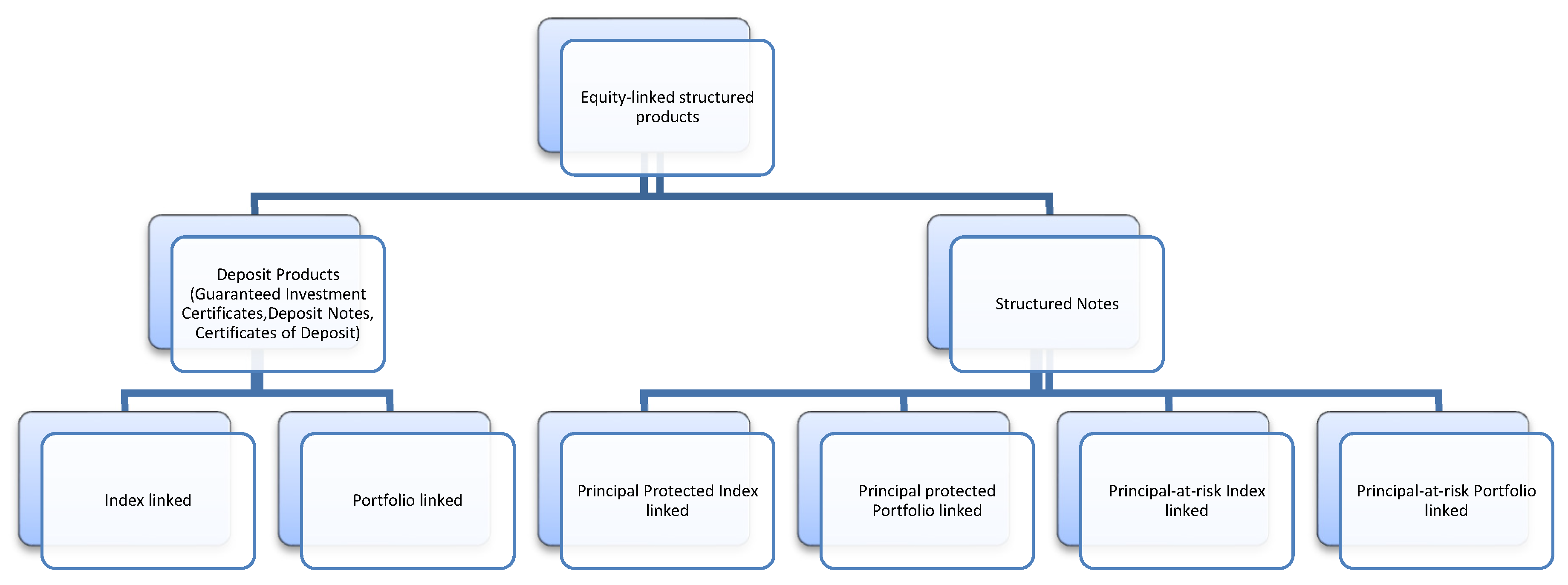

2.1. Typology of Structured Products

2.2. Regulatory Background

2.3. The UK Regulatory Framework

- The name of the product and the identity of the producer;

- The types of investors for whom it is intended;

- The risk and reward profile of the product, which includes a summary risk indicator, the possible maximum loss of invested capital, and appropriate performance scenarios of the products;

- The costs investors have to bear when investing in the product;

- Information about how and to whom an investor can make a complaint in case there is a problem with the product of the person producing, advising on, or selling the product.

2.4. The Canadian Regulatory Framework for Principal Protected Notes

“Principal protected note means a financial instrument that is issued in Canada by an institution to an investor and that

- (a)

- (b)

