4.1. Results

To investigate the comovements between precious metals and stock market returns, using the analytical framework presented in

Section 3, we analyzed the monthly financial returns of gold, palladium, platinum, silver, and US stocks for the period from February 2010 (Feb-10) to January 2023 (Jan-23). The precious metal returns were derived from the respective monthly prices (in USD) published by The London Bullion Market Association, while the US stock returns were downloaded from the OECD statistical database.

Table 1 includes summary statistics for all returns series, separately for the two phases considered in our analysis. Phase I (stable period) covers the months from February 2010 to December 2019, while Phase II (turbulent period) covers the months from January 2020 to January 2023. It can be observed that US stocks provided the highest positive average returns in both periods, despite the decline observed during the turbulent period. In contrast, increases were observed for gold, platinum, and silver in the turbulent period, suggesting a possible increase in demand for these precious metals once the period of economic uncertainty in the US market commenced.

US stocks also exhibited the highest standard deviation in both periods, as well as a large standard deviation increase during the turbulent period. With the exception of gold, which remained stable, increases were observed in the standard deviations of all other precious metal returns, although they were smaller in size.

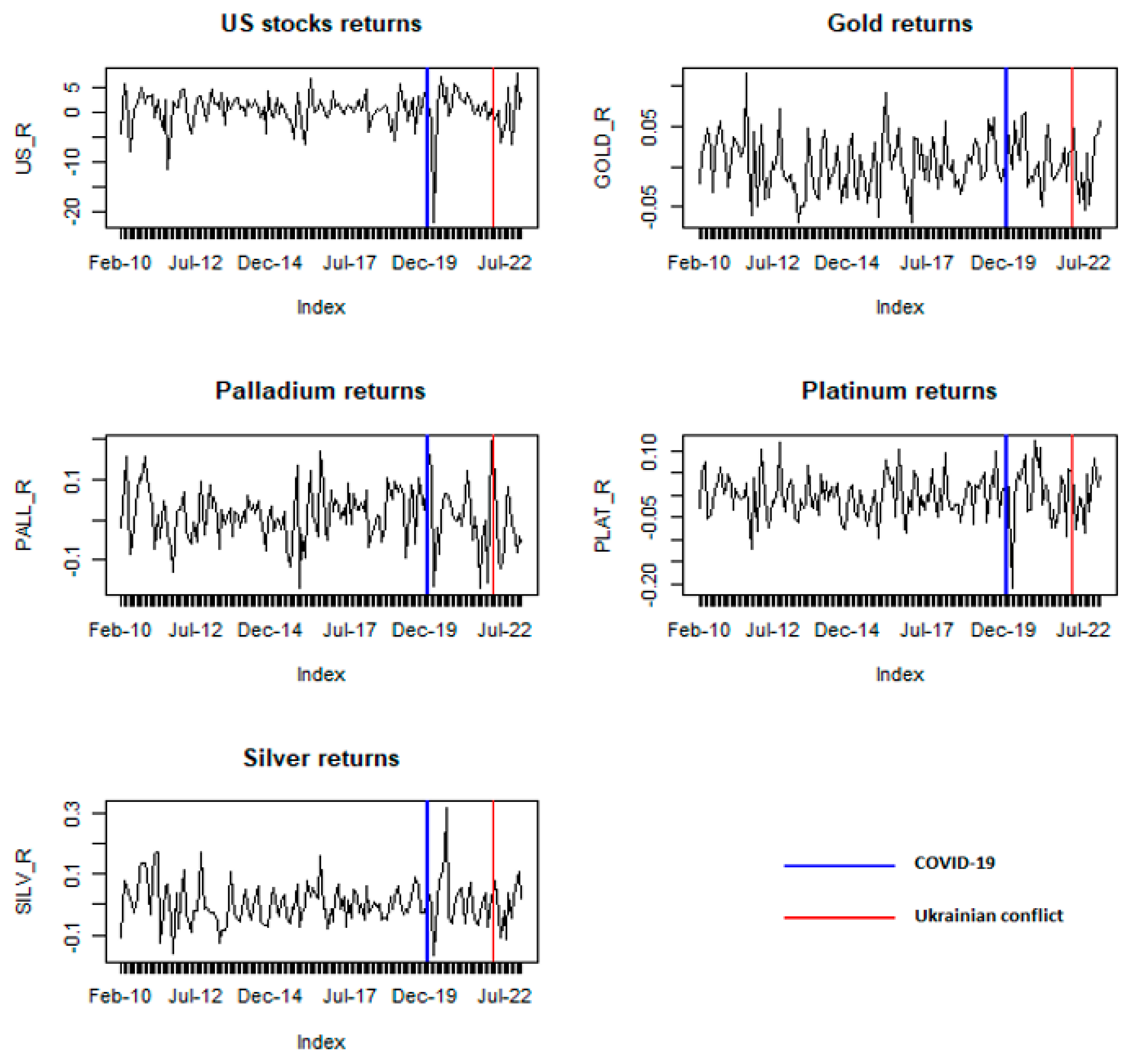

This is also evident in the respective plots for each series included in

Figure 1, where the vertical blue line marks the outbreak of the COVID-19 pandemic, dividing the sample into the two phases. It can be observed that immediately after the beginning of the COVID-19 pandemic, there was a large decline in US stock returns, followed by a recovery, then a short period of gradual decline and a subsequent increase in prices towards the end of the series.

This increase coincides with the beginning of the Ukrainian conflict on the 24 February 2022, marked with the thick red vertical line in

Figure 1. Collectively, these movements in US stocks increased the standard deviation of returns during the turbulent period. With the outbreak of the COVID-19 pandemic, declines were also observed for palladium, platinum, and silver; however, these series quickly returned to their pre-COVID-19 levels.

