Japanese Economic Performance after the Pandemic: A Sectoral Analysis

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Literature Review

3. Evidence from the Stock Market

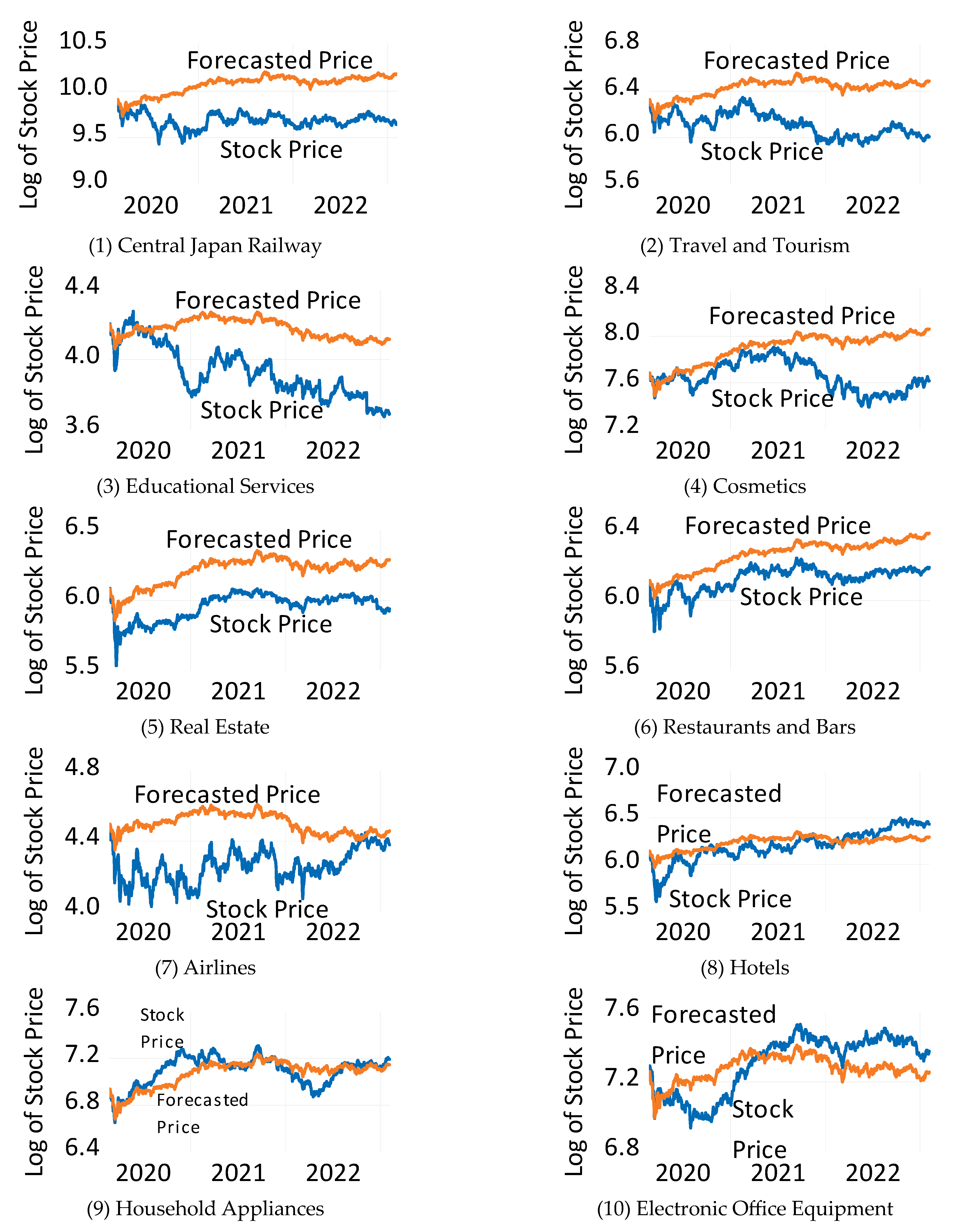

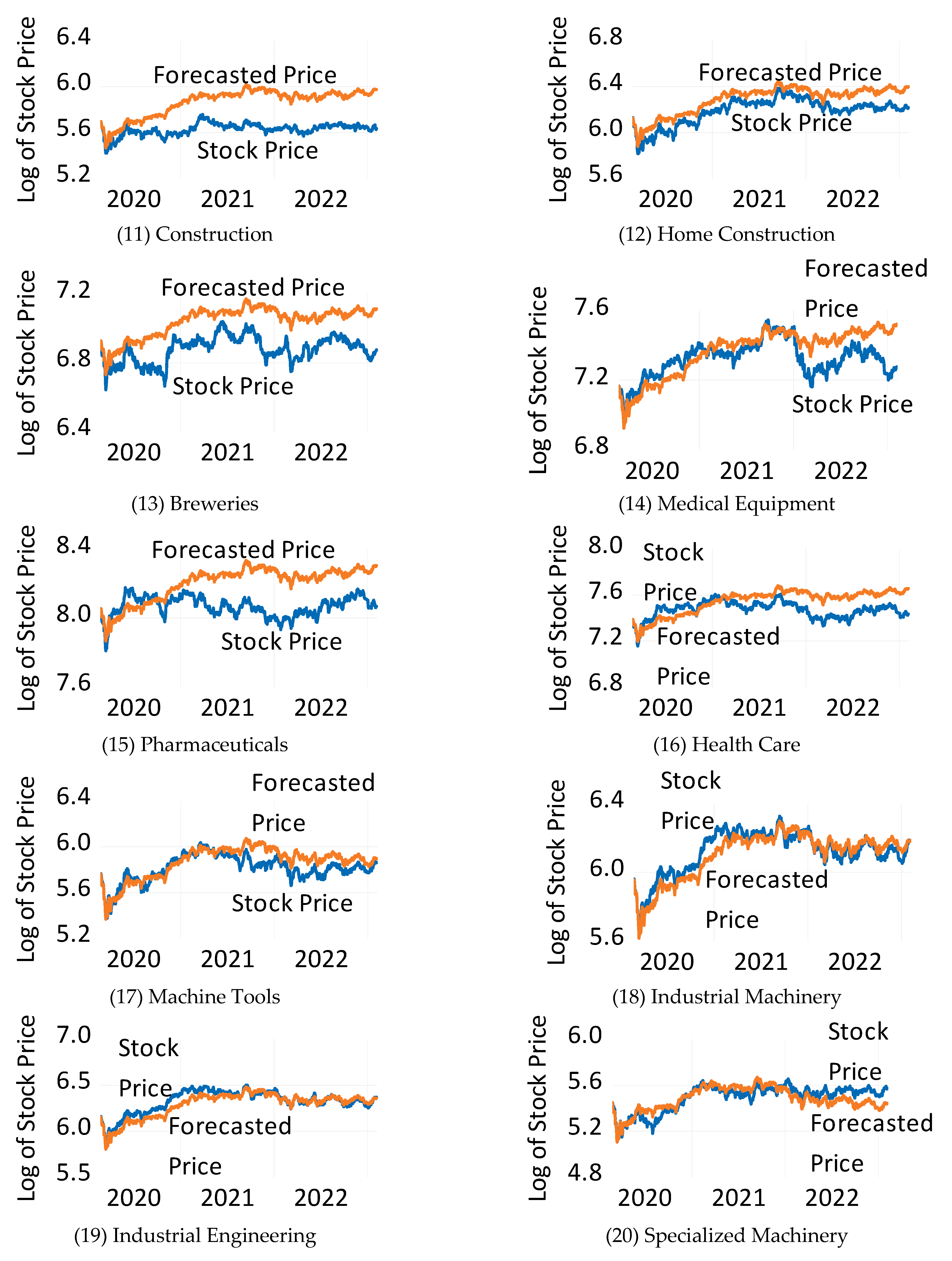

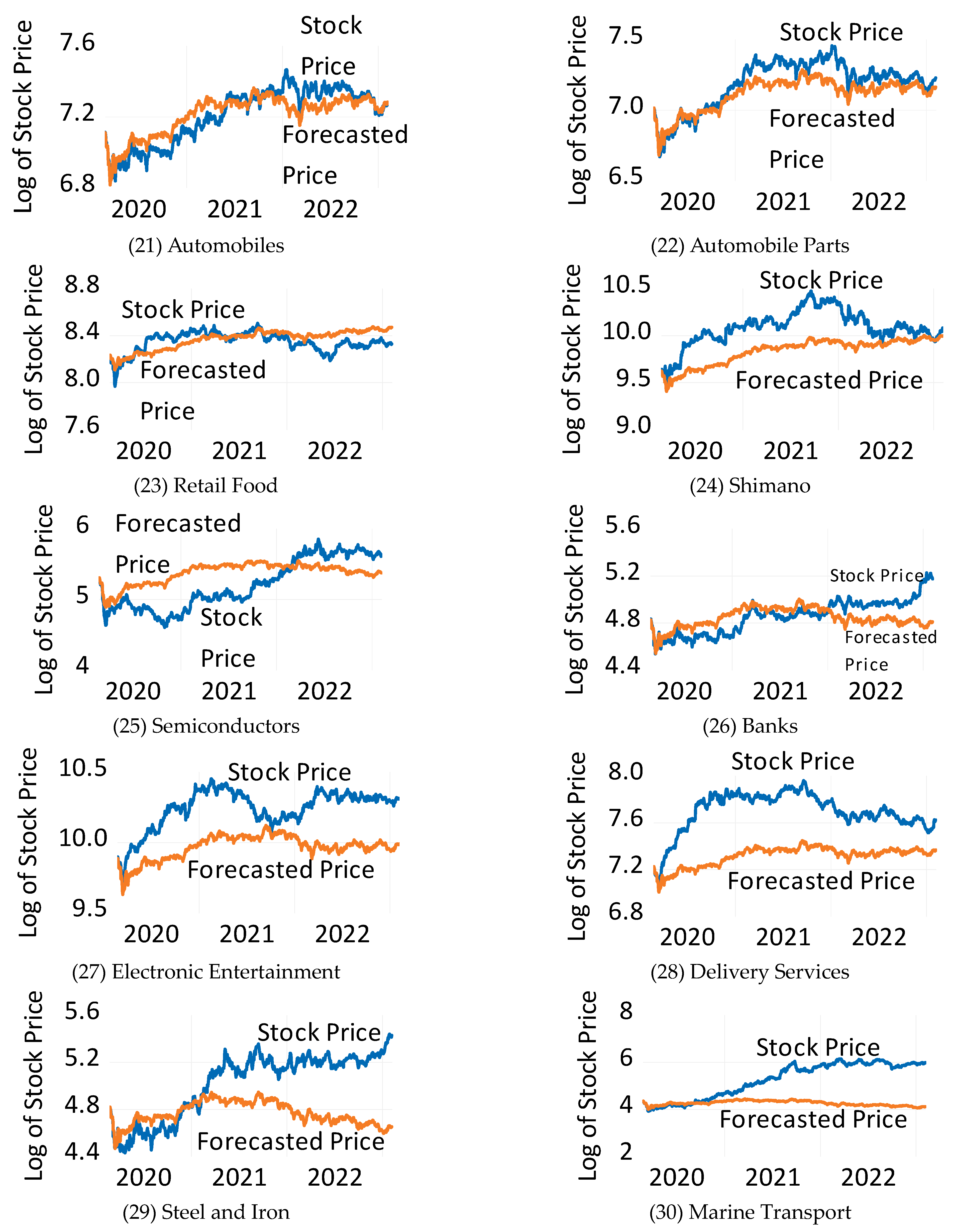

3.1. Data and Methodology

3.2. Results

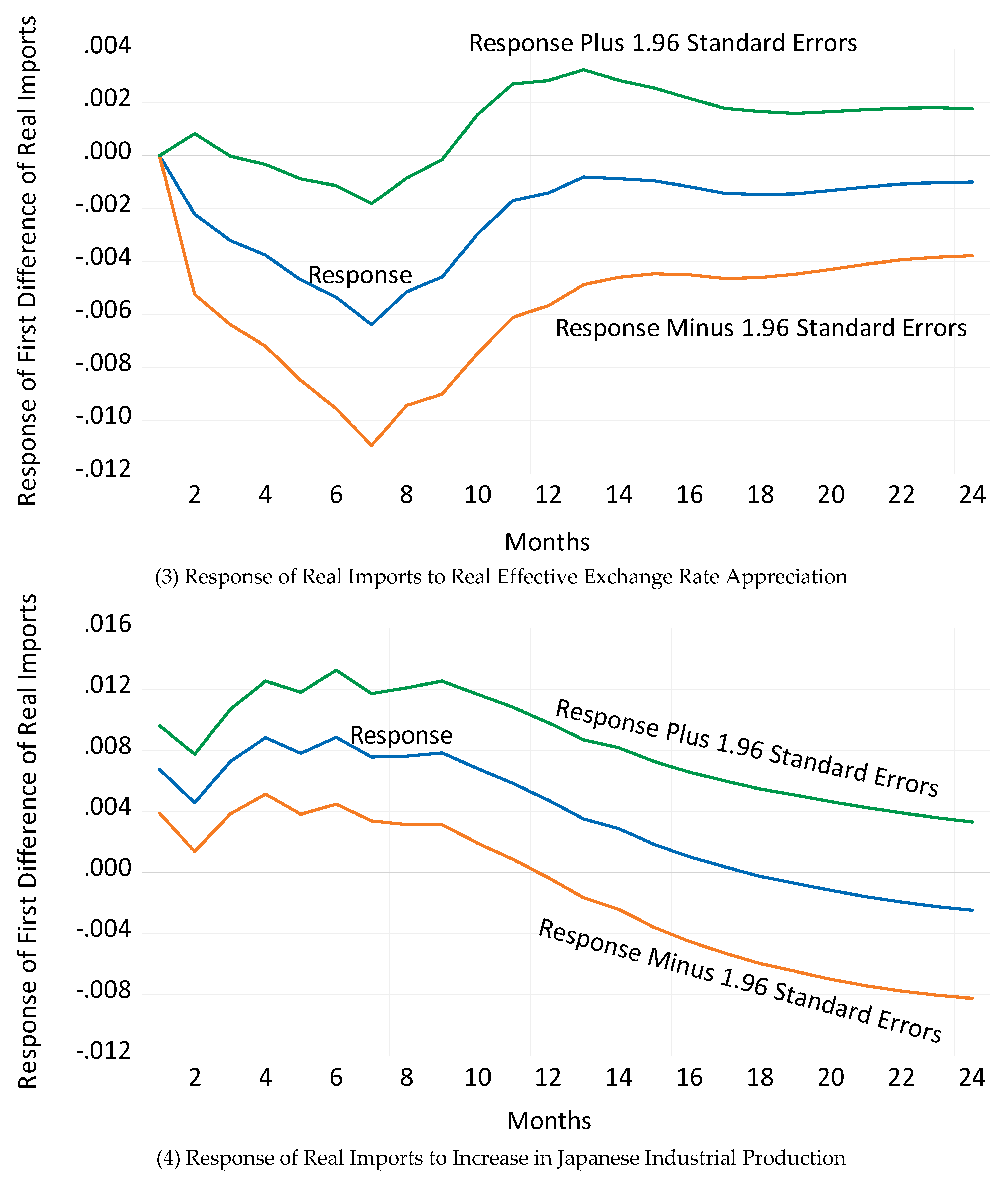

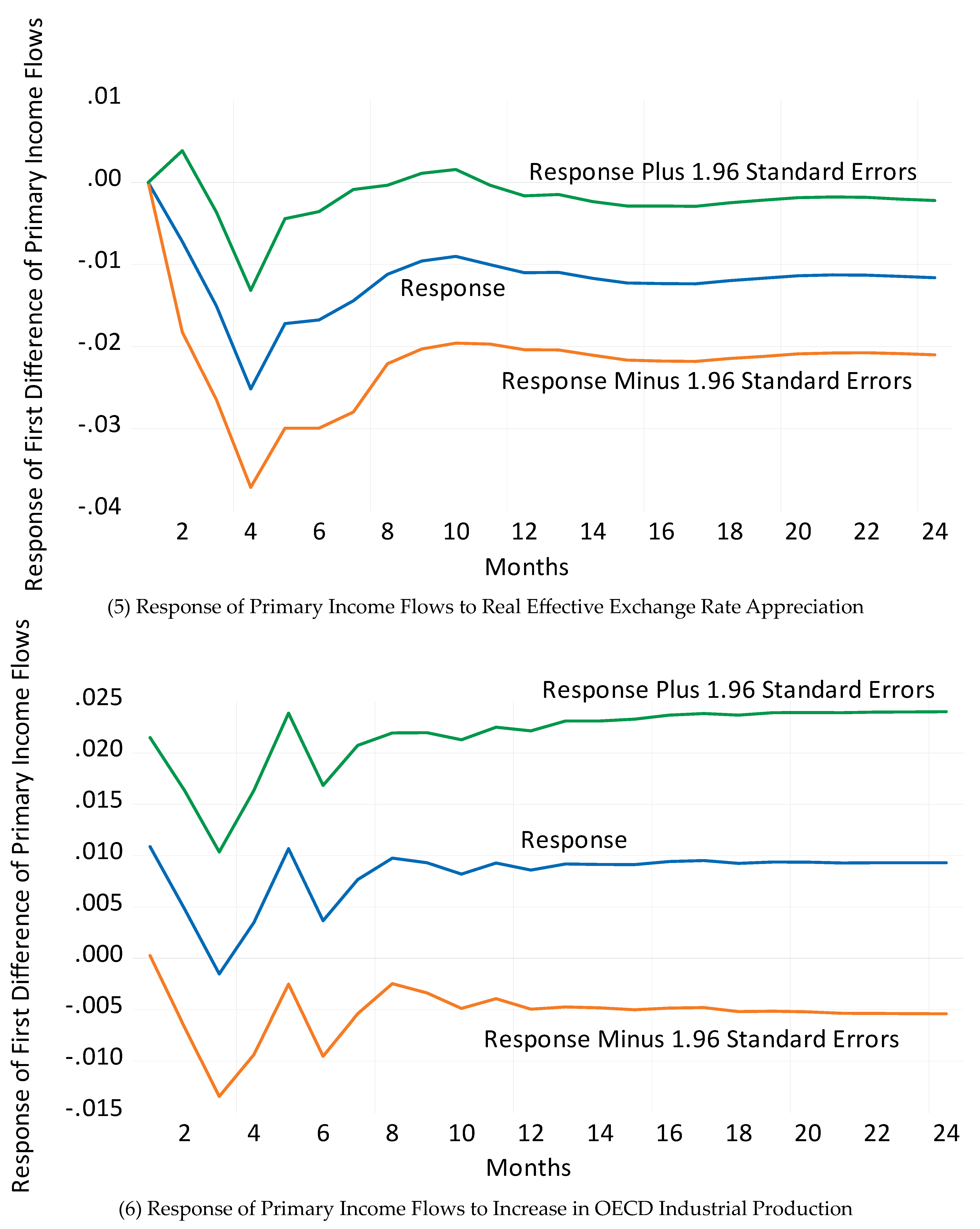

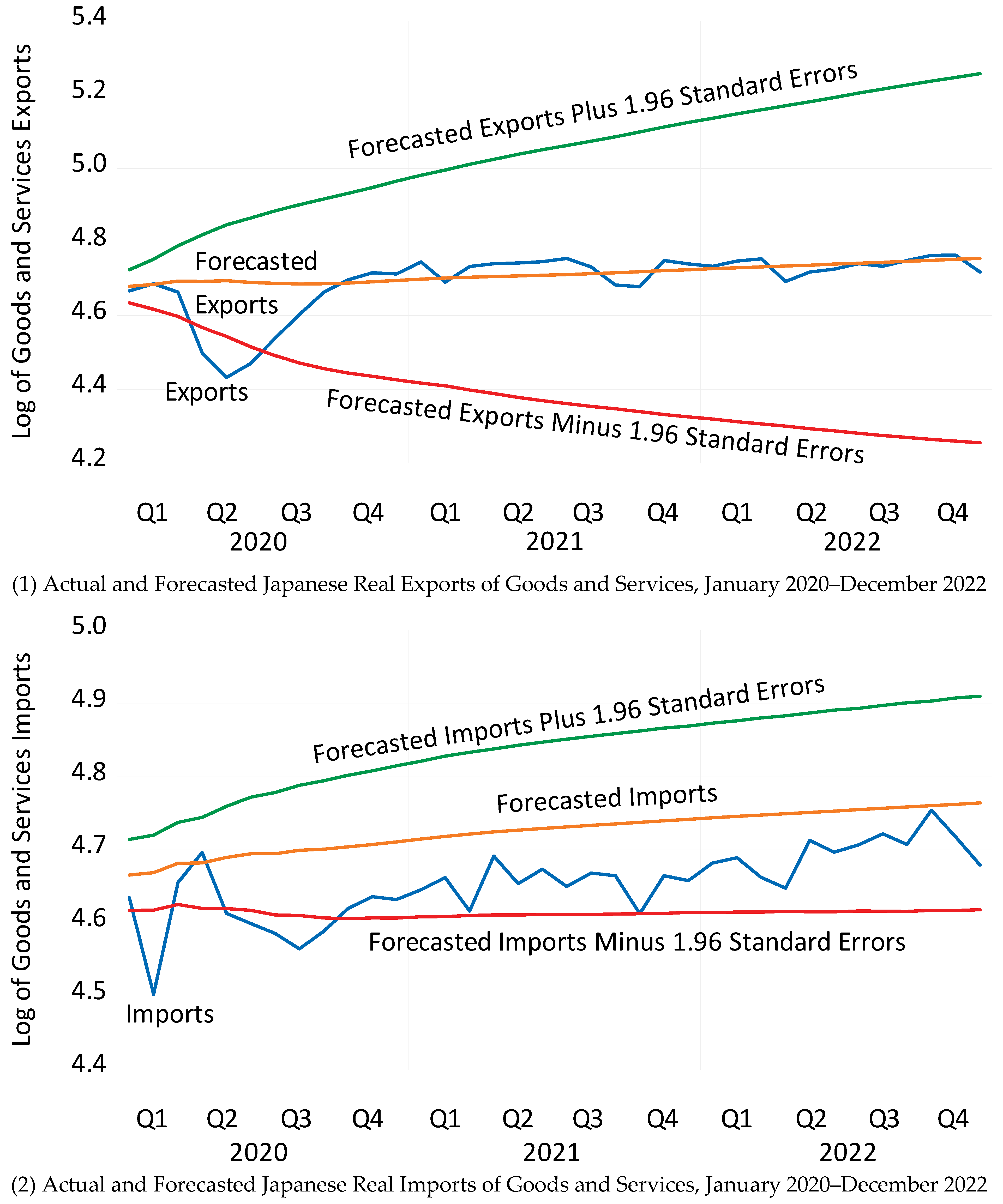

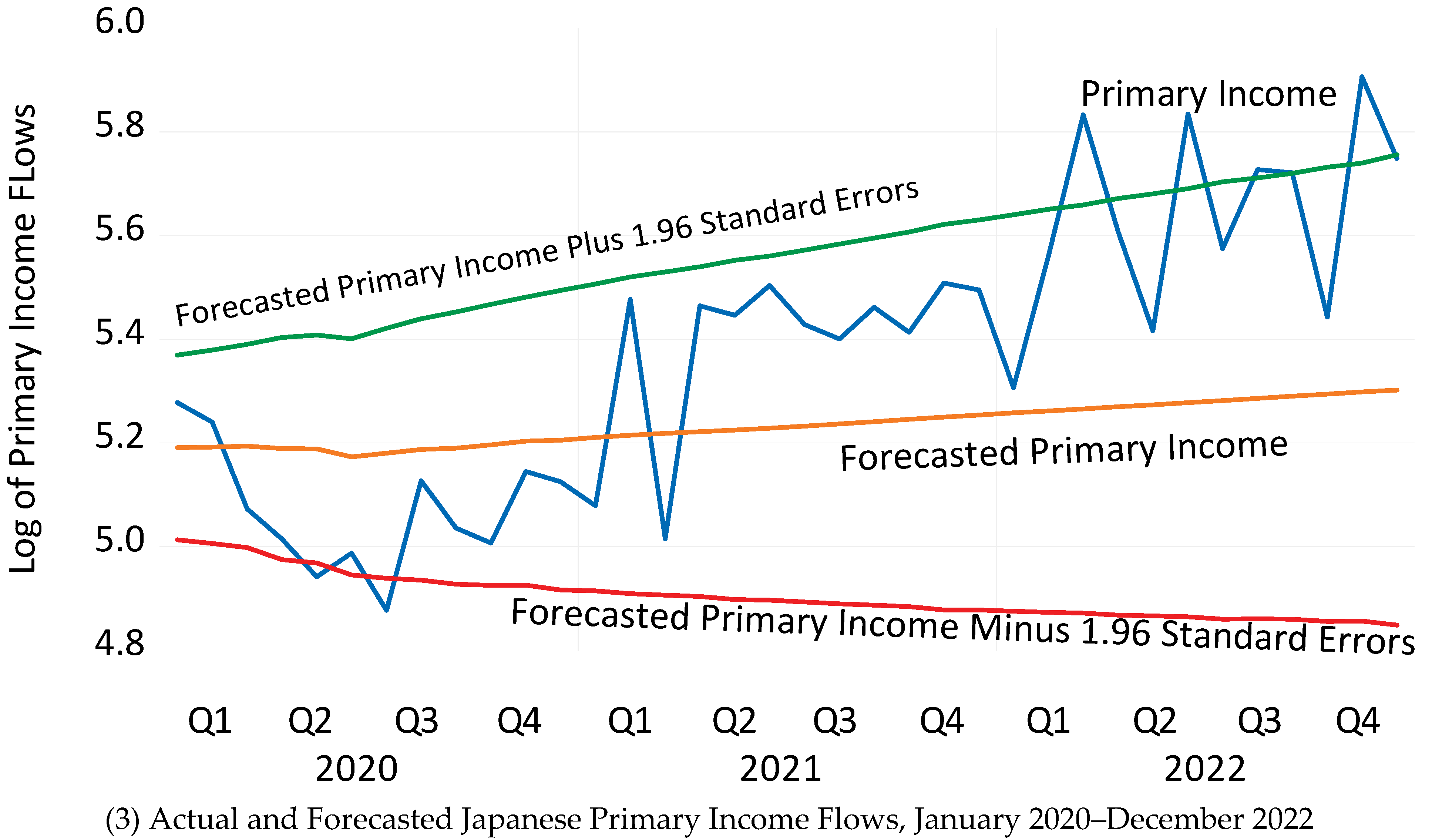

4. Evidence from Exports, Imports, and Primary Income Flows

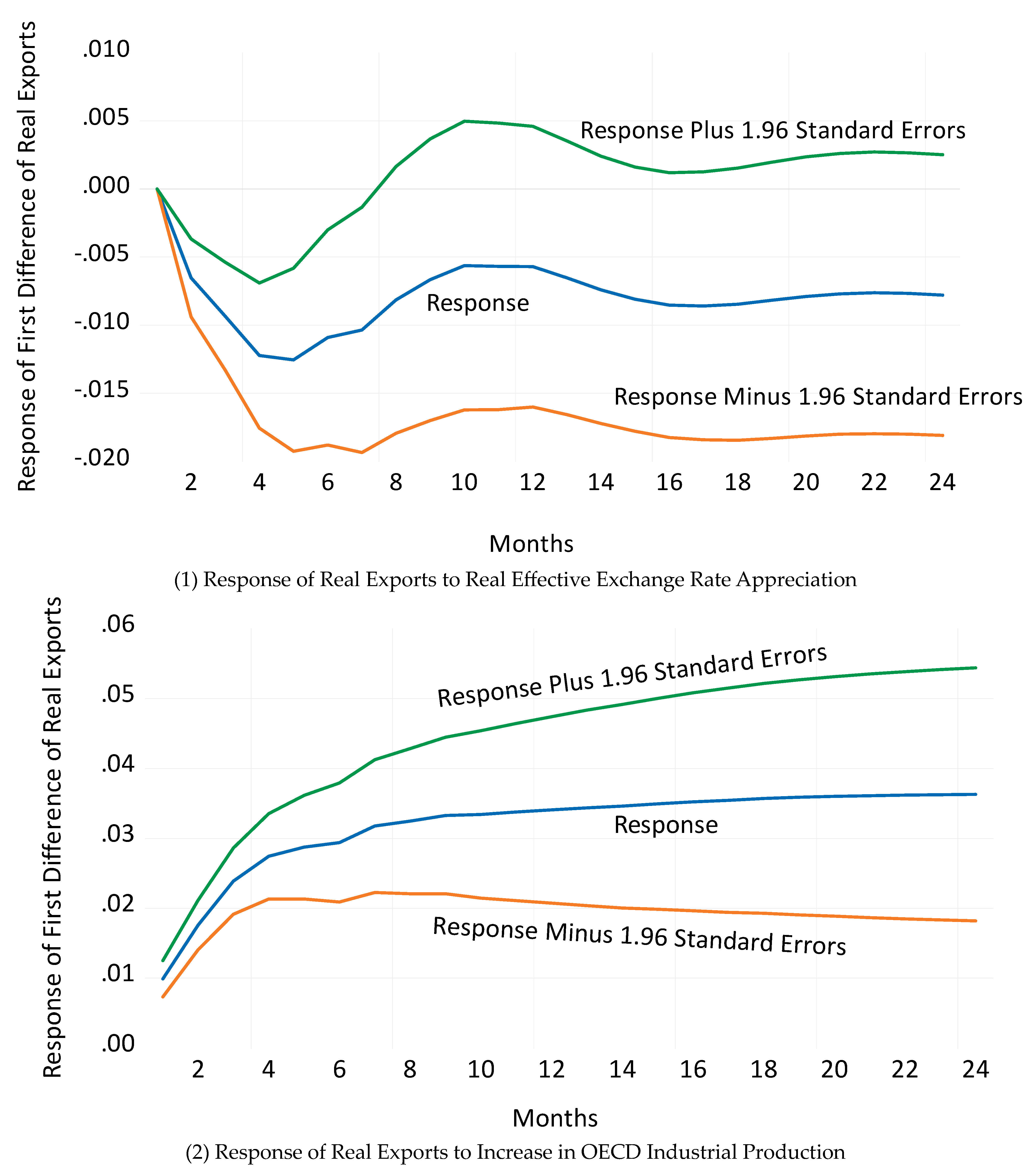

4.1. Data and Methodology

4.2. Results

5. Conclusions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | |

