The results have been discussed under three subsections: publication and citation structure, list of the most influential publications, and network analysis of leading publishers and publications.

3.1. Scientific Production Trend

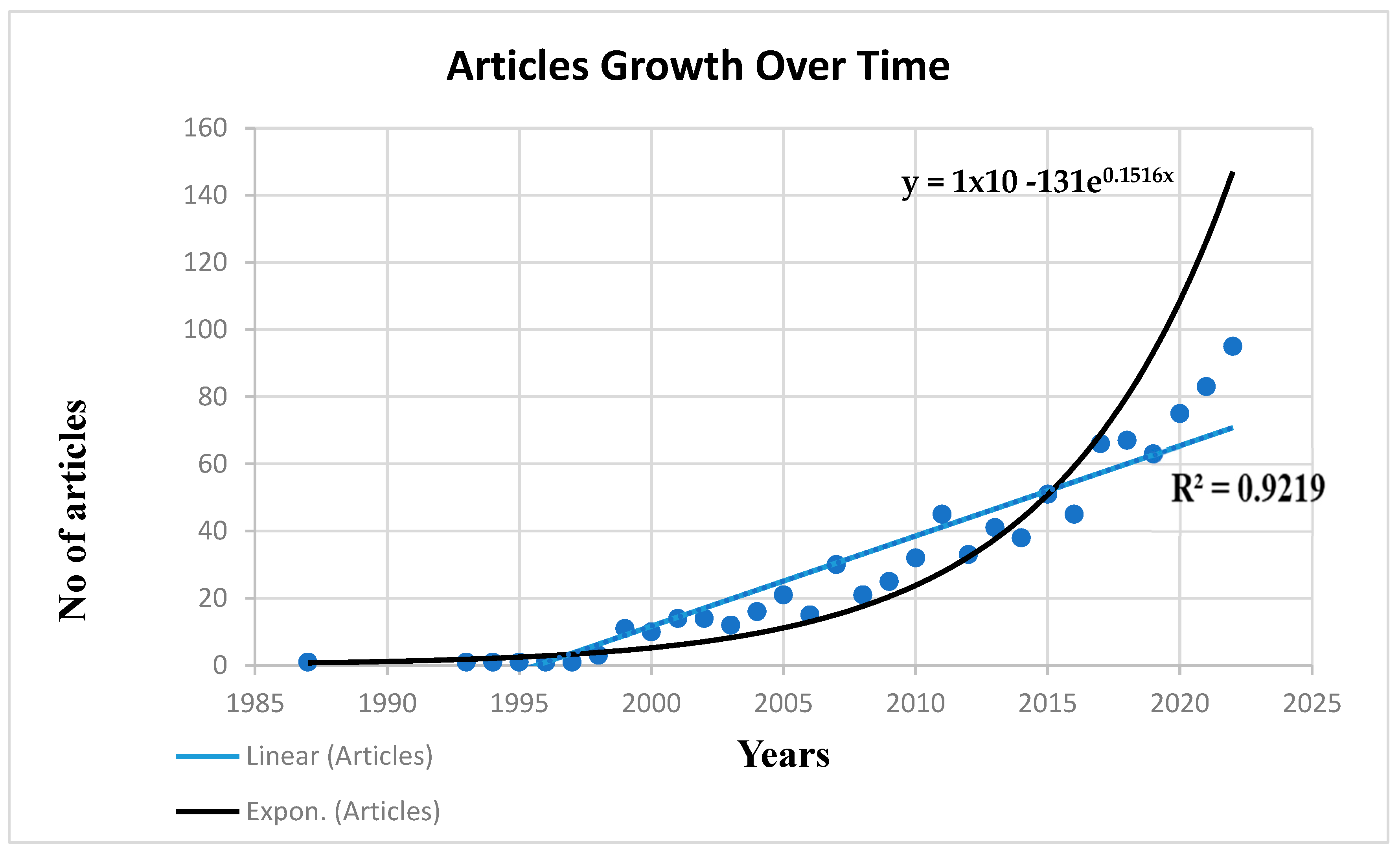

The research sought to establish the annual scientific output from 1987 to 2023. The results are shown in

Figure 2.

According to

Figure 2, there was a static trend in publications from 1987 to 1997, with at least 1 document and zero publications from 1988 to 1992. The trend changed in the next few decades. From 1998 on, there was a rapid increase in publications related to borrowers’ behavior. The highest production recorded was in 2022. This trend implies that the area has continuously gained interest among researchers. The research finding aligns with other studies related to behavioral finance, such as

Costa et al. (

2017), who established an increase in annual scientific production.