3. Literature Review and Hypothesis Development

3.1. Prior Literature and Our Contribution

3.2. Hypotheses and Research Design

4. Empirical Results

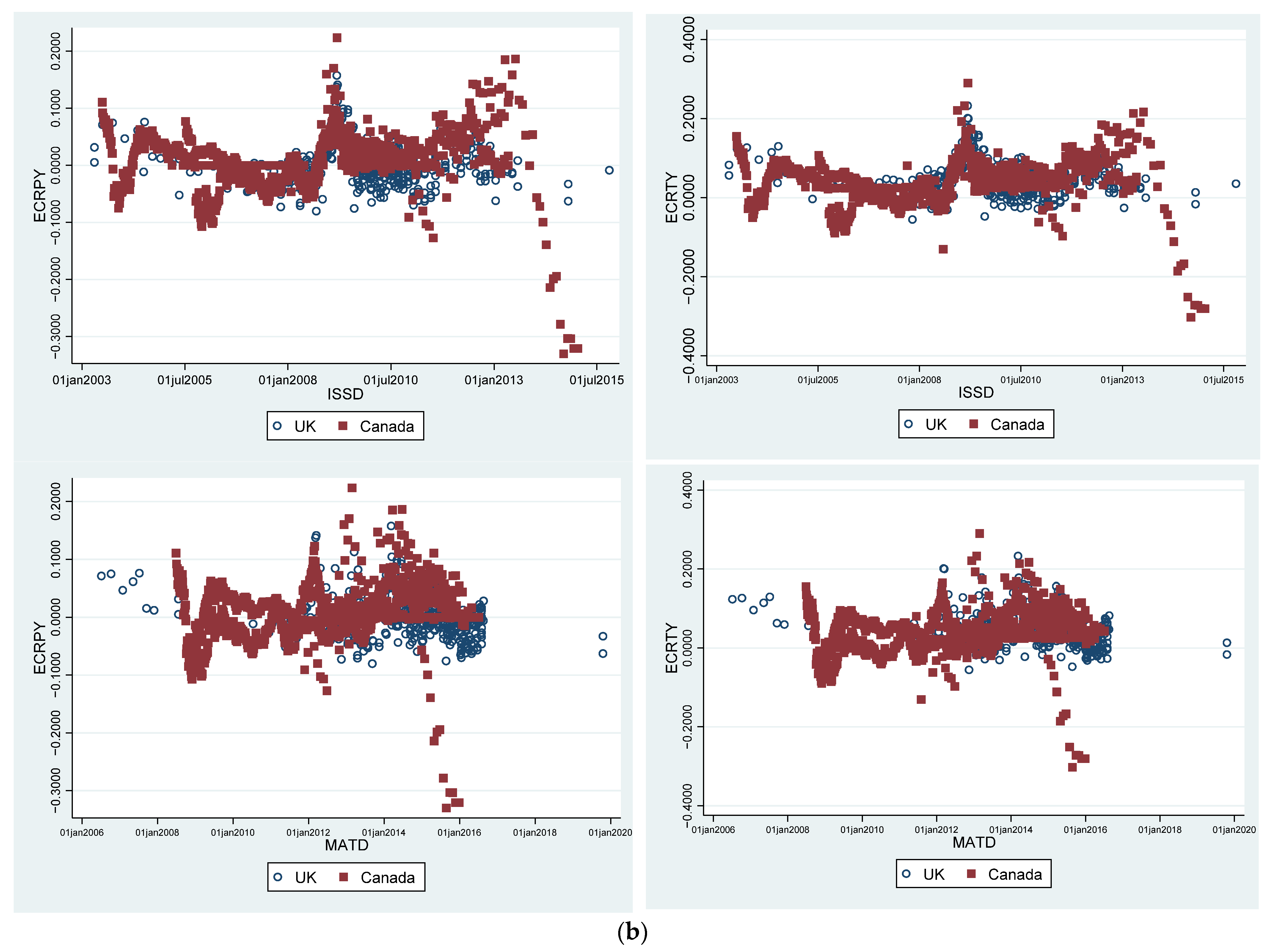

4.1. Data Description and Analysis

4.2. The Distribution of Returns

4.3. The Effects of and on the Return of EL-PAM-PPNs

4.4. The Effects of and on the Holding Cost of EL-PAM-PPNs (or the Excess Return of the Underlying Portfolio)

4.5. What Kind of EL-PAM-PPNs Should Investors Choose?

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Proof of

- (1)

- Let be a constant, and let z be a standard normal random variable, i.e., .where , and is the CDF of .

- (2)

- Let , , then .

- (3)

- (4)

- , or

| 1 | There are no secondary markets for structured products in Canada except as provided by the issuer. In the UK and Europe, a secondary market is available. |

| 2 | See ”What does the Bank of England do?” at https://www.bankofEngland.co.uk/about (accessed on 29 September 2022) and ”Structured Deposits: A consumer’s guide, produced jointly by TISA and the UK Structured Products Association” available at https://www.ukspassociation.co.uk/assets/documents/Structured%20Deposits%20Guide.pdf (accessed on 29 September 2022). The Basel Committee on Banking Supervision (BCBS) Joint Forum report, Point of Sale disclosure in the insurance, banking, and securities sectors, April 2014, notes that in most jurisdictions, only banks are usually able to issue structured deposits, whereas structured notes or certificates are usually issued by investment banks. See http://www.bis.org/publ/joint35.pdf (accessed on 29 September 2022). |

| 3 | See https://www.iosco.org/ (accessed on 29 September 2022). |

| 4 | Understanding UKSPA Risk Ratings for Structured Products: A guide to the UKSPA Risk Ratings for UK financial advisors, available at https://www.ukspassociation.co.uk/assets/documents/UKSPA_RiskRatingsGuide_FINAL.pdf (accessed on 29 September 2022). |

