The Optimal Level of Financial Growth in View of a Nonlinear Macroprudential Policy Regime Model: A Bayesian Approach

Abstract

:1. Introduction

- There is no optimal level of financial development required for growth in African countries.

- There is no nonlinearity in the data for African countries after controlling for spatial correlation problems.

- A transition from a non-macroprudential policy regime to a macroprudential policy regime has no effect on the traditional impact of the finance–growth relationship in African economics.

- Monetary policy through unconventional policy has no impact on the finance–growth relationship.

- The model adopted does not affect the finance–growth inequality.

2. Literature Review

2.1. Theoretical Channels of Financial Development and Economic Growth

2.2. Empirical Literature Review

2.2.1. The Empirical Relationship between Financial Development and Economic Growth

2.2.2. The Empirical Analysis of Macroprudential Policies and Economic Growth

2.2.3. The Empirical Literature concerning the Impact of Unconventional Monetary Policy on Economic Growth

3. Methodology Framework

3.1. Justification of Variables

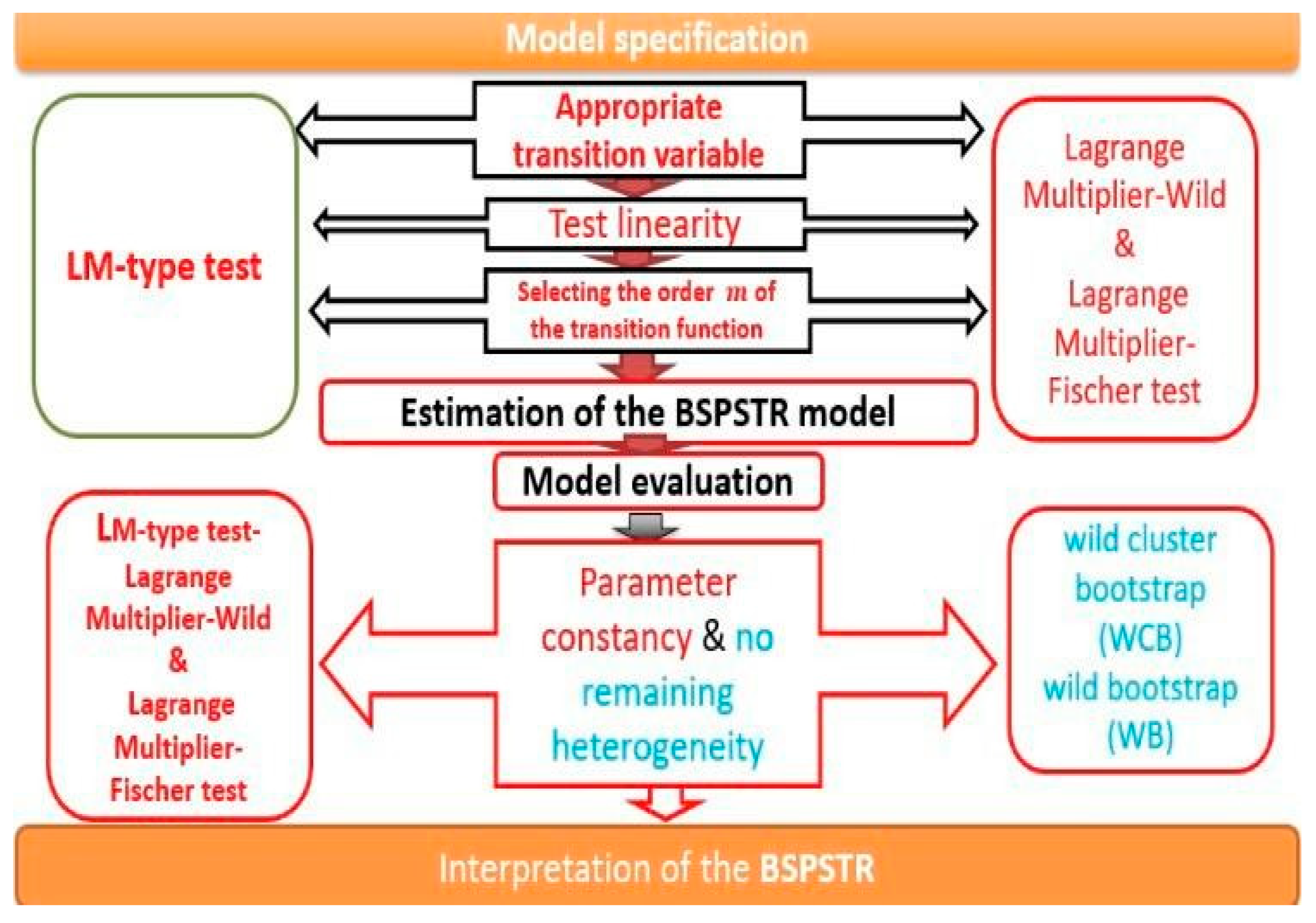

3.2. Spatial Lag Panel Smooth Transition Regression Model

Building a Bayesian Estimation for the PSTR Model

4. Analysis of the Study

4.1. The Results of the Testing Procedure of the BSPSTR Model

4.2. Model Evaluation and the Estimated Threshold of the BSPSTR Model

4.3. Empirical Results of the BSPSTR and Discussion

4.4. Sensitivity Analysis and Robustness Checks

5. Conclusions and Policy Recommendations

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Variables | Mean | Std. Dev | Min | Max |

|---|---|---|---|---|

| FD | 8.8093 | 1.1997 | 5.0865 | 9.4870 |

| FCRRM | 67.5594 | 7.9258 | 28.6367 | 80.919 |

| GCBRM | 70.2006 | 0.7838 | 9.6878 | 6.4411 |

| CRIM | 45.5768 | 0.3430 | 6.0412 | 11.2325 |

| BRIM | 21.6721 | 8.0535 | 2.6315 | 52.9388 |

| ICEIUN | 44.1316 | 5.3089 | 2.7740 | 60.8798 |

| PCHPUN | 29.1318 | 1.3086 | 2.8490 | 70.9998 |

| INFL | 10.2707 | 1.2594 | 24.326 | 29.1781 |

| TRD | 21.1218 | 8.0537 | 2.6315 | 52.9388 |

| GEF | 52.3199 | 1.3688 | 6.7408 | 70.7989 |

| INVE | 70.1187 | 0.3086 | 10.3679 | 60.77779 |

| TOD | 56.33789 | 3.2598 | 24.326 | 29.1781 |

References

