Crypto-Coins and Credit Risk: Modelling and Forecasting Their Probability of Death

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Credit Risk for Crypto-Coins

- The approach by Feder et al. (2018): first, a “candidate peak” is defined as a day in which the 7-day rolling price average is greater than any value 30 days before or after. Moreover, to choose only those peaks with sudden jumps, a candidate is defined as a peak only if it is greater than or equal 50% of the minimum value in the 30 days prior to the candidate peak, and if its value is at least 5% as large as the cryptocurrency’s maximum peak. Given these peak data, Feder et al. (2018) consider a coin abandoned (=dead), if the daily average volume for a given month is less than or equal to 1% of the peak volume. In addition, if the average daily trading volume for a month following a peak is greater than 10% of the peak value and that currency is currently abandoned, then Feder et al. (2018) change the coin status to resurrected.

- The simplified Feder et al. (2018) approach proposed by Schmitz and Hoffmann (2020): a crypto-currency can be classified as dead if its average daily trading volume for a given month is lower or equal to 1% of its past historical peak. Instead, a dead crypto-currency is classified as “resurrected” if this average daily trading volume reaches a value of more or equal to 10% of its past historical peak again.

- The professional rule that defines a coin dead if its value drops below 1 cent, and alive if its value rises above 1 cent.

3.2. Credit-Scoring Models and Machine Learning

3.3. Time-Series Methods

- Consider a generic conditional model for the differences in price levels without the log-transformation:where is the conditional mean, is the conditional standard deviation, while represents the standardized error.

- Simulate a high number N of price trajectories up to time , using the estimated time-series model (2) at step 1. We will compute the 1-day ahead, 30-day ahead, and 365-day ahead probability of death for each coin, that is , respectively.

- The probability of default/death for a crypto-coin i is simply the ratio , where n is the number of times out of N when the simulated price touched or crossed the zero barrier along the simulated trajectory:

3.4. Model Evaluation

3.5. Data

- https://coinmarketcap.com, accessed on 1 June 2022: CoinMarketCap is the main aggregator of crypto-coin market data, and it has been owned by the crypto-exchange Binance since April 2020, see https://crypto.marketswiki.com/index.php?title=CoinMarketCap, accessed on 1 June 2022. It provides open-high-low-close price data, volume data, market capitalization, and a wide range of additional information.

- Google Trends: the Search Volume Index provided by Google Trends shows how many searches have been performed for a keyword or a topic on Google over a specific period and a specific region. See https://support.google.com/trends/?hl=en, (accessed on 1 June 2022) for more details.

- The approach proposed by Feder et al. (2018);

- The approach proposed by Schmitz and Hoffmann (2020);

- The professional rule that defines a coin dead if its value drops below 1 cent, and alive if its value rises above 1 cent.

4. Results

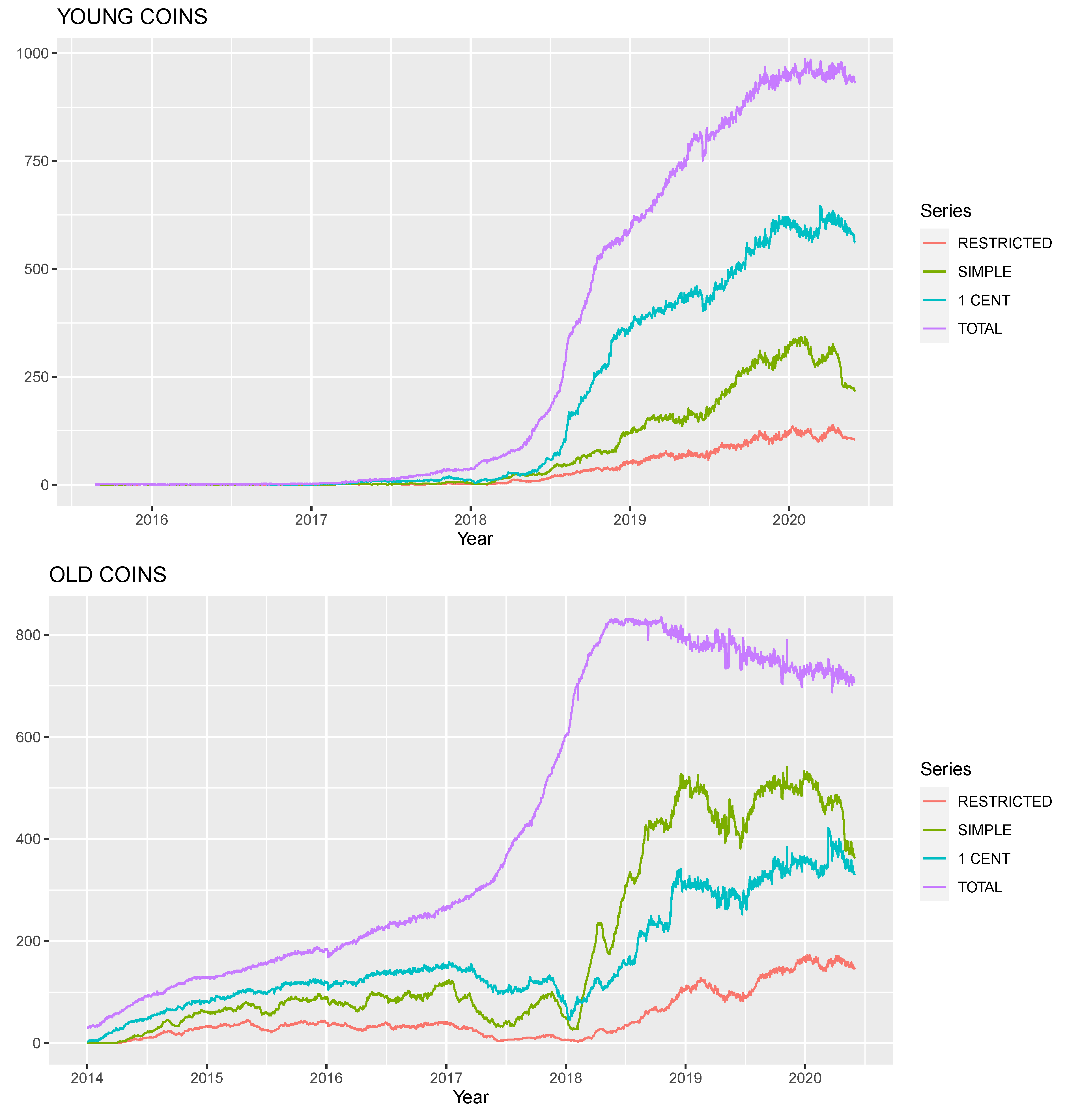

- A total of 1165 young coins for a total of 537,693 observations, whose names are reported in Table A1, Table A2 and Table A3 in Appendix A. We used this set of coins to forecast the 1-day and 30-day ahead probabilities of death.

- A total of 838 old coins for a total of 987,018 observations, whose names are reported in Table A4 and Table A5 in Appendix A. We used this set of coins to forecast the 1-day, 30-day, and 365-day ahead probabilities of death.

5. Robustness Checks

5.1. Forecasting the Probability of Death before and after the 2017 Bubble

5.2. Large Cap and Small Cap: Does It Matter?

6. Conclusions

Funding

Conflicts of Interest

Appendix A. Lists of Young and Old Coins

{kind=link}

| 1 | Bitcoin SV | 101 | Band Protocol | 201 | TROY | 301 | ETERNAL TOKEN |

| 2 | Crypto.com Coin | 102 | PLATINCOIN | 202 | Anchor | 302 | Pirate Chain |

| 3 | Acash Coin | 103 | UNI COIN | 203 | ShareToken | 303 | USDQ |

| 4 | UNUS SED LEO | 104 | Qubitica | 204 | QuarkChain | 304 | Electronic Energy Coin |

| 5 | USD Coin | 105 | MX Token | 205 | Content Value Network | 305 | VNDC |

| 6 | HEX | 106 | Ocean Protocol | 206 | Gemini Dollar | 306 | Egretia |

| 7 | Cosmos | 107 | BitMax Token | 207 | FLETA | 307 | Bitcoin Rhodium |

| 8 | VeChain | 108 | Origin Protocol | 208 | Cred | 308 | IPChain |

| 9 | HedgeTrade | 109 | XeniosCoin | 209 | Metadium | 309 | Digital Asset Guarantee Token |

| 10 | INO COIN | 110 | Project Pai | 210 | Cocos-BCX | 310 | BQT |

| 11 | OKB | 111 | WINk | 211 | MEXC Token | 311 | LINKA |

| 12 | FTX Token | 112 | Function X | 212 | Sport and Leisure | 312 | UGAS |

| 13 | VestChain | 113 | Fetch.ai | 213 | Nectar | 313 | Pundi X NEM |

| 14 | Paxos Standard | 114 | 1irstcoin | 214 | Morpheus.Network | 314 | Yap Stone |

| 15 | MimbleWimbleCoin | 115 | Wirex Token | 215 | Dimension Chain | 315 | Ondori |

| 16 | PlayFuel | 116 | Grin | 216 | Kleros | 316 | Lykke |

| 17 | Hedera Hashgraph | 117 | Aurora | 217 | Hxro | 317 | BOX Token |

| 18 | Algorand | 118 | Karatgold Coin | 218 | StakeCubeCoin | 318 | Sense |

| 19 | Largo Coin | 119 | SynchroBitcoin | 219 | Dusk Network | 319 | Newscrypto |

| 20 | Binance USD | 120 | DAD | 220 | Wixlar | 320 | CUTcoin |

| 21 | Hyperion | 121 | Ecoreal Estate | 221 | Diamond Platform Token | 321 | 1SG |

| 22 | The Midas Touch Gold | 122 | AgaveCoin | 222 | Aencoin | 322 | Global Social Chain |

| 23 | Insight Chain | 123 | Folgory Coin | 223 | Aladdin | 323 | Agrocoin |

| 24 | ThoreCoin | 124 | BOSAGORA | 224 | VITE | 324 | MVL |

| 25 | TAGZ5 | 125 | Tachyon Protocol | 225 | VNX Exchange | 325 | Robotina |

| 26 | Elamachain | 126 | Ultiledger | 226 | AMO Coin | 326 | Nyzo |

| 27 | MINDOL | 127 | Nash Exchange | 227 | XMax | 327 | Akropolis |

| 28 | Dai | 128 | NEXT | 228 | FNB Protocol | 328 | Trade Token X |

| 29 | Baer Chain | 129 | Loki | 229 | Aergo | 329 | VeriDocGlobal |

| 30 | HUSD | 130 | BigONE Token | 230 | CoinEx Token | 330 | Verasity |

| 31 | Flexacoin | 131 | WOM Protocol | 231 | QuickX Protocol | 331 | BitCapitalVendor |

| 32 | Velas | 132 | BitKan | 232 | Moss Coin | 332 | Kryll |

| 33 | Metaverse Dualchain Network Architecture | 133 | CONTRACOIN | 233 | Safe | 333 | EURBASE |

| 34 | ZB Token | 134 | Rocket Pool | 234 | Perlin | 334 | Cryptocean |

| 35 | GlitzKoin | 135 | IDEX | 235 | LiquidApps | 335 | GoCrypto Token |

| 36 | botXcoin | 136 | Egoras | 236 | OTOCASH | 336 | Sentivate |

| 37 | Divi | 137 | LuckySevenToken | 237 | Sentinel Protocol | 337 | Ternio |

| 38 | Terra | 138 | Jewel | 238 | LCX | 338 | CryptoVerificationCoin |

| 39 | DxChain Token | 139 | Celer Network | 239 | Tellor | 339 | VeriBlock |

| 40 | Quant | 140 | Bonorum | 240 | MixMarvel | 340 | VINchain |

| 41 | Seele-N | 141 | Kusama | 241 | CoinMetro Token | 341 | PCHAIN |

| 42 | Counos Coin | 142 | General Attention Currency | 242 | Levolution | 342 | Cardstack |

| 43 | Nervos Network | 143 | Everipedia | 243 | Endor Protocol | 343 | Tokoin |

| 44 | Matic Network | 144 | CryptalDash | 244 | IONChain | 344 | AmonD |

| 45 | Blockstack | 145 | Bitcoin 2 | 245 | HyperDAO | 345 | MargiX |

| 46 | Energi | 146 | Apollo Currency | 246 | #MetaHash | 346 | S4FE |

| 47 | Chiliz | 147 | BORA | 247 | Digix Gold Token | 347 | SnapCoin |

| 48 | QCash | 148 | Cryptoindex.com 100 | 248 | Effect.AI | 348 | EOSDT |

| 49 | BitTorrent | 149 | GoChain | 249 | Darico Ecosystem Coin | 349 | ZVCHAIN |

