Effects of Crude Oil Price Shocks on Stock Markets and Currency Exchange Rates in the Context of Russia-Ukraine Conflict: Evidence from G7 Countries

Abstract

:1. Introduction

2. Previous Studies

3. Methodology

3.1. Break-Point Unit Root Test

3.2. FIGARCH

Model

ht = α0 + ∑αiϵ2t−I + ∑βjht−j

i = 1 j = 1

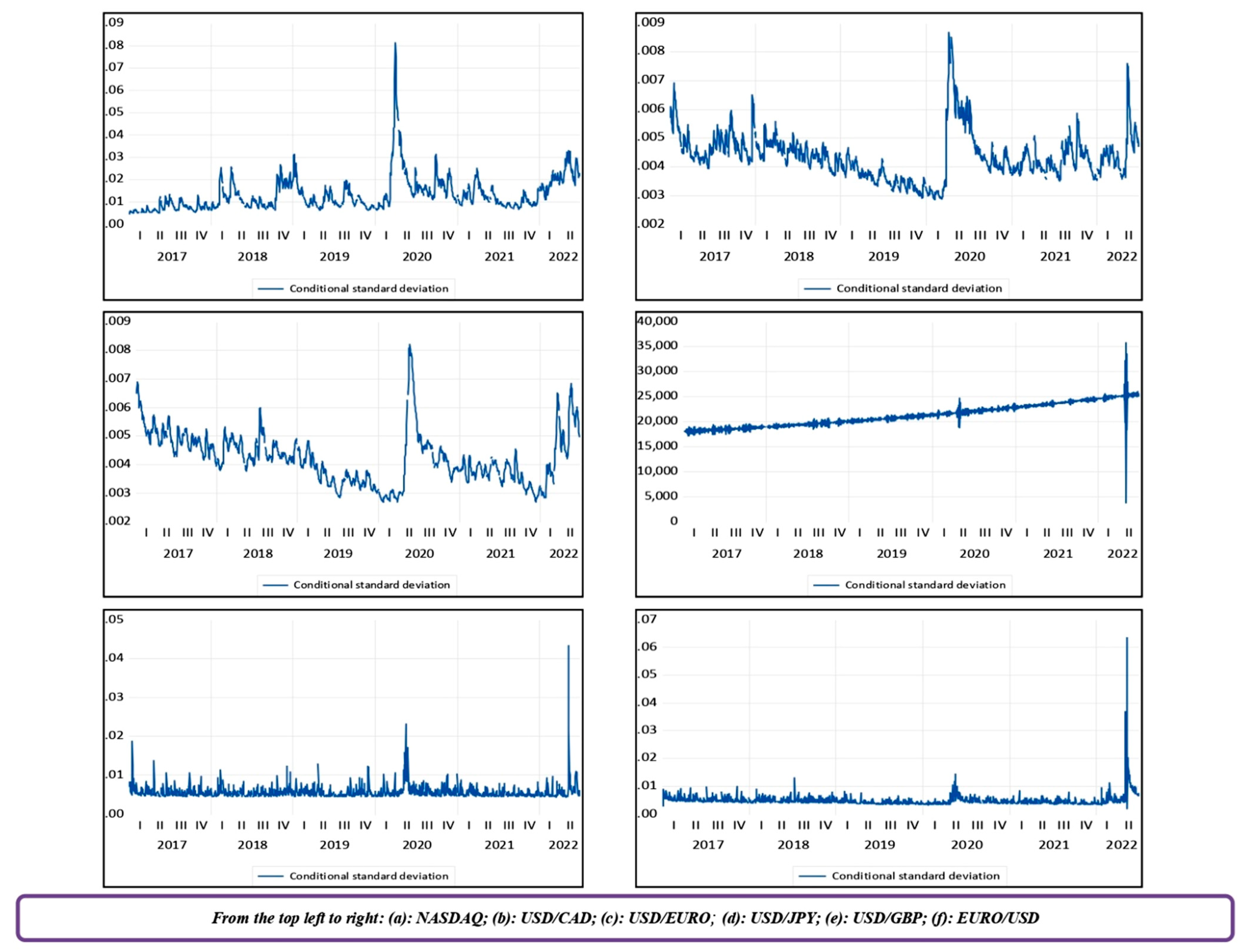

4. Empirical Results and Discussion

4.1. Descriptive Tests

4.2. Parameter Stability Test

4.3. Break-Point Unit Root Test

4.4. FIGARCH Estimation Results

5. Conclusions, Recommendations and Limitations

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Ahmad, Wasim, Ravi Prakash, Gazi Salah Uddin, Rishman Jot Kaur Chahal, Md Lutfur Rahman, and Anupam Dutta. 2020. On the intraday dynamics of oil price and exchange rate: What can we learn from China and India? Energy Economics 91: 104871. [Google Scholar] [CrossRef]