| 5 | See the web site for Structured Edge at http://www.structurededge.co.uk (accessed on 29 September 2022). |

| 6 | See Key information documents for packaged retail and insurance-based investment products (PRIIPs) that can be accessed at https://finance.ec.europa.eu/consumer-finance-and-payments/retail-financial-services/key-information-documents-packaged-retail-and-insurance-based-investment-products-priips_en#documents (accessed on 29 September 2022). |

| 7 | See SOR/2008-180 available at https://laws-lois.justice.gc.ca/eng/Regulations/SOR-2008-180/index.html (accessed on 29 September 2022). |

| 8 | Available from the Minister of Justice at available at https://laws-lois.justice.gc.ca/eng/Regulations/SOR-2008-180/index.html (accessed on 29 September 2022). |

| 9 | SOR/2008-180 Paragraph 13(3), page 6 available at available at https://laws-lois.justice.gc.ca/eng/Regulations/SOR-2008-180/index.html (accessed on 29 September 2022). |

| 10 | CDIC website at https://www.cdic.ca/your-coverage/protecting-your-deposit/principal-protected-notes/ (accessed on 29 September 2022). |

| 11 | IIROC Guidance Note 10-0233 31 August 2010 Principal Protected Notes Compliance Review: Findings, Requirements and Recommendations available at https://www.iiroc.ca/news-and-publications/notices-and-guidance/principal-protected-notes-compliance-review-findings-requirements-and-recommendations (accessed on 29 September 2022), and IIROC Guidance Note 12-034 18 December 2012 Sale of principal protected notes by Approved Persons of IIROC Dealer Members available at: https://www.iiroc.ca/news-and-publications/notices-and-guidance/sale-principal-protected-notes-approved-persons-iiroc-dealer-members (accessed on 29 September 2022). |

References

- Basel Committee on Banking Supervision. 2014. Point of Sale Disclosure in the Insurance, Banking and Securities Sectors, the Basel Committee on Banking Supervision Joint Forum Report. April. Available online: http://www.bis.org/publ/joint35.pdf (accessed on 29 September 2022).

- Bertrand, Philippe, and Jean-Luc Prigent. 2015. French Retail Financial Structured Products: A Typology and Assessment of Their Fair Pricing. Available online: http://ssrn.com/abstract=2513231 (accessed on 29 September 2022).

- Burth, Stefan, Thomas Kraus, and Hanspeter Wohlwend. 2001. The Pricing of structured products in the Swiss Market. Journal of Derivatives 9: 30–40. [Google Scholar] [CrossRef]

- Deng, Geng, Dulaney Tim, Husson Tim, and McCann Craig J. 2014. Structured Certificates of Deposit: Introduction and Valuation. Financial Services Review 23: 219–37. [Google Scholar] [CrossRef] [Green Version]

- Heinzl, John. 2016. A ‘growth GIC’? It sounds seductive, but I’ll pass. The Globe and Mail, December 2. [Google Scholar]

- International Organization of Securities Commissions. 2013a. Suitability Requirements with Respect to the Distribution of Complex Financial Products. Available online: https://www.iosco.org/library/pubdocs/pdf/IOSCOPD400.pdf (accessed on 29 September 2022).

- International Organization of Securities Commissions. 2013b. Regulation of Retail Structured Products. December 20. Available online: https://www.iosco.org/library/pubdocs/pdf/IOSCOPD434.pdf (accessed on 29 September 2022).

- Krein, David. 2007. Rethinking Principal Protection. The Journal of Wealth Management 9: 62–68. [Google Scholar] [CrossRef]

- Milevsky, Moshe Arye, and Sharon Kim. 1997. The Optimal Choice of Index-Linked GICs: Some Canadian Evidence. Financial Services Review 64: 271–84. [Google Scholar] [CrossRef]

- Milstead, David. 2016. Market-based GICs: A look under the hood. The Globe and Mail. Available online: http://www.theglobeandmail.com/globe-investor/investment-ideas/market-based-gics-a-look-under-the-hood/article28353990/ (accessed on 29 September 2022).

- Rathgeber, Andreas, and Yun Wang. 2011. Market pricing of credit-linked notes: The case of retail structured products in Germany. Journal of Credit Risk 7: 73–101. [Google Scholar] [CrossRef] [Green Version]

- Roseman, Ellen. 2014. Avoid GICs Linked to Stock Markets: Roseman. The Toronto Star. Available online: http://www.thestar.com/business/personal_finance/2014/02/02/you_can_profit_by_avoiding_packaged_gics_roseman.html (accessed on 29 September 2022).