- Abdul Bahri, Elya Nabila, Abu Hassan Shaari Md Nor, Tamat Sarmidi, and Nor Hakimah Haji Mohd Nor. 2019. The Role of financial development in the relationship between foreign direct investment and economic growth: A nonlinear approach. Review of Pacific Basin Financial Markets and Policies 22: 1950009. [Google Scholar] [CrossRef]

- Abeka, Mac Junior, Andon Eric, John Gartchie Gatsi, Seyram Kawor, and David Mcmillan. 2021. Financial development and economic growth nexus in SSA economies: The moderating role of telecommunication development. Cogent Economics and Finance 9: 25. [Google Scholar] [CrossRef]

- Abu-Lila, Ziad, Ajlouni Sameh, and Ghazo Abdallah. 2021. Nonlinearity between financial development and the shadow economy: Evidence from Jordan. Accounting 7: 1049–54. Available online: www.GrowingScience.com/ac/ac.html (accessed on 30 December 2021). [CrossRef]

- Alin, Marius Andries, and Melnic Florentina. 2019. Macroprudential policies and economic growth. Review of Economic Business Studies 12: 95–112. [Google Scholar]

- Alves, Jose, and Tomas Silva. 2020. An Empirical Assessment of Monetary Policy Channels on Income and Wealth Disparities. REM Working Paper 0144–2020. Available online: https://rem.rc.iseg.ulisboa.pt/wps/pdf/REM_WP_0144_2020.pdf (accessed on 24 February 2022).

- Andries, Alin Marius, and Florentina Melnic. 2019. Macroprudential policies and economic growth. Review of Economic and Business Studies, Alexandru Ioan Cuza University, Faculty of Economics and Business Administration 23: 95–112. [Google Scholar] [CrossRef] [Green Version]

- Arcand, Jean-Louis, Enrico Berkers, and Panizza Ugo. 2012. Too much finance? Journal of Economic Growth 20: 105–48. [Google Scholar] [CrossRef]

- Asif, Khan, Bibi Sughra, Lorenzo Ardito, Jiaying Lyu, and Udden Babar Zaheer. 2020. Tourism and development in developing economies: A policy implication perspective. Sustainability 12: 1618. [Google Scholar]

- Bandura, Withness Nyasha, and Canicio Dzingirai. 2019. Financial development and economic growth in Sub-Saharan Africa: The role of institutions. PSL Quarterly Review 72: 315–34. [Google Scholar]

- Belkhir, Naceur, Sami Ben Mohamed, Bertrand Candelon, and Jean-Charles Wijnandts. 2022. Macroprudential Regulation and Sector-Specific Default Risk. IMF Working Paper Series WP/22/121. Available online: https://www.imf.org/en/Publications/WP/Issues/2022/07/15/Macroprudential-Regulation-and-Sector-Specific-Default-Risk-520865 (accessed on 22 March 2022).

