Measures of Volatility, Crises, Sentiment and the Role of U.S. ‘Fear’ Index (VIX) on Herding in BRICS (2007–2021)

Abstract

:1. Introduction

1.1. Motivation

1.2. Contribution

2. Literature Review

2.1. Models

2.1.1. Theoretical Models

2.1.2. Statistical/Empirical Models

2.2. Volatility and Herding

2.3. Principal Component, Sentiment and Herding

2.4. The Role of the US

2.5. BRICS Research

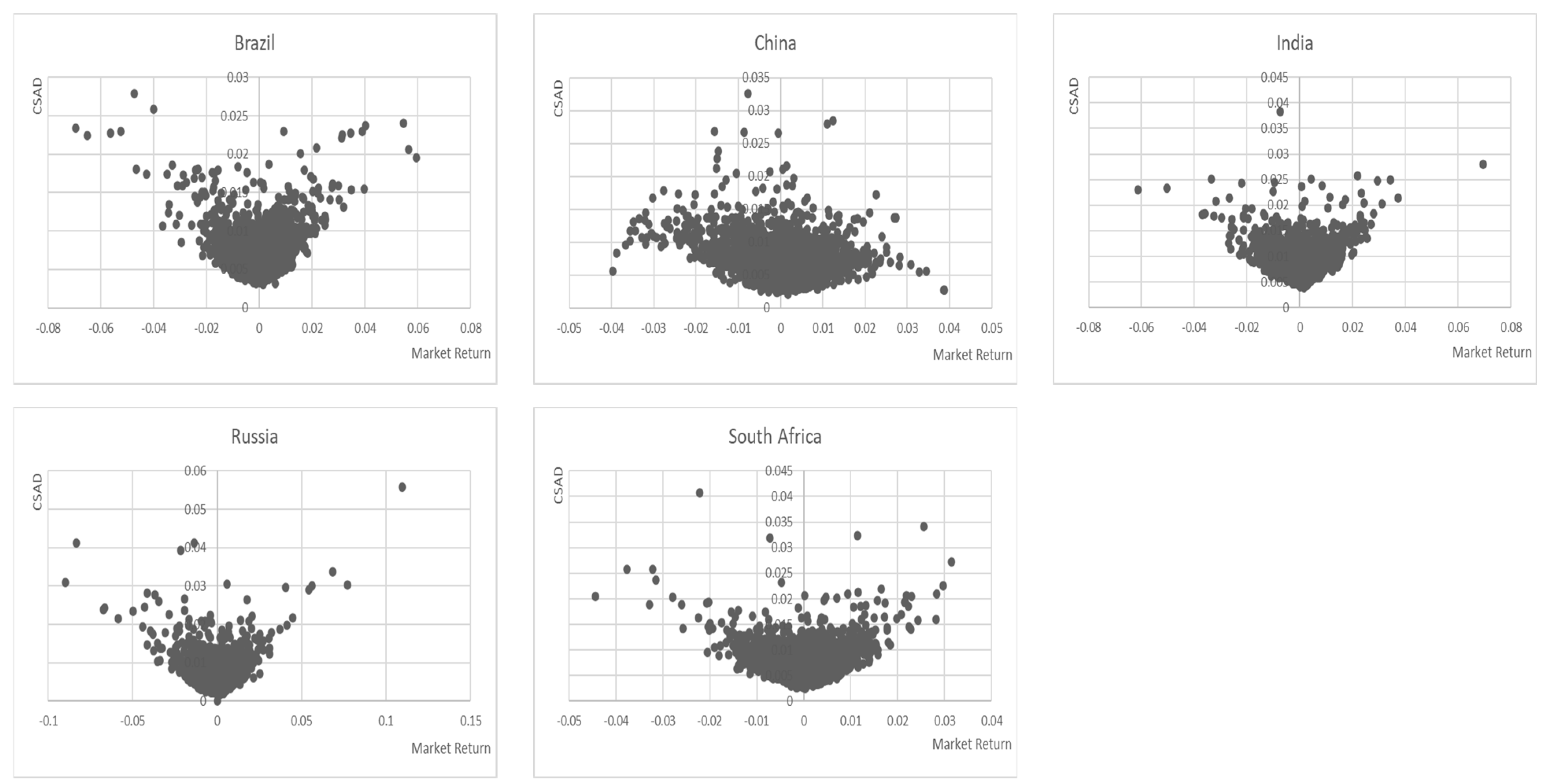

3. Methodology and Data

3.1. Data and Sample(s)

3.2. Basic Model

3.3. Volatility Models

3.3.1. Forecasting Volatility

Conditional Volatility (GARCH)

Exponentially Weighted Moving Average Volatility (EWMA)

3.3.2. Intraday Extreme Points Volatility

3.3.3. Equally Weighted Moving Average and Capitalisation (or Value) Weighted Moving Average

3.3.4. Herding and Volatility Models

3.4. Sentiment and Herding

3.5. The Role of the US

3.5.1. Basic Model

3.5.2. Granger Causality Test

4. Discussion and Findings

4.1. Time-Frequency Effect and Event Effect for Herding

4.2. Volatility and Herding

4.2.1. The Effect of Herding on Volatility

4.2.2. The Effect of Volatility on Herding

4.3. Sentiment Index and Herding

Granger Causality: CSAD and SIX (Sentiment Based on Principal Component)

4.4. The Effect of the US Stock Market on BRICS

4.5. The Effect of US Sentiment/Fear (VIX) on BRICS

4.6. Granger Causality: CSAD and VIX

5. Conclusions

6. Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ababio, Kofi Agyarko, and John Muteba Mwamba. 2017. Test of Herding Behaviour in the Johannesburg Stock Exchange: Application of Quantile Regression Model. Journal of Economic and Financial Sciences 10: 457–74. [Google Scholar]

- Adu, George, Paul Alagidede, and Amin Karimu. 2015. Stock Return Distribution in the BRICS. Review of Development Finance 5: 98–109. [Google Scholar] [CrossRef] [Green Version]

- Aït-Sahalia, Yacine, Jochen Andritzky, Andreas Jobst, Sylwia Nowak, and Natalia Tamirisa. 2012. Market response to policy initiatives during the global financial crisis. Journal of International Economic 87: 162–77. [Google Scholar] [CrossRef]

- Alemanni, Barbara, and José Renato Haas Ornelas. 2006. Herding Behavior by Equity Foreign Investors on Emerging Markets. Brasília: Banco Central do Brasil. [Google Scholar]

- Alexander, Carol. 1998. Volatility and Correlation: Measurement, Models and Applications. In Risk Management and Analysis, Measuring and Modeling Financial Risk: Risk Measurment and Management. Edited by Alexander Carol. Hoboken: John Wiley & Sons. [Google Scholar]

- Alexander, Carol. 2008. Moving Average Models for Volatility and Correlation, and Covariance Matrices. In Handbook of Finance. Edited by Fabozzi Frank J. New York: John Wiley & Sons, vol. 3, pp. 1–14. [Google Scholar]

- Alexander, Carol, and Anca Dimitriu. 2003. Source of Over-Performance in Equity Markets: Mean Reversion, Common Trends and Herding. Reading: The University of Reading. New York: Wiley. [Google Scholar]

- Alhashim, Mohammed. 2018. The Impact of Investor Sentiment on Herding Behavior: Evidence from a Social Network of Investors. Arlington: Department of Finance and Real Estate, University of Texas at Arlington. [Google Scholar]

- Amata, Evans Ombima, Willy Muturi, and Martin Mbewa. 2016. Relationship between Macro-economic variables, Investor Herding Behaviour and Stock Market Volatility in Kenya. International Journal of Economics, Commerce and Management 4: 36–54. [Google Scholar]

- Arkes, Hal R., Lisa Tandy Herren, and Alice M. Isen. 1988. The Role of Potential Loss in the Influence of Asset on Risk-Taking Behavior. Organizational Behavior and Human Processes 42: 181–93. [Google Scholar] [CrossRef]

- Arlen, Jennifer, and Stephan Tontrup. 2016. Strategic Bias Shifting: Herding as a Behaviorally Rational Response to Regret Aversion. Journal of Legal Analysis 7: 517–60. [Google Scholar] [CrossRef] [Green Version]

- Baele, Lieven, Geert Bekaert, Koen Inghelbrecht, and Min Wei. 2020. Flights to Safety. The Review of Financial Studies 33: 689–746. [Google Scholar] [CrossRef]

- Baker, Malcolm, and Jeremy C. Stein. 2004. Market Liquidity as a Sentiment Indicator. Journal of Financial Markets 7: 271–99. [Google Scholar] [CrossRef] [Green Version]

- Baker, Malcolm, and Jeffrey Wurgler. 2006. Investor Sentiment and the Cross-Section of Stock Returns. The Journal of Finance 61: 1645–80. [Google Scholar] [CrossRef] [Green Version]

- Baker, Malcolm, and Jeffrey Wurgler. 2007. Investor Sentiment in the Stock Market. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Baker, Malcolm, Jeffrey Wurgler, and Yu Yuan. 2012. Global, local, and Contagious Investor Sentiment. Journal of Financial Economics 104: 272–87. [Google Scholar] [CrossRef] [Green Version]

- Balcilar, Mehmet, Riza Demirer, and Shawkat Hammoudeh. 2013. Investor Herds and Regime-switching: Evidence from Gulf Arab Stock Markets. Journal of International Financial Markets, Institutional and Money 23: 295–321. [Google Scholar] [CrossRef]

- Banerjee, Ameet Kumar, and Purna Chandra Padhan. 2017. Herding Behavior in Futures Market: An Empirical Analysis from India. Theoretical Economics Letters 7: 1015–28. [Google Scholar] [CrossRef] [Green Version]

- Banerjee, Abhijit V. 1992. A Simple Model of Herd Behavior. The Quarterly Journal of Economics 107: 797–817. [Google Scholar] [CrossRef] [Green Version]

- Barberis, Nicholas, Andrei Shleifer, and Robert Vishny. 1998. A Model of Investor Sentiment. Journal of Financial Economics 49: 307–43. [Google Scholar] [CrossRef]

- Bathia, Deven, Don Bredin, and Dirk Nitzsche. 2016. International Sentiment Spillovers in Equity Returns. International Journal of Finance and Economics 21: 332–59. [Google Scholar] [CrossRef]

- Becketti, Sean, and Gordon H. Sellon. 1989. Has Financial Market Volatility Increased? Economic Review 74: 17–30. [Google Scholar]

- Bekaert, Geert, Campbell R. Harvey, and Christian T. Lundblad. 2003. Equity Market Liberalization in Emerging Markets. The Journal of Financial Research 26: 275–99. [Google Scholar] [CrossRef]

- Berument, Hakan, and Halil Kiymaz. 2001. The Day of the Week Effect on Stock Market Volatility. Journal of Economics 25: 181–93. [Google Scholar]

- Bikhchandani, Sushil, and Sunil Sharma. 2001. Herd Behavior in Financial Markets. IMF Staff Papers 47: 279–310. [Google Scholar]

- Bikhchandani, Sushil, David Hirshleifer, and Ivo Welch. 1992. A Theory of Fads, Fashion, Custom, and Cultural Change as Informational Cascades. Journal of Political Economy 100: 992–1026. [Google Scholar] [CrossRef]

- Black, Fischer. 1976. Studies of Stock Price Volatility Changes. In Proceedings of the 1976 Meeting of the Business and Economic Statistics Section, American Statistical Association. Washington, DC: American Statistical Association, pp. 177–81. [Google Scholar]

- Blasco, Natividad, Pilar Corredor, and Sandra Ferreruela. 2012. Does Herding Affect Volatility? Implications for the Spanish Stock Market 12: 311–27. [Google Scholar]

- Bodman, Samuel W., James D. Wolfensohn, and Julia E. Sweig. 2011. Independent Task Force Report No. 66—Global Brazil and U.S.-Brazil Relations. New York: Council on Foreign Relations Press. [Google Scholar]

