1. Introduction

In their work about anomalies

Fama and French (

2008) said of asset growth, “there is an asset growth anomaly”, and of profitability they said, “higher profitability tends to be associated with abnormally high returns.” Evaluating measures such as these has dominated the attention of academics everywhere in recent years. Two important recent measures in asset pricing literature are the

Cooper et al. (

2008) measure of asset growth and the

Novy-Marx (

2013) measure of scaled gross profit. Asset growth’s negative relationship to future profits perhaps serves as a proxy for agency costs or investor overreaction to growth (

Cooper et al. 2008). Scaled gross profit may provide a view of profitability which is less tainted by accounting error than income (

Novy-Marx 2013). Regardless, each measure has attracted a great deal of testing and discussion which we explore below.

However, to date, very limited evidence has been provided on how the asset-growth and profitability anomalies are related to each other, especially via managerial discretion in investment and other policies. This paper aims to fill this gap by investigating how their correlation is priced by investors in the market. In our paper, we construct a new measure which separates agency costs from Novy-Marx’s profitability measure. More specifically, we use the change in capital expenditure, one component of asset growth, to proxy for agency problems rising from managerial decisions on investment. We exclude the change in capital expenditure from gross profit and then scale by total assets. This allows us to capture highly profitable firms, rewarding those who do not over-invest in assets or who may be confounded by market exuberance from asset growth (

Cooper et al. 2008).

Our paper has two main motivations. First, we believe that the correlation between the asset-growth and profitability factors can provide important implications on how to identify a “cleaner” measure of profitability, which can help predict future returns more efficiently. Recently, several studies in this field are looking for a “cleaner” measure of profitability to explain the above anomalies and thus provide more explanatory power on future returns. For example,

Novy-Marx (

2013) argues that scaled gross profit can achieve such an objective by reducing accounting errors compared to other profitability measures below it in an income statement. In other words, his findings are driven by mitigating the impact of managerial decisions on how to disclose accounting profit via financial statements. On the other hand, investment decisions are also under managerial discretion, which is one of the determinants of asset growth. Therefore, both anomalies/factors could share the issues of managerial discretion, to some degree, if not completely. Thus, a measure of profitability can be “cleaner” and more “efficient” if it is able to take into account the agency problems shared by the asset-growth and gross profitability factors.

Such agency costs are hard to capture when calculating asset-growth and profitability measures in empirical studies because agency issues due to managerial discretion could vary dramatically across companies. The managers may have greatly different traits, including their educations, career paths, personal characteristics, and social networks, that may lead them to make completely different decisions even facing the same circumstances (

Graham et al. 2013). Consequently, a profitability measure without controls for agency costs is likely to make asset pricing models less powerful in terms of predicting the future returns. Therefore, our new variable can benefit the asset pricing model in enabling the models to be free of the impact of managerial discretion due to managerial personal traits within each firm. We believe that our new variable can provide a “cleaner” measure of profitability, after controlling for the potential agency costs demonstrated by over-investment.

Second, our study also aims to provide new evidence on the true reason for the asset-growth effect identified by

Cooper et al. (

2008). Currently, two main competing theories have been proposed by researchers, in order to explain the asset-growth anomaly (

Huang and Sun 2014). The first is the mispricing explanation which suggests that investors underreact to the negative information provided by managerial decisions on overinvestment, leading to a negative return in the following periods. The second refers to the efficient pricing theory, arguing that the asset-growth effect is driven by managers’ market-timing on the cost of capital, in order to maximize firm value. The essential difference depends on whether there is any agency problem arising from managerial discretion in investment.

We believe that our new measure helps test such hypotheses because managerial discretion could affect a firm’s investment and disclosure of accounting information in a similar way, due to the manager’s personal characteristics. It is presumably assumed that such agency problems should be priced only once, although affecting different decisions simultaneously. In other words, if our new variable is able to control for the agency cost related to disclosure of accounting profitability, it should also control for that from investment. Doing so would allow us to lend some supportive evidence to the mispricing explanation of the asset-growth anomaly.