| 2 | One shortcoming with using market values of stock prices is that they do not necessarily reflect intrinsic value (see Appel and Grabinski 2011). |

| 3 | Papers estimating exchange rate exposures include Bodnar et al. (2002) and Dominguez and Tesar (2006). |

| 4 | The sample starts on 8 April 2010 because this is when daily closing values for the yen/dollar exchange rate could be obtained from Datastream. |

| 5 | I am indebted to Professor Kiyotaka Sato for suggesting that I include crude oil prices in the VAR. |

| 6 | The random variables in the VAR are assumed to follow a Gaussian distribution. As Tormählen et al. (2021) discussed, assuming that random variables are Gaussian is a simplifying assumption that may cloud inference. Future work should explore deriving other distributions. |

| 7 | As an example, Matsuura and Saito (2022) have discussed cost-effective ways that the government has sought to stimulate tourism. |

References

- Appel, Dominik, and Michael Grabinski. 2011. The origin of financial crisis: A wrong definition of value. Portuguese Journal of Quantitative Methods 2: 33–51. [Google Scholar]

- Aruga, Kentaka. 2021. Changes in human mobility under the COVID-19 Pandemic and the Tokyo fuel market. Journal of Risk and Financial Management 14: 163. [Google Scholar] [CrossRef]

