Sovereign Debt Crisis and Fiscal Devolution

Abstract

:1. Introduction

2. Materials and Methods

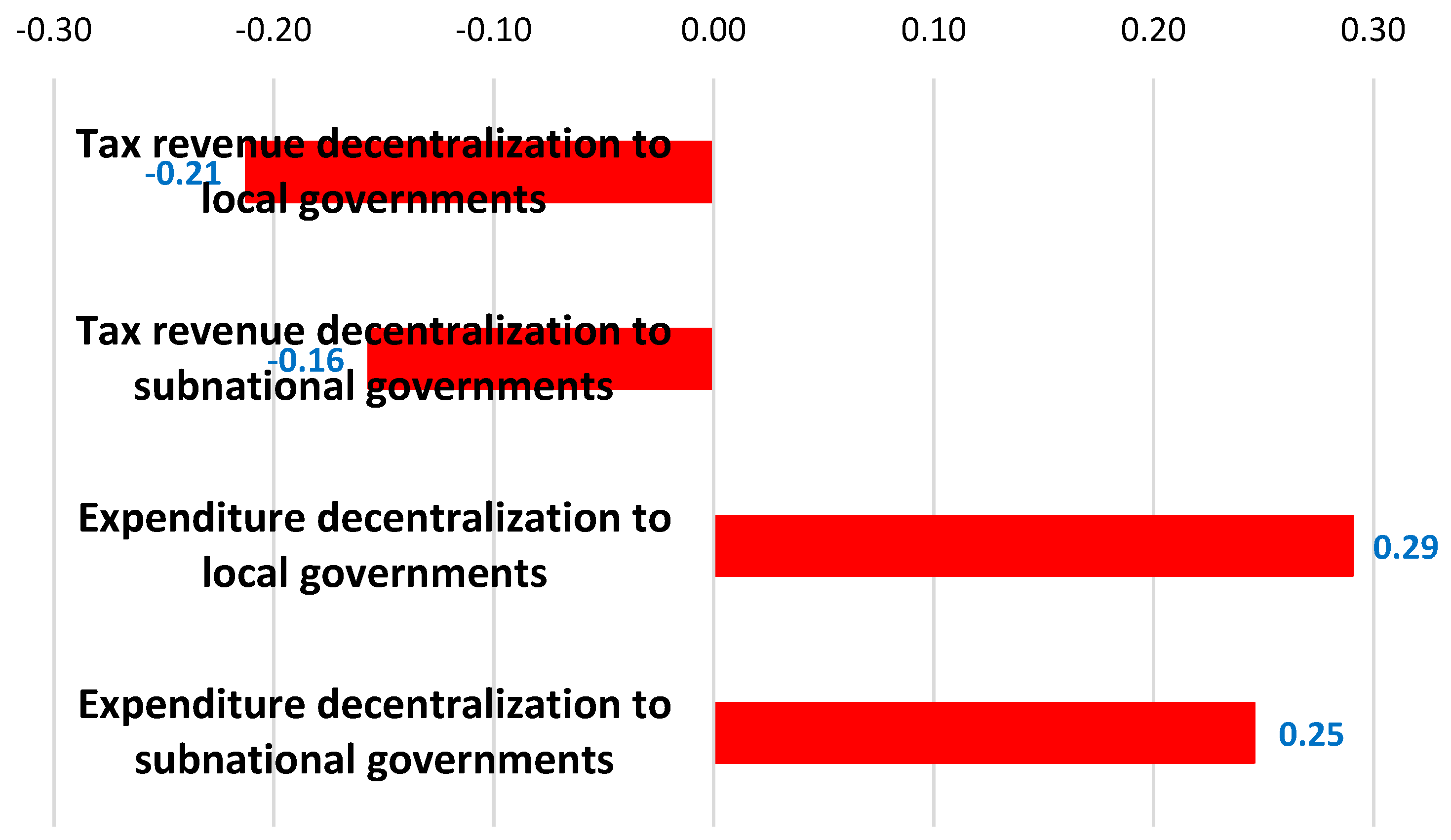

3. Results

4. Discussion

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Akin, Zafar, Zeynep B. Bulut-Cevik, and Bilin Neyapti. 2016. Does fiscal decentralization promote fiscal discipline? Emerging Markets Finance and Trade 52: 690–705. [Google Scholar] [CrossRef]

