Equity Investment Decisions of Operating Firms: Evidence from Property and Liability Insurers

Abstract

:1. Introduction

2. Previous Literature and Research Questions

3. Methodology

3.1. The Effects of ICMs and the Outsourcing Option

3.2. Quit Decisions

+ Controlsi,t (Firm, External Market) + Fixed_Yeart + Fixed_Statei,t

4. Data

5. Empirical Analysis: Participation and Volume Decisions

5.1. Univariate Analysis

5.2. Time-Series Analysis

5.3. Multivariate Analysis

5.3.1. Pure Equity Investment Incentives: Equity Investments on Unaffiliated Firms

5.3.2. The Effects of ICMs: Equity Investments in both Affiliated and Unaffiliated Firms

5.3.3. The Effects of the Outsourcing Option: Equity Investments Only on Mutual Funds

6. Empirical Analysis: Quit Decisions

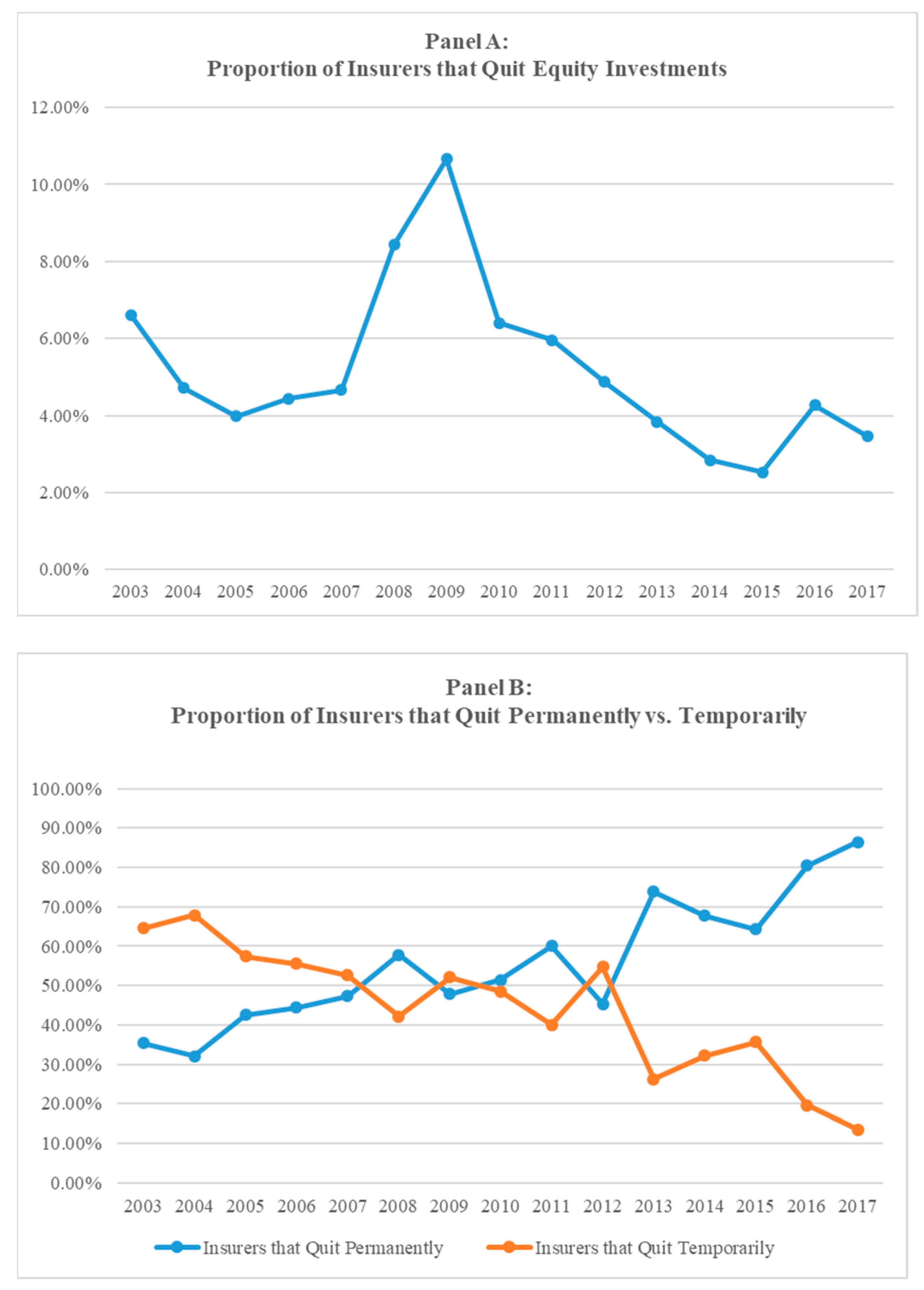

6.1. Time-Series and Univariate Analyses

6.2. Multivariate Analysis

7. Discussion and Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

| 1. | |

| 2. | For reference, hedge funds liquidated about 29% of their aggregate portfolio in 2008: Q3–Q4 (Ben-David et al. 2012). |

| 3. | Ge and Weisbach (2020) report that property and liability (also termed property and casualty) insurers held invested assets worth USD 6.5 trillion at the end of 2017, 30% of the total US assets held by endowments, foundations, pension funds, and insurance companies in the same year. |

| 4. | In insurance jargon, this is called the “float”. |

| 5. | The fraction of equity investing P&L insurers in this study’s sample fluctuates from 52.10% to 62.74%. The sample reports lower ratios in more recent years. |

| 6. | More than two thirds of the P&L insurers are affiliated, thus providing an ideal setting to study the potential impact of ICMs on equity investment decisions. |

| 7. | P&L insurers of this study’s sample invest on average about 3.29% of their total investments in affiliated firms in the form of equity investments, where the total equity investments take up about 11.87% of the total investments. Therefore, approximately 27.69% of P&L insurers’ equity investments are actually executed via ICMs in the form of capital contributions. Among the equity investments in affiliates, the vast majority of funds are invested in privately traded affiliates and proportions of publicly traded stocks are trivial. |

| 8. | The term “pure” is used in order to differentiate P&L insurers’ motivations to invest in equity investments from the work of ICMs, capital contributions, which are also recorded as equity investments. Pure equity investments denote equity investments in unaffiliated firms. |