- Borensztein, Eduardo, and R. Gaston Gelos. 2003. A Panic-Prone Pack? The Behavior of Emerging Market Mutual Funds. IMF Staff Papers 50: 43–63. [Google Scholar]

- Bouteska, Ahmed. 2020. Some Evidence from a Principal Component Approach to Measure a New Investor Sentiment Index in the Tunisian Stock Market. Managerial Finance 46: 401–20. [Google Scholar] [CrossRef]

- Brown, Gregory W., and Michael T. Cliff. 2004. Investor Sentiment and the Near-term Stock Market. Journal of Empirical Finance 11: 1–27. [Google Scholar] [CrossRef]

- Calomiris, Charles W., Inessa Love, and María Soledad Martínez Pería. 2012. Stock Returns’ Sensitivities to Crisis Shocks: Evidence from Developed and Emerging Markets. Journal of International Money and Finance 31: 743–65. [Google Scholar] [CrossRef]

- Campbell, John Y., and Ludger Hentschel. 1992. No News is Good News: An Asymmetric Model of Changing Volatility in Stock Returns. Journal of Financial Economics 31: 281–318. [Google Scholar] [CrossRef] [Green Version]

- Caporale, Guglielmo Maria, Fotini Economou, and Nikolaos Philippas. 2008. Herding behaviour in extreme market conditions: The case of the Athens Stock Exchange. Economics Bulletin 7: 1–13. [Google Scholar]

- Chang, Eric C., Joseph W. Cheng, and Ajay Khorana. 2000. An Examination of Herd Behavior in Equity Markets: An International Perspective. Journal of Banking & Finance 24: 1651–79. [Google Scholar]

- Chauhan, Yash, Nehal Ahmad, Vaishali Aggarwal, and Abhijeet Chandra. 2020. Herd Behaviour and Asset Pricing in the Indian Stock Market. IIMB Management Review 32: 143–52. [Google Scholar] [CrossRef]

- Chen, Haiqiang, Terence Tai Leung Chong, and Yingni She. 2014. A Principal Component Approach to Measuring Investor Sentiment in China. Quantitative Finance 14: 573–79. [Google Scholar] [CrossRef]

- Chiang, Thomas C., and Dazhi Zheng. 2010. An Empirical Analysis of Herd Behavior in Global Stock Markets. Journal of Banking & Finance 34: 1911–21. [Google Scholar]

- Chiang, Thomas C., Jiandong Li, Lin Tan, and Edward Nelling. 2013. Dynamic Herding Behavior in Pacific-Basin Markets: Evidence and Implications. Multinational Finance Journal 17: 165–200. [Google Scholar] [CrossRef]

- Chong, Terence Tai-Leung, Bingqing Cao, and Wing Keung Wong. 2014. A New Principal-Component Approach to Measur the Investor Sentiment. Hong Kong: The Chinese University of Hong Kong. [Google Scholar]

- Choudhary, Kapil, Parminder Singh, and Amit Soni. 2019. Relationship between FIIss’ Herding and Returns in the Indian Equity Market: Further Empirical Evidence. Global Business Review 2019: 1–19. [Google Scholar]

- Chow, Gregory C. 1960. Tests of Equality Between Sets of Coefficients in Two Linear Regressions. Econometrica 28: 591–605. [Google Scholar] [CrossRef]

- Christie, William G., and Roger D. Huang. 1995. Following the Pied Piper: Do Individual Returns Herd around the Market? Financial Analysts Journal 51: 31–37. [Google Scholar] [CrossRef]

- Dasgupta, Amil, Andrea Part, and Michela Verardo. 2011. Institutional Trade Persistence and Long-Term Equity Returns. The Journal of Finance 66: 635–53. [Google Scholar] [CrossRef]

- De Long, J. Bradford, Andrei Shleifer, Lawrence H. Summers, and Robert J. Waldmann. 1990. Noise Trade Risk in Financial Markets. Journal of Political Economy 98: 703–38. [Google Scholar] [CrossRef]

- Demirer, Riza, and Ali M. Kutan. 2006. Does Herding Behavior Exist in Chinese Stock Markets? Journal of International Financial Markets, Institutional and Money 16: 123–42. [Google Scholar] [CrossRef]

- Dos Santos, Luís G. G., and Sérgio Lagoa. 2017. Herding Behaviour in a Peripheral European Stock Market: The Impact of the Subprime and the European Sovereign Debt Crisis. International Journal of Banking, Accounting and Finance 8: 174–203. [Google Scholar] [CrossRef] [Green Version]

- Economou, Fotini, Christis Hassapis, and Nikolaos Philippas. 2018. Investors’ Fear and Herding in the Stock Market. Applied Economics 50: 1–10. [Google Scholar] [CrossRef]

- Eichengreen, Barry, and Ashoka Mody. 1998. Interest Rates in the North and Capital Flows to the South: Is There a Missing Link? International Finance 1: 35–57. [Google Scholar] [CrossRef] [Green Version]

- EMIS. 2019. BRICS in 2019: Going Digital. London: EMISS ISI Emerging Markets Group. [Google Scholar]

- Feliba, David, and Cheska Lozano. 2021. Foreign Investment Flows Return to Brazil in Q2, but Political Risks Loom. Available online: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/foreign-investment-flows-return-to-brazil-in-q2-but-political-risks-loom-65456134 (accessed on 20 January 2022).

- Friedman, Milton. 1953. Essays in Positive Economics. Chicago: University of Chicago Press. [Google Scholar]

- Galariotis, Emilios C., Wu Rong, and Spyros I. Spyrou. 2015. Herding on Fundamental Information: A Comparative Study. Journal of Banking & Finance 50: 589–98. [Google Scholar]

- Ganesh, R., G. Naresh, and S. Thiyagarajan. 2016. Industry Herding Behaviour in Indian Stock Market. American Journal of Finance and Accounting 4: 284–308. [Google Scholar] [CrossRef]

- Garman, Mark B., and Michael J. Klass. 1980. On the Estimation of Security Price Volatilities from Historical Data. The Journal of Bussiness 53: 67–78. [Google Scholar] [CrossRef]

- Gavriilidis, Konstantinos, Vasileios Kallinterakis, and Ioannis Tsalavoutas. 2016. Investor Mood, herding and the Ramadan Effect. Journal of Economic Behavior & Organization 132: 23–38. [Google Scholar]

- Gazel, Sümeyra. 2015. The Regret Aversion as an Investor Bias. International Journal of Business and Management Studies 4: 419–24. [Google Scholar]

- Gill, Chris. 2020. China Offers A Share to More Foreign Investors. Available online: https://www.asiafinancial.com/china-offers-a-shares-to-more-foreign-investors (accessed on 26 October 2020).

- Gong, Pu, and Jun Dai. 2017. Monetary Policy, Exchange Rate Fluctuation, and Herding Behavior in the Stock Market. Journal of business Research 76: 34–43. [Google Scholar] [CrossRef]

- Granger, C. W. J. 1969. Investigating Causal Relations by Econometric Models and Cross-spectral Methods. Econometrica 37: 424–38. [Google Scholar] [CrossRef]

- Guney, Yilmaz, Vasileios Kallinterakis, and Gabriel Komba. 2017. Herding in Frontier Markets: Evidence from African Stock Exchanges. Journal of International Financial Markets, Institutions and Money 47: 152–75. [Google Scholar] [CrossRef]

- Hair, Joseph F., Bill Black, Barry Babin, Rolph E. Anderson, and Ronald L. Tatham. 2006. Multivariate Data Analysis, 6th ed. London: Pearson. [Google Scholar]

- Hattori, Masazumi, Ilhyock Shim, and Yoshihiko Sugihara. 2018. Cross-Stock Market Spillovers through Variance Risk Premiums and Equity Flows. Basel: The Monetary and Economic Department of the Bank for International Settlements. [Google Scholar]

- He, Gang, Shuzhen Zhu, and Haifeng Gu. 2017. On the Construction of Chinese Stock Market Investor Sentiment Index. Cogent Economics & Finance 5: 1–10. [Google Scholar]

- Hong, Harrison, and Jeremy C. Stein. 1999. A Unified Theory of Underreaction, Momentum Trading, and Overreaction in Asset Markets. The Journal of Finance 54: 2143–84. [Google Scholar] [CrossRef] [Green Version]

- Hsieh, Meng-Fen, Tzu-Yi Yang, Yu-Tai Yang, and Jen-Sin Lee. 2011. Evidence of herding and positive feedback trading for mutual funds in emerging Asian countries. Quantitative Finance 11: 423–35. [Google Scholar] [CrossRef]

- Huang, Teng-Ching, and Kuei-Yuan Wang. 2017. Investors’ Fear and Herding Behavior: Evidence from the Taiwan Stock Market. Emerging Markets Finance and Trade 53: 2259–78. [Google Scholar] [CrossRef]

- Huang, Teng-Ching, Bing-Huei Lin, and Tung-Hsiao Yang. 2015. Herd Behavior and Idiosyncratic Volatility. Journal of Business Research 68: 763–70. [Google Scholar] [CrossRef]

- Hudson, Yawen. 2014. Investor Sentiment and Herding—An Empirical Study of UK Investor Sentiment and Herding Behaviour. Ph.D. thesis, Loughborough University, Loughborough, UK. [Google Scholar]

- Hwang, Soosung, and Mark Salmom. 2006. Sentiment and Beta Herding. Coventry: Warwick Business School. [Google Scholar]

- Indārs, Edgars Rihards, Aliaksei Savin, and Ágnes Lublóy. 2019. Herding Behaviour in an Emerging Market: Evidence from the Moscow Exchange. Emerging Markets Review 38: 468–87. [Google Scholar] [CrossRef]

- J. P. Morgan/Retuers. 1996. RiskMetricsTM-Technical Document, 4th ed. New York: Martin Spencer. [Google Scholar]

- Jlassi, Mouna, and Kamel Naoui. 2015. Herding Behaviour and Market Dynamic Volatility. Evidence from the US Stock Markets 4: 70–91. [Google Scholar]

- Ju, Xin-Ke. 2019. Herding Behaviour of Chinese A- and B-share Markets. Journal of Asian Business and Economic Studies 27: 49–65. [Google Scholar] [CrossRef] [Green Version]

- Júnior, Gerson De Souza Raimundo, Marcelo Cabus Klotzle, Antonio Carlos, Figueiredo Pinto, and André Luis Leite. 2019. Political Risk, Fear, and Herding on the Brazilian Stock Exchange. Applied Economics Letter 27: 759–63. [Google Scholar] [CrossRef]

- Kabir, M. Humayun. 2018. Did Investors Herd During the Financial Crisis? Evidence from the US Financial Industry. International Review of Finance 18: 59–90. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Amos Tversky. 1979. An Analysis of Decision under Risk. Econometrica 47: 263–92. [Google Scholar] [CrossRef] [Green Version]

- Kaiser, Henry F. 1970. A Second Generation Little Jiffy. Psychometrika 35: 401–15. [Google Scholar] [CrossRef]

- Kaiser, Henry F. 1974. An Index of Factorial Simplicity. Psychometrika 39: 31–36. [Google Scholar] [CrossRef]

- Khan, Mehwish Aziz, and Eatzaz Ahmad. 2018. Measurement of Investor Sentiment and Its Bi-Directional Contemporaneous and Lead-Lag Relationship with Returns: Evidence from Pakistan. Sustainability 11: 94. [Google Scholar] [CrossRef] [Green Version]

- Kremer, Stephanie, and Dieter Nautz. 2013. Causes and Consequences of Short-term Institutional Herding. Journal of Banking & Finance 37: 1676–86. [Google Scholar]

- Lakshman, M. V., Sankarshan Basu, and R. Vaidyanathan. 2013. Market-wide Herding and the Impact of Institutional Investors in the Indian Capital Market. Journal of Emerging Market Finance 12: 197–237. [Google Scholar] [CrossRef]

