When Institutional Plates Collide: The Dynamic Impact of Informal Institutions on Capital Market Development

Abstract

:1. Introduction

2. Empirical Setting

“... it [Polish capital market development] started building up very fast from the moment Poland entered the European Union, which was the breaking point for Polish companies to leverage their business potential.”

“[... the Warsaw stock exchange] has support from the whole country, which is actually behind the growth of the capital market.”

3. Literature Review, Theory and Hypotheses Development

3.1. Literature Review and Theoretical Framework

3.2. Informal Institutions and Capital Market Development

3.3. Informal Institutions and Interrelations with Formal Institutions

3.4. Informal Institutions in Emerging Economies

4. Data and Method

4.1. Sample and Estimation Methodology

4.2. Variable Measurement

5. Results

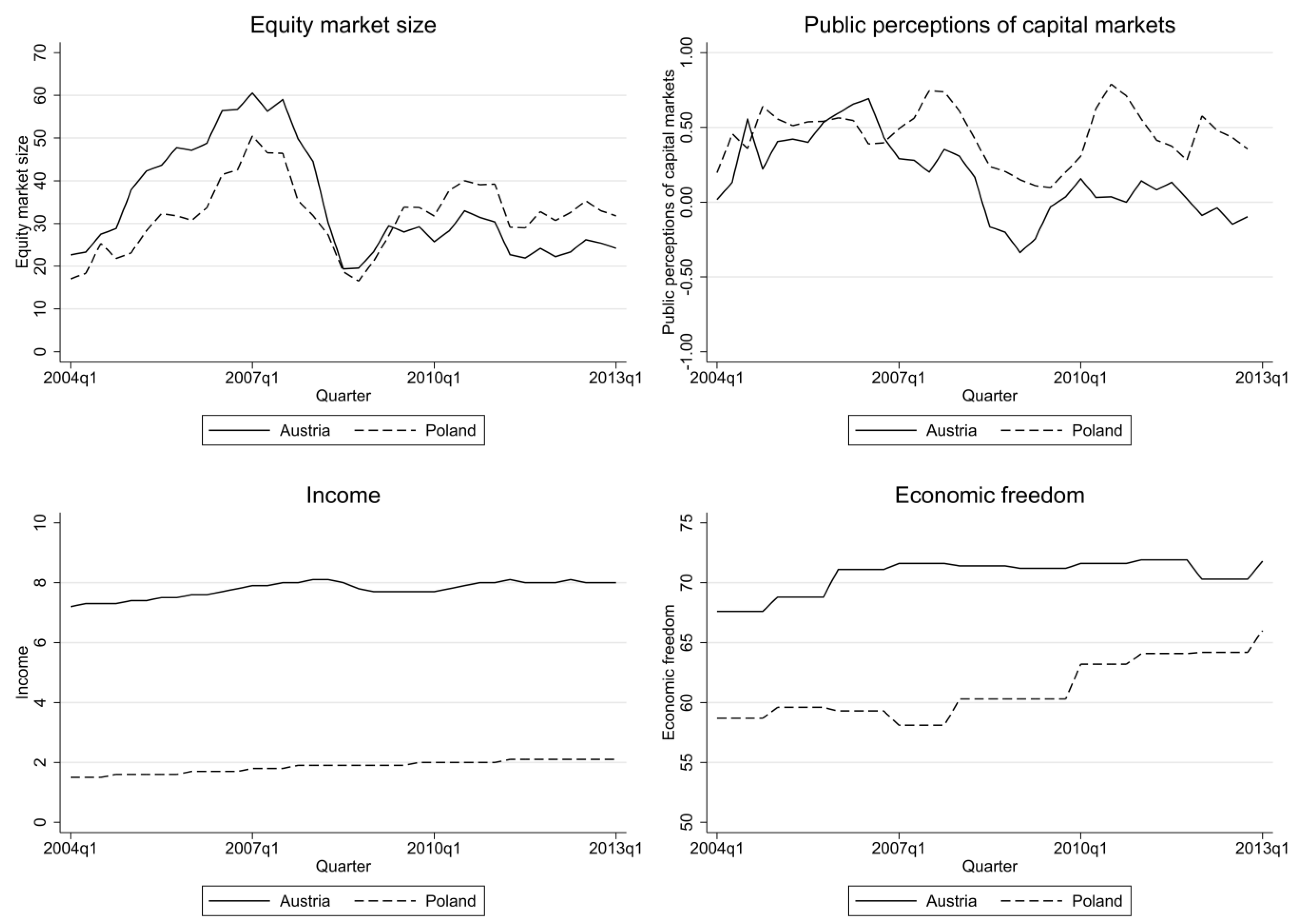

5.1. Descriptive Statistics

5.2. Regression Results

- (1a)