- Stoimenov, Pavel A., and Sascha Wilkens. 2005. Are structured products ‘fairly’ priced? An analysis of the German market for equity-linked instruments. Journal of Banking & Finance 29: 2971–93. [Google Scholar]

- Wallmeier, Martin, and Martin Diethelm. 2009. Market Pricing of Exotic Structured Products: The Case of Multi-Asset Barrier Reverse Convertibles in Switzerland. The Journal of Derivatives 17: 59–72. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable Name | Description |

|---|---|

| YTM | Years to maturity when issued |

| CDIC | The note may be insured by CDIC or FSCS, 1 if yes, 0 if no |

| BACK | The issuer can call the product, 1 if yes 0 if no |

| FEE | Account fee payable, 1 if yes, 0 if no |

| GPR | Guaranteed positive return, 1 if yes, 0 if no |

| VOA | 1 if the note return is calculated as a vanilla option, 2 if the note return is calculated as an Asian option, 0 otherwise |

| OBY | The number of performance observations per year |

| OBT | The total number of performance observations over the life of EL-PAM-PPNs |

| NSK | The number of stocks in the underlying portfolio |

| CAPSR | The cap on the positive return of individual stocks, 1000 if no cap |

| CASSR | Any positive stock return is treated as a digital option, 1000 if not digital |

| FLRSR | The floor on the negative stock return |

| DIVL | The stock dividend yield in the year before product issuance |

| PCRUP | The fixed rate the investor can receive as a percentage of the underlying portfolio’s return |

| CAPUP | A cap on the positive return of the underlying portfolio, 1 if yes, 0 if no |

| CAPAUP | The cap on the positive return of the underlying portfolio, 1000 if no cap |

| BUP | Estimated beta of the underlying portfolio |

| PRUP | The price return on the note’s underlying portfolio |

| TRUP | The total return (price and dividends) on the note’s underlying portfolio |

| NR | The return paid on the structured product |

| CTRY | 0 if Canada, 1 if United Kingdom |

| IDXL | 1 if linked to an index; 0 if not |

| EVOL | Expected volatility calculated as the standard deviation of the daily price return on the underlying asset or index (indices) calculated for the 365 days prior to issue date |

| RVOL | Realized volatility calculated as the standard deviation of daily price return on the underlying portfolio or index (indices) calculated from the issue date to the maturity (or call) date |

| ISSY | Issuance year of EL-PAM-PPN |

| MATY | Maturity year of EL-PAM-PPN |

| Canada | Portfolio-Based | Index-Linked | Subtotal |

| Structured Notes | 36 | 20 | 56 |

| GICs | 127 | 918 | 1045 |

| Subtotal | 163 | 938 | 1101 |

| UK | Portfolio-Based | Index-Linked * | Subtotal |

| Structured Notes | 0 | 228 | 228 |

| Deposit Notes | 0 | 239 | 239 |

| Subtotal | 0 | 467 | 467 |

| UK | Obs | Mean | SD | Min | Max |

| NR | 467 | 0.2194 | 0.1471 | 0.0000 | 0.8574 |

| ECRP | 467 | −0.0079 | 0.1643 | −0.4530 | 0.7884 |

| ECRT | 467 | 0.2044 | 0.1981 | −0.2846 | 1.1642 |

| ECRPY | 467 | 0.0000 | 0.0343 | −0.0802 | 0.1577 |

| ECRTY | 467 | 0.0445 | 0.0415 | −0.0552 | 0.2328 |

| Canada | Obs | Mean | SD | Min | Max |

| NR | 1101 | 0.0968 | 0.1300 | 0.0000 | 0.9723 |

| ECRP | 1101 | 0.0410 | 0.1491 | −0.3754 | 0.8864 |

| ECRT | 1101 | 0.1665 | 0.1839 | −0.3911 | 1.1492 |

| ECRPY | 1101 | 0.0083 | 0.0490 | −0.3301 | 0.2236 |

| ECRTY | 1101 | 0.0396 | 0.0537 | −0.3028 | 0.2899 |

| UK | Positive | Outperform |

| ECRP, ECRPY | 217 | 46.4668% |

| ECRT, ECRTY | 407 | 87.1520% |

| Canada | Positive | Outperform |

| ECRP, ECRPY | 650 | 59.0372% |

| ECRT, ECRTY | 902 | 81.9255% |

| UK | Canada | t-Stats | |

| NR | 21.9448% | 9.6768% | −15.6187 |

| ECRP | −0.7874% | 4.0990% | 5.5335 |

| ECRT | 20.4360% | 16.6497% | −3.5347 |

| ECRPY | 0.0009% | 0.8326% | 3.8375 |

| ECRTY | 4.4511% | 3.9635% | −1.9411 |

| NR | ECRP | ECRT | ECRPY | ECRTY | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | SE | Mean | SE | Mean | SE | Mean | SE | Mean | SE | |