- Aruga, Kentaka. 2022. Effects of the human-mobility change during the COVID-19 Pandemic on electricity demand. Journal of Risk and Financial Management 15: 422. [Google Scholar] [CrossRef]

- Bodnar, Gordon M., Bernard Dumas, and Richard C. Marston. 2002. Pass-through and exposure. Journal of Finance 57: 199–231. [Google Scholar] [CrossRef]

- Chan, Kam, and Terry Marsh. 2020. The Asset Markets and the Coronavirus Pandemic. VoxEU Weblog, April 3. Available online: https://www.voxeu.org (accessed on 5 May 2020).

- Chatelais, Nicolas, Arthur Stalla-Bourdillon, and Menzie Chinn. 2023. Forecasting real activity using cross- sectoral stock market information. Journal of International Money and Finance 131: 102800. [Google Scholar] [CrossRef]

- Croux, Christophe, and Peter Reusens. 2013. Do stock prices contain predictive power for the future economic activity? A Granger causality analysis in the frequency domain. Journal of Macroeconomics 35: 93–103. [Google Scholar] [CrossRef]

- Dominguez, Kathryn, and Linda Tesar. 2006. Exchange rate exposure. Journal of International Economics 68: 188–218. [Google Scholar] [CrossRef]

- Fama, Eugene, and Kenneth French. 1993. Common risk factors in the returns on stocks and bonds. Journal of Financial Economics 33: 3–56. [Google Scholar] [CrossRef]

- Gagnon, Joseph, Steven Kamin, and John Kearns. 2023. The impact of the COVID-19 pandemic on global GDP growth. Journal of the Japanese and International Economies. forthcoming. [Google Scholar] [CrossRef]