- Bist, Jagadish Prasad. 2018. Financial development and economic c growth: Evidence from a panel of 16 African and non-African low-income countries. Cogent Economics and Finance 6: 1–1899. [Google Scholar] [CrossRef] [Green Version]

- Boar, Codruta, Leonardo Gambacorta, Giovanni Lombardo, and Luiz Pereira Silva. 2017. What are the effects of macroprudential policies on macroeconomic performance? BIS Quarterly Review 2017: 71–88. [Google Scholar]

- Brenner, Thomas. 2014. The Impact of Foreign Direct Investment on Economic Growth—An Empirical Analysis of Different Effects in Less and More Developed Countries. Working Papers on Innovation and Space, Department? Marburg: Philipps Universität. Available online: http://hdl.handle.net/10419/111901 (accessed on 10 May 2022).

- Cerutti, Eugenio, Stijn Claessens, and Luc Laeven. 2017. The use and effectiveness of macropru-dential policies: New evidence. Journal of Financial Stability 28: 203–24. [Google Scholar] [CrossRef]

- Chu, Jenq Fei, Kun Sek Siok, and Tahir Ismail Mohd. 2022. Threshold effects of inflation on economic growth: Evidence from dynamic panel threshold regression analysis for 18 developed economies. Journal of Management, Economics, and Industrial Organization 3: 51–62. [Google Scholar]

- Ductor, Lorenzo, and Daryna Grechyna. 2015. Financial development, real sector, and economic growth. International Review of Economics & Finance 37: 393–405. [Google Scholar]

- Elijah, Sunday, and Namadina Hamza. 2019. The relationship between financial sector development and economic growth in Nigeria: Cointegration with structural break approach. International Journal of Engineering and Advanced Technology 8: 1081–88. [Google Scholar]

- Erkisi, Kemal. 2018. Financial development and economic growth in BRICS Countries and Turkey: A panel data analysis. Istanbul Gelism University Journal of Social Science 5: 17. [Google Scholar]

- Faathih, Zahir, and Masih Mansur. 2018. Is the Lead-Lag Relationship between Financial Development and Economic Growth Symmetric? New Evidence from Bangladesh Based on ARDL ad NARDL. MPRA Paper 87577. Munich: University Library of Munich. Available online: https://mpra.ub.uni-muenchen.de/87577 (accessed on 23 March 2022).

- Gillman, Max, and Mark Harris. 2004. Inflation, Financial Development and Growth in Transition Countries. Working Paper, No. 23/04. Melbourne: Monash University. [Google Scholar]

- Goldsmith, Raymond. 1969. Financial Structure and Development. New Haven: Yale University Press. [Google Scholar]

- González, Andres, Timo Teräsvirta, Dick van Dijk, and Yukai Yang. 2017. Panel Smooth Transition Regression Models. SSE/EFI Working Paper Series in Economics and Finance 604, Stockholm School of Economics, revised 11 October 2017. Available online: https://EconPapers.repec.org/RePEc:hhs:hastef:0604 (accessed on 23 March 2022).

- Gouider, Afrah Larnaout, and Mohamed Trabelsi. 2006. Does financial market development matter in explaining growth fluctuations? Savings and Development 30: 469–95. Available online: http://www.jstor.org/stable/25830945 (accessed on 23 March 2022).

- Granger, Clive William John, and Timo Terasvirta. 1993. Modelling non-linear economic rela-tionships. In OUP Catalogue. Oxford: Oxford University Press. Available online: https://ideas.repec.org/b/oxp/obooks/9780198773207.html (accessed on 20 May 2022).

