Two Types of Payments of Tax on Profit: Advanced Payments and at the End of Periods: Consideration within BFO Theory with Variable Profit

Abstract

:1. Introduction

1.1. A Literature Review

1.2. Methods and Materials

2. The BFO Theory for Companies with Variable Profit and Advance Tax on Profit Payments

2.1. The Value of a Financially Dependent Company, V

2.2. The Value of a Financially Independent Company, V0

2.3. The Tax Shield Value, TS

3. Results and Discussions

3.1. Calculations of the Equity Cost, ke

- Higher growth rate, g, justifies higher dividends.

- If a company pays income tax at the end of periods, it must pay large dividends.

- If the company pays income tax in advance, dividends should be lower.

3.2. Impact of kd on Financial Indicators

3.2.1. WACC

3.2.2. The Discount Rate, WACC–g

3.2.3. The Company Value, V

3.3. Influence of Company Age, n, on Main Financial Parameters of the Company

3.3.1. WACC(L)

3.3.2. Discount Rate WACC–g

3.3.3. Company Capitalization, V

3.3.4. Equity Cost, ke

3.3.5. Summary of Results

- -

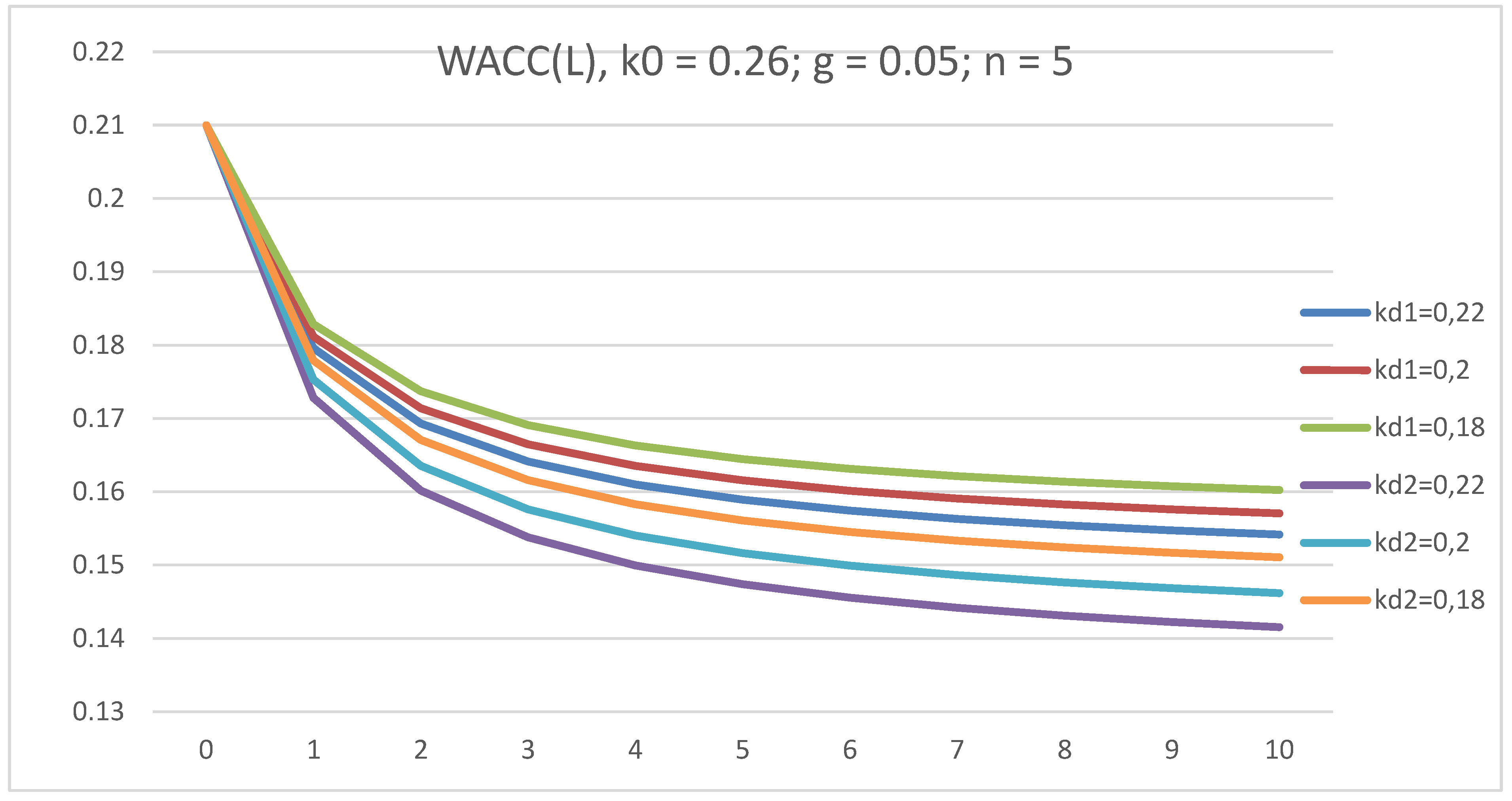

- All curves, WACC(L), start from one point (0; 0.26) at all values of kd. WACC(L) at all values of kd decrease with leverage level L. WACC(L) decrease with kd. This means that tax shield leads to the decrease of the cost of raising capital.