| FI1 | 25.47% | 1.63% | 1.65% | 1.84% | 26.53% | 2.12% | 0.62% | 0.40% | 5.77% | 0.46% |

| FI2 | 22.81% | 1.44% | 1.00% | 2.66% | 24.55% | 2.96% | 0.48% | 0.53% | 5.31% | 0.60% |

| FI3 | 28.93% | 4.48% | −2.62% | 4.14% | 26.35% | 4.23% | −0.40% | 0.72% | 4.47% | 0.76% |

| FI4 | 45.00% | 0.00% | −32.07% | 1.86% | −4.55% | 2.14% | −5.35% | 0.31% | −0.76% | 0.36% |

| FI5 | 9.21% | 0.41% | 3.14% | 0.52% | 15.75% | 0.65% | 0.42% | 0.17% | 3.51% | 0.19% |

| FI6 | 8.31% | 0.83% | 3.90% | 0.99% | 14.03% | 1.23% | 1.30% | 0.33% | 4.53% | 0.40% |

| FI7 | 5.06% | 0.79% | 9.46% | 1.20% | 19.55% | 1.34% | 3.83% | 0.51% | 7.37% | 0.56% |

| FI8 | 20.82% | 0.98% | 0.99% | 1.10% | 19.37% | 1.31% | 0.48% | 0.26% | 5.21% | 0.29% |

| FI9 | 29.10% | 0.71% | −6.76% | 1.83% | 17.22% | 2.05% | −1.35% | 0.37% | 3.44% | 0.41% |

| FI10 | 19.21% | 2.09% | −2.53% | 2.23% | 22.91% | 2.66% | −0.16% | 0.44% | 4.46% | 0.53% |

| FI11 | 21.47% | 3.08% | 7.00% | 1.03% | 22.68% | 0.87% | 1.79% | 0.24% | 4.82% | 0.27% |

| FI12 | 25.78% | 9.58% | −1.64% | 1.29% | 26.91% | 3.40% | −0.40% | 0.32% | 4.61% | 0.68% |

| FI13 | 12.54% | 1.93% | −10.80% | 1.56% | −0.80% | 1.87% | −2.10% | 0.31% | −0.10% | 0.36% |

| FI14 | 17.25% | 2.01% | 31.20% | 3.72% | 45.40% | 4.16% | 6.58% | 0.77% | 9.53% | 0.83% |

| FI15 | 42.50% | −33.78% | −7.56% | −5.63% | . | −1.26% | . | |||

| UK | Canada | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Variable | Obs | Mean | SD | Min | Max | Obs | Mean | SD | Min | Max |

| YTM | 467 | 4.5658 | 1.2394 | 1.0000 | 6.0000 | 1101 | 3.9570 | 1.3016 | 0.9589 | 8.0301 |

| CDIC | 467 | 0.5118 | 0.5004 | 0.0000 | 1.0000 | 1101 | 0.9491 | 0.2198 | 0.0000 | 1.0000 |

| BACK | 467 | 0.0835 | 0.2770 | 0.0000 | 1.0000 | 1101 | 0.0227 | 0.1490 | 0.0000 | 1.0000 |

| FEE | 467 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 1101 | 0.0227 | 0.1490 | 0.0000 | 1.0000 |