| 9. | Rauh (2009) studies the asset allocation of defined benefit pension and finds that risk management theory plays a considerably larger role than risk shifting theory in explaining variation in pension fund investment policy. Almeida et al. (2011) also show that firms may reduce rather than increase risk when leverage increases exogenously, thus supporting risk management theory but not risk shifting theory. |

| 10. | Che and Liebenberg (2017) find that multi-line (more diversified) insurers invest more in risky assets than do single-line (less diversified) insurers, providing supporting evidence for the coordinated risk management theory, but not for risk management theory. Moreover, McShane et al. (2012) test and document evidence for the coordinated risk management theory, reporting that insurers hedge investment risk using derivatives, while simultaneously increasing underwriting risk. |

| 11. | This study’s sample reports that P&L insurers invest on average 39.40% of their funds on government bonds that include municipal bonds, while they invest 17.56% and 10.86% on corporate bonds and equity, respectively. The fraction decreased to 35.17% in 2018, arguably due to the low market interest rates. |

| 12. | Lian et al. (2019) demonstrate that individual investors have a greater appetite for risk-taking when interest rates are low. |

| 13. | Prior studies document a wide range of determinants of ICMs, such as group financial constraints and status, product market competition, risk sharing, and growth prospects. See for example, Almeida et al. (2015), Kuppuswamy and Villalonga (2016), Gopalan and Xie (2011), Matvos and Seru (2014), Campello (2002), Maksimovic and Phillips (2008), Belenzon and Berkovitz (2010). In the insurance literature, Powell et al. (2008) provide supporting evidence that P&L insurance firms used internal capital markets to transfer capital to the affiliated firms with the best investment opportunities. However, Niehaus (2018) finds that insurance groups provide a risk-sharing mechanism for life insurers. Moreover, Chiang (2020) finds that life insurers with bank affiliates use internal capital market to reallocate resources to weaker divisions. Most recently, Fier and Liebenberg (2023) show that P&L insurers use internal capital markets to manage the risk of regulatory scrutiny. |

| 14. | Guiso et al. (2018) state that the distribution of wealth and background risks of investors can initiate different changes in their risk aversion. |

| 15. | For further details, refer to Wooldridge (2010, pp. 692–94). |

| 16. | Under the “summary investment schedule” in the statutory annual statements, equity investments are reported as following, 3.1 Investments in mutual funds, 3.2 Preferred stocks (3.21 Affiliated, 3.22 Unaffiliated), 3.3 Publicly traded equity securities (excluding preferred stocks) (3.31 Affiliated, 3.32 Unaffiliated), 3.4 Other equity securities (3.41 Affiliated, 3.42 Unaffiliated), 3.5 Other equity interests, including tangible personal property under lease (3.51 Affiliated, 3.52 Unaffiliated). |

| 17. | Due to lack of within variation, firm fixed effects to be conditioned out of likelihood do not exist. The reported random effects model results are robust to the pooled regression model that is clustered at firm level. The analysis controls for unobservable year and state effects and it is conducted at the insurers’ level. |

| 18. | The initial sample comprises 2717 different firms, on average, per year and 46,182 total firm-year observations over the entire sample period. |

| 19. | The line diversification calculation is, |

| 20. | As in the line of business diversification, the geographical diversification measure is calculated as: |

| 21. | Following Phillips et al. (1998), long-tail lines consist of Farm Owners Multiple Peril, Homeowners Multiple Peril, Commercial Multiple Peril, Ocean Marine, Medical Professional Liability, Workers’ Compensation, Other Liability, Product Liability, Automobile Liability, Aircraft, Boiler and Machinery, International, and Reinsurance. |

| 22. | The E_Affiliated mean of 3.286 divided by the E_Total mean of 11.868. |

References

- Almeida, Heitor, Chang-Soo Kim, and Hwanki Brian Kim. 2015. Internal capital markets in business groups: Evidence from the Asian financial crisis. Journal of Finance 70: 2539–86. [Google Scholar] [CrossRef]

- Almeida, Heitor, Murillo Campello, and Michael S. Weisbach. 2011. Corporate financial and investment policies when future financing is not frictionless. Journal of Corporate Finance 17: 675–93. [Google Scholar] [CrossRef] [Green Version]

- Andersen, Steffen, Tobin Hanspal, and Kasper Meisner Nielsen. 2019. Once bitten, twice shy: The power of personal experiences in risk taking. Journal of Financial Economics 132: 97–117. [Google Scholar] [CrossRef]

- Andonov, Aleksandar, Rob M. M. J. Bauer, and K. J. Martijn Cremers. 2017. Pension fund asset allocation and liability discount rates. Review of Financial Studies 30: 2555–95. [Google Scholar] [CrossRef]

- Belenzon, Sharon, and Tomer Berkovitz. 2010. Innovation in business groups. Management Science 56: 519–35. [Google Scholar] [CrossRef] [Green Version]

- Ben-David, Itzhak, Francesco Franzoni, and Rabih Moussawi. 2012. Hedge Fund Stock Trading in the Financial Crisis of 2007–2009. Review of Financial Studies 25: 1–54. [Google Scholar] [CrossRef] [Green Version]

- Berry-Stölzle, Thomas R., Andre P. Liebenberg, Joseph S. Ruhland, and David W. Sommer. 2012. Determinants of corporate diversification: Evidence from the property–liability insurance industry. Journal of Risk and Insurance 79: 381–413. [Google Scholar] [CrossRef]

- Campello, Murillo. 2002. Internal capital markets in financial conglomerates: Evidence from small bank responses to monetary policy. Journal of Finance 57: 2773–805. [Google Scholar] [CrossRef]

- Che, Xin, and Andre P. Liebenberg. 2017. Effects of business diversification on asset risk-taking: Evidence from the US property-liability insurance industry. Journal of Banking & Finance 77: 122–36. [Google Scholar]

- Chernenko, Sergey, Samuel G. Hanson, and Adi Sunderam. 2016. Who neglects risk? Investor experience and the credit boom. Journal of Financial Economics 122: 248–69. [Google Scholar] [CrossRef]

- Chiang, Chia-Chun. 2020. Does Having an Affiliated Bank Improve Life Insurer Performance in a Turbulent Market? Journal of Risk and Insurance 87: 627–64. [Google Scholar] [CrossRef]

- Chiang, Yao-Min, David Hirshleifer, Yiming Qian, and Ann E. Sherman. 2011. Do investors learn from experience? Evidence from frequent IPO investors. Review of Financial Studies 24: 1560–89. [Google Scholar] [CrossRef] [Green Version]