We investigate the performance of our new variable following the same methodologies as in prior literature, mainly in

Novy-Marx (

2013), in sets of both regression analysis of future returns and portfolio analysis. The results show that our new variable outperforms other profitability measures suggested by

Novy-Marx (

2013) and

Ball et al. (

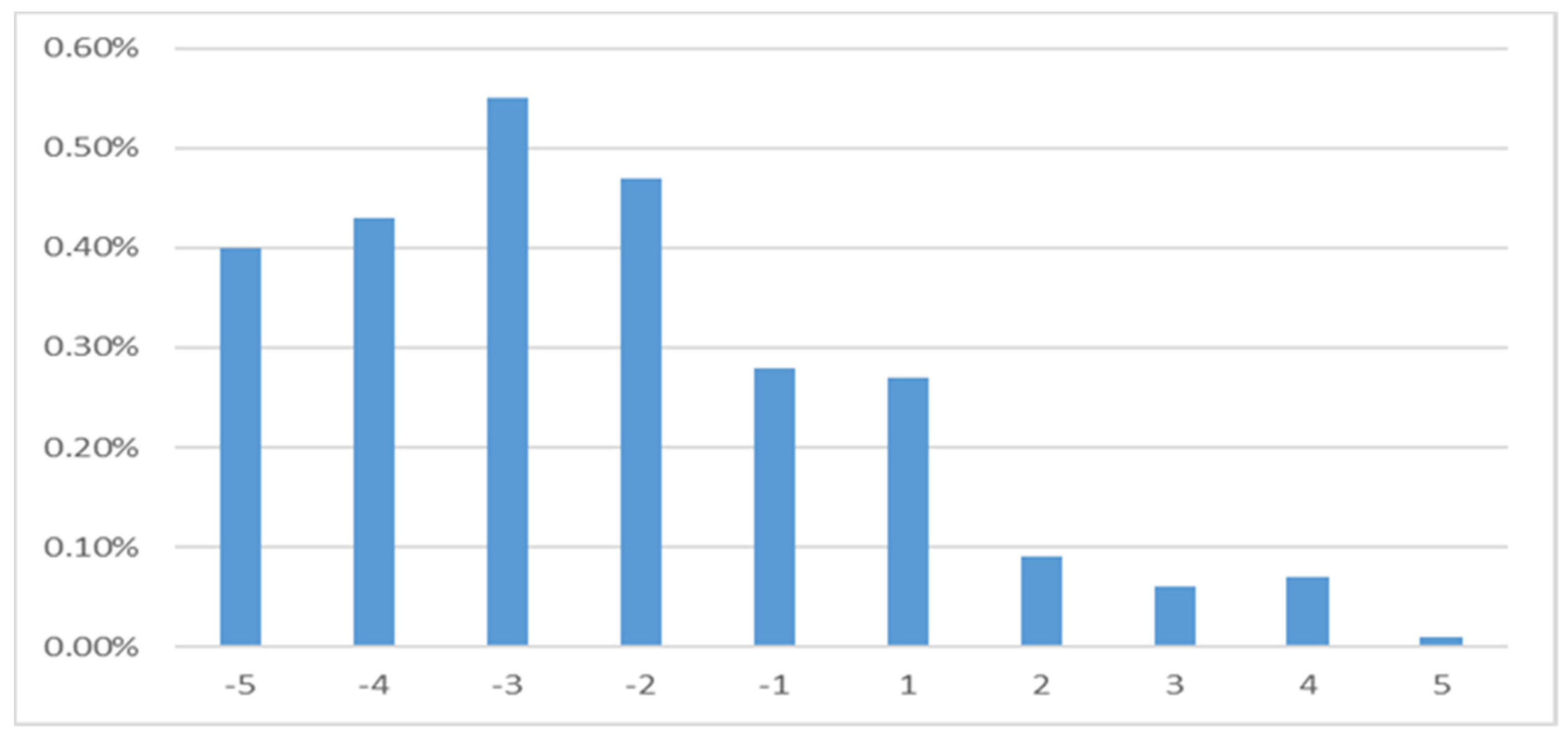

2016). First, our new variable has similar explanatory power of future returns to the others. Second, we find that the impact of asset growth on future returns becomes insignificant when our new variable is used, while remaining significant if other profitability measures are used. This suggests that our new measure captures agency problems raised from managerial discretion shared by investment activities and disclosure of accounting profits. We also test this measure over time periods of up to five years and find that its explanatory power persists.