- -

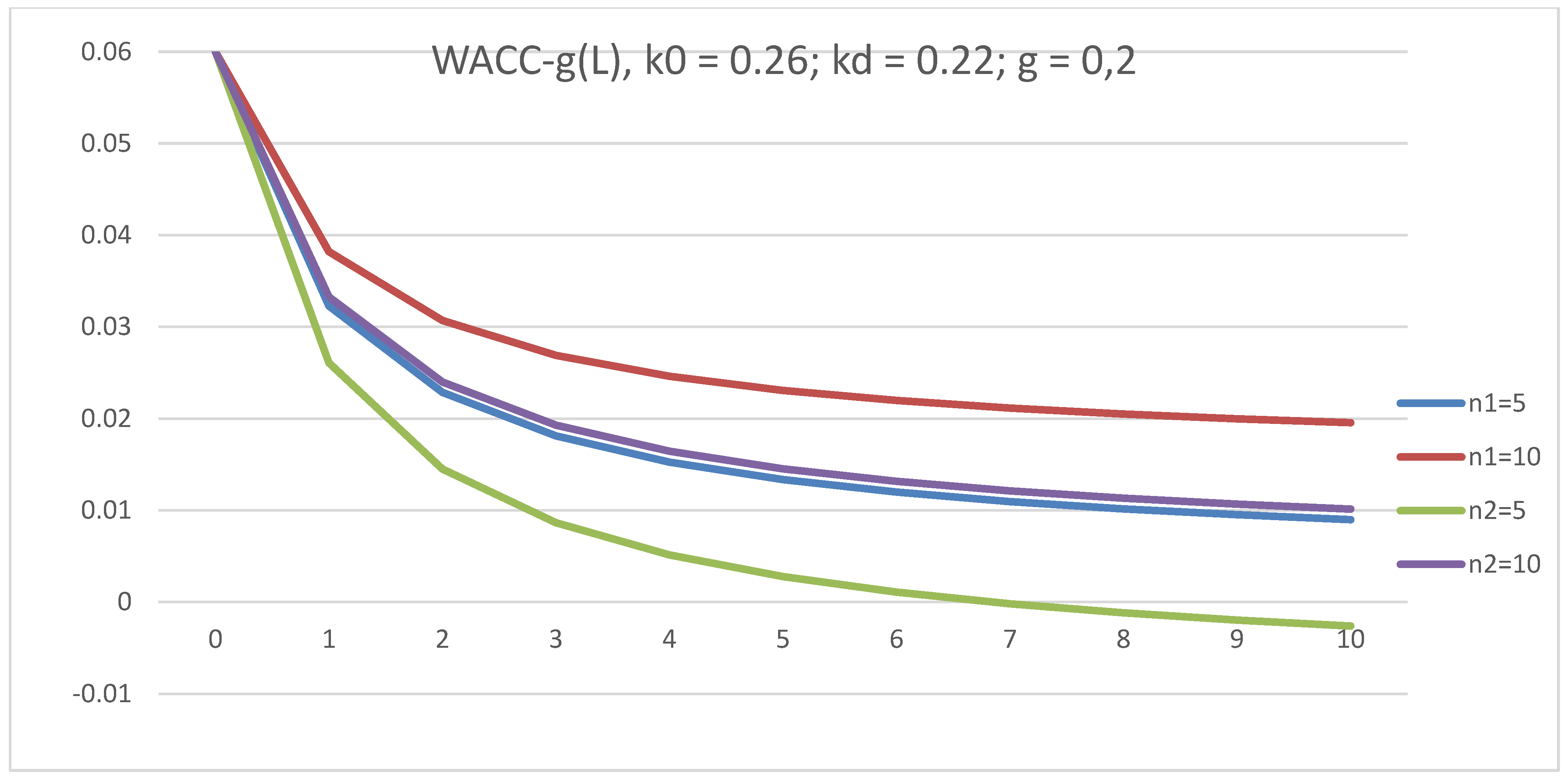

- All curves, (WACC–g)(L), start from one point (0; 0.21) at all values of kd. At all values of kd, (WACC–g)(L) decrease with L. With the increase of debt cost, kd, (WACC–g)(L) decrease. Thus, the tax shield tends to lower the value of the discount rate (WACC–g) and, hence, increase the value of the company, V.