- Chodorow-Reich, Gabriel. 2014. Effects of Unconventional Monetary Policy on Financial Institutions. No. w20230. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Choi, Jaewon, and Mathias Kronlund. 2018. Reaching for yield in corporate bond mutual funds. Review of Financial Studies 31: 1930–65. [Google Scholar] [CrossRef]

- Colquitt, L. Lee, David W. Sommer, and Norman H. Godwin. 1999. Determinants of cash holding by property-liability insurers. Journal of Risk and Insurance 66: 401–15. [Google Scholar] [CrossRef]

- Cragg, John G. 1971. Some statistical models for limited dependent variables with application to the demand for durable goods. Econometrica: Journal of the Econometric Society 39: 829–44. [Google Scholar] [CrossRef]

- Cummins, J. David, Richard D. Phillips, and Stephen D. Smith. 2001. Derivatives and corporate risk management: Participation and volume decisions in the insurance industry. Journal of Risk and Insurance 68: 51–91. [Google Scholar] [CrossRef] [Green Version]

- Di Maggio, Marco, and Marcin Kacperczyk. 2017. The unintended consequences of the zero lower bound policy. Journal of Financial Economics 123: 59–80. [Google Scholar] [CrossRef] [Green Version]

- Fier, Stephen G., and Andre P. Liebenberg. 2023. Do Insurers Use Internal Capital Markets to Manage Regulatory Scrutiny Risk? Available online: https://ssrn.com/abstract=4324199 (accessed on 5 March 2023).

- Froot, Kenneth A., David S. Scharfstein, and Jeremy C. Stein. 1993. Risk management: Coordinating corporate investment and financing policies. Journal of Finance 48: 1629–58. [Google Scholar] [CrossRef] [Green Version]

- Ge, Shan, and Michael S. Weisbach. 2020. The Role of Financial Conditions in Portfolio Choices: The Case of Insurers. Journal of Financial Economics 142: 803–30. [Google Scholar] [CrossRef]

- Gopalan, Radhakrishnan, and Kangzhen Xie. 2011. Conglomerates and industry distress. Review of Financial Studies 24: 3642–87. [Google Scholar] [CrossRef]

- Guiso, Luigi, Paola Sapienza, and Luigi Zingales. 2018. Time varying risk aversion. Journal of Financial Economics 128: 403–21. [Google Scholar] [CrossRef] [Green Version]

- Hanson, Samuel G., and Jeremy C. Stein. 2015. Monetary policy and long-term real rates. Journal of Financial Economics 115: 429–48. [Google Scholar] [CrossRef] [Green Version]

- Hertwig, Ralph, Greg Barron, Elke U. Weber, and Ido Erev. 2004. Decisions from experience and the effect of rare events in risky choice. Psychological Science 15: 534–39. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Jiménez, Gabriel, Steven Ongena, José-Luis Peydró, and Jesús Saurina. 2014. Hazardous times for monetary policy: What do twenty-three million bank loans say about the effects of monetary policy on credit risk-taking? Econometrica 82: 463–505. [Google Scholar]

- Kim, Ryoonhee. 2016. Financial weakness and product market performance: Internal capital market evidence. Journal of Financial and Quantitative Analysis 51: 1–26. [Google Scholar] [CrossRef]

- Knüpfer, Samuli, Elias Rantapuska, and Matti Sarvimäki. 2017. Formative experiences and portfolio choice: Evidence from the Finnish great depression. Journal of Finance 72: 133–66. [Google Scholar] [CrossRef]

- Kuppuswamy, Venkat, and Belén Villalonga. 2016. Does diversification create value in the presence of external financing constraints? Evidence from the 2007–2009 financial crisis. Management Science 62: 905–23. [Google Scholar] [CrossRef] [Green Version]

- Lian, Chen, Yueran Ma, and Carmen Wang. 2019. Low interest rates and risk-taking: Evidence from individual investment decisions. Review of Financial Studies 32: 2107–48. [Google Scholar] [CrossRef] [Green Version]

- Maddaloni, Angela, and José-Luis Peydró. 2011. Bank risk-taking, securitization, supervision, and low interest rates: Evidence from the Euro-area and the US lending standards. Review of Financial Studies 24: 2121–65. [Google Scholar] [CrossRef] [Green Version]

- Maksimovic, Vojislav, and Gordon Phillips. 2008. The industry life cycle, acquisitions and investment: Does firm organization matter? Journal of Finance 63: 673–708. [Google Scholar] [CrossRef]

- Malmendier, Ulrike, and Stefan Nagel. 2011. Depression babies: Do macroeconomic experiences affect risk taking? Quarterly Journal of Economics 126: 373–416. [Google Scholar] [CrossRef] [Green Version]

- Malmendier, Ulrike, Demian Pouzo, and Victoria Vanasco. 2020. Investor experiences and financial market dynamics. Journal of Financial Economics 136: 597–622. [Google Scholar] [CrossRef] [Green Version]

- Matvos, Gregor, and Amit Seru. 2014. Resource allocation within firms and financial market dislocation: Evidence from diversified conglomerates. Review of Financial Studies 27: 1143–89. [Google Scholar] [CrossRef]

- McShane, Michael K., Tao Zhang, and Larry A. Cox. 2012. Risk allocation across the enterprise: Evidence from the insurance industry. Journal of Insurance Issues 35: 73–99. [Google Scholar] [CrossRef] [Green Version]

- Niehaus, Greg. 2018. Managing capital via internal capital market transactions: The case of life insurers. Journal of Risk and Insurance 85: 69–106. [Google Scholar] [CrossRef]

- Nisbett, Richard E., and Lee Ross. 1980. Human Inference: Strategies and Shortcomings of Social Judgment. Englewood Cliffs: Prentice Hall. [Google Scholar]

- Phillips, Richard D., J. David Cummins, and Franklin Allen. 1998. Financial Pricing of Insurance in the Multiple Line Insurance Company. Journal of Risk and Insurance 65: 597–636. [Google Scholar] [CrossRef] [Green Version]

- Pottier, Steven W. 2007. The determinants of private debt holdings: Evidence from the life insurance industry. Journal of Risk and Insurance 74: 591–612. [Google Scholar] [CrossRef]

- Powell, Lawrence S., David W. Sommer, and David L. Eckles. 2008. The role of internal capital markets in financial intermediaries: Evidence from insurer groups. Journal of Risk and Insurance 75: 439–61. [Google Scholar] [CrossRef]