- Lao, Paulo, and Harminder Singh. 2011. Herding Behaviour in the Chinese and Indian Stock Markets. Journal of Asian Economics 22: 495–506. [Google Scholar] [CrossRef]

- Lee, Charles M. C., Andrei Shleifer, and Richard H. Thaler. 1991. Investor Sentiment and the Closed-End Fund Puzzle. The Journal of Finance 46: 75–109. [Google Scholar] [CrossRef]

- Lee, Keun Yeong. 2006. The Contemporaneous Interactions between the U.S., Japan, and Hong Kong Stock Markets. Economiics Letters 90: 21–27. [Google Scholar] [CrossRef]

- Liao, Tsai-Ling, Chih-Jen Huang, and Chieh-Yuan Wu. 2011. Do Fund Managers Herd to Counter Investor Sentiment? Journal of Business Research 64: 207–12. [Google Scholar] [CrossRef]

- Lin, William T., Shih-Chuan Tsai, and Pei-Yau Lung. 2013. Investors’ Herd Behavior: Rational or Irrational? Asia-Pacific Journal of Financial Studies 43: 755–76. [Google Scholar] [CrossRef] [Green Version]

- Liu, Hai Yue, Aqsa Manzoor, Cang Yu Wang, Lei Zhang, and Zaira Manzoor. 2020. The COVID-19 Outbreak and Affected Countries Stock Markets Response. International Journal of Environmental Research and Public Health 17: 2800. [Google Scholar] [CrossRef] [Green Version]

- Liu, Y. Angela, and Ming-Shiun Pan. 1997. Mean and Volatility Spillover Effects in the U.S. and Pacific-Basin Stock Markets. Multinational Finance Journal 1: 47–62. [Google Scholar] [CrossRef]

- Luo, Ziyao, and Christophe Schinckus. 2015. The Influence of the US Market on Herding Behaviour in China. Applied Economics Letters 22: 1055–58. [Google Scholar] [CrossRef]

- Lux, Thomas. 1995. Herd Behaviour, Bubbles and Crashes. The Economic Journal 105: 881–96. [Google Scholar] [CrossRef]

- Masson, Paul Robert, and Catherine Pattillo. 2005. The Monetary Geography of Africa. Washington, DC: Brookings Institution Press. [Google Scholar]

- McKinsey. 2017. Digital China: Powering the Economy to Global Competitiveness. London: McKinsey Global Institute. [Google Scholar]

- Mulki, Rafika U., and Eko Rizkianto. 2020. Herding Behavior in BRICS Countries, during Asian and Global Financial Crisis. Available online: https://www.researchgate.net/publication/339998992 (accessed on 1 March 2022).

- Nelson, Daniel B. 1991. Conditional Heteroscedasticity in Asset Returns: A New Approach. Econometrica 59: 347–70. [Google Scholar] [CrossRef]

- Oliveira, Marcelle Colares, Domenico Ceglia, and Fernando Antonio Filho. 2016. Analysis of Corporate Governance Disclosure: A Study through BRICS Countries. Corporate Governance 16: 923–40. [Google Scholar] [CrossRef]

- Ouarda, Moatemri, Abdelfatteh El Bouri, and Olivero Bernard. 2013. Herding Behavior under Markets Condition: Empirical Evidence on the European Financial Markets. International Journal of Economics and Financial Issues 3: 214–28. [Google Scholar]

- Parkinson, Michael. 1980. The Extreme Value Method for Estimating the Variance of the Rate of Return. The Journal of Business 53: 61–65. [Google Scholar] [CrossRef]

- Philippas, Nikolaos, Fotini Economou, Vassilios Babalos, and Alexandros Kostakis. 2013. Herding Behavior in REITs: Novel Tests and the Role of Financial Crisis. International Review of Financial Analysis 29: 166–74. [Google Scholar] [CrossRef]

- Poterba, James M., and Lawrence H. Summers. 1988. Mean Reversion in Stock Prices: Evidence and Implication. Journal of Financial Economics 22: 27–59. [Google Scholar] [CrossRef]

- Rapoza, Kenneth. 2019. Most Foreign Capital Flowing into Russian Stock Market Is American. Available online: https://www.forbes.com/sites/kenrapoza/2019/10/22/most-foreign-capital-flowing-into-russia-stock-market-is-american/?sh=418bae4a99e1 (accessed on 1 November 2020).

- Roll, Richard. 1984. A Simple Implicit Measure of the Effective Bid-Ask Spread in an Efficient Market. The Journal of Finance 39: 1127–39. [Google Scholar] [CrossRef]

- Sardjoe, Joey. 2012. Herding in Investor’s Behavior: An Investigation of Herd Behavior in the Russian Stock Market. Tilburg: International Business Administration (Finance), Tilburg University. [Google Scholar]

- Scheinkman, José. A., and Wei Xiong. 2003. Overconfidence and Speculative Bubbles. Journal of Political Economy 111: 1183–219. [Google Scholar] [CrossRef]

- Schwert, G. William. 1990. Stock Volatility and the Crash of ’87. The Review of Financial Studies 3: 77–102. [Google Scholar] [CrossRef] [Green Version]

- Scott, Louis O. 1991. Financial Market Volatility: A Survey. IMF Staff Papers 38: 582–625. [Google Scholar] [CrossRef]

- Seetharam, Yudhvir, and James Britten. 2013. An Analysis of Herding Behaviour during Market Cycles in South Africa. Journal of Economic and Behavioral Studies 5: 89–98. [Google Scholar] [CrossRef] [Green Version]

- Shieber, Jonathan, and Danny Crichton. 2020. Stock Markets Halted for Unprecedented Third Time due to Coronavirus Scare. Available online: https://techcrunch.com/2020/03/16/stock-markets-halted-for-third-time-as-heavy-selling-trips-circuit-breakers-due-to-coronavirus-scare/?guccounter=1 (accessed on 26 October 2020).

- Shiller, Robert J. 1981. Do Stock Prices Move too Much to be Justified by Subsequent Changes in Dividends? The American Economic Review 71: 421–36. [Google Scholar]

- Sias, Richard W. 2004. Institutional Herding. The Review of Financial Studies 17: 165–206. [Google Scholar] [CrossRef]

- Simon, David P., and Roy. A. Wiggins III. 2001. S&P Futures Returns and Contrary Sentiment Indicators. The Journal of Futures Markets 21: 447–62. [Google Scholar]

- Syriopoulos, Theodore, and George Bakos. 2019. Investor herding behaviour in globally listed shipping stocks. Maritime Policy & Management 46: 545–64. [Google Scholar]

- Tan, Lin, Thomas C. Chiang, Joseph R. Mason, and Edward Nelling. 2008. Herding Behavior in Chinese Stock Markets: An Examination of A and B Shares. Pacific-Basin Finance Journal 16: 61–77. [Google Scholar] [CrossRef]

- Topol, Richard. 1991. Bubbles and Volatility of Stock Prices: Effects of Mimetic Contagion. The Economic Journal 101: 786–800. [Google Scholar] [CrossRef]

- U.S. Department of State. 2021. U.S. Relations with Brazil. Available online: https://www.state.gov/u-s-relations-with-brazil/ (accessed on 20 January 2022).

- Vieira, Elisabete F. Simões, and Márcia S. Valente Pereira. 2015. Herding Behaviour and Sentiment: Evidence in a Small European Market. Revista de Contabilidad—Spanish Accounting Review 18: 78–86. [Google Scholar] [CrossRef] [Green Version]

- Wang, Kuei-Yuan, and Yu-Sin Huang. 2018. Effects of Transparency on Herding Behavior: Evidence from the Taiwanese Stock Market. Emerging Markets Finance & Trade 55: 1821–40. [Google Scholar]

- Wang, Tianyi, and Zhuo Huang. 2012. The Relationship between Volatility and Trading Volume in the Chinese Stock Market: A Volatility Decomposition Perspective. Annals of Economics and Finance 13: 211–36. [Google Scholar]

- Welch, Ivo. 1992. Sequential Sales, Learning, and Cascades. The Journal of Finance 47: 695–732. [Google Scholar] [CrossRef]

- Whaley, Robert E. 2000. The Investor Fear Gauge. The Journal of Portfolio Management 26: 12–17. [Google Scholar] [CrossRef]

- World Bank. 2020. Foreign Direct Investment, Net Inflows (%of GDP)—South Africa. Available online: https://data.worldbank.org/indicator/BX.KLT.DINV.WD.GD.ZS?locations=ZA (accessed on 26 October 2020).

- World Health Organization. 2020. Novel Coronavirus—China. Available online: https://www.who.int/emergencies/disease-outbreak-news/item/2020-DON233 (accessed on 1 November 2020).

- Wright, William F., and Gordon. H. Bower. 1992. Mood Effects on Subjective Probability Assessment. Organizational Behavior and Human Decision Processes 52: 276–91. [Google Scholar] [CrossRef]

- Wroblewska, Anna B. 2016. How China’s Stock Market Affects US Indexes. Available online: https://www.wiseradvisor.com/article/how-chinas-stock-market-affects-us-indexes-4190/ (accessed on 1 November 2020).

- Yadav, Sameer. 2017. Stock Market Volatility—A Study of Indian Stock Market. Global Journal for Research Analysis 6: 629–32. [Google Scholar]

- Zheng, Dazhi, Huimin Li, and Xiaowei Zhu. 2015. Herding Behavior in Institutional Investors: Evidence from China’s Stock Market. Journal of Multinational Financial Management 32–33: 59–76. [Google Scholar] [CrossRef]

- Zhu, Lei, Huimin Li, and Dazhi Zheng. 2020. Institutional Industry Herding in China. The Chinese Economy 53: 246–64. [Google Scholar] [CrossRef]

- Zweig, Martin E. 1973. An Investor Expectations Stock Price Predictive Model Using Closed-End Fund Premiums. The Journal of Finance 28: 67–78. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Brazil | China | India | Russia | South Africa | US |

|---|---|---|---|---|---|---|

| CSAD | −7.98 | −7.81 | −8.67 | −4.77 | −5.80 | −6.77 |

| (p value) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) |

| Rmt | −63.38 | −57.39 | −56.87 | −59.02 | −59.25 | −69.28 |

| (p value) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) |

| |Rmt| | −4.51 | −3.72 | −4.48 | −3.22 | −3.79 | −4.67 |

| (p value) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) |

| Rmt2 | −7.70 | −4.81 | −8.42 | −5.51 | −3.64 | −8.15 |

| (p value) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) |

| VIX Index | −65.88 | |||||

| (p value) | (0.00) | |||||

| ŋGARCH(t) | −6.51 | −5.82 | −7.40 | −4.40 | −5.95 | |

| (p value) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| ŋEWMA(t) | −5.93 | −5.17 | −6.37 | −3.13 | −4.54 | |

| (p value) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| ŋP(t) | −10.78 | −4.42 | −11.05 | −3.44 | −4.64 | |

| (p value) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| ŋGK(t) | −10.50 | −4.67 | −5.86 | −3.65 | −5.04 | |

| (p value) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| ŋMA(t) | −5.57 | −4.96 | −8.16 | −4.06 | −8.10 | |

| (p value) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| ŋCW(t) | −5.13 | −6.01 | −8.44 | −3.67 | −5.48 | |

| (p value) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| Result | Stationarity | Stationarity | Stationarity | Stationarity | Stationarity | Stationarity |

