Global Spillovers of a Chinese Growth Slowdown

Abstract

:1. Introduction

2. Literature Review

3. Sources of Vulnerabilities in China and Transmission Channels to the Rest of the World

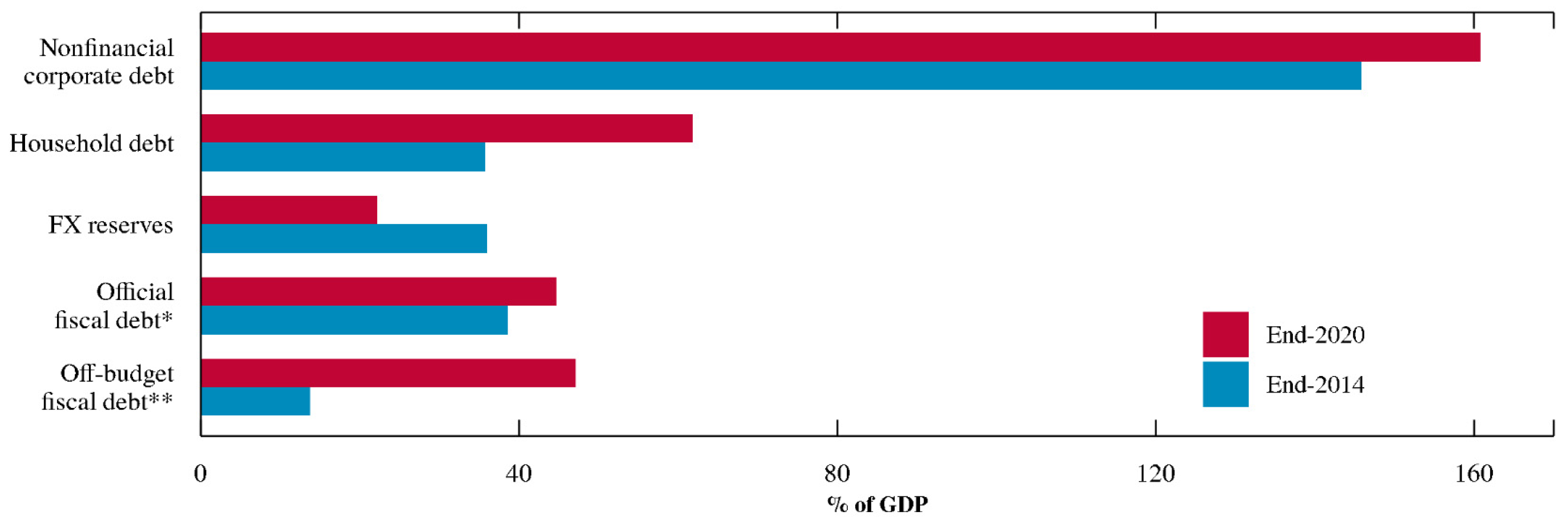

3.1. Financial Vulnerabilities

3.2. China’s Trade and Financial Linkages with the Rest of the World

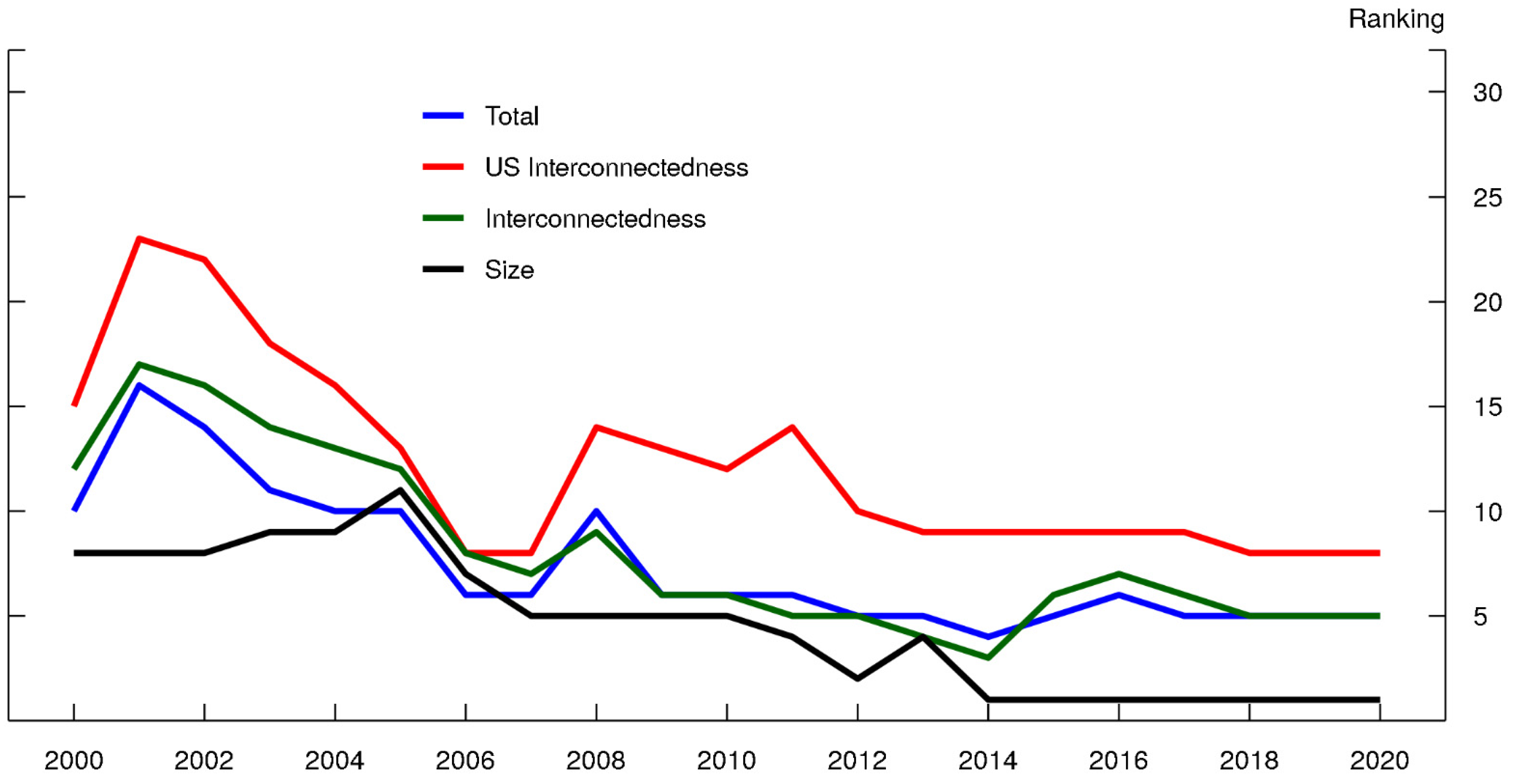

3.3. U.S. Financial Institutions’ Direct and Indirect Exposures to China