| GPR | 467 | 0.2869 | 0.4528 | 0.0000 | 1.0000 | 1101 | 0.0572 | 0.2324 | 0.0000 | 1.0000 |

| VOA | 467 | 1.8694 | 0.3498 | 0.0000 | 2.0000 | 1101 | 1.7911 | 0.4067 | 1.0000 | 2.0000 |

| OBY | 400 | 59 | 55 | 0 | 250 | 1101 | 5 | 2 | 1 | 12 |

| OBT | 400 | 59 | 54 | 0 | 250 | 1101 | 5 | 3 | 1 | 20 |

| NSK | 467 | 115 | 107 | 40 | 875 | 1101 | 53 | 16 | 10 | 60 |

| CAPSR | 467 | 842 | 365 | 0 | 1000 | 1101 | 955 | 208 | 0 | 1000 |

| CASSR | 467 | 703 | 457 | 0 | 1000 | 1101 | 955 | 208 | 0 | 1000 |

| FLRSR | 467 | −1.0000 | 0.0000 | −1.0000 | −1.0000 | 1101 | −0.9591 | 0.1875 | −1.0000 | −0.1000 |

| DIVL | 467 | 0.0381 | 0.0111 | 0.0000 | 0.0613 | 1101 | 0.0264 | 0.0064 | 0.0000 | 0.0657 |

| PCRUP | 461 | 1.4552 | 1.1508 | 0.5000 | 5.0000 | 1101 | 0.6395 | 0.2187 | 0.2000 | 1.1500 |

| CAPUP | 467 | 0.7666 | 0.4235 | 0.0000 | 1.0000 | 1101 | 0.0581 | 0.2341 | 0.0000 | 1.0000 |

| CAPAUP | 362 | 20 | 138 | 0 | 1000 | 1101 | 938 | 241 | 0 | 1000 |

| BUP | 299 | 1.0000 | 0.0000 | 1.0000 | 1.0000 | 1101 | 0.9835 | 0.2597 | 0.4122 | 7.1440 |

| EVOL | 467 | 0.0142 | 0.0058 | −0.0136 | 0.0392 | 1101 | 0.0125 | 0.0074 | 0.0050 | 0.0778 |

| RVOL | 465 | 0.0109 | 0.0026 | 0.0019 | 0.0221 | 1101 | 0.0129 | 0.0056 | 0.0057 | 0.1104 |

| PRUP | 467 | 0.2116 | 0.2058 | −0.3639 | 0.8884 | 1101 | 0.1378 | 0.2300 | −0.3165 | 1.1480 |

| TRUP | 467 | 0.4238 | 0.2635 | −0.2762 | 1.3369 | 1101 | 0.2633 | 0.2694 | −0.3911 | 1.3992 |

| IDXL | 467 | 1.0000 | 0.0000 | 1.0000 | 1.0000 | 1101 | 0.8520 | 0.3553 | 0.0000 | 1.0000 |

| NR | 467 | 0.2194 | 0.1471 | 0.0000 | 0.8574 | 1101 | 0.0968 | 0.1300 | 0.0000 | 0.9723 |

| ECRP | 467 | −0.0079 | 0.1643 | −0.4530 | 0.7884 | 1101 | 0.0410 | 0.1491 | −0.3754 | 0.8864 |

| ECRT | 467 | 0.2044 | 0.1981 | −0.2846 | 1.1642 | 1101 | 0.1665 | 0.1839 | −0.3911 | 1.1492 |

| ECRPY | 467 | 0.0010 | 0.0358 | −0.0802 | 0.1577 | 1101 | 0.0083 | 0.0490 | −0.3301 | 0.2236 |

| ECRTY | 467 | 0.0475 | 0.0426 | −0.0552 | 0.2328 | 1101 | 0.0396 | 0.0537 | −0.3028 | 0.2899 |

| ISSY | 467 | 2009 | 2 | 2003 | 2015 | 1101 | 2008 | 2 | 2003 | 2015 |

| MATY | 467 | 2014 | 2 | 2006 | 2019 | 1101 | 2012 | 2 | 2008 | 2016 |

| UK Note Return (NR) | Canada Note Return (NR) | |||||

|---|---|---|---|---|---|---|

| Model 3a | Model 3b | Model 3c | Model 3a | Model 3b | Model 3c | |

| YTM | 0.0212 *** | 0.0184 *** | −0.0813 *** | 0.0515 *** | 0.0364 *** | 0.00705 |

| (4.08) | (3.52) | (−6.30) | (8.69) | (6.61) | (0.62) | |

| CDIC | −0.0185 | −0.0208 | −0.0223 * | 0.0110 | 0.00334 | −0.0253 |

| (−1.14) | (−1.39) | (−2.13) | (0.22) | (0.06) | (−0.49) | |

| BACK | −0.000490 | 0.0301 | −0.0215 | 0.0705 | 0.151 * | 0.163 * |

| (−0.02) | (0.92) | (−1.00) | (1.06) | (2.21) | (2.55) | |

| FEE | 0 | 0 | 0 | 0.0290 | 0.0285 | −0.0340 |

| (.) | (.) | (.) | (0.69) | (0.68) | (−0.77) | |