The large increase in the volatility of US stock returns should be expected to cause a bias in the correlation coefficient estimates between US stocks and the precious metal returns, leading to misleading inferences concerning their comovements.

Table 2 summarizes these correlation coefficient estimates for the different periods. First, we provide results using the conditional (on heteroscedasticity) correlation coefficient for the stable and turbulent subperiods separately, and then for the full sample that covers both phases. With the exception of palladium returns, it can be observed that in all cases, there is a noticeable increase in the size of the correlation coefficient in the turbulent period, which is also evident (albeit to a smaller extent) in the full period sample estimates.

The unconditional correlation coefficient estimates between the US stocks and precious metal returns are presented in the rightmost column in

Table 2. In all cases, the coefficient estimates are smaller, because the unconditional correlation coefficient corrects the heteroscedasticity bias associated with the conditional correlation coefficient. For palladium, platinum, and silver, these reductions are considerable with potential implications for the resource allocation decisions of the investors interested in these assets.

To investigate the synchronization of comovements between the different asset classes, we constructed separate correlation matrices using both the conditional and unconditional correlation coefficient estimates. These were subsequently used to derive correlation distance metrics that were used in an MSA, with the purpose of generating two-dimensional configurations that depict the similarities or dissimilarities between the financial returns. The correlation matrices are included in

Appendix A.

Table 3 includes the results of the model fit criteria presented in Equation (5) for the MSA applications examined. The scores in column 2 correspond to two-dimensional configurations and are analogous in the case for the other columns (e.g., column 3 is for three-dimensional configurations). All scores included in column 2 are higher than 0.8 which, as explained in

Section 3, indicates a good fit to the data. It is also worth mentioning that the configurations generated with the unconditional distance metric in Equation (4) provided the best fit to the data of all the two-dimensional configurations. Similarly,

Camacho et al. (

2006),

Aguiar-Conraria et al. (

2013) and

Michis (

2021) used two-dimensional configurations for the representations of economic time series.

