The Moderating Role of Corporate Governance on the Associations of Internal Audit and Its Quality with the Financial Reporting Quality: The Case of Yemeni Banks

Abstract

:1. Introduction

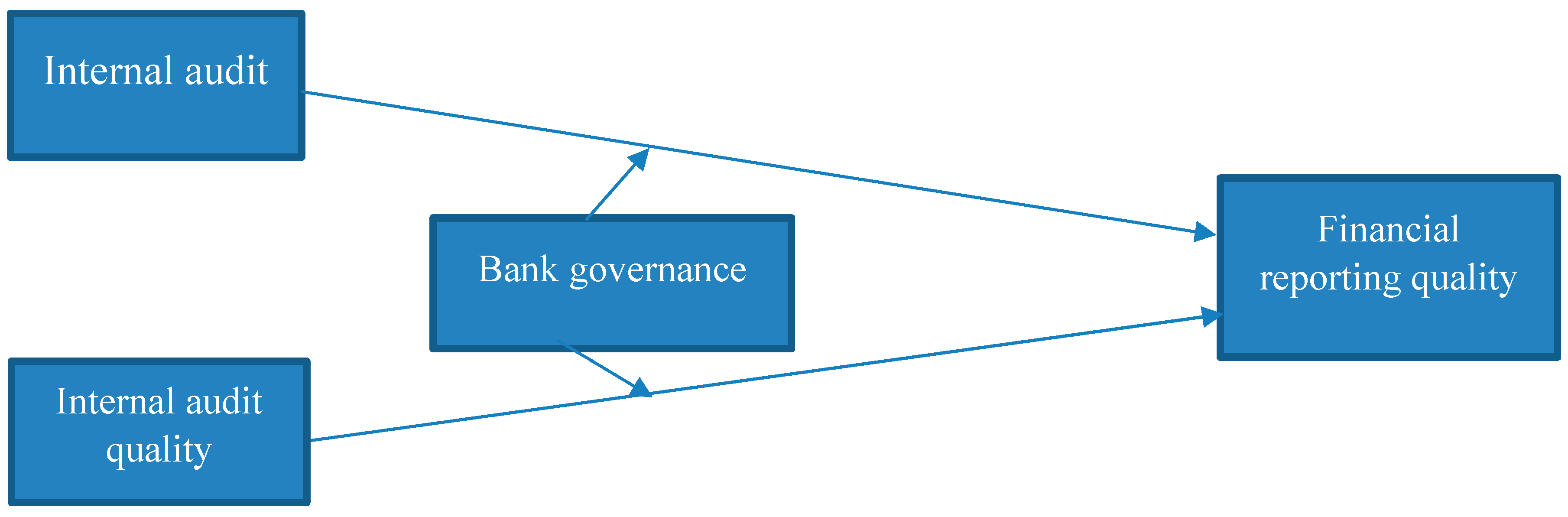

2. Literature Review and Developing Hypotheses

2.1. Internal Audit

2.2. The QIA

2.3. BG and SFR

2.4. Corporate Governance, IA, and Quality of Financial Reports

2.5. Methodology

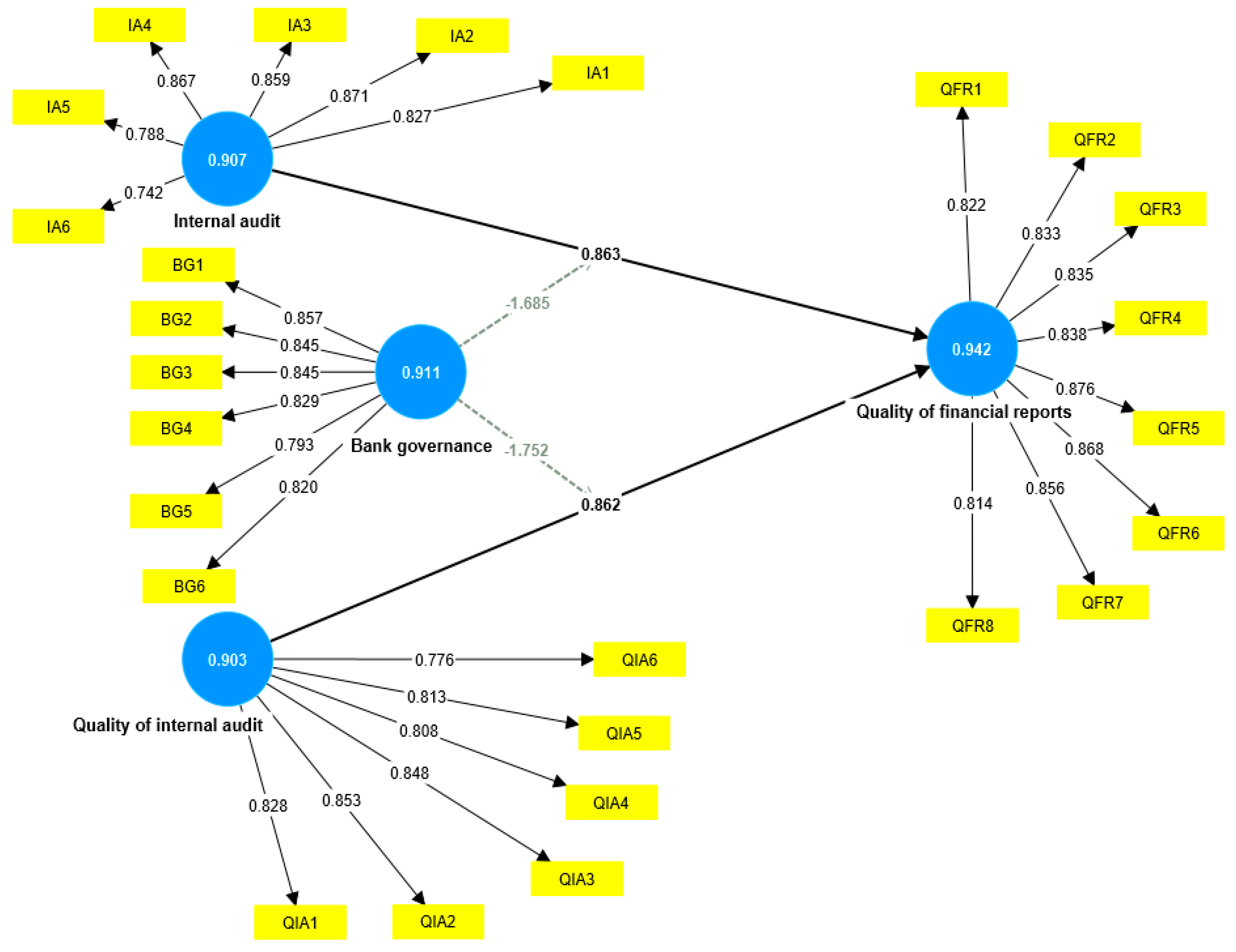

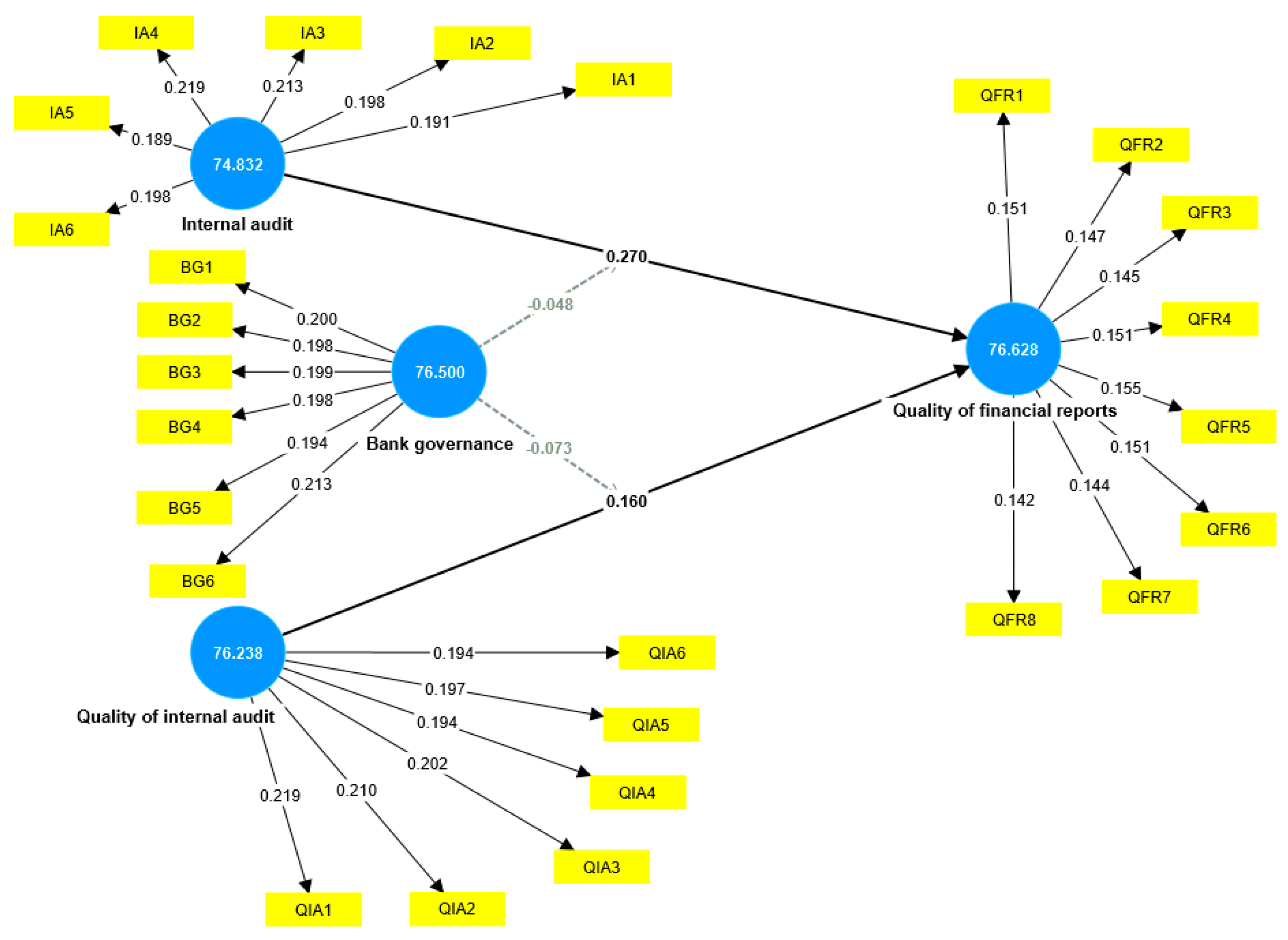

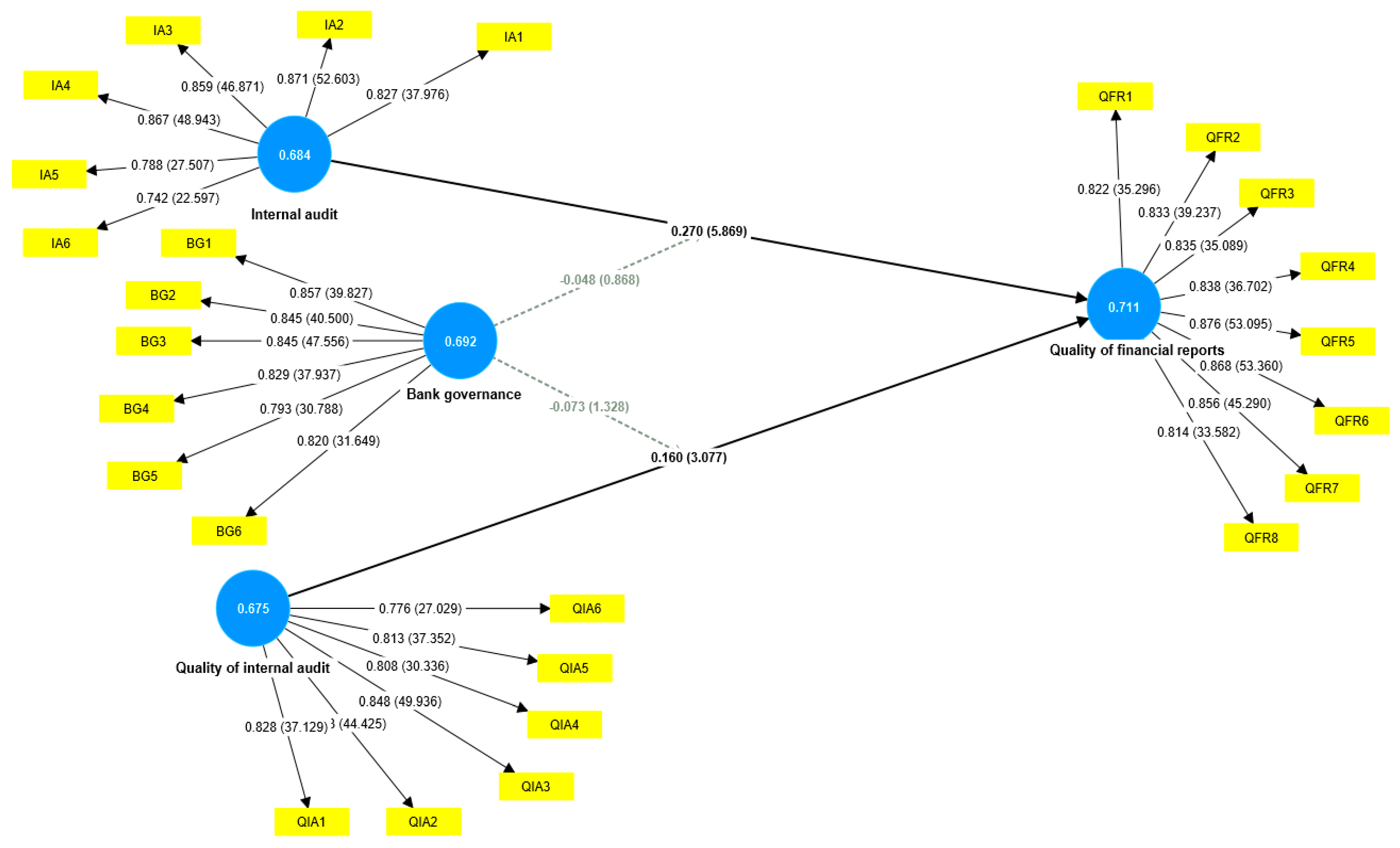

3. Results Desiccations

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Abdullah, Razimah Binti. 2014. Redefining Internal Audit Performance: Impact on Corporate Governance. Edith Cowan University: Available online: https://ro.ecu.edu.au/theses/1567 (accessed on 15 August 2023).

