Do the Inward and Outward Foreign Direct Investments Spur Domestic Investment in Bangladesh? A Counterfactual Analysis

,

,

and

and

Abstract

:1. Introduction

2. Literature Review

3. Theoretical Framework

4. Methodology

4.1. Data Specifications

4.2. Econometric Estimation

4.2.1. Unit Root Tests

4.2.2. ARDL Bounds Testing Approach to Co-Integration

- (1)

- Lag level of the coefficients of all variables using F-test: H0: against H1: ;

- (2)

- Lag level of the coefficients of dependent variable using t-test: H0: , against H1:;

- (3)

- Lag level of the coefficients of independent variable using F-test: H0: , against H1: .

4.2.3. Dynamic ARDL Simulations Model

5. Results and Discussions

5.1. Data Stationarity

5.2. Model Estimation

5.3. ARDL Bounds Testing Approach to Co-Integration

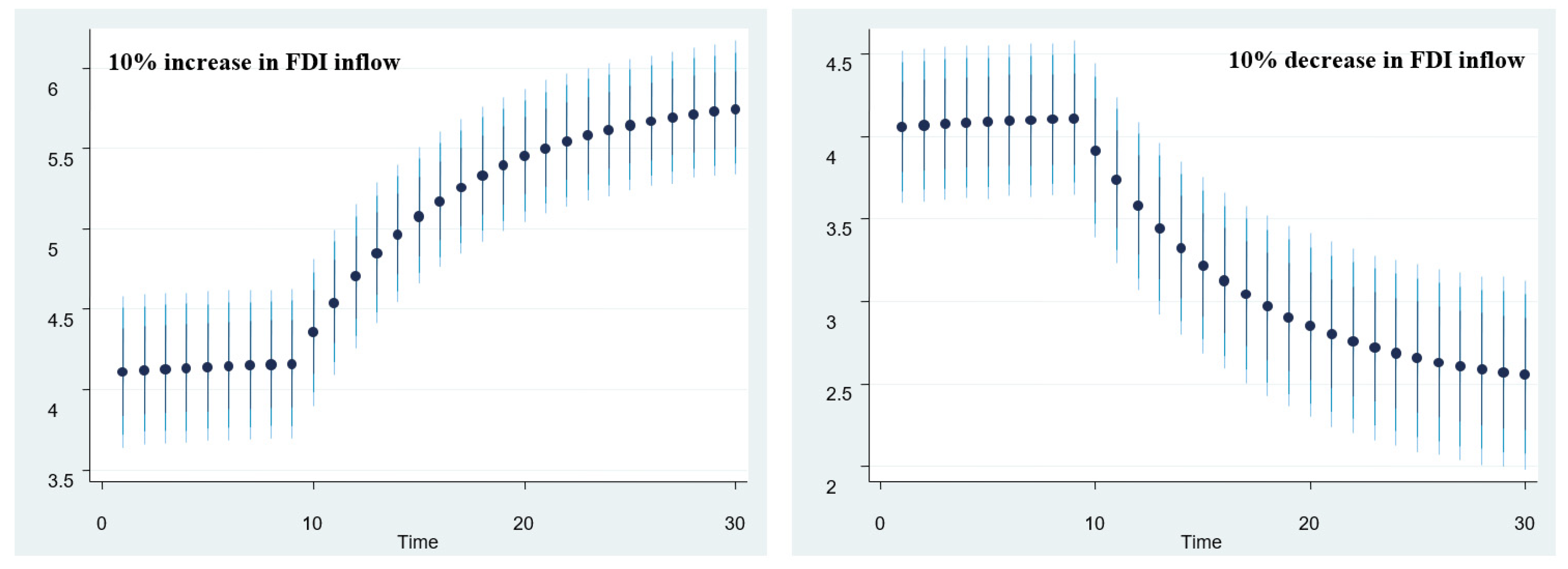

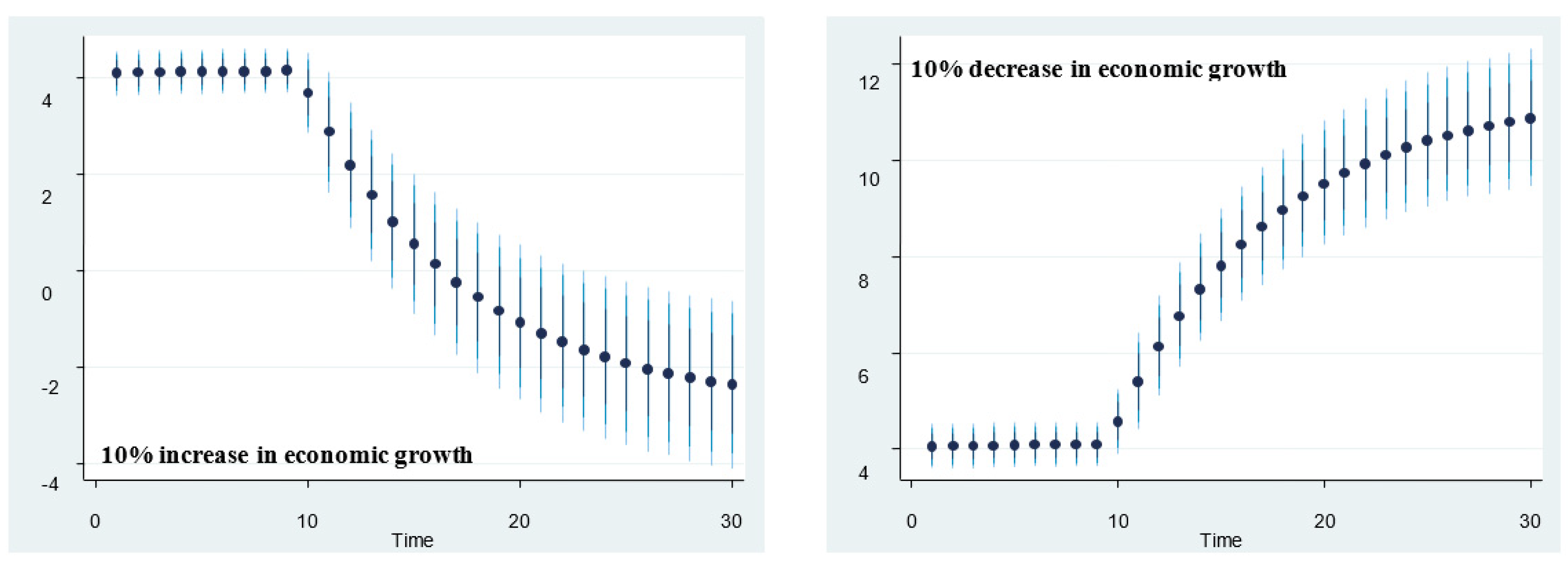

5.4. Dynamic ARDL Simulations-Based Counterfactual Shock Analysis

6. Conclusions and Policy Recommendations

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Domestic Investment (DI) | FDI Inflow (IDI) | FDI Outflow (ODI) | Per Capita GDP (GDP) | Real Interest Rates (RIR) | Violation of Political Rights (VPR) | |