Annual scientific production growth using Price Law

The price law was formulated by Derek Solla Price to describe productivity distribution in numerous fields. The law states that a significant contribution in a given discipline is made by a small number of contributors. This principle is central in bibliometric analysis as it shows the concentration of productivity, aids in resource allocation, enables research evaluation, and helps to identify key contributors to the academic discipline. We run an exponential growth curve to estimate growth over time, and the results are shown in

Figure 3 below.

The results show a growth value (0.1516) over time. The model’s R

2 = 0.9219 indicates a high goodness of fit, as it explains 92.19% of the data variability. These findings support the results in

Figure 3, which showed growth over time. Therefore, articles on borrowers’ behavior have increasingly been published, and the area has attracted interest over time.

Further examination of journal listings from 1988, when the first article was published, to 2022 supports the findings on the rapid increase in publications, as shown in

Figure 4.

The leap in publications from 1987 can be attributed to the establishment of numerous journals focusing on development economics, such as the Journal of Development Economics, the European Economic Review, and Applied Economics, among others. The World Development Organization has also intensified research on borrowers’ behavior in its quest to address economic disparity and poverty in emerging economies relative to sustainable development goals. In addition, it can be attributed to multiple economic events, such as the debt crisis, structural adjustment programs, economic liberalization, poverty alleviation, and global trade and development, that the world has been experiencing since the beginning of 1980s. Examining cognitive biases and their effect on decision making gained traction in 1980s and 2000s (

Røpke 2005).

Journal Listing Using Bradford’s Law

Bradford’s law was developed in 1934 by Bradford and is widely used to examine the output of scientific journals. The law states that “if scientific journals are arranged in order of decreasing productivity of articles on a given subject, they may be divided into a nucleus of periodicals more particularly devoted to the subject and several groups or zones containing the same number of articles as the nucleus” (

Bradford 1934).

Table 2 below shows the top 20 core sources based on Bradford’s law.

The results show that among the top 20 journals, 15 are related to economics, 3 to finance, 1 to management, and 1 to development. One is a multidisciplinary journal. Upon further examination of the top sources, we established that the majority of the sources cover financial inclusion, poverty alleviation, credit distribution, and financial behavior, which is in tandem with the scope of borrowers’ behavior. In addition, the journals are mainly in economics, finance, management, and development, which cover borrowers’ behavior. Nonetheless, even though borrowers’ behavior is closely related to finance, only one finance-related journal has published articles related to borrowers’ behavior.

Articles Distribution According to Bradford’s Law

The research examined the distribution of articles in the three zones to determine whether it adheres to Bradford’s law. The results are shown in

Table 3.

The above findings show that Zone 1 had a minimum of 14 journals, which increases fourfold in zone 2. Similarly, the journals in zone 3 are fourfold more than those in zone 2. The distribution of articles across the three zones implies that each zone had about 329 articles, or 33% of the articles. These findings are in tandem with Bradford’s law, which posits that zones should have a roughly equal distribution of articles, and a few core journals contain the majority of articles. Therefore, the distribution of articles across different sources aligns with Bradford’s law.

Prolific Scholars, Articles, Journals, and Countries

Examining prolific scholars, articles, journals, and countries helps to identify influential research, benchmark research productivity, track research trends, and highlight global perspectives on the distribution of research resources and knowledge.

