1. Introduction

Small to medium businesses (SMEs) have been found to be the engine that drives most economies, owing to the significant contribution they make to economic growth and employment. SMEs account for 60% of employment and up to 90% of the businesses worldwide (

World Bank 2019). Furthermore, in emerging economies, 70% of the employment is generated from the small business sector (

OECD 2017). To the contrary, the other strand of literature demonstrates a limited contribution of SMEs to job creation. For instance,

Henrekson and Johansson (

2010) argued that employment is created by few rapidly growing firms. Similarly, (

Kerr et al. 2013) posited that in South Africa, a larger portion of job creation is attributable to large firms rather than small firms. Therefore, there is a need to nurture the growth of SMEs and ensure they become larger firms to create employment and ultimately contribute to economic growth.

Despite playing such a major role, small businesses have failed to realise the full potential of their growth, particularly in developing countries. Correspondingly,

Adeniran and Johnston (

2012) estimated that the failure rate of small businesses in South Africa is over 70%. Many studies (see for instance

Hussen 2015;

Buckley and Webster 2016) have concluded that lack of access to finance is a major obstacle to the growth of small businesses. Moreover, many scholars (such as

Muriithi 2017;

Adisa et al. 2014) have corroborated the finding that most small businesses, particularly in Africa, rely on internal finance; that is, finance which is sourced from their own savings. However, according to the capital structure theory, both internal and external finance are important for the growth and development of business. Nevertheless, there is more emphasis on the positive influence of external finance on the growth of business (

Cheng and Degryse 2010). Lack of external finance can explain the low survival rate of African businesses, which is below 20%. Many business owners have managed to start their businesses using their savings but are not able to sustain the growth with their personal funds. Consequently, internal funds are not enough to sustain growth; hence, the business fails to make it out of the introduction stage. Therefore, external funding is necessary to facilitate the growth of the business.

External funding can be classified into formal and informal financing.

Elston et al. (

2016) define formal finance as financing capital that has been sourced from banks and other formal financial intermediaries, whereas

Nguyen and Canh (

2020) describe informal finance as small, unsecured and short-in-maturity funding capital. It is sourced from private moneylender(s), other enterprises and relatives and friends of the business owners. Furthermore,

Aliber (

2015) differentiates formal finance from informal finance in terms of regulation, stating that formal financing is under regulation by monetary authorities such as the central bank, while informal financing is not.

Although formal institutions have been used as the main suppliers of funds to the businesses, they are, however, reluctant to offer financial support to small businesses.

Mazanai and Fatoki (

2012) established that the banks are reluctant to extend credit to small businesses because of information asymmetry, high costs of lending small amounts, high perceived risks and lack of collateral security. This has resulted in small businesses being excluded from the financial system. On the other hand, some scholars (such as

Bigsten et al. 2003;

Beck and Torre 2007;

Osei-Assibey 2010) assert that financial exclusion can be voluntary. Similarly,

Fraser et al. (

2015) postulate that some business owners make financial decisions to exclude external finance from their capital. This may be due to a lack of financial and management skills by business owners, particularly in developing countries which are characterised by high illiteracy levels (

Messy and Monticone 2012).

Nguyen and Canh (

2020) classify entrepreneurs into four groups according to their financing decisions: (1) those who do not use external finance at all; (2) those who use external finance sourced from formal funding; (3) those who use external finance sourced from informal funding; and (4) those who use both formal and informal finance. In other words, external finance can be divided into two groups: formal and informal financing. Generally, the small businesses that decide to use external funding opt for informal financing.

Many studies (see for instance

Satta 2004;

Fjose et al. 2010) have revealed that most small businesses, particularly in Africa, depend on informal finance. While these studies have concentrated on analysing the reasons for inability to access formal finance, there is scant literature available to explain the ineffectiveness of informal finance. It should be borne in mind here that most entrepreneurs have used informal finance to start their businesses. Therefore, the attributes of informal finance, which are success factors in the accessing of finance, cannot be ignored in the process of improving the effectiveness of finance provision to small businesses. This study will therefore examine the advantages and disadvantages of informal finance in the context of access to finance by small businesses in Africa.