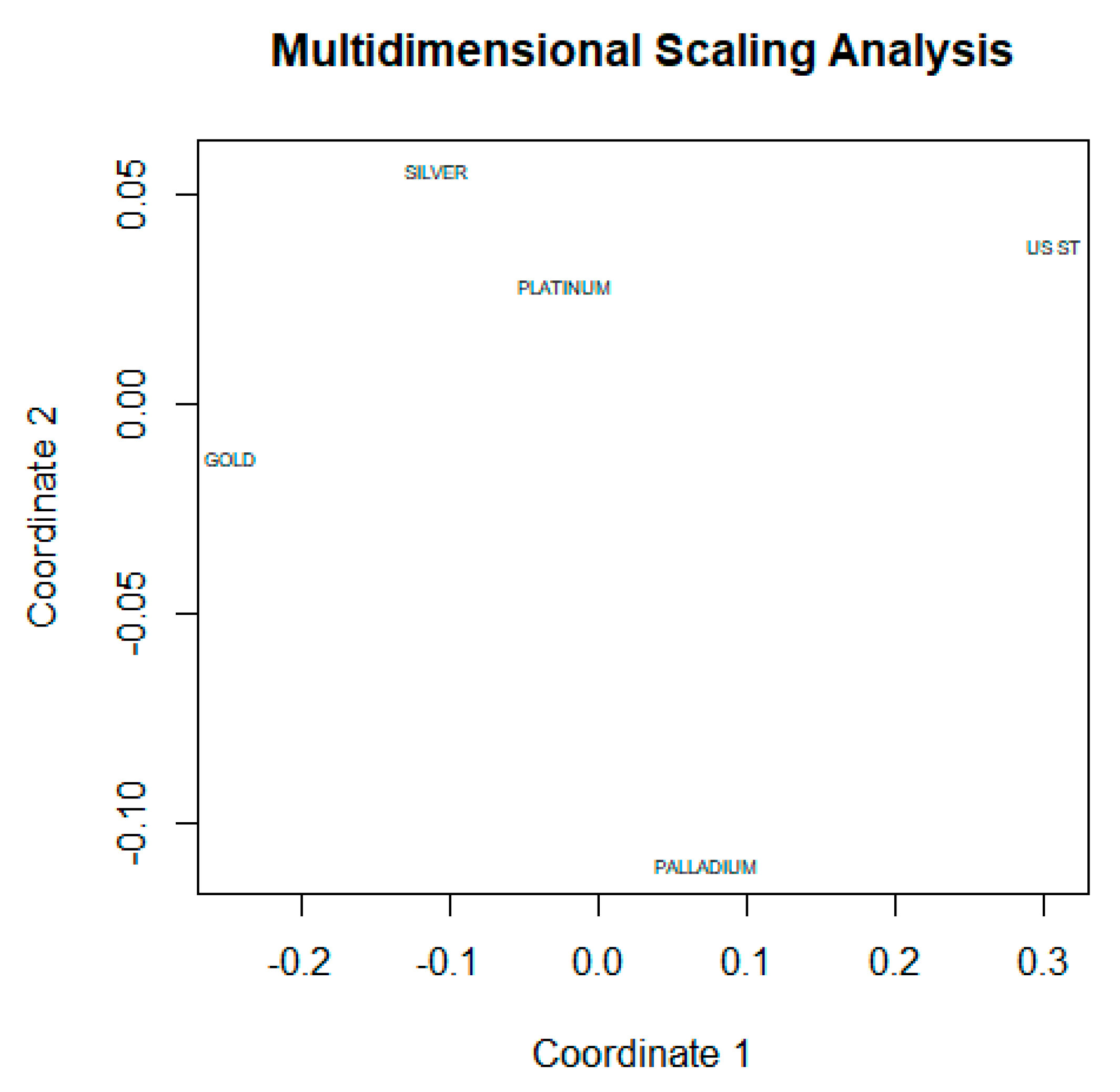

The two-dimensional configurations for the stable and turbulent periods, derived from the conditional correlation matrices in

Appendix A, are included in

Figure 2 and

Figure 3, respectively. The results in

Figure 2 suggest three distinct, and therefore, dissimilar, comovement asset returns: gold, palladium, and US stocks (US ST). Thus, during the stable period, gold and platinum could have potentially provided diversification benefits when included in portfolios that track the movements of the US stock market index. Silver and platinum are located closer to US stocks in the two-dimensional space, suggesting greater similarity with US stocks compared with the other precious metals.