| GPR | 0.0564 *** | 0.0490 *** | 0.0320 ** | −0.113 *** | −0.0967 *** | −0.0732 *** |

| (3.83) | (3.71) | (2.94) | (−6.11) | (−5.04) | (−3.85) | |

| VOA | −0.104 *** | −0.0620 *** | −0.0555 *** | −0.0548 | 0.0182 | 0.0195 |

| (−7.51) | (−3.84) | (−4.46) | (−1.27) | (0.47) | (0.49) | |

| OBT | 0.000474 * | 0.000353 * | 0.000245 | 0.00251 | −0.00268 | −0.00417 |

| (2.44) | (2.01) | (1.81) | (0.73) | (−0.93) | (−1.41) | |

| NSK | −0.000131 * | −0.000127 * | 0.000244 *** | −0.00232 * | −0.00144 | −0.00124 |

| (−2.48) | (−2.20) | (3.90) | (−2.41) | (−1.57) | (−1.30) | |

| CAPSR | −0.0000166 | −0.0000160 | 0.00000534 | −0.0000763** | −0.0000675 ** | −0.0000225 |

| (−0.80) | (−0.83) | (0.37) | (−3.30) | (−2.97) | (−0.86) | |

| DIVL | 0.881 | 0.781 | −2.108 *** | −1.628 * | −0.886 | −1.384 * |

| (1.36) | (1.15) | (−3.61) | (−2.47) | (−1.44) | (−2.29) | |

| CAPUP | −0.0651 ** | −0.0468 | −0.0700 *** | 0.0412 | 0.0283 | 0.0123 |

| (−2.75) | (−1.93) | (−3.93) | (0.89) | (0.66) | (0.27) | |

| PCRUP | 0.0403 *** | 0.0325 *** | 0.0204 *** | −0.0680 | 0.0332 | 0.0346 |

| (7.82) | (6.52) | (4.40) | (−1.02) | (0.60) | (0.61) | |

| EVOL | 12.80 *** | 16.41 *** | 9.837 *** | 0.886 | −0.241 | −0.940 |

| (8.82) | (9.55) | (7.74) | (1.30) | (−0.42) | (−1.60) | |

| RVOL | −10.22 *** | −13.18 *** | −17.55 *** | −1.547 | −0.430 | −0.441 |

| (−3.71) | (−4.60) | (−8.72) | (−0.53) | (−0.17) | (−0.17) | |

| ECRP | −0.274 *** | −2.469 *** | 0.258 *** | −0.617 * | ||

| (−4.19) | (−7.73) | (5.70) | (−2.06) | |||

| ECRT | 1.933 *** | 0.781 ** | ||||

| (7.53) | (2.97) | |||||

| BUP | −0.0140 | −0.00545 | −0.0140 | |||

| (−0.96) | (−0.36) | (−1.02) | ||||

| CONS | 0.210 ** | 0.127 | 0.400 *** | 0.275 ** | 0.0783 | 0.110 |

| (3.19) | (1.75) | (8.28) | (3.09) | (0.89) | (1.28) | |

| N | 396 | 396 | 396 | 1101 | 1101 | 1101 |

| Adj. R | 0.479 | 0.532 | 0.756 | 0.332 | 0.390 | 0.410 |

| UK | Canada | |||||||

|---|---|---|---|---|---|---|---|---|

| ECRP | ECRT | ECRPY | ECRTY | ECRP | ECRT | ECRPY | ECRTY | |

| YTM | −0.0100 | 0.0402 *** | −0.00521 ** | −0.00415 * | 0.0587 *** | 0.103 *** | 0.0146 *** | 0.0183 *** |

| (−1.49) | (4.97) | (−3.20) | (−2.21) | (8.99) | (14.18) | (7.10) | (8.03) | |

| CDIC | −0.00843 | −0.00879 | −0.00504 | −0.00492 | 0.0297 | 0.0699 | 0.0222 * | 0.0336 ** |

| (−0.45) | (−0.40) | (−1.24) | (−1.03) | (0.75) | (1.65) | (2.22) | (3.08) | |

| BACK | 0.112 *** | 0.153 *** | 0.0244 *** | 0.0328 *** | −0.310 *** | −0.364 *** | −0.0615 *** | −0.0707 *** |

| (4.28) | (5.17) | (4.84) | (5.63) | (−5.29) | (−5.42) | (−4.16) | (−4.12) | |

| FEE | 0 | 0 | 0 | 0 | 0.00168 | 0.0821 | 0.0113 | 0.0273 * |

| (.) | (.) | (.) | (.) | (0.04) | (1.73) | (1.05) | (2.15) | |

| GPR | −0.0270 | −0.0219 | −0.000348 | 0.00116 | −0.0614 | −0.0991 ** | −0.0272 *** | −0.0367 *** |

| (−1.36) | (−0.95) | (−0.08) | (0.24) | (−1.93) | (−2.95) | (−3.67) | (−4.60) | |