| 50 | ABBC Coin | 150 | MovieBloc | 250 | GreenPower | 350 | FansTime |

| 51 | Unibright | 151 | TOP | 251 | PlayChip | 351 | EOS Force |

| 52 | NewYork Exchange | 152 | Bit-Z Token | 252 | Cosmo Coin | 352 | ContentBox |

| 53 | Beldex | 153 | IRISnet | 253 | Atomic Wallet Coin | 353 | Maincoin |

| 54 | ExtStock Token | 154 | Machine Xchange Coin | 254 | IQeon | 354 | BaaSid |

| 55 | Celsius | 155 | CWV Chain | 255 | HYCON | 355 | Constant |

| 56 | Bitbook Gambling | 156 | NKN | 256 | LNX Protocol | 356 | USDx stablecoin |

| 57 | SOLVE | 157 | ZEON | 257 | Prometeus | 357 | PumaPay |

| 58 | Sologenic | 158 | Neutrino Dollar | 258 | V-ID | 358 | NIX |

| 59 | Tratin | 159 | WazirX | 259 | suterusu | 359 | JD Coin |

| 60 | RSK Infrastructure Framework | 160 | Nimiq | 260 | T.OS | 360 | FarmaTrust |

| 61 | v.systems | 161 | BHPCoin | 261 | XYO | 361 | Futurepia |

| 62 | PAX Gold | 162 | Fantom | 262 | ChronoCoin | 362 | Themis |

| 63 | BitcoinHD | 163 | Newton | 263 | YOU COIN | 363 | IntelliShare |

| 64 | Elrond | 164 | The Force Protocol | 264 | Telos | 364 | Content Neutrality Network |

| 65 | Bloomzed Token | 165 | COTI | 265 | Contents Protocol | 365 | BitMart Token |

| 66 | THORChain | 166 | ILCoin | 266 | EveryCoin | 366 | Vipstar Coin |

| 67 | Joule | 167 | Ethereum Meta | 267 | Ferrum Network | 367 | Humanscape |

| 68 | Xensor | 168 | TrustVerse | 268 | LINA | 368 | CanonChain |

| 69 | CRYPTOBUCKS | 169 | sUSD | 269 | Origo | 369 | Litex |

| 70 | STEM CELL COIN | 170 | VideoCoin | 270 | Atlas Protocol | 370 | Waves Enterprise |

| 71 | APIX | 171 | Ankr | 271 | VIDY | 371 | Spectre.ai Utility Token |

| 72 | Tap | 172 | Chimpion | 272 | Ampleforth | 372 | Esportbits |

| 73 | Bankera | 173 | Rakon | 273 | GNY | 373 | Beaxy |

| 74 | Breezecoin | 174 | Travala.com | 274 | ChainX | 374 | SINOVATE |

| 75 | FABRK | 175 | ThoreNext | 275 | DAPS Coin | 375 | SIX |

| 76 | Bitball Treasure | 176 | BitForex Token | 276 | Zano | 376 | Phantasma |

| 77 | BHEX Token | 177 | Wrapped Bitcoin | 277 | 0Chain | 377 | BetProtocol |

| 78 | Theta Fuel | 178 | ZBG Token | 278 | GAPS | 378 | pEOS |

| 79 | Gatechain Token | 179 | Orchid | 279 | DigitalBits | 379 | MIR COIN |

| 80 | STASIS EURO | 180 | TTC | 280 | HitChain | 380 | Winding Tree |

| 81 | Kava | 181 | LTO Network | 281 | WeShow Token | 381 | Grid+ |

| 82 | BTU Protocol | 182 | MicroBitcoin | 282 | apM Coin | 382 | BlockStamp |

| 83 | Thunder Token | 183 | Contentos | 283 | Sakura Bloom | 383 | BOLT |

| 84 | Beam | 184 | Lambda | 284 | Clipper Coin | 384 | INLOCK |

| 85 | Swipe | 185 | Constellation | 285 | FOAM | 385 | CEEK VR |

| 86 | Reserve Rights | 186 | Ultra | 286 | qiibee | 386 | Nuggets |

| 87 | Digitex Futures | 187 | FIBOS | 287 | Nestree | 387 | Lition |

| 88 | Orbs | 188 | DREP | 288 | SymVerse | 388 | Rublix |

| 89 | Buggyra Coin Zero | 189 | Invictus Hyperion Fund | 289 | ROOBEE | 389 | Spendcoin |

| 90 | IoTeX | 190 | CONUN | 290 | CryptoFranc | 390 | Bitrue Coin |

| 91 | inSure | 191 | Standard Tokenization Protocol | 291 | DDKoin | 391 | HoryouToken |

| 92 | Davinci Coin | 192 | Mainframe | 292 | Zel | 392 | RealTract |

| 93 | USDK | 193 | Chromia | 293 | Metronome | 393 | BidiPass |

| 94 | Super Zero Protocol | 194 | ARPA Chain | 294 | NPCoin | 394 | PlayCoin [ERC20] |

| 95 | Huobi Pool Token | 195 | REPO | 295 | ProximaX | 395 | MultiVAC |

| 96 | Harmony | 196 | Carry | 296 | NOIA Network | 396 | Artfinity |

| 97 | Poseidon Network | 197 | Valor Token | 297 | Eminer | 397 | EXMO Coin |

| 98 | Handshake | 198 | Zenon | 298 | Observer | 398 | Credit Tag Chain |

| 99 | 12Ships | 199 | Elitium | 299 | Baz Token | 399 | Wowbit |

| 100 | Vitae | 200 | Emirex Token | 300 | KARMA | 400 | RSK Smart Bitcoin |

| 401 | PegNet | 501 | ZeuxCoin | 601 | SPINDLE | 701 | Raise |

| 402 | Trias | 502 | TurtleCoin | 602 | Proton Token | 702 | Arbidex |

| 403 | PIBBLE | 503 | WPP TOKEN | 603 | Swap | 703 | W Green Pay |

| 404 | PLANET | 504 | Linkey | 604 | Olive | 704 | Digital Insurance Token |

| 405 | Snetwork | 505 | Noku | 605 | ImageCoin | 705 | Essentia |

| 406 | Cryptaur | 506 | Coineal Token | 606 | Infinitus Token | 706 | BioCoin |

| 407 | Aryacoin | 507 | Hashgard | 607 | ATMChain | 707 | Zen Protocol |

| 408 | Safe Haven | 508 | Fast Access Blockchain | 608 | WinStars.live | 708 | ZUM TOKEN |

| 409 | Rotharium | 509 | MEET.ONE | 609 | Alpha Token | 709 | Celeum |

| 410 | Traceability Chain | 510 | DACSEE | 610 | Grimm | 710 | MTC Mesh Network |

| 411 | Abyss Token | 511 | Kambria | 611 | TouchCon | 711 | TrueFeedBack |

| 412 | Naka Bodhi Token | 512 | ADAMANT Messenger | 612 | Lobstex | 712 | ZCore |

| 413 | Eterbase Coin | 513 | Merculet | 613 | Bitblocks | 713 | Agrolot |

| 414 | CashBet Coin | 514 | SBank | 614 | Sapien | 714 | Jobchain |

| 415 | Azbit | 515 | QChi | 615 | NOW Token | 715 | Global Awards Token |

| 416 | ZumCoin | 516 | YGGDRASH | 616 | GAMB | 716 | FidentiaX |

| 417 | MenaPay | 517 | Ouroboros | 617 | Xriba | 717 | Nerva |

| 418 | Fatcoin | 518 | Insureum | 618 | Alphacat | 718 | Scorum Coins |

| 419 | Netbox Coin | 519 | Sparkpoint | 619 | BitNewChain | 719 | Patron |

| 420 | VNT Chain | 520 | LHT | 620 | FLIP | 720 | TCASH |

| 421 | Cajutel | 521 | MassGrid | 621 | Nebula AI | 721 | ALL BEST ICO |

| 422 | Vexanium | 522 | QuadrantProtocol | 622 | OVCODE | 722 | wave edu coin |

| 423 | Callisto Network | 523 | KuboCoin | 623 | Plair | 723 | Membrana |

| 424 | Smartlands | 524 | Hashshare | 624 | Auxilium | 724 | PlayGame |

| 425 | TERA | 525 | Ivy | 625 | RED | 725 | Rapidz |

| 426 | GoWithMi | 526 | Banano | 626 | EUNO | 726 | Eristica |

| 427 | Egoras Dollar | 527 | DABANKING | 627 | NeuroChain | 727 | CryptoPing |

| 428 | Tolar | 528 | Ubex | 628 | Rivetz | 728 | x42 Protocol |

| 429 | Vetri | 529 | Bitsdaq | 629 | Coinsuper Ecosystem Network | 729 | Cubiex |

| 430 | WinCash | 530 | VegaWallet Token | 630 | BZEdge | 730 | OSA Token |

| 431 | 1World | 531 | Ecobit | 631 | Bancacy | 731 | EvenCoin |

| 432 | Airbloc | 532 | Liquidity Network | 632 | CrypticCoin | 732 | CREDIT |

| 433 | Pigeoncoin | 533 | Eden | 633 | Evedo | 733 | Coinlancer |

| 434 | OneLedger | 534 | Beetle Coin | 634 | Niobium Coin | 734 | EXMR FDN |

| 435 | DEX | 535 | Merebel | 635 | LocalCoinSwap | 735 | TrueDeck |

| 436 | Pivot Token | 536 | Open Platform | 636 | EBCoin | 736 | AC3 |

| 437 | Kuai Token | 537 | Locus Chain | 637 | Moneytoken | 737 | DAV Coin |

| 438 | Mcashchain | 538 | TEAM (TokenStars) | 638 | CoinUs | 738 | Jarvis+ |

| 439 | Leverj | 539 | Proxeus | 639 | Enecuum | 739 | 3DCoin |

| 440 | Databroker | 540 | BonusCloud | 640 | Noir | 740 | Silent Notary |

| 441 | Unification | 541 | Business Credit Substitute | 641 | BeatzCoin | 741 | IP Exchange |

| 442 | Blue Whale EXchange | 542 | MalwareChain | 642 | Quasarcoin | 742 | Moneynet |

| 443 | Color Platform | 543 | IQ.cash | 643 | Graviocoin | 743 | OWNDATA |

| 444 | Flowchain | 544 | Digital Gold | 644 | Max Property Group | 744 | uPlexa |

| 445 | CoinDeal Token | 545 | Brickblock | 645 | Ethereum Gold | 745 | StarCoin |

| 446 | PlatonCoin | 546 | MARK.SPACE | 646 | TigerCash | 746 | Mithril Ore |

| 447 | Krios | 547 | Conceal | 647 | DPRating | 747 | Ryo Currency |

| 448 | Nasdacoin | 548 | SafeCoin | 648 | Almeela | 748 | StarterCoin |

| 449 | LikeCoin | 549 | Spiking | 649 | Nexxo | 749 | CryptoBonusMiles |

| 450 | Okschain | 550 | COVA | 650 | smARTOFGIVING | 750 | MMOCoin |

| 451 | Bitex Global XBX Coin | 551 | PUBLISH | 651 | On.Live | 751 | FSBT API Token |

| 452 | Colu Local Network | 552 | Sessia | 652 | XcelToken Plus | 752 | PAL Network |

| 453 | Caspian | 553 | DOS Network | 653 | 0xcert | 753 | Shadow Token |

| 454 | BOOM | 554 | NeoWorld Cash | 654 | Block-Logic | 754 | Scanetchain |

| 455 | Raven Protocol | 555 | ESBC | 655 | Actinium | 755 | BlitzPredict |

| 456 | DECOIN | 556 | BitBall | 656 | MineBee | 756 | Truegame |

| 457 | Gleec | 557 | Gold Bits Coin | 657 | eXPerience Chain | 757 | EurocoinToken |

| 458 | Amoveo | 558 | CoTrader | 658 | TurtleNetwork | 758 | Typerium |

| 459 | Teloscoin | 559 | Coinsbit Token | 659 | HashCoin | 759 | Ether-1 |

| 460 | Zipper | 560 | Lisk Machine Learning | 660 | VeriSafe | 760 | TrakInvest |

| 461 | Quanta Utility Token | 561 | USDX | 661 | ZENZO | 761 | GoNetwork |

| 462 | IG Gold | 562 | SureRemit | 662 | Paytomat | 762 | Blockparty (BOXX Token) |

| 463 | ROAD | 563 | SnowGem | 663 | Seal Network | 763 | OptiToken |

| 464 | Midas | 564 | 0xBitcoin | 664 | SnodeCoin | 764 | Bigbom |

| 465 | Cloudbric | 565 | Rate3 | 665 | Bittwatt | 765 | Bethereum |

| 466 | Stronghold Token | 566 | Faceter | 666 | SpectrumCash | 766 | Sharpay |

| 467 | X-CASH | 567 | FREE Coin | 667 | WebDollar | 767 | Amino Network |

| 468 | Iconiq Lab Token | 568 | Qwertycoin | 668 | TV-TWO | 768 | PTON |

| 469 | Blockchain Certified Data Token | 569 | Gene Source Code Chain | 669 | Master Contract Token | 769 | MFCoin |