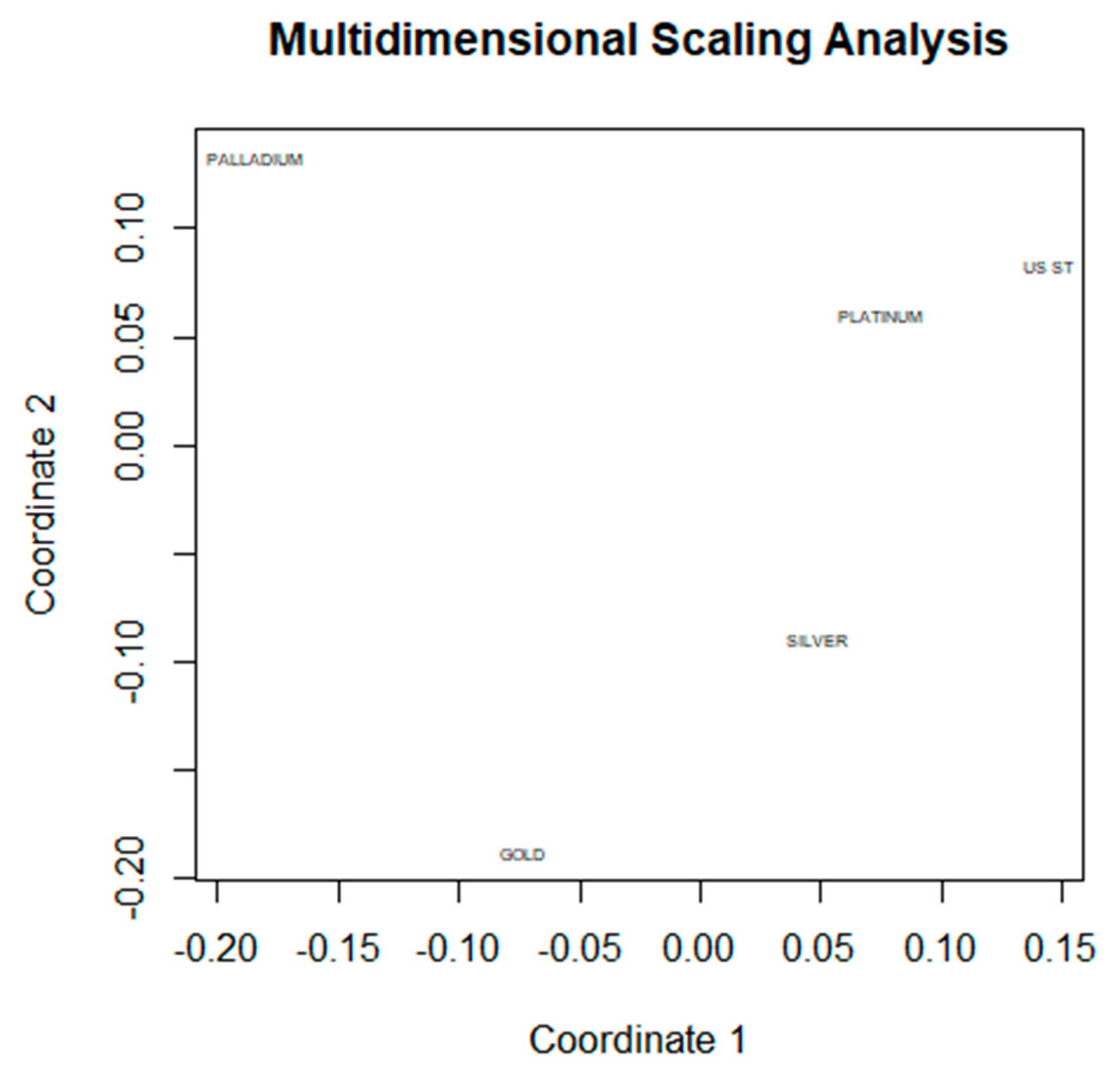

When considering the configurations in

Figure 3 for the turbulent phase, two basic conclusions emerge. First, gold, palladium, and US stocks continue to be located further apart (albeit with different distances compared with