- Al Momani, Mohammed Abdullah, and Mohammed Ibrahim Obeidat. 2013. The effect of auditors’ ethics on their detection of creative accounting practices: A field study. International Journal of Business and Management 8: 118–36. [Google Scholar] [CrossRef]

- Awang, Zainudin, Asyraf Afthanorhan, Mahadzirah Mohamad, and M. A. M. Asri. 2015. An evaluation of measurement model for medical tourism research: The confirmatory factor analysis approach. International Journal of Tourism Policy 6: 29–45. [Google Scholar] [CrossRef]

- Bananuka, Juma, Sadress Night, Muhammed Ngoma, and Grace Muganga Najjemba. 2019a. Internet financial reporting adoption: Exploring the influence of board role performance and isomorphic forces. Journal of Economics, Finance and Administrative Science 24: 266–87. [Google Scholar] [CrossRef]

- Bananuka, Juma, Stephen Korutaro Nkundabanyanga, Irene Nalukenge, and Twaha Kaawaase. 2018. Internal audit function, audit committee effectiveness and accountability in the Ugandan statutory corporations. Journal of Financial Reporting and Accounting 16: 138–57. [Google Scholar] [CrossRef]

- Bananuka, Juma, Zainabu Tumwebaze, Doreen Musimenta, and Patience Nuwagaba. 2019b. Determinants of adoption of international financial reporting standards in Ugandan micro finance institutions. African Journal of Economic and Management Studies 10: 336–55. [Google Scholar] [CrossRef]

- Bartov, Eli, Ferdinand A. Gul, and Judy S. L. Tsui. 2000. Discretionary-accruals models and audit qualifications. Journal of Accounting and Economics 30: 421–52. [Google Scholar] [CrossRef]

- Beasley, Mark S., and Kathy R. Petroni. 2001. Board independence and audit-firm type. Auditing: A Journal of Practice & Theory 20: 97–114. [Google Scholar] [CrossRef]

- Betti, Nathanaël, Gerrit Sarens, and Ingrid Poncin. 2021. Effects of digitalisation of organisations on internal audit activities and practices. Managerial Auditing Journal 36: 872–88. [Google Scholar] [CrossRef]

- Changezi, Nadia Ishaq, and A. Saeed. 2014. Impact of corporate governance framework on the organizational performance. IOSR Journal of Business and Management 16: 73–78. [Google Scholar] [CrossRef]

- Chin, Wynne W. 1998a. Commentary: Issues and opinion on structural equation modeling. MIS Quarterly 1998: 7–16. [Google Scholar]

- Chin, Wynne W. 1998b. The partial least squares approach to structural equation modeling. Modern Methods for Business Research 295: 295–336. [Google Scholar]

- D’Onza, Giuseppe, Georges M. Selim, Rob Melville, and Marco Allegrini. 2015. A Study on Internal Auditor Perceptions of the Function Ability to Add Value. International Journal of Auditing 19: 182–94. [Google Scholar] [CrossRef]

- Drábková, Zita, and Martin Pech. 2022. Comparison of Creative Accounting Risks in Small Enterprises: The Different Branches Perspective. Available online: https://dspace5.zcu.cz/handle/11025/47484 (accessed on 10 August 2023).