| Variables | Brazil | China | India | Russia | South Africa | |

|---|---|---|---|---|---|---|

| CSAD | Mean | 0.6973 | 0.6562 | 0.8262 | 0.5949 | 0.6847 |

| Median | 0.6410 | 0.5978 | 0.7668 | 0.5092 | 0.6207 | |

| Maximum | 2.7927 | 3.2570 | 3.8298 | 5.5714 | 4.0678 | |

| Minimum | 0.3086 | 0.2144 | 0.3959 | 0.0038 | 0.2530 | |

| Standard Deviation | 0.2414 | 0.2716 | 0.2531 | 0.3386 | 0.2819 | |

| Rmt | Mean | 0.0088 | 0.0032 | 0.0172 | 0.0109 | 0.0100 |

| Median | 0.0299 | 0.0263 | 0.0298 | 0.0194 | 0.0235 | |

| Maximum | 5.9404 | 3.8786 | 6.9444 | 10.9556 | 3.1536 | |

| Minimum | −6.9460 | −3.9757 | −6.1243 | −8.9713 | −4.4415 | |

| Standard deviation | 0.7797 | 0.7356 | 0.6128 | 0.7986 | 0.5393 | |

| Observations | 3524 | 3471 | 3531 | 3577 | 3563 |

| Brazil | China | India | Russia | South Africa | |||

|---|---|---|---|---|---|---|---|

| Panel A: Sub-Period 1 (02/07/2007–31/03/2009) | |||||||

| (1) Pre-Global Financial Crisis (02/07/2007–14/09/2008) (2) Global Financial Crisis (15/09/2008–31/03/2009) | F-statistic (Prob.) | Daily | 52.38 ** (0.00) | 2.20 *** (0.09) | 11.45 ** (0.00) | 122.53 ** (0.00) | 56.12 ** (0.00) |

| Weekly | 13.26 ** (0.00) | 0.63 (0.60) | 0.68 (0.57) | 32.79 ** (0.00) | 8.14 ** (0.00) | ||

| Monthly | 3.86 ** (0.03) | 3.86 ** (0.03) | 0.95 (0.44) | 9.72 ** (0.00) | 0.86 (0.48) | ||

| Panel B: Sub-Period 2 (01/04/2009–31/01/2012) | |||||||

| (1) Pre-European Debt Crisis (01/04/2009–31/03/2010) (2) European Debt Crisis (01/04/2010–31/01/2012) | F-statistic (Prob.) | Daily | 10.97 ** (0.00) | 14.41 ** (0.00) | 53.23 ** (0.00) | 57.90 ** (0.00) | 114.51 ** (0.00) |

| Weekly | 7.61 ** (0.00) | 4.63 ** (0.00) | 10.86 ** (0.00) | 16.53 ** (0.00) | 26.42 ** (0.00) | ||

| Monthly | 0.17 (0.91) | 0.69 (0.57) | 1.86 (0.16) | 2.38 *** (0.09) | 6.85 ** (0.00) | ||

| Panel C: Sub-Period 3 (01/02/2012–30/09/2021) | |||||||

| (1) Pre COVID-19 Disease Crisis (01/02/2012–30/12/2019) (2) COVID-19 Disease Crisis (31/12/2019–30/09/2021) | F-statistic (Prob.) | Daily | 40.62 ** (0.00) | 20.75 ** (0.00) | 98.44 ** (0.00) | 10.97 ** (0.00) | 251.86 ** (0.00) |

| Weekly | 5.19 ** (0.00) | 4.68 ** (0.00) | 15.88 ** (0.00) | 3.21 ** (0.02) | 55.39 ** (0.00) | ||

| Monthly | 3.03 ** (0.03) | 10.11 ** (0.00) | 7.84 ** (0.00) | 0.86 (0.47) | 10.91 ** (0.00) | ||

| Brazil | China | India | Russia | South Africa | |||

|---|---|---|---|---|---|---|---|

| Panel A: Non-Crisis Period | |||||||

| Pre-Global Financial Crisis (02/07/2007–14/09/2008) | Daily | Rmt2 (Prob.) | 0.79 (0.72) | −2.52 (0.18) | 12.98 (0.00) | −0.44 (0.79) | 9.34 (0.01) |

| R-square | 0.21 | 0.02 | 0.29 | 0.42 | 0.41 | ||

| Weekly | Rmt2 (Prob.) | 1.35 (0.71) | −1.60 (0.52) | 4.65 (0.49) | 9.47 (0.01) | 24.00 (0.00) | |

| R-square | 0.02 | 0.03 | 0.02 | 0.31 | 0.34 | ||

| Monthly | Rmt2 (Prob.) | 4.38 (0.51) | 0.33 (0.90) | −7.74 (0.24) | 1.84 (0.64) | 1.37 (0.91) | |

| R-square | 0.25 | 0.04 | 0.31 | 0.46 | 0.31 | ||

| Pre-European Debt Crisis (01/04/2009–31/03/2010) | Daily | Rmt2 (Prob.) | 8.11 (0.00) | 1.16 (0.63) | 0.82 (0.47) | 2.77 (0.26) | 16.36 (0.01) |

| R-square | 0.40 | 0.10 | 0.21 | 0.19 | 0.52 | ||

| Weekly | Rmt2 (Prob.) | 17.10 (0.00) | −5.09 (0.53) | 9.46 (0.01) | 4.86 (0.19) | 2.15 (0.83) | |

| R-square | 0.46 | 0.07 | 0.47 | 0.07 | 0.20 | ||

| Monthly | Rmt2 (Prob.) | 4.66 (0.25) | −1.15 (0.35) | 7.86 (0.00) | −0.71 (0.92) | 4.97 (0.67) | |

| R-square | 0.57 | 0.81 | 0.81 | 0.46 | 0.13 | ||

| Pre COVID-19 Disease Crisis (01/02/2012–30/12/2019) | Daily | Rmt2 (Prob.) | 11.54 (0.00) | −0.72 (0.53) | 15.30 (0.00) | 2.99 (0.00) | 11.18 (0.00) |

| R-square | 0.30 | 0.16 | 0.12 | 0.24 | 0.18 | ||

| Weekly | Rmt2 (Prob.) | 6.15 (0.00) | 6.28 (0.00) | 0.21 (0.97) | 6.17 (0.01) | 4.03 (0.37) | |

| R-square | 0.32 | 0.24 | 0.08 | 0.21 | 0.15 | ||

| Monthly | Rmt2 (Prob.) | 5.17 (0.04) | 4.42 (0.00) | 5.79 (0.35) | 1.41 (0.59) | 14.87 (0.08) | |

| R-square | 0.33 | 0.45 | 0.02 | 0.15 | 0.03 | ||

| Panel B: Crisis Period | |||||||

| Global Financial Crisis (15/09/2008–31/03/2009) | Daily | Rmt2 (Prob.) | 0.43 (0.70) | −5.52 ** (0.02) | 3.13 (0.10) | 1.51 (0.04) | 4.84 (0.04) |

| R-square | 0.55 | 0.12 | 0.44 | 0.55 | 0.69 | ||

| Weekly | Rmt2 (Prob.) | 0.17 (0.94) | 3.39 (0.24) | 6.30 (0.02) | −0.46 (0.59) | 5.53 (0.03) | |

| R-square | 0.45 | 0.08 | 0.45 | 0.59 | 0.70 | ||

| Monthly | Rmt2 (Prob.) | −2.68 (0.56) | 1.98 (0.13) | 4.69 (0.22) | 6.63 (0.13) | 14.33 (0.06) | |

| R-square | 0.30 | 0.85 | 0.77 | 0.60 | 0.82 | ||

| European Debt Crisis (01/04/2010–31/01/2012) | Daily | Rmt2 (Prob.) | 1.26 (0.27) | 5.99 (0.02) | 3.87 (0.37) | 2.56 (0.13) | 9.69 (0.00) |

| R-square | 0.32 | 0.09 | 0.14 | 0.25 | 0.65 | ||

| Weekly | Rmt2 (Prob.) | −1.28 (0.51) | 17.44 (0.00) | −0.91 (0.88) | 0.07 (0.97) | 2.72 (0.31) | |

| R-square | 0.36 | 0.40 | 0.13 | 0.26 | 0.48 | ||

| Monthly | Rmt2 (Prob.) | 5.46 (0.24) | 4.76 (0.36) | 6.16 (0.25) | 12.86 (0.04) | 2.44 (0.56) | |

| R-square | 0.33 | 0.25 | 0.15 | 0.26 | 0.36 | ||

| COVID-19 Disease Crisis (31/12/2019–30/09/2021) | Daily | Rmt2 (Prob.) | −0.51 (0.39) | 0.52 (0.82) | −0.87 (0.27) | 5.19 (0.00) | −0.13 (0.95) |

| R-square | 0.54 | 0.11 | 0.48 | 0.51 | 0.39 | ||

| Weekly | Rmt2 (Prob.) | 1.90 (0.05) | 12.92 (0.03) | 3.73 (0.19) | 3.16 (0.03) | −2.59 (0.46) | |

| R-square | 0.60 | 0.12 | 0.24 | 0.51 | 0.31 | ||

| Monthly | Rmt2 (Prob.) | 2.15 (0.01) | 2.03 (0.85) | 0.55 (0.78) | 2.96 (0.59) | 31.44 (0.00) | |

| R-square | 0.70 | 0.03 | 0.52 | 0.28 | 0.74 | ||

| Brazil | China | India | Russia | South Africa | ||

|---|---|---|---|---|---|---|

| ηGARCH (t) | M t | −1.74 × 10−5 | −2.79 × 10−5 | 8.16 × 10−5 | −4.32 × 10−5 | 0.0002 |

| (Prob.) | (0.89) | (0.83) | (0.50) | (0.82) | (0.05) | |

| V t | 0.0028 | 0.0004 | 0.50 | 0.0002 | 0.04 | |

| (Prob.) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| R-square | 0.0031 | 0.0096 | 0.16 | 0.01 | 0.03 | |

| ηEWMA (t) | M t | 0.0010 | −0.0004 | 0.0013 | −0.0005 | 0.0029 |

| (Prob.) | (0.67) | (0.85) | (0.49) | (0.89) | (0.08) | |

| V t | 0.05 | 0.0058 | 8.27 | 0.0025 | 0.64 | |

| (Prob.) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| R-square | 0.0027 | 0.0096 | 0.16 | 0.01 | 0.03 | |

| ηP(t) | M t | 0.0001 | 0.0010 | 0.0005 | 0.0004 | 0.0008 |

| (Prob.) | (0.69) | (0.00) | (0.08) | (0.37) | (0.00) | |

| V t | 0.02 | 0.0022 | 1.10 | 0.0007 | 0.14 | |

| (Prob.) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| R-square | 0.02 | 0.06 | 0.16 | 0.04 | 0.06 | |

| ηGK (t) | M t | −0.0004 | 0.0002 | 0.0003 | −4.70 × 10−5 | 0.0005 |

| (Prob.) | (0.23) | (0.46) | (0.28) | (0.91) | (0.01) | |

| V t | 0.02 | 0.0022 | 1.06 | 0.0007 | 0.12 | |

| (Prob.) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| R-square | 0.02 | 0.06 | 0.17 | 0.04 | 0.06 | |

| ηMV (t) | M t | 6.96 × 10−6 | 2.13 × 10−5 | 9.74 × 10−5 | −8.65 × 10−6 | 0.0002 |

| (Prob.) | (0.97) | (0.88) | (0.46) | (0.97) | (0.10) | |

| V t | 0.0025 | 0.0004 | 0.53 | 0.0002 | 0.04 | |

| (Prob.) | (0.02) | (0.00) | (0.00) | (0.00) | (0.00) | |

| R-square | 0.0017 | 0.01 | 0.15 | 0.01 | 0.02 | |

| ηCW (t) | V t | 0.0004 | 6.42 × 10−5 | 0.05 | 1.30 × 10−5 | 0.01 |

| (Prob.) | (0.12) | (0.00) | (0.00) | (0.12) | (0.00) | |

| R-square | 0.01 | 0.09 | 0.34 | 0.01 | 0.19 |

| Brazil | China | India | Russia | South Africa | |||

|---|---|---|---|---|---|---|---|

| Panel A: Sub-Period 1 (02/07/2007–31/03/2009) | |||||||

| (1) Pre-Global Financial Crisis (02/07/2007–14/09/2008) (2) Global Financial Crisis (15/09/2008–31/03/2009) | F-statistic (Prob.) | ηGARCH | 124.07 ** (0.00) | 13.60 ** (0.00) | 75.83 ** (0.00) | 91.25 ** (0.00) | 106.13 ** (0.00) |