Figure 2), suggesting that the financial return movements of gold and palladium continued to be dissimilar and less synchronized to US stocks, and are therefore useful for diversification purposes during the phase. Second, platinum is located closer to US stocks, while silver is still located halfway between US stocks and gold. These changes are also reflected in the respective conditional correlation matrices in

Appendix A.

Figure 4 provides a two-dimensional configuration based on the unconditional correlation matrix across the two periods (full sample), using the distance metric in Equation (4) in the context of MSA. It can be observed that when correcting the heteroscedasticity bias in the estimated correlations, the two-dimensional configuration becomes more similar to the configuration in

Figure 2 for the stable period.

Gold, palladium, and US stocks are located further apart, suggesting a dissimilarity in their financial returns. Therefore, these precious metals remain useful considerations for portfolios that track the US stock market index, because they can provide diversification benefits. Furthermore, compared with the configuration in

Figure 2, silver and platinum are located closer to gold in

Figure 4, which suggests financial return movements that are more synchronized with gold returns and less similar to US stock returns. This similarity is more pronounced in the case of silver.

4.2. Tests for Normality, Variance Stabilization and Sample Size Adjustment

In addition to the correlation estimates for the different periods,

Table 2 also includes the results of

t-tests for the null hypothesis of zero correlation (

Chen and Popovich 2002) between the financial returns. According to the results, only the correlation estimates between US stocks and gold returns were not found to be significantly different from zero (except for the conditional correlation estimate in the turbulent period). However, when working with non-normal data, the

t-test becomes problematic and Type I error rates tend to be inflated (

Bishara and Hittner 2012).

Figure 5 includes density histograms for all the variables considered in this study. It can be observed that for some of the return series asymmetries exist that suggest departures from normality, such as the skewness of gold returns and the asymmetric tails of US stock returns. The normality assumption for the return series was also evaluated using the well-known Shapiro–Wilk and Kolmogorov–Smirnov normality tests that are frequently used in applied work (

Romão et al. 2010). The

p-values derived from these tests are included in

Table 4. The normality assumption was accepted only for the gold and palladium time series when using the Shapiro–Wilk test (at either the 5% or 10% significance level), while it was rejected for all the time series when using the Kolmogorov–Smirnov test.

When normality does not hold alternative non-parametric methods of statistical inference need to be used (

Lee and Rodgers 1998). For the purposes of this study we used a bias-corrected accelerated bootstrap resampling procedure with 999 replications, (

Efron and Tibshirani 1994) to generate two-sided 95% confidence intervals for the correlation estimates in

Table 2. The computations were performed with the confintr package for R, available from the CRAN archive and the generated confidence intervals are included in

Table 5. The results indicate that for all reported periods, the correlation estimates in

Table 2 fall within the corresponding bootstrap confidence intervals of

Table 5.

Forbes and Rigobon (

2002) showed that the heteroscedasticity bias in the conditional correlation formula is due to parameter

, which is the relative increase in the variance of

, not the variance of the regression coefficient in the linear model (1). Since the conditional correlation coefficient is increasing in

, conditional correlation estimates will tend to increase in volatile periods, even if the underlying unconditional correlation coefficient remains the same.