|---|---|---|---|---|---|---|

| Mean | 24.56090 | 0.642864 | 0.055538 | 692.1635 | 6.740026 | 3.800000 |

| Median | 25.41113 | 0.581693 | 0.006128 | 602.9350 | 5.936576 | 4.000000 |

| Maximum | 31.57030 | 1.735419 | 0.364608 | 1287.821 | 14.82143 | 4.000000 |

| Minimum | 16.45868 | 0.004491 | 0.000391 | 411.1646 | −4.316833 | 3.000000 |

| Std. Dev. | 4.402946 | 0.529085 | 0.093574 | 254.8791 | 3.508104 | 0.406838 |

| Skewness | −0.354223 | 0.338965 | 1.854168 | 0.825373 | −0.381102 | −1.500000 |

| Kurtosis | 2.137786 | 1.940036 | 5.492636 | 2.556909 | 5.229498 | 3.250000 |

| Jarque–Bera | 1.556635 | 1.978890 | 24.95623 | 3.651615 | 6.939520 | 11.32812 |

| Probability | 0.459178 | 0.371783 | 0.000004 | 0.161088 | 0.031125 | 0.003468 |

| Sum | 736.8269 | 19.28593 | 1.666141 | 20764.91 | 202.2008 | 114.0000 |

| Sum Sq. Dev. | 562.1920 | 8.117991 | 0.253927 | 1883937. | 356.8970 | 4.800000 |

| Observations | 44 | 44 | 44 | 44 | 44 | 44 |

References

- Acemoglu, Daron. 2012. Introduction to Economic Growth. Journal of Economic Theory 147: 545–50. [Google Scholar] [CrossRef]