- EMSit = β0 + β1 PPCMit + β2 EFit + β3 C + β4+(t−1) Tt−1 + εit,

- (1b)

- EMSit = β0 + β1 PPCMit + β2 EFit + β3 INCit + β4 INFit + β5 C + β6+(t−1) Tt−1 + εit,

- (2)

- EMSit = β0 + β1 PPCMit + β2 EFit + β3 (PPCMit*EFit) + β4 C + β5+(t−1) Tt−1 + εit,

- (3)

- EMSit = β0 + β1 PPCMit + β2 EFit + β3 (PPCMit*C) + β4 C + β5+(t−1) Tt−1 + εit,

5.3. Robustness Checks

6. Discussion and Implications

6.1. Discussion and Research Implications

6.2. Policy Implications

“If we try to cover the privatization transactions without the politicians’ support, it’s going to be impossible... our minister of the state, as a main shareholder of the Warsaw Stock Exchange, is giving us support.”

6.3. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Content Coding

{kind=link}

| Public perception of capital markets: Content coding. |

| The aim of categorizing the newspaper articles according to the conveyed content lies in the complex task of considering relevant articles only. Thus, content coding may prevent using articles that may bias the resulting variable measurement. Because the aim is to capture public perception of capital markets, the analysis should only consider articles that reflect the public discourse and are not displaying ex post information on capital markets or capital market actors. Therefore, the following categories and respective descriptions are provided to select those articles that are not reflecting public perception of capital markets: |

| “Data extraction failure” comprises articles that should not have been displayed by the Factiva database. This category comprises articles that are textually precisely the same as another article already considered for the analysis. |

| “Misleading keyword” comprises articles that are not related to capital markets, although the keyword is mentioned in the title or lead paragraph. Examples within this category can be manifold and comprise, for example, articles about (1) country ratings or (2) bank bailouts. |

| “Capital market report” comprises articles that display capital market related ex post information. These articles are characterized by a tabular or abbreviated form and comprise facts on capital market activities such as (1) stock tickers, (2) bond tickers, and (3) index developments. |

| “Corporate fact” comprises articles that display firm related ex post information. These articles comprise facts on corporate activities such as (1) capital market performance, (2) share issues, and (3) capital increases. |

| 1 | As both countries of analysis only have one stock exchange, we do not have to differentiate between country- and exchange-level data. |

| 2 | The Heritage Foundation considers countries that score in the 80–100 range as having the best (“most free”) institutions; those in the 70–79.9 range as having good institutions, and those in the 60–69.9 range as having moderately good institutions. Countries in the 50–59.9 range are characterized by mostly weak institutions, and countries in the 0–49.9 range have the weakest institutions. |

| 3 | For Model 2 and Model 3 results of an F-test further indicate that the coefficients of our interaction variables are significantly different from zero (p < 0.001 for Model 2; p < 0.001 for Model 3). |

References

- Aixalá, José, and Gema Fabro. 2008. Does the impact of institutional quality on economic growth depend on initial income level? Economic Affairs 28: 45–49. [Google Scholar] [CrossRef]

- Arslan, Ahmad, and Jorma Larimo. 2010. Ownership strategy of multinational enterprises and the impacts of regulative and normative institutional distance: Evidence from Finnish foreign direct investments in Central and Eastern Europe. Journal of East-West Business 16: 179–200. [Google Scholar] [CrossRef]

- Beck, Nathaniel, and Jonathan N. Katz. 1995. What to do (and not to do) with time-series cross-section data. American Political Science Review 89: 634–47. [Google Scholar] [CrossRef]

- Bell, Gregg R., Igor Filatotchev, and Abdul A. Rasheed. 2012. The liability of foreignness in capital markets: Sources and remedies. Journal of International Business Studies 43: 107–22. [Google Scholar] [CrossRef] [Green Version]

- Berggren, Niclas, Andreas Bergh, and Christian Bjørnskov. 2012. The growth effects of institutional instability. Journal of Institutional Economics 8: 187–224. [Google Scholar] [CrossRef] [Green Version]