Notwithstanding the advantages of using formal financing, the use of informal financing by small business owners can be viewed from two perspectives. Firstly, entrepreneurs opt for informal financing even if they qualify for formal financing (

Fraser 2009). Factors which motivate entrepreneurs to choose informal financing are not covered in the available literature, particularly in African countries where there is so much use of informal financing by small businesses. This study therefore aimed at discovering the factors that motivate the business owners to opt for informal financing.

Secondly, entrepreneurs use informal finance as a last resort when they fail to access formal finance or are ineligible for such finance. Some businesses prefer to use formal financing because it has certain attributes that are desirable for businesses in terms of financing. This research effort sought to analyse the main differences between formal and informal financing in an African perspective and how these affect access to finance for small businesses. A number of studies (such as

Muriithi 2017;

Adisa et al. 2014) have explained the reasons for formal lenders’ rationing of credit to small businesses. In addition, a credit gap is created when borrowers fail to obtain sufficient funds from informal lenders while at the same time not qualifying for formal financing. This situation is prevalent among small businesses as they are in the growth stage. Informal lenders often do not have the amount of funds required by SMEs who do not meet the requirements for applying for loans at the banks. The main objective of this article is to recommend what can be done by informal lenders to close the credit gap in order to improve access to finance for businesses which are not eligible for formal finance, yet require funds that are above the credit base of informal lenders.

The rest of the article is organised as follows:

Section 2 compares the features of formal and informal finance in respect to access to finance by small businesses.

Section 3 analyses the factors that militate against SMEs when attempting to access finance in the formal credit market. The factors that motivate entrepreneurs to opt for informal finance even if they are eligible for formal finance are analysed in

Section 4. The conceptual framework is formulated and explained in

Section 5. Recommendations for improving access to finance by small businesses for various stakeholders are discussed in

Section 6.

Section 7 concludes the article.

2. Characteristics of Formal and Informal Finance

The theoretical foundations of this study are anchored on the financial intermediation theory which asserts that intermediaries serve to reduce transaction costs and information asymmetries. Consequently, financial intermediaries tend to shun lending to informal firms as the incidence of information asymmetry would be very high. Secondly, this inquiry is also predicated upon the bank market power hypothesis. African banking markets are by and large very concentrated, with a few players dominating the market and yielding monopolistic power. In such a scenario with limited competition, credit advanced to the informal sector could be curtailed as it could prove costly.

Atieno (

2010) posits that the credit markets in Africa are not able to satisfy the demand for finance from the market from two perspectives. Firstly, the informal financial sector is small, in terms of its resources, which are insufficient to accommodate all the borrowers. In other words, loan rationing in the informal financial sector is attributable to the limited financial resources. Secondly, while the formal finance sector has sufficient resources, the loan administration processes and lending terms and conditions constrain access to loans by some borrowers, particularly small businesses. Similarly,

Aryeetey (

2008) posited that sub-Saharan African financial markets are too fragmented, and they result in credit gaps.

Atieno (

2010) further highlights that credit gaps are created when borrowers fail to obtain the required finance from the formal sector because of ineligibility, at the same time failing to acquire sufficient finance from the informal sector because of inadequate funds in the lenders’ coffers.

Formal finance has been acknowledged as a reliable source of finance and is secured from regulated financial institutions, usually banks.

Aryeetey (

2008) differentiated formal finance from informal in terms of principal clients and being regulated by a central bank. The principal clients for informal finance are self-employed and poor, while the large businesses are clients for the formal finance sector, which is regulated by the central bank. Securing finance from the banks is a cumbersome task, particularly for small businesses. The collateral asset and Know-Your-Client (KYC) information requirements by banks inhibit access to finance for SMEs. SMEs’ inability to keep proper records also results in them failing to provide the required information. Large businesses have greater advantages over small ones in regard to the provision of the information requirement, as their systems enable them to keep proper records. The element of a separate legal entity enables them to keep proper records, and in some cases their information (particularly public companies) is also publicly available.

Generally, small business owners or managers in developing countries lack financial management skills since these regions are generally characterised by low financial literacy rates (

Adams and Nyuur 2018). An inability to keep proper records can be attributable to low financial literacy. In developed countries, credit bureaus help in acquiring information about borrowers at a low cost. However, most of the developing countries do not have such infrastructure nor the expertise required to run sound credit bureaus; hence, obtaining such information tends to be expensive and seldom available. On the other hand, informal finance lenders do not put much emphasis on searching and using KYC information for screening a borrower’s eligibility to access a loan. They depend more on relationships and they trust information (

Karaivanov and Kessler 2017). Accordingly, owing to less rigorous information requirements, SMEs tend to turn to informal lenders for financial assistance.