- Greenwood, Jeremy, and Boyan Jovanovic. 1990. Financial development, growth, and the distribution of income. Journal of Political Economy 98: 1076–107. Available online: http://www.jstor.org/stable/2937625 (accessed on 20 May 2022). [CrossRef] [Green Version]

- Husam-Aldin, Al-Malkawi, Marashden Hazem, and Abdullah Naziruddin. 2012. Financial development and economic growth in the UAE: Empirical assessment using ARDL approach to co-integration. International Journal of Economics and Finance 4: 5. [Google Scholar]

- Ibrahim, Muazu, and Imhotep Alagidede. 2018. Effect of financial development on economic growth in sub-Saharan Africa. Journal of Policy Modeling 40: 1104–25. [Google Scholar] [CrossRef]

- Ibrahim, Muazu, and Paul Imhotep. 2018. Nonlinearities in financial development—Economic growth nexus: Evidence from sub-Saharan Africa. Research in International Business and Finance 46: 95–104. [Google Scholar] [CrossRef]

- Inoue, Atsushi, and Barbara Rossi. 2018. A new approach to measuring economic policy shocks, with an application to conventional and unconventional monetary policy. Quantitative Economics 12: 1085–38. [Google Scholar] [CrossRef]

- Jain, Megha, Aishwarya Nagpal, and Abhay Jain. 2021. Government size and economic growth: An empirical examination of selected emerging economies. South Asian Journal of Macroeconomics and Public Finance 10: 7–39. [Google Scholar] [CrossRef]

- Jinqi, Song. 2020. Institutions, Financial Development and Economic Growth. Nanchang: Francis Academic Press. [Google Scholar]

- Jobarteh, Mustapha, and Huseyin Kaya. 2019. Revisiting Financial Development and Income Inequality Nexus for Africa. The African Finance Journal 21: 1–22. [Google Scholar]

- Keho, Yaya, and M. G. Wang. 2017. The impact of trade openness on economic growth: The case of Cote d’Ivoire. Cogent Economics & Finance 5: 2017. [Google Scholar]

- Khan, Mohsin, and Abdelhak Senhadji. 2000. Financial Development and Economic Growht: An Overview. IMF working paper series WP/00/209. Available online: https://www.imf.org/external/pubs/ft/wp/2000/wp00209.pdf (accessed on 22 March 2022).

- Kim, Soyoung, and Aaron Mehrotra. 2017. Effects of Monetary and Macro-Prudential Policies—Evidence from Inflation Targeting Economies in the Asia-Pacific Region and Potential Implications for China. BOFIT Discussion Papers, No. 4/2017. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2929407 (accessed on 19 March 2022).

- King, Robert, and Ross Levine. 1993. Economic and growth: Schumpeter might be right. Quarterly Journal of Economics 108: 717–37. [Google Scholar] [CrossRef]

- Lombardi, Domenico, Pierre Siklos, and Samantha St. Amand. 2018. A Survey of the International Evidence and Lessons Learned About Unconventional Monetary Policies: Is a ‘New Normal’ in our Future? Contemporary Topics in Finance: A Collection of Literature Surveys, 11–40. [Google Scholar] [CrossRef]

- Machado, Celsa, Machadi Antonio, and Vieira Paulo. 2021. Finance–growth nexus in sub-Saharan Africa. South African Journal of Economic and Management Sciences 24: 3435. [Google Scholar] [CrossRef]

- Mahmoud, Mohieldin, Hussein Khaled, and Rostom Ahmed. 2019. On financial development and economic growth in Egypt. Journal of Humanities and Applied Social Sciences 1: 70–86. [Google Scholar]

- McKinnon, Ronald. 1973. Money and Capital in Economic Development. Washington, DC: Brookings Institution Press, p. 184. ISBN 9780815718499. [Google Scholar]

- Mohamed, Belkhir, Sami Ben Naceur, Bertrand Candelon, and Jean-Charles Wijnandts. 2022. Macroprudential policies, economic growth and banking crises. Emerging Markets Review, 100936. [Google Scholar] [CrossRef]

- Mosesov, Alexander, and Nizar Sahawneh. 2005. UAE: Financial development and economic growth. Skyline Business Journal 1: 1–11. [Google Scholar]

- Patrick, Hugh. 1966. Financial development and economic growth in underdeveloped countries. Economic Development and Cultural Change 14: 74–189. [Google Scholar] [CrossRef] [Green Version]

- Puatwoe, Janice Tieguhong, and Serge Mandiefe Piabou. 2017. Financial sector development and economic growth: Evidence from Cameroon. Financial Innovation 3: 25. [Google Scholar] [CrossRef] [Green Version]

- Ram, Rati. 1999. Financial development and economic growth: Additional evidence. The Journal of Development Studies 35: 164–74. [Google Scholar] [CrossRef]