To demonstrate this, we also applied a variance stabilization transform to the time series before proceeding with the correlation estimates, using the power transformation proposed by

Yeo and Johnson (

2000). This transformation can be seen as a generalization of the Box–Cox transformation (

Greene 2018), which is frequently used in variance stabilization applications (

Michis and Nason 2017). With strictly positive data, the two transforms become equal; however, the Yeo–Johnson transformation can also handle time series with negative observations. The transformation parameter in our application was estimated through the maximization of a log-likelihood criterion function (

Raymaekers and Rousseeuw 2021) and the Yeo–Johnson transformation was implemented using the VGAM and car packages for R, available from the CRAN archive.

The correlation coefficient estimates for the different periods are summarized in

Table 6. The differences in the conditional correlation estimates between the reported periods are similar to those included in

Table 2. With the exception of palladium returns, in all cases, there is a noticeable increase in the size of the conditional correlation coefficient in the turbulent period, which is also evident in the full period estimates.

Despite the application of the variance stabilization procedure, the conditional correlation coefficient is still biased upwards due to the structural change in the variance of US stock returns in the turbulent period (). In contrast, the unconditional correlation estimates are in all cases smaller, which underlines the importance of correcting the heteroskedasticity bias using Formula (2). This formula is specifically designed to adjust the conditional correlation estimate based on the value of parameter .

As an additional robustness check for our results, we also estimated the “Phase I” stable period correlation coefficients using a reduced sample size that covers only the period January 2017–December 2019. The available observations for the period February 2010–December 2016 were excluded due to the existence of some other minor economic downturns and stock market volatility events within this time interval. Specifically, the European debt crisis concerns in 2011, the downgrade of US credit rating in August 2011, the Flash Crash of 2010 and the 2015–2016 stock market sell-off.

Even though these events did not escalate into full-blown economic crises, they can complicate inference from our correlation coefficient estimates, since “Phase I” (stable period) is considered as a benchmark for evaluating the correlation changes in “Phase II” (the turbulent period). The correlation coefficient estimates for this alternative stable period are included in

Table 7. The full period estimates for both the conditional and unconditional correlation coefficients were also derived using a reduced sample size (January 2017–January 2023).

In this case too, the differences in the conditional correlation estimates between the reported periods are similar to those reported in

Table 2. There is a noticeable increase in the size of the conditional correlation coefficients in the turbulent period, which is also evident in the full period sample estimates. This heteroscedasticity bias is corrected when the unconditional correlation coefficient is used, as demonstrated in the last column of

Table 7. Furthermore, the unconditional correlation levels are similar to those reported in

Table 2. However, it is important to emphasize that with the exception of platinum returns, all other conditional correlation coefficient estimates for the alternative stable period are not statistically significant at the 5% or 10% level and, therefore, these results should be used with caution.

4.3. Discussion

The theoretical foundation of our proposed method derives from the financial contagion literature and the large increases in cross-correlations observed between financial market indices when a financial crisis (shock) hits one of the interdependent countries.

Forbes and Rigobon (

2002) note that in such cases, large movements in one major stock market (e.g., the US stock market crash in 1987) tend to be associated with similarly large movements in other interconnected markets.

However, since correlation estimates are conditional on market volatility, they are biased upwards, providing the wrong impression of a large increase in cross-market linkages and, therefore, financial contagion. In contrast, the authors showed that adjusting this bias deflates the correlation estimates, suggesting only interdependence between the markets, which is a condition that exists across all phases of the economy.

Our study provides similar evidence for the cross market linkages that exist between US stocks and precious metal returns. These linkages derive from the investment characteristics of precious metals, which as explained in

Section 2 are considered by investors as possessing hedging and safe haven properties in times of financial distress. For example,

Mishkin (

2016) notes the following factors as important determinants for the demand for gold: lower perceived riskiness relative to other assets, higher expected returns relative to other assets and higher liquidity relative to other assets.

The transmission mechanism in this case most commonly begins with a shock to the US stock market, which generates renewed interest for investments in precious metals (the “flight to quality” effect). When correlation estimates between US stocks and precious metal returns are performed during this period of increased market volatility, the results will be biased upwards, providing misleading inferences to investors seeking to adjust their investment portfolios. The large movements in US stocks are erroneously perceived as being associated with a significant increase in the linkages between US stocks and precious metal returns.