| VOA | 0.153 *** | 0.170 *** | 0.0272 *** | 0.0303 *** | −0.282 *** | −0.318 *** | −0.0821 *** | −0.0929 *** |

| (9.60) | (9.16) | (7.88) | (7.57) | (−5.83) | (−5.77) | (−5.55) | (−5.59) | |

| OBT | −0.000441 * | −0.000445 | −0.0000679 | −0.0000696 | 0.0201 *** | 0.0244 *** | 0.00748 *** | 0.00901 *** |

| (−2.06) | (−1.79) | (−1.57) | (−1.40) | (6.41) | (6.58) | (6.32) | (6.79) | |

| NSK | 0.0000135 | −0.000177 * | −0.00000312 | −0.0000391 * | −0.00339 *** | −0.00406 *** | −0.00137 *** | −0.00162 *** |

| (0.28) | (−2.29) | (−0.32) | (−2.59) | (−3.41) | (−3.45) | (−4.35) | (−4.56) | |

| CAPSR | 0.00000226 | −0.00000847 | −0.00000649 | −0.00000811 | −0.0000342 | −0.0000959 * | 0.0000119 | −0.00000267 |

| (0.09) | (−0.29) | (−1.10) | (−1.21) | (−0.86) | (−2.31) | (0.56) | (−0.12) | |

| DIVL | −0.362 | 1.084 | −0.160 | 0.0907 | −2.872 * | −2.583 | −1.286 ** | −1.248 ** |

| (−0.58) | (1.15) | (−1.21) | (0.47) | (−2.31) | (−1.82) | (−3.29) | (−2.91) | |

| CAPUP | 0.0669 * | 0.0880 * | 0.00676 | 0.0105 | 0.0499 | 0.0765 | 0.0326 * | 0.0427 ** |

| (2.41) | (2.57) | (1.22) | (1.58) | (1.18) | (1.52) | (2.39) | (2.75) | |

| PCRUP | −0.0282 *** | −0.0258 ** | −0.00456 ** | −0.00397 * | −0.392 *** | −0.441 *** | −0.129 *** | −0.144 *** |

| (−3.64) | (−2.87) | (−2.83) | (−2.14) | (−6.16) | (−6.09) | (−5.82) | (−5.93) | |

| EVOL | 13.15 *** | 18.34 *** | 2.722 *** | 3.781 *** | 4.362 *** | 5.788 *** | 0.916 *** | 1.211 *** |

| (6.98) | (8.30) | (6.78) | (8.17) | (5.28) | (5.54) | (4.34) | (4.73) | |

| RVOL | −10.79 *** | −9.991 * | −2.370 *** | −2.256 ** | −4.321 * | −4.833 * | −1.801 * | −1.924 * |

| (−3.65) | (−2.49) | (−3.56) | (−2.59) | (−2.06) | (−2.05) | (−2.13) | (−2.12) | |

| BUP | −0.0330 *** | −0.0260 * | −0.00411 | −0.00316 | ||||

| (−3.49) | (−2.37) | (−1.22) | (−0.84) | |||||

| CONS | −0.302 *** | −0.485 *** | −0.0235 | −0.0132 | 0.760 *** | 0.812 *** | 0.231 *** | 0.281 *** |

| (−5.20) | (−5.78) | (−1.66) | (−0.69) | (5.96) | (5.72) | (5.51) | (6.16) | |

| N | 396 | 396 | 396 | 396 | 1101 | 1101 | 1101 | 1101 |

| Adj. R | 0.355 | 0.402 | 0.338 | 0.385 | 0.334 | 0.432 | 0.283 | 0.317 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, Y.; Anderson, S.; McGraw, P.A. Do the Underlying Portfolios Matter? A Comparative Study of Equity-Linked Pay-at-Maturity Principal Protected Notes in Canada and the UK. J. Risk Financial Manag. 2022, 15, 462. https://doi.org/10.3390/jrfm15100462

Li Y, Anderson S, McGraw PA. Do the Underlying Portfolios Matter? A Comparative Study of Equity-Linked Pay-at-Maturity Principal Protected Notes in Canada and the UK. Journal of Risk and Financial Management. 2022; 15(10):462. https://doi.org/10.3390/jrfm15100462

Chicago/Turabian StyleLi, Yuanshun, Scott Anderson, and Patricia A. McGraw. 2022. "Do the Underlying Portfolios Matter? A Comparative Study of Equity-Linked Pay-at-Maturity Principal Protected Notes in Canada and the UK" Journal of Risk and Financial Management 15, no. 10: 462. https://doi.org/10.3390/jrfm15100462

APA StyleLi, Y., Anderson, S., & McGraw, P. A. (2022). Do the Underlying Portfolios Matter? A Comparative Study of Equity-Linked Pay-at-Maturity Principal Protected Notes in Canada and the UK. Journal of Risk and Financial Management, 15(10), 462. https://doi.org/10.3390/jrfm15100462