- Billmeier, Andreas, and Isabella Massa. 2009. What drives stock market development in emerging markets—institutions, remittances, or natural resources? Emerging Markets Review 10: 23–35. [Google Scholar] [CrossRef]

- Bitektine, Alex. 2011. Toward a theory of social judgments of organizations: The case of legitimacy, reputation, and status. Academy of Management Review 36: 151–79. [Google Scholar] [CrossRef]

- Cantwell, John, John H. Dunning, and Sarianna M. Lundan. 2010. An evolutionary approach to understanding international business activity: The co-evolution of MNEs and the institutional environment. Journal of International Business Studies 41: 567–68. [Google Scholar] [CrossRef]

- Chadee, Doren, and Banjo Roxas. 2013. Institutional environment, innovation capacity and firm performance in Russia. Critical Perspectives on International Business 9: 19–39. [Google Scholar] [CrossRef] [Green Version]

- Chang, Ha-Joon. 2011. Institutions and economic development: Theory, policy and history. Journal of Institutional Economics 7: 473–98. [Google Scholar] [CrossRef] [Green Version]

- Chinn, Menzie D., and Hiro Ito. 2006. What matters for financial development? Capital controls, institutions, and interactions. Journal of Development Economics 81: 163–92. [Google Scholar] [CrossRef] [Green Version]

- Chui, Andy C. W., Alison E. Lloyd, and Chuck C. Y. Kwok. 2002. The determination of capital structure: Is national culture a missing piece to the puzzle? Journal of International Business Studies 33: 99–127. [Google Scholar] [CrossRef]

- Cruz-García, Paula, and Jesús Peiró-Palomino. 2019. Informal, formal institutions and credit: Complements or substitutes? Journal of Institutional Economics 15: 649–71. [Google Scholar] [CrossRef]

- Cumming, Douglas J., Igor Filatotchev, April M. Knill, David M. Reeb, and Lemma W. Senbet. 2017. Law, finance and the international mobility of corporate governance. Journal of International Business Studies 48: 123–47. [Google Scholar] [CrossRef] [Green Version]

- Deephouse, David. L. 1996. Does isomorphism legitimate? Academy of Management Journal 39: 1024–39. [Google Scholar] [CrossRef]

- Deephouse, David. L. 2000. Media reputation as a strategic resource: An integration of mass communication and resource-based theories. Journal of Management 26: 1091–112. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, Asli, and Ross Levine. 1996. Stock market development and financial intermediaries: Stylized facts. World Bank Economic Review 10: 291–321. [Google Scholar] [CrossRef]

- Djankov, Simeon, Rafael La Porta, Florencio Lopez-de-Silanes, and Andrei Shleifer. 2008. The law and economics of self-dealing. Journal of Financial Economics 88: 430–65. [Google Scholar] [CrossRef] [Green Version]

- Dobija, Dorota, and Karol M. Klimczak. 2010. Development of Accounting in Poland: Market Efficiency and the Value Relevance of Reported Earnings. The International Journal of Accounting 45: 356–74. [Google Scholar] [CrossRef]

- Doidge, Craig, Andrew G. Karolyi, and René M. Stulz. 2013. The US left behind? Financial globalization and the rise of IPOs outside the US. Journal of Financial Economics 110: 546–73. [Google Scholar] [CrossRef]

- Driffield, Nigel L., Tomasz M. Mickiewicz, and Yama Temouri. 2016. Ownership control of foreign affiliates: A property rights theory perspective. Journal of World Business 51: 965–76. [Google Scholar] [CrossRef] [Green Version]

- Engelen, Peter-Jan, and Marc van Essen. 2010. Underpricing of IPOs: Firm-, issue- and country-specific characteristics. Journal of Banking and Finance 34: 1958–69. [Google Scholar] [CrossRef]

- Estrin, Saul, Delia Baghdasaryan, and Klaus E. Meyer. 2009. The impact of institutional and human resource distance on international entry strategies. Journal of Management Studies 46: 1171–96. [Google Scholar] [CrossRef] [Green Version]

- Gaur, Ajai, and Mukesh Kumar. 2018. A systematic approach to conducting review studies: An assessment of content analysis in 25 years of IB research. Journal of World Business 53: 280–89. [Google Scholar] [CrossRef]