In contrast, the standard deviation changes in

Table 1 (e.g., for US stocks and gold returns) between the stable and turbulent periods, do not provide any evidence for this assertion (increasing for US stock returns but not for gold returns). As demonstrated in

Table 2, adjusting the heteroscedasticity bias using the unconditional correlation coefficient provides estimates that are closer to the levels estimated with the conditional correlation coefficient for the stable period. These estimates represent the interdependence that exists between US stock and precious metal returns in all phases of the financial system.

Most existing studies in the literature rely on dynamic conditional correlation GARCH models that suggest an increase in the correlation levels during times of financial distress. For example,

Creti et al. (

2013) found that the 2007–2008 financial crisis strengthened the links of commodities (including metals) with stock markets, and

Sadorsky (

2014) reported an increase in the correlation levels between emerging market stocks, copper, oil and wheat since 2008.

Furthermore, the empirical results of

Mensi et al. (

2017) provide strong evidence of volatility spillovers between stocks and precious metals since the global financial crisis of 2007–2008 and the European sovereign debt crisis of 2010–2012. Interestingly, the authors found precious metals to be the net recipients and the stocks the source of the spillovers. Similarly,

Junttila et al. (

2018) found the correlation levels between equity returns and gold to have increased since the 2008 financial crisis.

Our results provide a different perspective on the correlation levels observed between stock market and precious metal returns across different phases of the economy, concentrating on the turbulent period that began with the outbreak of the COVID-19 pandemic. While we agree with

Mensi et al. (

2017) that the transmission mechanism between stocks and precious metals is indicative of contagion effects, as suggested in the financial contagion literature, our results are more compatible with the analysis of

Forbes and Rigobon (

2002) who provided a critical evaluation of the financial contagion literature.

According to the authors, since correlation coefficient estimates are conditional on market volatility, they will tend to increase significantly following a shock, giving the impression of an increase in cross-market linkages and, therefore, the existence of strong financial contagion effects from one stock market to other markets. When this heteroscedasticity bias is corrected, as in the case of the unconditional correlation coefficient, a different level of market linkages can exist, which is more compatible with the pre-existing conditions and the underlying long-term interdependence between the markets, not contagion.

The results reported in

Section 4 for the stock market–precious metals linkages are more compatible with the second case. After correcting the heteroscedasticity bias introduced by the COVID-19 pandemic and the subsequent Ukrainian conflict, the correlation levels of gold, silver, platinum, and palladium returns with US stock returns were not found to have changed substantially during Phase II. They are more compatible with the stable period (Phase I) considered in our analysis, suggesting a continuation of the interdependence levels that existed prior to the pandemic.

Our methodology and results will be of interest to investors considering the synthesis of their portfolios or the adoption of hedging strategies during turbulent periods. For example, resisting the temptation to make large changes in the synthesis of their portfolios when the underlying cross-market correlations between asset returns have not changed significantly, or to construct effective hedge ratios by hedging a long position in US stocks using a short position in a carefully selected precious metal. In this respect, the results in

Section 4 suggest that gold and palladium can be useful considerations for hedging long positions in US stocks.

We also note two results from the aforementioned literature that are consistent with our analysis in

Section 4. First,

Mensi et al. (

2017) found stock markets to be the source and precious metals the net recipients of volatility slipovers during financial crises. This is consistent with our definition of US stock returns, as the benchmark source financial variable in all applications of the unconditional correlation formula in

Section 4.

Second, the results by

Uddin et al. (

2020) suggest a similarity in the behaviour of silver and platinum returns towards US stocks during market downturns and a rather different behaviour in the case of gold, whose relationship with US stocks was found to be weaker. These associations are compatible with our graphical analysis in

Section 4 where silver and platinum are depicted closer together and with US stocks in the two-dimensional configurations, while gold is always located further away.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}