| 470 | Fountain | 570 | Golos Blockchain | 670 | BetterBetting | 770 | DeVault |

| 471 | MB8 Coin | 571 | ICE ROCK MINING | 671 | BitScreener Token | 771 | GoldFund |

| 472 | Origin Sport | 572 | REAL | 672 | Smartshare | 772 | Leadcoin |

| 473 | Tixl | 573 | PAYCENT | 673 | Vodi X | 773 | Carboneum [C8] Token |

| 474 | ParkinGo | 574 | StableUSD | 674 | Naviaddress | 774 | iDealCash |

| 475 | Ether Zero | 575 | NEXT.coin | 675 | FortKnoxster | 775 | Alt.Estate token |

| 476 | Asian Fintech | 576 | UpToken | 676 | HorusPay | 776 | EnergiToken |

| 477 | Bitcoin Confidential | 577 | SafeInsure | 677 | Ulord | 777 | MorCrypto Coin |

| 478 | DreamTeam Token | 578 | Eureka Coin | 678 | Q DAO Governance token v1.0 | 778 | Hyper Speed Network |

| 479 | nOS | 579 | DEEX | 679 | ODUWA | 779 | eSDChain |

| 480 | HashBX | 580 | ZPER | 680 | RedFOX Labs | 780 | DogeCash |

| 481 | TEMCO | 581 | Bob’s Repair | 681 | XPA | 781 | Daneel |

| 482 | Axe | 582 | Tarush | 682 | Birake | 782 | Gravity |

| 483 | BOMB | 583 | Mallcoin | 683 | savedroid | 783 | Kuende |

| 484 | HyperExchange | 584 | MIB Coin | 684 | TOKPIE | 784 | Kuverit |

| 485 | AIDUS TOKEN | 585 | Skychain | 685 | Halo Platform | 785 | Decentralized Machine Learning |

| 486 | Amon | 586 | Qredit | 686 | DeltaChain | 786 | Winco |

| 487 | Education Ecosystem | 587 | Project WITH | 687 | Mindexcoin | 787 | Monarch |

| 488 | X8X Token | 588 | Zippie | 688 | View | 788 | DOWCOIN |

| 489 | TRONCLASSIC | 589 | FYDcoin | 689 | Swace | 789 | Relex |

| 490 | Footballcoin | 590 | Howdoo | 690 | Ubcoin Market | 790 | Bitcoin CZ |

| 491 | Block-Chain.com | 591 | MidasProtocol | 691 | OLXA | 791 | Omnitude |

| 492 | SafeCapital | 592 | Shivom | 692 | Maximine Coin | 792 | Bee Token |

| 493 | POPCHAIN | 593 | Cashbery Coin | 693 | Webflix Token | 793 | RightMesh |

| 494 | Vision Industry Token | 594 | Lunes | 694 | Trittium | 794 | Catex Token |

| 495 | Opacity | 595 | Bitcoin Free Cash | 695 | Thrive Token | 795 | Bridge Protocol |

| 496 | Titan Coin | 596 | Honest | 696 | Bitcoin Incognito | 796 | Birdchain |

| 497 | Blocktrade Token | 597 | Safex Cash | 697 | Bitfex | 797 | BLOC.MONEY |

| 498 | Semux | 598 | GMB | 698 | FNKOS | 798 | Business Credit Alliance Chain |

| 499 | Uptrennd | 599 | PIXEL | 699 | Rapids | 799 | Alchemint Standards |

| 500 | Veil | 600 | Vezt | 700 | ebakus | 800 | Dynamite |

| 801 | Mainstream For The Underground | 901 | Blockburn | 1001 | BitRent | 1101 | Dash Green |

| 802 | WandX | 902 | LOCIcoin | 1002 | Decentralized Asset Trading Platform | 1102 | Joint Ventures |

| 803 | Blockpass | 903 | OPCoinX | 1003 | ROIyal Coin | 1103 | WXCOINS |

| 804 | ZMINE | 904 | BitCoen | 1004 | ShareX | 1104 | e-Chat |

| 805 | CryptoAds Marketplace | 905 | FUZE Token | 1005 | RefToken | 1105 | iBTC |

| 806 | CROAT | 906 | Commercium | 1006 | SHPING | 1106 | VikkyToken |

| 807 | BoatPilot Token | 907 | Hurify | 1007 | ETHplode | 1107 | CPUchain |

| 808 | Storiqa | 908 | Impleum | 1008 | Bitcoin Classic | 1108 | MiloCoin |

| 809 | Rupiah Token | 909 | Transcodium | 1009 | Bitcoin Adult | 1109 | BunnyToken |

| 810 | Ifoods Chain | 910 | Knekted | 1010 | GenesisX | 1110 | Electrum Dark |

| 811 | AiLink Token | 911 | No BS Crypto | 1011 | Intelligent Trading Foundation | 1111 | Playgroundz |

| 812 | Parachute | 912 | BlockMesh | 1012 | Zenswap Network Token | 1112 | Kora Network Token |

| 813 | Swapcoinz | 913 | PluraCoin | 1013 | Signatum | 1113 | Ragnarok |

| 814 | ONOToken | 914 | Aigang | 1014 | MetaMorph | 1114 | Escroco Emerald |

| 815 | Helium Chain | 915 | Arqma | 1015 | ShowHand | 1115 | Helper Search Token |

| 816 | Fire Lotto | 916 | Regalcoin | 1016 | 4NEW | 1116 | Fivebalance |

| 817 | The Currency Analytics | 917 | Thar Token | 1017 | GoldenPyrex | 1117 | 1X2 COIN |

| 818 | Matrexcoin | 918 | Mobile Crypto Pay Coin | 1018 | RPICoin | 1118 | Crystal Clear |

| 819 | BitClave | 919 | XMCT | 1019 | EOS TRUST | 1119 | Xenoverse |

| 820 | Zennies | 920 | Xuez | 1020 | Gold Poker | 1120 | VectorAI |

| 821 | BBSCoin | 921 | Ethouse | 1021 | Neural Protocol | 1121 | Bitcoinus |

| 822 | Civitas | 922 | Kind Ads Token | 1022 | EtherInc | 1122 | PAXEX |

| 823 | Aston | 923 | CommunityGeneration | 1023 | Sola Token | 1123 | MNPCoin |

| 824 | Bitnation | 924 | Agora | 1024 | SkyHub Coin | 1124 | Apollon |

| 825 | SRCOIN | 925 | nDEX | 1025 | Global Crypto Alliance | 1125 | Project Coin |

| 826 | PYRO Network | 926 | BTC Lite | 1026 | Level Up Coin | 1126 | Crystal Token |

| 827 | Veles | 927 | PUBLYTO Token | 1027 | Havy | 1127 | Veltor |

| 828 | BEAT | 928 | EtherSportz | 1028 | QUINADS | 1128 | Decentralized Crypto Token |

| 829 | Streamit Coin | 929 | Freyrchain | 1029 | EUNOMIA | 1129 | Fintab |

| 830 | Oxycoin | 930 | NetKoin | 1030 | EagleX | 1130 | Flit Token |

| 831 | HeartBout | 931 | REBL | 1031 | Asura Coin | 1131 | MoX |

| 832 | Atonomi | 932 | Vivid Coin | 1032 | Castle | 1132 | LiteCoin Ultra |

| 833 | SwiftCash | 933 | EveriToken | 1033 | Tourist Token | 1133 | Qbic |

| 834 | PDATA | 934 | UChain | 1034 | Gexan | 1134 | PAWS Fund |

| 835 | Artis Turba | 935 | Bitsum | 1035 | UOS Network | 1135 | Bitvolt |

| 836 | Rentberry | 936 | Cheesecoin | 1036 | Authorship | 1136 | Cannation |

| 837 | Plus-Coin | 937 | APR Coin | 1037 | WITChain | 1137 | BROTHER |

| 838 | Bitcoin Token | 938 | Soverain | 1038 | Netrum | 1138 | Silverway |

| 839 | ProxyNode | 939 | HyperQuant | 1039 | Eva Cash | 1139 | Staker |

| 840 | Signals Network | 940 | Bitcoin Zero | 1040 | YoloCash | 1140 | Cointorox |

| 841 | Giant | 941 | Narrative | 1041 | Cyber Movie Chain | 1141 | Secrets of Zurich |

| 842 | RoBET | 942 | HOLD | 1042 | TRAXIA | 1142 | Zoomba |

| 843 | XDNA | 943 | Italo | 1043 | Beacon | 1143 | Orbis Token |

| 844 | TENA | 944 | Gossip Coin | 1044 | KWHCoin | 1144 | Dinero |

| 845 | EtherGem | 945 | BLAST | 1045 | InterCrone | 1145 | Helpico |

| 846 | Vanta Network | 946 | ZeusNetwork | 1046 | ALAX | 1146 | X12 Coin |

| 847 | Linfinity | 947 | Japan Content Token | 1047 | Phonecoin | 1147 | Concoin |

| 848 | StrongHands Masternode | 948 | HYPNOXYS | 1048 | GINcoin | 1148 | LitecoinToken |

| 849 | Voise | 949 | Biotron | 1049 | Spectrum | 1149 | Xchange |

| 850 | Kalkulus | 950 | UNICORN Token | 1050 | Octoin Coin | 1150 | iBank |

| 851 | CryptoSoul | 951 | BUDDY | 1051 | Save Environment Token | 1151 | Benz |

| 852 | WOLLO | 952 | Guider | 1052 | Magic Cube Coin | 1152 | Abulaba |

| 853 | Cashpayz Token | 953 | InternationalCryptoX | 1053 | AceD | 1153 | Dystem |

| 854 | InterValue | 954 | InvestFeed | 1054 | CustomContractNetwork | 1154 | Storeum |

| 855 | WIZBL | 955 | BitStash | 1055 | ConnectJob | 1155 | QYNO |

| 856 | Ethereum Gold Project | 956 | IOTW | 1056 | Stakinglab | 1156 | Coin-999 |

| 857 | Asgard | 957 | Stipend | 1057 | wys Token | 1157 | Posscoin |

| 858 | VULCANO | 958 | CyberMusic | 1058 | Bulleon | 1158 | LRM Coin |

| 859 | Wavesbet | 959 | Herbalist Token | 1059 | GoPower | 1159 | Elliot Coin |

| 860 | HeroNode | 960 | Thingschain | 1060 | SONDER | 1160 | UltraNote Coin |

| 861 | Gentarium | 961 | Arion | 1061 | Provoco Token | 1161 | Newton Coin Project |

| 862 | Webcoin | 962 | WABnetwork | 1062 | Cryptrust | 1162 | HarmonyCoin |

| 863 | SignatureChain | 963 | EZOOW | 1063 | Atheios | 1163 | TerraKRW |

| 864 | Bitcoin Fast | 964 | Arepacoin | 1064 | ArbitrageCT | 1164 | Bitpanda Ecosystem Token |