Further, we test a relative version of our measure which compares profitability and investment on a scale relative to other firms. We find that our relative measure of profitability also provides extra explanatory power of future returns in addition to the scaled one and may provide the basis for other relative measures in the future.

Our study contributes to the literature in three aspects. First, our new measure provides a look at firm agency issues that has not been present in factor development. The prior literature has well documented that the identified factors such as asset growth could be driven by agency problems. However, it is difficult to control for the impact of managers’ personal characteristics on their decision-making processes, lowering our predicting power of future returns based on the current factor models. Our paper provides an important implication as to how this issue could be addressed by generating a profitability measure free of managerial discretion in firm decisions in investment. Second, our measure integrates the asset-growth and gross profitability factors into a single measure. Therefore, it can help make factor models more efficient by reducing the number of factors needed. Our findings also provide new evidence on the argument that the anomaly of asset growth shown by

Cooper et al. (

2008) is likely driven by managerial discretion in their decisions on investment. Third, our results show that not only scaled measures but also relative measures of profitability should receive more attention in order to predict the future returns more precisely. It is consistent with the fact that investors in the market find it difficult to collect information on managers’ personal characteristics and incorporate such information into their asset-pricing models. By removing capital expenditure, our measure is more positively correlated with those highly profitable companies which do not have exposure to significant agency issues. Alternatively, the relative measures of the factors related to agency problems are implemented to mitigate this issue, leading to the extra power provided by the relative version of our new measure.

The reminder of this paper is organized as follows.

Section 2 includes a literature review.

Section 3 introduces the data and methodology.

Section 4 describes the empirical results.

Section 5 concludes this paper.

2. Literature Review

Cooper et al. (

2008) use an asset-growth measure which is calculated as the change in total assets divided by beginning assets. Their work suggests that this measure provides an accurate prediction of future profitability, doing so because it “synergistically benefits from the predictability of all subcomponents of growth, allowing asset growth to better predict the cross-section of returns relative to any single component.” They demonstrate that their measure outperforms a decomposition of the balance sheet into its component parts which includes cash, operating assets, debt, and equity. It seems counterintuitive that this “blended” and simple measure could have much predictive power. Despite trying several different ways to explain this anomaly they finally offer a simple one. The most intuitive explanation is that investors overreact to the changes in business prospects implied by asset growth and thus create mispricing.

While the intuition behind the asset-growth measure is not particularly straightforward the results are very straightforward. The strong negative correlation between asset growth and profitability is remarkably consistent in testing. Returns on low asset-growth stocks exceed those of high asset-growth stocks by 71% on a value-weighted basis (

Cooper et al. 2008). These effects do not just persist for one year but for up to five years after portfolio formation. The authors suggest that this effect is simple mispricing mostly because they find no empirical evidence of risk-based explanations.

Others have tested the measure and found similar results. Using Australian stocks,

Gray and Johnson (

2011) find that the effect is not limited solely to U.S. stocks and, finding no suggestion of pricing of risk, further support the idea that the effect is due to mispricing.

Lam and Wei (

2011) evaluate the anomaly using two prominent explanations, one based on investment frictions and the other on limits to arbitrage. The investment frictions argument relies on the q-theory which argues that managers invest more when expected returns are lower and invest less when expected returns are higher. Thus, realized investment is negatively correlated with subsequent cross-sectional returns.

Lam and Wei (

2011) also explore limits to arbitrage as an explanation for the asset- growth anomaly. They argue that if investors truly misprice these investments then the relationship should be stronger in stocks which are difficult to arbitrage. The authors find limited support for each theory but overwhelming support for neither.

Despite reporting the relationship quoted in the opening paragraph of this paper,

Fama and French (

2008) provide mixed results for the explanatory power of profitability over stock returns. They find that kinds of profitability are not effective in predicting future returns and that they “do not provide much basis for the conclusion that, with controls for market cap and B/M, there is a positive relation between average returns and profitability.”