- Rauh, Joshua D. 2009. Risk shifting versus risk management: Investment policy in corporate pension plans. Review of Financial Studies 22: 2687–733. [Google Scholar] [CrossRef] [Green Version]

- Schrand, Catherine, and Haluk Unal. 1998. Hedging and coordinated risk management: Evidence from thrift conversions. Journal of Finance 53: 979–1013. [Google Scholar] [CrossRef] [Green Version]

- Smith, Clifford W., and Rene M. Stulz. 1985. The determinants of firms’ hedging policies. Journal of Financial and Quantitative Analysis 20: 391–405. [Google Scholar] [CrossRef]

- Stein, Jeremy C. 2003. Agency, information and corporate investment. Handbook of the Economics of Finance 1: 111–65. [Google Scholar]

- Weber, Elke U., Ulf Böckenholt, Denis J. Hilton, and Brian Wallace. 1993. Determinants of diagnostic hypothesis generation: Effects of information, base rates, and experience. Journal of Experimental Psychology: Learning, Memory, and Cognition 19: 1151. [Google Scholar] [CrossRef] [PubMed]

- Wooldridge, Jeffrey M. 2010. Econometric Analysis of Cross Section and Panel Data. Cambridge, MA: MIT Press. [Google Scholar]

- Yu, Tong, Bingxuan Lin, Henry R. Oppenheimer, and Xuanjuan Chen. 2008. Intangible assets and firm asset risk taking: An analysis of property and liability insurance firms. Risk Management and Insurance Review 11: 157–78. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Description |

|---|---|

| E_Total | The fraction of insurers’ equity investment on affiliated and unaffiliated firms over total investments. |

| E_Unaffiliated | The fraction of insurers’ equity investment on unaffiliated firms over total investments. |

| E_Affiliated | The fraction of insurers’ equity investment on affiliated firms over total investments. |

| E_Mutual | The fraction of insurers’ equity investment on mutual funds over total investments. |

| Firm_size | Insurers’ total net admitted assets in the scale of natural logarithm. |

| Ownership | Dummy variable equal to 1 for mutual insurers and 0 for stock insurers. |

| Group | Dummy variable equal to 1 for affiliated insurers and 0 for unaffiliated. |

| Long_tail_ratio | The fraction of net premiums written on long-tail business lines. |

| Riskybond_ratio | The fraction of risky bond (NAIC class 3 and above) over total investments. |

| ROA | Return on assets: The ratio of net income to total net admitted assets. |

| Lines_Div | The complement of the Herfindahl Index of net premiums written across business lines. |

| Geo_Div | The complement of the Herfindahl Index of net premiums written across states. |

| Leverage | The ratio of policyholder surplus to total net admitted assets. |

| Reinsurance | The ratio of premiums ceded to the sum of direct premiums written and reinsurance assumed. |

| Combined_ratio | The sum of incurred losses and underwriting expenses that are proportional to premiums earned; the sum of loss ratio and expense ratio. |

| RBC_adjusted | Insurers’ surplus that is adjusted to the risk based capital measurement. |

| Financial_slack | The ratio of cash and short-term investments to total net admitted assets. |

| Treasury_3m | The average of the 3-month Treasury bill yields for the given year. |

| Quit_All | Dummy variable equal to 1 for all insurers who quit equity investments in a given year. |

| Quit_Permanent | Dummy variable equal to 1 for insurers who quit equity investments permanently (do not re-enter). |

| Quit_Temporary | Dummy variable equal to 1 for insurers who quit equity investments temporarily (re-enter). |

| Net_G_Naff_IC | Equity investment income on the unaffiliated, adjusted for realized capital gains. |

| Net_G_Total_IC | Equity investment income on the unaffiliated and the affiliated, adjusted for realized capital gains. |

| Net_G_Naff_ICu | Equity investment income on the unaffiliated, adjusted for realized and unrealized capital gains. |

| Net_G_Total_ICu | Equity investment income on the unaffiliated and the affiliated, adjusted for realized and unrealized capital gains. |

| Net_G_Udw | Net gains from underwriting: Premiums earned minus loss incurred and expenses. |

| Variables | Obs | Mean | Median | Min | Max | Std. Dev. | Skewness |

|---|---|---|---|---|---|---|---|

| E_Total | 31,130 | 11.868 | 5.765 | 0.000 | 49.332 | 14.672 | 1.235 |

| E_Unaffiliated | 31,130 | 7.705 | 1.992 | 0.000 | 36.876 | 10.756 | 1.478 |

| E_Affiliated | 31,130 | 3.286 | 0.000 | 0.000 | 25.137 | 7.019 | 2.188 |

| E_Mutual | 31,130 | 1.255 | 0.000 | 0.000 | 11.392 | 3.030 | 2.507 |

| Firm_size | 31,130 | 18.330 | 18.290 | 15.130 | 21.759 | 1.849 | 0.089 |

| Ownership | 31,130 | 0.214 | 0.000 | 0.000 | 1.000 | 0.410 | 1.393 |

| Group | 31,130 | 0.685 | 1.000 | 0.000 | 1.000 | 0.464 | −0.799 |

| Long_tail_ratio | 31,130 | 0.787 | 0.948 | 0.000 | 1.000 | 0.332 | −1.650 |

| Riskybond_ratio | 31,130 | 0.008 | 0.000 | 0.000 | 0.072 | 0.019 | 2.634 |

| ROA | 31,130 | 0.021 | 0.024 | −0.074 | 0.096 | 0.041 | −0.447 |

| Lines_Div | 31,130 | 0.367 | 0.394 | 0.000 | 0.839 | 0.324 | 0.067 |

| Geo_Div | 31,130 | 0.389 | 0.310 | 0.000 | 0.944 | 0.386 | 0.244 |

| Leverage | 31,130 | 0.463 | 0.421 | 0.197 | 0.888 | 0.193 | 0.705 |

| Reinsurance | 31,130 | 0.365 | 0.303 | 0.000 | 0.907 | 0.301 | 0.415 |

| Combined_ratio | 31,130 | 1.049 | 0.992 | 0.530 | 2.155 | 0.338 | 1.798 |

| RBC_adjusted | 31,130 | 16.440 | 17.289 | 0.000 | 20.697 | 4.497 | −2.837 |

| Finnancial_slack | 31,130 | 0.133 | 0.070 | 0.003 | 0.589 | 0.158 | 1.723 |

| Treasury_3m | 31,130 | 1.284 | 0.931 | 0.033 | 4.727 | 1.484 | 1.206 |

| Net_G_Naff_IC | 31,130 | 0.361 | 0.013 | −2.325 | 4.931 | 0.935 | 2.126 |

| Net_G_Total_IC | 31,130 | 0.461 | 0.031 | −2.581 | 6.389 | 1.150 | 2.451 |

| Net_G_Naff_ICu | 31,130 | 0.423 | 0.000 | −6.704 | 7.890 | 1.752 | 0.642 |

| Net_G_Total_ICu | 31,130 | 0.579 | 0.009 | −7.808 | 9.658 | 2.152 | 0.675 |

| Net_G_Udw | 31,130 | −0.304 | 0.180 | −28.270 | 18.226 | 6.653 | −1.008 |

| Variables | E_Total | E_Unaffiliated | E_Affiliated | E_Mutual_Only | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Yes | No | Diff. | Yes | No | Diff. | Yes | No | Diff. | Yes | No | Diff. | |