| 865 | Fiii | 965 | Waletoken | 1065 | INDINODE | 1165 | EmberCoin |

| 866 | CrowdWiz | 966 | Datarius Credit | 1066 | TokenDesk | ||

| 867 | Fox Trading | 967 | TrustNote | 1067 | EnterCoin | ||

| 868 | Verify | 968 | Data Transaction Token | 1068 | P2P Global Network | ||

| 869 | Klimatas | 969 | CYBR Token | 1069 | FidexToken | ||

| 870 | PRASM | 970 | FantasyGold | 1070 | ICOBID | ||

| 871 | MODEL-X-coin | 971 | IGToken | 1071 | Fantasy Sports | ||

| 872 | Menlo One | 972 | Coinchase Token | 1072 | Simmitri | ||

| 873 | Arionum | 973 | Micromines | 1073 | CryptoFlow | ||

| 874 | BlockCAT | 974 | Exosis | 1074 | JavaScript Token | ||

| 875 | Version | 975 | SteepCoin | 1075 | ARAW | ||

| 876 | KAASO | 976 | TOKYO | 1076 | EthereumX | ||

| 877 | CyberFM | 977 | Galilel | 1077 | FUTURAX | ||

| 878 | Ethersocial | 978 | MesChain | 1078 | Nyerium | ||

| 879 | Neutral Dollar | 979 | Bitcoiin | 1079 | Natmin Pure Escrow | ||

| 880 | Paymon | 980 | PRiVCY | 1080 | BitMoney | ||

| 881 | Taklimakan Network | 981 | CFun | 1081 | Quantis Network | ||

| 882 | HashNet BitEco | 982 | Zealium | 1082 | onLEXpa | ||

| 883 | Netko | 983 | Connect Coin | 1083 | Akroma | ||

| 884 | ZINC | 984 | GoHelpFund | 1084 | Carebit | ||

| 885 | Asian Dragon | 985 | xEURO | 1085 | TravelNote | ||

| 886 | IFX24 | 986 | BitStation | 1086 | CCUniverse | ||

| 887 | KanadeCoin | 987 | Italian Lira | 1087 | Alpha Coin | ||

| 888 | Elementeum | 988 | Iungo | 1088 | TrueVett | ||

| 889 | LALA World | 989 | MESG | 1089 | Couchain | ||

| 890 | SiaCashCoin | 990 | Parkgene | 1090 | Absolute | ||

| 891 | CYCLEAN | 991 | BitNautic Token | 1091 | MASTERNET | ||

| 892 | Bitether | 992 | SCRIV NETWORK | 1092 | Luna Coin | ||

| 893 | INMAX | 993 | FundRequest | 1093 | BitGuild PLAT | ||

| 894 | Thore Cash | 994 | JSECOIN | 1094 | XOVBank | ||

| 895 | Guaranteed Ethurance Token Extra | 995 | AirWire | 1095 | Peerguess | ||

| 896 | Niobio Cash | 996 | Kabberry Coin | 1096 | EVOS | ||

| 897 | Social Activity Token | 997 | Digiwage | 1097 | Eurocoin | ||

| 898 | Iridium | 998 | Ether Kingdoms Token | 1098 | ICOCalendar.Today | ||

| 899 | SF Capital | 999 | BitRewards | 1099 | Dragon Option | ||

| 900 | Elysian | 1000 | BitcoiNote | 1100 | Crowdholding |

| 1 | Bitcoin | 106 | DeviantCoin | 211 | Peercoin | 316 | Insights Network |

| 2 | Ethereum | 107 | Storj | 212 | Namecoin | 317 | Sentinel |

| 3 | Tether | 108 | Polymath | 213 | Quark | 318 | Aeron |

| 4 | XRP | 109 | Fusion | 214 | MOAC | 319 | ChatCoin |

| 5 | Bitcoin Cash | 110 | Waltonchain | 215 | Quantum Resistant Ledger | 320 | Red Pulse Phoenix |

| 6 | Litecoin | 111 | PIVX | 216 | Stakenet | 321 | Blockmason Credit Protocol |

| 7 | Binance Coin | 112 | Cortex | 217 | Steem Dollars | 322 | Hydro Protocol |

| 8 | EOS | 113 | Storm | 218 | Kcash | 323 | Tidex Token |

| 9 | Cardano | 114 | FunFair | 219 | United Traders Token | 324 | Litecoin Cash |

| 10 | Tezos | 115 | Enigma | 220 | All Sports | 325 | Refereum |

| 11 | Chainlink | 116 | CasinoCoin | 221 | EDUCare | 326 | Counterparty |

| 12 | Stellar | 117 | Dent | 222 | CargoX | 327 | MintCoin |

| 13 | Monero | 118 | XinFin Network | 223 | Genesis Vision | 328 | MediShares |

| 14 | TRON | 119 | Hellenic Coin | 224 | BnkToTheFuture | 329 | Incent |

| 15 | Huobi Token | 120 | TrueChain | 225 | Neumark | 330 | PolySwarm |

| 16 | Ethereum Classic | 121 | Loom Network | 226 | SIRIN LABS Token | 331 | Nucleus Vision |

| 17 | Neo | 122 | Metal | 227 | Tokenomy | 332 | Blackmoon |

| 18 | Dash | 123 | Acute Angle Cloud | 228 | TE-FOOD | 333 | NAGA |

| 19 | IOTA | 124 | Civic | 229 | ALQO | 334 | Lamden |

| 20 | Maker | 125 | Syscoin | 230 | PressOne | 335 | Global Cryptocurrency |

| 21 | Zcash | 126 | Aidos Kuneen | 231 | Mithril | 336 | Lympo |

| 22 | NEM | 127 | Dynamic Trading Rights | 232 | Ambrosus | 337 | Spectrecoin |

| 23 | Ontology | 128 | Populous | 233 | Dero | 338 | Penta |

| 24 | Basic Attention Token | 129 | Nebulas | 234 | Everex | 339 | Emercoin |

| 25 | Dogecoin | 130 | Ignis | 235 | SALT | 340 | Feathercoin |

| 26 | Synthetix Network Token | 131 | OriginTrail | 236 | Lightning Bitcoin | 341 | BOScoin |

| 27 | DigiByte | 132 | CRYPTO20 | 237 | UnlimitedIP | 342 | Lunyr |

| 28 | 0x | 133 | Gas | 238 | Molecular Future | 343 | Switcheo |

| 29 | Kyber Network | 134 | Groestlcoin | 239 | Wings | 344 | ColossusXT |

| 30 | OMG Network | 135 | SingularityNET | 240 | Pillar | 345 | NaPoleonX |

| 31 | Zilliqa | 136 | Uquid Coin | 241 | Ruff | 346 | BitGreen |

| 32 | THETA | 137 | Tierion | 242 | WePower | 347 | Blockport |

| 33 | BitBay | 138 | Vertcoin | 243 | U Network | 348 | DeepBrain Chain |

| 34 | Augur | 139 | Obyte | 244 | Revain | 349 | LinkEye |

| 35 | Decred | 140 | Melon | 245 | High Performance Blockchain | 350 | BitTube |

| 36 | ICON | 141 | Factom | 246 | INT Chain | 351 | Hydro |

| 37 | Aave | 142 | Dragon Coins | 247 | Ergo | 352 | Boolberry |

| 38 | Qtum | 143 | Cindicator | 248 | Wagerr | 353 | Mobius |

| 39 | Nano | 144 | Request | 249 | Metrix Coin | 354 | Skrumble Network |

| 40 | Siacoin | 145 | Envion | 250 | YOYOW | 355 | Odyssey |

| 41 | Lisk | 146 | Nexus | 251 | Blox | 356 | Myriad |

| 42 | Bitcoin Gold | 147 | Telcoin | 252 | SmartMesh | 357 | PotCoin |

| 43 | Enjin Coin | 148 | Voyager Token | 253 | Gulden | 358 | FintruX Network |

| 44 | Ravencoin | 149 | Utrust | 254 | ECC | 359 | Cube |

| 45 | TrueUSD | 150 | LBRY Credits | 255 | HTMLCOIN | 360 | Apex |

| 46 | Verge | 151 | Einsteinium | 256 | BABB | 361 | carVertical |

| 47 | Waves | 152 | Unobtanium | 257 | Viacoin | 362 | Paypex |

| 48 | MonaCoin | 153 | Quantstamp | 258 | Dock | 363 | YEE |

| 49 | Bitcoin Diamond | 154 | QASH | 259 | district0x | 364 | CanYaCoin |

| 50 | Advanced Internet Blocks | 155 | Tael | 260 | TokenClub | 365 | BlackCoin |

| 51 | Ren | 156 | Bread | 261 | AppCoins | 366 | Radium |

| 52 | Nexo | 157 | Nxt | 262 | Polybius | 367 | Loopring [NEO] |

| 53 | Loopring | 158 | Raiden Network Token | 263 | Ubiq | 368 | OKCash |

| 54 | Holo | 159 | Arcblock | 264 | doc.com Token | 369 | Cryptopay |

| 55 | SwissBorg | 160 | B2BX | 265 | Peculium | 370 | GridCoin |

| 56 | Cryptonex | 161 | Spectre.ai Dividend Token | 266 | SmartCash | 371 | Scry.info |

| 57 | IOST | 162 | Electra | 267 | OneRoot Network | 372 | Pluton |

| 58 | Status | 163 | MediBloc | 268 | GameCredits | 373 | AI Doctor |

| 59 | Komodo | 164 | NavCoin | 269 | Dentacoin | 374 | Crown |

| 60 | Mixin | 165 | PeepCoin | 270 | LockTrip | 375 | TokenPay |

| 61 | Steem | 166 | Haven Protocol | 271 | FLO | 376 | Change |

| 62 | MCO | 167 | AdEx | 272 | GET Protocol | 377 | bitUSD |

| 63 | Bytom | 168 | Asch | 273 | SwftCoin | 378 | Bloom |

| 64 | KuCoin Shares | 169 | RChain | 274 | bitCNY | 379 | Ixcoin |

| 65 | Centrality | 170 | Burst | 275 | SyncFab | 380 | Sumokoin |

| 66 | Horizen | 171 | Aeon | 276 | Universa | 381 | Unikoin Gold |

| 67 | WAX | 172 | Safex Token | 277 | Cashaa | 382 | Curecoin |

| 68 | BitShares | 173 | CyberMiles | 278 | Genaro Network | 383 | DAOBet |

| 69 | Numeraire | 174 | Time New Bank | 279 | DAOstack | 384 | WeOwn |

| 70 | Electroneum | 175 | ShipChain | 280 | Bitcoin Atom | 385 | Chrono.tech |

| 71 | Decentraland | 176 | Bibox Token | 281 | POA | 386 | THEKEY |

| 72 | Bancor | 177 | DMarket | 282 | Matrix AI Network | 387 | Mysterium |

| 73 | aelf | 178 | IoT Chain | 283 | QLC Chain | 388 | Stealth |

| 74 | Golem | 179 | Neblio | 284 | BLOCKv | 389 | Restart Energy MWAT |

| 75 | Ardor | 180 | SaluS | 285 | SONM | 390 | AMLT |

| 76 | Stratis | 181 | Moeda Loyalty Points | 286 | Etherparty | 391 | VeriCoin |

| 77 | HyperCash | 182 | Skycoin | 287 | Jibrel Network | 392 | ZClassic |

| 78 | iExec RLC | 183 | Santiment Network Token | 288 | Auctus | 393 | Denarius |

| 79 | MaidSafeCoin | 184 | DigixDAO | 289 | ZrCoin | 394 | Primas |

| 80 | ERC20 | 185 | FirstBlood | 290 | Covesting | 395 | Bean Cash |

| 81 | Aion | 186 | Kin | 291 | Agrello | 396 | Banca |

| 82 | Aeternity | 187 | LATOKEN | 292 | OAX | 397 | DAEX |

| 83 | Zcoin | 188 | Bezant | 293 | Presearch | 398 | CoinPoker |

| 84 | WhiteCoin | 189 | Veritaseum | 294 | Hi Mutual Society | 399 | PayBX |

| 85 | CyberVein | 190 | Metaverse ETP | 295 | Morpheus Labs | 400 | Peerplays |

| 86 | Bytecoin | 191 | Propy | 296 | Etheroll | 401 | I/O Coin |

| 87 | Power Ledger | 192 | Gifto | 297 | VIBE | 402 | Bismuth |

| 88 | WaykiChain | 193 | AirSwap | 298 | Measurable Data Token | 403 | e-Gulden |

| 89 | Aragon | 194 | Mooncoin | 299 | Selfkey | 404 | Remme |

| 90 | NULS | 195 | Bluzelle | 300 | DigitalNote | 405 | Diamond |

| 91 | Streamr | 196 | Blocknet | 301 | Hiveterminal Token | 406 | SpaceChain |

| 92 | ReddCoin | 197 | Achain | 302 | SunContract | 407 | ATC Coin |

| 93 | Ripio Credit Network | 198 | ODEM | 303 | TrueFlip | 408 | indaHash |

| 94 | Crypterium | 199 | OST | 304 | Edge | 409 | Clams |

| 95 | Dragonchain | 200 | Polis | 305 | Viberate | 410 | ATLANT |

| 96 | GXChain | 201 | SingularDTV | 306 | Everus | 411 | Rise |

| 97 | Ark | 202 | Monolith | 307 | Bitcore | 412 | Pascal |

| 98 | Pundi X | 203 | Credits | 308 | Xaurum | 413 | Rubycoin |

| 99 | Insolar | 204 | EDC Blockchain | 309 | Monetha | 414 | COS |

| 100 | PRIZM | 205 | Po.et | 310 | Phore | 415 | GoldMint |

| 101 | Gnosis | 206 | TenX | 311 | QunQun | 416 | Substratum |

| 102 | TomoChain | 207 | Game.com | 312 | DATA | 417 | Swarm |

| 103 | Eidoo | 208 | TaaS | 313 | Tripio | 418 | NewYorkCoin |

| 104 | Elastos | 209 | Particl | 314 | Credo | 419 | Adshares |

| 105 | Wanchain | 210 | Monero Classic | 315 | Flash | 420 | Flixxo |

| 421 | Bottos | 526 | DECENT | 631 | Dether | 736 | BERNcash |

| 422 | CommerceBlock | 527 | ION | 632 | Primalbase Token | 737 | VoteCoin |

| 423 | Dynamic | 528 | Waves Community Token | 633 | PiplCoin | 738 | Aricoin |

| 424 | AquariusCoin | 529 | Playkey | 634 | Bitcloud | 739 | GuccioneCoin |

| 425 | IHT Real Estate Protocol | 530 | Sentient Coin | 635 | Ties.DB | 740 | Zurcoin |