4. Quantifying the Spillovers

4.1. Methodology

4.1.1. First Stage

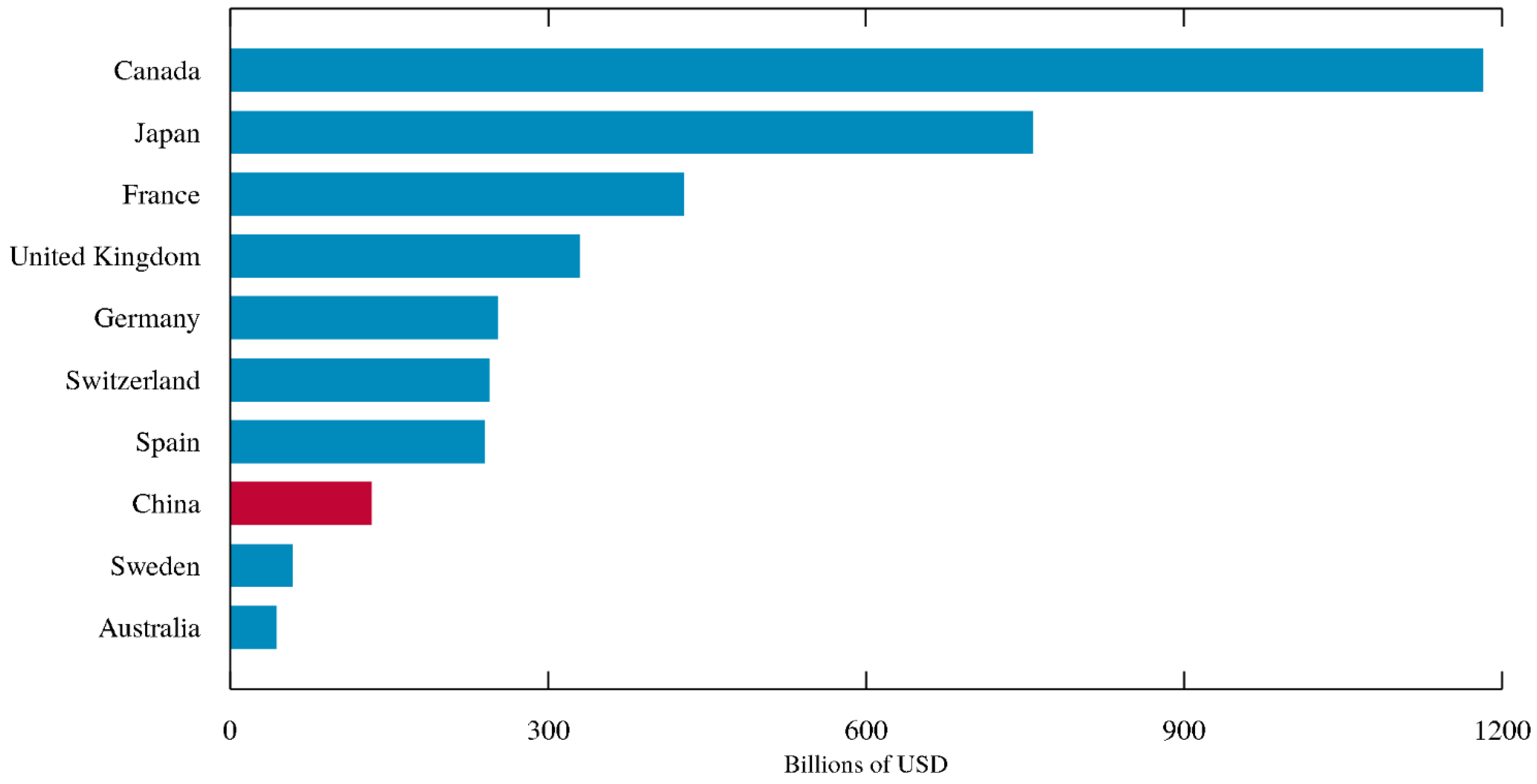

4.1.2. Second Stage

4.2. Results

4.2.1. First-Stage Results

4.2.2. Second-Stage Results

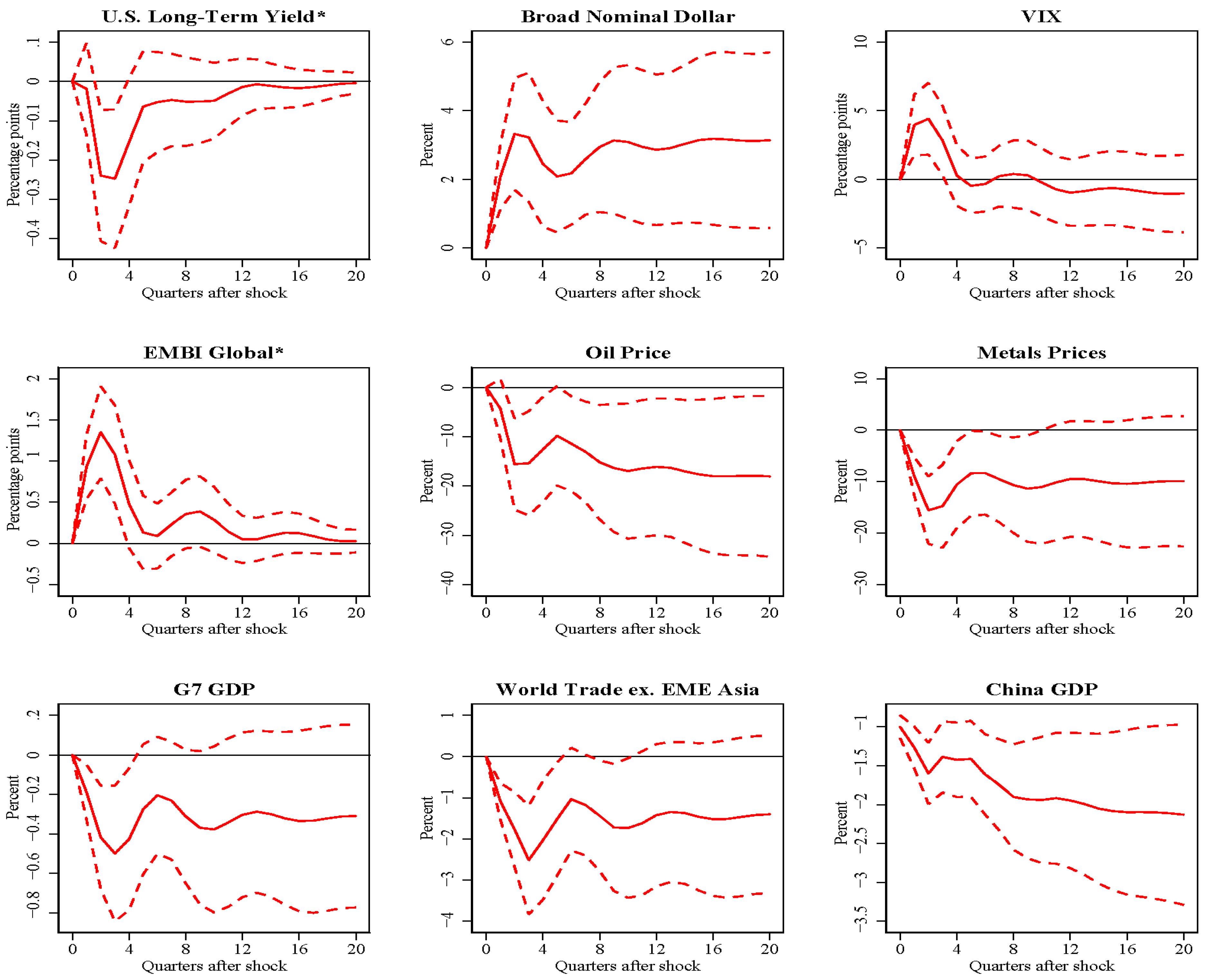

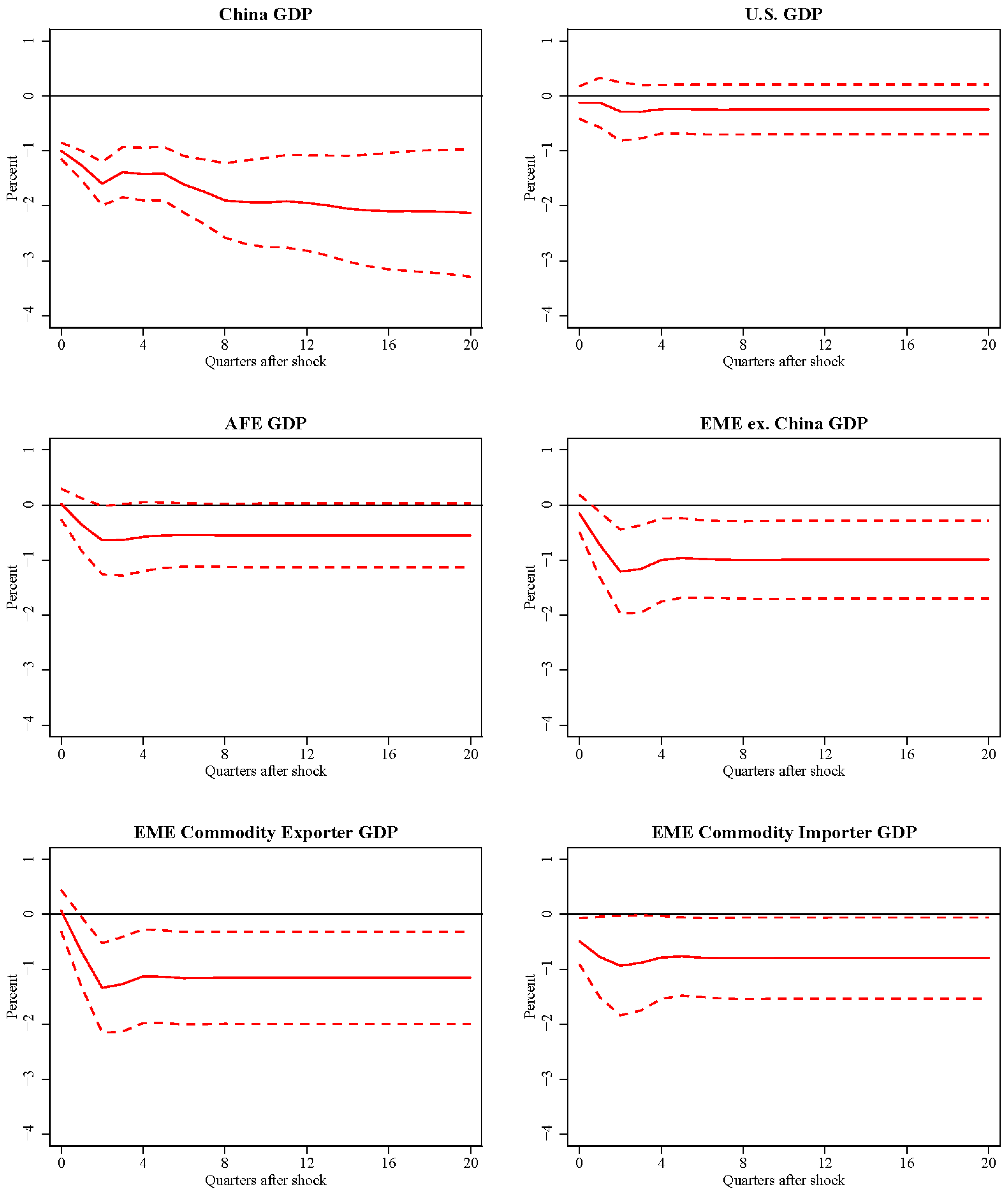

4.2.3. Spillovers of a China GDP Growth Slowdown

5. Spillovers Using DSGE Model Simulations

- (1)

- A sudden, discrete 2 percent devaluation of the Chinese renminbi against the dollar occurred on 11 August 2015, which triggered a depreciation in many emerging market currencies and appreciation of the U.S. dollar.

- (2)

- A precipitous drop in the Chinese stock market occurred on 24 August 2015, that became known as “China’s Black Monday”, where the Shanghai stock index declined by almost 8½ percent of its value overnight.

- (3)