Collateral security, which lenders usually request so they can hedge against default risk, is another requirement which hinders SMEs in acquiring formal finance. Generally, SMEs do not own much property which can be pledged as collateral security. In Africa, default rates by SMEs in the formal financial sector are high, and hence, they are considered the riskiest clients (

Nguyen and Canh 2020). Contrary to the formal sector, informal lenders normally do not request collateral security because the borrower is assessed on the basis of the relationship and trust.

Karaivanov and Kessler (

2017) posit that unlike formal credit, informal credit uses ‘social collateral’ as a substitute for physical collateral. In addition, loan recovery rates in the informal finance sector are high. In general, informal finance lenders do not provide large or long-term loans, and this also helps as a form of risk management to limit loss. By virtue of less interference from regulators, informal finance is client oriented. The transactions are customised based on trust and relationships, which provides the flexibility and convenience that is more advantageous to small businesses.

However, informal finance is also characterised by exorbitant interest rates charged by lenders (

Babajide 2011). Unlike the rates of formal finance, informal finance rates are not regulated; hence, lenders are at liberty to charge whatever they want. Additionally, borrowers who approach informal lenders are usually perceived to be stranded, as they are not able to secure loans from the formal sector, hence lenders are at an advantage when it comes to bargaining. Against this backdrop, some governments have attempted to reduce the existence of informal finance by introducing softer loans to the business sector through banks. Despite such attempts to eliminate it, the informal finance sector remains almost indispensable because it keeps re-emerging and mobilising the savings which later helps in creating many lending units.

Notably, SMEs in developing economies are usually informal and constitute the majority of the business sector. For instance,

Fapohunda (

2012) postulated that over 60% of the working population in developing economies earn their living in the informal sector. However,

Distinguin et al. (

2016) argue that economies dominated by informal sectors tend to face tighter constraints on access to formal finance by SMEs. Arguably, this can be due to a lack of traceability of their activities. Furthermore,

Atieno (

2010) posits that informal lenders do not attach much importance on monitoring the use of funds; instead, they concentrate on loan screening. However, if lenders fail to control or monitor the activities of borrowers, moral hazards may occur.

Table 1 compares and contrasts the important aspects of formal and informal finance lending by drawing from existing studies.

3. Accessing Finance from the Formal Credit Markets

Formal credit markets, particularly in developing economies, have been mainly dominated by banks. Arguably, the banking sector is the most regulated industry. This is to ensure financial stability and other important aspects such as consumer protection. Notably, the role of banks within the financial system is to mobilise savings from surplus units and allocate them to deficit units (the borrowers) (

Mishkin 2007;

Cecchetti 2012). Therefore, banks are compelled to ensure that adequate deposits are mobilised, and profitable projects are funded while monitoring the risks. However, sub-Saharan African banks tend to be excessively liquid due to a lack of screening expertise and entrepreneurship support (

Beck and Torre 2007). At the same time, small businesses that are in need of finance struggle with access to bank finance due to excessive bureaucracy.

By virtue of its rigorous regulatory framework, banks’ operations are rigid and frequently not favourable for some clients such as small businesses. Therefore, because of excessive bureaucracy in the formal market, access to finance is a problem. Attempts to improve access to finance by small businesses have attracted a lot of attention by researchers and policymakers alike so as to foster the growth and development of the SME sector. Various scholars have analysed the barriers to access to finance from different perspectives. Scholars such as

Buckley and Webster 2016 and

Hussen (

2015) differentiate the barriers as supply- and demand-side barriers. They regard supply-side barriers as those originating from financial institutions, while demand-side barriers originate from SMEs.

From another point of view,

Hyz (

2011) contends that the barriers will depend on the business life cycle of the firm. During the early stages of the life cycle, businesses rely mainly on personal savings and borrowings from family and friends. In those early stages, small businesses are also considered to be high risk by financial institutions because assessment of their chances of survival is difficult. Additionally, the availability of information to be used is very limited. As the business develops through the growth stages, the need for external finance increases and barriers differ from those encountered in the initial stage. This supports the pecking order hypothesis, which holds that businesses prefer internal funds first, then the external finding as they grow.