To improve upon this,

Novy-Marx (

2013) proposes a measure that “moves up” the income statement to provide a cleaner look at profitability. He posits that “moving up” provides less room for accrual, adjustment, earnings management, and other accounting manipulation which may taint earnings quality. With this measure he attempts to identify firms with higher average returns on assets, or more productive assets in general. He does so by using a measure based on gross profit. The “theory” behind this is as follows: “moving up” the income statement provides a truer measure of economic profitability. The gross profit measure captures discretionary cash flows at their source. Novy-Marx indicates that firms with large cash flows below gross margin are able to “invest” these in things which can be capitalized (R&D, capex) or expensed (advertising) which will “unambiguously translate into future profits.”

Novy-Marx defines the measure as gross profit scaled by total assets. The assertion made by is that scaling avoids “hopelessly conflating…. with book to market” (

Novy-Marx 2013). Further, the paper claims that using book assets provides a measure of productive assets that is not reduced by interest payments and is wholly independent of leverage.

The measure is found to be positively and significantly related to future returns. It works most effectively when combined in a portfolio strategy with book-to-market. The combined strategy provides nearly an 8% excess return trading only in the most liquid of listed stocks. However, in contrast to the asset growth work of

Cooper et al. (

2008),

Novy-Marx (

2013) re-sorts portfolios annually and does not present results of this measure beyond one year.

Ball et al. (

2016) suggest that it is the strength in the Novy-Marx measure lies in the deflating of gross profit by total assets. In fact, they suggest that, when deflated by total assets, net income and other measures are equal to gross profit as a predictor. While not tested by the authors and not tested here, it is possible that the richness in the asset-growth measure may suffer from the same impairment.

Much of what our measure attempts to tackle is agency issues. The idea that asymmetric information can be harmful dates back to

Akerlof (

1970) and the “lemons” model. Firms may attempt to lower their cost of capital by overcoming asymmetric information through disclosure (

Diamond and Verrecchia 1981). One such way is signaling. Signaling models in the literature attempt to explain many corporate behaviors such as capital structure decisions (

Ross 1977;

Myers and Majluf 1984;

John et al. (

1992);

MacKay 2003;

Kalay et al. (

2007)), return of capital in the form of dividend policy (

Bhattacharya 1979;

Miller and Rock 1985), and management as shareholders (

Leland and Pyle 1977). As stated by

Jensen (

1986), “managers have incentives to cause their firms to grow beyond the optimal size.” This increasing size increases “resources under their control” and “changes in compensation are positively related to the growth in sales.”

5. Conclusions

We test a factor that includes a scale measure of both asset growth and gross profitability. By its construction our variable is able to take into account agency problems related to the asset-growth and gross profitability factors, resulting from managerial discretion over the processes of investment decision and information disclosure of accounting profits. After excluding the change in capital expenditure from gross profit, our new measure provides a cleaner proxy of profitability in terms of predicting future returns. This added dimension to our variable provides superior performance to the scaled gross profit variable alone using the same dataset as

Novy-Marx (

2013), in two aspects. First, our new variable makes the asset growth redundant in the regression of future returns, maintaining the same explanatory power of future returns as other profitability measures suggested by the prior literature. Second, the outperformance of our new variable is also robust to the scaling issue raised by the prior literature (

Ball et al. 2016). As agency issues are key in both of these factors, this implies that combining them correctly can lead to a more efficient factor model.

On the other hand, our new measure failed to outperform among the 500 largest nonfinancial companies. This is consistent with the prior literature and with our main findings because these largest companies should have the least agency problems through managerial decisions on investments and accounting rules. Therefore, our new variable should be applied with caution, depending on the degree of information asymmetry between managers and shareholders.

In sum, our new measure provides a new view of both cash generation and disposition. This variable should provide a more effective portfolio application than scaled gross profit, depending on the information asymmetry issue with the firms. It should be implemented with caution in a sample of larger firms with stronger disclosure mechanisms. Also, our findings could be biased by other factors not covered in this paper. Therefore, the results here should not be interpreted as how to price the agency problem directly. Instead, our study aims to propose a new factor, after considering the agency problem. Future research with direct measurement of agency costs may help address the issue of pricing agency problems directly.

{kind=link}