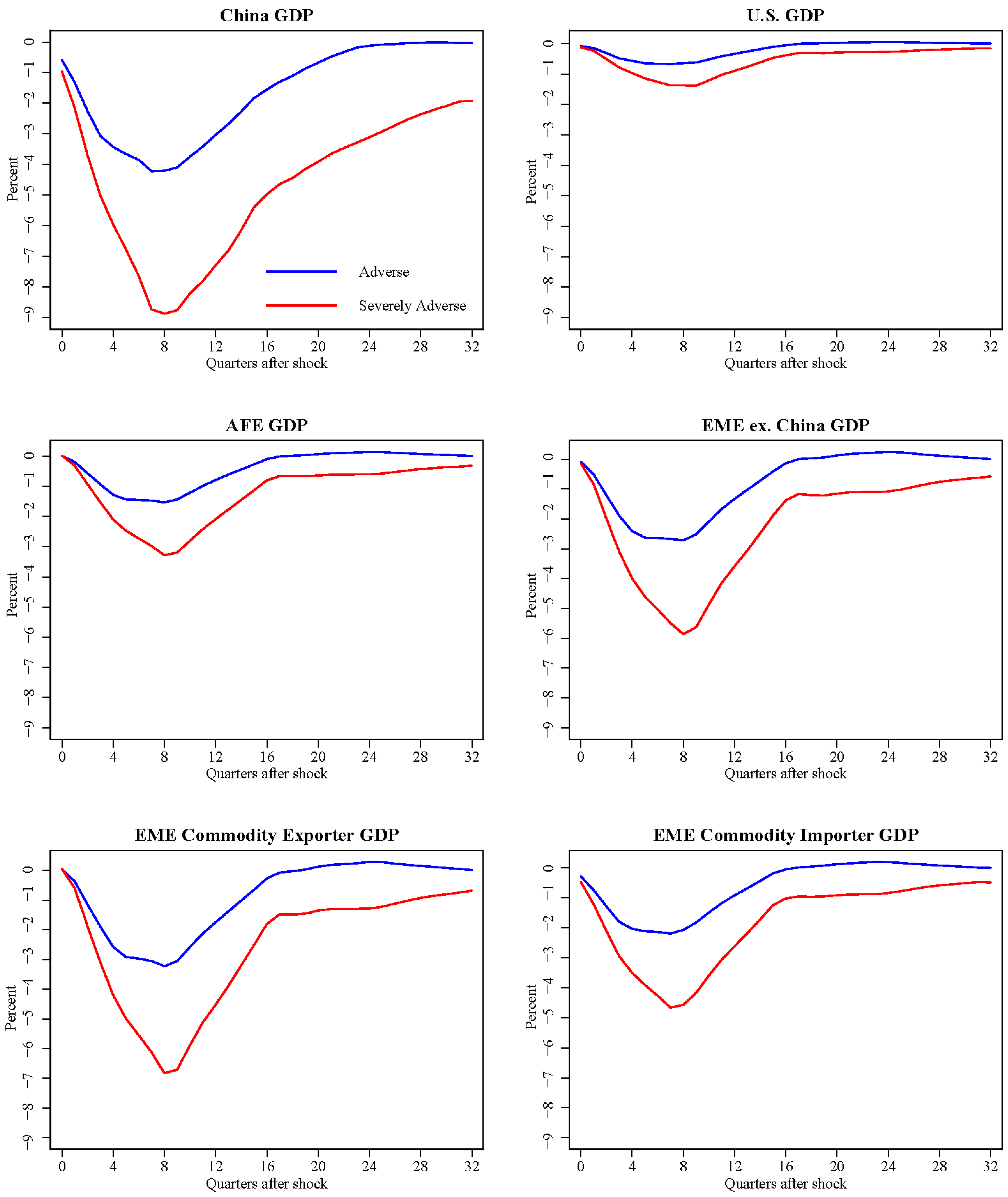

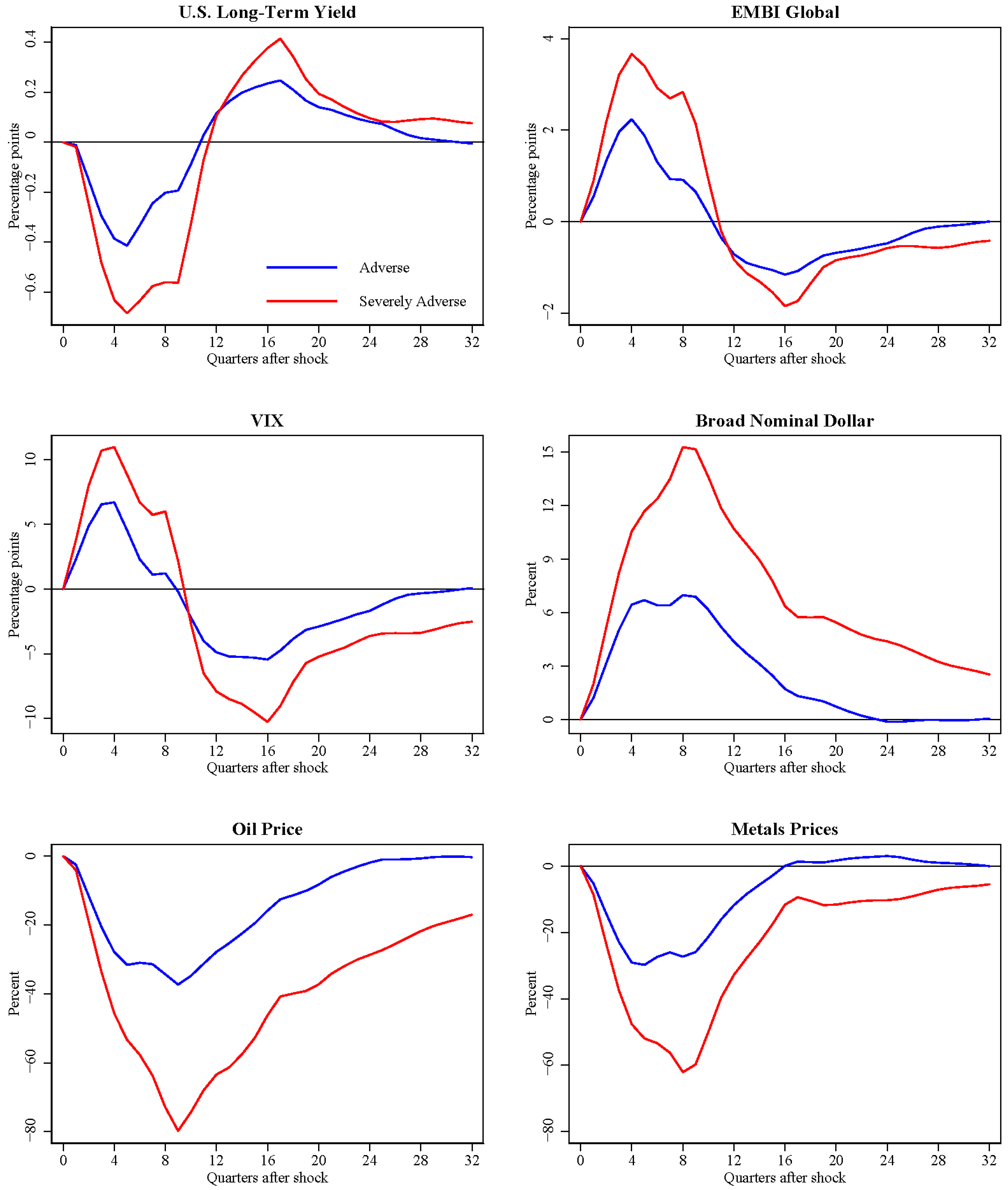

- Two large and sudden declines in the Chinese stock market of more than 7 percent occurred between 4–7 January 2016, that led to the trigger of automatic circuit breakers that halted trading.25 Capital outflows continued during these episodes.