- -

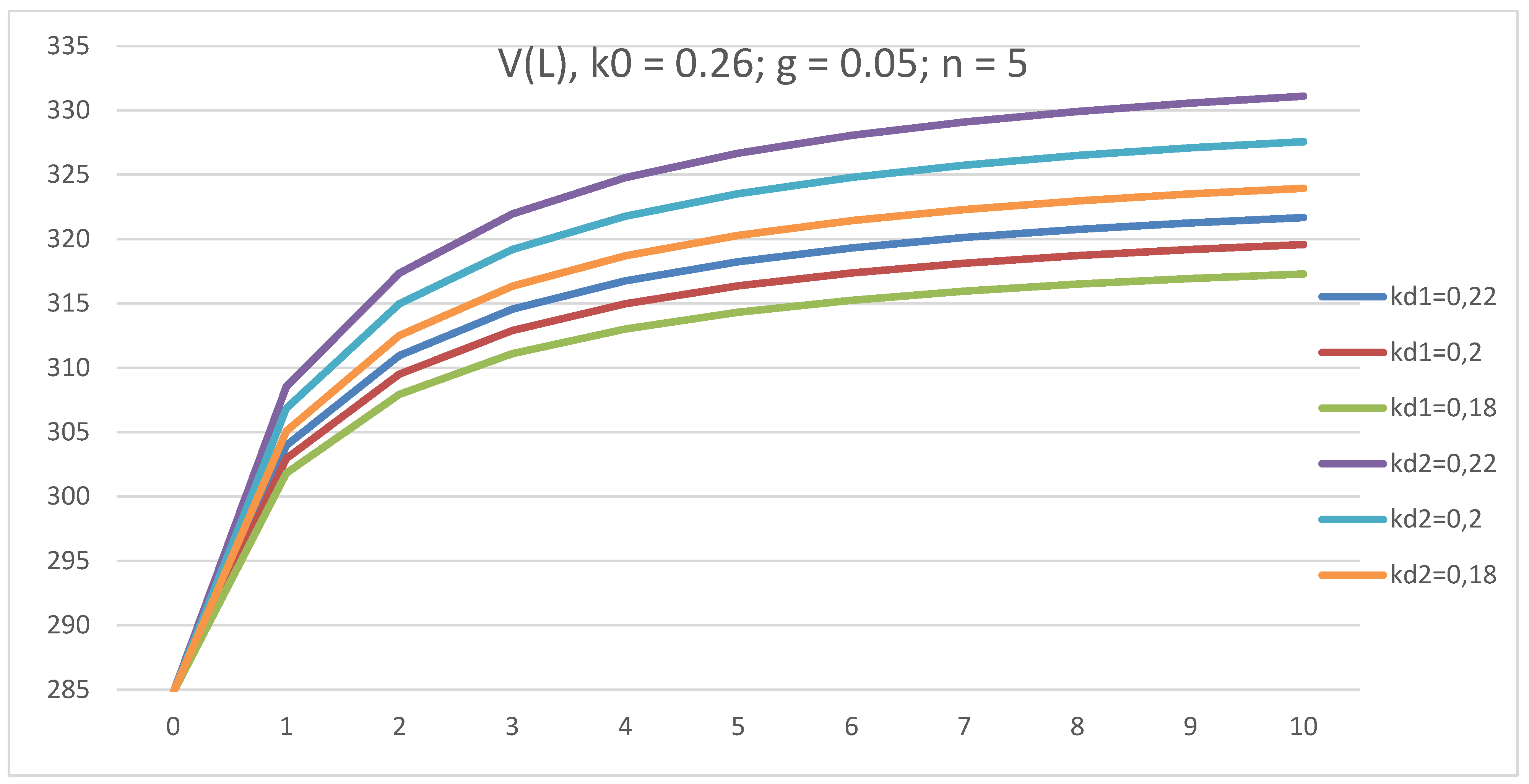

- At all values of kd all curves of the company value V(L) start from one point (0; 285) and increases with leverage level L. V(L) increases with kd. Thus, the tax shield leads to the increase of the company value, V.