| 426 | Dinastycoin | 531 | Karbo | 636 | bitEUR | 741 | PureVidz |

| 427 | CPChain | 532 | Internet of People | 637 | Indorse Token | 742 | Adzcoin |

| 428 | Nexty | 533 | Neutron | 638 | Energo | 743 | ELTCOIN |

| 429 | Aventus | 534 | Minereum | 639 | RealChain | 744 | SmartCoin |

| 430 | Sharder | 535 | Ink Protocol | 640 | Tokenbox | 745 | Bela |

| 431 | HalalChain | 536 | CryCash | 641 | Chronologic | 746 | EDRCoin |

| 432 | BANKEX | 537 | BUZZCoin | 642 | Limitless VIP | 747 | Blocklancer |

| 433 | 42-coin | 538 | SIBCoin | 643 | Maxcoin | 748 | MarteXcoin |

| 434 | Pandacoin | 539 | DecentBet | 644 | Emerald Crypto | 749 | SparksPay |

| 435 | Omni | 540 | TraDove B2BCoin | 645 | Lampix | 750 | PayCoin |

| 436 | NuBits | 541 | AllSafe | 646 | PutinCoin | 751 | ClearPoll |

| 437 | Primecoin | 542 | XEL | 647 | AdHive | 752 | Ellaism |

| 438 | Ormeus Coin | 543 | AudioCoin | 648 | Pesetacoin | 753 | Digital Money Bits |

| 439 | MonetaryUnit | 544 | Pirl | 649 | Dropil | 754 | Acoin |

| 440 | Hush | 545 | Trinity Network Credit | 650 | Emphy | 755 | Theresa May Coin |

| 441 | Medicalchain | 546 | ProChain | 651 | KZ Cash | 756 | BTCtalkcoin |

| 442 | Hubii Network | 547 | Sentinel Chain | 652 | BitBar | 757 | GeyserCoin |

| 443 | Datum | 548 | Zeepin | 653 | BitSend | 758 | Nitro |

| 444 | Humaniq | 549 | GlobalBoost-Y | 654 | LEOcoin | 759 | Citadel |

| 445 | Lendingblock | 550 | The ChampCoin | 655 | Bonpay | 760 | YENTEN |

| 446 | KickToken | 551 | Zap | 656 | ACE (TokenStars) | 761 | STRAKS |

| 447 | PAC Global | 552 | Trollcoin | 657 | Gems | 762 | MojoCoin |

| 448 | EXRNchain | 553 | Datawallet | 658 | Bata | 763 | Blakecoin |

| 449 | PetroDollar | 554 | Espers | 659 | Rupee | 764 | Coin2.1 |

| 450 | Nework | 555 | BitDegree | 660 | Adelphoi | 765 | Elementrem |

| 451 | NativeCoin | 556 | Qbao | 661 | PWR Coin | 766 | MedicCoin |

| 452 | Zero | 557 | OBITS | 662 | Carboncoin | 767 | ICO OpenLedger |

| 453 | SoMee.Social | 558 | Patientory | 663 | Unify | 768 | GoldBlocks |

| 454 | ToaCoin | 559 | Freicoin | 664 | InsaneCoin | 769 | FuzzBalls |

| 455 | SolarCoin | 560 | DATx | 665 | Bitradio | 770 | Titcoin |

| 456 | GeoCoin | 561 | adToken | 666 | Energycoin | 771 | Jupiter |

| 457 | Upfiring | 562 | Starbase | 667 | Profile Utility Token | 772 | Dreamcoin |

| 458 | Cappasity | 563 | HEROcoin | 668 | Digitalcoin | 773 | NevaCoin |

| 459 | DeepOnion | 564 | HOQU | 669 | TrumpCoin | 774 | Ratecoin |

| 460 | Edgeless | 565 | LIFE | 670 | Aditus | 775 | ParkByte |

| 461 | eosDAC | 566 | Electrify.Asia | 671 | Bitcoin Interest | 776 | Dalecoin |

| 462 | Snovian.Space | 567 | HempCoin | 672 | Cobinhood | 777 | Spectiv |

| 463 | NoLimitCoin | 568 | ExclusiveCoin | 673 | Litecoin Plus | 778 | Datacoin |

| 464 | Matryx | 569 | Zilla | 674 | Elcoin | 779 | BoostCoin |

| 465 | CloakCoin | 570 | Memetic / PepeCoin | 675 | Photon | 780 | Open Trading Network |

| 466 | Terracoin | 571 | Solaris | 676 | Lethean | 781 | Desire |

| 467 | SpankChain | 572 | VouchForMe | 677 | Zetacoin | 782 | X-Coin |

| 468 | Bitswift | 573 | Friendz | 678 | Synergy | 783 | PostCoin |

| 469 | Experty | 574 | Zeitcoin | 679 | Kobocoin | 784 | Galactrum |

| 470 | iEthereum | 575 | Swarm City | 680 | MicroMoney | 785 | bitJob |

| 471 | PayPie | 576 | LanaCoin | 681 | Global Currency Reserve | 786 | Ccore |

| 472 | SHIELD | 577 | Sociall | 682 | Eroscoin | 787 | Quebecoin |

| 473 | UNIVERSAL CASH | 578 | EverGreenCoin | 683 | Capricoin | 788 | BriaCoin |

| 474 | CannabisCoin | 579 | IDEX Membership | 684 | MktCoin | 789 | SpreadCoin |

| 475 | NuShares | 580 | Zeusshield | 685 | PoSW Coin | 790 | Centurion |

| 476 | DomRaider | 581 | DopeCoin | 686 | Cryptonite | 791 | Zayedcoin |

| 477 | Neurotoken | 582 | FujiCoin | 687 | Opal | 792 | Independent Money System |

| 478 | STK | 583 | EncryptoTel [WAVES] | 688 | SounDAC | 793 | ARbit |

| 479 | Delphy | 584 | KekCoin | 689 | Universe | 794 | Litecred |

| 480 | Sphere | 585 | IXT | 690 | CDX Network | 795 | Nekonium |

| 481 | MobileGo | 586 | CoinFi | 691 | Paragon | 796 | Rupaya |

| 482 | Pinkcoin | 587 | VeriumReserve | 692 | Bitstar | 797 | Bitcoin 21 |

| 483 | Zebi Token | 588 | Motocoin | 693 | ATBCoin | 798 | Californium |

| 484 | Infinitecoin | 589 | Ignition | 694 | Kurrent | 799 | Comet |

| 485 | LUXCoin | 590 | FedoraCoin | 695 | Deutsche eMark | 800 | Phantomx |

| 486 | Manna | 591 | FlypMe | 696 | Suretly | 801 | AmsterdamCoin |

| 487 | BitCrystals | 592 | JET8 | 697 | bitBTC | 802 | High Voltage |

| 488 | HEAT | 593 | CaixaPay | 698 | Rimbit | 803 | MustangCoin |

| 489 | Internxt | 594 | Ultimate Secure Cash | 699 | GCN Coin | 804 | Dollar International |

| 490 | Pylon Network | 595 | Pakcoin | 700 | BlueCoin | 805 | Dollarcoin |

| 491 | Dovu | 596 | Devery | 701 | FirstCoin | 806 | CrevaCoin |

| 492 | BitcoinZ | 597 | Bitzeny | 702 | Evil Coin | 807 | BowsCoin |

| 493 | StrongHands | 598 | Swing | 703 | ParallelCoin | 808 | Coinonat |

| 494 | Dimecoin | 599 | MinexCoin | 704 | BitWhite | 809 | DNotes |

| 495 | WeTrust | 600 | Masari | 705 | Autonio | 810 | LiteBitcoin |

| 496 | Bitcoin Plus | 601 | EventChain | 706 | TransferCoin | 811 | BitCoal |

| 497 | adbank | 602 | Bounty0x | 707 | TajCoin | 812 | SONO |

| 498 | EchoLink | 603 | NANJCOIN | 708 | 2GIVE | 813 | SpeedCash |

| 499 | ATN | 604 | DIMCOIN | 709 | Golos | 814 | PlatinumBAR |

| 500 | Megacoin | 605 | Monkey Project | 710 | GlobalToken | 815 | Experience Points |

| 501 | Auroracoin | 606 | Veros | 711 | TagCoin | 816 | HollyWoodCoin |

| 502 | EncrypGen | 607 | Maverick Chain | 712 | SkinCoin | 817 | Prime-XI |

| 503 | Phoenixcoin | 608 | GoByte | 713 | Anoncoin | 818 | Cabbage |

| 504 | FuzeX | 609 | HelloGold | 714 | DraftCoin | 819 | BenjiRolls |

| 505 | Ink | 610 | GravityCoin | 715 | Cryptojacks | 820 | PosEx |

| 506 | PHI Token | 611 | Goldcoin | 716 | vSlice | 821 | Wild Beast Block |

| 507 | Bitcoin Private | 612 | Jetcoin | 717 | Bitcoin Red | 822 | Iconic |

| 508 | AICHAIN | 613 | MyWish | 718 | Advanced Technology Coin | 823 | PLNcoin |

| 509 | Scala | 614 | Crowd Machine | 719 | SuperCoin | 824 | SocialCoin |

| 510 | Stox | 615 | Startcoin | 720 | XGOX | 825 | SportyCo |

| 511 | Maecenas | 616 | LiteDoge | 721 | Blocktix | 826 | Project-X |

| 512 | Bulwark | 617 | Bezop | 722 | Worldcore | 827 | PonziCoin |

| 513 | SmileyCoin | 618 | InvestDigital | 723 | More Coin | 828 | Save and Gain |

| 514 | OracleChain | 619 | Bolivarcoin | 724 | iTicoin | 829 | Argus |

| 515 | AidCoin | 620 | Graft | 725 | Garlicoin | 830 | SongCoin |

| 516 | eBitcoin | 621 | MyBit | 726 | InflationCoin | 831 | CoinMeet |

| 517 | BiblePay | 622 | Equal | 727 | SophiaTX | 832 | Agoras Tokens |

| 518 | Shift | 623 | Privatix | 728 | SelfSell | 833 | Sexcoin |

| 519 | Orbitcoin | 624 | Matchpool | 729 | ChessCoin | 834 | RabbitCoin |

| 520 | Novacoin | 625 | eBoost | 730 | Eternity | 835 | Quotient |

| 521 | Expanse | 626 | Utrum | 731 | Moin | 836 | Bubble |

| 522 | CVCoin | 627 | imbrex | 732 | PopularCoin | 837 | Axiom |

| 523 | Blue Protocol | 628 | Yocoin | 733 | Payfair | 838 | Francs |

| 524 | TrezarCoin | 629 | BoutsPro | 734 | Rubies | ||

| 525 | HiCoin | 630 | CryptoCarbon | 735 | bitGold |

| 1 | At the end of December 2021, almost 15,000 crypto-assets were listed on Coinmarketcap.com, accessed on 1 June 2022. CoinMarketCap is the main aggregator of cryptocurrency market data, and it has been owned by the crypto-exchange Binance since April 2020; see https://crypto.marketswiki.com/index.php?title=CoinMarketCap, accessed on 1 June 2022 for more details. |

| 2 | Lansky (2018), p. 19, formally defined a crypto-currency as a system that satisfies these six conditions: “(1) The system does not require a central authority, its state is maintained through distributed consensus. (2) The system keeps an overview of cryptocurrency units and their ownership. (3) The system defines whether new cryptocurrency units can be created. If new cryptocurrency units can be created, the system defines the circumstances of their origin and how to determine the ownership of these new units. (4) Ownership of cryptocurrency units can be proved exclusively cryptographically. (5) The system allows transactions to be performed in which ownership of the cryptographic units is changed. A transaction statement can only be issued by an entity proving the current ownership of these units. (6) If two different instructions for changing the ownership of the same cryptographic units are simultaneously entered, the system performs at most one of them.” |

| 3 | https://www.investopedia.com/news/crypto-carnage-over-800-cryptocurrencies-are-dead/, accessed on 1 June 2022; https://www.coinopsy.com/dead-coins/, accessed on 1 June 2022. |

| 4 | We will use the terms “probability of death” and “probability of default” interchangeably. |

| 5 | https://www.investopedia.com/news/crypto-carnage-over-800-cryptocurrencies-are-dead/, accessed on 1 June 2022. |

| 6 | https://www.coinopsy.com/dead-coins/, accessed on 1 June 2022. |

| 7 | Note that Schmitz and Hoffmann (2020) presented this method as the Feder et al. (2018) approach when, in reality, the latter involves many more restrictions. The methodology used by Schmitz and Hoffmann (2020) in their empirical analysis is even more simplified, and it assumes that a coin is (temporarily) inactive if data gaps are present in its time series. |