The need for external finance can be seen in terms of

Modigliani and Miller’s (

1963) theory of capital structure, which postulates that the firm will benefit from an interest tax shield when debt is included in the capital structure. However, the benefit of a tax shield is only relevant to businesses that are liable for tax payments. Considering that most small businesses in Africa are exempt from paying tax due to low income, they would not benefit from an interest tax shield.

Additionally,

Chimpango (

2017) avers that bank loans are the most available option for small businesses since most capital markets in developing economies are underdeveloped. However, various studies (for instance

Fafchamps et al. 1995;

Mazanai and Fatoki 2012;

Buckley and Webster 2016;

Hussen 2015) have shown that the banks are rationing the extension of loans to most SMEs. The extant literature has shown that the reasons for barriers to access to finance can be attributable to credit rationing by the financial institutions and the inadequacy of the financial and physical infrastructure of the financial system.

The credit rationing theory by

Fafchamps et al. 1995 exonerates banks from giving loans to small businesses, as it states that banks can only give credit to debtors if their opportunity cost is less than the maximum that the debtor can repay. Similarly,

Mazanai and Fatoki (

2012) contend that the financial institutions operate under credit rationing so as to protect the depositors’ interests, as they have to bear the responsibility for nonperforming loans that are given to small businesses. Therefore, in dealing with nonperforming loans, banks need to concentrate more on credit risk management and credit monitoring. Moreover,

Mazanai and Fatoki (

2012) conclude that the banks are reluctant to extend credit to SMEs because of asymmetric information, high administration costs, lack of collateral and perceptions of high risk.

Various studies (such as

Kodippiliarachchi 2018;

Prempeh 2015, p. 9;

Mazanai and Fatoki 2012) have revealed that information asymmetry is the major basis of credit rationing. However, information asymmetry is also associated with adverse selection and moral hazard problems. Furthermore,

Moyo and Sibindi (

2020) postulate that adverse selection and moral hazard problems may lead to increased costs and reduced availability of credit. Lack of information leads to increased costs in gathering information; hence, the administration costs of extending credit to SMEs are relatively higher. Additionally, according to

Steel et al. (

1997), information asymmetry raises greater concerns regarding the selection of noncreditworthy clients (adverse selection) even though there is the problem of a client potentially changing their mind about loan use (moral hazard).

Furthermore, lack of information also leads to SMEs being perceived as high-risk clients. One of the major responsibilities of the financial institution is to ensure safety of depositors’ funds. Therefore, to minimise risk, financial institutions will always request collateral security. Apparently, small businesses in developing countries do not have enough assets. Moreover,

Bigsten et al. (

2003) established that 90% of SMEs in Africa are failing to secure loans because of lack of collateral security.

As the business grows, the need for external finance also increases. Generally, large and long-term finance is the type of finance suitable for business expansion. However, the informal finance sector is usually not capable of offering such finance due to limited resources. Therefore, businesses in the growth stage need to source finance from the formal sector, as their financial requirements exceed the limits of the informal sector. Furthermore, the formal sector provides other nonfinancial services such as financial and management (expertise) advice to clients. The loans given to clients are monitored throughout the entire term, and this also helps as a form of risk management.

Notwithstanding the backdrop of excessive regulation of formal financial markets, there are attractive attributes which include consumer protection, controlled interest rates and the availability of larger and long-term loans. In this regard,

Jones et al. (

2000) summarise the advantages of formal finance as low interest, availability of large amounts—which is good for expanding business particularly when timing is not crucial—and also when collateral is available. In contrast to the informal financial sector, interest rates are monitored by the central banks (

Sagrario Floro and Ray 1997); hence, they are normally lower and clients are protected from being exploited. Moreso, the regulators ensure transparency so as to safeguard the stability of the financial system.

Table 2 summarises empirical evidence on the factors that affect access to finance by SMEs.

4. Factors That Influence the Use of Informal Finance by SMEs

Notwithstanding the benefits for the economy that stem from the use of formal finance, various studies (such as

Sagrario Floro and Ray 1997;

Wiyani and Prihantono 2016;

Babajide 2011) have shown that informal finance also plays a major role in the financial system. Apart from enhancing the financial system, informal finance has been the backbone of small businesses, especially those in the informal sector and particularly in developing economies. Therefore, informal finance is not just a manifestation of weaknesses in the formal financial system but is also a necessary faction of the financial system.