- -

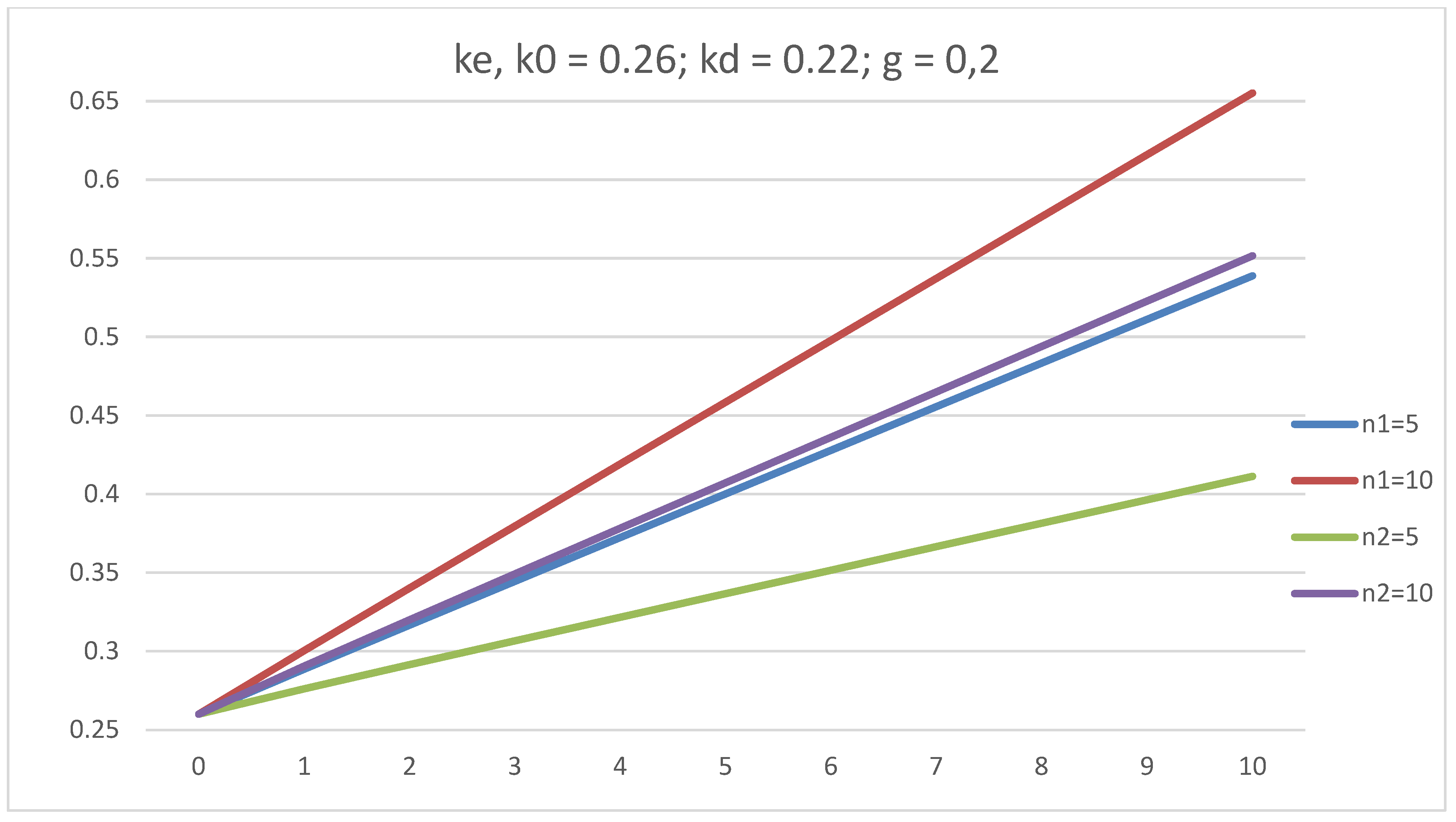

- At all values of kd, all curves of equity cost, ke(L), start from one point (0; 0.26) and increase with L. The slope of ke(L) decreases with kd. Thus, kd impacts the dividend policy of the company, because ke determines the economically justified amount of dividends.

4. Conclusions

- The generalization of the BFO theory for the case of variable income with advance payments of income tax.

- Generalized BFO formulas for the main financial parameters of the company have been derived.

- Using the obtained formulas, an investigation of the influence of the growth rate, g; the cost of debt, kd; and the company’s age, n, on the dependence of the company’s financial performance on debt financing, has been conducted.

- A comparison of the obtained results with those for the case of paying income tax at the end of the periods has been performed.

- The development of the recommendations for both companies and regulators on how to pay income tax has been created.

- The developed methodology makes it possible to study companies with growing profits and companies with decreasing profits, which is quite important in practice. Regarding the direction of future research, the proposed theory will be used in the future for a more detailed study of companies with both rising and falling profits.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Angotti, M., R. de Lacerda Moreira, J. Hipólito Bernardes do Nascimento, and O. Neto de Almeida Bispo. 2018. Analysis of an equity investment strategy based on accounting and financial reports in Latin American markets. Reficont 5: 22–40. [Google Scholar]

- Barbi, Massimiliano. 2011. On the risk-neutral value of debt tax shields. Applied Financial Economics 22: 251–58. [Google Scholar] [CrossRef]

- Batrancea, Larissa. 2021a. An Econometric Approach Regarding the Impact of Fiscal Pressure on Equilibrium: Evidence from Electricity, Gas and Oil Companies Listed on the New York Stock Exchange. Mathematics 9: 630. [Google Scholar] [CrossRef]

- Batrancea, Larissa. 2021b. The Influence of Liquidity and Solvency on Performance within the Healthcare Industry: Evidence from Publicly Listed Companies. Mathematics 9: 2231. [Google Scholar] [CrossRef]

- Becker, Denis Mike. 2022. Getting the valuation formulas right when it comes to annuities. Managerial Finance 48: 470–99. [Google Scholar] [CrossRef]

- Berk, Jonathan, and Peter De Marzo. 2017. Corporate Finance. Boston: Pearson–Addison Wesley. [Google Scholar]