- Ali, Syed Riaz Mahmood, Walid Mensi, Kaysul Islam Anik, Mishkatur Rahman, and Sang Hoon Kang. 2022. The impacts of COVID-19 crisis on spillovers between the oil and stock markets: Evidence from the largest oil importers and exporters. Economic Analysis and Policy 73: 345–72. [Google Scholar] [CrossRef]

- Baillie, Richard T., Tim Bollerslev, and Hans Ole Mikkelsen. 1996. Fractionally integrated generalized autoregressive conditional heteroscedasticity. Journal of Econometrics 74: 3–30. [Google Scholar] [CrossRef]

- Bollerslev, Tim. 1986. Generalized autoregressive conditional heteroscedasticity. Journal of Econometrics 31: 307–27. [Google Scholar] [CrossRef] [Green Version]

- Bollerslev, Tim, and Ole Mikkelsen Hans. 1996. Modeling and pricing long memory in stock market volatility. Journal of Econometrics 73: 151–84. [Google Scholar] [CrossRef]

- Bordignon, Silvano, Massimiliano Caporin, and Francesco Lisi. 2004. A Seasonal Fractionally Integrated GARCH Model. Working Paper. Padova: University of Padova. [Google Scholar]

- Bourghelle, David, Fredj Jawadi, and Philippe Rozin. 2021. Oil price volatility in the context of COVID-19. International Economics 167: 39–49. [Google Scholar] [CrossRef]

- Cai, Yifei, Dongna Zhang, Tsangyao Chang, and Chien-Chiang Lee. 2022. Macroeconomic outcomes of OPEC and non-OPEC oil supply shocks in the euro area. Energy Economics 109: 105975. [Google Scholar] [CrossRef]

- Chen, Lin, Fenghua Wen, Wanyang Li, Hua Yin, and Lili Zhao. 2022. Extreme risk spillover of the oil, exchange rate to Chinese stock market: Evidence from implied volatility indexes. Energy Economics 107: 105857. [Google Scholar] [CrossRef]

- Chen, Mei-Ping, Chien-Chiang Lee, Yu-Hui Lin, and Wen-Yi Chen. 2018. Did the SARS pandemic weaken the integration of Asian stock markets? Evidence from smooth time-varying cointegration analysis. Economic Research-Ekonomskaistraživanja 31: 908–926. [Google Scholar]

- Conrad, C., and Berthould Haag. 2006. Inequality constraints in the fractionally integrated GARCH model. Journal of Financial Econometrics 4: 413–49. [Google Scholar] [CrossRef]

- Dacorogna, Michel, A. Muller Ulrich, J. Nagler Robert, B. Olsen Richard, and V. Pictet Olivier. 1993. A geographical model for the daily and weekly seasonal volatility in the foreign exchange market. Journal of International Money and Finance 12: 413–38. [Google Scholar] [CrossRef]

- Dai, Zhifeng, Haoyang Zhu, and Xinhua Zhang. 2022. Dynamic spillover effects and portfolio strategies between Crude Oil, Gold and Chinese stock markets related to new energy vehicle. Energy Economics 109: 105959. [Google Scholar] [CrossRef]

- Davidson, James. 2004. Moment and memory properties of linear conditional heteroskedasticity models, and a new model. Journal of Business and Economic Statistics 22: 16–190. [Google Scholar] [CrossRef] [Green Version]

- Ding, Zhuanxin, Clive W. J. Granger, and Robert F. Engle. 1993. A long memory property of stock market returns and a new model. Journal of Empirical Finance 1: 83–106. [Google Scholar] [CrossRef]

- Emrah, Ismail Cevik, Sel Dibooglu, Atif Awad Abdallah, and Eisa Abdul Rahman Al-Eisa. 2021. Oil prices, stock market returns, and volatility spillovers: Evidence from Saudi Arabia. International Economics and Economic Policy 18: 157–75. [Google Scholar]

- Engle, Robert F. 1982. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica: Journal of the Econometric Society 32: 987–1007. [Google Scholar] [CrossRef]

- Engle, Robert F., and Tim Bollerslev. 1986. Modelling the persistence of conditional variances. Econometric Reviews 5: 1–50. [Google Scholar] [CrossRef]