Prolific Scholars

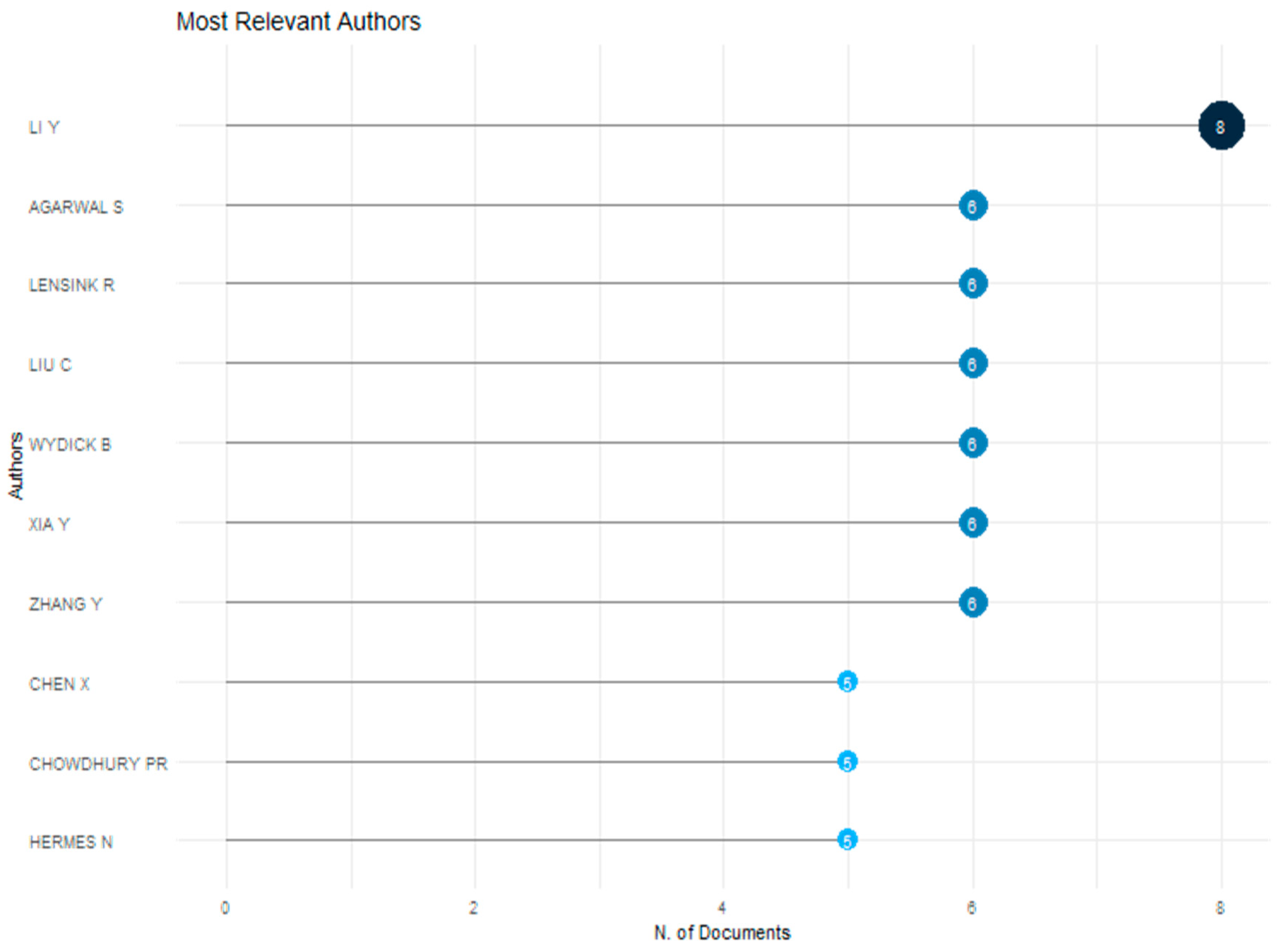

This study sought to examine the most prolific scholars based on the number of publications and H-index. The results are shown in

Figure 5 below.

Li Y has eight publications, authored individually or coauthored with other scholars. Agarwal S., Lensik R., Liu C., Wydick B., Xia Y., and Zhang Y. have made six publications each, while Chen X., Chowdhruy PR., and Hermes N. have five publications. A review of their scholarly work shows that analysis of borrowers’ behavior requires a multidisciplinary approach. For instance, Li Yinguo and Xia Yufei, though experts in computer science, have collaborated with other scholars to develop models that predict borrowers’ behavior. The authors’ research output shows that addressing biases in borrowers’ decisions can help alleviate poverty. Agarwal Sumit, Bruce Wydick, and Chowdhury focus mainly on household finance, poverty alleviation, and economic growth. This further shows a close relationship between borrowers’ behavior, household finance, poverty alleviation, and economic growth.

Source Local Impact Using the H-index

The H-index is a single indicator introduced in 2005 to measure the quantity of scientific output of a given researcher. According to

Hirsch (

2005), “A scientist has index H if H of his or her Np papers have at least H citations each and the other (Np-h) papers have less or equal H citations each”. It is an effective measure since it combines measures of impact and quantity, characterizes researchers’ scientific output objectively, and outperforms other single measures.

The results show that seven authors had an H-index of 5, while three had 4 (see

Table 4). These findings imply that the top seven authors have published five papers, and each paper has been cited at least five times by others. Similarly, the authors with an H-index of 4 have published four papers and been cited at least five times by others. Though scholars such as Li Y. have published more papers than Agarwal S., as shown in

Figure 5, both have the same H-index, which implies that Agarwal has received more citations despite publishing fewer papers than Li Y.

