1. Introduction

The financial services industry is expanding rapidly, and there is a growing number of digital innovations that, along with globalization, provide individuals with an increasing number of products and services. Rapidly evolving technologies and financial market integration have broadened the range of services offered and their availability. Even relatively simple financial products, however, can appear complex and incomprehensible, especially to a person who has not built up practical financial experience since youth. Therefore, a growing number of countries are recognising the value of financial literacy education. In recent years, many countries have developed and implemented national education strategies to improve peoples’ financial literacy, including Poland, Australia, Peru, Portugal, Italy, the United States, and Spain (

OECD 2020). They frequently focus primarily on the young generation, which ensures long-term progress.

Financial literacy and financial education are modern concepts. Financial literacy is not an absolute state: it is a continuum of abilities that are conditioned by factors such as age, family, culture, or residence, as will be discussed in the subsequent chapters. It represents the state of continuous development, enabling each individual to respond effectively to new events and a continuously changing economic environment (

NBS 2019). The European Economic and Social Committee has defined financial education as “the process by which consumers improve their understanding of financial products, financial risks, and market opportunities to make informed decisions about their finances” (

Pintó 2011, p. 2).

Policymakers in economies around the world recognize the importance of financial education. The European Union has been paying increased attention to citizens’ financial literacy since 2007, when the European Commission emphasised the need for financial education and called on member states to support it through public authorities, non-government organizations, and the financial services sector. Making financial education available to the general public, according to the Commission, will encourage consumers to plan both their spending and saving in order to avoid over-indebtedness (

Pintó 2011). In 2021, The European Banking Federation issued a Financial Literacy Playbook for Europe, outlining the work and ongoing activities, developments, and events in the field of financial education. It concluded that a growing number of countries in Europe are using public–private partnerships as a model for financial education. Such cooperation can be a key success factor in increasing financial literacy (

Katroshi et al. 2020). The Organisation for Economic Cooperation and Development (OECD) and its International Network for Financial Education provide governments with a unique forum for exchanging views and experiences, such as National Strategies for Financial Education, Financial Education and Women, Measuring Financial Literacy, and others (

Katroshi et al. 2020). The OECD 2016 Report (

OECD 2016a) gave an assessment of the most relevant and innovative financial education policies and initiatives at the intersection between financial education, financial consumer protection, and financial inclusion. Given the growing interest in financial education in Europe and the rapid development of many initiatives from various stakeholders, this report is complemented by other regional reports from Africa, Latin America, the Caribbean, and the Asia-Pacific.

In 2008, the Government of the Slovak Republic approved a Draft Strategy for Education in the Financial Field and in the Management of Personal Finances. Subsequently, the National Standard for Financial Literacy was developed, which, in addition to financial topics, also integrates consumer education, anti-corruption education, business education, and anti-fraud education. The current version of the National Standard for Financial, valid from September 2017, defines the breadth of knowledge, skills, and experience in the field of financial education and personal finance management among high school graduates.

Many institutions in Slovakia address the issue of the level of financial literacy. The National Bank of Slovakia (NBS) is aware that the low financial literacy of the population in Slovakia is a frequent cause of financial problems that consumers get into and is the reason for their dissatisfaction with financial services. One of the goals of the NBS’s communication policy is to further participate in the implementation of education aimed at supporting the development of financial literacy. To achieve this goal, the NBS prepared the Strategy of the National Bank of Slovakia to support financial literacy. In addition to the NBS, commercial banks and non-profit organizations also contribute to improving financial literacy. As an example, the Grant Idea for Schools from Poštová banka and the Slovenská sporiteľňa Foundation can be stated. A large range of long-term and short-term projects is also organised by the non-profit educational organization Ja Slovensko, such as Me and Money, Basics of Business, Applied Economics, and More Than Money (

NBS 2019;

O programe Ja a peniaze 2021).

Furthermore, many schools are implementing innovative e-learning teaching methods (

Štofko and Štofková 2014). Despite the aforementioned activities, research suggests that the level of financial literacy in Slovakia is not improving. In 2010–2017, the National Bank of Slovakia, in cooperation with the Statistical Office of the Slovak Republic, carried out a partial measurement of the financial literacy of adults, a module within The Household Finance and Consumption Survey. Despite this research, knowledge about the level of financial literacy of the adult population of Slovakia is currently considerably limited. However, looking at the data for Slovakia on property foreclosures, household indebtedness, and consumer behaviour, we can conclude that the level of financial literacy of a significant part of the population is insufficient. The poor state of financial literacy in Slovakia compared to other countries is also pointed out by related surveys such as the Financial Literacy Around the World, Standard & Poor’s Financial Literacy in the World, and the Slovak Investment Behaviour Survey. A 2017 survey of undergraduate students from the Slovak University of Technology found that only 10% of respondents had a relatively good level of financial literacy (

Janáková and Fabová 2017). On the contrary, up to 50% of students had financial literacy only at a basic level. These results were worse than the results of the previous analysis conducted in 2007. Similarly, the research of financial literacy at the University of Žilina (

Böhm et al. 2021) in 2020, which examined the impact of secondary education on the level of financial literacy, showed that the success rate of first-year undergraduate students was just 56%, even though students of economics were also included in the study. One explanation for poor financial literacy may be the insufficient connection of theoretical knowledge with practical requirements, which is an essential part of the educational process (

Štofková et al. 2016). In addition to the aforementioned studies, the research of

Pružinský and Mihalčová (

2014) evaluated the financial literacy of students at three universities in Slovakia and analysed the correlation between them. Similarly,

Zvaríková and Majerová (

2014) aimed at determining the financial literacy of the adult population in Slovakia without a special focus on university students.