- Alfada, Anisah. 2019. Does fiscal decentralization encourage corruption in local governments? Evidence from Indonesia. Journal of Risk and Financial Management 12: 118. [Google Scholar] [CrossRef]

- Bahl, Roy, and Johannes Linn. 1994. Fiscal decentralization and intergovernmental transfers in less developed countries. Publius: The Journal of Federalism 24: 1–19. [Google Scholar] [CrossRef]

- Canavire-Bacarreza, Gustavo, Jorge Martinez-Vazquez, and Bauyrzhan Yedgenov. 2020. Identifying and disentangling the impact of fiscal decentralization on economic growth. World Development 127: 104742. [Google Scholar] [CrossRef]

- Chakrabarti, Avik, and Hussein Zeaiter. 2014. The determinants of sovereign default: A sensitivity analysis. International Review of Economics and Finance 33: 300–18. [Google Scholar] [CrossRef]

- Dawood, Mary, Nicholas Horsewood, and Frank Stobel. 2017. Predicting sovereign debt crises: An Early Warning System approach. Journal of Financial Stability 28: 16–28. [Google Scholar] [CrossRef]

- Digdowiseiso, Kumba. 2022. Is fiscal decentralization growth enhancing? A cross-country study in developing countries over the period 1990–2014. Economies 10: 62. [Google Scholar] [CrossRef]

- Eichler, Stefan, and Michael Hofmann. 2013. Sovereign default risk and decentralization: Evidence for emerging markets. European Journal of Political Economy 32: 113–34. [Google Scholar] [CrossRef]

- Foremny, Dirk, Agnese Sacchi, and Simone Salotti. 2017. Decentralization and the duration of fiscal consolidation: Shifting the burden across layers of government. Public Choice 171: 359–87. [Google Scholar] [CrossRef]

- Gärtner, Manfred, Björn Griesbach, and Florian Jung. 2011. PIGS or lambs? The European sovereign debt crisis and the role of rating agencies. International Advances in Economic Research 17: 288–99. [Google Scholar] [CrossRef]

- Honda, Jiro, Rene Tapsoba, and Ismael Issifou. 2022. When do we repair the roof? Insights from responses to fiscal crisis early warning signals. International Economics 172: 349–67. [Google Scholar] [CrossRef]

- Jia, Junxue, Yongzheng Liu, Jorge Martinez-Vasquez, and Kewei Zhang. 2021. Vertical fiscal imbalance and local fiscal indiscipline: Empirical evidence from China. European Journal of Political Economy 68: 101992. [Google Scholar] [CrossRef]

- Kornai, Janos. 1986. The soft budget constraint. Kyklos 39: 3–30. [Google Scholar] [CrossRef]

- Laeven, Luc, and Fabian Valencia. 2020. Systemic banking crises database II. IMF Economic Review 68: 307–61. [Google Scholar] [CrossRef]

- László, Török. 2022. Breakdown of government debt into components in Euro Area countries. Journal of Risk and Financial Management 15: 64. [Google Scholar] [CrossRef]

- Martinez-Vazquez, Jorge, Santiago Lago-Peñas, and Agnese Sacchi. 2017. The impact of fiscal decentralization: A survey. Journal of Economic Surveys 31: 1095–129. [Google Scholar] [CrossRef]

- Medas, Paulo, Tigran Poghosyan, Yizhi Xu, Juan Farah-Yacoub, and Kerstin Gerling. 2018. Fiscal crises. Journal of International Money and Finance 88: 191–207. [Google Scholar] [CrossRef]

- Moreno Badia, Marialuz, Paulo Medas, Pranav Gupta, and Yuan Xiang. 2022. Debt is not free. Journal of International Money and Finance 127: 102654. [Google Scholar] [CrossRef]