Most Cited Articles

Further review of the most cited articles globally can help to identify influential research, measure research impact, understand research trends, benchmark research quality, identify pioneering researchers, and inform research strategies.

Table 5 shows the topmost cited articles globally.

Publications by Berger AN are among the most cited. However, they were published earlier compared to other scholars, such as Gomper P., whose studies have gained great interest over time. The most-cited article by Berger AN examined relationship lending and the importance of “soft” information to the loan officer, who acts as a repository of the soft information. On the other hand, Diamond DW article explores lenders’ relationship-specific skills with borrowers and their impact on liquidity, while Berger’s AN second article examines relationship lending, growth in non-core funding, and off-balance-sheet guarantees as the main drivers of crises. These studies underscore the importance of understanding soft information and relationships in the borrower-lender decision-making process. Even though institutions have developed mechanisms to determine borrowers’ credit worthiness, “soft” information is mainly overlooked and plays a critical role in the decision-making process. Other most-cited studies focus on consumer credit scoring metrics, fintech, rational herding, credit risks, home biases, group lending, cultural differences, herding behavior, and crowdfunding campaigns. These themes are prevalent at both the household and firm levels and have a great impact on the decision-making process. Therefore, the top cited articles show a rising interest in the roles and effects of soft information in financial decisions.

Productivity of Authors Based on Lotka’s Law

The research used Lotka’s law to examine the productivity of authors. The law was proposed by Lotka in 1926 to test the frequency distribution of scientific output. The law states that “The number of authors making n contributions is 1/n

2 of those making one, and the proportion of contributors making a single contribution is 60%.

Table 6 shows authors productivity based on Lotka’s law.

The results show that 87.1% of the researchers studying borrowers’ behavior had written a single document. This finding contradicts Lotka’s law, which expects 60% of the authors to have one publication. Therefore, this study’s data deviated from the assumption made by Lotka’s law.

Most prolific Sources (Journals)

The research sought to establish the most prolific journals using the H-index. Similar to articles, the H-index is used to show the quality of a journal (

Mingers et al. 2012). It is robust to extreme values and poor data, easy to understand and compute, and a good measure of the overall impact of a journal. The higher the h-index, the higher the quality of the journal.

Table 7 shows the h-index of the top ten journals.

Table 7 shows that the top three journals in borrowers’ behavior were Management Science, Applied Economics, and World Development, with H-indexes of 278, 278, and 208, respectively. The journal with the lowest h-index is Economic Development and Cultural Change, with a H-index of 80. These metrics imply that the top 10 journals have a high impact, as evidenced by their high H-index. Moreover, all the top 10 journals are ranked Q1 in SCIMAGO.

Countries Production Over Time

Countries production over time helps to assess the research performance and productivity of different countries in a given field based on the affiliation of the authors. In addition, it shows the research trends and patterns in a country’s research output. The research sought to establish countries’ production over time, and the results are shown in

Figure 6.

In terms of countries, the United States has the largest number of publications on borrowers’ behavior, as shown in

Figure 6. Between 1987 and 1997, China, Germany, Italy, the United Kingdom, and the United States of America had almost equal but fewer publications. This trend continued until 2000, when the USA and the United Kingdom published more scientific papers compared to other countries. Since then, the USA has published more articles than other countries, as scholars’ interests were drawn towards understanding borrowers’ behavior to enhance access to credit. This finding is in line with

Costa et al. (

2017) and

Paule-Vianez et al. (

2020), who observed that the USA has been leading in scientific production in behavioral finance. The rise in scientific production in the USA can be attributed to industrial deregulation in the 1980s, after the introduction of the depository institutions deregulation and monetary control act of 1982. Policymakers and researchers’ interests were drawn to examine the impact of these changes on borrowers’ behavior. On the other hand, developing countries are missing since none appear among the countries with the largest publications.

3.2. Conceptual Structure and Network Analysis

In this section, word cloud, keyword frequency, network analysis of co-occurrence of keywords, and bibliographic coupling of sources and authors have been undertaken.

Word Cloud

Word cloud is a text visualization tool that shows common words within the researcher’s area of study. Frequently used words appear bigger, while less used words appear smaller (

Cooshna-Naik 2022).

Figure 7 shows frequent keywords in borrowers’ behavior.