- Adams, Samuel. 2009. Foreign Direct Investment, Domestic Investment, and Economic Growth in Sub-Saharan Africa. Journal of Policy Modeling 31: 939–49. [Google Scholar] [CrossRef]

- Agosin, Manuel R., and Roberto Machado. 2005. Foreign Investment in Developing Countries: Does It Crowd in Domestic Investment? Oxford Development Studies 33: 149–62. [Google Scholar] [CrossRef] [Green Version]

- Ali, Walid, and Ali Mna. 2019. The Effect of FDI on Domestic Investment and Economic Growth Case of Three Maghreb Countries: Tunisia, Algeria and Morocco. International Journal of Law and Management 61: 91–105. [Google Scholar] [CrossRef]

- Ali, Usman, and Jian-Jun Wang. 2018. Does Outbound Foreign Direct Investment Crowd Out Domestic Investment in China? Evidence from Time Series Analysis. Global Economic Review 47: 419–33. [Google Scholar] [CrossRef]

- Ali, Usman, Wei Shan, Jian-Jun Wang, and Azka Amin. 2018. Outward Foreing Direct Investment and Economic Growth in China: Evidence from Asymetric ARDL Approach. Journal of Business Economics and Management 19: 706–21. [Google Scholar] [CrossRef] [Green Version]

- Ali, Usman, Jian-Jun Wang, Veronica Patricia Yanez Morales, and Meng-Meng Wang. 2019. Foreign Direct Investment Flows and Domestic Investment in China: A Multivariate Time Series Analysis. Investment Analysts Journal 48: 42–57. [Google Scholar] [CrossRef]

- Al-sadiq, Ali J. 2013. Outward Foreign Direct Investment and Domestic Investment: The Case of Developing Countries. IMF Working Papers 13/52. Washington, DC: International Monetary Fund. [Google Scholar] [CrossRef]

- Ameer, Waqar, Helian Xu, and Mohammed Saud M Alotaish. 2017. Outward Foreign Direct Investment and Domestic Investment: Evidence from China. Economic Research-Ekonomska Istraživanja 30: 777–88. [Google Scholar] [CrossRef] [Green Version]

- Ameer, Waqar, Helian Xu, Kazi Sohag, and Syed Hasanat Shah. 2021. Outflow FDI and Domestic Investment: Aggregated and Disaggregated Analysis. Sustainability 13: 7240. [Google Scholar] [CrossRef]

- Andersen, Palle Schelde (deceased), and Philippe Hainaut. 1998. Foreign Direct Investment and Employment in the Industrial Countries. BIS Working Paper No. 61. Basle: Bank for International Settlements. [Google Scholar] [CrossRef] [Green Version]

- Arndt, Christian, Claudia M. Buch, and Monika E. Schnitzer. 2010. FDI and Domestic Investment: An Industry-Level View. The BE Journal of Economic Analysis & Policy 10: 1–45. [Google Scholar] [CrossRef] [Green Version]

- Bashar, Omar K. M. R., and Habibullah Khan. 2007. Liberalization and Growth: An Econometric Study of Bangladesh. U21Global Working Paper Series, No. 001/2007; Kuala Lumpur: U21Global. [Google Scholar] [CrossRef]

- Business France. 2019. Business France Annual Report 2018. La French Tec. Available online: https://www.businessfrance.fr/discover-france-news-business-france-publishes-2018-annual-report# (accessed on 25 September 2020).

- Carvalho, Carlos, Andrea Ferrero, and Fernanda Nechio. 2016. Demographics and Real Interest Rates: Inspecting the Mechanism. European Economic Review 88: 208–26. [Google Scholar] [CrossRef] [Green Version]

- Chen, Kun-Ming, and Shu-Fei Yang. 2013. Impact of Outward Foreign Direct Investment on Domestic R&D Activity: Evidence from T Aiwan’s Multinational Enterprises in Low-wage Countries. Asian Economic Journal 27: 17–38. [Google Scholar]

- Chen, George S., Yao Yao, and Julien Malizard. 2017. Does Foreign Direct Investment Crowd in or Crowd out Private Domestic Investment in China? The Effect of Entry Mode. Economic Modelling 61: 409–19. [Google Scholar] [CrossRef]