- Glaeser, Edward L., Rafael La Porta, Florencio Lopez-de-Silanes, and Andrei Shleifer. 2004. Do Institutions Cause Growth? Journal of Economic Growth 9: 271–303. [Google Scholar] [CrossRef]

- Globerman, Steven, and Daniel Shapiro. 2003. Governance infrastructure and US foreign direct investment. Journal of International Business Studies 34: 19–39. [Google Scholar] [CrossRef]

- Golder, Peter N. 2000. Historical method in marketing research with new evidence on long-term market share stability. Journal of Marketing Research 37: 156–72. [Google Scholar] [CrossRef]

- Gourevitch, Peter A., and James Shinn. 2007. Political Power and Corporate Control: The New Global Politics of Corporate Governance. Princeton: Princeton University Press. [Google Scholar]

- Grosfeld, Irena, and Iraj Hashi. 2007. Changes in Ownership Concentration in Mass Privatised Firms: Evidence from Poland and the Czech Republic. Corporate Governance—An International Review 15: 520–34. [Google Scholar] [CrossRef]

- Guiso, Luigi, Paola Sapienza, and Luigi Zingales. 2004. The role of social capital in financial development. American Economic Review 94: 526–56. [Google Scholar] [CrossRef] [Green Version]

- Gurevitch, Michael, and Marc R. Levy. 1985. Mass Communication Review Yearbook. Thousand Oaks: Sage. [Google Scholar]

- Hartwell, Christopher A. 2013. Institutional Barriers in the Transition to Market: Examining Performance and Divergence in Transition Economies. Basingstoke: Palgrave Macmillan. [Google Scholar]

- Hartwell, Christopher A., and Anna P. Malinowska. 2019. Informal institutions and firm valuation. Emerging Markets Review 40: 100603. [Google Scholar] [CrossRef]

- Helmke, Gretchen, and Steven Levitsky. 2004. Informal institutions and comparative politics: A research agenda. Perspectives on Politics 2: 725–40. [Google Scholar] [CrossRef] [Green Version]

- Hilgartner, Stephen, and Charles L. Bosk. 1988. The rise and fall of social problems: A public arenas model. American Journal of Sociology 94: 53–78. [Google Scholar] [CrossRef]

- Hoffman, Andrew J. 1999. Institutional evolution and change: Environmentalism and the US chemical industry. Academy of Management Journal 42: 351–71. [Google Scholar] [CrossRef] [Green Version]

- Holmes, Michael R., Toyah L. Miller, Michael A. Hitt, and Maria Paz Salmador. 2013. The interrelationships among informal institutions, formal institutions, and inward foreign direct investment. Journal of Management 39: 531–66. [Google Scholar] [CrossRef]

- Hoskisson, Robert E., Mike Wright, Igor Filatotchev, and Mike W. Peng. 2013. Emerging multinationals from mid-Range economies: The influence of institutions and factor markets. Journal of Management Studies 50: 1295–321. [Google Scholar] [CrossRef] [Green Version]

- Humphreys, Ashlee. 2010. Megamarketing: The creation of markets as a social process. Journal of Marketing 74: 1–19. [Google Scholar] [CrossRef]

- Inglehart, Ronald, and Wayne E. Baker. 2000. Modernization, cultural change, and the persistence of traditional values. American Sociological Review 65: 19–51. [Google Scholar] [CrossRef] [Green Version]

- Khanna, Tarun, and Krishna G. Palepu. 1997. Why focused strategies may be wrong for emerging markets. Harvard Business Review 75: 41–51. [Google Scholar]

- Kingston, Christopher, and Gonzalo Caballero Miguez. 2009. Comparing theories of institutional change. Journal of Institutional Economics 5: 151–80. [Google Scholar] [CrossRef] [Green Version]

- Knack, Stephen, and Philip Keefer. 1997. Does social capital have an economic payoff? A cross-country investigation. Quarterly Journal of Economics 112: 1251–88. [Google Scholar] [CrossRef]

- Kostova, Tatiana, and Kendall Roth. 2002. Adoption of an organizational practice by subsidiaries of multinational corporations: Institutional and relational effects. Academy of Management Journal 45: 215–33. [Google Scholar] [CrossRef]

- Krause, Ryan, Igor Filatotchev, and Garry D. Bruton. 2016. When in Rome, look like Cesar? Investigating the link between demand-side cultural power distance and CEO power. Academy of Management Journal 59: 1361–84. [Google Scholar] [CrossRef]