- Foroni, Claudia, Pierre Guerin, and Massimiliano Marcellino. 2017. Explaining the time-varying effects of oil market shocks on US stock returns. Economics Letters 155: 84–88. [Google Scholar] [CrossRef]

- Granger, Clive W. J., and Zhuanxin Ding. 1996. Varieties of long memory models. Journal of Econometrics 73: 61–77. [Google Scholar] [CrossRef]

- Hashmi, Shabir Mohsin, Ahmed Farhan, Alhayki Zainab, and Aamir Aijaz Syed. 2022. The impact of crude oil prices on Chinese stock markets and selected sectors: Evidence from the VAR-DCC-GARCH model. Environmental Science and Pollution Research 29: 52560–73. [Google Scholar] [CrossRef]

- Huang, Shupei, Haizhong An, Xiangyun Gao, Shaobo Wen, and Xiaoqing Hao. 2017. The multi-scale impact of exchange rates on the oil-stock nexus: Evidence from China and Russia. Applied Energy 194: 667–78. [Google Scholar] [CrossRef]

- Jiang, Mengting, and Dongmin Kong. 2021. The impact of international crude oil prices on energy stock prices: Evidence from China. Energy Research Letters 2: 28–33. [Google Scholar] [CrossRef]

- Li, Chang Shuai, and Qing Xian Xiao. 2011. Structural break in persistence of European stock market: Evidence from panel GARCH model. International Journal of Intelligent Information Processing 2: 40–48. [Google Scholar]

- Li, Jingyu, Ranran Liu, Yanzhen Yao, and Qiwei Xie. 2022. Time-frequency volatility spillovers across the international crude oil market and Chinese major energy futures markets: Evidence from COVID-19. Resources Policy 77: 102646. [Google Scholar] [CrossRef]

- Ma, Richie Ruchuan, Tao Xiong, and Yukun Bao. 2021. The Russia–Saudi Arabia oil price war during the COVID-19 pandemic. Energy Economics 102: 105517. [Google Scholar] [CrossRef]

- Meiyu, Tian, Wanyang Li, and Fenghua Wen. 2021. The dynamic impact of oil price shocks on the stock market and the USD/RMB exchange rate: Evidence from implied volatility indices. The North American Journal of Economics and Finance 55: 101310. [Google Scholar]

- Mensi, Walid, Khamis Hamed Al-Yahyaee, Xuan Vinh Vo, and Sang Hoon Kang. 2021. Modeling the frequency dynamics of spillovers and connectedness between crude oil and MENA stock markets with portfolio implications. Economic Analysis and Policy 71: 397–419. [Google Scholar] [CrossRef]

- Nasr, Adnen Ben, Mohamed Boutahr, and Abdelwahed Trabelsi. 2010. Fractionally integrated time varying GARCH model. Statistical Methods and Applications 19: 399–430. [Google Scholar] [CrossRef]

- Nguyen, Tra Ngoc, Dat Thanh Nguyen, and Vu Ngoc Nguyen. 2020. The Impacts of Oil Price and Exchange Rate on Vietnamese Stock Market. Journal of Asian Finance, Economics, and Business 7: 143–50. [Google Scholar] [CrossRef]

- Nusair, Salah A., and Dennis Olson. 2022. Dynamic relationship between exchange rates and stock prices for the G7 countries: A nonlinear ARDL approach. Journal of International Financial Markets, Institutions and Money 78: 101541. [Google Scholar] [CrossRef]

- Perron, Pierre. 1989. The great crash, the oil price shock, and the unit root hypothesis. Econometrica 57: 1361–401. [Google Scholar] [CrossRef] [Green Version]

- Perron, Pierre. 1997. Further evidence on breaking trend functions in macroeconomic variables. Journal of Econometrics 80: 355–85. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, M. Hashem, and Bahram Pesaran. 1997. Working with Microfit 4.0: Interactive Econometric Analysis. Oxford: Oxford University Press. [Google Scholar]

- Rapach, David E., and Jack K. Strauss. 2008. Structural breaks and GARCH models of exchange rate volatility. Journal of Applied Econometrics 23: 65–90. [Google Scholar] [CrossRef]

- Ready, Robert C. 2018. Oil prices and the stock market. Review of Finance 22: 155–76. [Google Scholar] [CrossRef]

- Rohan, Neelabh, and T. V. Ramanathan. 2012. Asymmetric volatility models with structural breaks. Communications in Statistics-Simulations and Computations 14: 89–101. [Google Scholar] [CrossRef]