- Desai, Mihir A, C. Fritz Foley, and James R. Hines. 2005. Foreign Direct Investment and the Domestic Capital Stock. American Economic Review 95: 33–38. [Google Scholar] [CrossRef] [Green Version]

- Dickey, David A., and Wayne A. Fuller. 1981. Likelihood Ratio Statistics for Autoregressive Time Series with a Unit Root. Econometrica 49: 1057–72. [Google Scholar] [CrossRef]

- Elheddad, Mohamed. 2019. Foreign Direct Investment and Domestic Investment: Do Oil Sectors Matter? Evidence from Oil-Exporting Gulf Cooperation Council Economies. Journal of Economics and Business 103: 1–12. [Google Scholar] [CrossRef]

- Farla, Kristine, Denis De Crombrugghe, and Bart Verspagen. 2016. Institutions, Foreign Direct Investment, and Domestic Investment: Crowding out or Crowding in? World Development 88: 1–9. [Google Scholar] [CrossRef] [Green Version]

- Feldstein, Martin S. 1995. The Effects of Outbound Foreign Direct Investment on the Domestic Capital Stock. In The Effects of Taxation on Multinational Corporations. Chicago: University of Chicago Press, pp. 43–66. [Google Scholar]

- Feldstein, Martin S., and Charles Horioka. 1980. Domestic Saving and International Capital Flows. The Economic Journal 90: 314. [Google Scholar] [CrossRef]

- Gibney, M., L. Cornett, R. Wood, and A. Daniel. 2019. Political Terror Scale 1976–2018. Asheville: University of North Carolina. Available online: http://www.politicalterrorscale.org/ (accessed on 10 March 2020).

- Goedegebuure, R. V. 2006. The Effects of Outward Foreign Direct Investment on Domestic Investment. Investment Management and Financial Innovations 3: 9–22. [Google Scholar]

- Goh, Soo Khoon, and Robert McNown. 2020. Macroeconomic Implications of Population Aging: Evidence from Japan. Journal of Asian Economics 68: 101198. [Google Scholar] [CrossRef]

- Gujarati, Damodar N., and Dawn C. Porter. 2010. Essentials Ofeconometrics, 4th ed. New York: McGraw-Hill Irwin. [Google Scholar]

- Hanousek, Jan, Anastasiya Shamshur, Jan Svejnar, and Jiri Tresl. 2021. Corruption Level and Uncertainty, FDI and Domestic Investment. Journal of International Business Studies 52: 1750–74. [Google Scholar] [CrossRef]

- He, Qing, Pak-Ho Leung, and Terence Tai-Leung Chong. 2013. Factor-augmented VAR analysis of the monetary policy in China. China Economic Review 25: 88–104. [Google Scholar] [CrossRef]

- Hejazi, Walid, and Peter Pauly. 2003. Motivations for FDI and Domestic Capital Formation. Journal of International Business Studies 34: 282–89. [Google Scholar] [CrossRef]

- Herzer, Dierk. 2010. Outward FDI and Economic Growth. Journal of Economic Studies 37: 476–94. [Google Scholar] [CrossRef]

- Herzer, Dierk, and Mechthild Schrooten. 2008. Outward FDI and Domestic Investment in Two Industrialized Countries. Economics Letters 99: 139–43. [Google Scholar] [CrossRef]

- Imbriani, Cesare, Rosanna Pittiglio, and Filippo Reganati. 2011. Outward Foreign Direct Investment and Domestic Performance: The Italian Manufacturing and Services Sectors. Atlantic Economic Journal 39: 369–81. [Google Scholar] [CrossRef]

- Islam, Md. Monirul, and Md. Saiful Islam. 2021a. Energy Consumption–Economic Growth Nexus within the Purview of Exogenous and Endogenous Dynamics: Evidence from Bangladesh. OPEC Energy Review. [Google Scholar] [CrossRef]

- Islam, Md. Monirul, and Md. Saiful Islam. 2021b. Globalization and Politico-administrative Factor-driven Energy-growth Nexus: A Case of South Asian Economies. Journal of Public Affairs, e2736. [Google Scholar] [CrossRef]