- Kwok, Chuck C. Y., and Solomon Tadesse. 2006. National culture and financial systems. Journal of International Business Studies 37: 227–47. [Google Scholar] [CrossRef] [Green Version]

- La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert W. Vishny. 1997. Legal determinants of external finance. Journal of Finance 52: 1131–50. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert W. Vishny. 1998. Law and finance. Journal of Political Economy 106: 1113–55. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert W. Vishny. 2000. Investor protection and corporate governance. Journal of Financial Economics 58: 3–27. [Google Scholar] [CrossRef] [Green Version]

- Landis, Richard J., and Gary G. Koch. 1977. The measurement of observer agreement for categorical data. Biometrics 33: 159–74. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Lee, Keun, and Byung-Yeon Kim. 2009. Both institutions and policies matter but differently for different income groups of countries: Determinants of long-run economic growth revisited. World Development 37: 533–49. [Google Scholar] [CrossRef]

- Levine, Ross, and Sara Zervos. 1998. Stock markets, banks, and economic growth. American Economic Review 88: 537–58. [Google Scholar]

- Lewellyn, Krista B., and Shuyi R. Bao. 2014. A cross-national investigation of IPO activity: The role of formal institutions and national culture. International Business Review 23: 1167–78. [Google Scholar] [CrossRef]

- Li, Jian T. 2013. The Internationalization of Entrepreneurial Firms from Emerging Economies: The Roles of Institutional Transitions and Market Opportunities. Journal of International Entrepreneurship 11: 158–71. [Google Scholar] [CrossRef]

- Lindorfer, Robert, Anne d’Arcy, and Jonas Puck. 2016. Location decisions and the liability of foreignness: Spillover effects between factor market and capital market strategies. Journal of International Management 22: 222–33. [Google Scholar] [CrossRef] [Green Version]

- Maksimov, Vladislav, Stephanie L. Wang, and Yadong Luo. 2017. Institutional imprinting, entrepreneurial agency, and private firm innovation in transition economies. Journal of World Business 52: 854–65. [Google Scholar] [CrossRef]

- McCombs, Maxwell E., and Donald L. Shaw. 1972. The agenda-setting function of mass media. Public Opinion Quarterly 36: 176–87. [Google Scholar] [CrossRef]

- Meyer, Klaus E., and Mike W. Peng. 2005. Probing theoretically into Central and Eastern Europe: Transactions, resources, and institutions. Journal of International Business Studies 36: 600–21. [Google Scholar] [CrossRef] [Green Version]

- Meyer, Renate E., and Markus A. Höllerer. 2010. Meaning structures in a contested issue field: A topographic map of shareholder value in Austria. Academy of Management Journal 53: 1241–62. [Google Scholar] [CrossRef]

- Meyer, Renate E., and Markus A. Höllerer. 2016. Laying a smoke screen: Ambiguity and neutralization as strategic responses to intra-institutional complexity. Strategic Organization 14: 373–406. [Google Scholar] [CrossRef] [Green Version]

- Moore, Curt B., R. Greg Bell, Igor Filatotchev, and Abdul A. Rasheed. 2012. Foreign IPO capital market choice: Understanding the institutional fit of corporate governance. Strategic Management Journal 33: 914–37. [Google Scholar] [CrossRef] [Green Version]

- Muthuri, Judy N., and Victoria Gilbert. 2011. An institutional analysis of corporate social responsibility in Kenya. Journal of Business Ethics 98: 467–83. [Google Scholar] [CrossRef]

- Naceur, Sami B., Bertrand Candelon, and Quentin Lajaunie. 2019. Taming financial development to reduce crises. Emerging Markets Review 40: 100618. [Google Scholar] [CrossRef] [Green Version]

- North, Douglas. 1990. Institutions, Institutional Change, and Economic Performance: Political Economy of Institutions and Decisions. Cambridge: Cambridge University Press. [Google Scholar]

- Park, Se M. 2021. The interrelation between formal and informal institutions through international trade. Review of International Economics 29: 1358–81. [Google Scholar] [CrossRef]

- Pejovich, Svetozar. 1999. The effects of the interaction of formal and informal institutions on social stability and economic development. Journal of Markets and Morality 2: 164–81. [Google Scholar]