6. Conclusions

Supplementary Materials

Author Contributions

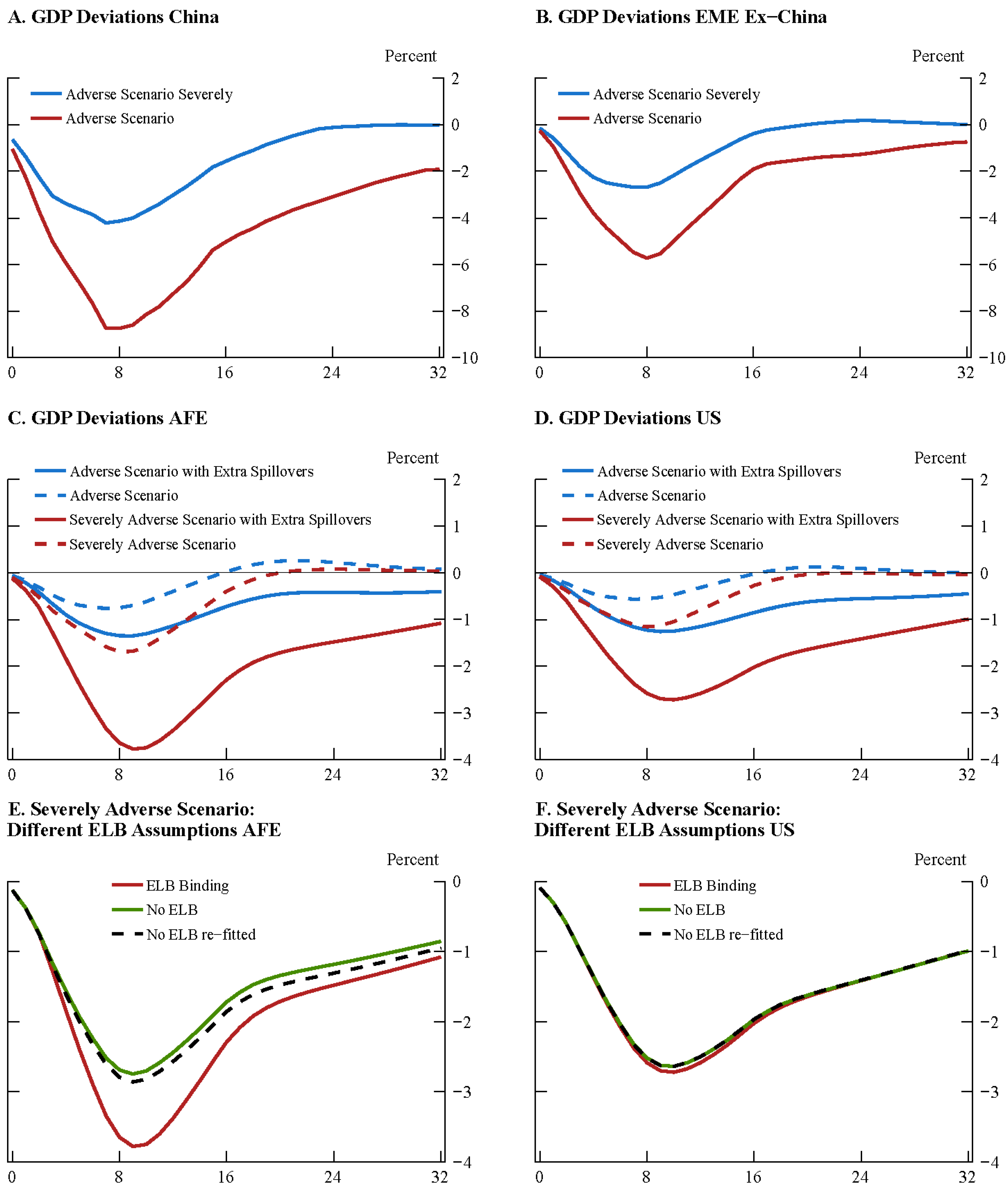

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | Using the DSGE model also allows us to provide a more forward-looking estimate in some regards, as the estimation of the SVAR necessarily forces us to use a long-time span in the data. |

| 2 | Ericsson et al. (2014) use both VAR and GVAR models to study the effects on global growth of a China GDP growth slowdown and find that the results based on the two models are broadly comparable (especially in the short-to-medium term). |

| 3 | Barro (2016) predicted China’s per capita growth rate in a conditional-convergence framework estimated from a large panel of countries. He estimated China’s per capita growth rate in 2015 to be 3.5 percent and declining, in contrast to the official 6 to 7 percent per year. He concluded that it is unlikely that China can deviate in the long run from the results predicted by global historical growth experience. |

| 4 | Almost half of the 11 countries that have sustained this level of debt as a percent of GDP experienced a financial crisis within five years of crossing this threshold. |

| 5 | The main products in the Chinese shadow-banking sector are trust company loans, entrusted loans, and WMPs. Trust companies manage assets for high-net individuals and institutions and invest in a range of products including bank loans and corporate bonds and loans. Entrusted loans are loans made by one nonfinancial firm to another nonfinancial firm, with a bank serving as an intermediary. WMPs are short-term investment products, often marketed by banks that invest in both equity and fixed-income products. |

| 6 | LGFVs are entities founded by local governments to finance projects on their behalf. They enjoy implicit debt repayment support but are legally separate from the government. The use of these off-budget vehicles has greatly expanded after the GFC. In recent years, the central government has attempted to clamp down on this off-budget borrowing by prohibiting local governments from providing support to LGFVs while at the same time allowing local governments greater leeway to borrow on-budget. Nonetheless, LGFV borrowing has continued to grow. |

| 7 | A financial stability event encompasses financial crises and other periods of financial stress not officially classified as crises that create notable financial disruptions. |

| 8 | To construct the rankings, we use information from the Bank for International Settlements (BIS), Bloomberg, Haver Analytics, and the International Monetary Fund (IMF). The size category is composed of a measure of real GDP, equity and bond market capitalization, and the size of the banking sector and other nonbank financial institutions. For interconnectedness we use measures of trade, foreign direct investment, and cross-border portfolio investments and bank loans. |

| 9 | If at least two of the series in the size category have observed values (i.e., are not missing) for a country in a given year, then we calculate the size ranking for that country; otherwise, we set that ranking to “missing”. For the interconnectedness and U.S. interconnectedness series, we require a minimum of four observed values to calculate the ranking for the country in a specific year. To calculate the overall ranking for a country, we require at least two categories with nonmissing rankings. |

| 10 | For U.S. banks, these bank exposures are collected in the Federal Financial Institutions Examination Council (FFIEC) 009 report, and bank capital information is aggregated using the reporting in the FFIEC 031 and FR Y-9C forms. Note that the FFIEC 009 report provides a conservative measure of exposures. Claims are only adjusted for explicit third-party guarantees, near-perfect hedges, and certain liquid collateral held outside the country of the borrower. |

| 11 | Banks in the United Kingdom have the largest exposures to China and Hong Kong (Table 2), with claims representing 181 percent of this banking sector’s Tier 1 capital. |

| 12 | Available data suggest holdings of Chinese securities represent only about 1 percent of U.S. portfolio investment, even when including securities issued through offshore affiliates (from Treasury International Capital (TIC) data by residence, adjusted to a nationality basis using the methodology of Bertaut et al. (2019)). |

| 13 | U.S. bank exposures to EME commodity exporters totaled almost $300 billion at the end of June 2021 (Table 4). |

| 14 | Money market funds’ exposure to Chinese financial institutions was $2.5 billion at the end of September 2021 (Table 5), mostly in unsecured instruments (such as time deposits). |

| 15 | We begin our sample in 2002:Q1 to avoid the structural break introduced by the entry of China into the WTO and the resulting increase in international trade. Indeed, when we extend our sample back to 1990:Q1, we find significantly smaller effects of a reduction in Chinese growth on international variables. We also end the sample period in 2017:Q4 to avoid the uncertainty generated due to the trade tensions between the United States and China and the COVID pandemic. More detailed results from this analysis are available from the authors upon request. |

| 16 | Part A of the Supplementary Materials provides a more detailed description of the VAR model and how the shocks are identified. |

| 17 | The eight global variables are ordered as follows: U.S. long-term yields, broad nominal dollar, VIX, EMBI spreads, oil prices, metals prices, G-7 economies’ GDP growth, and growth of global imports excluding Asian EMEs. |

| 18 | During the GFC, the correlation between some of the variables and China’s GDP was very strong, which translates into larger estimated effects of internally originated shocks to China’s GDP on some of the other variables (both variables analyzed in the first stage and variables analyzed in the second stage) when the GFC dummy variable is not included in the model. Results without the GFC dummy variable are available from the authors upon request. |

| 19 | For ease of exposition, we will use “China GDP shock” and “domestic China GDP shock” interchangeably throughout the rest of the paper. Unless specifically noted, we are always referring to the part of unexpected fluctuations in China’s GDP growth that can be attributed to domestic factors. |