- Islam, Md. Monirul, Kazi Sohag, and Muhammad Shahbaz. 2022. Assessment of Nexus between Energy Consumption and Sustainable Development in Russian Federation: A Disaggregate Analysis. World Development Sustainability 1: 100027. [Google Scholar] [CrossRef]

- Ivanović, Igor. 2015. Impact of Foreign Direct Investment (FDI) on Domestic Investment in Republic of Croatia. Review of Innovation and Competitiveness: A Journal of Economic and Social Research 1: 137–60. [Google Scholar] [CrossRef] [Green Version]

- Jordan, Soren, and Andrew Q Philips. 2018. Cointegration Testing and Dynamic Simulations of Autoregressive Distributed Lag Models. The Stata Journal 18: 1–22. [Google Scholar] [CrossRef] [Green Version]

- Jude, Cristina. 2019. Does FDI Crowd out Domestic Investment in Transition Countries? Economics of Transition and Institutional Change 27: 163–200. [Google Scholar] [CrossRef]

- Li, Xiaoying, and Xiaming Liu. 2005. Foreign Direct Investment and Economic Growth: An Increasingly Endogenous Relationship. World Development 33: 393–407. [Google Scholar] [CrossRef]

- Li, Jian, Roger Strange, Lutao Ning, and Dylan Sutherland. 2016. Outward Foreign Direct Investment and Domestic Innovation Performance: Evidence from China. International Business Review 25: 1010–19. [Google Scholar] [CrossRef] [Green Version]

- Mahmood, Haider, and A. R. Chaudhary. 2012. Foreign Direct Investment-Domestic Investment Nexus in Pakistan. Middle-East Journal of Scientific Research 11: 1500–1507. [Google Scholar]

- Makki, Shiva S, and Agapi Somwaru. 2004. Impact of Foreign Direct Investment and Trade on Economic Growth: Evidence from Developing Countries. American Journal of Agricultural Economics 86: 795–801. [Google Scholar] [CrossRef]

- McNown, Robert, Chung Yan Sam, and Soo Khoon Goh. 2018. Bootstrapping the Autoregressive Distributed Lag Test for Cointegration. Applied Economics 50: 1509–21. [Google Scholar] [CrossRef]

- Mengistu, Alemu Aye, and Bishnu Kumar Adhikary. 2011. Does Good Governance Matter for FDI Inflows? Evidence from Asian Economies. Asia Pacific Business Review 17: 281–99. [Google Scholar] [CrossRef]

- Miao, Miao, Dinkneh Gebre Borojo, Jiang Yushi, and Tigist Abebe Desalegn. 2021. The Impacts of Chinese FDI on Domestic Investment and Economic Growth for Africa. Cogent Business & Management 8: 1886472. [Google Scholar]

- Min, Feng, Fenghua Wen, and Xiong Wang. 2022. Measuring the effects of monetary and fiscal policy shocks on domestic investment in China. International Review of Economics & Finance 77: 395–412. [Google Scholar]

- Ndikumana, Leonce, and Sher Verick. 2008. The Linkages between FDI and Domestic Investment: Unravelling the Developmental Impact of Foreign Investment in Sub-Saharan Africa. Development Policy Review 26: 713–26. [Google Scholar] [CrossRef] [Green Version]

- Ni, Bin, Mariana Spatareanu, Vlad Manole, Tsunehiro Otsuki, and Hiroyuki Yamada. 2017. The Origin of FDI and Domestic Firms’ Productivity—Evidence from Vietnam. Journal of Asian Economics 52: 56–76. [Google Scholar] [CrossRef]

- Onaran, Özlem, Engelbert Stockhammer, and Klara Zwickl. 2013. FDI and Domestic Investment in Germany: Crowding in or Out?”. International Review of Applied Economics 27: 429–48. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem. 2015. Time Series and Panel Data Econometrics. Oxford: Oxford University Press. [Google Scholar]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds Testing Approaches to the Analysis of Level Relationships. Journal of Applied Econometrics 16: 289–326. [Google Scholar] [CrossRef]

- Prasanna, N. 2010. Direct and Indirect Impact of Foreign Direct Investment (FDI) on Domestic Investment (DI) in India. Journal of Economics 1: 77–83. [Google Scholar] [CrossRef]

- Rodrik, Dani. 2006. Goodbye Washington Consensus, Hello Washington Confusion? A Review of the World Bank’s Economic Growth in the 1990s: Learning from a Decade of Reform. Journal of Economic Literature 44: 973–87. [Google Scholar] [CrossRef] [Green Version]