- Roubaud, David, and Mohamed Arouri. 2018. Oil prices, exchange rates and stock markets under uncertainty and regime-switching. Finance Research Letters 27: 28–33. [Google Scholar] [CrossRef]

- Saraswat, Gopal Bihari, Saraswat Madhav, Singh Sanjay Kumar, and Tiwari Ravi Shekhar. 2022. The Fluctuation in Interest Rate, Exchange Rate and Crude Oil Price and its impact on Stock Market. YMER 21: 484–502. [Google Scholar] [CrossRef]

- Shabir, Mohsin Hashmi, and Hussain Chang Bisharat. 2022. Revisiting the relationship between oil prices, exchange rate, and stock prices: An application of quantile ARDL model. Resources Policy 75: 102543. [Google Scholar]

- Tayefi, Maryam, and T. V. Ramanathan. 2012. An overview of FIGARCH and related time series models. Austrian Journal of Statistics 41: 175–96. [Google Scholar] [CrossRef]

- Taylor, Stephen J. 1986. Modelling Financial Time Series. Chichester: John Wiley and Sons, Ltd. [Google Scholar]

- Vochozka, Marek, Zuzana Rowland, Petr Suler, and Josef Marousek. 2020. The Influence of the International Price of Oil on the Value of the EUR/USD Exchange Rate. Journal of Competitiveness 12: 167–90. [Google Scholar] [CrossRef]

- Wen, Danyan, Li Liu, Chaoqun Ma, and Yudong Wang. 2020. Extreme risk spillovers between crude oil prices and the U.S. exchange rate: Evidence from oil-exporting and oil-importing countries. Energy 212: 118740. [Google Scholar] [CrossRef]

- Wen, Fenghua, Minzhi Zhang, Jihong Xiao, and Wei Yue. 2022. The impact of oil price shocks on the risk-return relation in the Chinese stock market. Finance Research Letters 47: 102788. [Google Scholar] [CrossRef]

- Yuan, Di, Sufang Li, Rong Li, and Feipeng Zhang. 2022. Economic policy uncertainty, oil and stock markets in BRIC: Evidence from quantiles analysis. Energy Economics 110: 105972. [Google Scholar] [CrossRef]

- Zhang, Zitao, and Yun Qin. 2022. Study on the nonlinear interactions among the international oil price, the RMB exchange rate and China’s gold price. Resources Policy 77: 102683. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| TSX | CAC 40 | DAX 30 | FTSE MIB | Nikkei 225 | FTSE 100 | NASDAQ | |

|---|---|---|---|---|---|---|---|

| Mean | 0.001 | 0.001 | 0.001 | 0.001 | 0.002 | 0.068 | 0.006 |

| Median | 0.001 | 0.001 | 0.001 | 0.001 | 0.000 | 0.005 | 0.002 |

| Maximum | 0.113 | 0.081 | 0.104 | 0.085 | 0.077 | 0.087 | 0.096 |

| Minimum | −0.132 | −0.131 | −0.131 | −0.185 | −0.063 | −0.115 | −0.130 |

| Std. Dev. | 0.012 | 0.012 | 0.012 | 0.014 | 0.011 | 0.011 | 0.015 |

| Skewness | −2.109 | −1.052 | −0.964 | −2.261 | −0.054 | −1.262 | −0.756 |

| Kurtosis | 51.928 | 19.643 | 19.668 | 32.946 | 7.930 | 21.587 | 12.438 |

| Jarque–Bera | 133,350 | 15,559.530 | 15,567.290 | 50,715.440 | 1344.332 | 19,454.250 | 5051.605 |

| Probability | 0.000 * | 0.000 * | 0.000 * | 0.000 * | 0.000 * | 0.000 * | 0.000 * |