Some business owners voluntarily opt for informal finance because of its advantages which include, amongst others, its flexibility and convenience in disbursing finance. Flexibility and convenience attract small business borrowers as there is low information required for accessing the loans, considering that such businesses lack such information. Similarly,

Wiyani and Prihantono (

2016) posit that small businesses are comfortable in dealing with the informal financial sector as they perceive that it is easy to obtain funds and they do not need various requirements and collateral. Additionally, there are less stringent KYC requirements; thus, borrowers believe they can still maintain their privacy.

Wiyani and Prihantono (

2016) also postulate that small business owners believe that the assessment period in the informal financial sector tends to be short, resulting in speedy processing of the transaction. Considering that small businesses constantly struggle with cash flows for working capital, this works to their advantage. Although many studies have established that the interest rates charged by informal lenders are relatively high compared to the formal sector, the perceptions of informal borrowers differ.

Wiyani and Prihantono (

2016), for example, established that the perception of informal borrowers is that the interest rates charged by informal lenders are justified and they are cost effective when considering the turnaround time of the loan application.

Considering that most informal lenders do not operate under particularly formalised or regulated environments, some firms can benefit from that. Some firms prefer informal finance to avoid regulations and taxes. Due to the fact that the informal lenders are not regulated by monetary authorities, borrowers can easily escape the taxes.

Nguyen and Canh (

2020) examined the factors influencing entrepreneurs to make formal and informal financing decisions. They postulate that financing decisions depend on (1) the type of owner, (2) the type of assets owned and (3) the location of the firm. They also posit that business owners can be influenced by cognitive financial constraints emanating from the cultural background and lack of financial skills and knowledge of the advantages of formal finance. Some small business owners are afraid of being turned down, while others associate borrowing with high risk. Furthermore, they also conclude that the entrepreneurs who are likely to use informal finance are younger and more comfortable with taking risks. They also established that firms located in remote areas and those located in places with better governance are most likely to use informal finance.

Santos (

2019) analysed the perceptions of vendors toward informal lending. He established that the vendors were convinced that informal lenders are helpful in terms of costs and reliability. This finding on cost effectiveness is in line with other scholars such as

Wiyani and Prihantono (

2016). Notwithstanding the high nominal interest rates, other costs associated with loan disbursement include opportunity costs incurred while waiting for the whole process of loan application and the costs of travelling to the formal financial institutions in some cases. Arguably, in informal finance, such costs are reduced since the borrowers and lenders in the informal financial sector are usually within the same vicinity. Additionally,

Santos (

2019) discovered that vendors attached positive attributes (such as patience, sympathy and humanity) to informal lenders. This is attributable to the social ties because the informal lenders normally extend credit to known clients.

On the other hand,

Aryeetey (

1993) analysed the characteristics of informal finance in relation to the private sector. He concludes that informal finance has not been effective for the private sector. He further contends that the experience of dealing with small loans is less germane to growing businesses. In line with other studies such as that performed by

Jones et al. (

2000), growing businesses need large and long-term loans. Therefore, informal finance is invariably more useful to small businesses, while formal finance is crucial for large and growing businesses. This is supported by various studies (for instance

Sagrario Floro and Ray 1997;

Madestam 2014;

Babajide 2011) which analysed the links between formal and informal finance.

Madestam (

2014) evaluated the coexistence of the formal and informal credit markets and established that banks have unlimited funds but are unable to control the use of loans, whilst informal lenders have limited funds but can prevent nondiligent behaviour of the borrower.

Madestam (

2014) also established that legal institutions increase the availability of formal finance but that borrowers often divert their bank loans (moral hazards). At the same time, informal finance can monitor borrowers by extending credit to known clients. In other words, the informal lenders’ monitoring ability can help the banks to channel formal credit to the clients through the informal sector. Therefore, in light of this argument, informal finance cannot be viewed as a competitor of, but rather as complementary to, formal finance.

Although studies show that economies are supporting the coexistence of both the formal and informal financial sector, some flaws have emerged. For instance,

Babajide (

2011) established that there is a strong link between formal and informal finance on the saving side but a weak link on the credit side. Similarly,

Sagrario Floro and Ray (

1997) investigated the linkage between formal and informal finance in The Philippines. They opine that the relationship can either be vertical where the informal lenders act as a conduit for formal finance, or horizontal where they are competitors of the banks. They further argue that the strategic–cooperation relationship between formal and informal lenders may reduce the availability of formal credit.