- Mpapalika, Jane, and Christopher Malikane. 2019. The determinants of sovereign risk premium in African countries. Journal of Risk and Financial Management 12: 29. [Google Scholar] [CrossRef]

- Nakatani, Ryota. 2023a. Fiscal crises, decentralization, and indiscipline. Scottish Journal of Political Economy 70: 459–78. [Google Scholar] [CrossRef]

- Nakatani, Ryota. 2023b. Revenue decentralization and the probability of a fiscal crisis: Is there a tipping point for adverse effects? Public Finance Review, in press. [Google Scholar] [CrossRef]

- Nakatani, Ryota. 2023c. Debt maturity and firm productivity—The role of intangibles. Research in Economics 77: 116–21. [Google Scholar] [CrossRef]

- Nakatani, Ryota, Qianqian Zhang, and Isaura Garcia Valdes. 2022. Fiscal Decentralization Improves Social Outcomes When Countries Have Good Governance. IMF Working Paper 22/111. Washington, DC: IMF. [Google Scholar] [CrossRef]

- Nakatani, Ryota, Qianqian Zhang, and Isaura Garcia Valdes. 2024. Health expenditure decentralization and health outcomes: The importance of governance. Publius: The Journal of Federalism 54: 59–87. [Google Scholar] [CrossRef]

- Neyapti, Bilin. 2013. Fiscal decentralization, fiscal rules and fiscal discipline. Economics Letters 121: 528–32. [Google Scholar] [CrossRef]

- Nguyen, Thanh Cong, Vítor Castro, and Justine Wood. 2022. A new comprehensive database of financial crises: Identification, frequency, and duration. Economic Modelling 108: 105770. [Google Scholar] [CrossRef]

- Rodden, Johathan. 2002. The dilemma of fiscal federalism: Grants and fiscal performance around the world. American Journal of Political Science 46: 670–87. [Google Scholar] [CrossRef]

- Rodríguez-Pose, Andrés, and Adala Bwire. 2004. The economic (in)efficiency of devolution. Environment and Planning A: Economy and Space 36: 1907–28. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Mean | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|

| Sovereign debt crisis | 0.0449 | 0.2073 | 0 | 1 |

| Tax revenue decentralization to local governments | 0.1116 | 0.1058 | 0 | 0.4613 |

| Tax revenue decentralization to subnational governments | 0.1783 | 0.1731 | 0 | 0.5828 |

| Expenditure decentralization to local governments | 0.1892 | 0.1054 | 0.0011 | 0.4920 |

| Expenditure decentralization to subnational governments | 0.2771 | 0.1654 | 0.0018 | 0.6891 |

| Polity | 4.8468 | 14.6993 | −88 | 10 |

| Land area | 1216.554 | 2883.265 | 2.03 | 16,381.39 |

| GDP growth | 3.2265 | 3.3075 | −15.1 | 20.585 |

| Current account balance | −1.2925 | 7.5848 | −43.825 | 63.39 |

| Exchange rates | 0.0262 | 0.0575 | −0.2181 | 0.5159 |

| Government debt | 51.2610 | 33.4599 | 3.221 | 233.528 |

| Interest cost | 1.8063 | 1.3927 | 0.0050 | 8.369 |

| Income per capita | 2.9699 | 0.7956 | 0.4770 | 4.2535 |

| Inflation | 4.3650 | 5.3665 | −6.811 | 59.218 |

| Banking crisis | 0.0859 | 0.2804 | 0 | 1 |

| Currency crisis | 0.0291 | 0.1681 | 0 | 1 |

| Variable | SC | TL | TS | EL | ES | Pol | LA | GG |

|---|---|---|---|---|---|---|---|---|

| Sovereign debt crisis (SC) | 1 | |||||||

| Tax revenue decentralization to local governments (TL) | 0.011 | 1 | ||||||

| Tax revenue decentralization to subnational governments (TS) | −0.071 | 0.654 | 1 | |||||

| Expenditure decentralization to local governments (EL) | 0.005 | 0.712 | 0.374 | 1 | ||||

| Expenditure decentralization to subnational governments (ES) | −0.093 | 0.416 | 0.734 | 0.531 | 1 | |||