- Rubio-Ramirez, Juan F., Daniel F. Waggoner, and Tao Zha. 2010. Structural vector autoregressions: Theory of identification and algorithms for inference. The Review of Economic Studies 77: 665–96. [Google Scholar] [CrossRef] [Green Version]

- Salim, Ruhul, Yao Yao, George Chen, and Lin Zhang. 2017. Can Foreign Direct Investment Harness Energy Consumption in China? A Time Series Investigation. Energy Economics 66: 43–53. [Google Scholar] [CrossRef]

- Sam, Chung Yan, Robert McNown, and Soo Khoon Goh. 2019. An Augmented Autoregressive Distributed Lag Bounds Test for Cointegration. Economic Modelling 80: 130–41. [Google Scholar] [CrossRef]

- Serrasqueiro, Zélia. 2017. Investment Determinants: High-Investment versus Low-Investment Portuguese SMEs. Investment Analysts Journal 46: 1–16. [Google Scholar] [CrossRef]

- Shah, Syed Hasanat, Hafsa Hasnat, Simon Cottrell, and Mohsin Hasnain Ahmad. 2020. Sectoral FDI Inflows and Domestic Investments in Pakistan. Journal of Policy Modeling 42: 96–111. [Google Scholar] [CrossRef]

- Su, Kun, Rui Wan, and Taiwen Feng. 2015. Government Control Structure and Allocation of Credit: Evidence from Government-Owned Companies in China. Investment Analysts Journal 44: 151–70. [Google Scholar] [CrossRef]

- Sylwester, Kevin. 2005. Foreign Direct Investment, Growth and Income Inequality in Less Developed Countries. International Review of Applied Economics 19: 289–300. [Google Scholar] [CrossRef]

- Szkorupová, Zuzana. 2015. Relationship between Foreign Direct Investment and Domestic Investment in Selected Countries of Central and Eastern Europe. Procedia Economics and Finance 23: 1017–22. [Google Scholar] [CrossRef]

- Tan, Bee Wah, Soo Khoon Goh, and Koi Nyen Wong. 2016. The Effects of Inward and Outward FDI on Domestic Investment: Evidence Using Panel Data of ASEAN–8 Countries. Journal of Business Economics and Management 17: 717–33. [Google Scholar] [CrossRef] [Green Version]

- Türkcan, Burcu. 2008. How Does FDI and Economic Growth Affect Each Other? The OECD Case. In Proceedings of the International Conference on Emerging Economic Issues in a Globalizing World. İzmir: Izmir University of Economics, pp. 21–40. [Google Scholar]

- Ullah, Irfan, Mahmood Shah, and Farid Ullah Khan. 2014. Domestic Investment, Foreign Direct Investment, and Economic Growth Nexus: A Case of Pakistan. Economics Research International 2014: 592719. [Google Scholar] [CrossRef] [Green Version]

- UNCTAD (United Nations Conference on Trade and Development). 2018. Available online: https://unctad.org/en/PublicationsLibrary/wir2018_en.pdf (accessed on 10 October 2020).

- UNCTAD (United Nations Conference on Trade and Development). 2019. World Investment Report 2019. Available online: https://unctad.org/en/PublicationsLibrary/wir2019_en.pdf (accessed on 12 December 2020).

- Wang, Miao. 2010. Foreign Direct Investment and Domestic Investment in the Host Country: Evidence from Panel Study. Applied Economics 42: 3711–21. [Google Scholar] [CrossRef] [Green Version]

- World Bank. 2020. Doing Business 2020: Comparing Business Regulation in 190 Economies. Washington, DC: World Bank. [Google Scholar] [CrossRef] [Green Version]

- World Bank. 2022. World Development Indicators. Available online: https://data.worldbank.org/products/wdi (accessed on 10 January 2022).