| 20 | The confidence intervals shown in Figure 6 should be seen as a lower bound for the real size of the 90 percent confidence intervals around the estimated impulse response functions because we did not account for the fact that the China GDP shocks were estimated in the first stage. Ultimately, what these confidence intervals tell us is that the effects of a China GDP slowdown are quite uncertain, and therefore any policy response to such an event should take this high degree of uncertainty into consideration. |

| 21 | We estimate the historical impact on growth of financial crises by computing the difference between the average annualized real GDP growth in the two years before a financial crisis with the average real GDP growth in the two years after a financial crisis. The financial crisis episodes are taken from the database compiled by Reinhart and Rogoff (2011) and Laeven and Valencia (2013). These estimates exclude the most recent wave of economic recessions caused by the COVID-19 pandemic. |

| 22 | To obtain the sequence of shocks hitting China’s GDP that generate GDP paths such as those in the top panel of Figure 7, we use the estimated impulse response functions from the first-stage SVAR to account for the dynamic effects of the shocks in China’s GDP but also on the global variables included in the model. We also had to make the simplifying assumption that these shocks were serially uncorrelated. |

| 23 | Part B of the Supplementary Materials provides a brief summary of the SIGMA model. |

| 24 | Using price quotes from Bloomberg, we compute the market return and level changes from the previous day’s close (4 p.m. Eastern Standard Time) to the event day’s open (9 a.m. Eastern Standard Time). This uniform time horizon allows us to capture the pre-market open in China (4 a.m. China Standard Time) and post-market close (9 p.m. China Standard Time), even though the European markets and U.S. markets continue trading after the end of our event window. This timing convention is used for all assets in Table 6 except for U.S. corporate spreads, which is the previous day close (4 p.m. Eastern Standard Time) to the event day close (4 p.m. Eastern Standard Time). |

| 25 | The automatic circuit breakers led to a halting of trading for brief periods and also led, early in the day on 7 July, after a quick 7 percent decline, to a suspension of trading for the remainder of the day. The circuit breakers were later abandoned because, outside of the period when trading stood suspended, they appeared to increase volatility. |

| 26 | As the current version of SIGMA has only an aggregate EME bloc, we use the results from our SVAR to construct an overall EME GDP response to an adverse growth event in China. In each simulation, we feed in a series of shocks to the EMEs in our SIGMA model to mimic the response in each of our two Chinese adverse scenarios. Therefore, the GDP responses of the EMEs, shown in Figure 9, panels A and B, are by construction identical to the ones embedded in the SVAR analysis. |

| 27 | We also used a set of demand shocks triggered two years before the crisis begins to place the model into an initial policy rate condition similar to the world economy in mid-2018. These initial conditions are interesting as they allow for the possibility of a binding ELB in one, but not both, of the two advanced economy blocs in the simulation. All simulation results are reported as deviations from the paths implied by those initial shocks. We used data from Haver Analytics and the World Economic Outlook to construct that baseline. |

| 28 | The GDP losses occur despite an accommodative U.S. monetary policy response, which follows the model’s policy reaction function. |

| 29 | In the simulation, the ELB binds for seven quarters. |

References

- Ahmed, Shaghil. 2017. China’s Footprints on the Global Economy: Remarks Delivered at the Second IMF and Federal Reserve Bank of Atlanta Research Workshop on the Chinese Economy; IFDP Notes. Washington, DC: Board of Governors of the Federal Reserve System, September 28. Available online: https://www.federalreserve.gov/econres/notes/ifdp-notes/chinas-footprints-on-the-global-economy-20170928.htm (accessed on 1 October 2021).

- Aldasoro, Iñaki, Claudio Borio, and Mathias Drehmann. 2018. Early Warning Indicators of Banking Crises: Expanding the Family. BIS Quarterly Review, 29–45. Available online: https://www.bis.org/publ/qtrpdf/r_qt1803e.pdf (accessed on 1 October 2021).

- Barro, Robert J. 2016. Economic Growth and Convergence, Applied Especially to China. NBER Working Paper Series 21872; Cambridge: National Bureau of Economic Research. Available online: https://www.nber.org/papers/w21872 (accessed on 1 October 2021).

- Bernanke, Ben, Jean Boivin, and Piotr Eliasz. 2005. Measuring the Effects of Monetary Policy: A Factor Augmented Vector Autoregressive (FAVAR) Approach. Quarterly Journal of Economics 120: 387–422. [Google Scholar]

- Bertaut, Carol, Beau Bressler, and Stephanie Curcuru. 2019. Globalization and the Geography of Capital Flows. FEDS Notes. Washington, DC: Board of Governors of the Federal Reserve System, September 6. [Google Scholar] [CrossRef]

- Buch, Claudia, and Linda Goldberg. 2015. International Banking and Liquidity Risk Transmission: Lessons from Across Countries. IMF Economic Review 63: 377–410. [Google Scholar] [CrossRef] [Green Version]

- Cecchetti, Stephen, Madhusudan Mohanty, and Fabrizio Zampolli. 2011. The Real Effects of Debt. BIS Working Papers No. 352. Basel: Bank for International Settlements, September, Available online: https://www.bis.org/publ/work352.pdf (accessed on 1 October 2021).

- Cetorelli, Nicola, and Linda Goldberg. 2012. Follow the Money: Quantifying Domestic Effects of Foreign Bank Shocks in the Great Recession. American Economic Review 102: 213–18. [Google Scholar] [CrossRef] [Green Version]

- Chen, Sally, and Joong Shik Kang. 2018. Credit Booms—Is China Different? IMF Working Paper No. 18/2. Washington, DC: International Monetary Fund, January, Available online: https://www.imf.org/en/Publications/WP/Issues/2018/01/05/Credit-Booms-Is-China-Different-45537 (accessed on 1 October 2021).

- Correa, Ricardo, Horacio Sapriza, and Andrei Zlate. 2021. Wholesale Funding Runs, Global Banks’ Supply of Liquidity Insurance, and Corporate Investment. Journal of International Economics 133: 103519. [Google Scholar] [CrossRef]

- Dell’Ariccia, Giovanni, Deniz Igan, Luc Laeven, and Hui Tong. 2016. Credit Booms and Macrofinancial Stability. Economic Policy 31: 299–355. [Google Scholar] [CrossRef]

- Dieppe, Alister, Robert Gilhooly, Jenny Han, Iikka Korhonen, and David Lodge. 2018. The Transition of China to Sustainable Growth–Implications for the Global Economy and the Euro Area. ECB Occasional Paper Series No. 206; Frankfurt: European Central Bank, January, Available online: https://www.ecb.europa.eu/pub/pdf/scpops/ecb.op206.en.pdf (accessed on 1 October 2021).

- Ehlers, Thorsten, Steven Kong, and Feng Zhu. 2018. Mapping Shadow Banking in China: Structure and Dynamics. BIS Working Paper No. 701. Basel: Bank for International Settlements. Available online: https://www.bis.org/publ/work701.pdf (accessed on 1 October 2021).