| 8 | See Section 5 in Giudici and Figini (2009) for a review. |

| 9 | In-sample analysis is also known as training, while the out-of-sample analysis can be named as validation. |

| 10 | Note that this result is already known in the traditional financial literature because “the ratio of default and (normally distributed) market risk losses is proportional to the square-root of the holding period. Since the ratio goes to 0 as the holding period goes to 0, over short horizons market risk is relatively more important, while over longer horizons losses due to default become more important”(Basel Committee on Banking Supervision (2009), pp. 16–17). |

| 11 | Fantazzini and Zimin (2020) proposed a multivariate approach to compute the ZPP of 42 coins. Given the very large dataset at our disposal, such an approach is not feasible in our case due to the curse of dimensionality. An extension of this methodology to large portfolios is left as an avenue for further research. |

| 12 | For ease of reference, we will refer to the Feder et al. (2018) approach as “restrictive”, to the simplified Feder et al. (2018) approach as “simple”, while to the professional rule as “1 cent”. |

| 13 | The experience of the author (both in academia and in the professional field) with credit-risk management for SMEs and with potentially noisy and fraudulent data suggested a minimum dataset of 50.000–100.000 data to have robust estimates. |

| 14 | We remark that the datasets used for the estimation of credit scoring, ML models and time series-based models were different, so there were dates for which forecasts from all models were not available. This situation had no impact on individual metrics such as the AUC, but it affected the computation of the model confidence set using the Brier score: in the latter case, we used only dates where forecasts from all models were available. |

| 15 | The author wants to thank three anonymous professionals working in the crypto-industry for pointing his work in this direction. |

| 16 | The development of ZPP models allowing for direct forecasts is left as an avenue for further research. |

| 17 | We also tried to add these regressors in the mean equation of the simple random walk model, but the results did not change qualitatively (results not reported). This was not a surprise because it is the variance modelling that is the key ingredient when computing the ZPP, see Fantazzini and Zimin (2020)—Section 4.3—and references therein for more details. |

| 18 |

References

- Aas, Kjersti, and Ingrid Hobæk Haff. 2006. The generalized hyperbolic skew student’st-distribution. Journal of Financial Econometrics 4: 275–309. [Google Scholar] [CrossRef] [Green Version]

- Antonopoulos, Andreas. 2014. Mastering Bitcoin: Unlocking Digital Cryptocurrencies. Sebastopol: O’Reilly Media, Inc. [Google Scholar]

- Ardia, David, Keven Bluteau, and Maxime Rüede. 2019. Regime changes in Bitcoin GARCH volatility dynamics. Finance Research Letters 29: 266–71. [Google Scholar] [CrossRef]

- Baesens, Bart, and Tony Van Gestel. 2009. Credit Risk Management: Basic Concepts. Oxford: Oxford University Press. [Google Scholar]

- Baig, Ahmed S., Omair Haroon, and Nasim Sabah. 2020. Price clustering after the introduction of bitcoin futures. Applied Finance Letters 9: 36–42. [Google Scholar] [CrossRef]

- Barboza, Flavio, Herbert Kimura, and Edward Altman. 2017. Machine learning models and bankruptcy prediction. Expert Systems with Applications 83: 405–17. [Google Scholar] [CrossRef]

- Basel Committee on Banking Supervision. 2009. Findings on the Interaction of Market and Credit Risk; Technical Report, BCBS Working Papers, n. 16.. Basel, Switzerland. Available online: https://www.bis.org/publ/bcbs_wp16.pdf (accessed on 1 June 2022).

- Bianchi, Carluccio, Maria Elena De Giuli, Dean Fantazzini, and Mario Maggi. 2011. Small sample properties of copula-GARCH modelling: A Monte Carlo study. Applied Financial Economics 21: 1587–97. [Google Scholar] [CrossRef] [Green Version]

- Breiman, Leo. 2001. Random forests. Machine Learning 45: 5–32. [Google Scholar] [CrossRef] [Green Version]

- Brier, Glenn. 1950. Verification of forecasts expressed in terms of probability. Monthly Weather Review 78: 1–3. [Google Scholar] [CrossRef]

- Brummer, Chris. 2019. Cryptoassets: Legal, Regulatory, and Monetary Perspectives. Oxford: Oxford University Press. [Google Scholar]

- Burniske, Chris, and Jack Tatar. 2018. Cryptoassets: The Innovative Investor’s Guide to Bitcoin and Beyond. New York: McGraw-Hill. [Google Scholar]

- Corbet, Shaen, Brian Lucey, and Larisa Yarovaya. 2018. Datestamping the bitcoin and ethereum bubbles. Finance Research Letters 26: 81–88. [Google Scholar] [CrossRef] [Green Version]

- Dalla Valle, Luciana, Maria Elena De Giuli, Claudia Tarantola, and Claudio Manelli. 2016. Default probability estimation via pair copula constructions. European Journal of Operational Research 249: 298–311. [Google Scholar] [CrossRef] [Green Version]

- De Prado, Marcos Lopez. 2018. Advances in Financial Machine Learning. Hoboken: John Wiley & Sons. [Google Scholar]

- Dixon, Matthew F., Igor Halperin, and Paul Bilokon. 2020. Machine Learning in Finance. New York: Springer. [Google Scholar]

- Everitt, Brian. 2011. Cluster Analysis. Chichester: Wiley. [Google Scholar]

- Fantazzini, Dean. 2009. The effects of misspecified marginals and copulas on computing the Value-at-Risk: A Monte Carlo study. Computational Statistics & Data Analysis 53: 2168–88. [Google Scholar]

- Fantazzini, Dean. 2019. Quantitative Finance with R and Cryptocurrencies. Seattle: Amazon KDP, ISBN-13: 978-1090685315. [Google Scholar]

- Fantazzini, Dean, and Raffaella Calabrese. 2021. Crypto Exchanges and Credit Risk: Modeling and Forecasting the Probability of Closure. Journal of Risk and Financial Management 14: 516. [Google Scholar] [CrossRef]

- Fantazzini, Dean, Maria Elena De Giuli, and Mario Alessandro Maggi. 2008. A new approach for firm value and default probability estimation beyond merton models. Computational Economics 31: 161–80. [Google Scholar]

- Fantazzini, Dean, and Silvia Figini. 2008. Default forecasting for small-medium enterprises: Does heterogeneity matter? International Journal of Risk Assessment and Management 11: 138–63. [Google Scholar] [CrossRef]

- Fantazzini, Dean, and Silvia Figini. 2009. Random survival forests models for sme credit risk measurement. Methodology and Computing in Applied Probability 11: 29–45. [Google Scholar] [CrossRef]

- Fantazzini, Dean, and Nikita Kolodin. 2020. Does the hashrate affect the bitcoin price? Journal of Risk and Financial Management 13: 263. [Google Scholar] [CrossRef]

- Fantazzini, Dean, and Mario Maggi. 2015. Proposed coal power plants and coal-to-liquids plants in the us: Which ones survive and why? Energy Strategy Reviews 7: 9–17. [Google Scholar] [CrossRef]

- Fantazzini, Dean, and Stephan Zimin. 2020. A multivariate approach for the simultaneous modelling of market risk and credit risk for cryptocurrencies. Journal of Industrial and Business Economics 47: 19–69. [Google Scholar] [CrossRef] [Green Version]

- Feder, Amir, Neil Gandal, James Hamrick, Tyler Moore, and Marie Vasek. 2018. The rise and fall of cryptocurrencies. Paper presented at 17th Workshop on the Economics of Information Security (WEIS), Innsbruck, Austria, June 18–19. [Google Scholar]

- Fiorentini, Gabriele, Giorgio Calzolari, and Lorenzo Panattoni. 1996. Analytic derivatives and the computation of GARCH estimates. Journal of Applied Econometrics 11: 399–417. [Google Scholar] [CrossRef]

- Fry, John. 2018. Booms, busts and heavy-tails: The story of bitcoin and cryptocurrency markets? Economics Letters 171: 225–29. [Google Scholar] [CrossRef] [Green Version]

- Fuertes, Ana-Maria, and Elena Kalotychou. 2006. Early warning systems for sovereign debt crises: The role of heterogeneity. Computational Statistics and Data Analysis 51: 1420–41. [Google Scholar] [CrossRef]

- Gandal, Neil, James Hamrick, Tyler Moore, and Tali Oberman. 2018. Price manipulation in the Bitcoin ecosystem. Journal of Monetary Economics 95: 86–96. [Google Scholar] [CrossRef]

- Gandal, Neil, James Hamrick, Tyler Moore, and Marie Vasek. 2021. The rise and fall of cryptocurrency coins and tokens. Decisions in Economics and Finance 44: 981–1014. [Google Scholar] [CrossRef]

- Gerlach, Jan-Christian, Guilherme Demos, and Didier Sornette. 2019. Dissection of bitcoin’s multiscale bubble history from january 2012 to february 2018. Royal Society Open Science 6: 180643. [Google Scholar] [CrossRef] [Green Version]

- Giudici, Paolo, and Silvia Figini. 2009. Applied Data Mining for Business and Industry. Chichester: Wiley Online Library. [Google Scholar]

- Griffin, John, and Amin Shams. 2020. Is Bitcoin really untethered? The Journal of Finance 75: 1913–64. [Google Scholar] [CrossRef]

- Grobys, Klaus, and Niranjan Sapkota. 2020. Predicting cryptocurrency defaults. Applied Economics 52: 5060–76. [Google Scholar] [CrossRef]

- Gündüz, Necla, and Ernest Fokoué. 2017. On the predictive properties of binary link functions. Communications Faculty of Sciences University of Ankara Series A1 Mathematics and Statistics 66: 1–18. [Google Scholar]

- Hamrick, James Farhang Rouhi, Arghya Mukherjee, Amir Feder, Neil Gandal, Tyler Moore, and Marie Vasek. 2021. An examination of the cryptocurrency pump-and-dump ecosystem. Information Processing & Management 58: 102506. [Google Scholar]

- Hanley, James, and Barbara McNeil. 1982. The meaning and use of the area under a receiver operating characteristic (ROC) curve. Radiology 143: 29–36. [Google Scholar] [CrossRef] [Green Version]

- Hansen, Peter, Asger Lunde, and James Nason. 2011. The model confidence set. Econometrica 79: 453–97. [Google Scholar] [CrossRef] [Green Version]

- Hartmann, Philipp. 2010. Interaction of market and credit risk. Journal of Banking and Finance 4: 697–702. [Google Scholar] [CrossRef]

- Hastie, Trevor, Robert Tibshirani, and Jerome Friedman. 2009. The Elements of Statistical Learning: Data Mining, Inference, and Prediction. New York: Springer. [Google Scholar]

- Hattori, Takahiro, and Ryo Ishida. 2021. Did the introduction of bitcoin futures crash the bitcoin market at the end of 2017? The North American Journal of Economics and Finance 56: 101322. [Google Scholar] [CrossRef]

- Ho, Tin Kam. 1995. Random decision forests. Paper presented at the 3rd International Conference on Document Analysis and Recognition, Montreal, QC, Canada, August 14–16; pp. 278–82. [Google Scholar]

- Hwang, Soosung, and Pedro Valls Pereira. 2006. Small sample properties of GARCH estimates and persistence. The European Journal of Finance 12: 473–94. [Google Scholar] [CrossRef]

- Hyndman, Rob, and George Athanasopoulos. 2018. Forecasting: Principles and Practice. OTexts: Available online: https://otexts.com/fpp2/ (accessed on 1 June 2022).