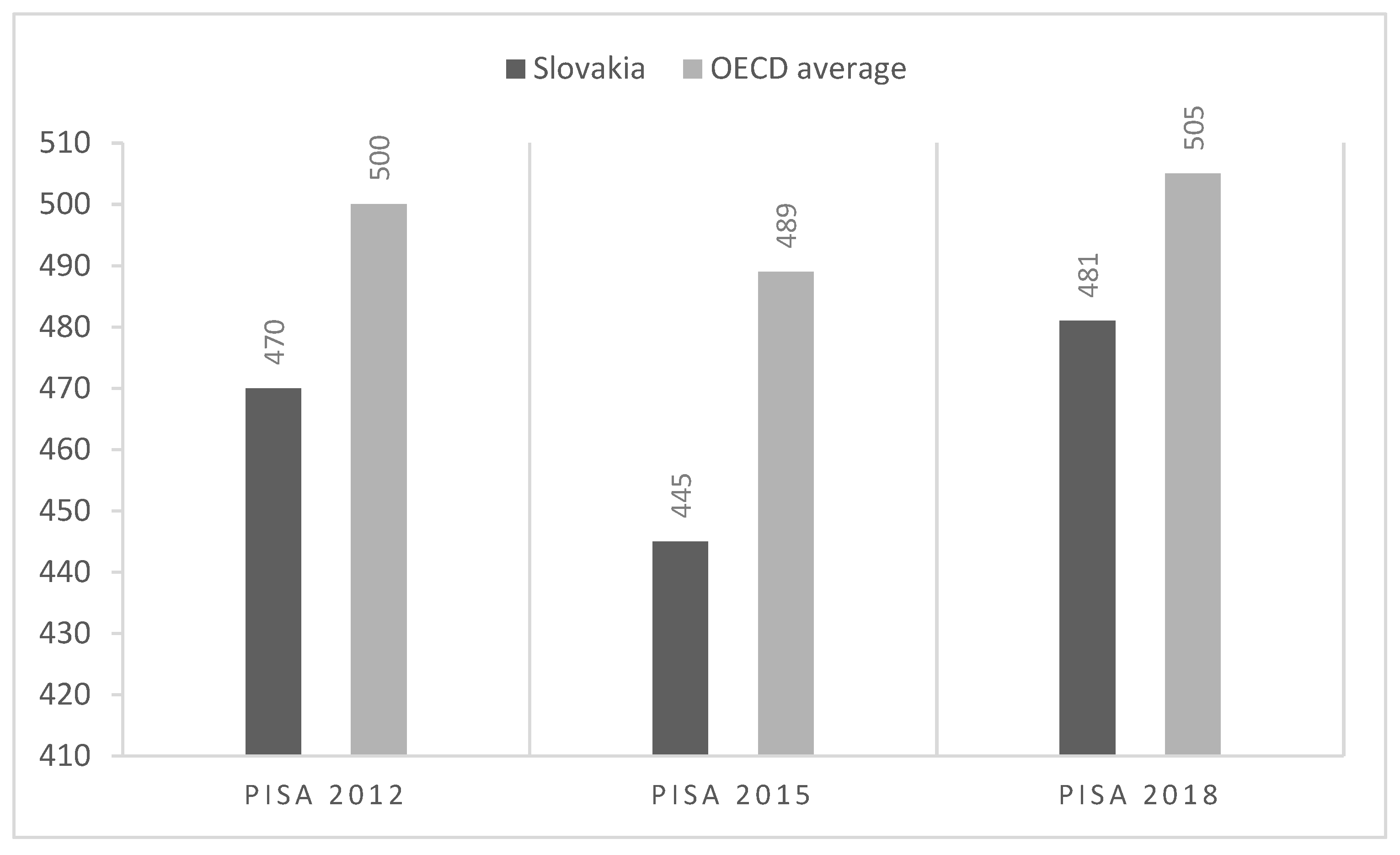

International comparisons of students’ level of knowledge at three-year intervals are regularly provided by the Program for International Student Assessment (PISA), which documents the level of students’ knowledge in the field of reading, science, and mathematics, as well as financial literacy. In the area of financial literacy, Slovak students gained an average of 470, 445, and 481 points in 2012, 2015, and 2018, respectively, which were all below the OECD average. An important finding is that Slovakia has ranked among the countries with an above-average impact of socioeconomic background on student performance (

OECD 2020). It is alarming that Slovakia did not apply for the PISA 2021 financial literacy testing. The results of Slovak students compared to the OECD average in PISA testing are shown in

Figure 1.

The absence of consistent financial literacy education from preschool to secondary school, as well as a lack of teacher training, might be among the reasons why Slovak students have deteriorated in testing. Furthermore, as PISA assessments consistently reveal, the level of financial literacy at the system, school, and student levels is related to the student’s socioeconomic status—and there are considerable inequalities in Slovakia in this regard. The Economic, Social, and Cultural Status Index (ESCS), introduced by PISA, was created on the basis of the following variables: International Socio-Economic Index of Occupational Status; the highest level of education of the student’s parents, converted into years of schooling; PISA family wealth index; PISA index of home educational resources; and the PISA index of possessions related to “classical” culture in the family home (

OECD 2002). The ESCS index summarizes many different aspects of student’s family backgrounds and can be used to estimate the impact of socioeconomic status on student performance (

OECD 2016b).

Current Research

Most researchers tried to identify the factors that affect the level of financial literacy. The following section describes research that focused mainly on the influence of socioeconomic factors on the level of financial literacy.

Rudeloff (

2019) investigated how various informal learning opportunities affect students’ financial literacy. Discussions with parents and siblings were among the most important informal source of financial education, but socioeconomic background was associated with the level of financial literacy as well. The aim of the study of

Setiyani and Solichatun (

2019) was to examine the impact of financial literacy and financial socialisation on financial wellbeing through financial behaviour. In particular, they pointed to the positive influence of parents, friends, and the media on financial behaviour. The research of

Pahlevan Sharif et al. (

2020) revealed that parents’ behaviour directly affects young adults’ financial behaviour. The impact of parents’ financial behaviour on their children, especially in the area of financial planning, was also studied by

Kagotho et al. (

2017). The effect of social influence on savings behaviour was evaluated by

Jamal et al. (

2015) as well. Their results suggested that the influence of family and peers played an important role in shaping students’ financial behaviour. According to

Vijaykumar (

2022), the effect of family discussions is the most important factor of financial literacy. The influence of parents on children’s financial decisions and gender differences was also highlighted in a study by

Agnew et al. (

2018). Their findings support the argument that a different type of financial socialisation occurs depending on the child’s gender. Specifically, for men, financial literacy is positively influenced by objective mathematical skills, while for women, the main predictor of financial literacy is self-efficacy (

Al-Bahrani et al. 2020). Inequality in the financial literacy of Korean adolescents with respect to gender, parental education, financial socialising agents, financial experience, monetary attitudes, and demographic characteristics has been studied in (

Sohn et al. 2012).

Dangol and Maharjan (

2018) assessed the impact of parents’ education, gender, marital status, and income and the influence of parents and peers on the economic behaviour of Nepalese youth.

Ansong and Gyensare (

2012) attempted to find a link between financial literacy and demographic characteristics. They observed that age, work experience, and the mother’s education were positively associated with financial literacy, while, contrary to previous research, the level of study outcomes, work location, father’s education, and the source of education on financial literacy were not significantly correlated with financial literacy.

Lopus et al. (

2019) showed that increases in students’ financial literacy knowledge in West Java were found to relate to prior knowledge, job experience, and the type of school they attend.

Lusardi and Mitchell (

2009) showed that financial literacy was closely linked to gender, parental education, sociodemographic characteristics, and family financial requirements. The influence of parents’ level of education on university students’ financial knowledge, along with other indicators such as race, gender, and age, was studied by

Murphy (

2005). Consistent with the results of previous studies, the impact of academic skills along with students’ personal and family backgrounds on the level of financial literacy of undergraduates in Malaysia was confirmed in

Sabri et al. (

2010). In addition,

Lusardi et al. (

2009) examined young peoples’ financial literacy using data from the National Longitudinal Youth Survey. Their findings give evidence that financial literacy is strongly related to sociodemographic characteristics and the family’s financial sophistication. However, as Brillová pointed out, parents who should be a role model in their children’s financial planning often have irresponsible financial behaviour themselves (

Brillová 2017).

Gutter et al. (

2010) examined the relationship between financial behaviour and age, race, marital status, school status, income, and loan amounts.

Danes and Hira (

1987) showed that gender, income, marital status, and students’ employment have a significant impact on their financial literacy levels, as previous research has shown. The aim of the study of

Gutter and Copur (

2011) was to examine the relationship between gender, race, marital status, and the use of credit cards on the one hand and the financial wellbeing of students on the other. In addition to gender differences, significantly strong ethnic inequality was found in a study by

Falahati et al. (

2011).

de Clercq (

2009) also examined whether age, gender, and students’ out-of-pocket allowances had an impact on financial opportunities.

Bhushan and Medury (

2013) concluded that there is gender disparity in the level of financial literacy. They confirmed the hypothesis that the level of financial literacy of students depends on education, income, and place of employment, but the hypothesis of dependence on the place of residence was not confirmed. The financial literacy survey among university students also identified gender differences in financial literacy levels and confirmed the impact of work experience, age, and school success on students’ financial literacy (

Chen and Volpe 2002).

Falahati and Paim (

2011) examined the gender differences in the financial wellbeing, financial socialisation, and financial knowledge among Malaysian college students. In contrast to previous research, their overall findings indicated higher financial satisfaction of female students over male students, which could be due to their lower levels of desire and expectations from life in the male preference culture. Other research findings, namely that female students achieved a lower level of financial knowledge and later-age financial socialisation, are in line with other research.

Unlike other research, the study of

Sachitra and Wijesinghe (

2018) conducted on management undergraduate university students in Sri Lanka suggested that female university students performed better in money management behaviour tests than male students. They argued that attending university is one of the rare occasions where young women have the right to stay away from home, and therefore have the responsibility to manage their money independently. The study revealed that economic, social, and psychological factors significantly affect money management behaviour as well.

Financial literacy education is an ongoing process. Products and services that require new knowledge and skills are constantly emerging in the financial market. In addition, since financial decisions are made by people of all ages from children who are learning to save small amounts, from young people who make their first money to adults who want to secure their first home, it is useful to provide financial education at all ages. Based on the above analyses, it is evident that in the field of financial literacy testing, the most attention is paid to primary and secondary school students in national and international research, while testing of university students is not in the spotlight. Likewise, Slovak university students are not sufficiently tested, and this study fills a gap in this area. This research attempted to identify factors influencing the financial literacy of university students in Slovakia, with the goal of determining whether students between the ages of 15 and 19 can improve their financial literacy—for example, because they use banking services to a greater extent.