- Xu, Yang, and Xiaoling Yuan. 2012. Research on China’s Regional Differences of Crowding-In or Crowding-Out Effect of FDI on Domestic Investment. Modern Economy 3: 884–90. [Google Scholar] [CrossRef] [Green Version]

- You, Kefei, and Offiong Helen Solomon. 2015. China’s Outward Foreign Direct Investment and Domestic Investment: An Industrial Level Analysis. China Economic Review 34: 249–60. [Google Scholar] [CrossRef]

- Zivot, Eric, and Donald Andrews. 2002. Further Evidence on the Great Crash, the Oil-Price Shock, and the Unit-Root Hypothesis. Journal of Business & Economic Statistics 20: 25–44. [Google Scholar]

| Authors | Titles | Methods and Country | Findings |

|---|---|---|---|

| Agosin and Machado (2005) | Foreign Investment in Developing Countries: Does it Crowd in Domestic Investment? | GMM and Latin America, Asia, and Africa | Crowding-out effect for Latin America and crowding-in effect for Asia and Africa. |

| Ndikumana and Verick (2008) | The Linkages Between FDI and Domestic Investment: Unravelling the Developmental Impact of Foreign Investment in Sub-Saharan Africa | Fixed effects model and Sub-Saharan Africa | Crowding-in effect |

| Arndt et al. (2010) | FDI and Domestic Investment: An Industry-Level View | OLS, DOLS, and FMOLS and Germany | FDIDI |

| Prasanna (2010) | Direct and Indirect Impact of Foreign Direct Investment (FDI) on Domestic Investment (DI) in India | Multiple linear regression (MLR) and India | FDIDI |

| Herzer and Schrooten (2008) | Outward FDI and domestic investment in two industrialized countries | Autoregressive distributed lag (ARDL) and the USA and Germany | ODIDI in the USA and complementary and substitution effects in the long run and short run, respectively, in Germany. |

| Onaran et al. (2013) | FDI and domestic investment in Germany: crowding in or out? | Generalized method of moments (GMM) and developing and developed countries | Crowding-out in low-wage countries; crowding-in high-wage countries. |

| Tan et al. (2016) | The Effects of Inward and Outward FDI on Domestic Investment: Evidence using Panel Data of ASEAN-8 Countries | Mean group (MG) and pooled mean group (PMG) and ASEAN-8 economies | IDIDI |

| Farla et al. (2016) | Institutions, Foreign Direct Investment, and Domestic Investment: Crowding Out or Crowding In? | Alternative GMM estimation and 46 FDI-receiving countries | Crowding-out effect |

| Ali and Mna (2019) | The effect of FDI on domestic investment and economic growth case of three Maghreb countries: Tunisia, Algeria, and Morocco | GMM and Tunisia, Algeria, and Morocco | FDIDI |

| Shah et al. (2020) | Sectoral FDI inflows and domestic investments in Pakistan | Autoregressive distributed lag (ARDL) and Pakistan | Crowding-in effect |

| Jude (2019) | Does FDI crowd out domestic investment in transition countries? | GMM estimation and 10 Central and Eastern European countries | Crowding-in effect in the long run |

| Ameer et al. (2021) | Outflow FDI and Domestic Investment: Aggregated and Disaggregated Analysis | Cross-sectional autoregressive distributed lag (CS-ARDL) and GCC countries | Crowding-out effect |

| Hanousek et al. (2021) | Corruption level and uncertainty, FDI, and domestic investment | Matched sample regression (MSR) and 13 European countries | No effect of FDI on DI |

| Miao et al. (2021) | The impacts of Chinese FDI on domestic investment and economic growth for Africa | The two-step system GMM estimation and 44 African countries | Positive effect of FDI on DI |

| Variable Type | Name | Label | Description | Source |

|---|---|---|---|---|

| Dependent variable | Domestic investment | LnDI | Gross capital formation to GDP ratio | (World Bank 2020) |

| Independent Variables | Inward FDI | LnIDI | Net inward FDI to GDP ratio | (World Bank 2020) |

| Outward FDI | LnODI | Net outward FDI to GDP ratio | (World Bank 2020) | |

| Economic growth | LnGDP | Per capita GDP growth | (World Bank 2020) | |

| Real interest rate | RIR | Real interest rate in % | (World Bank 2020) | |

| Violation of political rights | LnVPR | Political terror scale (PTS) | (Gibney et al. 2019) |