- Eichengreen, Barry, Donghyun Park, and Kwanho Shin. 2012. When Fast-Growing Economies Slow Down: International Evidence and Implications for China. Asian Economic Papers 11: 42–87. [Google Scholar] [CrossRef]

- Ericsson, Neil, Lucas Husted, and J. E. Seymour. 2014. Potential Spillovers of a Sudden Slowdown in China. Unpublished paper. Board of Governors of the Federal Reserve System. [Google Scholar]

- Erten, Bilge. 2012. Macroeconomic transmission of Eurozone shocks to emerging economies. Economie Internationale 131: 43–70. [Google Scholar] [CrossRef]

- European Central Bank. 2017. China’s economic growth and rebalancing and the implications for the global and euro area economies. ECB Economic Bulletin Volume 7: 32–52. [Google Scholar]

- Fontaine, Idriss, Laurent Didier, and Justinien Razafindravaosolonirina. 2017. Foreign policy uncertainty shocks and US macroeconomic activity: Evidence from China. Economics Letters 155: 121–25. [Google Scholar] [CrossRef]

- Gauvin, Ludovic, and Cyril C. Rebillard. 2018. Towards Recoupling? Assessing the Global Impact of a Chinese Hard Landing Through Trade and Commodity Price Channels. World Economy 41: 3379–415. [Google Scholar] [CrossRef] [Green Version]

- Gilhooly, Robert, Jen Han, Simon Lloyd, Niamh Reynolds, and David Young. 2018. From the Middle Kingdom to the United Kingdom: Spillovers from China. In Quarterly Bulletin 2018 Q2. London: Bank of England. Available online: https://www.bankofengland.co.uk/quarterly-bulletin/2018/2018-q2/from-the-middle-kingdom-to-the-united-kingdom-spillovers-from-china (accessed on 1 October 2021).

- Hsieh, Chang-Tai, and Peter J. Klenow. 2009. Misallocation and Manufacturing TFP in China and India. Quarterly Journal of Economics 124: 1403–48. [Google Scholar] [CrossRef]

- Huang, Zhuo, Chen Tong, Han Qiu, and Yan Shen. 2018. The Spillover of Macroeconomic Uncertainty between the U.S. and China. Economic Letters 171: 123–27. [Google Scholar] [CrossRef]

- Laeven, Luc, and Fabian Valencia. 2013. Systemic Banking Crises Database. IMF Economic Review 61: 225–70. [Google Scholar] [CrossRef] [Green Version]

- Lee, Jong-Wha, and Kiseok Hong. 2010. Economic Growth in Asia: Determinants and Prospects. Asian Development Bank Economics Working Paper Series, (220); Mandaluyong: Asian Development Bank. [Google Scholar]

- Lee, Seung J., Kelly E. Posenau, and Viktors Stebunovs. 2020. The Anatomy of Financial Vulnerabilities and Banking Crises. Journal of Banking and Finance 112: 105334. [Google Scholar] [CrossRef]

- Li, Cindy. 2016. The Changing Face of Shadow Banking in China. Asia Focus. San Francisco: Federal Reserve Bank of San Francisco, December, Available online: https://www.frbsf.org/banking/wp-content/uploads/sites/5/Asia-Focus-The-Changing-Face-of-Shadow-Banking-in-China-December-2016.pdf (accessed on 1 October 2021).

- Li, Jianjun, Sara Hsu, and Yanzhi Qin. 2014. Shadow Banking in China: Institutional Risks. China Economic Review 31: 119–29. [Google Scholar] [CrossRef] [Green Version]

- Ma, Guonan, Ivan Roberts, and Gerard Kelly. 2017. Rebalancing China’s Economy: Domestic and International Implications. China & World Economy 25: 1–31. [Google Scholar]

- Manu, Ana-Simona, Peter McAdam, and Alpo Willman. 2018. The Role of Factor Substitution and Technical Progress in China’s Great Expansion. ECB Working Paper No. 2180. Frankfurt: European Central Bank, September, Available online: https://www.ecb.europa.eu/pub/pdf/scpwps/ecb.wp2180.en.pdf (accessed on 1 October 2021).

- McCauley, Robert N., and Chang Shu. 2019. Recent renminbi policy and currency co-movements. Journal of International Money and Finance 95: 444–56. [Google Scholar] [CrossRef]

- Pang, Ke, and Pierre L. Siklos. 2016. Macroeconomic Consequences of the Real-Financial Nexus: Imbalances and Spillovers between China and the U.S. Journal of International Money and Finance 65: 195–212. [Google Scholar] [CrossRef] [Green Version]

- Perry, Emily, and Florian Weltewitz. 2015. Wealth Management Products in China; Bulletin, June Quarter. Sydney: Reserve Bank of Australia, pp. 59–67. Available online: https://www.rba.gov.au/publications/bulletin/2015/jun/pdf/bu-0615-7.pdf (accessed on 1 October 2021).

- Plagborg-Møller, Mikkel, and Christian K. Wolf. 2021. Local Projections and VARs Estimate the Same Impulse Responses. Econometrica 89: 955–80. [Google Scholar] [CrossRef]

- Pritchett, Lant, and Larry H. Summers. 2014. Asiaphoria Meets Regression to the Mean. NBER Working Paper Series 20573; Cambridge: National Bureau of Economic Research, October, Available online: https://www.nber.org/papers/w20573 (accessed on 1 October 2021).

- Reinhart, Carmen, and Kenneth Rogoff. 2011. From Financial Crash to Debt Crisis. American Economic Review 101: 1676–706. [Google Scholar] [CrossRef] [Green Version]

- Song, Zheng, Kjetil Storesletten, and Fabrizio Zilibotti. 2011. Growing Like China. American Economic Review 101: 196–233. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| China | Hong Kong | China and Hong Kong | |

|---|---|---|---|

| In USD Billions ** | 139 | 89 | 228 |

| As Percent of Tier 1 Capital | 9.8 | 6.2 | 16.0 |

| USD Billions | Pct. of Tier 1 | |

|---|---|---|

| United Kingdom | 767 | 180.5 |

| Singapore ** | 237 | |

| United States | 228 | 16 |

| Japan | 171 | 24.6 |

| France | 93 | 20.4 |

| USD Billions | Pct. of Tier 1 | |

|---|---|---|

| United Kingdom | 37 | 2.6 |

| Singapore | 8 | 0.6 |

| Japan | 98 | 6.9 |

| France | 33 | 2.3 |

| Commodity Exporters | USD Billions |

|---|---|

| Mexico | 109 |

| Brazil | 86 |

| Saudi Arabia | 22 |

| Malaysia | 18 |

| Russia | 16 |

| Indonesia | 14 |

| Chile | 9 |

| Argentina | 7 |

| Colombia | 7 |

| Total | 287.0 |

| Panel A: By Issuer Type | |||||||||||

| Issuer | Total MMF Exposure (USD Billions) | By Instrument Type | By Maturity | Holding WAM (Days) | |||||||

| (USD Billions) | (USD Billions) | ||||||||||

| CP | CDs | Time Deposits | O/N | 2–7 Days | 8–30 Days | >30 Days | |||||

| China Total | 2.5 | 0.6 | 0.5 | 1.5 | 0.9 | 1.2 | 0.2 | 192.0 | -- | ||

| Banks Subtotal | 2.4 | 0.5 | 0.5 | 1.5 | 0.9 | 1.2 | 0.1 | 192.0 | -- | ||

| Industrial & Commercial Bank of China | 0.3 | 0.2 | 0.0 | 0.1 | 0.3 | 0.0 | 0.0 | 0 | 1 | ||