2. Materials and Methods

The main goal of the research was to identify the factors that most influence the level of financial literacy and to assess the magnitude of their influence, using Tobit regression analysis. As already mentioned, there are many possible factors influencing the level of financial literacy. The most frequently referenced socioeconomic and demographic characteristics impacting financial literacy are, for example, specifically identified in

Oliveira and Santana (

2019). We also used prior research in this study to determine the factors influencing financial literacy, as indicated in the chapter “1.1 Current research”. We identified the most frequently investigated factors that have been included in the previous research on the correlation between financial literacy and socioeconomic factors and classified them into five groups—gender, secondary education, family’s economic background, demographic factors, and economic behaviour of the student. These five groups, along with relevant sources, are listed in

Table 1.

The following is a detailed description of the five groups of factors used in the research.

Gender: Students stated their gender in the questionnaire—male, female, NaN.

Secondary education: In Slovakia, the secondary education system consists of grammar schools (which prepare students for university studies and provide them with general education), business schools (which prepare graduates for business and entrepreneurial functions), and other vocational schools. Students also reported their average success rate in secondary education. The classification scale of students in schools in Slovakia consists of five levels: 1 excellent, 2 commendable, 3 good, 4 sufficient, 5 insufficient. Respondents were consequently divided into three groups: average grade up to 1.5, average grade from 1.5 to 2.0, and average grade greater than 2.0.

The family’s economic background: Students specified the average net monthly income of their family: from less than 1500 €, from 1500 € to 3000 €, and more than 3000 €. Students also reported their monthly earnings for part-time work or any other type of additional income. They chose from three options: no income from part-time work, less than 200 €, and more than 200 €. Other information provided by students was the highest educational attainment of their father and mother. There were two options to choose from: lower education or secondary and tertiary education. Students also reported the amount of monthly allowance they received from parents. They could choose from two options: less than 60 € and more than 60 € per month.

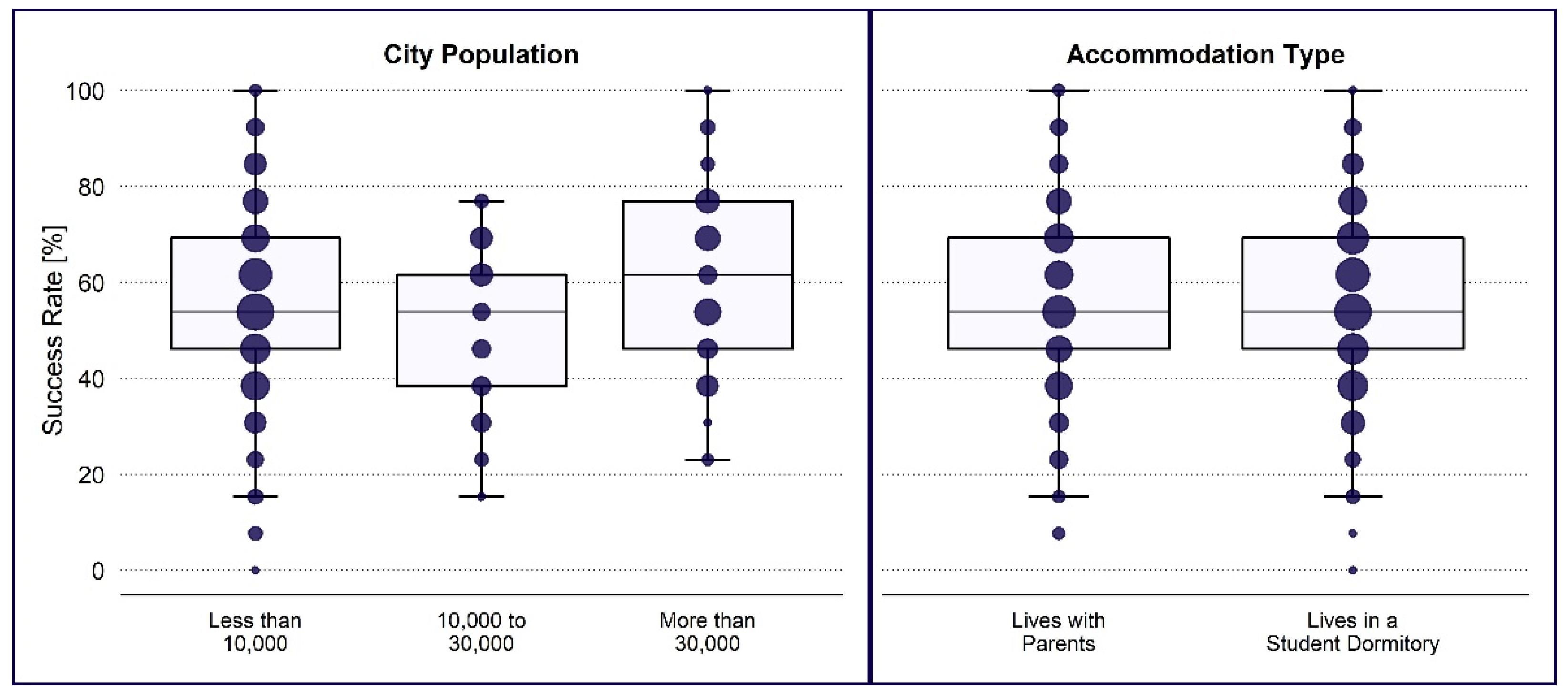

Demographic factors: Slovakia is a small country with a population of just over 5.4 million. Most cities have only a few thousand inhabitants, and as a result, students could choose their place of residence from three alternatives: up to 10,000 inhabitants, from 10,000 to 30,000 inhabitants, and over 30,000 inhabitants. Students also stated whether—during their studies at the university—they lived at home with their parents or not (in a university campus or rental apartment, for example).