- Gormsen, Niels, and Ralph Koijen. 2020. Coronavirus: Impact on Stock Prices and Growth Expectations. Thesis, University of Chicago, Chicago, IL, USA. Available online: https://academic.oup.com/raps/article/10/4/574/5904278?login=false (accessed on 15 March 2023).

- Hayakawa, Kazunobu, and Hiroshi Mukunoki. 2021. The impact of COVID-19 on international trade: Evidence from the first shock. Journal of the Japanese and International Economies 60: 101135. [Google Scholar] [CrossRef]

- Hayakawa, Kazunobu, Souknilanh Souknilanh, and Shujiro Urata. 2022. How effective was the restaurant restraining order against COVID-19? A nighttime light study in Japan. Japan and the World Economy 63: 101136. [Google Scholar] [CrossRef] [PubMed]

- Honda, Tomohito, Kaoru Hosono, Daisuke Miyakawa, Arito Ono, and Iichiro Uesugi. 2023. Determinants and effects of the use of COVID-19 business support programs in Japan. Journal of The Japanese and International Economies 67: 101239. [Google Scholar] [CrossRef]

- Imahashi, Rurika. 2021. Japan startups cash in on e-learning demand spurred by COVID. Nikkei Asia, January 6. [Google Scholar]

- IMF. 2023. Japan: Staff Concluding Statement of the 2023 Article IV Mission. January 26. Available online: https://www.imf.org/en/News/Articles/2023/01/25/japan-staff-concluding-statement-of-the-2023-article-iv-mission (accessed on 15 March 2023).