- Romer, Paul. 1986. Increasing returns and long-run growth. Journal of Political Economy 94: 1002–37. Available online: https://www.jstor.org/stable/1833190 (accessed on 20 May 2022). [CrossRef] [Green Version]

- Rose, Malefa, and Nicholas Odhiambo. 2018. Impact of trade openness on economic growth: Empirical evidence from South Africa. Economia Internazionale/International Economics 71: 387–416. [Google Scholar]

- Samargandi, Nahla, Jan Fidrmuc, and Sugata Ghosh. 2015. Is the relationship between financial development and economic growth monotonic? Evidence from a sample of Middle-Income Countries. World Development 68: 66–81. [Google Scholar] [CrossRef] [Green Version]

- Samimi, Ahmad Jafari, Somaye Sadeghi, and Soraya Sadeghi. 2011. Tourism and Economic Growth in Developing Countries: P-VAR Approach. Middle East Journal of Scientific Research 10: 28–32. [Google Scholar]

- Schumpeter, Joseph Alois. 1934. The Theory of Economic development. Translated by Redvers Opie. Cambridge: Harvard University Press. [Google Scholar]

- Shaw, Edward Stone. 1973. Financial Deepening in Economic Development. New York: Oxford University Press. [Google Scholar]

- Swamy, Vighneswara, and Munusamy Dharani. 2019. The dynamics of finance–growth nexus in advanced economies. International Review of Economics and Finance 64: 122–46. [Google Scholar] [CrossRef]

- Tatiana, Fic. 2013. The Spillover Effects of Unconventional Monetary Policies in Major Developed Countries on Developing Countries. DESA Working Paper No. 131. Available online: https://www.un.org/en/desa/spillover-effects-unconventional-monetary-policies-major-developed-countries (accessed on 20 January 2022).

- Ufuo, Oro Oro, and Paul Alagidede. 2018. The Nature of the finance–growth relationship: Evidence from a panel of oil-producing countries. Economic Analysis and Policy 60: 89–102. [Google Scholar]

- Vinayagathasan, Thanabalasingam. 2013. Inflation and Economic Growth: A Dynamic Panel Threshold Analysis for Asian Economies. GRIPS Discussion Paper 12–17. Available online: https://www.grips.ac.jp/r-center/wp-content/uploads/12-17.pdf (accessed on 20 January 2022).

- WDI. 2022. World Bank. Washington, DC. Available online: http://data.worldbank.org/data-catalog/world-development-indicators (accessed on 10 February 2022).

- Zungu, Lindokuhle Talent. 2022. Nonlinear dynamics of the financial–growth nexus in African Emerging Economies: The case of a macroprudential policy regime. Economies 10: 90. [Google Scholar] [CrossRef]

- Zungu, Lindokuhle Talent, and Lorraine Greyling. 2022. Government size and economic growth in African emerging economies: Does the BARS curve exist? International Journal of Social Economics 49: 356–71. [Google Scholar] [CrossRef]

- Zungu, Lindokuhle Talent, Yoland Nkomo, Bongumusa Prince Makhoba, and Greyling Lorraine. 2022. The Nonlinear Dynamic Impact of Development-Inequality in the Prudential Policy Regime in Emerging Economies: A Bayesian Spatial Lag Panel Smooth Transition Regression Approach. Business, Management and Economics. London: IntechOpen. [Google Scholar] [CrossRef]

| Fs | 2.90 | 5.22 | 2.54 | 16.89 | 4.90 | 15.98 | 9.89 | |

| pv | 0.00054 | 0.00000 | 0.056 | 0.0000 | 0.60 | 10.209 × 10−09 | 5.984 × 10−10 | |

| Fs | 20.22 | 15.58 | 14.89 | 7.50 | 9.98 | 60.89 | 8.21 | |

| pv | 0.00009 | 0.00004 | 00000 | 0.0000 | 0.70 | 6.985 × 10−02 | 0.00009 | |

| WB | pv | - | - | - | 0.00 | - | - | - |

| WCB | pv | - | - | - | 0.00 | - | - | - |

| Parameter Constancy test | ||

| 6.384 (5.958 × 10−18) | ||

| 98.89 (5.745 × 10−78) | ||

| No Remaining Nonlinearity | ||

| 1 (p-value) | ||

| 1 (p-value) | ||

| The estimated threshold model | ||

| Model 1:Baseline | Model 2:Baseline | |

| 0.92 ***(0.02) | 0.58 ***(0.05) | |

| 18.11 ** (4.20) | 13.99 **(2.90) | |

| Variables: | Model 1: Financial Growth: Macroprudential Policy Regime (2000–2021) | Model 2: Financial Growth: Non-Macroprudential Policy Regime (1983–1999) | ||