| ηEwma | 212.79 ** (0.00) | 12.60 ** (0.00) | 106.62 ** (0.00) | 164.59 ** (0.00) | 163.11 ** (0.00) | ||

| ηP | 40.45 ** (0.00) | 1.40 (0.25) | 22.82 ** (0.00) | 12.33 ** (0.00) | 13.41 ** (0.00) | ||

| ηGK | 19.45 ** (0.00) | 2.03 (0.13) | 11.55 ** (0.00) | 1.15 (0.32) | 16.93 ** (0.00) | ||

| ηMA | 144.39 ** (0.00) | 10.27 ** (0.00) | 66.00 ** (0.00) | 89.78 ** (0.00) | 99.68 ** (0.00) | ||

| ηCW | 4.96 ** (0.02) | 0.15 (0.86) | 9.51 ** (0.00) | 1.28 (0.30) | 11.93 ** (0.00) | ||

| Panel B: Sub-Period 2 (01/04/2009–31/01/2012) | |||||||

| (1) Pre-European Debt Crisis (01/04/2009–31/03/2010) (2) European Debt Crisis (01/04/2010–31/01/2012) | F-statistic (Prob.) | ηGARCH | 3.68 ** (0.03) | 30.67 ** (0.00) | 97.47 ** (0.00) | 28.04 ** (0.00) | 13.85 ** (0.00) |

| ηEwma | 17.12 ** (0.00) | 34.84 ** (0.00) | 90.55 ** (0.00) | 55.55 ** (0.00) | 25.60 ** (0.00) | ||

| ηP | 27.61 ** (0.00) | 106.09 ** (0.00) | 1.69 (0.18) | 0.15 (0.86) | 27.61 ** (0.00) | ||

| ηGK | 1.77 (0.17) | 13.22 ** (0.00) | 2.08 (0.13) | 1.39 (0.25) | 8.11 ** (0.00) | ||

| ηMA | 2.74 *** (0.07) | 16.50 ** (0.00) | 72.31 ** (0.00) | 29.95 ** (0.00) | 20.81 ** (0.00) | ||

| ηCW | 0.86 (0.43) | 2.57 *** (0.09) | 7.50 ** (0.00) | 0.30 (0.82) | 4.01 ** (0.03) | ||

| Panel C: Sub-Period 3 (01/02/2012–30/09/2021) | |||||||

| (1) Pre COVID-19 Crisis (01/02/2012–30/12/2019) (2) COVID-19 Crisis (31/12/2019–30/09/2021) | F-statistic (Prob.) | ηGARCH | 871.35 ** (0.00) | 51.17 ** (0.00) | 350.56 ** (0.00) | 142.38 ** (0.00) | 413.30 ** (0.00) |

| ηEwma | 906.32 ** (0.00) | 903.22 ** (0.00) | 268.73 ** (0.00) | 121.54 ** (0.00) | 377.22 ** (0.00) | ||

| ηP | 18.90 ** (0.00) | 28.07 ** (0.00) | 236.99 ** (0.00) | 40.88 ** (0.00) | 95.15 ** (0.00) | ||

| ηGK | 19.08 ** (0.00) | 39.61 ** (0.00) | 222.95 ** (0.00) | 52.88 ** (0.00) | 97.69 ** (0.00) | ||

| ηMA | 564.70 ** (0.00) | 41.57 ** (0.00) | 263.44 ** (0.00) | 98.24 ** (0.00) | 341.37 ** (0.00) | ||

| ηCW | 61.64 ** (0.00) | 3.42 ** (0.04) | 7.12 ** (0.00) | 19.94 ** (0.00) | 14.28 ** (0.00) | ||

| Brazil | China | India | Russia | South Africa | |||

|---|---|---|---|---|---|---|---|

| Panel A: Non-Crisis Period | |||||||

| Pre-Global Financial Crisis (02/07/2007–14/09/2008) | ηGARCH | CSAD (Prob.) | 0.08 ** (0.04) | −0.04 (0.52) | 0.08 *** (0.06) | 0.44 ** (0.00) | 0.26 ** (0.00) |

| ηEwma | CSAD (Prob.) | 1.56 ** (0.01) | −0.57 ** (0.51) | 0.04 (0.95) | 0.14 ** (0.04) | 3.79 ** (0.00) | |

| ηP | CSAD (Prob.) | 1.02 ** (0.00) | 0.85 ** (0.00) | 0.92 ** (0.00) | 2.16 ** (0.00) | 1.12 ** (0.00) | |

| ηGK | CSAD (Prob.) | 0.84 ** (0.00) | 0.89 ** (0.00) | 0.82 ** (0.00) | 1.86 ** (0.00) | 0.56 ** (0.00) | |

| ηMA | CSAD (Prob.) | −0.03 (0.47) | −0.08 (0.23) | 0.05 (0.27) | 0.39 ** (0.00) | 0.26 ** (0.00) | |

| ηCW | CSAD (Prob.) | −0.03 (0.75) | 0.12 (0.12) | 0.10 ** (0.00) | 0.14 ** (0.04) | 0.10 ** (0.00) | |

| Pre-European Debt Crisis (01/04/2009–31/03/2010) | ηGARCH | CSAD (Prob.) | 0.09 ** (0.01) | 0.04 (0.51) | 0.59 ** (0.00) | 0.47 ** (0.00) | 0.34 (0.00) |

| ηEwma | CSAD (Prob.) | 3.28 ** (0.00) | 0.49 (0.58) | 8.84 ** (0.00) | 8.72 ** (0.00) | 6.85 ** (0.00) | |

| ηP | CSAD (Prob.) | 1.03 ** (0.00) | 0.51 (0.00) | 0.62 ** (0.00) | 1.10 ** (0.00) | 1.12 ** (0.00) | |

| ηGK | CSAD (Prob.) | 1.39 ** (0.00) | 1.06 ** (0.00) | 0.50 ** (0.00) | 0.75 ** (0.00) | 0.79 ** (0.00) | |

| ηMA | CSAD (Prob.) | 0.08 ** (0.05) | 0.03 (0.70) | 0.58 ** (0.00) | 0.54 ** (0.00) | 0.44 ** (0.00) | |

| ηCW | CSAD (Prob.) | −0.0025 (0.97) | 0.08 *** (0.08) | 0.15 ** (0.00) | 0.07 (0.25) | 0.24 ** (0.00) | |

| Pre COVID-19 Crisis (01/02/2012–30/12/2019) | ηGARCH | CSAD (Prob.) | −0.03 ** (0.00) | 0.18 ** (0.00) | −0.03 *** (0.09) | −0.03 ** (0.01) | −0.01 (0.22) |

| ηEwma | CSAD (Prob.) | −0.93 ** (0.00) | 2.79 ** (0.00) | −0.54 ** (0.05) | −0.78 ** (0.00) | −0.62 ** (0.00) | |

| ηP | CSAD (Prob.) | 0.41 ** (0.00) | 0.51 ** (0.00) | 0.13 ** (0.00) | 0.33 ** (0.00) | 0.16 ** (0.00) | |

| ηGK | CSAD (Prob.) | 0.30 ** (0.00) | 0.55 ** (0.00) | 0.06 (0.14) | 0.39 ** (0.00) | 0.11 ** (0.00) | |

| ηMA | CSAD (Prob.) | −0.05 ** (0.00) | 0.19 ** (0.00) | −0.04 ** (0.01) | −0.04 ** (0.00) | −0.02 ** (0.04) | |

| ηCW | CSAD (Prob.) | 0.04 ** (0.04) | 0.02 (0.24) | 0.0015 (0.93) | −0.02 (0.25) | 0.04 ** (0.04) | |

| Panel B: Crisis Period | |||||||

| Global Financial Crisis (15/09/2008–31/03/2009) | ηGARCH | CSAD (Prob.) | 0.91 ** (0.00) | 0.28 ** (0.00) | 0.58 ** (0.00) | 0.57 ** (0.00) | 0.30 ** (0.00) |

| ηEwma | CSAD (Prob.) | 15.92 ** (0.00) | 4.17 ** (0.00) | 7.13 ** (0.00) | 7.23 ** (0.00) | 3.80 ** (0.00) | |

| ηP | CSAD (Prob.) | 3.47 ** (0.00) | 1.28 ** (0.00) | 1.95 ** (0.00) | 3.06 ** (0.00) | 1.89 ** (0.00) | |

| ηGK | CSAD (Prob.) | 2.42 ** (0.00) | 1.52 ** (0.00) | 1.65 ** (0.00) | 2.22 ** (0.00) | 0.79 ** (0.00) | |

| ηMA | CSAD (Prob.) | 1.10 ** (0.00) | 0.29 ** (0.00) | 0.57 ** (0.00) | 0.61 (0.00) | 0.33 ** (0.00) | |

| ηCW | CSAD (Prob.) | 0.44 ** (0.05) | 0.20 (0.28) | 0.32 ** (0.00) | 0.32 (0.12) | 0.09 (0.63) | |

| European Debt Crisis (01/04/2010–31/01/2012) | ηGARCH | CSAD (Prob.) | 0.11 ** (0.00) | 0.02 (0.25) | −0.02 (0.44) | 0.19 ** (0.00) | 0.17 ** (0.00) |

| ηEwma | CSAD (Prob.) | 1.03 *** (0.07) | 0.24 (0.39) | −0.05 (0.88) | 2.50 ** (0.00) | 2.32 ** (0.00) | |

| ηP | CSAD (Prob.) | 0.63 ** (0.00) | 0.45 ** (0.00) | 0.40 ** (0.00) | 1.19 ** (0.00) | 1.08 ** (0.00) | |

| ηGK | CSAD (Prob.) | 0.34 ** (0.01) | 0.37 ** (0.00) | 0.28 ** (0.00) | 1.03 ** (0.00) | 0.45 ** (0.00) | |

| ηMA | CSAD (Prob.) | 0.06 (0.17) | 0.04 ** (0.05) | −0.03 (0.28) | 0.18 ** (0.00) | 0.17 ** (0.00) | |

| ηCW | CSAD (Prob.) | −0.08 (0.14) | −0.02 (0.47) | −0.01 ** (0.61) | 0.12 ** (0.04) | 0.01 ** (0.86) | |

| COVID-19 Crisis (31/12/2019–30/09/2021) | ηGARCH | CSAD (Prob.) | 1.06 ** (0.00) | −0.01 (0.70) | 0.90 ** (0.00) | 0.30 ** (0.00) | 0.46 ** (0.00) |

| ηEwma | CSAD (Prob.) | 18.32 ** (0.00) | −0.14 (0.65) | 12.62 ** (0.00) | 3.49 ** (0.00) | 7.27 ** (0.00) | |

| ηP | CSAD (Prob.) | 2.45 ** (0.00) | −0.07 (0.24) | 1.84 ** (0.00) | 0.75 ** (0.00) | 0.79 ** (0.00) | |

| ηGK | CSAD (Prob.) | 2.09 ** (0.00) | −0.16 (0.00) | 1.70 ** (0.00) | 0.96 ** (0.00) | 0.67 ** (0.00) | |

| ηMA | CSAD (Prob.) | 1.15 ** (0.00) | −0.05 ** (0.02) | 0.86 ** (0.00) | 0.29 ** (0.00) | 0.49 ** (0.00) | |

| ηCW | CSAD (Prob.) | 0.48 ** (0.00) | −0.04 ** (0.15) | 0.16 ** (0.00) | 0.25 ** (0.00) | 0.12 ** (0.00) | |

| Panel A: Group 1: Volatilities Level ≤ 25% of Volatilities Distributions | ||||||