Empirical studies on informal finance in developing countries backdate to

Mrak (

1989), where informal finance was differentiated from formal finance in Zambia in terms of flexibility, which is reflected in heterogeneity forms. It was also ascertained that there is better accessibility, popular participation, local adaptability and social integration at both the local and regional level at the informal financial markets. Despite these positive attributes,

Mrak (

1989) also noted that the interest rates are higher in the informal financial sector. The latter study, by

Sebatta et al. (

2014), assessed the factors that affect the decision to access the informal finance in Zambia. They established that the level of education, size of household and payback period influence the decision to participate in the informal financial markets.

Similarly,

Okurut et al. (

2005) investigated the individual character that influence demand and supply of informal credit in Uganda. They established that age, educational level, dependency ratio household expenditure and regional location are factors that influence demand for informal credit. On the other hand,

Okurut and Botlhole (

2009) investigated the terms and conditions of the informal credit market and its target clientele in Botswana. They established that the market is mainly used by customers who need short-term consumption loans and small amounts; however, they also highlighted that the interest rates are higher than the formal counterparts. They further noted that they use innovative collateral substitutes such as ATM cards and other valuable household assets.

Atieno (

2010) established that 67% of the enterprises in Kenya who use credit acquire it from the informal financial markets and those who did not apply for credit do not reflect that they do not need credit because only 15% of them are not credit constrained. She posited that informal finance provides easier access to credit facilities for SMEs; therefore, there is a need to expand the capacity of informal finance to increase the potential ability of lending to SMEs. However,

Mwangi and Kimani (

2015) revealed that the challenges hindering participation in Kenyan informal markets include poor governance, low attendance and payment defaulting. In addition,

Sile and Bett (

2015) analysed the determinants of informal finance use in Kenya. The results revealed the attitude toward the use of formal finance and internal business regulations are determinants of use of informal finance. However, they posited that informality is a result of inefficiencies of formal finance.

Table 3 summarises the key findings from select empirical studies on the factors that influence the selection of informal finance as a source of funding by SMEs.