- Kikuchi, Junichi, Ryoya Nagao, and Yoshiyuki Nakazano. 2023. Expenditure responses to the COVID-19 pandemic. Japan and the World Economy 65: 101174. [Google Scholar] [CrossRef] [PubMed]

- Koren, Miklós, and Rita Pető. 2020. Business disruptions from social distancing. In Covid Economics: Vetted and Real-Time Papers 2. London: CEPR Press. Available online: https://cepr.org/content/covid-economics-vetted-and-real-time-papers-0#block-block-10 (accessed on 1 June 2020).

- Kubota, So, Koichiro Onishi, and Yuta Toyama. 2021. Consumption responses to COVID-19 payments: Evidence from a natural experiment and bank account data. Journal of Economic Behavior & Organization 188: 1–17. [Google Scholar]

- Lintner, John. 1965. The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. Review of Economics and Statistics 47: 13–37. [Google Scholar] [CrossRef]

- Masuda, Yuki. 2022. Shiseido slashes profit forecast on weak beauty sales in Japan, China. Nikkei Asia, August 11. [Google Scholar]

- Matsuura, Toshiyuki, and Hisamitsu Saito. 2022. The COVID-19 pandemic and domestic travel subsidies. Annals of Tourism Research 92: 103326. [Google Scholar] [CrossRef]

- McMillan, David. 2021. Predicting GDP growth with stock and bond markets: Do they contain different information? International Journal of Finance and Economics 26: 3651–75. [Google Scholar] [CrossRef]

- Nagumo, Jada. 2021. Tokyo Game Show turns to virtual reality in face of COVID. Nikkei Asia, September 29. [Google Scholar]

- Pagano, Marco, Christian Wagner, and Josef Zechner. 2020. Disaster resilience and asset prices. In Covid Economics: Vetted and Real-Time Papers 2. Paris: CEPR Press. Available online: https://arxiv.org/abs/2005.08929 (accessed on 1 June 2020).

- Ramelli, Stefano, and Alexander Wagner. 2020. Feverish stock price reactions to COVID-19. Review of Corporate Finance Studies 9: 622–55. [Google Scholar] [CrossRef]

- Rose, Andrew. 1991. The role of exchange rates in a popular model of international trade: Does the ‘Marshall-Lerner’ condition hold? Journal of International Economics 30: 301–16. [Google Scholar] [CrossRef]

- Sakurai, Yusuke, and Takemi Nakagawa. 2023. 70% of Japan’s local railways say pre-COVID ridership won’t return. Nikkei Asia, May 5. [Google Scholar]

- Sato, Kiyotaka, Junko Shimizu, Nagendra Shrestha, and Shajuan Zhang. 2013. Industry-specific real effective exchange rates and export price competitiveness: The cases of Japan, China, and Korea. Asia Economic Policy Review 8: 298–321. [Google Scholar] [CrossRef]

- Shirai, Sayuri. 2020. Japan’s triple economic shock. East Asia Forum Quarterly 12: 25–26. [Google Scholar]

- Shoji, Masahiro, Susumu Cato, Takashi Iida, Kenji Ishida, Asei Ito, and Kenneth McElwain. 2022. Variations in early-Stage responses to pandemics: Survey evidence from the COVID-19 pandemic in Japan. Economics of Disasters and Climate Change 6: 235–58. [Google Scholar] [CrossRef] [PubMed]

- Thorbecke, Willem. 2019. How oil prices affect East and Southeast Asian economies: Evidence from financial markets and implications for energy security. Energy Policy 128: 628–38. [Google Scholar] [CrossRef]

- Thorbecke, Willem. 2022. Investigating how exchange rates affected the Japanese economy after the advent of Abenomics. Asia and the Global Economy 2: 100028. [Google Scholar] [CrossRef]

- Tormählen, Maike, Galiya Klinkova, and Michael Grabinski. 2021. Statistical significance revisited. Mathematics 9: 958. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Thorbecke, W. Japanese Economic Performance after the Pandemic: A Sectoral Analysis. J. Risk Financial Manag. 2023, 16, 267. https://doi.org/10.3390/jrfm16050267

Thorbecke W. Japanese Economic Performance after the Pandemic: A Sectoral Analysis. Journal of Risk and Financial Management. 2023; 16(5):267. https://doi.org/10.3390/jrfm16050267

Chicago/Turabian StyleThorbecke, Willem. 2023. "Japanese Economic Performance after the Pandemic: A Sectoral Analysis" Journal of Risk and Financial Management 16, no. 5: 267. https://doi.org/10.3390/jrfm16050267

APA StyleThorbecke, W. (2023). Japanese Economic Performance after the Pandemic: A Sectoral Analysis. Journal of Risk and Financial Management, 16(5), 267. https://doi.org/10.3390/jrfm16050267