| Brazil | China | India | Russia | South Africa | ||

| ηGARCH | Rmt2 (Prob.) | 4.28 (0.03) | 3.46 (0.03) | 21.09 (0.00) | 5.21 (0.00) | 10.33 (0.01) |

| R-square | 0.22 | 0.14 | 0.17 | 0.29 | 0.17 | |

| ηEwma | Rmt2 (Prob.) | 7.25 (0.01) | 3.81 (0.01) | 10.68 (0.00) | 6.09 (0.00) | 6.04 (0.14) |

| R-square | 0.15 | 0.15 | 0.10 | 0.28 | 0.16 | |

| ηP | Rmt2 (Prob.) | 19.70 (0.00) | −0.73 (0.65) | 23.16 (0.00) | 26.93 (0.00) | 72.85 (0.00) |

| R-square | 0.03 | 0.01 | 0.08 | 0.09 | 0.09 | |

| ηGK | Rmt2 (Prob.) | 6.37 (0.03) | −3.46 (0.06) | 6.74 (0.03) | 12.66 (0.00) | 12.64 (0.05) |

| R-square | 0.14 | 0.05 | 0.11 | 0.16 | 0.15 | |

| ηMA | Rmt2 (Prob.) | 8.05 (0.00) | 3.37 (0.03) | 12.20 (0.00) | 6.10 (0.00) | 7.00 (0.08) |

| R-square | 0.25 | 0.14 | 0.16 | 0.28 | 0.19 | |

| ηCW | Rmt2 (Prob.) | 1.87 (0.56) | 0.78 (0.84) | −3.57 (0.60) | 3.53 (0.00) | 11.30 (0.12) |

| R-square | 0.25 | 0.03 | 0.04 | 0.48 | 0.13 | |

| Panel B: Group 2: 25% of Volatilities Distributions < Volatilities Level ≤ 50% of Volatilities Distributions | ||||||

| Brazil | China | India | Russia | South Africa | ||

| ηGARCH | Rmt2 (Prob.) | 9.59 (0.00) | 0.73 (0.70) | 8.34 (0.01) | 0.77 (0.78) | 13.01 (0.01) |

| R-square | 0.25 | 0.10 | 0.08 | 0.13 | 0.18 | |

| ηEwma | Rmt2 (Prob.) | 12.80 (0.00) | −0.64 (0.80) | 19.82 (0.00) | 1.33 (0.60) | 12.80 (0.00) |

| R-square | 0.16 | 0.10 | 0.15 | 0.17 | 0.16 | |

| ηP | Rmt2 (Prob.) | 17.10 (0.00) | 10.93 (0.00) | 8.67 (0.01) | 19.40 (0.00) | 46.74 (0.00) |

| R-square | 0.07 | 0.13 | 0.09 | 0.09 | 0.13 | |

| ηGK | Rmt2 (Prob.) | 5.75 (0.04) | 0.98 (0.61) | 11.12 (0.00) | 1.82 (0.23) | 27.34 (0.00) |

| R-square | 0.13 | 0.09 | 0.18 | 0.21 | 0.24 | |

| ηMA | Rmt2 (Prob.) | 0.83 (0.49) | 0.71 (0.74) | 8.47 (0.01) | 4.75 (0.11) | 19.80 (0.00) |

| R-square | 0.18 | 0.09 | 0.10 | 0.16 | 0.21 | |

| ηCW | Rmt2 (Prob.) | 2.65 (0.43) | 2.05 (0.42) | 7.15 (0.30) | −3.10 (0.42) | 11.59 (0.40) |

| R-square | 0.10 | 0.15 | 0.03 | 0.10 | 0.03 | |

| Panel C: Group 3: 50% of Volatilities Distributions < Volatilities Level ≤ 85% of Volatilities Distributions | ||||||

| Brazil | China | India | Russia | South Africa | ||

| ηGARCH | Rmt2 (Prob.) | 7.65 (0.00) | 0.02 (0.99) | 4.65 (0.02) | 7.59 (0.01) | 8.36 (0.01) |

| R-square | 0.29 | 0.12 | 0.18 | 0.19 | 0.22 | |

| ηEwma | Rmt2 (Prob.) | 4.52 (0.01) | 0.55 (0.74) | 10.12 (0.00) | 6.27 (0.05) | 10.36 (0.00) |

| R-square | 0.20 | 0.55 | 0.21 | 0.21 | (0.25) | |

| ηP | Rmt2 (Prob.) | 7.60 (0.04) | −0.24 (0.95) | 9.86 (0.00) | 9.39 (0.06) | 0.79 (0.94) |

| R-square | 0.19 | 0.11 | 0.23 | 0.18 | 0.14 | |

| ηGK | Rmt2 (Prob.) | 6.07 (0.00) | 0.61 (0.84) | 5.85 (0.04) | 6.59 (0.02) | 14.12 (0.00) |

| R-square | 0.27 | 0.11 | 0.16 | 0.25 | 0.22 | |

| ηMA | Rmt2 (Prob.) | 9.91 (0.00) | −1.04 (0.50) | 6.62 (0.00) | 0.62 (0.80) | 7.39 (0.01) |

| R-square | 0.34 | 0.13 | 0.24 | 0.19 | 0.24 | |

| ηCW | Rmt2 (Prob.) | 4.84 (0.31) | 1.03 (0.82) | 14.93 (0.01) | 0.62 (0.80) | −19.10 (0.12) |

| R-square | 0.18 | 0.16 | 0.31 | 0.19 | 0.06 | |

| Panel D: Group 4: 75% of Volatilities Distributions < Volatilities Level ≤ 100% of Volatilities Distributions | ||||||

| Brazil | China | India | Russia | South Africa | ||

| ηGARCH | Rmt2 (Prob.) | −0.85 *** (0.07) | −9.37 ** (0.00) | −1.11 *** (0.09) | −0.15 (0.65) | 1.09 (0.46) |

| R-square | 0.57 | 0.19 | 0.44 | 0.56 | 0.50 | |

| ηEwma | Rmt2 (Prob.) | −1.25 ** (0.01) | −9.37 ** (0.00) | −1.12 *** (0.08) | −0.20 (0.56) | 0.27 (0.86) |

| R-square | 0.60 | 0.19 | 0.44 | 0.57 | 0.50 | |

| ηP | Rmt2 (Prob.) | −0.24 (0.56) | −6.82 ** (0.00) | 0.27 (0.67) | 0.12 (0.72) | 5.29 (0.00) |

| R-square | 0.60 | 0.18 | 0.41 | 0.56 | 0.48 | |

| ηGK | Rmt2 (Prob.) | −0.89 *** (0.06) | −8.55 ** (0.00) | −0.51 (0.43) | −0.19 (0.59) | 2.40 (0.11) |

| R-square | 0.58 | 0.20 | 0.44 | 0.55 | 0.49 | |

| ηMA | Rmt2 (Prob.) | 1.93 (0.20) | −9.51 ** (0.00) | −1.05 (0.10) | 1.93 (0.20) | 1.93 (0.20) |

| R-square | 0.50 | 0.20 | 0.44 | 0.50 | 0.50 | |

| ηCW | Rmt2 (Prob.) | −0.77 (0.44) | 0.48 (0.74) | 1.86 (0.16) | 3.25 (0.06) | 16.02 (0.03) |

| R-square | 0.49 | 0.36 | 0.59 | 0.51 | 0.46 | |

| Indicator Name | Formula/Symbol | |

|---|---|---|

| Market transaction indicator | Turnover | TURN (t) = (turn (t))/(TURNMV5) |

| Market valuation indicator | Price-earnings ratio | PE (t) = Price to earnings ratio |

| Macroeconomic indicators | Consumer price index | GCPI (t) = Log (CPI (t)/CPI (t−1)) |

| Industrial production | GIP (t) = Log (IP (t)/IP (t−1)) | |

| Money supply | GM2 (t) = Log (M2 (t)/M2 (t−1))/ | |

| Exchange rate | GER (t) = Log (ER (t)/ER (t−1)) |

| Brazil | China | India | Russia | South Africa | |

|---|---|---|---|---|---|

| KMO Measure of Sampling Adequacy | 0.5540 | 0.4980 | 0.5270 | 0.5430 | 0.4860 |

| Bartlett Test of Sphericity (Sig.) | 0.0010 | 0.0040 | 0.0300 | 0.0000 | 0.0500 |

| Panel A: Brazil | |||||||

| PC 1 | PC 2 | PC 3 | PC 4 | PC 5 | PC 6 | ||

| TURN(t) | −0.3539 | 0.5736 | −0.1727 | −0.2717 | 0.5539 | 0.3678 | |

| PE(t) | 0.0011 | 0.1688 | 0.9605 | −0.2173 | 0.0341 | −0.0230 | |

| Eigenvector | GCPI(t) | 0.1791 | −0.7056 | 0.0730 | −0.1623 | 0.5939 | 0.2926 |

| GIP(t) | −0.5449 | −0.1937 | 0.1689 | 0.4949 | −0.2370 | 0.5796 | |

| GM2(t) | 0.4355 | 0.2789 | 0.1061 | 0.7512 | 0.3961 | −0.0078 | |

| GER(t) | 0.5967 | 0.1711 | −0.0492 | −0.2083 | −0.3553 | 0.6653 | |

| Eigenvalues | 1.4891 | 1.2080 | 1.0004 | 0.8766 | 0.7498 | 0.6762 | |

| Proportion | 0.2482 | 0.2013 | 0.1667 | 0.1461 | 0.1250 | 0.1127 | |

| Cumulative Proportion | 0.2482 | 0.4495 | 0.6162 | 0.7623 | 0.8873 | 1.0000 | |

| Panel B: China | |||||||

| TURN(t) | 0.1019 | 0.5722 | 0.1350 | −0.6527 | 0.4558 | 0.1013 | |

| PE(t) | 0.6720 | −0.0109 | 0.0887 | 0.2215 | −0.0014 | 0.7010 | |

| Eigenvector | GCPI(t) | 0.4809 | −0.4878 | 0.1484 | −0.0267 | 0.5289 | −0.4779 |

| GIP(t) | 0.0852 | 0.4759 | −0.5339 | 0.5543 | 0.3755 | −0.1811 | |

| GM2(t) | 0.2477 | 0.4516 | 0.6279 | 0.2727 | −0.3296 | −0.3968 | |

| GER(t) | −0.4880 | −0.0638 | 0.5221 | 0.3777 | 0.5126 | 0.2825 | |

| Eigenvalues | 1.3811 | 1.2405 | 1.0332 | 0.9304 | 0.7588 | 0.6561 | |

| Proportion | 0.2302 | 0.2068 | 0.1722 | 0.1551 | 0.1265 | 0.1093 | |

| Cumulative Proportion | 0.2302 | 0.4369 | 0.6091 | 0.7642 | 0.8907 | 1.0000 | |

| Panel C: India | |||||||

| TURN(t) | 0.1996 | 0.4706 | 0.6300 | 0.5560 | −0.1112 | 0.1425 | |

| PE(t) | 0.4602 | 0.0780 | 0.3014 | −0.6714 | 0.1173 | 0.4762 | |

| Eigenvector | GCPI(t) | −0.4506 | −0.1999 | 0.2344 | 0.1349 | 0.7615 | 0.3225 |

| GIP(t) | 0.4679 | −0.0956 | −0.5554 | 0.4398 | 0.1320 | 0.5026 | |

| GM2(t) | −0.0560 | 0.8195 | −0.3585 | −0.1494 | 0.3862 | −0.1589 | |

| GER(t) | −0.5685 | 0.2274 | −0.1425 | −0.0785 | −0.4770 | 0.6091 | |

| Eigenvalues | 1.4528 | 1.0368 | 0.9829 | 0.9633 | 0.9023 | 0.6619 | |

| Proportion | 0.2421 | 0.1728 | 0.1638 | 0.1606 | 0.1504 | 0.1103 | |

| Cumulative Proportion | 0.2421 | 0.4149 | 0.5788 | 0.7393 | 0.8897 | 1.0000 | |