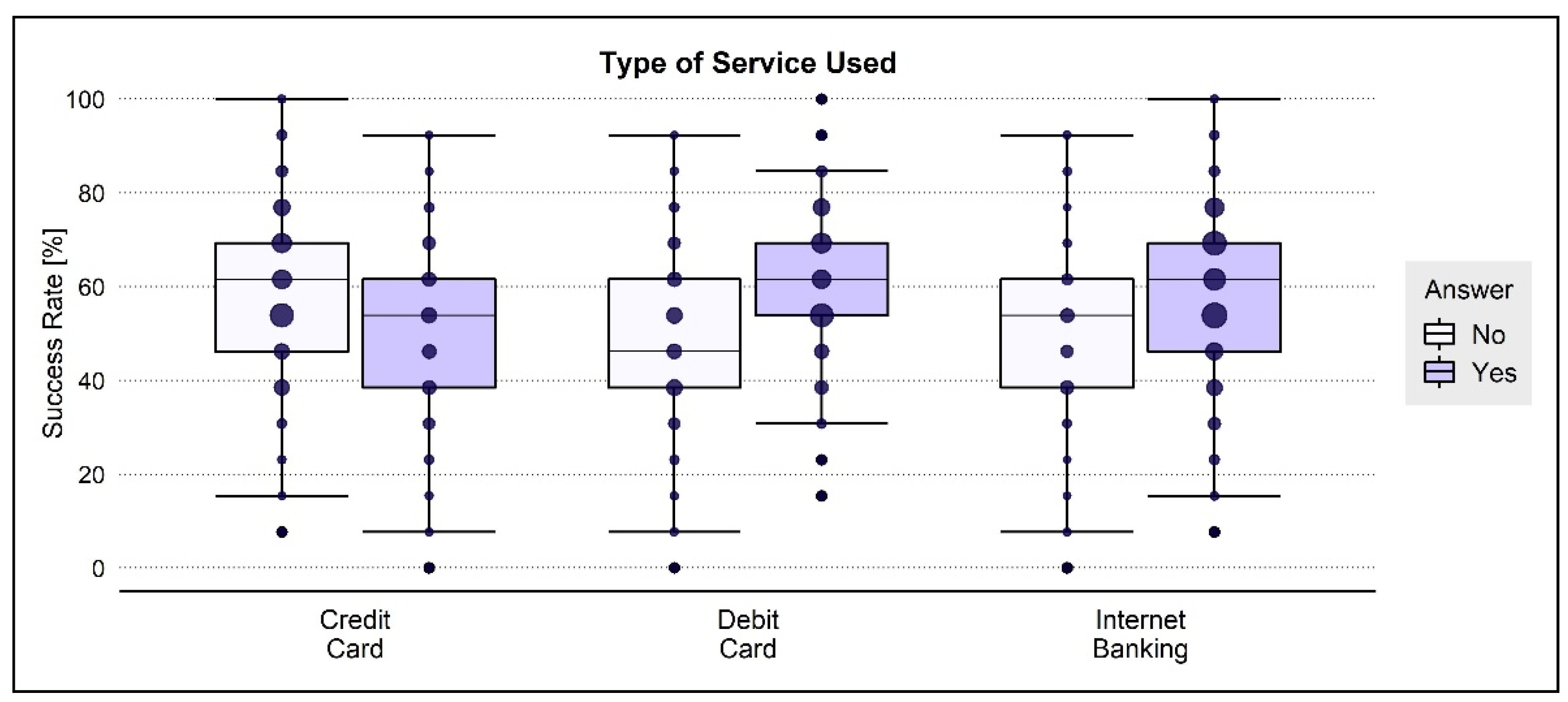

The economic behaviour of the student: The main socialisation factors were also included in the questionnaire. Students listed their information sources on financial literacy from family, friends, press, media, or school. Students listed the banking products they actively used, namely debit card, credit card, and internet banking. Additionally, the students were introduced to a model situation that was to detect the degree of their risky behaviour. Students should have answered the question: “If you want to buy a product but don’t have the money, what would you do?” They chose from the answers: “I borrow money from relatives or friends.” or “I won’t buy it”.

To meet the research goal, the following hypotheses were formulated (

Table 2):

This research included a questionnaire and a financial literacy test. The questionnaire contained nineteen questions focusing on demographic, educational, and socio-economic factors that could affect students’ financial literacy. The test subsequently examined the general knowledge of students in the field of financial literacy with regard to the financial market of the Slovak Republic. There were 13 items included in the test. For each correctly answered question, students scored one point, and then their overall success rate was calculated. The financial literacy test contained items that were inspired by the tasks of the PISA 2015 tests, tasks from other financial literacy surveys in Slovakia, and our own experience with teaching subjects focused on financial literacy. Only items with the possibility of one correct answer were included in the test. Open-ended items were not included in the test either. The relevance of the questions was verified in the pre-survey, where 50 students answered all 13 questions on financial literacy. Since no disproportions were observed, all questions were used in the test.

The research focused on the undergraduate students of the University of Žilina and was conducted during the 2019/2020 school year. Students had 60 min to complete a questionnaire and a financial literacy test. A sample of 50 students was first evaluated to see whether the questions and test items were well defined and to determine the amount of time required to complete the test. Subsequently, 363 first-year bachelor’s students were tested.

Students from all types of secondary schools from different regions took part in the research, and both sexes were equally represented. It can be stated that the examined students formed a representative sample of students from Slovakia at technical and economic universities. The sociodemographic characteristics of the sample are shown in

Table 3.

Data analysis was performed in two steps. In the first step, the students’ success ratio was calculated. In the second step, a Tobit regression model was used to determine which determinants influence the financial literacy of students. Factors included in the regression analysis were selected based on previous studies. The Tobit regression model was designed to estimate the linear relation between variables. Using the variation inflation factor, it was verified that the selected factors are not linearly dependent, and multicollinearity is not present. All control variables used in the regression analysis are shown in

Table 4.

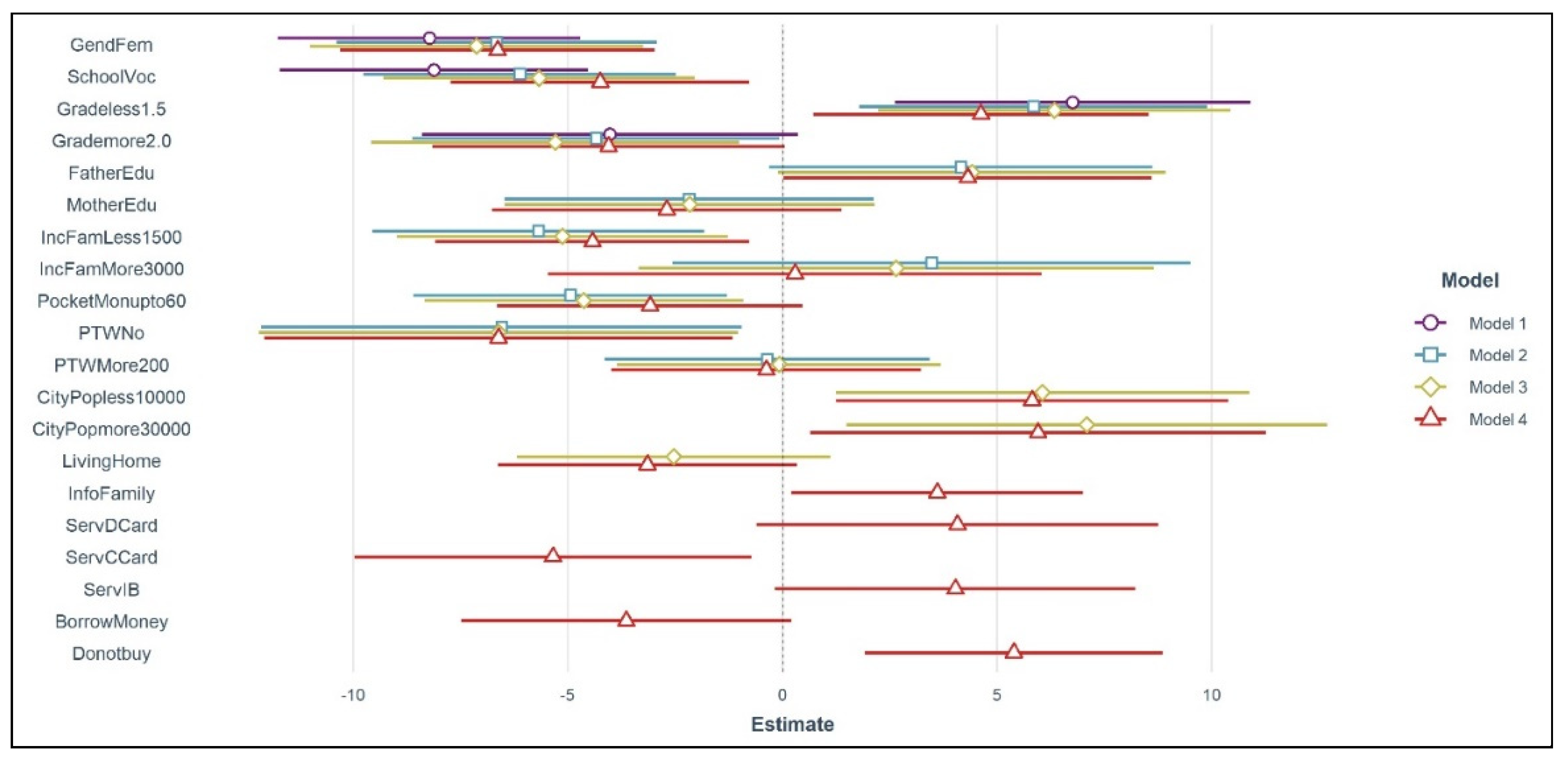

In order to analyse the impact of individual groups of factors on financial literacy, four regression models were constructed. The first model (Model A) included variables from the Gender and Secondary Education groups. In Model B, variables from the Family’s Economic Background group were further added to the variables from the previous two groups. The third Model C contained variables from four groups: Gender, Secondary Education, Family’s Economic Background, and Demographic factors. The last Model D included the variables from all five groups.

For data processing, R statistical language and environment for statistical computing was used (

R Core Team 2013). The censReg package (

Henningsen 2020) was used to calculate censored regression model.