- Brusov, Peter, and Tatiana Filatova. 2022. Generalization of the Brusov–Filatova–Orekhova Theory for the Case of Variable Income. Mathematics 10: 3661. [Google Scholar] [CrossRef]

- Brusov, Peter, Tatiana Filatova, Natali Orekhova, and Mukhadin Eskindarov. 2018. Modern Corporate Finance, Investments, Taxation and Ratings, 2nd ed. Cham: Springer Nature Publishing, pp. 1–571. [Google Scholar]

- Brusov, Peter, Tatiana Filatova, Natali Orekhova, Veniamin Kulik, She-I. Chang, and George Lin. 2021. Generalization of the Modigliani–Miller Theory for the Case of Variable Profit. Mathematics 9: 1286. [Google Scholar] [CrossRef]

- Brusov, Peter, Tatiana Filatova, and Veniamin Kulik. 2023. BFO Theory with Variable Profit in Case of Advance Payments of Tax on Profit. Journal of Reviews on Global Economics 12: 1–17. [Google Scholar] [CrossRef]

- Dimitropoulos, Panagiotis. 2014. Capital structure and corporate governance of soccer clubs: European evidence. Management Research Review 37: 658–78. [Google Scholar] [CrossRef]

- El-Chaarani, Hani, Rebecca Abraham, and Yahya Skaf. 2022. The Impact of Corporate Governance on the Financial Performance of the Banking Sector in the MENA (Middle Eastern and North African) Region: An Immunity Test of Banks for COVID-19. Journal of Risk and Financial Management 15: 82. [Google Scholar] [CrossRef]

- Farber, André, Roland L. Gillet, and Ariane Szafarz. 2006. A General Formula for the WACC. International Journal of Business 11: 211–18. [Google Scholar]

- Fernandez, Pablo. 2006. A General Formula for the WACC: A Comment. International Journal of Business 11: 219. [Google Scholar]

- Franc-Dąbrowska, Justyna, Magdalena Mądra-Sawicka, and Anna Milewska. 2021. Energy Sector Risk and Cost of Capital Assessment—Companies and Investors Perspective. Energies 14: 1613. [Google Scholar] [CrossRef]

- Hamada, Robert. 1969. Portfolio Analysis, Market Equilibrium, and Corporate Finance. Journal of Finance 24: 13–31. [Google Scholar] [CrossRef]

- Harris, Robert S., and John J. Pringle. 1985. Risk-adjusted discount rates-extensions from the average-risk case. Journal of Financial Research 8: 237–44. [Google Scholar] [CrossRef]

- Huang, Song, Huixia Sun, Huimin Zhao, and Yuening Zhang. 2020. Influence of leverage on the return on equity. Systems Engineering—Theory & Practice 40: 355. [Google Scholar]

- Islam, Silvia Z., and Sarod Khandaker. 2015. Firm leverage decisions: Does industry matter? The North American Journal of Economics and Finance 31: 94. [Google Scholar] [CrossRef]

- Luiz, K., and M. Cruz. 2015. The relevance of capital structure on firm performance: A multivariate analysis of publicly traded Brazilian companies. REPeC Brasília 9: 384–401. [Google Scholar]

- Miller, Merton H. 1977. Debt and taxes. The Journal of Finance 32: 261–75. [Google Scholar]

- Modigliani, Franco, and Merton H. Miller. 1958. The cost of capital, corporate finance, and the theory of investment. The American Economic Review 48: 261–97. [Google Scholar]

- Modigliani, Franco, and Merton H. Miller. 1963. Corporate income taxes and the cost of capital: A correction. The American Economic Review 53: 147–75. [Google Scholar]

- Modigliani, Franco, and Merton H. Miller. 1966. Some estimates of the cost of capital to the electric utility industry 1954–57. American Economic Review 56: 333–91. [Google Scholar]