| Panel D: Russia | |||||||

| TURN(t) | 0.4356 | 0.1878 | 0.5487 | −0.3907 | −0.5548 | −0.1157 | |

| PE(t) | 0.5066 | 0.2570 | −0.4655 | 0.3133 | −0.3046 | 0.5194 | |

| Eigenvector | GCPI(t) | −0.1440 | 0.7273 | −0.2072 | 0.2147 | −0.0993 | −0.5929 |

| GIP(t) | 0.4192 | 0.2859 | −0.1720 | −0.5488 | 0.6417 | 0.0028 | |

| GM2(t) | 0.4528 | −0.0407 | 0.4651 | 0.6330 | 0.3890 | −0.1583 | |

| GER(t) | −0.3901 | 0.5351 | 0.4398 | 0.0362 | 0.1627 | 0.5833 | |

| Eigenvalues | 1.5745 | 1.2736 | 0.8889 | 0.8625 | 0.8091 | 0.5914 | |

| Proportion | 0.2624 | 0.2123 | 0.1482 | 0.1437 | 0.1348 | 0.0986 | |

| Cumulative Proportion | 0.2624 | 0.4747 | 0.6228 | 0.7666 | 0.9014 | 1.0000 | |

| Panel E: South Africa | |||||||

| TURN(t) | 0.0589 | 0.6031 | 0.5104 | −0.3349 | −0.2354 | −0.4524 | |

| PE(t) | −0.2694 | −0.1360 | 0.6346 | 0.6794 | 0.1858 | −0.1001 | |

| Eigenvector | GCPI(t) | −0.1449 | 0.4977 | −0.5682 | 0.5031 | 0.0441 | −0.3918 |

| GIP(t) | −0.5640 | 0.4681 | 0.0412 | −0.0483 | −0.0769 | 0.6729 | |

| GM2(t) | 0.5067 | 0.3622 | 0.0920 | 0.0240 | 0.7342 | 0.2528 | |

| GER(t) | 0.5727 | 0.1404 | 0.0615 | 0.4125 | −0.6026 | 0.3394 | |

| Eigenvalues | 1.3297 | 1.1928 | 1.0521 | 0.9145 | 0.8336 | 0.6774 | |

| Proportion | 0.2216 | 0.1988 | 0.1753 | 0.1524 | 0.1389 | 0.1129 | |

| Cumulative Proportion | 0.2216 | 0.4204 | 0.5958 | 0.7482 | 0.8871 | 1.0000 | |

| Null Hypothesis | Period | Brazil | China | India | Russia | South Africa |

|---|---|---|---|---|---|---|

| Panel A: CSADt does not Granger Cause SIXt (Prob.) | Pre-Global Financial Crisis Period | 0.74 | 0.60 | 0.12 | 0.66 | 0.67 |

| Global Financial Crisis Period | 0.05 ** | 0.97 | 0.17 | 0.48 | 0.24 | |

| Pre-European Debt Crisis Period | 0.04 ** | 0.85 | 0.26 | 0.52 | 0.43 | |

| European Crisis Period | 0.01 ** | 0.30 | 0.04 ** | 0.95 | 0.40 | |

| Pre-COVID-19 Crisis Period | 0.50 | 0.04 ** | 0.90 | 0.17 | 0.90 | |

| COVID-19 CRISIS Period | 0.03 ** | 0.18 | 0.01 ** | 0.65 | 0.01 ** | |

| Panel B: SIXt does not Granger Cause CSADt (Prob.) | Pre-Global Financial Crisis Period | 0.22 | 0.47 | 0.02 ** | 0.05 ** | 0.28 |

| Global Financial Crisis Period | 0.97 | 0.50 | 0.14 | 0.98 | 0.83 | |

| Pre-European Debt Crisis Period | 0.43 | 0.15 | 0.69 | 0.51 | 0.10 | |

| European Crisis Period | 0.92 | 0.44 | 0.08 *** | 0.00 ** | 0.75 | |

| Pre-COVID-19 Crisis Period | 0.42 | 0.06 *** | 0.08 *** | 0.17 | 0.00 ** | |

| COVID-19 CRISIS Period | 0.50 | 0.06 *** | 0.03 ** | 0.22 | 0.21 |

| Brazil | China | India | Russia | South Africa | |||

|---|---|---|---|---|---|---|---|

| Panel A: Sub-Period 1 (02/07/2007–31/03/2009) | |||||||

| (1) Pre-Global Financial Crisis (02/07/2007–14/09/2008) (2) Global Financial Crisis (15/09/2008–31/03/2009) | F-statistic (Prob.) | Daily | 3.84 ** (0.00) | 1.89 *** (0.09) | 8.92 ** (0.00) | 4.48 ** (0.06) | 5.51 ** (0.00) |

| Weekly | 0.94 (0.45) | 0.75 (0.59) | 1.82 (0.12) | 5.06 (0.00) | 1.84 (0.11) | ||

| Monthly | 1.50 (0.27) | 0.87 (0.53) | 0.51 (0.76) | 0.77 (0.59) | 3.23 ** (0.04) | ||

| Panel B: Sub-Period 2 (01/04/2009–31/01/2012) | |||||||

| (1) Pre-European Debt Crisis (01/04/2009–31/03/2010) (2) European Debt Crisis (01/04/2010–31/01/2012) | F-statistic (Prob.) | Daily | 3.79 ** (0.00) | 3.70 ** (0.00) | 17.72 ** (0.00) | 7.49 ** (0.00) | 31.90 ** (0.00) |

| Weekly | 2.71 ** (0.02) | 2.91 ** (0.02) | 3.47 ** (0.01) | 7.65 ** (0.00) | 8.85 ** (0.00) | ||

| Monthly | 2.04 (0.11) | 0.71 (0.62) | 0.83 (0.00) | 2.57 ** (0.05) | 3.43 ** (0.02) | ||

| Panel C: Sub-Period 3 (01/02/2012–30/09/2021) | |||||||

| (1) Pre COVID-19 Crisis (01/02/2012–30/12/2019) (2) COVID-19 Crisis (31/12/2019–30/09/2021) | F-statistic (Prob.) | Daily | 29.53 ** (0.00) | 14.64 ** (0.00) | 30.42 ** (0.00) | 53.53 ** (0.00) | 54.57 ** (0.00) |

| Weekly | 5.55 ** (0.00) | 3.26 ** (0.01) | 6.82 ** (0.00) | 6.39 ** (0.00) | 20.32 ** (0.00) | ||

| Monthly | 1.04 (0.40) | 4.43 (0.00) | 5.25 ** (0.00) | 2.00 *** (0.08) | 4.22 ** (0.00) | ||

| Brazil | China | India | Russia | South Africa | |||

|---|---|---|---|---|---|---|---|

| Panel A: Non-Crisis Period | |||||||

| Pre-Global Financial Crisis (02/07/2007–14/09/2008) | Daily | R (us) mt2 (Prob.) | −5.34 (0.01) | 1.76 (0.59) | −0.22 (0.94) | −2.06 (0.73) | 1.39 (0.51) |

| R-square | 0.31 | 0.02 | 0.28 | 0.69 | 0.50 | ||

| Weekly | R (us) mt2 (Prob.) | −2.55 (0.42) | 5.03 (0.41) | −7.19 (0.23) | −4.55 (0.21) | −2.05 (0.66) | |

| R-square | 0.20 | 0.05 | 0.19 | 0.33 | 0.42 | ||

| Monthly | R (us) mt2 (Prob.) | −1.11 (0.80) | 10.38 (0.31) | −3.12 (0.89) | −3.00 (0.52) | −8.49 (0.16) | |

| R-square | 0.36 | 0.28 | 0.33 | 0.57 | 0.75 | ||

| Pre-European Debt Crisis (01/04/2009–31/03/2010) | Daily | R (us) mt2 (Prob.) | −4.62 ** (0.04) | −5.61 ** (0.04) | −12.44 ** (0.01) | 30.92 (0.00) | −3.90 (0.03) |

| R-square | 0.59 | 0.20 | 0.40 | 0.47 | 0.71 | ||

| Weekly | R (us) mt2 (Prob.) | 3.59 (0.21) | −3.39 (0.35) | −8.62 ** (0.04) | −8.53 *** (0.06) | −0.01 (0.99) | |

| R-square | 0.64 | 0.16 | 0.68 | 0.46 | 0.60 | ||

| Monthly | R (us) mt2 (Prob.) | 9.99 (0.03) | 1.99 (0.70) | −8.41 (0.36) | −0.55 (0.95) | −7.56 (0.14) | |

| R-square | 0.82 | 0.83 | 0.85 | 0.83 | 0.67 | ||

| Pre COVID-19 Disease Crisis (01/02/2012–30/12/2019) | Daily | R (us) mt2 (Prob.) | −3.54 ** (0.01) | 7.27 (0.00) | −0.17 (0.90) | 5.45 (0.03) | −1.34 (0.36) |

| R-square | 0.32 | 0.16 | 0.13 | 0.38 | 0.24 | ||

| Weekly | R (us) mt2 (Prob.) | 1.11 (0.50) | 2.47 (0.37) | −1.98 (0.32) | 0.19 (0.92) | 1.96 (0.23) | |

| R-square | 0.38 | 0.24 | 0.09 | 0.22 | 9.20 | ||

| Monthly | R (us) mt2 (Prob.) | −3.15 (0.14) | 3.15 (0.21) | −1.61 (0.52) | −3.36 (0.20) | −1.83 (0.40) | |

| R-square | 0.47 | 0.46 | 0.03 | 0.18 | 0.16 | ||

| Panel B: Crisis Period | |||||||

| Global Financial Crisis (15/09/2008–31/03/2009) | Daily | R (us) mt2 (Prob.) | −1.91 *** (0.06) | −0.12 (0.85) | −1.44 *** (0.06) | −7.30 (0.18) | 0.26 (0.60) |

| R-square | 0.60 | 0.15 | 0.51 | 0.47 | 0.73 | ||

| Weekly | R (us) mt2 (Prob.) | −3.83 *** (0.06) | −0.29 (0.80) | −2.03 (0.11) | −2.30 (0.17) | −0.80 (0.19) | |

| R-square | 0.60 | 0.18 | 0.60 | 0.65 | 0.78 | ||

| Monthly | R (us) mt2 (Prob.) | −9.60 (0.41) | −2.52 (0.47) | −9.27 ** (0.07) | −6.66 (0.52) | 4.31 (0.28) | |

| R-square | 0.58 | 0.90 | 0.97 | 0.83 | 0.91 | ||

| European Debt Crisis (01/04/2010–31/01/2012) | Daily | R (us) mt2 (Prob.) | 0.53 (0.67) | −0.33 (0.84) | −0.24 (0.82) | 5.16 (0.13) | 0.42 (0.55) |

| R-square | 0.40 | 0.09 | 0.15 | 0.40 | 0.56 | ||

| Weekly | R (us) mt2 (Prob.) | −2.84 ** (0.03) | −1.55 (0.47) | −1.48 (0.44) | 1.41 (0.50) | −2.24 (0.03) | |

| R-square | 0.51 | 0.41 | 0.15 | 0.28 | 0.56 | ||

| Monthly | R (us) mt2 (Prob.) | −2.29 (0.22) | −4.56 (0.19) | −4.05 *** (0.08) | 0.85 (0.81) | 1.33 (0.45) | |

| R-square | 0.49 | 0.32 | 0.31 | 0.26 | 0.47 | ||

| COVID-19 Disease Crisis (31/12/2019–30/09/2021) | Daily | R (us) mt2 (Prob.) | −0.69 ** (0.41) | −0.28 (0.61) | 0.39 (0.41) | 0.81 (0.05) | −0.94 (0.31) |