- Peng, Mike W., Sunny L. Sun, Brian Pinkham, and Hao Chen. 2009. The institution-based view as a third leg for a strategy tripod. Academy of Management Perspectives 23: 63–81. [Google Scholar] [CrossRef] [Green Version]

- Rajan, Raghuram G., and Luigi Zingales. 2003. The great reversals: The politics of financial development in the twentieth century. Journal of Financial Economics 69: 5–50. [Google Scholar] [CrossRef]

- Redek, Tjasa, and Andrej Sušjan. 2005. The impact of institutions on economic growth: The case of transition economies. Journal of Economic Issues 39: 995–1027. [Google Scholar] [CrossRef]

- Salomon, Robert, and Zheying Wu. 2012. Institutional distance and local isomorphism strategy. Journal of International Business Studies 43: 343–67. [Google Scholar] [CrossRef]

- Sartor, Michael A., and Paul W. Beamish. 2014. Offshoring innovation to emerging markets: Organizational control and informal institutional distance. Journal of International Business Studies 45: 1072–95. [Google Scholar] [CrossRef]

- Scott, Richard W. 2008. Institutions and Organizations. Thousand Oaks: Sage. [Google Scholar]

- Shleifer, Andrei, and Daniel Wolfenzon. 2002. Investor protection and equity markets. Journal of Financial Economics 66: 3–27. [Google Scholar] [CrossRef] [Green Version]

- Slangen, Arjen H. L., and Rob J. M. van Tulder. 2009. Cultural distance, political risk, or governance quality? Towards a more accurate conceptualization and measurement of external uncertainty in foreign entry mode research. International Business Review 18: 276–91. [Google Scholar] [CrossRef]

- Smaoui, Houcem, Martin Grandes, and Akintoye Akindele. 2017. Determinants of Bond Market Development: Further Evidence from Emerging and Developed Countries. Emerging Markets Review 32: 148–67. [Google Scholar] [CrossRef]

- Suchman, Mark C. 1995. Managing legitimacy: Strategic and institutional approaches. Academy of Management Review 20: 571–610. [Google Scholar] [CrossRef]

- Tanas, Janusz K., and David B. Audretsch. 2011. Entrepreneurship in transitional economy. International Entrepreneur Management Journal 7: 431–42. [Google Scholar] [CrossRef]

- Tupper, Christina, Orhun Guldiken, and Mirko Benischke. 2018. Capital market liability of foreignness of IPO firms. Journal of World Business 53: 555–67. [Google Scholar] [CrossRef]

- Weber, Robert P. 1990. Basic Content Analysis. Newbury Park: Sage. [Google Scholar]

- Williamson, Oliver E. 1991. Comparative economic organization: The analysis of discrete structural alternatives. Administrative Science Quarterly 36: 269–96. [Google Scholar] [CrossRef] [Green Version]

- Williamson, Oliver E. 2000. The New Institutional Economics: Taking Stock, Looking Ahead. Journal of Economic Literature 38: 595–613. [Google Scholar] [CrossRef] [Green Version]

- Wrona, Thomas, Tina Ladwig, and Markus Gunnesch. 2013. Socio-cognitive processes in strategy formation: A conceptual framework. European Management Journal 31: 697–705. [Google Scholar] [CrossRef]

- Zajac, Edward J., and James D. Westphal. 2004. The social construction of market value: Institutionalization and learning perspectives on stock market reactions. American Sociological Review 69: 433–57. [Google Scholar] [CrossRef] [Green Version]

- Zilber, Tammar B. 2006. The work of the symbolic in institutional processes: Translations of rational myths in Israeli high tech. Academy of Management Journal 49: 281–303. [Google Scholar] [CrossRef]

- Zucker, Lynne G. 1987. Institutional theories of organization. Annual Review of Sociology 13: 443–64. [Google Scholar] [CrossRef]

| Variable | Definition |

|---|---|

| Equity market size | Equity market capitalization as a share of real GDP per year (base year 2005) |

| Public perception of capital markets | Janis–Fadner coefficient of coded newspaper articles from Factiva database |

| Economic freedom | Heritage Foundation’s Index of Economic Freedom 2014 edition |