| Firm_size | 18.673 | 17.605 | 1.068 (***) | 18.636 | 17.829 | 0.807 (***) | 19.546 | 17.788 | 1.758 (***) | 17.442 | 18.364 | −0.922 (***) |

| Ownership | 0.281 | 0.073 | 0.209 (***) | 0.301 | 0.072 | 0.229 (***) | 0.320 | 0.167 | 0.153 (***) | 0.171 | 0.216 | −0.045 (***) |

| Group | 0.677 | 0.703 | −0.026 (***) | 0.659 | 0.728 | −0.069 (***) | 0.856 | 0.610 | 0.246 (***) | 0.543 | 0.691 | −0.148 (***) |

| Long_tail_ratio | 0.798 | 0.766 | 0.032 (***) | 0.805 | 0.759 | 0.045 (***) | 0.808 | 0.778 | 0.030 (***) | 0.793 | 0.787 | 0.006 ( ) |

| Riskybond_ratio | 0.010 | 0.003 | 0.008 (***) | 0.011 | 0.003 | 0.007 (***) | 0.013 | 0.006 | 0.007 (***) | 0.003 | 0.008 | −0.005 (***) |

| ROA | 0.023 | 0.017 | 0.006 (***) | 0.023 | 0.017 | 0.006 (***) | 0.023 | 0.020 | 0.002 (***) | 0.019 | 0.021 | −0.003 (**) |

| Lines_Div | 0.407 | 0.281 | 0.126 (***) | 0.412 | 0.292 | 0.120 (***) | 0.463 | 0.324 | 0.139 (***) | 0.235 | 0.372 | −0.136 (***) |

| Geo_Div | 0.421 | 0.320 | 0.101 (***) | 0.412 | 0.350 | 0.062 (***) | 0.512 | 0.334 | 0.178 (***) | 0.302 | 0.392 | −0.090 (***) |

| Leverage | 0.452 | 0.487 | −0.035 (***) | 0.452 | 0.481 | −0.029 (***) | 0.431 | 0.478 | −0.047 (***) | 0.478 | 0.463 | 0.015 (**) |

| Reinsurance | 0.333 | 0.433 | −0.101 (***) | 0.325 | 0.431 | −0.106 (***) | 0.341 | 0.376 | −0.035 (***) | 0.310 | 0.367 | −0.058 (***) |

| Combined_ratio | 1.026 | 1.098 | −0.072 (***) | 1.020 | 1.096 | −0.076 (***) | 1.032 | 1.056 | −0.025 ( ) | 1.030 | 1.050 | −0.020 ( ) |

| RBC_adjusted | 16.924 | 15.420 | 1.504 (***) | 16.972 | 15.570 | 1.402 (***) | 17.883 | 15.797 | 2.086 (***) | 15.256 | 16.486 | −1.230 (***) |

| Financial_slack | 0.108 | 0.186 | −0.078 (***) | 0.108 | 0.175 | −0.067 (***) | 0.082 | 0.156 | −0.074 (***) | 0.152 | 0.133 | 0.019 (***) |