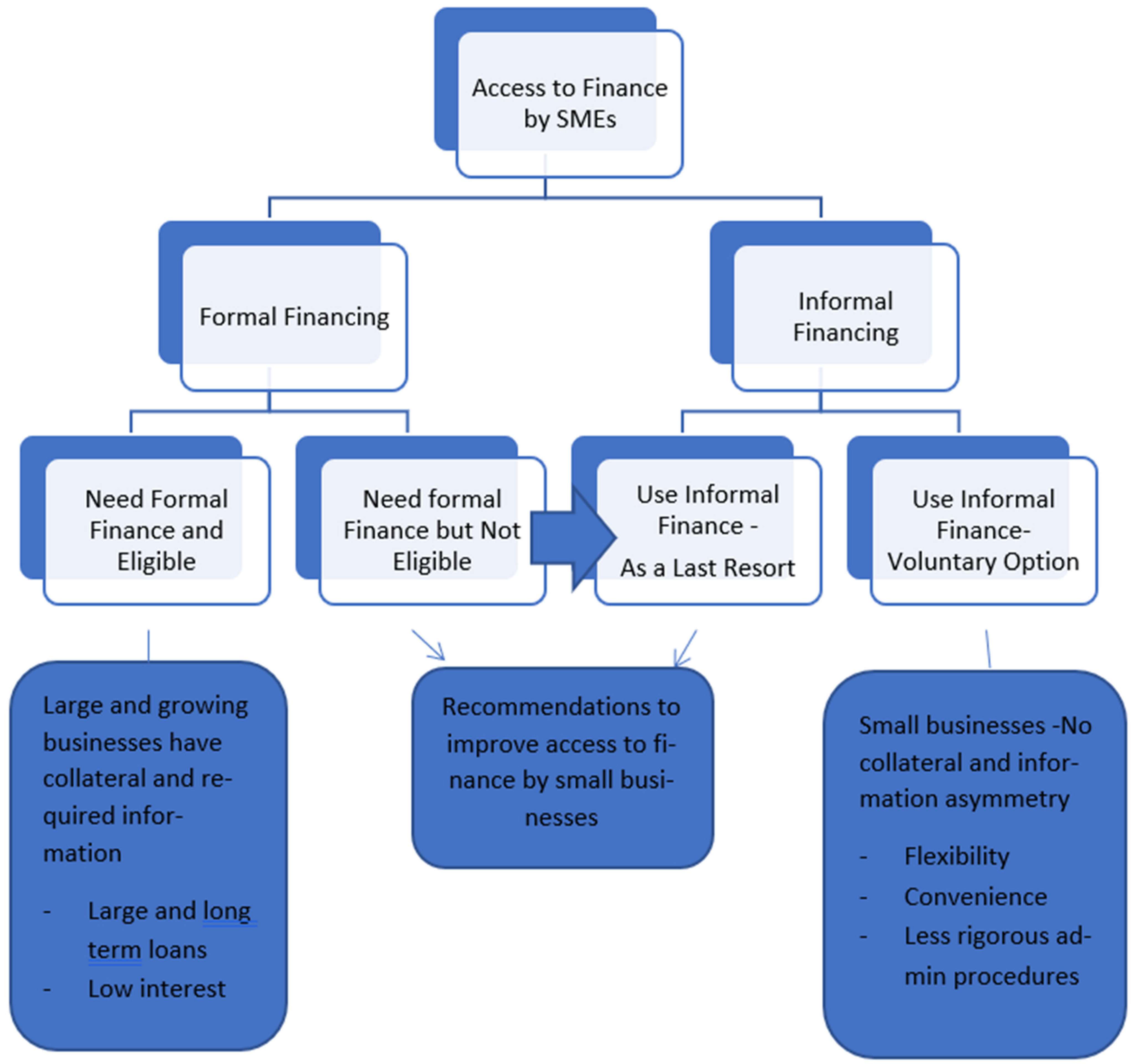

5. Conceptual Framework for Accessing Finance by SMEs

The conceptual framework for accessing finance by SMEs is depicted in

Figure 1. In essence, the conceptual framework is predicated on the fact that SMEs that seek funding have two options for sourcing finance: formal and informal finance. However, the formal finance sector has some restrictions resulting in some SMEs being eligible and some not. Usually those that are eligible are large, growing and have collateral assets, as well as access to large and long-term loans with low interest. Those who do not qualify are forced to access informal finance. On the other hand, there is less eligibility assessment in the informal financial sector.

There are two viewpoints of using informal finance. Firstly, users voluntarily opt for informal finance because of its flexibility, convenience and less rigorous administrative procedures. The other users opt for informal finance as a last resort because they are not eligible for formal finance; hence, the users are not fully satisfied with the products. The financial products in the informal sector normally comprise small, short-term loans with high interest rates which are not attractive to some SMEs. Therefore, this study is aimed at coming up with recommendations about how to improve access to finance, particularly for this unsatisfied group of SMEs.

6. Recommendations to Improve Access to Finance by SMEs

Considering the role played by informal finance in the economy, the sector is indispensable, particularly in facilitating the availability of finance to small businesses. Given this background, there is much need for all the relevant stakeholders to support the sector. The strengths and advantages of formal financing should be adopted and simultaneously improve the weaknesses of the informal sector. Some recommendations for improving the access to finance by African SMEs are enumerated as follows:

(a) Establishment of a relevant regulatory framework

The informal financial sector has been regarded as being exploitative of stranded clients due to the lack of a structured regulatory framework. Monetary authorities have played an important role in financial systems coming up with regulatory frameworks that protect consumers from being exploited by formal lenders. Hence, formal financial institutions cannot exploit consumers by charging high interest rates. Therefore, the regulations that are proposed to reduce the exploitation problems include the establishment of operating licences and contract terms and conditions which are not as rigorous as those of the formal financial sector. Although there might be scepticism about regulations as being a duplication of the formal sector, emphasis should be placed on ensuring that the set conditions are viable for the intended clientele. Since the regulatory framework of formal finance has frequently failed to accommodate the small business, the other option is to improve the frameworks used in the financial system.

(b) Linking formal and informal finance

Informal finance can be linked to the formal finance sector from two standpoints. Firstly, savings can be mobilised in the informal sector, and deposited in the formal sector. Thereafter, the deposits can be used as insurance or collateral for each member to obtain a loan from the formal institution where the deposits are made. In this case, the formal financial institution will have covered the collateral security in the form of deposits, while an element of information asymmetry for individuals is covered at the level of the informal sector by the group which selects its members based on the social costs. Secondly, informal lenders can act as a conduit for finance by obtaining large amounts from formal finance and lending small, manageable amounts to small businesses. Unfortunately, this will only work well when the funds needed by the small businesses are within the manageable range.