| CAD | Euro | JPY | GBP | USD | Brent Crude Oil | |

|---|---|---|---|---|---|---|

| Mean | −0.042 | −0.076 | 0.002 | −0.053 | 0.071 | 0.001 |

| Median | 0.000 | 0.000 | −0.002 | 0.000 | 0.000 | 0.002 |

| Maximum | 0.021 | 0.021 | 0.334 | 0.037 | 0.057 | 0.329 |

| Minimum | −0.019 | −0.016 | −0.031 | −0.030 | −0.021 | −0.280 |

| Std. Dev. | 0.004 | 0.004 | 0.010 | 0.005 | 0.004 | 0.028 |

| Skewness | 0.112 | 0.039 | 26.688 | −0.032 | 1.467 | −0.144 |

| Kurtosis | 4.711 | 4.120 | 875.569 | 6.609 | 22.370 | 34.292 |

| Jarque–Bera | 164.724 | 69.737 | 173.345 | 140.510 | 121.46 | 144.47 |

| Probability | 0.000 * | 0.000 * | 0.000 * | 0.000 * | 0.000 * | 0.000 * |

| Trend and Intercept (Innovative Outlier Model) | |||

|---|---|---|---|

| At Level | |||

| Variables | t-Statistics | p-Value | Break Date |

| TSX | −12.2611 | 0.01 * | 24 February 2022 |

| CAC 40 | −36.2886 | 0.01 * | 28 February 2022 |

| DAX 30 | −37.2328 | 0.01 * | 1 March 2022 |

| FTSE MIB | −39.0779 | 0.01 * | 24 February 2022 |

| Nikkei 225 | −23.56 | 0.01 * | 1 March 2022 |

| FTSE 100 | −13.5555 | 0.01 * | 24 February 2022 |

| NASDAQ | −15.0214 | 0.01 * | 26 February 2022 |

| CAD | −36.8506 | 0.01 * | 24 February 2022 |

| EUR | −36.3835 | 0.01 * | 16 March 2022 |

| JPY | −36.8619 | 0.01 * | 24 February 2022 |

| GBP | −35.3468 | 0.01 * | 15 March 2022 |

| USD | −35.216 | 0.01 * | 26 March 2022 |

| Brent Crude Oil Price | −32.7856 | 0.01 * | 28 March 2022 |

| Dependent Variable | Constant () | p-Value | ARCH Effect (α) | p-Value | GARCH Effect (β) | p-Value | α + β |

|---|---|---|---|---|---|---|---|

| TSX | 0.027 | 0.00 * | 0.187 | 0.10 *** | 0.467 | 0.00 * | 0.653 |

| CAC 40 | 0.011 | 0.00 * | 0.456 | 0.10 *** | 0.499 | 0.02 ** | 0.955 |

| DAX 30 | 0.013 | 0.00 * | 0.461 | 0.00 * | 0.519 | 0.03 ** | 0.980 |

| FTSE MIB | 0.010 | 0.00 * | 0.472 | 0.08 *** | 0.501 | 0.00 * | 0.973 |

| Nikkei 225 | 0.064 | 0.00 * | 0.312 | 0.00 * | 0.681 | 0.00 * | 0.992 |

| FTSE 100 | 0.079 | 0.01 * | 0.401 | 0.03 ** | 0.532 | 0.01 * | 0.933 |

| NASDAQ | 0.088 | 0.00 * | 0.013 | 0.84 | 0.553 | 0.00 * | 0.567 |

| CAD | 0.010 | 0.01 * | 0.393 | 0.00 * | 0.603 | 0.00 * | 0.996 |

| EUR | 0.062 | 0.14 | 0.375 | 0.00 * | 0.565 | 0.00 * | 0.941 |

| JPY | 0.202 | 0.01 * | 0.438 | 0.07 ** | 0.555 | 0.04 ** | 0.993 |

| GBP | 0.021 | 0.00 * | 0.080 | 0.00 * | 0.841 | 0.00 * | 0.9215 |

| USD | 0.201 | 0.22 | 0.151 | 0.52 | 0.601 | 0.05 ** | 0.750 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bagchi, B.; Paul, B. Effects of Crude Oil Price Shocks on Stock Markets and Currency Exchange Rates in the Context of Russia-Ukraine Conflict: Evidence from G7 Countries. J. Risk Financial Manag. 2023, 16, 64. https://doi.org/10.3390/jrfm16020064

Bagchi B, Paul B. Effects of Crude Oil Price Shocks on Stock Markets and Currency Exchange Rates in the Context of Russia-Ukraine Conflict: Evidence from G7 Countries. Journal of Risk and Financial Management. 2023; 16(2):64. https://doi.org/10.3390/jrfm16020064

Chicago/Turabian StyleBagchi, Bhaskar, and Biswajit Paul. 2023. "Effects of Crude Oil Price Shocks on Stock Markets and Currency Exchange Rates in the Context of Russia-Ukraine Conflict: Evidence from G7 Countries" Journal of Risk and Financial Management 16, no. 2: 64. https://doi.org/10.3390/jrfm16020064

APA StyleBagchi, B., & Paul, B. (2023). Effects of Crude Oil Price Shocks on Stock Markets and Currency Exchange Rates in the Context of Russia-Ukraine Conflict: Evidence from G7 Countries. Journal of Risk and Financial Management, 16(2), 64. https://doi.org/10.3390/jrfm16020064