- Jalan, Akanksha, Roman Matkovskyy, and Andrew Urquhart. 2021. What effect did the introduction of bitcoin futures have on the bitcoin spot market? The European Journal of Finance 27: 1251–81. [Google Scholar] [CrossRef]

- James, Gareth, Daniela Witten, Trevor Hastie, and Robert Tibshirani. 2013. An Introduction to Statistical Learning. New York: Springer, vol. 112. [Google Scholar]

- Jing, Jiabao, Wenwen Yan, and Xiaomei Deng. 2021. A hybrid model to estimate corporate default probabilities in China based on zero-price probability model and long short-term memory. Applied Economics Letters 28: 413–20. [Google Scholar] [CrossRef]

- Joseph, Ciby. 2013. Advanced Credit Risk Analysis and Management. Chichester: John Wiley & Sons. [Google Scholar]

- Köchling, Gerrit, Janis Müller, and Peter N. Posch. 2019. Does the introduction of futures improve the efficiency of bitcoin? Finance Research Letters 30: 367–70. [Google Scholar] [CrossRef]

- Koenker, Roger, and Jungmo Yoon. 2009. Parametric links for binary choice models: A fisherian-bayesian colloquy. Journal of Econometrics 152: 120–30. [Google Scholar] [CrossRef]

- Krzanowski, Wojtek, and David Hand. 2009. ROC Curves for Continuous Data. Boca Raton: Crc Press. [Google Scholar]

- Lansky, Jan. 2018. Possible state approaches to cryptocurrencies. Journal of Systems Integration 9: 19. [Google Scholar] [CrossRef]

- Li, Lili, Jun Yang, and Xin Zou. 2016. A study of credit risk of Chinese listed companies: ZPP versus KMV. Applied Economics 48: 2697–710. [Google Scholar] [CrossRef]

- Liu, Ruozhou, Shanfeng Wan, Zili Zhang, and Xuejun Zhao. 2020. Is the introduction of futures responsible for the crash of bitcoin? Finance Research Letters 34: 101259. [Google Scholar] [CrossRef]

- Maciel, Leandro. 2021. Cryptocurrencies value-at-risk and expected shortfall: Do regime-switching volatility models improve forecasting? International Journal of Finance & Economics 26: 4840–55. [Google Scholar]

- McCullagh, Peter, and John A. Nelder. 1989. Generalized Linear Model. Boca Raton: Chapman Hall. [Google Scholar]

- Metz, Charles. 1978. Basic principles of ROC analysis. Seminars in Nuclear Medicine 8: 283–98. [Google Scholar] [CrossRef]

- Metz, Charles, and Helen Kronman. 1980. Statistical significance tests for binormal ROC curves. Journal of Mathematical Psychology 22: 218–43. [Google Scholar] [CrossRef]

- Moscatelli, Mirko, Fabio Parlapiano, Simone Narizzano, and Gianluca Viggiano. 2020. Corporate default forecasting with machine learning. Expert Systems with Applications 161: 113567. [Google Scholar] [CrossRef]

- Narayanan, Arvind, Joseph Bonneau, Edward Felten, Andrew Miller, and Steven Goldfeder. 2016. Bitcoin and Cryptocurrency Technologies: A Comprehensive Introduction. Princeton: Princeton University Press. [Google Scholar]

- Provost, Foster, and R Kohavi. 1998. Glossary of terms. Journal of Machine Learning 30: 271–74. [Google Scholar]

- Rodriguez, Arnulfo, and Pedro N Rodriguez. 2006. Understanding and predicting sovereign debt rescheduling: A comparison of the areas under receiver operating characteristic curves. Journal of Forecasting 25: 459–79. [Google Scholar] [CrossRef]

- Romesburg, Charles. 2004. Cluster Analysis for Researchers. North Carolina: Lulu.com. [Google Scholar]

- Sammut, Claude, and Geoffrey Webb. 2011. Encyclopedia of Machine Learning. New York: Springer. [Google Scholar]

- Schar, Fabian, and Aleksander Berentsen. 2020. Bitcoin, Blockchain, and Cryptoassets: A Comprehensive Introduction. Cambridge: MIT Press. [Google Scholar]

- Schmitz, Tim, and Ingo Hoffmann. 2020. Re-evaluating cryptocurrencies’ contribution to portfolio diversification—A portfolio analysis with special focus on german investors. arXiv arXiv:2006.06237v2. [Google Scholar] [CrossRef]

- Sid. 2018. How Peng Coin Will Surge 8–12x These Coming Weeks. Medium, July 8. [Google Scholar]

- Soni, Sandeep. 2021. RIP Cryptocurrencies: Number of ‘Dead’ Coins Up 35% over Last Year; Tally Nears 2000-Mark. Financial Express, April 3. [Google Scholar]

- Su, En-Der, and Shih-Ming Huang. 2010. Comparing firm failure predictions between logit, KMV, and ZPP models: Evidence from Taiwan’s electronics industry. Asia-Pacific Financial Markets 17: 209–39. [Google Scholar] [CrossRef]

- Wei, Wang Chun. 2018. The impact of Tether grants on Bitcoin. Economics Letters 171: 19–22. [Google Scholar] [CrossRef]

- Xiong, Jinwu, Qing Liu, and Lei Zhao. 2020. A new method to verify bitcoin bubbles: Based on the production cost. The North American Journal of Economics and Finance 51: 101095. [Google Scholar] [CrossRef]

| Observed/Predicted | Dead Coins | Alive |

|---|---|---|

| Dead coins | a | b |

| Alive | c | d |

| Young coins | |||||

| Feder et al. (2018) | Simplified Feder et al. (2018) | 1 cent | |||

| N. of dead days | % | N. of dead days | % | N. of dead days | % |

| 53,169 | 9.89 | 128,163 | 23.84 | 310,707 | 57.79 |

| Old coins | |||||

| Feder et al. (2018) | Simplified Feder et al. (2018) | 1 cent | |||

| N. of dead days | % | N. of dead days | % | N. of dead days | % |

| 114,790 | 11.63 | 428,288 | 43.39 | 379,226 | 38.42 |

| Coins | Time | Alive (dep. Variable) | Regressor 1 | … | Regressor n |

|---|---|---|---|---|---|

| 0 | … | … | … | ||

| 0 | … | … | … | ||

| COIN 1 | 1 | … | … | … | |

| 0 | |||||

| 0 | … | … | … | ||

| 0 | … | … | … | ||

| 0 | … | … | … | ||

| COIN 2 | 0 | … | … | … | |

| 0 | |||||

| 0 | … | … | … | ||

| 0 | … | … | … | ||

| COIN 3 | 1 | ||||

| 0 | … | … | … | ||

| 0 | … | … | … | ||

| COIN 4 | 0 | … | … | … | |

| 0 | |||||

| 1 | … | … | … |

| Young coins: 1-day ahead probability of death | ||||||||||

| Models | AUC (Restrictive) | AUC (Simple) | AUC (1 cent) | Brier Score (Restrictive) | Brier Score (Simple) | Brier Score (1 cent) | MCS (Restrictive) | MCS (Simple) | MCS(1 cent) | % Not Converged |

| Logit (expanding window) | 0.79 | 0.73 | 0.60 | 0.089 | 0.182 | 0.238 | not included | not included | not included | 0.00 |

| Probit (expanding window) | 0.75 | 0.70 | 0.59 | 0.091 | 0.186 | 0.240 | not included | not included | not included | 0.00 |

| Cauchit (expanding window) | 0.86 | 0.80 | 0.64 | 0.077 | 0.161 | 0.233 | not included | not included | INCLUDED | 0.00 |

| Random Forest (expanding window) | 0.78 | 0.78 | 0.72 | 0.080 | 0.158 | 0.240 | not included | INCLUDED | not included | 0.00 |

| Logit (fixed window) | 0.84 | 0.77 | 0.58 | 0.081 | 0.170 | 0.250 | not included | not included | not included | 0.00 |

| Probit (fixed window) | 0.83 | 0.74 | 0.58 | 0.083 | 0.175 | 0.250 | not included | not included | not included | 0.00 |

| Cauchit (fixed window) | 0.86 | 0.80 | 0.64 | 0.077 | 0.157 | 0.241 | INCLUDED | INCLUDED | not included | 0.00 |

| Random Forest (fixed window) | 0.74 | 0.75 | 0.65 | 0.089 | 0.180 | 0.291 | not included | not included | not included | 0.00 |

| ZPP - Random walk | 0.79 | 0.75 | 0.77 | 0.152 | 0.199 | 0.384 | not included | not included | not included | 0.00 |

| ZPP - Normal GARCH(1,1) | 0.74 | 0.69 | 0.65 | 0.107 | 0.248 | 0.512 | not included | not included | not included | 1.70 |

| ZPP - Student’st GARCH(1,1) | 0.60 | 0.57 | 0.66 | 0.098 | 0.244 | 0.532 | not included | not included | not included | 0.90 |

| ZPP - GH Skew-Student GARCH(1,1) | 0.62 | 0.59 | 0.44 | 0.099 | 0.250 | 0.540 | not included | not included | not included | 43.17 |

| ZPP - MSGARCH(1,1) | 0.73 | 0.70 | 0.83 | 0.101 | 0.241 | 0.469 | not included | not included | not included | 0.81 |

| Young coins: 30-day ahead probability of death | ||||||||||

| Models | AUC (Restrictive) | AUC (Simple) | AUC (1 cent) | Brier Score (Restrictive) | Brier Score (Simple) | Brier Score (1 cent) | MCS (Restrictive) | MCS (Simple) | MCS(1 cent) | % NotConverged |

| Logit (expanding window) | 0.71 | 0.63 | 0.60 | 0.091 | 0.201 | 0.238 | not included | not included | not included | 0.00 |

| Probit (expanding window) | 0.69 | 0.61 | 0.59 | 0.092 | 0.203 | 0.239 | not included | not included | not included | 0.00 |

| Cauchit (expanding window) | 0.82 | 0.74 | 0.63 | 0.081 | 0.182 | 0.234 | not included | not included | not included | 0.00 |

| Random Forest (expanding window) | 0.65 | 0.65 | 0.64 | 0.102 | 0.218 | 0.290 | not included | not included | not included | 0.00 |

| Logit (fixed window) | 0.71 | 0.66 | 0.57 | 0.090 | 0.190 | 0.249 | not included | not included | not included | 0.00 |

| Probit (fixed window) | 0.69 | 0.66 | 0.57 | 0.091 | 0.191 | 0.250 | not included | not included | not included | 0.00 |

| Cauchit (fixed window) | 0.82 | 0.76 | 0.60 | 0.081 | 0.174 | 0.244 | INCLUDED | INCLUDED | not included | 0.00 |

| Random Forest (fixed window) | 0.64 | 0.65 | 0.61 | 0.107 | 0.221 | 0.305 | not included | not included | not included | 0.00 |

| ZPP - Random walk | 0.73 | 0.71 | 0.76 | 0.615 | 0.471 | 0.305 | not included | not included | not included | 0.00 |

| ZPP - Normal GARCH(1,1) | 0.69 | 0.66 | 0.65 | 0.360 | 0.358 | 0.385 | not included | not included | not included | 1.70 |

| ZPP - Student’st GARCH(1,1) | 0.67 | 0.63 | 0.55 | 0.213 | 0.253 | 0.448 | not included | not included | not included | 0.90 |

| ZPP - GH Skew-Student GARCH(1,1) | 0.69 | 0.64 | 0.50 | 0.183 | 0.243 | 0.437 | not included | not included | not included | 43.17 |

| ZPP - MSGARCH(1,1) | 0.72 | 0.70 | 0.85 | 0.228 | 0.233 | 0.197 | not included | not included | INCLUDED | 0.81 |

| Old coins: 1-day ahead probability of death | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Models | AUC (Restrictive) | AUC (Simple) | AUC (1 cent) | Brier Score (Restrictive) | Brier Score (Simple) | Brier Score (1 cent) | MCS (Restrictive) | MCS (Simple) | MCS (1 cent) | % Not Converged |

| Logit (expanding window) | 0.74 | 0.74 | 0.69 | 0.109 | 0.227 | 0.194 | not included | not included | not included | 0.00 |

| Probit (expanding window) | 0.73 | 0.71 | 0.67 | 0.117 | 0.241 | 0.197 | not included | not included | not included | 0.00 |

| Cauchit (expanding window) | 0.76 | 0.86 | 0.74 | 0.103 | 0.167 | 0.181 | not included | not included | not included | 0.00 |

| Random Forest (expanding window) | 0.96 | 0.97 | 0.95 | 0.034 | 0.065 | 0.069 | INCLUDED | INCLUDED | INCLUDED | 0.00 |

| Logit (fixed window) | 0.77 | 0.75 | 0.75 | 0.103 | 0.224 | 0.196 | not included | not included | not included | 0.00 |

| Probit (fixed window) | 0.76 | 0.74 | 0.74 | 0.106 | 0.228 | 0.202 | not included | not included | not included | 0.00 |

| Cauchit (fixed window) | 0.77 | 0.85 | 0.76 | 0.104 | 0.183 | 0.193 | not included | not included | not included | 0.00 |

| Random Forest (fixed window) | 0.78 | 0.84 | 0.77 | 0.087 | 0.191 | 0.167 | not included | not included | not included | 0.00 |

| ZPP - Random walk | 0.76 | 0.75 | 0.71 | 0.182 | 0.257 | 0.216 | not included | not included | not included | 0.00 |

| ZPP - Normal GARCH(1,1) | 0.64 | 0.59 | 0.64 | 0.125 | 0.402 | 0.243 | not included | not included | not included | 1.22 |

| ZPP - Student’st GARCH(1,1) | 0.57 | 0.54 | 0.63 | 0.117 | 0.387 | 0.248 | not included | not included | not included | 1.92 |

| ZPP - GH Skew-Student GARCH(1,1) | 0.57 | 0.55 | 0.42 | 0.120 | 0.396 | 0.251 | not included | not included | not included | 42.70 |