3. Results

The research on the level of financial literacy of university students included 363 students. The average success rate of the test was 56.18%, which equals the average level of financial literacy. All questions were answered correctly by three students, and one student did not have a single correct answer. Descriptive statistics of students’ financial literacy test results are in

Table 5.

Tobit’s ordinary least squares regression analysis (OLS) was used to assess the level of influence of the five groups of indicators on the level of financial literacy of students. Using the criteria of the coefficient of variation inflation (VIF), selected indicators were tested for multicollinearity, and all variables had VIFs within acceptable limits (less than 5). To assess the impact of selected variables on the level of financial literacy, four regression models A–D, described in the previous chapter, were constructed.

Table 6 summarizes the results of the multiple regression analysis of all four models. Estimated values of all variables together with corresponding

p-values are presented.

Model A contained four explanatory variables, three of which were statistically significant at the 0.001 significant level—Gender, SchoolVoc, Gradeless1.5, Grademore2.0. This model explained approximately 12% of the variability in financial literacy. Model A shows that women had a financial literacy level 8.41 percentage points lower than men. Gender was statistically significant in the other three models as well, with a level of significance of 0.001. On average, women had a level of financial literacy 6.8–8.4 percentage points lower than men.

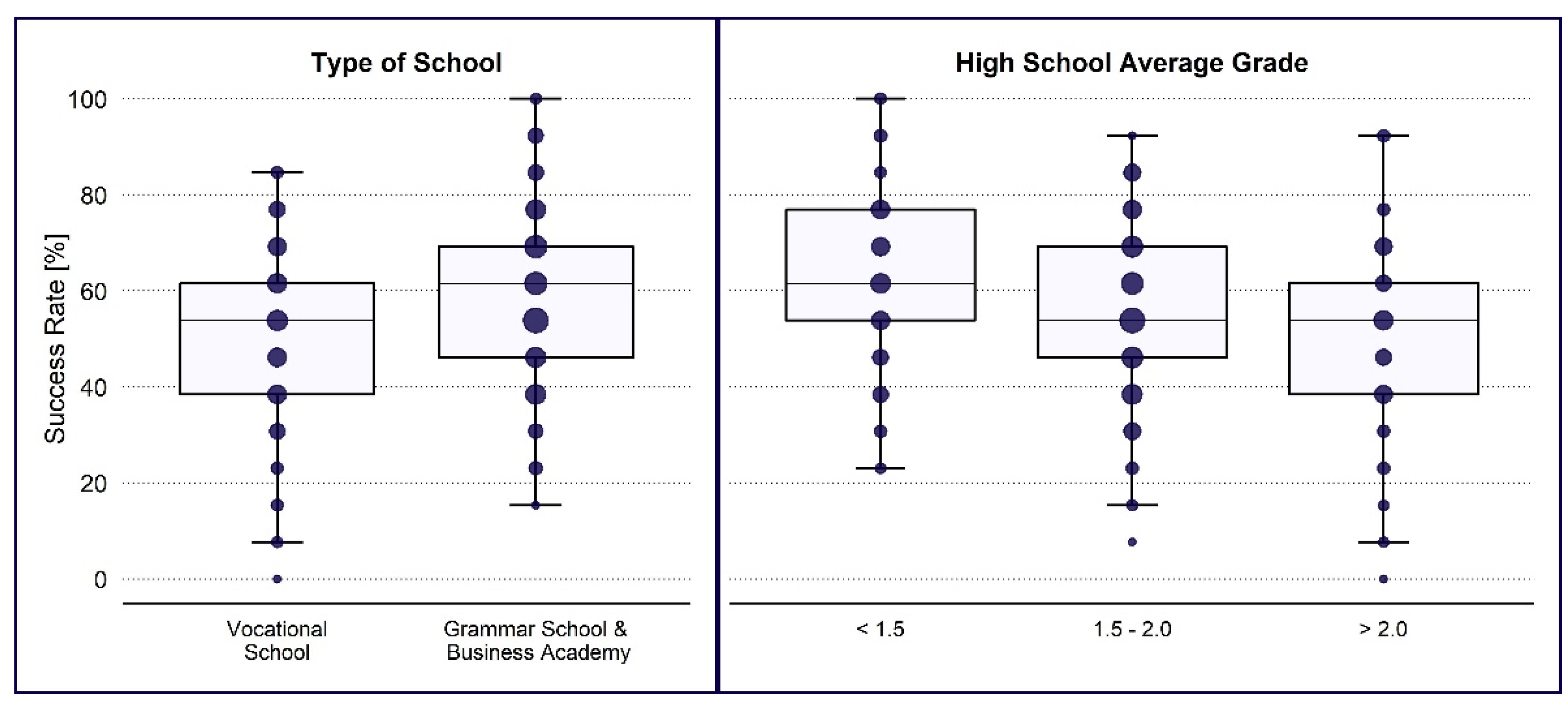

Figure 2 shows the success rate of students in the financial literacy test depending on the type of high school and their high school performance. Model A further shows that students with an average grade of less than 1.5 in high school performed almost 7 percentage points better than students with an average grade of 1.5 to 2.0, and students with an average grade in high school greater than 2.0 had 4 percent worse results as their peers with a grade from 1.5 to 2.0.

Gradeless1.5 and

Grademore2.0 were statistically significant factors in the other three models as well. Students with learning outcomes below 2.0 had a lower level of financial literacy than students with scores from 1.5 to 2.0, ranging from 4.1 percentage points (Model D) to 5.4 percentage points (Model C). Students with excellent high school results of up to 1.5 had a better level of financial weight from 4.8 percentage points (Model D) to 6.6 percentage points (Model C) compared to their peers with results from 1.5 to 2.0.

In Model A, SchoolVoc was a statistically significant variable, with students studying at vocational and business schools having a level of financial literacy 8.27 percentage points worse than high school students. SchoolVoc was also statistically significant in other models, with students studying at vocational and business schools having worse financial literacy scores, from 4.3 percentage points (Model D) to 6.2 percentage points (Model B), than students studying at grammar schools.

Model B contained eleven explanatory variables, with the variables FatherEdu, MotherEdu, IncFamLess1500, IncFamMore3000, PocMonupto60, PTWMore200, and PTWNo added to the variables from Model A. Of the seven added variables, two were statistically significant at the significance level of 0.001—Gender, SchoolVoc; three were statistically significant at the level of significance 0.01—Gradeless1.5, IncFamLes1500, PocMonup60; and two were statistically significant at the level of significance 0.05—Grademore2.0 and PTWNo. This model explained approximately 17% of the variability in financial literacy.