- Mundi, Hardeep Singh, Parmjit Kaur, and R. L. N. Murty. 2021. A qualitative inquiry into the capital structure decisions of overconfident finance managers of family-owned businesses in India. Qualitative Research in Financial Markets 14: 357–79. [Google Scholar] [CrossRef]

- Myers, Stewart C. 2001. Capital structure. Journal of Economic Perspectives 15: 81–102. [Google Scholar] [CrossRef] [Green Version]

- Pavel, Zhukov. 2018. The Impact of Cash Flows and Weighted Average Cost of Capital to Enterprise Value in the Oil and Gas Sector. Journal of Reviews on Global Economics 7: 138–45. [Google Scholar] [CrossRef]

- Sadiq, Muhammad, Sami Alajlani, Muhammed Sajjad Hussain, Rashid Ahmad, Furrukh Bashir, and Supat Chupradit. 2021. Impact of credit, liquidity, and systematic risk on financial structure: Comparative investigation from sustainable production. Environmental Science and Pollution Research 29: 20963–75. [Google Scholar] [CrossRef]

- Singhal, Nikita, Shikha Goyal, Divya Sharma, Sapna Kumari, and Shweta Nagar. 2022. Capitalization and profitability: Applicability of capital theories in BRICS banking sector. Future Business Journal 8: 1–13. [Google Scholar] [CrossRef]

- Vergara-Novoa, Cristian, Juan Pedro Sepúlveda-Rojas, Miguel D. Alfaro, and Nicolás Riveros. 2018. Cost of Capital Estimation for Highway Concessionaires in Chile. Journal of Advanced Transportation 2153536. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| g Growth Rate | kd Debt Cost | n Company Age | Comparison of (1) and (2) | |||||

|---|---|---|---|---|---|---|---|---|

| Payments at the Ends of Periods (1) | Advance Payments (2) | Payments at the Ends of Periods (1) | Advance Payments (2) | Payments at the Ends of Periods (1) | Advance Payments (2) | |||

| WACC | ↑ | ↑ | ↓ | ↓ | g ≥ 0 | ↑ | ↑ | 1 ≥ 2 |

| g ≤ 0 | ↓ | ↓ | ||||||

| WACC–g | ↓ | ↓ | ↓ | ↓ | g ≥ 0 | ↑ | ↑ | 1 ≥ 2 |

| g ≤ 0 | ↓ | ↓ | ||||||

| V | ↑ | ↑ | ↑ | ↑ | g ≥ 0 | ↑ | ↑ | 1 ≤ 2 |

| g ≤ 0 | ↑ | ↑ | ||||||

| ke | ↑ | ↑ | ↓ | ↓ | g ≥ 0 | ↑ | ↑ | 1 ≤ 2 |

| g ≤ 0 | ↓ | ↓ | ||||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Brusov, P.; Filatova, T.; Kulik, V. Two Types of Payments of Tax on Profit: Advanced Payments and at the End of Periods: Consideration within BFO Theory with Variable Profit. J. Risk Financial Manag. 2023, 16, 208. https://doi.org/10.3390/jrfm16030208

Brusov P, Filatova T, Kulik V. Two Types of Payments of Tax on Profit: Advanced Payments and at the End of Periods: Consideration within BFO Theory with Variable Profit. Journal of Risk and Financial Management. 2023; 16(3):208. https://doi.org/10.3390/jrfm16030208

Chicago/Turabian StyleBrusov, Peter, Tatiana Filatova, and Veniamin Kulik. 2023. "Two Types of Payments of Tax on Profit: Advanced Payments and at the End of Periods: Consideration within BFO Theory with Variable Profit" Journal of Risk and Financial Management 16, no. 3: 208. https://doi.org/10.3390/jrfm16030208

APA StyleBrusov, P., Filatova, T., & Kulik, V. (2023). Two Types of Payments of Tax on Profit: Advanced Payments and at the End of Periods: Consideration within BFO Theory with Variable Profit. Journal of Risk and Financial Management, 16(3), 208. https://doi.org/10.3390/jrfm16030208