|---|---|---|---|---|

| BSPSTR | BSPSTR | |||

| 8.23 **(2.02) | −3.99 **(0.21) | −1.98 ***(0.09) | 5.88(1.99) ** | |

| −2.34 **(0.14) | −4.67 **(1.00) | |||

| −0.76(0.17) | 2.98 **(0.50) | |||

| 4.09 **(1.23) | −5.90 **(1.00) | |||

| −2.33 ***(0.20) | 1.60 **(0.87) | |||

| 1.40 **(0.89) | −4.80 **(0.90) | |||

| 3.04(0.56) | 2.94 **(1.00) | |||

| 2.06 **(0.91) | −0.76 **(0.05) | 2.99 ***(0.02) | −3.90 **(4.60) | |

| 3.56 **(1.00) | 2.78 **(0.67) | 3.80 **(0.40) | 0.3(0.10) | |

| 5.04 **(2.08) | −2.45 **(0.05) | 4.00 **(1.94) | −0.99 **(0.02) | |

| 3.56 ***(1.22) | 4.90 **(1.70) | 2.99 **(0.09) | 4.30 **(0.20) | |

| 2.99 **(1.00) | 3.10 **(0.04) | 0.99 **(0.03) | 2.00 **(0.20) | |

| Dummy | Yes | No | Yes | No |

| 0.92 ***(0.02) | 0.58 *(0.05) | |||

| 15.09 **(3.90) | 13.99 **(7.90) | |||

| ESD | 0.089 | 0.010 | ||

| # of obs. | 220 | 170 | ||

| # of countries | 10 | |||

| Model 3: Macroprudential Policy Regime (2000–2021) | ECNO = 5.56DCPS *** − 0.78FCRRM ** + 2.65GCBRM *** + 2.40CRIM *** + 3.55MI-12 ** − 1.11BRIM * + 3.23ICEIUN − 2.95PCHPUN ** + 0.98INFL ** + 2.01TRD ** + 3.57PINVE **3.080GEF** + 4.10TOD ** − 2.67DCPS *** − 3.10FCRRM *** + 1.33GCBRM ** − 3.20CRIM *** + 2.00MI-12 *** − 2.09BRIM * + 1.10ICEIUN ** + 3.05PCHPUN ** + 0.67INFL + 1.08TRD ** + 3.57PINVE ***1.080GEF *** + 2.88TOD ** |

| Model 4: Non-macroprudential Policy Regime (1985–1999) | ECONO = −3.70DCPS *** + 1.56INFL ** + 3.39TRD *** + 3.00GEF *** + 1.90PINVE ** + 2.13TOD ** + 4.51DCPS *** − 3.35INFL * + 4.09TRD ** − 2.30GEF ** + 2.00PINV ** + 0.87TOD ** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dlamini, S.N.; Zungu, L.T.; Nkomo, N.Y. The Optimal Level of Financial Growth in View of a Nonlinear Macroprudential Policy Regime Model: A Bayesian Approach. J. Risk Financial Manag. 2023, 16, 234. https://doi.org/10.3390/jrfm16040234

Dlamini SN, Zungu LT, Nkomo NY. The Optimal Level of Financial Growth in View of a Nonlinear Macroprudential Policy Regime Model: A Bayesian Approach. Journal of Risk and Financial Management. 2023; 16(4):234. https://doi.org/10.3390/jrfm16040234

Chicago/Turabian StyleDlamini, Sifundo Ntokozo, Lindokuhle Talent Zungu, and Nomusa Yolanda Nkomo. 2023. "The Optimal Level of Financial Growth in View of a Nonlinear Macroprudential Policy Regime Model: A Bayesian Approach" Journal of Risk and Financial Management 16, no. 4: 234. https://doi.org/10.3390/jrfm16040234

APA StyleDlamini, S. N., Zungu, L. T., & Nkomo, N. Y. (2023). The Optimal Level of Financial Growth in View of a Nonlinear Macroprudential Policy Regime Model: A Bayesian Approach. Journal of Risk and Financial Management, 16(4), 234. https://doi.org/10.3390/jrfm16040234