| Polity (Pol) | −0.052 | 0.053 | 0.141 | 0.182 | 0.282 | 1 | ||

| Land area (LA) | −0.057 | −0.091 | 0.399 | −0.080 | 0.411 | 0.049 | 1 | |

| GDP growth (GG) | 0.007 | −0.106 | −0.203 | −0.090 | −0.211 | −0.129 | −0.040 | 1 |

| Current account balance (CA) | −0.021 | 0.120 | 0.198 | 0.086 | 0.150 | −0.104 | 0.032 | −0.118 |

| Exchange rates (ER) | 0.132 | 0.079 | −0.070 | 0.030 | −0.131 | −0.121 | 0.079 | 0.172 |

| Government debt (GD) | −0.046 | 0.341 | 0.334 | 0.176 | 0.244 | 0.177 | −0.046 | −0.280 |

| Interest cost (IC) | −0.022 | −0.179 | −0.023 | −0.215 | 0.004 | 0.146 | 0.009 | −0.127 |

| Income per capita (IPC) | −0.317 | 0.310 | 0.500 | 0.365 | 0.594 | 0.358 | 0.135 | 0.322 |

| Inflation (Inf) | 0.128 | 0.063 | −0.068 | 0.003 | −0.141 | −0.105 | 0.052 | 0.081 |

| Banking crisis (BC) | 0.069 | 0.127 | 0.077 | 0.123 | 0.090 | 0.074 | −0.042 | −0.295 |

| Currency crisis (CC) | 0.113 | 0.049 | 0.020 | 0.049 | 0.024 | −0.042 | 0.076 | −0.187 |

| Variable | CA | ER | GD | IC | IPC | Inf | BC | CC |

| Current account balance (CA) | 1 | |||||||

| Exchange rates (ER) | −0.143 | 1 | ||||||

| Government debt (GD) | 0.062 | −0.303 | 1 | |||||

| Interest cost (IC) | −0.188 | −0.023 | 0.407 | 1 | ||||

| Income per capita (IPC) | 0.288 | −0.297 | 0.325 | −0.028 | 1 | |||

| Inflation (Inf) | −0.189 | 0.844 | −0.247 | 0.058 | −0.305 | 1 | ||

| Banking crisis (BC) | 0.015 | 0.039 | 0.131 | 0.092 | 0.089 | 0.124 | 1 | |

| Currency crisis (CC) | −0.051 | 0.275 | −0.052 | 0.036 | −0.061 | 0.318 | 0.091 | 1 |