| Income | Real GDP per capita in constant EUR thousandth (base year 2005) |

| Inflation | Change in consumer price index (base year 2005) in percent |

| Country dummy | Country dummy with Austria = 0; Poland = 1 |

| Full Sample (n = 74) | Austria (n = 37) | Poland (n = 37) | t-Tests | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | S.D. | Min | Max | Mean | S.D. | Min | Max | Mean | S.D. | Min | Max | ||

| Equity market size | 32.86 | 10.95 | 16.27 | 60.54 | 34.30 | 12.82 | 19.36 | 60.54 | 31.41 | 8.62 | 16.27 | 50.46 | 1.24 *** |

| Public perception of capital markets | 0.30 | 0.27 | −0.34 | 0.79 | 0.16 | 0.26 | −0.34 | 0.69 | 0.44 | 0.19 | 0.06 | 0.79 | −5.19 *** |

| Economic freedom | 65.71 | 5.20 | 58.10 | 71.90 | 70.53 | 1.47 | 67.60 | 71.90 | 60.89 | 2.22 | 58.10 | 64.20 | 22.03 *** |

| Income | 4.80 | 2.99 | 1.50 | 8.10 | 7.76 | 0.28 | 7.20 | 8.10 | 1.84 | 0.20 | 1.50 | 2.10 | 103.89 *** |

| Inflation | 0.66 | 0.64 | −0.64 | 2.49 | 0.55 | 0.50 | −0.45 | 1.97 | 0.77 | 0.74 | −0.34 | 2.49 | −1.46 |

| 1 | 2 | 3 | 4 | 5 | ||||

|---|---|---|---|---|---|---|---|---|

| 1 Equity market size | 1 | |||||||

| 2 Public perception of capital markets | 0.4775 | *** | 1 | |||||

| 3 Economic freedom | 0.1560 | −0.5219 | *** | 1 | ||||

| 4 Income | 0.1422 | −0.5340 | *** | 0.9518 | *** | 1 | ||

| 5 Inflation | −0.0394 | 0.1133 | −0.1497 | −0.1602 | 1 |

| Equity Market Size | ||||||||

|---|---|---|---|---|---|---|---|---|

| Model 1a | Model 1b | Model 2 | Model 3 | |||||

| Independent variables | ||||||||

| H1: Public perception of capital markets | 4.7958 | ** | 5.4003 | ** | 5.2572 | ** | 12.3374 | *** |

| Economic freedom | 1.5171 | *** | 1.5911 | *** | 1.1307 | *** | 1.4272 | *** |

| 2-way interaction terms | ||||||||

| H2: Economic freedom x Public perception of capital markets | 1.8491 | *** | ||||||

| H3: Country dummy x Public perception of capital markets | −14.2853 | +++ | ||||||

| Control variables | ||||||||

| Income | −0.1489 | |||||||

| Inflation | −0.1536 | |||||||

| Country dummy | 10.2819 | *** | 9.9745 | 6.3877 | * | 9.1921 | ** | |

| Time dummies | YES | YES | YES | YES | ||||

| Wald-Chi2 | 554.80 | *** | 565.19 | *** | 812.70 | *** | 693.25 | *** |

| R2 | 0.8701 | 0.8722 | 0.9080 | 0.8938 | ||||

| Change in R2 | 0.0021 | 0.0379 | 0.0237 | |||||

| Observations (n) | 74 | 74 | 74 | 74 | ||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lindorfer, R.; d’Arcy, A.; Filatotchev, I. When Institutional Plates Collide: The Dynamic Impact of Informal Institutions on Capital Market Development. J. Risk Financial Manag. 2023, 16, 178. https://doi.org/10.3390/jrfm16030178

Lindorfer R, d’Arcy A, Filatotchev I. When Institutional Plates Collide: The Dynamic Impact of Informal Institutions on Capital Market Development. Journal of Risk and Financial Management. 2023; 16(3):178. https://doi.org/10.3390/jrfm16030178

Chicago/Turabian StyleLindorfer, Robert, Anne d’Arcy, and Igor Filatotchev. 2023. "When Institutional Plates Collide: The Dynamic Impact of Informal Institutions on Capital Market Development" Journal of Risk and Financial Management 16, no. 3: 178. https://doi.org/10.3390/jrfm16030178

APA StyleLindorfer, R., d’Arcy, A., & Filatotchev, I. (2023). When Institutional Plates Collide: The Dynamic Impact of Informal Institutions on Capital Market Development. Journal of Risk and Financial Management, 16(3), 178. https://doi.org/10.3390/jrfm16030178