| Year | Total | E_Total | E_Unaffiliated | E_Affiliated | E_Mutual_Only |

|---|---|---|---|---|---|

| 2002 | 1973 | 1365 (69.18%) | 1238 (62.74%) | 677 (34.31%) | 43 (2.17%) |

| 2003 | 1923 | 1315 (68.38%) | 1194 (62.09%) | 633 (32.92%) | 42 (2.18%) |

| 2004 | 1892 | 1299 (68.65%) | 1189 (62.84%) | 598 (31.61%) | 64 (3.38%) |

| 2005 | 1866 | 1291 (69.18%) | 1182 (63.34%) | 590 (31.62%) | 77 (4.12%) |

| 2006 | 1919 | 1316 (68.57%) | 1218 (63.47%) | 596 (31.06%) | 103 (5.36%) |

| 2007 | 1926 | 1318 (68.43%) | 1224 (63.55%) | 578 (30.01%) | 104 (5.39%) |

| 2008 | 1939 | 1309 (67.5%) | 1209 (62.35%) | 586 (30.22%) | 74 (3.81%) |

| 2009 | 1902 | 1239 (65.14%) | 1117 (58.72%) | 582 (30.60%) | 62 (3.25%) |

| 2010 | 1877 | 1212 (64.57%) | 1093 (58.23%) | 565 (30.10%) | 61 (3.24%) |

| 2011 | 1842 | 1202 (65.25%) | 1090 (59.17%) | 557 (30.24%) | 59 (3.20%) |

| 2012 | 1820 | 1202 (66.04%) | 1088 (59.78%) | 555 (30.49%) | 60 (3.29%) |

| 2013 | 1771 | 1199 (67.70%) | 1094 (61.77%) | 539 (30.43%) | 69 (3.89%) |

| 2014 | 1741 | 1195 (68.63%) | 1090 (62.60%) | 520 (29.87%) | 74 (4.25%) |

| 2015 | 1738 | 1199 (68.98%) | 1108 (63.75%) | 525 (30.21%) | 69 (3.97%) |

| 2016 | 1697 | 1176 (69.29%) | 1079 (63.58%) | 514 (30.29%) | 76 (4.47%) |

| 2017 | 1672 | 1153 (68.95%) | 1069 (63.93%) | 493 (29.49%) | 67 (4.00%) |

| 2018 | 1632 | 1117 (68.44%) | 1028 (62.99%) | 482 (29.53%) | 61 (3.73%) |

| E_Unaffiliated | E_Mutual_Only | |||

|---|---|---|---|---|

| Participation | Volume | Participation | Volume | |

| Firm_size | 0.1258 *** | −1.8415 *** | 0.0231 | −1.3784 *** |

| (0.0156) | (0.5092) | (0.0155) | (0.2062) | |

| Ownership | 1.1312 *** | 8.7137 *** | 0.7508 *** | 1.0517 ** |

| (0.0606) | (1.5295) | (0.0500) | (0.5086) | |

| Group | −0.4038 *** | −9.2380 *** | −0.2781 *** | −1.5601 *** |

| (0.0481) | (1.5289) | (0.0484) | (0.5467) | |

| Long_tail_ratio | 0.1104 * | 6.7956 *** | 0.0735 | 1.2558 |

| (0.0623) | (2.2799) | (0.0660) | (0.7761) | |

| Riskybond_ratio | 13.2930 *** | 114.509 *** | 2.6248 *** | −19.3528 * |

| (0.9283) | (22.7756) | (0.7791) | (10.3826) | |

| ROA | −0.1487 | −28.4323 ** | −0.6554 | −2.3390 |

| (0.4105) | (13.8505) | (0.4103) | (4.9586) | |

| Lines_Div | 0.4511 *** | 1.5944 | 0.1498 ** | 0.6775 |

| (0.0652) | (2.2259) | (0.0667) | (0.8342) | |

| Geo_Div | 0.2304 *** | 3.8428 * | −0.0317 | 3.6037 ** |

| (0.0602) | (2.0583) | (0.1111) | (1.4030) | |

| Leverage | 0.0011 | 42.7821 *** | 0.0399 | −0.6821 |

| (0.1072) | (4.1096) | (0.0622) | (0.8560) | |

| Reinsurance | −0.7866 *** | −15.1529 *** | −0.5608 *** | −0.3189 |

| (0.0617) | (2.6614) | (0.0655) | (0.9136) | |

| Combined_ratio | −0.2200 *** | −1.9175 | −0.2485 *** | 0.4817 |

| (0.0508) | (2.2487) | (0.0565) | (0.6828) | |

| RBC_adjusted | 0.0310 *** | −0.1119 | 0.0120 ** | −0.0647 |

| (0.0049) | (0.1561) | (0.0052) | (0.0554) | |

| Financial_slack | −1.0040 *** | −10.4305 ** | −1.0695 *** | −1.6694 |

| (0.1115) | (5.2115) | (0.1315) | (1.6015) | |

| Treasury_3m | 0.0165 | −1.0907 *** | −0.0195 * | −0.2972 ** |

| (0.0102) | (0.2908) | (0.0103) | (0.1194) | |

| Constant | −1.9563 *** | 10.5739 | −0.9491 * | 17.1548 *** |

| (0.4361) | (12.0516) | (0.4988) | (4.8230) | |

| Sigma | 17.9033 *** | 17.1548 *** | ||

| (0.5694) | (4.8230) | |||

| Fixed_State | Yes | Yes | ||

| Fixed_Year | Yes | Yes | ||

| Observations | 31,129 | 31,129 | ||

| E_Total | E_Affiliated | |||

|---|---|---|---|---|

| Participation | Volume | Participation | Volume | |

| Firm_size | 0.2073 *** | 2.0777 *** | 0.3289 *** | 0.1780 |

| (0.0167) | (0.5222) | (0.0179) | (0.4775) | |

| Ownership | 1.1643 *** | 12.4260 *** | 1.0703 *** | −3.8262 ** |

| (0.0650) | (1.5949) | (0.0626) | (1.4864) | |

| Group | −0.3353 *** | 0.6390 | 0.6011 *** | 30.2774 *** |

| (0.0502) | (1.7012) | (0.0605) | (3.8819) | |

| Long_tail_ratio | 0.0552 | 5.1640 ** | −0.0491 | 2.3725 |

| (0.0643) | (2.5521) | (0.0739) | (2.3191) | |

| Riskybond_ratio | 13.3146 *** | 131.191 *** | 4.5369 *** | 19.1463 |

| (1.0145) | (22.5869) | (0.8233) | (18.6491) | |

| ROA | −0.8737 ** | −93.2503 *** | −1.8493 *** | −76.5657 *** |

| (0.4208) | (15.3412) | (0.4496) | (12.7091) | |

| Lines_Div | 0.3893 *** | 6.7485 *** | 0.2206 *** | 2.0751 |

| (0.0683) | (2.3686) | (0.0748) | (2.0731) | |

| Geo_Div | 0.2980 *** | 5.0711 ** | 0.2602 *** | 4.1751 ** |

| (0.0631) | (2.1803) | (0.0677) | (1.7885) | |

| Leverage | 0.2201 ** | 70.7753*** | 0.4903 *** | 37.6857 *** |

| (0.1123) | (4.3558) | (0.1260) | (3.5628) | |

| Reinsurance | −0.7907 *** | −6.1609 ** | −0.4486 *** | 5.4578 *** |

| (0.0645) | (2.4684) | (0.0699) | (1.8884) | |

| Combined_ratio | −0.2084 *** | 0.3643 | −0.0038 | 2.0372 |

| (0.0523) | (2.2803) | (0.0574) | (1.6171) | |

| RBC_adjusted | 0.0265 *** | −0.1975 | 0.0105 * | −0.0240 |

| (0.0050) | (0.1857) | (0.0056) | (0.1866) | |

| Financial_slack | −1.0508 *** | −20.6284 *** | −0.3180 ** | −9.2134 ** |

| (0.1094) | (5.3602) | (0.1318) | (4.6405) | |

| Treasury_3m | 0.0191 * | −0.7035 ** | 0.0454 *** | −0.3022 |

| (0.0106) | (0.3176) | (0.0108) | (0.2813) | |

| Constant | −3.3204 *** | −91.7357 *** | −8.0826 *** | −71.8032 *** |

| (0.4514) | (13.3605) | (0.5232) | (23.1229) | |

| Sigma | 21.8932 *** | 12.7207 *** | ||

| (0.5825) | (4.8230) | |||

| Fixed_State | Yes | Yes | ||

| Fixed_Year | Yes | Yes | ||

| Observations | 31,129 | 31,129 | ||

| Year | Total | E_Unaffiliated | Quit_All | Quit_Permanent | Quit_Temporary | |||