Figure 7 shows that lending behavior and credit provision are the main keywords of interest among the analyzed publications examining borrowers’ behavior. In addition, banking, finance, microfinance, financial market, financial system, interest rate, risk assessment, and financial crisis are other notable words that attracted attention. This shows a strong interdependence between notable keywords and borrowers’ behavior. The two main keywords aforementioned, lending behavior and credit provision, appeared 365 and 279 times, respectively. Banking came close with a frequency of 239, as shown in

Table 8. The banking sector examines borrowers’ behavior before availing credit, which defines their lending behavior and explains the relationship between the key terms and borrowers’ behavior. The behavior of the borrowers, such as saving, history of paying credit, and earnings, is critical when creditors are evaluating and determining the borrowers’ default risk.

Frequency of Key Words According to Zipf’s Law

Created by George K. Zipf, Zipf’s law states that “if words occurring in natural language text of sizeable length were listed in the order of decreasing frequency, then the rank of any given word in the list would be inversely proportional to the frequency occurrence of the word.”

Table 8 below shows the frequency of the top 10 words.

Table 8 shows that lending behavior, credit provision, and banking have the highest frequency, while financial crises, interest rates, the financial market, and debt have the least frequency. The words with the least frequency indicate potential study directions (

Mulay et al. 2020). Therefore, further studies can focus on the nexus between the financial crisis, interest rate, debt, financial crisis, financial market, and borrowers’ behavior. A graph was developed to determine whether there is an inverse relationship between word rank and frequency as stated in Zipf’s law, as shown in

Figure 8.

A line of best fit was drawn to show the relationship between word frequency and rank. The results show an inverse relationship between word frequency and rank, as postulated in Zipf’s law. Therefore, the findings from the analysis of the data used in this study are in tandem with Zipf’s law.

Analysis of Co-occurrence of Keywords

Co-occurrence network visualization shows the connexon of key texts centered on their combined occurrence. Prior to analysis, similar keywords were combined. The publication keyword was set to the default value of 5.212 key terms met the criteria; nonetheless, it was not possible to do meaningful analysis since the resulting image was cluttered. Consequently, the minimum co-occurrence of keywords was constantly increased by 1 until the best outcome was achieved. The best outcome was attained at the value of 12, which resulted in 31 items, 5 clusters, 162 links, and 452 total link strengths, as shown in

Figure 9.

Cluster 1, marked in red, has banking as the keyword with 121 occurrences, followed by adverse selection with 19 occurrences. Other keywords in this cluster are asymmetric information, moral hazard, credit rationing, competition, banks, and small and medium enterprises. The key idea that can be derived from this cluster is how the banking sector examines borrowers’ behavior when providing credit facilities. The second cluster (2), marked in green, has peer-to-peer lending as the main keyword with 24 occurrences.

Others include fintech, crowdfunding, credit scoring, financial inclusion, and credit risk. The third cluster (3) has micro-finance as the keyword, with 215 occurrences. Others include group lending, poverty, and social capital. The fourth cluster (4), marked in green, has sustainability as the main keyword with 15 occurrences. Others include risk, financial inclusion, and regulation. The fifth cluster (5), marked in purple, has finance as the keyword with 50 occurrences. Others include gender and entrepreneurship.