| R-square | 0.73 | 0.13 | 0.56 | 0.61 | 0.65 | ||

| Weekly | R (us) mt2 (Prob.) | −1.53 (0.15) | −0.40 (0.65) | −0.89 (0.41) | 0.29 (0.61) | 4.88 (0.00) | |

| R-square | 0.74 | 0.18 | 0.56 | 0.66 | 0.72 | ||

| Monthly | R (us) mt2 (Prob.) | 2.97 (0.24) | −2.85 (0.45) | −4.24 (0.28) | −0.48 (0.88) | −6.86 (0.41) | |

| R-square | 0.76 | 0.17 | 0.58 | 0.46 | 0.82 | ||

| Brazil | China | India | Russia | South Africa | ||||

|---|---|---|---|---|---|---|---|---|

| Panel A: Sub-Period 1 (02/07/2007–31/03/2009) | ||||||||

| (1) Pre-Global Financial Crisis (02/07/2007–14/09/2008) (2) Global Financial Crisis (15/09/2008–31/03/2009) | F-statistic (Prob.) | Daily | 37.37 ** (0.00) | 1.44 (0.22) | 8.92 ** (0.00) | 17.35 ** (0.00) | 42.75 ** (0.00) | |

| Weekly | 10.25 ** (0.00) | 1.11 (0.36) | 0.92 (0.45) | 24.87 ** (0.00) | 7.48 ** (0.00) | |||

| Monthly | 3.83 ** (0.03) | 0.61 (0.62) | 1.14 (0.38) | 8.11 ** (0.00) | 0.48 (0.75) | |||

| Panel B: Sub-Period 2 (01/04/2009–31/01/2012) | ||||||||

| (1) Pre European Debt Crisis (01/04/2009–31/03/2010) (2) European Debt Crisis (01/04/2010–31/01/2012) | F-statistic (Prob.) | Daily | 9.72 ** (0.00) | 10.38 ** (0.00) | 40.85 ** (0.00) | 15.25 ** (0.00) | 85.35 ** (0.00) | |

| Weekly | 5.58 ** (0.00) | 3.91 ** (0.00) | 8.13 ** (0.00) | 12.53 ** (0.00) | 19.63 ** (0.00) | |||

| Monthly | 0.42 (0.79) | 0.95 (0.45) | 3.55 ** (0.02) | 1.99 (0.13) | 6.36 ** (0.00) | |||

| Panel C: Sub-Period 3 (01/02/2012–30/09/2021) | ||||||||

| (1) Pre COVID-19 Disease Crisis (01/02/2012–30/12/2019) (2) COVID-19 Disease Crisis (31/12/2019–30/09/2021) | F-statistic (Prob.) | Daily | 33.92 ** (0.00) | 15.22 (0.00) | 78.39 ** (0.00) | 68.74 ** (0.00) | 188.81 ** (0.00) | |

| Weekly | 3.74 ** (0.01) | 3.61 ** (0.01) | 12.82 ** (0.00) | 2.60 ** (0.04) | 43.s38 ** (0.00) | |||

| Monthly | 0.57 (0.69) | 7.37 ** (0.00) | 5.85 ** (0.00) | 0.67 (0.62) | 8.03 ** (0.00) | |||

| Brazil | China | India | Russia | South Africa | |||

|---|---|---|---|---|---|---|---|

| Panel A: Non-Crisis Period | |||||||

| Pre-Global Financial Crisis (02/07/2007–14/09/2008) | Daily | VIX US (t) (Prob.) | −0.0054 *** (0.06) | 0.0018 (0.71) | −0.0042 (0.36) | −0.0074 (0.41) | −0.0022 (0.51) |

| R-squared | 0.23 | 0.02 | 0.23 | 0.67 | 0.42 | ||

| Weekly | VIX US (t) (Prob.) | −0.02 ** (0.03) | −0.01 (0.35) | −0.0068 (0.62) | −0.0017 (0.83) | −0.02 ** (0.05) | |

| R-squared | 0.10 | 0.05 | 0.02 | 0.31 | 0.38 | ||

| Monthly | VIX US (t) (Prob.) | −0.0070 (0.73) | 0.0015 (0.98) | 0.07 (0.22) | −0.02 (0.48) | −0.02 (0.70) | |

| R-squared | 0.26 | 0.04 | 0.41 | 0.49 | 0.32 | ||

| Pre-European Debt Crisis (01/04/2009–31/03/2010) | Daily | VIX US (t) (Prob.) | −0.0074 ** (0.05) | 0.0010 (0.95) | −0.0012 (0.89) | 0.02 (0.26) | −0.01 (0.14) |

| R-squared | 0.42 | 0.10 | 0.23 | 0.38 | 0.54 | ||

| Weekly | VIX US (t) (Prob.) | 0.0016 (0.84) | 0.03 (0.02) | 0.0055 (0.72) | −0.02 (0.24) | 0.0021 (0.80) | |

| R-squared | 0.46 | 0.18) | 0.47 | 0.10 | 0.20 | ||

| Monthly | VIX US (t) (Prob.) | 0.01 (0.69) | −0.03 (0.23) | 0.08 (0.04) | 0.06 (0.41) | −0.05 (0.22) | |

| R-squared | 0.58 | 0.84 | 0.90 | 0.51 | 0.29 | ||

| Pre COVID−19 Crisis (01/02/2012–30/12/2019) | Daily | VIX US (t) (Prob.) | −0.0022 (0.05) | 0.0004 (0.82) | 0.0019 (0.06) | 0.0044 (0.02) | −0.0006 (0.57) |

| R-squared | 0.29 | 0.16 | 0.13 | 0.38 | 0.18 | ||

| Weekly | VIX US (t) (Prob.) | −0.0011 (0.66) | 0.0038 (0.35) | 0.0037 (0.21) | −0.0006 (0.83) | −0.0014 (0.55) | |

| R-squared | 0.32 | 0.24 | 0.09 | 0.21 | 0.15 | ||

| Monthly | VIX US (t) (Prob.) | −0.0001 (0.98) | 0.01 (0.49) | −0.0004 (0.96) | 0.0023 (0.77) | 0.0034 (0.61) | |

| R-squared | 0.33 | 0.45 | 0.02 | 0.15 | 0.04 | ||

| Panel B: Crisis Period | |||||||

| Global Financial Crisis (15/09/2008 -31/03/2009) | Daily | VIX US (t) (Prob.) | −0.0034 (0.58) | 0.0027 (0.61) | −0.02 ** (0.01) | −0.0050 (0.90) | −0.0041 (0.31) |

| R-squared | 0.55 | 0.12 | 0.47 | 0.46 | 0.70 | ||

| Weekly | VIX US (t) (Prob.) | −0.01 (0.55) | 0.03 (0.16) | −0.03 *** (0.08) | −0.02 (0.42) | 0.01 (0.44) | |

| R-squared | 0.46 | 0.17 | 0.52 | 0.60 | 0.70 | ||

| Monthly | VIX US (t) (Prob.) | 0.08 (0.28) | 0.0047 (0.78) | −0.0021 (0.96) | −0.10 (0.30) | −0.0066 (0.86) | |

| R-squared | 0.55 | 0.85 | 0.77 | 0.74 | 0.82 | ||

| European Debt Crisis (01/04/2010 -31/01/2012) | Daily | VIX US (t) (Prob.) | 0.0009 (0.56) | 0.0003 (0.89) | −0.0002 (0.89) | 0.02 (0.00) | −0.0006 (0.56) |

| R-squared | 0.32 | 0.09 | 0.15 | 0.36 | 0.65 | ||

| Weekly | VIX US (t) (Prob.) | −0.0005 (0.87) | 0.01 (0.16) | 0.0029 (0.53) | −0.0073 (0.17) | −0.0012 (0.64) | |

| R-squared | 0.36 | 0.42 | 0.14 | 0.27 | 0.48 | ||

| Monthly | VIX US (t) (Prob.) | 0.02 (0.15) | 0.0048 (0.78) | 0.0025 (0.83) | 0.0047 (0.76) | 0.0032 (0.59) | |

| R-squared | 0.40 | 0.85 | 0.15 | 0.26 | 0.37 | ||

| COVID-19 Crisis (31/12/2019 -30/09/2021) | Daily | VIX US (t) (Prob.) | −0.0121 ** (0.00) | −0.0010 (0.69) | −0.0040 *** (0.09) | −0.0050 ** (0.02) | −0.0142 ** (0.00) |

| R-squared | 0.55 | 0.12 | 0.49 | 0.52 | 0.40 | ||

| Weekly | VIX US (t) (Prob.) | −0.0131 ** (0.04) | −0.0061 (0.31) | −0.0078 (0.24) | −0.0003 (0.95) | −0.02 (0.11) | |

| R-squared | 0.62 | 0.13 | 0.25 | 0.51 | 0.33 | ||

| Monthly | VIX US (t) (Prob.) | −0.0195 ** (0.05) | 0.0077 (0.66) | 0.0067 (0.67) | 0.0052 (0.69) | 0.0091 (0.61) | |

| R-squared | 0.77 | 0.04 | 0.52 | 0.29 | 0.75 | ||

| Null Hypothesis | Period | Brazil | China | India | Russia | South Africa |

|---|---|---|---|---|---|---|

| Panel A: CSADi,t does not cause VIXU.S(Prob.) | Pre-Global Crisis Period | 0.39 | 0.07 *** | 0.62 | 0.88 | 0.54 |

| Global Crisis Period | 0.72 | 0.46 | 0.34 | 0.68 | 0.41 | |

| Pre-European Debt Crisis Period | 0.49 | 0.28 | 0.73 | 0.44 | 0.66 | |

| European Crisis Period | 0.09 *** | 0.64 | 0.48 | 0.16 | 0.02 ** | |

| Pre-COVID-19 Crisis Period | 0.02 ** | 0.08 *** | 0.96 | 0.11 | 0.59 | |

| COVID-19 CRISIS Period | 0.01 ** | 0.84 | 0.52 | 0.01 ** | 0.54 | |

| Panel B: VIXU.S(t) does not cause CSADi,t(Prob.) | Pre-Global Crisis Period | 0.28 | 0.36 | 0.33 | 0.27 | 0.62 |

| Global Crisis Period | 0.51 | 0.03 ** | 0.21 | 0.01 ** | 0.44 | |

| Pre-European Debt Crisis Period | 0.03 ** | 0.56 | 0.95 | 0.15 | 0.58 | |

| European Crisis Period | 0.08 *** | 0.27 | 0.91 | 0.14 | 0.00 ** | |

| Pre-COVID-19 Crisis Period | 0.03 ** | 0.01 ** | 0.10 *** | 0.14 | 0.00 ** | |

| COVID-19 CRISIS Period | 0.07 *** | 0.56 | 0.46 | 0.01 ** | 0.36 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, H.; Giouvris, E. Measures of Volatility, Crises, Sentiment and the Role of U.S. ‘Fear’ Index (VIX) on Herding in BRICS (2007–2021). J. Risk Financial Manag. 2022, 15, 134. https://doi.org/10.3390/jrfm15030134

Zhang H, Giouvris E. Measures of Volatility, Crises, Sentiment and the Role of U.S. ‘Fear’ Index (VIX) on Herding in BRICS (2007–2021). Journal of Risk and Financial Management. 2022; 15(3):134. https://doi.org/10.3390/jrfm15030134

Chicago/Turabian StyleZhang, Hang, and Evangelos Giouvris. 2022. "Measures of Volatility, Crises, Sentiment and the Role of U.S. ‘Fear’ Index (VIX) on Herding in BRICS (2007–2021)" Journal of Risk and Financial Management 15, no. 3: 134. https://doi.org/10.3390/jrfm15030134

APA StyleZhang, H., & Giouvris, E. (2022). Measures of Volatility, Crises, Sentiment and the Role of U.S. ‘Fear’ Index (VIX) on Herding in BRICS (2007–2021). Journal of Risk and Financial Management, 15(3), 134. https://doi.org/10.3390/jrfm15030134