|---|---|---|---|---|---|---|---|---|

| 2003 | 1923 | 1194 | 79 | 6.62% | 28 | 35.44% | 51 | 64.56% |

| 2004 | 1892 | 1189 | 56 | 4.71% | 18 | 32.14% | 38 | 67.86% |

| 2005 | 1866 | 1182 | 47 | 3.98% | 20 | 42.55% | 27 | 57.45% |

| 2006 | 1919 | 1218 | 54 | 4.43% | 24 | 44.44% | 30 | 55.56% |

| 2007 | 1926 | 1224 | 57 | 4.66% | 27 | 47.37% | 30 | 52.63% |

| 2008 | 1939 | 1209 | 102 | 8.44% | 59 | 57.84% | 43 | 42.16% |

| 2009 | 1902 | 1117 | 119 | 10.65% | 57 | 47.90% | 62 | 52.10% |

| 2010 | 1877 | 1093 | 70 | 6.40% | 36 | 51.43% | 34 | 48.57% |

| 2011 | 1842 | 1090 | 65 | 5.96% | 39 | 60.00% | 26 | 40.00% |

| 2012 | 1820 | 1088 | 53 | 4.87% | 24 | 45.28% | 29 | 54.72% |

| 2013 | 1771 | 1094 | 42 | 3.84% | 31 | 73.81% | 11 | 26.19% |

| 2014 | 1741 | 1090 | 31 | 2.84% | 21 | 67.74% | 10 | 32.26% |

| 2015 | 1738 | 1108 | 28 | 2.53% | 18 | 64.29% | 10 | 35.71% |

| 2016 | 1697 | 1079 | 46 | 4.26% | 37 | 80.43% | 9 | 19.57% |

| 2017 | 1672 | 1069 | 37 | 3.46% | 32 | 86.49% | 5 | 13.51% |

| Quit_Not | Quit_All | Quit_Permanent | Quit_Temporary | ||||

|---|---|---|---|---|---|---|---|

| Mean | Mean | Diff. | Mean | Diff. | Mean | Diff. | |

| Firm_size | 18.642 | 18.223 | 0.42 (***) | 18.254 | 0.39 (***) | 18.139 | 0.50 (***) |

| Ownership | 0.311 | 0.099 | 0.21(***) | 0.062 | 0.25 (***) | 0.201 | 0.11 (***) |

| Group | 0.657 | 0.699 | −0.04 (***) | 0.751 | −0.09 (***) | 0.553 | 0.10 (***) |

| Long_tail_ratio | 0.807 | 0.761 | 0.05 ( ) | 0.757 | 0.05 ( ) | 0.774 | 0.03 ( ) |

| Risykbond_ratio | 0.011 | 0.006 | 0.00 (***) | 0.006 | 0.00 (***) | 0.006 | 0.01 (***) |

| ROA | 0.024 | 0.016 | 0.01 (***) | 0.016 | 0.01 (***) | 0.018 | 0.01 (**) |

| Lines_Div | 0.417 | 0.355 | 0.06 (***) | 0.357 | 0.06 (***) | 0.352 | 0.06 (***) |

| Geo_Div | 0.411 | 0.425 | −0.01 ( ) | 0.439 | −0.03 (*) | 0.385 | 0.03 ( ) |

| Leverage | 0.452 | 0.442 | 0.01 ( ) | 0.440 | 0.01 ( ) | 0.448 | 0.00 ( ) |

| Reinsurance | 0.322 | 0.387 | −0.07 (***) | 0.398 | −0.08 (***) | 0.356 | −0.03 ( ) |

| Combined_ratio | 1.019 | 1.067 | −0.05 (***) | 1.076 | −0.06 (***) | 1.040 | −0.02 ( ) |

| RBC_adjusted | 16.993 | 16.023 | 0.97 (***) | 15.994 | 1.00 (***) | 16.106 | 0.89 (***) |

| Financial_slack | 0.107 | 0.137 | −0.03 (***) | 0.128 | −0.02 (***) | 0.160 | −0.05 (***) |

| Net_G_Naff_IC | 0.560 | 0.164 | 0.40 (***) | 0.145 | 0.41 (***) | 0.214 | 0.35 (***) |

| Net_G_Total_IC | 0.692 | 0.238 | 0.45 (***) | 0.226 | 0.47 (***) | 0.272 | 0.42 (***) |

| Net_G_Naff_ICu | 0.784 | 0.137 | 0.65 (***) | 0.130 | 0.65 (***) | 0.158 | 0.63 (***) |

| Net_G_Total_ICu | 1.016 | 0.221 | 0.79 (***) | 0.207 | 0.81 (***) | 0.262 | 0.75 (***) |

| Net_G_Udw | −0.008 | −1.079 | 1.07 (***) | −1.287 | 1.28 (***) | −0.505 | 0.50 ( ) |