| China Construction Bank Corporation | 0.6 | 0.2 | 0.4 | 0.0 | 0.1 | 0.3 | 0.1 | 75 | 12 | ||

| Agricultural Bank of China | 1.5 | 0.1 | 0.1 | 1.4 | 0.5 | 0.9 | 0.0 | 117 | 8 | ||

| Bank of China | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0 | 15 | ||

| Other Financial Subtotal | 0.1 | 0.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.1 | 0.0 | -- | ||

| COFCO Capital Corporation | 0.1 | 0.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0 | 0 | 16.0 | ||

| Panel B: By U.S. Mutual Fund Complex | |||||||||||

| Complex | Total Exposure (USD Billions) | By Security Type | Pct. Of Complex AUM | Pct. Of Complex Prime AUM | Maximum Pct. Of Fund AUM | Exposure WAM (Days) | |||||

| (USD Billions) | |||||||||||

| CP | CDs | Time Deposits | |||||||||

| Goldman Sachs | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.4 | 0.4 | 6 | |||

| Invesco | 0.3 | 0.2 | 0.1 | 0.0 | 0.3 | 7.9 | 6.9 | 41 | |||

| JP Morgan | 2.0 | 0.3 | 0.3 | 1.5 | 0.4 | 2.4 | 1.7 | 3 | |||

| Legg Mason | 0.1 | 0.0 | 0.1 | 0.0 | 0.1 | 0.6 | 0.8 | 12 | |||

| Wells Fargo | 0.1 | 0.1 | 0.0 | 0.0 | 0.0 | 0.9 | 1.0 | 16 | |||

| Horizon | U.S. Long-Term Yield | Broad Nominal Dollar | VIX | EMBI Global | Oil Price | Metals Price | G7 GDP | World Trade ex. EME Asia | China GDP |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 79.9 | ||||||||

| 2 | 0.0 | 11.3 | 7.3 | 8.7 | 1.4 | 13.1 | 3.7 | 7.5 | 65.3 |

| 3 | 4.3 | 14.0 | 6.7 | 18.6 | 9.2 | 17.4 | 7.8 | 8.9 | 60.4 |

| 4 | 7.5 | 13.4 | 7.3 | 22.9 | 9.0 | 16.7 | 7.8 | 10.2 | 56.8 |

| 8 | 7.6 | 14.5 | 9.3 | 20.8 | 9.4 | 17.7 | 8.9 | 11.5 | 49.1 |

| 12 | 7.8 | 14.7 | 9.3 | 21.1 | 9.7 | 17.8 | 9.4 | 11.8 | 48.8 |

| ∞ | 7.8 | 14.7 | 9.4 | 21.0 | 9.7 | 17.8 | 9.5 | 11.9 | 48.3 |

| Horizon | China GDP | U.S. GDP | AFE GDP | EME ex. China GDP | EME Commodity Exporter GDP | EME Commodity Importer GDP |

|---|---|---|---|---|---|---|

| 1 | 79.9 | 0.7 | 0.0 | 0.9 | 0.1 | 5.9 |

| 2 | 65.3 | 0.7 | 6.4 | 10.1 | 13.5 | 6.5 |

| 3 | 60.4 | 1.9 | 9.6 | 15.9 | 21.3 | 6.9 |

| 4 | 56.8 | 1.9 | 9.6 | 15.8 | 21.4 | 6.8 |

| 8 | 49.1 | 2.0 | 9.7 | 16.4 | 21.7 | 6.9 |

| 12 | 48.8 | 2.0 | 9.7 | 16.4 | 21.7 | 6.9 |

| ∞ | 48.3 | 2.0 | 9.7 | 16.4 | 21.7 | 6.9 |

| Market Reaction * | Historical Percentiles | |||||

|---|---|---|---|---|---|---|

| Event #1 11 August 2015 | Event #2 ** 24 August 2015 | Event #3 ** 4–7 January 2016 | 1% Tail | 5% Tail | Most Extreme Value | |

| Broad Dollar | 0.70% | −0.10% | 1.30% | 0.65% | 0.40% | 1.62% |

| Broad AFE | 0.10% | −0.90% | 0.50% | 0.92% | 0.56% | 1.95% |

| Broad EME | 1.20% | 0.50% | 1.90% | 0.59% | 0.38% | 2.24% |

| U.S. 2Y yield | −4.8 | −5.7 | −8.8 | −5.7 | −2.8 | −15.4 |

| U.S. 10Y | −6.4 | −7.5 | −10.8 | −9.8 | −6.2 | −19.9 |

| German 10Y | −4.2 | −0.3 | −10.1 | −9.4 | −5.8 | −23.8 |

| U.K. 10Y | −5.7 | 8 | −16.5 | −11.1 | −7.1 | −29.7 |

| Japan 10Y | −1.4 | −1 | −2.4 | −4.8 | −2.8 | −12.7 |

| S&P 500 Futures | −0.6% | −3.8% | −4.5% | −1.8% | −1.0% | −3.8% |

| EuroSTOXX | −1.4% | −4.5% | −6.4% | −2.8% | −1.6% | −7.7% |

| FTSE 100 | −0.8% | −4.0% | −5.4% | −2.2% | −1.3% | −5.1% |

| MSCI EM | −0.4% | −4.3% | −5.8% | −2.9% | −1.5% | −7.3% |

| VIX | 1.01 | 4.7 | 3.7 | 2.60 | 1.25 | 6.55 |

| VDAX | 2.25 | 9.5 | 8.06 | 3.67 | 2.02 | 9.49 |

| US Corp Spread | 2.9 | 3.7 | 4.6 | 9.21 | 4.56 | 35.05 |

| EMBI+ Spread | 8 | 13 | 15 | 15 | 8 | 28 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ahmed, S.; Correa, R.; Dias, D.A.; Gornemann, N.; Hoek, J.; Jain, A.; Liu, E.; Wong, A. Global Spillovers of a Chinese Growth Slowdown. J. Risk Financial Manag. 2022, 15, 596. https://doi.org/10.3390/jrfm15120596

Ahmed S, Correa R, Dias DA, Gornemann N, Hoek J, Jain A, Liu E, Wong A. Global Spillovers of a Chinese Growth Slowdown. Journal of Risk and Financial Management. 2022; 15(12):596. https://doi.org/10.3390/jrfm15120596

Chicago/Turabian StyleAhmed, Shaghil, Ricardo Correa, Daniel A. Dias, Nils Gornemann, Jasper Hoek, Anil Jain, Edith Liu, and Anna Wong. 2022. "Global Spillovers of a Chinese Growth Slowdown" Journal of Risk and Financial Management 15, no. 12: 596. https://doi.org/10.3390/jrfm15120596

APA StyleAhmed, S., Correa, R., Dias, D. A., Gornemann, N., Hoek, J., Jain, A., Liu, E., & Wong, A. (2022). Global Spillovers of a Chinese Growth Slowdown. Journal of Risk and Financial Management, 15(12), 596. https://doi.org/10.3390/jrfm15120596