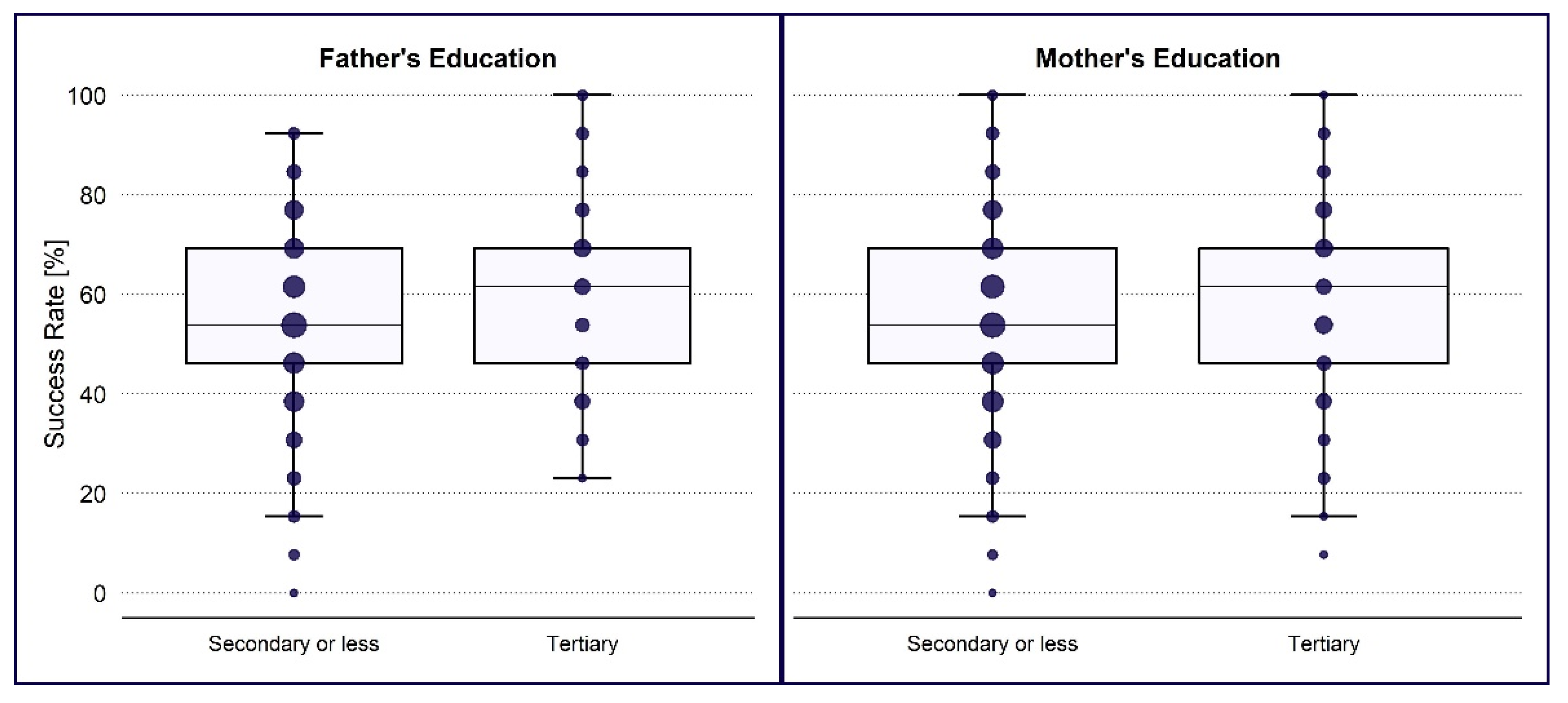

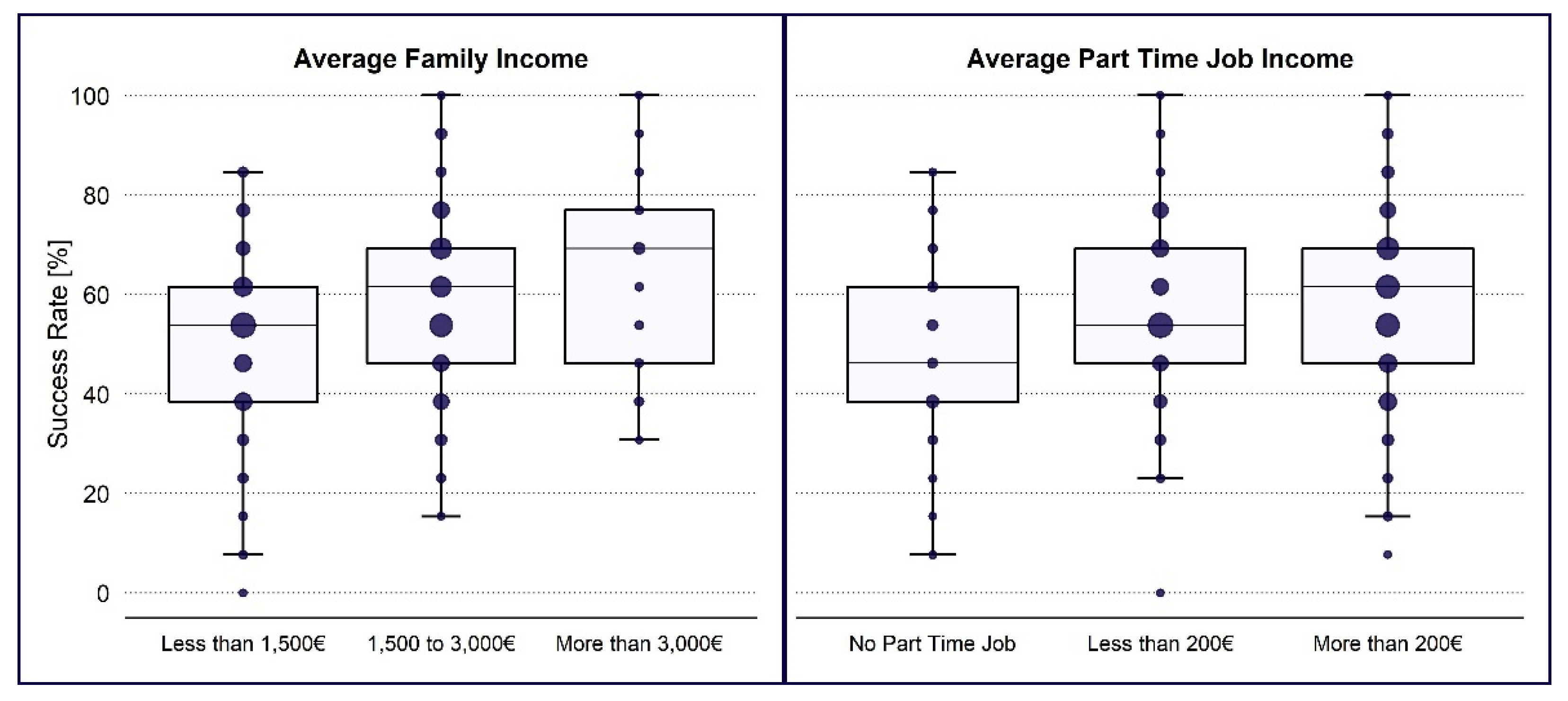

Figure 3 and

Figure 4 show the success rate of students in the financial literacy test depending on the education of their parents and their family’s economic background.

The variable FatherEdu in Model B was not statistically significant, but in Models C and D it was statistically significant at the level of significance 0.05. If the father had a tertiary education, students had better results by 4.69 and 4.45 percentage points in Models C and D, respectively, than students whose father did not have a tertiary education. The MotherEdu variable was not statistically significant in any of the models where it was used (Models B–D).

IncFamLess1500 was statistically significant in all three Models B, C, and D. Students with a family income of up to 1500 € performed worse on the financial literacy test than students with a family income of 1500 € to 3000 €, ranging from 5.8 percentage points in Model B to 4.5 percentage points in Model D. PocMonupto60 was statistically significant in Models B and C. If students received pocket money of more than 60 € per month, they performed approximately 5 percentage points better than students with a smaller amount of pocket money. The PTWNo variable was statistically significant in all three Models B, C, and D. Students who had no side income scored approximately 6.6 percentage points lower than students who had part time work.

Model C contained fourteen explanatory variables, with the variables

CityPopless10000,

CityPopmore30000 and

LivingHome added to the variables from Model B. Variables

CityPopless10000,

CityPopmore30000 were statistically significant at the level of significance 0.05. This model explained approximately 19% of the variability in financial literacy. Students living either in small towns with less than 10,000 inhabitants or in larger cities with more than 30,000 inhabitants had better financial literacy results by an average of 6 percentage points than students living in a city with a population of 10,000 to 30,000. The

LivingHome variable was not statistically significant in any of the models.

Figure 5 shows the success rate of students in the financial literacy test depending on the demographic factors.

The fourth Model D contained twenty explanatory variables, with the variables InfoFamily, ServDCard, ServCCard, ServIB, BorrowMoney, and Donotbuy added to the variables from Model C. Variables InfoFamily, ServCCard, ServIB were statistically significant at the level of significance 0.05, and Donotbuy was statistically significant at the level of significance 0.01. This model explained approximately 28% of the variability in financial literacy.

Figure 6 shows the success rate of students in the financial literacy test depending on the type of services used by students.

Students with their family as their primary financial literacy agent performed 3.77 percentage points better than students who had another primary source of information. Students who used a credit card performed 5.47 percentage points worse than students who did not use one, and conversely, students who used internet banking had 4.18 percentage points better results than students who did not use it. Students, whose answer to the question, “If you want to buy a product but don’t have enough money, what would you do?”, was: “I won’t buy it.”, had 5.20 percentage points better financial literacy results than students who did not choose this answer.