| Decentralized Government Level | Local | Subnational | Local | Subnational |

|---|---|---|---|---|

| Tax revenue decentralization | −10.1570 *** | −6.2877 *** | - | - |

| (0.4492) | (0.6126) | - | - | |

| Expenditure decentralization | - | - | 10.7513 *** | 7.9495 *** |

| - | - | (0.5340) | (0.3415) | |

| GDP growth | 0.0081 | −0.0195 | −0.0445 ** | −0.0150 |

| (0.0135) | (0.0156) | (0.0192) | (0.0152) | |

| Current account balance | 0.0197 *** | 0.0264 *** | 0.0111 * | 0.0024 |

| (0.0047) | (0.0053) | (0.0064) | (0.0053) | |

| Exchange rates | 3.1840 ** | 3.9836 *** | −1.5436 | −0.7542 |

| (1.2709) | (1.5317) | (1.9677) | (1.5295) | |

| Government debt | 0.0147 *** | 0.0110 *** | −0.0059 ** | −0.0003 |

| (0.0017) | (0.0019) | (0.0027) | (0.0019) | |

| Interest cost | −0.2514 *** | −0.1324 *** | 0.1870 *** | −0.0102 |

| (0.0220) | (0.0291) | (0.0528) | (0.0356) | |

| Income per capita | 0.1132 | 0.0597 | −1.0640 *** | −1.2452 *** |

| (0.2048) | (0.2636) | (0.2767) | (0.2138) | |

| Inflation | 0.0201 * | −0.0029 | −0.0202 | 0.0030 |

| (0.0120) | (0.0143) | (0.0176) | (0.0145) | |

| Banking crisis | 0.1976 | 0.1143 | −0.1067 | 0.0058 |

| (0.1210) | (0.1553) | (0.2418) | (0.1775) | |

| Currency crisis | 0.3056 | 0.4290 * | −0.0362 | −0.3141 |

| (0.2275) | (0.2567) | (0.3123) | (0.2553) | |

| Number of observations | 1378 | 1383 | 858 | 872 |

| Area under ROC curve | 0.9310 | 0.9329 | 0.9468 | 0.9473 |

| Log likelihood | 1145.90 | 581.69 | 666.47 | 434.72 |

| Wald chi (10) | 2074.04 *** | 580.88 *** | 428.49 *** | 854.92 *** |

| Wald test of exogeneity | 4.41 ** | 9.00 *** | 8.22 *** | 8.36 *** |

| Decentralized Government Level | Local | Subnational | Local | Subnational |

|---|---|---|---|---|

| Tax revenue decentralization | −9.7135 *** | −3.5508 * | - | - |

| (0.6656) | (2.1432) | - | - | |

| Expenditure decentralization | - | - | 10.7263 *** | −3.0389 |

| - | - | (0.4915) | (4.3142) | |

| GDP growth | 0.0062 | −0.0320 | −0.0340 * | −0.0240 |

| (0.0122) | (0.0210) | (0.0190) | (0.0262) | |

| Current account balance | 0.0131 *** | 0.0122 | 0.0023 | −0.0015 |

| (0.0044) | (0.0100) | (0.0057) | (0.0095) | |

| Exchange rates | 3.9954 *** | 5.3077 *** | −2.2482 | 4.3927 * |

| (1.2602) | (2.0191) | (2.5372) | (2.3960) | |

| Government debt | 0.0153 *** | 0.0129 *** | −0.0059 | 0.0065 * |

| (0.0015) | (0.0021) | (0.0037) | (0.0038) | |

| Interest cost | −0.2445 *** | −0.0482 | 0.1988 *** | −0.0634 |

| (0.0302) | (0.0645) | (0.0515) | (0.0793) | |

| Income per capita | 0.0227 | −0.6237 * | −0.9169 * | −0.4402 |

| (0.1954) | (0.3606) | (0.4959) | (0.8559) | |

| Inflation | 0.0073 | −0.0207 | −0.0169 | −0.0250 |

| (0.0116) | (0.0199) | (0.0176) | (0.0212) | |

| Banking crisis | 0.2616 ** | 0.3240 | −0.0926 | 0.5366 |

| (0.1254) | (0.2437) | (0.3217) | (0.3339) | |

| Currency crisis | 0.2204 | 0.4154 | −0.0036 | 0.4486 |

| (0.2291) | (0.3700) | (0.3360) | (0.3798) | |

| Number of observations | 1422 | 1435 | 882 | 895 |

| Area under ROC curve | 0.9275 | 0.9283 | 0.9366 | 0.9395 |

| Log likelihood | 1179.79 | 768.92 | 682.99 | 513.20 |

| Wald chi (10) | 1283.77 *** | 121.02 *** | 627.09 *** | 77.92 *** |

| Wald test of exogeneity | 9.20 ** | 3.08 * | 1.72 | 1.20 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nakatani, R. Sovereign Debt Crisis and Fiscal Devolution. J. Risk Financial Manag. 2024, 17, 9. https://doi.org/10.3390/jrfm17010009

Nakatani R. Sovereign Debt Crisis and Fiscal Devolution. Journal of Risk and Financial Management. 2024; 17(1):9. https://doi.org/10.3390/jrfm17010009

Chicago/Turabian StyleNakatani, Ryota. 2024. "Sovereign Debt Crisis and Fiscal Devolution" Journal of Risk and Financial Management 17, no. 1: 9. https://doi.org/10.3390/jrfm17010009

APA StyleNakatani, R. (2024). Sovereign Debt Crisis and Fiscal Devolution. Journal of Risk and Financial Management, 17(1), 9. https://doi.org/10.3390/jrfm17010009