(c) Improving risk management techniques

Generally, informal lenders provide small and short-term loans which are a way of managing the risk of default, as there is more exposure to default risk in long-term loans. This, however, tends to exclude the small businesses that need large amounts of finance but which at the same time do not qualify for formal finance. In such situations, informal lenders have to incorporate some of the attributes of formal finance. In other words, they have to increase the risk management techniques by customising those that are applied by formal lenders. For large amounts, it would be necessary to concentrate on monitoring the use of loans to reduce moral hazards. The keeping of records and management advice should also be provided to the borrower to ensure the high performance of the business. Moreover, this will be more effective particularly if the business in question is pledged as collateral. Furthermore, when assessing the business for loan eligibility, its viability must be considered rather than its present state. Additionally, governments must provide guarantees to promote access to finance by small businesses.

(d) Making use of FinTech platforms

It has been documented that FinTech has managed to speed up financial inclusion, particularly in developing economies (

Rizvi et al. 2017). At the same time, FinTech platforms are known to offer solutions to both physical infrastructure and cost challenges. Although the adoption of FinTech has its own risks and shortcomings, its benefits in terms of access to finance surpass the disadvantages. Therefore, both the formal and informal finance sectors need to cautiously adopt FinTech to improve access to finance.

With the advent of the Fourth Industrial Revolution, FinTech platforms cannot be ignored in any sector including informal finance lenders. FinTech products such as mobile money and crowd funding can still be used by informal lenders.

FinTech products are widely acknowledged as tools for reducing the costs of financial products (

Rizvi et al. 2017). The reduction of costs will ultimately have positive impacts on the high interest rates charged by lenders. On the other hand, some businesses are restricted by the proximity of formal institutions from accessing finance, particularly those in remote areas. Adoption of FinTech products can solve the proximity challenges as well as disbursement time. Although FinTech can solve a number of challenges, the involvement of other stakeholders would be necessary, and large investments in terms of infrastructure and administration are needed.

7. Conclusions

The informal financial sector has played a vital role in the financial system by servicing small businesses which are struggling to access financial help from the formal financial system. Notwithstanding the fact that the informal sector has been characterised as exploitative of clients, some business owners voluntarily opt for informal finance. The aim of the study was to ascertain the factors that motivate entrepreneurs to opt for informal finance. Accordingly, entrepreneurs perceive that the sector is advantageous in terms of convenience, flexibility and less rigorous information requirements. On the other hand, some businesses access the informal finance sector as a last resort, as they do not qualify for formal finance because of credit rationing by the banks and the inadequacy of the financial and physical infrastructure in the financial system. Even though the informal finance sector is a rescuer of small businesses, it also suffers from the limited resources to finance the growing businesses, and this ultimately cripples the survival of small businesses.

The study also analysed the characteristics of both formal and informal finance from the point of view of access to finance by SMEs. Formal finance is characterised by large and long-term finance, and it operates within a regulated environment. Interest rates charged in the formal financial system are relatively lower than the informal financial market. The study also documented that both sectors are important in the financial system, and they can be complementary to each other rather than competitors. While the formal lenders’ forte is its unlimited availability of funds and the informal lenders’ forte is that of monitoring ability, formal credit can reach the SMEs through informal channels. It was also established that FinTech platforms can be used by the informal sector, considering its rapid growth particularly in developing economies.

Therefore, there is a need for the government and relevant stakeholders to create a suitable environment and policies which will nurture the growth of the informal finance sector. Furthermore, informal finance should not be perceived as a weakness of the financial system or a competitor of formal finance, but rather as a complementary sector.

Considering that informal finance lies on a wide continuum ranging from loans from family and friends to microfinance, more research should be conducted to ascertain the effects of each type of informal finance on access to finance by SMEs. Furthermore, SMEs can either be formal or informal, and this can also affect their ability to access finance. Further research should be conducted to find out if formalising SMEs could improve access to finance. If policymakers are to come up with regulations for the informal financial sector, it cannot be one-size-fit-all. The regulations should depend on the type of informal financial provider and the type of SME.

{kind=link}