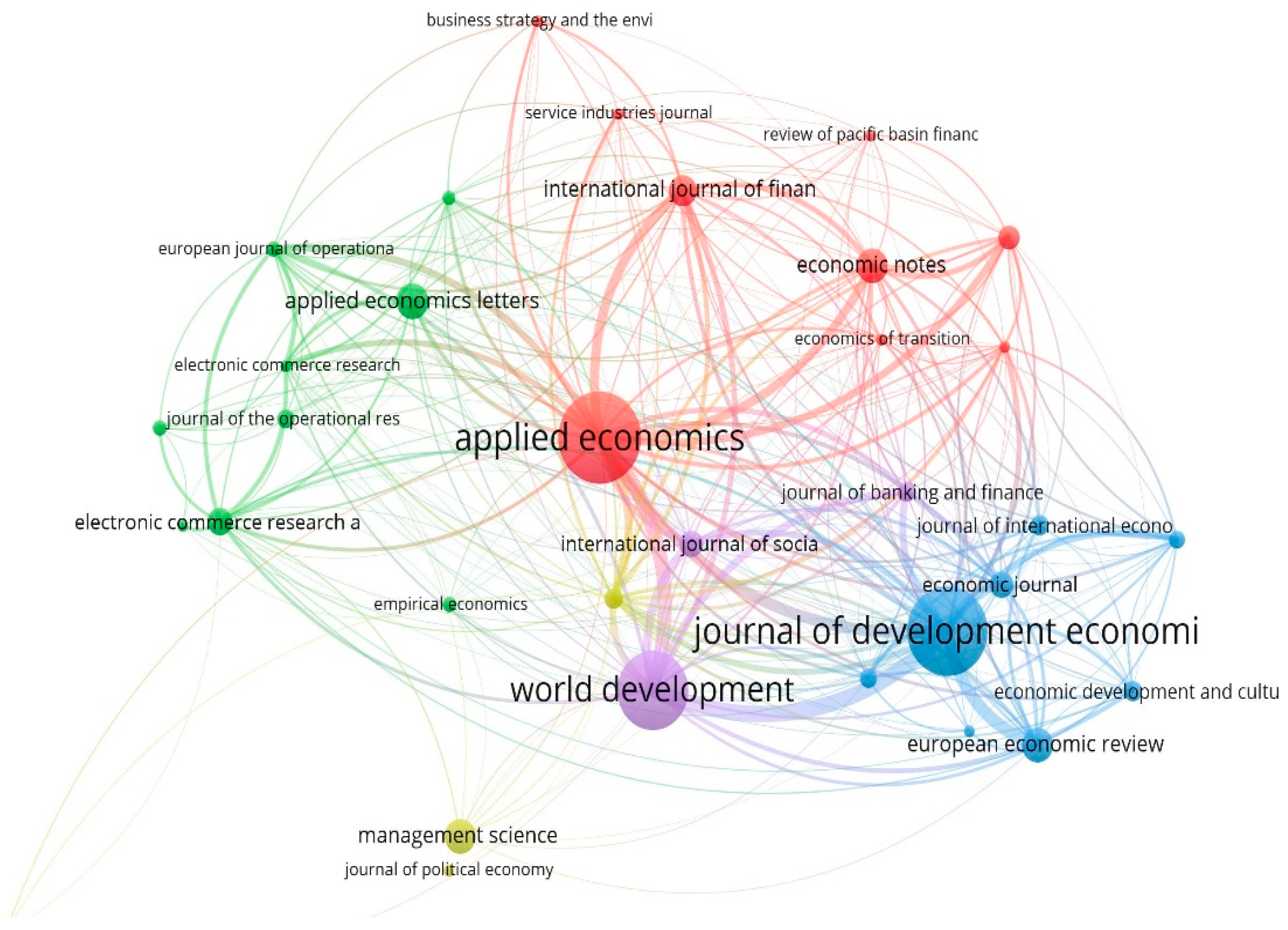

Bibliographic Coupling of Sources

The bibliographic coupling of sources increases when journals or sources have a greater number of common references. The results of the bibliographic coupling of sources are shown in

Figure 10 below. In this study, only sources with at least seven publications were selected, but the count of citations for a publication was kept at default zero. Consequently, 33 sources were obtained. The Journal of Applied Economics had the highest number of publications, 54 documents, and 938 total link strength. The Journal of Development Economics had 53 documents, which is close to the Journal of Applied Economics but has a weaker total link strength of 773. The analysis yielded five clusters. The first cluster, red, has major documents related to applied economics. The second cluster, blue, has economic documents. The third cluster, purple, has predominantly social development documents that are linked to both economics and applied economics Journals. The fourth cluster, yellow, has sources related to economic surveys, political economy, and management science. The fifth cluster, green, has sources related to Applied Economics Letters, electronic commerce research, technological forecasting, and operational economics research.

Three-Field Plot Analysis on Borrowers Behavior

Three-field plot analysis is an analytical and visualization approach that shows the relationship between keywords, journals, countries, and authors. It helps to identify research trends, map interdisciplinary research, and evaluate research impact. The top 10 countries, keywords, and sources were selected to develop a Sankey three-plot diagram, which aids in visualizing the flow of scientific literature grounded in selected fields. As shown in

Figure 11 below, the USA dominates scientific research on borrowers’ behavior, followed by India, France, Australia, Italy, Spain, the United Kingdom, Germany, Canada, and China. On the other hand, the top 10 dominant keywords are microfinance, banking, finance, gender, micro-credit, group lending, peer-to-peer lending, social capital, crowdfunding, and credit risk. The top ten sources of scientific information on borrowers’ behavior are the Journal of Development Economics, World Development, Applied Economics, Management Science, Electronic Commerce Research and Applications, European Economic Review, Applied Economic Review, International Journal of Finance and Economics, and Economic Notes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}