The parameter estimates of all four regression models along with 95 percent confidence intervals are shown in the

Figure 7. The robustness of computational models can also be seen in this figure.

4. Discussion

The main goal of this research was to identify the factors that most influence the level of financial literacy and to assess the magnitude of their influence using Tobit regression analysis. In this part, the validity of the stated hypotheses will be evaluated.

HGender: The gender factor has a statistically significant impact on the financial literacy level.

The results of this research are consistent with most previous studies. On average, women performed 8.41 percentage points worse on the financial literacy test than men. Similar results were shown in a study by

Lusardi et al. (

2009), in which a gap of 13% in the correct response rate to the questions of inflation and risk diversifications was found. In addition,

Bhushan and Medury (

2013) reported that women’s mean score was about 10% lower than men’s. However, further research shows that these differences are not so clearcut. For example, in terms of money management,

Sachitra and Wijesinghe (

2018) argued that women performed better in money management than men.

Falahati et al. (

2011) demonstrated statistically significant better results for women in financial management. Similarly, female students’ spending behaviour was safer than that of male students, but on the contrary, men’s financial management in savings was significantly better.

Agnew et al. (

2018) demonstrated another significant gender difference. If girls were under parental supervision, they spent 200% more pocket money compared to parents not being present. However, this difference did not exist for boys.

Despite the three studies mentioned, the majority of research has shown that women have a statistically significant lower level of financial literacy. As early as 2012, the G20 Leaders’ Declaration recognised the need for women to gain access to financial services and financial education and asked their partners—OECD and the World Bank—to identify barriers women may face and call for a progress report to be delivered by the next Summit (

Alliance for Financial Inclusion 2012). In addition, the OECD launched the Gender Initiative in 2010 to examine existing barriers to gender equality in education, employment, and entrepreneurship in order to improve policies and promote gender equality in the economies of OECD countries. However, this study—together with other studies mentioned—indicates that these long-term initiatives are not yet providing expected outcomes, as also indicated by the findings of this study.

HSecondaryeducation: The secondary education factors have a statistically significant impact on financial literacy levels.

Research published so far has shown a relationship between students’ level of education and their level of financial literacy. For example,

Chen and Volpe (

2002) found that education, class ranking, and experience had a statistically significant impact on financial literacy.

Amagir et al. (

2020) showed that Netherland students on the lowest track in high school had lower levels of financial literacy. In addition,

Lusardi et al. (

2009) concluded that education attainment was a clear and strong determinant of financial literacy. More specifically,

Lusardi and Mitchell (

2009) stated that financial literacy is closely related to the mathematical skills required at a young age.

Rudeloff (

2019) proved that interest in economics, education aspirations, and mother language grade were positively correlated with students’ financial literacy. In addition, the goal of

Sabri et al. (

2010) was to examine the financial literacy of Malaysian university students depending on their academic ability. However, their research did not yield statistically significant results. In addition,

Ansong and Gyensare (

2012) showed that the level of study was not significantly correlated with financial literacy.

This research has shown that secondary education has a statistically significant positive effect on the level of financial literacy, with a difference of 9 to almost 12 percentage points.

This research also examined the dependence of financial literacy on the type of secondary school attended. Students studying at vocational and business schools had worse financial literacy scores, from 4.3 percentage points to 6.2 percentage points, than students studying at grammar schools. On the contrary, the results of

Kozina and Ponikvar (

2014) suggested that the likelihood of students’ confidence in their financial management capability and knowledge was significantly higher for students that did specialize in economics or business studies.

These results suggest that the level of financial literacy cannot be separated from the overall students’ level of education. Financial literacy should not be viewed as a standalone subject, but rather as an integral aspect of the broader educational process. Students do not only have to acquire knowledge in the field of finance in classes specifically dedicated to financial literacy, but also in other lessons. We consider this to be a key factor leading to an improvement in financial literacy in Slovakia.

HFamilyeconomicbackground: The family’s economic background factors have a statistically significant impact on financial literacy level.

This research confirmed the impact of the family’s economic background on the level of financial literacy. It turned out that the highest achieved education of the father had a statistically significant effect in the two models, while the influence of the mother’s education was not statistically significant in either model. Similarly, previous research has yielded ambiguous results. According to

Lusardi and Mitchell (

2009), parental education was a strong predictor of financial literacy: if a mother graduated from university, the likelihood of correctly completing the test was almost 5 percentage points higher. Moreover,

Lusardi et al. (

2009) showed that the mother’s education was strongly associated with financial literacy: respondents whose mothers graduated from college had correct response rates about 19 percentage points higher for the inflation question and 18 percentage points higher for the risk diversification question. Conversely,

Ansong and Gyensare (

2012) showed that the mother’s education was positively significantly correlated with respondents’ financial literacy, while the father’s education was not.

Amagir et al. (

2020) also found that the mother’s university education had a positive effect on the financial literacy of 15-year-old students in the Netherlands.

It concludes that most studies have shown the impact of parents’ education on their children’s financial literacy, but with inconsistent conclusions. The mechanism of knowledge transfers between parents and their children, which may differ from country to country due to different cultural and social stereotypes, has not yet been precisely explored and explained.

This research showed that students from families with the lowest incomes (up to 1500 €) have a statistically significant lower level of financial literacy by about 5 percentage points compared to wealthier families. However, other differences did not appear to be statistically significant.

Lusardi and Mitchell (

2009) showed that a family’s financial sophistication played an important role. Students whose parents owned stocks were over 7 percentage points more likely to answer the risk diversification question correctly. Furthermore, students whose parents had retirement savings were 6 percentage points more likely to answer correctly. Similarly,

Lusardi et al. (

2009) concluded that the differences in a family’s financial sophistication resulted in the differences in correct response rates to the inflation and risk diversification questions by at least 11 percentage points in both questions—and these differences were statistically significant. It is apparent that students acquire financial literacy not only through school, but especially through their own life experience, where the family plays an important role.

Other research focused on the student’s income rather than the student’s family’s income. Therefore, factors describing students’ income were included in this research—pocket money or money from a part-time job. In this research, it turned out to be important whether the student had part-time work, and not how big their income actually was.

Chen and Volpe (

2002) and

Sachitra and Wijesinghe (

2018) also indicated that work experience and working hours had a statistically significant effect on financial literacy. On the contrary,

Rudeloff (

2019) did not find the impact of part-time jobs on financial literacy.

This research further showed that students with higher amounts of pocket money achieved a level of financial literacy 5 percentage points higher on average.

Sohn et al. (

2012) also demonstrated that monthly allowance was related with financial literacy. Our research showed that students with an average amount of pocket money (20 € to 100 €) had a higher financial literacy level than students with an amount of pocket money below 20 € or over 100 €.

This research has clearly confirmed that students who have part-time jobs have a higher level of financial literacy than students without experience with part-time jobs. At the same time, it turns out that it does not matter how large the amount of income is. Student work requires better time management, knowledge of employment contracts, taxes, social security, and health insurance. These experiences increase students’ general economic knowledge, which is likely to have a positive effect on their level of financial literacy. Simultaneously, it turned out that the more money students had, the better their financial literacy. This correlation was statistically significant, but it is not easy to determine the direction of this correlation. It is possible that students with higher income want to manage money better and therefore educate themselves in this area. On the contrary, it is possible that students with a higher level of financial literacy can better manage their money and increase their savings. It is likely that these two factors interact, though.

HDemographicfactors: The demographic factors have a statistically significant impact on the financial literacy level.

Slovakia is a small country with a population of just over 5.4 million. Only two cities in Slovakia have over 100,000 inhabitants, and most cities have only a few tens of thousands of inhabitants. This research showed that students living either in small towns with less than 10,000 inhabitants or in larger cities with more than 30,000 inhabitants had better financial literacy results by an average of 6 percentage points than students living in a city with a population of 10,000 to 30,000. The national testing from 2018, carried out by the Ministry of Education among primary school students, confirms the large differences in educational outcomes between districts and regions (

European Union 2018).

This research shows that secondary schools with the highest quality of education in Slovakia are located in larger cities. Since previous sections of this research have shown that the level of financial literacy is related to the overall level of education, it can be argued that knowledge in the field of financial literacy is also higher in large cities. Secondary schools are not located in small towns, so rural students complete secondary education in large cities. As a result, rural students also perform better in the area of financial literacy.