| ZPP - MSGARCH(1,1) | 0.69 | 0.68 | 0.70 | 0.111 | 0.374 | 0.229 | not included | not included | not included | 0.67 |

| Old coins: 30-day ahead probability of death | ||||||||||

| Models | AUC (Restrictive) | AUC (Simple) | AUC (1 cent) | Brier Score (Restrictive) | Brier Score (Simple) | Brier Score (1 cent) | MCS (Restrictive) | MCS (Simple) | MCS(1 cent) | % Not Converged |

| Logit (expanding window) | 0.71 | 0.73 | 0.68 | 0.104 | 0.220 | 0.194 | not included | not included | not included | 0.00 |

| Probit (expanding window) | 0.70 | 0.68 | 0.67 | 0.104 | 0.240 | 0.197 | not included | not included | not included | 0.00 |

| Cauchit (expanding window) | 0.74 | 0.77 | 0.74 | 0.102 | 0.211 | 0.181 | not included | not included | not included | 0.00 |

| Random Forest (expanding window) | 0.76 | 0.80 | 0.77 | 0.096 | 0.210 | 0.170 | INCLUDED | not included | INCLUDED | 0.00 |

| Logit (fixed window) | 0.74 | 0.77 | 0.74 | 0.103 | 0.205 | 0.197 | not included | INCLUDED | not included | 0.00 |

| Probit (fixed window) | 0.73 | 0.77 | 0.74 | 0.103 | 0.207 | 0.200 | not included | INCLUDED | not included | 0.00 |

| Cauchit (fixed window) | 0.75 | 0.79 | 0.75 | 0.103 | 0.207 | 0.194 | not included | INCLUDED | not included | 0.00 |

| Random Forest (fixed window) | 0.69 | 0.72 | 0.71 | 0.107 | 0.247 | 0.193 | not included | not included | not included | 0.00 |

| ZPP - Random walk | 0.75 | 0.69 | 0.68 | 0.514 | 0.331 | 0.440 | not included | not included | not included | 0.00 |

| ZPP - Normal GARCH(1,1) | 0.66 | 0.58 | 0.58 | 0.222 | 0.325 | 0.269 | not included | not included | not included | 1.22 |

| ZPP - Student’st GARCH(1,1) | 0.63 | 0.55 | 0.61 | 0.209 | 0.301 | 0.313 | not included | not included | not included | 1.92 |

| ZPP - GH Skew-Student GARCH(1,1) | 0.64 | 0.57 | 0.60 | 0.191 | 0.309 | 0.294 | not included | not included | not included | 42.70 |

| ZPP - MSGARCH(1,1) | 0.68 | 0.67 | 0.74 | 0.178 | 0.261 | 0.193 | not included | not included | not included | 0.67 |

| Old coins: 365-day ahead probability of death | ||||||||||

| Models | AUC (Restrictive) | AUC (Simple) | AUC (1 cent) | Brier Score (Restrictive) | Brier Score (Simple) | Brier Score (1 cent) | MCS (Restrictive) | MCS (Simple) | MCS(1 cent) | % Not Converged |

| Logit (expanding window) | 0.59 | 0.57 | 0.61 | 0.121 | 0.323 | 0.210 | not included | not included | INCLUDED | 0.00 |

| Probit (expanding window) | 0.58 | 0.55 | 0.61 | 0.119 | 0.319 | 0.211 | INCLUDED | INCLUDED | not included | 0.00 |

| Cauchit (expanding window) | 0.63 | 0.61 | 0.65 | 0.124 | 0.337 | 0.212 | not included | not included | not included | 0.00 |

| Random Forest (expanding window) | 0.61 | 0.60 | 0.59 | 0.131 | 0.338 | 0.237 | not included | not included | not included | 0.00 |

| Logit (fixed window) | 0.60 | 0.58 | 0.65 | 0.135 | 0.347 | 0.223 | not included | not included | not included | 0.00 |

| Probit (fixed window) | 0.60 | 0.57 | 0.63 | 0.138 | 0.345 | 0.246 | not included | not included | not included | 0.00 |

| Cauchit (fixed window) | 0.63 | 0.60 | 0.65 | 0.132 | 0.368 | 0.231 | not included | not included | not included | 0.00 |

| Random Forest (fixed window) | 0.62 | 0.61 | 0.61 | 0.129 | 0.318 | 0.227 | not included | INCLUDED | not included | 0.00 |

| ZPP - Random walk | 0.69 | 0.50 | 0.63 | 0.998 | 0.707 | 0.828 | not included | not included | not included | 0.00 |

| ZPP - Normal GARCH(1,1) | 0.66 | 0.51 | 0.55 | 0.929 | 0.668 | 0.806 | not included | not included | not included | 1.22 |

| ZPP - Student’st GARCH(1,1) | 0.68 | 0.52 | 0.56 | 0.390 | 0.400 | 0.368 | not included | not included | not included | 1.92 |

| ZPP - GH Skew-Student GARCH(1,1) | 0.67 | 0.50 | 0.54 | 0.362 | 0.395 | 0.351 | not included | not included | not included | 42.70 |

| ZPP - MSGARCH(1,1) | 0.63 | 0.52 | 0.70 | 0.366 | 0.354 | 0.304 | not included | not included | not included | 0.67 |

| Old coins: 1-day ahead probability of death (2016 –2017) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Models | AUC (Restrictive) | AUC (Simple) | AUC (1 cent) | Brier Score (restrictive) | Brier Score (Simple) | Brier Score (1 cent) | MCS (Restrictive) | MCS (Simple) | MCS (1 cent) |

| Logit (expanding window) | 0.76 | 0.72 | 0.76 | 0.087 | 0.197 | 0.232 | not included | not included | not included |

| Probit (expanding window) | 0.71 | 0.69 | 0.76 | 0.103 | 0.215 | 0.238 | not included | not included | not included |

| Cauchit (expanding window) | 0.80 | 0.83 | 0.81 | 0.079 | 0.142 | 0.195 | not included | not included | not included |

| Random Forest (expanding window) | 0.97 | 0.96 | 0.96 | 0.025 | 0.052 | 0.066 | INCLUDED | INCLUDED | INCLUDED |

| Logit (fixed window) | 0.77 | 0.81 | 0.80 | 0.086 | 0.147 | 0.198 | not included | not included | not included |

| Probit (fixed window) | 0.71 | 0.69 | 0.79 | 0.100 | 0.219 | 0.204 | not included | not included | not included |

| Cauchit (fixed window) | 0.81 | 0.84 | 0.82 | 0.079 | 0.137 | 0.184 | not included | not included | not included |

| Random Forest (fixed window) | 0.93 | 0.92 | 0.90 | 0.039 | 0.083 | 0.117 | not included | not included | not included |

| ZPP - Random walk | 0.81 | 0.76 | 0.72 | 0.105 | 0.202 | 0.292 | not included | not included | not included |

| ZPP - Normal GARCH(1,1) | 0.60 | 0.60 | 0.65 | 0.118 | 0.249 | 0.307 | not included | not included | not included |

| ZPP - Student’st GARCH(1,1) | 0.56 | 0.51 | 0.37 | 0.097 | 0.236 | 0.312 | not included | not included | not included |

| ZPP - GH Skew-Student GARCH(1,1) | 0.55 | 0.51 | 0.43 | 0.098 | 0.240 | 0.315 | not included | not included | not included |

| ZPP - MSGARCH(1,1) | 0.71 | 0.71 | 0.83 | 0.092 | 0.232 | 0.289 | not included | not included | not included |

| Old coins: 30-day ahead probability of death (2016–2017) | |||||||||

| Models | AUC (Restrictive) | AUC (Simple) | AUC (1 cent) | Brier Score (Restrictive) | Brier Score (Simple) | Brier Score (1 cent) | MCS (restrictive) | MCS (Simple) | MCS (1 cent) |

| Logit (expanding window) | 0.76 | 0.73 | 0.76 | 0.083 | 0.174 | 0.236 | not included | not included | not included |

| Probit (expanding window) | 0.76 | 0.72 | 0.75 | 0.084 | 0.177 | 0.242 | not included | not included | not included |

| Cauchit (expanding window) | 0.77 | 0.74 | 0.81 | 0.081 | 0.165 | 0.202 | not included | not included | not included |

| Random Forest (expanding window) | 0.81 | 0.78 | 0.84 | 0.078 | 0.160 | 0.170 | INCLUDED | INCLUDED | INCLUDED |

| Logit (fixed window) | 0.76 | 0.73 | 0.78 | 0.081 | 0.170 | 0.207 | not included | not included | not included |

| Probit (fixed window) | 0.76 | 0.73 | 0.77 | 0.081 | 0.172 | 0.213 | not included | not included | not included |

| Cauchit (fixed window) | 0.77 | 0.75 | 0.81 | 0.080 | 0.163 | 0.190 | not included | not included | not included |

| Random Forest (fixed window) | 0.78 | 0.74 | 0.82 | 0.084 | 0.177 | 0.181 | not included | not included | not included |

| ZPP - Random walk | 0.80 | 0.74 | 0.70 | 0.288 | 0.257 | 0.328 | not included | not included | not included |

| ZPP - Normal GARCH(1,1) | 0.66 | 0.62 | 0.58 | 0.170 | 0.239 | 0.303 | not included | not included | not included |

| ZPP - Student’st GARCH(1,1) | 0.65 | 0.55 | 0.63 | 0.133 | 0.225 | 0.343 | not included | not included | not included |

| ZPP - GH Skew-Student GARCH(1,1) | 0.66 | 0.57 | 0.63 | 0.128 | 0.230 | 0.338 | not included | not included | not included |

| ZPP - MSGARCH(1,1) | 0.69 | 0.69 | 0.86 | 0.135 | 0.206 | 0.171 | not included | not included | INCLUDED |

| Old coins: 365-day ahead probability of death (2016–2017) | |||||||||

| Models | AUC (Restrictive) | AUC (Simple) | AUC (1 cent) | Brier Score (Restrictive) | Brier Score (Simple) | Brier Score (1 cent) | MCS (Restrictive) | MCS (Simple) | MCS (1 cent) |

| Logit (expanding window) | 0.67 | 0.61 | 0.68 | 0.071 | 0.189 | 0.299 | INCLUDED | not included | not included |

| Probit (expanding window) | 0.67 | 0.60 | 0.67 | 0.071 | 0.189 | 0.300 | INCLUDED | not included | not included |

| Cauchit (expanding window) | 0.64 | 0.64 | 0.70 | 0.072 | 0.186 | 0.282 | not included | INCLUDED | not included |

| Random Forest (expanding window) | 0.65 | 0.61 | 0.69 | 0.130 | 0.273 | 0.300 | not included | not included | not included |

| Logit (fixed window) | 0.66 | 0.60 | 0.65 | 0.073 | 0.191 | 0.282 | not included | not included | not included |

| Probit (fixed window) | 0.66 | 0.60 | 0.64 | 0.073 | 0.191 | 0.285 | not included | not included | not included |

| Cauchit (fixed window) | 0.65 | 0.62 | 0.69 | 0.073 | 0.206 | 0.271 | not included | not included | not included |

| Random Forest (fixed window) | 0.64 | 0.59 | 0.72 | 0.129 | 0.285 | 0.267 | not included | not included | INCLUDED |

| ZPP - Random walk | 0.67 | 0.64 | 0.60 | 1.106 | 0.881 | 0.878 | not included | not included | not included |

| ZPP - Normal GARCH(1,1) | 0.65 | 0.58 | 0.54 | 0.764 | 0.647 | 0.682 | not included | not included | not included |

| ZPP - Student’st GARCH(1,1) | 0.62 | 0.58 | 0.53 | 0.358 | 0.328 | 0.394 | not included | not included | not included |

| ZPP - GH Skew-Student GARCH(1,1) | 0.66 | 0.61 | 0.49 | 0.302 | 0.285 | 0.358 | not included | not included | not included |

| ZPP - MSGARCH(1,1) | 0.59 | 0.64 | 0.84 | 0.443 | 0.377 | 0.300 | not included | not included | not included |

| Old coins: 1-day ahead probability of death (2018 –2020) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Models | AUC (Restrictive) | AUC (Simple) | AUC (1 cent) | Brier Score (Restrictive) | Brier Score (Simple) | Brier Score (1 cent) | MCS (Restrictive) | MCS (Simple) | MCS (1 cent) |

| Logit (expanding window) | 0.78 | 0.75 | 0.68 | 0.115 | 0.235 | 0.184 | not included | not included | not included |

| Probit (expanding window) | 0.76 | 0.73 | 0.66 | 0.120 | 0.247 | 0.187 | not included | not included | not included |

| Cauchit (expanding window) | 0.78 | 0.87 | 0.72 | 0.110 | 0.173 | 0.177 | not included | not included | not included |