| Series | Level | First Difference | ||||

|---|---|---|---|---|---|---|

| ADF | ZA | Break | ADF | ZA | Break | |

| LnDI | −2.386 | −4.664 *** | 1996 | −5.349 * | −3.741 | 1985 |

| LnIDI | −1.534 | −4.558 | 1997 | −8.176 * | −9.130 * | 1990 |

| LnODI | −2.393 | −4.202 | 2007 | −7.558 * | −6.183 * | 2013 |

| LnGDP | −5.745 * | −6.236 * | 2005 | −13.741 * | −11.407 * | 1990 |

| RIR | −3.963 * | −8.017 * | 1985 | −7.718 * | −4.715 *** | 1984 |

| LnVPR | −3.136 ** | −6.134 * | 1987 | −8.572 * | −7.573 * | 1986 |

| Lag | LogL | LR | FPE | AIC | SC | HQ |

|---|---|---|---|---|---|---|

| 0 | −180.4659 | NA | 0.000289 | 8.879329 | 9.127567 | 8.970318 |

| 1 | −39.56758 | 234.8305 | 2.00 × 10−6 | 3.884171 | 5.621840 * | 4.521095 * |

| 2 | 3.058836 | 58.86505 * | 1.62 × 10−6 * | 3.568627 * | 6.795728 | 4.751487 |

| Variables | Coefficients | t-Statistic | Prob. |

|---|---|---|---|

| Long run | |||

| Constant | 0.5003 * (0.1407) | 3.55 | 0.001 |

| 0.0196 ** (0.0078 | 2.52 | 0.017 | |

| 0.0045 (0.0055) | 0.82 | 0.420 | |

| 0.0472 ** (0.0297) | 1.59 | 0.022 | |

| 0.0102 (0.0142) | 0.72 | 0.478 | |

| 0.0407 (0.0482) | 0.84 | 0.405 | |

| Short run | |||

| 0.0203 * (0.0059) | 3.41 | 0.002 | |

| −0.0035 (0.0057) | −0.61 | 0.544 | |

| 0.0869 *** (0.0497) | 1.75 | 0.091 | |

| 0.0102 (0.0142) | 0.72 | 0.478 | |

| 0.0668 (0.0564) | 1.18 | 0.246 | |

| DUM_90 | −0.0478 (0.0503) | −0.94 | 0.351 |

| DUM_13 | −0.0217 (0.0419) | −0.51 | 0.608 |

| DUM_84 | −0.1724 ** (0.0657) | −2.62 | 0.014 |

| DUM_86 | −0.0886 (0.0646) | −1.37 | 0.182 |

| ECT (−1) | −0.2213 ** (0.0538) | −2.26 | 0.031 |

| Diagnostic checks for model fitting | |||

| F-test | 4.56 * | ||

| t-test (lagged DV) | 6.80 * | ||

| F-test (lagged IDV) | 4.50 * | ||

| N | 43 | ||

| R2 | 0.983 | ||

| J–B Normality | 1.016 (0.601) | ||

| χ2 LM | 3.405 (0.182) | ||

| χ2 ARCH | 0.792 (0.373) | ||

| χ2 RESET | 1.156 (0.255) | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Islam, M.M.; Tareque, M.; Wahid, A.N.M.; Alam, M.M.; Sohag, K. Do the Inward and Outward Foreign Direct Investments Spur Domestic Investment in Bangladesh? A Counterfactual Analysis. J. Risk Financial Manag. 2022, 15, 603. https://doi.org/10.3390/jrfm15120603

Islam MM, Tareque M, Wahid ANM, Alam MM, Sohag K. Do the Inward and Outward Foreign Direct Investments Spur Domestic Investment in Bangladesh? A Counterfactual Analysis. Journal of Risk and Financial Management. 2022; 15(12):603. https://doi.org/10.3390/jrfm15120603

Chicago/Turabian StyleIslam, Md. Monirul, Mohammad Tareque, Abu N. M. Wahid, Md. Mahmudul Alam, and Kazi Sohag. 2022. "Do the Inward and Outward Foreign Direct Investments Spur Domestic Investment in Bangladesh? A Counterfactual Analysis" Journal of Risk and Financial Management 15, no. 12: 603. https://doi.org/10.3390/jrfm15120603

APA StyleIslam, M. M., Tareque, M., Wahid, A. N. M., Alam, M. M., & Sohag, K. (2022). Do the Inward and Outward Foreign Direct Investments Spur Domestic Investment in Bangladesh? A Counterfactual Analysis. Journal of Risk and Financial Management, 15(12), 603. https://doi.org/10.3390/jrfm15120603