The geographical factor has been the subject of a small amount of research. A survey by

Bhushan and Medury (

2013) found that the financial literacy level did not depend on the geographical region. However, the same research has shown that the level of financial literacy was affected by the geographical location of work location. If the work was performed in an urban area, respondents demonstrated a level of financial literacy 5 percentage points higher than if it was performed in a rural area. This dependence, however, was not confirmed by the research of

Ansong and Gyensare (

2012), which concluded that work location was not significantly correlated with financial literacy.

The student’s place of residence during university did not prove to be a statistically significant factor influencing the level of financial literacy in our research. This relation was also discussed by

Sabri et al. (

2010), where a statistically significant negative effect of staying on campus on the level of financial literacy was demonstrated. Remarkably, this factor proved to be the second most important in their research.

HEconomicbehaviour: The students’ economic behaviour has a statistically significant impact on financial literacy levels.

Many studies—for example (

Jamal et al. 2015;

Setiyani and Solichatun 2019)—have suggested that the influence of family and friends, and in some cases the influence of the media and other opinion formers, can have a significant impact on the level of financial literacy. This hypothesis was confirmed by our research, which concluded that students whose family is their primary financial literacy agent outperformed students who had another primary source of financial literacy information by 3.77 percentage points. Research by

Sabri et al. (

2010), which examined the impact of interviews on the finances of children of different ages with parents, brought similar conclusions. Interviews with children had the third largest impact on the level of financial literacy. Similarly, research by

Jamal et al. (

2015) detected the influence of the family as the most powerful and significant factor influencing the level of financial literacy of Malaysian students. At the same time, this study stated that the second most powerful factor were peers and friends. In contrast,

Sohn et al. (

2012) confirmed in their research that those who chose the media as their primary agent of financial socialisation reported a higher level of financial literacy than those who had the family as their primary agent. The findings of our research are in line with previous studies, as they all came to the conclusion that the influence of parents is the key to better financial literacy for their children. Therefore, parents should discuss their family’s finance management with their children, encouraging them to save from an early age. It is also important for parents to show positive financial behaviour and to be a role model for their children in managing their finances. It turns out that friends and the media also have a positive effect on financial literacy, but these factors are more difficult to control.

We assumed that the use of banking products increases the level of financial literacy, because students practically encountered concepts that they previously knew only theoretically. The use of debit and credit cards, a bank account, and internet banking therefore appear to be factors that should positively influence the level of financial literacy. However, the research on this topic is inconclusive.

Sohn et al. (

2012), showed that the possession of a bank account was positively related to financial literacy, but

Sabri et al. (

2010) did not find that owning a saving account was positively correlated with financial literacy.

Sachitra and Wijesinghe (

2018) also analysed how using a credit card and performing online transactions affected their money management and economic, social, and psychological factors. The impact of credit card usage was not statistically significant, but performing online transactions had a statistically significant positive effect on money management and economic factors.

Our research has also yielded mixed results. The use of a debit card was not a statistically significant predictor of financial literacy. Students who used the credit card performed 5.47 percentage points worse than students who did not use it. In Slovakia, the term “credit card” is often incorrectly used instead of “debit card”. Moreover, very often these two terms are used interchangeably, although it is obvious that a credit card is a type of loan. In the Slovak Republic, the loan is provided only to people with permanent employment, and therefore, students usually do not have credit cards. Thus, it can be assumed that most students who claimed to use a credit card did not understand the difference between a credit card and debit card. This misunderstanding also points to the fact that the level of financial literacy of Slovak students is low.

In line with the hypothesis HEconomicbehaviour, students who used internet banking had better results than students who did not use internet banking by 4.18 percentage points.

The students were also introduced to a model situation that addressed their risky behaviour. Students who did not show a hazardous attitude toward money management had better financial literacy results by 5.20 percentage points. Similarly,

Gutter and Copur (

2011) evaluated the impact of risky usage of a credit card on the financial literacy of college students. They concluded that students who made late payments on their credit cards and did not pay their credit card balance each month had a significantly lower level of financial literacy than students who paid their credit card balance in full each month. Contrary to other research,

Popovich et al. (

2020) showed that attitudes are more debt-tolerant after the intervention.

5. Conclusions

A modern financially literate person is familiar with the concept of money and prices, and responsibly manages their financial budget in terms of future developments and changing life situations. Financial services are among the fastest growing industries, providing an increasing number of products and services on a daily basis. This trend is also supported by technological progress, the development of electronic services, and improvements in the availability of the services offered. However, for some customers, many of the products and services offered are complex, and they are unable to use them effectively.

To ensure the development of financial literacy, financial education alone is no longer enough for individuals to adjust their financial behaviour in an appropriate way. For effective education in the field of financial literacy, it is necessary to develop standardised techniques for its measurement and tools for assessing the effectiveness of financial education programs. At the same time, it is necessary to analyse in detail the factors that affect the level of financial literacy of the population in the long run.

The current system of education in the field of financial literacy shows signs of significant inequality in the field of gender, socioeconomic, demographic, and psychological indicators. To increase the overall financial literacy of the population, it is necessary to eliminate these disparities.

According to previous research, a variety of socioeconomic factors determine personal financial literacy. An important finding of this research is the identification of characteristics influencing financial literacy. The most important factors were the gender of the students, their high school performance, the type of high school attended, whether they had part-time work, and the city size in which the students lived. In many ways, the results of this research confirm the findings of previous research, but this research also reveals new correlations.

Consistent with other studies, this research shows a relationship between students’ levels of financial literacy and their overall learning outcomes. In addition, this research has shown that the level of financial literacy is also influenced by the type of secondary school they attended. This confirms that the curriculum and its complexity can significantly increase the level of financial literacy. A significant benefit of this research is the finding that students who did not have part-time work had lower financial literacy. This seems to be evidence that acquiring practical experience and the associated financial responsibilities are also an important source of financial knowledge. This research also revealed another important factor influencing the level of financial literacy, which is the population of the city in which the students lived. This fact is probably caused by a large variance in the quality of education between regions in Slovakia.

Furthermore, the purpose of this study was to determine if a student may improve their financial literacy between the ages of 15 and 19 and what factors impact this. As a result, we included variables in the regression analysis that reflected young people’s increasing familiarity with banking services and financial management. Research has shown that students who have more experience managing their own finances—which they received either from their parents as pocket money or earned through part-time jobs—have better results in financial literacy. Regular experience with banking services (such as internet banking and debit cards) also increases the level of financial literacy. It implies that young people’s financial literacy can improve as their own experience with money grows. However, these factors only complement other determinants, such as their education and family influence.

This research was carried out in the school year 2019/2020, and since the participants in the research were only first-year undergraduate students, it would be appropriate to repeat the research with a new sample of students. It will be interesting to see whether pandemic restrictions, distance learning, and the rise of electronic and digital services have changed students’ financial behaviour and knowledge.

Research suggests that educating students (including in the field of financial literacy) should start as soon as possible so that children can develop the right financial habits at an early age. The aim of future research will be to determine the impact of university studies on the level of financial literacy. It will also be important to monitor if the knowledge in the field of financial literacy is changing due to the growing number of new technologies. According to

Morgan et al. (

2019), the concept of Digital Financial Literacy and the need to develop digital financial education programs and skills also come to the fore. Appropriate tools need to be designed to develop programs to support digital financial education, as well as special programs for vulnerable groups, including older people, women, and the less educated.

The study sought to determine whether there is an increase in financial literacy between the 15th and 19th years of a student’s life. However, the limiting factor is that when comparing the results, the statistical sample is not the same, and thus it is not possible to directly compare the levels of financial literacy, but only the statistical significance of particular determinants. Research shows the importance of financial literacy socialisation agents, but in this research, we identify only the primary source of financial socialisation. More detailed research in this area could bring more accurate information about this type of relationship. Additionally, only Slovak students participated in the research. Currently, however, more and more foreign students are starting to study at Slovak universities. It would be appropriate to include them in further research and also examine financial literacy in the context of cultural background differences.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}