| Net Gains | Net Gains (Capital Gain Adjusted) | |||

|---|---|---|---|---|

| E_Unaffiliated | E_Total | E_Unaffiliated | E_Total | |

| Equity Investment | −4.1010 *** | −1.5510 *** | −0.1401 *** | −0.1227 *** |

| (−0.2799) | (−0.1523) | (0.0244) | (0.0199) | |

| Underwriting | −0.0429 *** | −0.0480 *** | −0.0370 *** | −0.0384 *** |

| (−0.0119) | (−0.0118) | (0.0116) | (0.0116) | |

| Firm_size | −0.2615 *** | −0.2069 *** | −0.2222 *** | −0.2125 *** |

| (−0.0382) | (−0.0379) | (0.0391) | (0.0391) | |

| Ownership | −1.3619 *** | −1.4450 *** | −1.5982 *** | −1.5904 *** |

| (−0.1499) | (−0.1499) | (0.1552) | (0.1552) | |

| Group | 0.3045 *** | 0.3600 *** | 0.4602 *** | 0.4584 *** |

| (−0.1167) | (−0.1158) | (0.1194) | (0.1192) | |

| Long_tail_ratio | −0.2093 | −0.2682 * | −0.3227 ** | −0.3194 ** |

| (−0.1549) | (−0.1528) | (0.1570) | (0.1569) | |

| Riskybond_ratio | −11.4558 *** | −13.1091 *** | −16.4539 *** | −16.2892 *** |

| (−2.6822) | (−2.6574) | (2.6699) | (2.6683) | |

| ROA | 8.4256 *** | 9.6594 *** | 8.1631 *** | 8.4688 *** |

| (−1.8199) | (−1.816) | (1.7517) | (1.7633) | |

| Lines_Div | −0.3288 ** | −0.3654 ** | −0.4374 *** | −0.4339 *** |

| (−0.1617) | (−0.1605) | (0.1655) | (0.1654) | |

| Geo_Div | 0.223 | 0.2931 ** | 0.2425 | 0.2499 |

| (−0.1474) | (−0.1476) | (0.1537) | (0.1536) | |

| Leverage | 0.0813 | −0.0246 | −0.4727 | −0.4251 |

| (−0.2852) | (−0.2861) | (0.2901) | (0.2904) | |

| Reinsurance | 0.6346 *** | 0.8189 *** | 0.9958 *** | 1.0002 *** |

| (−0.1608) | (−0.1607) | (0.1639) | (0.1640) | |

| Combined_ratio | 0.4838 *** | 0.4881 *** | 0.5019 *** | 0.4811 ** |

| (−0.1865) | (−0.1858) | (0.1886) | (0.1886) | |

| RBC_adjusted | −0.0296 ** | −0.0334 *** | −0.0358 *** | −0.0352 *** |

| (−0.0127) | (−0.0125) | (0.0127) | (0.0127) | |

| Financial_slack | 1.1124 *** | 1.1806 *** | 1.3012 *** | 1.3035 *** |

| (−0.3147) | (−0.3101) | (0.3160) | (0.3161) | |

| Treasury_3m | −0.0281 | −0.0162 | −0.3571 | −0.3208 |

| (−0.2567) | (−0.2542) | (0.2603) | (0.2584) | |

| Constant | 3.0751 *** | 1.5252 | 2.2437 ** | 1.9593 * |

| (−1.0555) | (−1.0511) | (1.0798) | (1.0788) | |

| Fixed_State | Yes | Yes | Yes | Yes |

| Fixed_Year | Yes | Yes | Yes | Yes |

| Observations | 17,590 | 18,210 | 18,210 | 18,210 |

| Variables | Quit_Permanent | Quit_Temporary | ||

|---|---|---|---|---|

| Net Gains | Net Gains (Capital Gain Adjusted) | Net Gains | Net Gains (Capital Gain Adjusted) | |

| Equity Investment | −5.4505 *** | −0.2398 *** | −2.5840 *** | −0.1036 *** |

| (0.4818) | (0.0402) | (0.3206) | (0.0336) | |

| Underwriting | −0.0560 *** | −0.0543 *** | −0.0242 | −0.0240 |

| (0.0163) | (0.0176) | (0.0167) | (0.0164) | |

| Firm_size | −0.3604 *** | −0.3894 *** | −0.1369 *** | −0.0996 * |

| (0.0587) | (0.0739) | (0.0516) | (0.0515) | |

| Ownership | −2.3206 *** | −3.0719 *** | −0.7675 *** | −0.8618 *** |

| (0.2960) | (0.3769) | (0.1792) | (0.1793) | |

| Group | 0.8735 *** | 1.2703 *** | −0.2938 * | −0.2100 |

| (0.1811) | (0.2299) | (0.1555) | (0.1548) | |

| Long_tail_ratio | −0.1574 | −0.3051 | −0.2029 | −0.2727 |

| (0.2215) | (0.2662) | (0.2121) | (0.2100) | |

| Riskybond_ratio | −11.0092 *** | −17.3900 *** | −9.4501 ** | −13.5781 *** |

| (3.8304) | (4.1700) | (3.7341) | (3.6853) | |

| ROA | 10.7285 *** | 11.7285 *** | 4.3377 * | 4.7592 * |

| (2.5452) | (2.6940) | (2.5217) | (2.4432) | |

| Lines_Div | −0.5033 ** | −0.6597 ** | −0.0652 | −0.1964 |

| (0.2343) | (0.2852) | (0.2193) | (0.2177) | |

| Geo_Div | 0.1278 | 0.2049 | 0.3147 | 0.3417 * |

| (0.2067) | (0.2587) | (0.2035) | (0.2061) | |

| Leverage | 0.2064 | −0.3112 | 0.0040 | −0.3943 |

| (0.3967) | (0.4726) | (0.4009) | (0.3999) | |

| Reinsurance | 0.6287 *** | 1.1732 *** | 0.6332 *** | 0.9165 *** |

| (0.2270) | (0.2749) | (0.2254) | (0.2247) | |

| Combined_ratio | 0.6489 *** | 0.7871 *** | 0.1276 | 0.1266 |

| (0.2466) | (0.2838) | (0.2817) | (0.2840) | |

| RBC_adjusted | −0.0443 ** | −0.0661 *** | −0.0018 | −0.0029 |

| (0.0177) | (0.0212) | (0.0179) | (0.0176) | |

| Financial_slack | 1.0813 ** | 1.3283 ** | 1.2590 *** | 1.4348 *** |

| (0.4481) | (0.5186) | (0.4164) | (0.4124) | |

| Treasury_3m | −0.1416 | 0.0382 | −0.8896 | −0.8832 |

| (0.4441) | (0.4651) | (0.9251) | (0.9233) | |

| Constant | −12.7337 | −16.9625 | −0.1970 | −1.2196 |

| (2799.2725) | (9430.8936) | (1.3216) | (1.3171) | |

| Fixed_State | Yes | Yes | Yes | Yes |

| Fixed_Year | Yes | Yes | Yes | Yes |

| Observations | 16,154 | 16,154 | 15,437 | 15,437 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bae, S.; Liebenberg, A.P.; Liebenberg, I.A. Equity Investment Decisions of Operating Firms: Evidence from Property and Liability Insurers. J. Risk Financial Manag. 2023, 16, 228. https://doi.org/10.3390/jrfm16040228

Bae S, Liebenberg AP, Liebenberg IA. Equity Investment Decisions of Operating Firms: Evidence from Property and Liability Insurers. Journal of Risk and Financial Management. 2023; 16(4):228. https://doi.org/10.3390/jrfm16040228

Chicago/Turabian StyleBae, Sunghan, Andre P. Liebenberg, and Ivonne A. Liebenberg. 2023. "Equity Investment Decisions of Operating Firms: Evidence from Property and Liability Insurers" Journal of Risk and Financial Management 16, no. 4: 228. https://doi.org/10.3390/jrfm16040228

APA StyleBae, S., Liebenberg, A. P., & Liebenberg, I. A. (2023). Equity Investment Decisions of Operating Firms: Evidence from Property and Liability Insurers. Journal of Risk and Financial Management, 16(4), 228. https://doi.org/10.3390/jrfm16040228