- Drogalas, George, Michail Pazarskis, Evgenia Anagnostopoulou, and Angeliki Papachristou. 2017. The effect of internal audit effectiveness, auditor responsibility and training in fraud detection. Accounting and Management Information Systems 16: 434–54. [Google Scholar] [CrossRef]

- Field, Andy. 2009. Discovery Statistics Using SPSS: And Sex, and Drugs and Rock ‘N’roll. London: Sage. [Google Scholar]

- Hair, Joe F., Jr., Marko Sarstedt, Lucas Hopkins, and Volker G. Kuppelwieser. 2014. Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review 26: 106–21. [Google Scholar] [CrossRef]

- Hair, Joe F., Jr., Marko Sarstedt, Lucy M. Matthews, and Christian M. Ringle. 2016. Identifying and treating unobserved heterogeneity with FIMIX-PLS: Part I–method. European Business Review 28: 63–76. [Google Scholar] [CrossRef]

- Hanim Fadzil, Faudziah, Hasnah Haron, and Muhamad Jantan. 2005. Internal auditing practices and internal control system. Managerial Auditing Journal 20: 844–66. [Google Scholar] [CrossRef]

- Hazaea, Saddam A., Jinyu Zhu, Ebrahim Mohammed Al-Matari, Nabil Ahmed M. Senan, Saleh F. A. Khatib, and Saif Ullah. 2021. Mapping of internal audit research in China: A systematic literature review and future research agenda. Cogent Business & Management 8: 1938351. [Google Scholar] [CrossRef]

- Hazami-Ammar, Sourour. 2019. Internal auditors’ perceptions of the function’s ability to investigate fraud. Journal of Applied Accounting Research 20: 134–53. [Google Scholar] [CrossRef]

- IFRS. 2020. Conceptual Framework for Financial Reporting. Available online: https://www.ifrs.org/-/media/project/conceptual-framework/fact-sheet-project-summary-and-feedback-statement/conceptual-framework-project-summary.pdf (accessed on 20 June 2020).

- Jarah, Baker Akram Falah, Mufleh Amin Al Jarrah, Murad Ali Ahmad Al-Zaqeba, and Mefleh Faisal Mefleh Al-Jarrah. 2022. The role of internal audit to reduce the effects of creative accounting on the reliability of financial statements in the Jordanian islamic banks. International Journal of Financial Studies 10: 60. [Google Scholar] [CrossRef]

- Johnstone, Karla, Chan Li, and Kathleen Hertz Rupley. 2011. Changes in corporate governance associated with the revelation of internal control material weaknesses and their subsequent remediation. Contemporary Accounting Research 28: 331–83. [Google Scholar] [CrossRef]

- Khlif, Hichem, and Khaled Samaha. 2014. Internal control quality, Egyptian standards on auditing and external audit delays: Evidence from the E gyptian stock exchange. International Journal of Auditing 18: 139–54. [Google Scholar] [CrossRef]

- Levis, Julien. 2006. Adoption of corporate social responsibility codes by multinational companies. Journal of Asian Economics 17: 50–55. [Google Scholar] [CrossRef]

- Mansor, N., Ayoib Che-Ahmad, Nurwati Ashikkin Ahmad-Zaluki, and A. H. Osman. 2013. Corporate governance and earnings management: A study on the Malaysian family and non-family owned PLCs. Procedia Economics and Finance 7: 221–29. [Google Scholar] [CrossRef]

- Munteanu, Victor, Lavinia Copcinschi, Carmen Luschi, and Anda Laceanu. 2016. Internal audit-determinanat factor in preventing and detecting fraud related activity to public entities financial accounting. Knowledge Horizons. Economics 8: 14. [Google Scholar]

- Murphy, Tim, and Vincent O’Connell. 2013. Discourses surrounding the evolution of the IASB/FASB Conceptual Framework: What they reveal about the “living law” of accounting. Accounting, Organizations and Society 38: 72–91. [Google Scholar] [CrossRef]

- Nalukenge, Irene. 2020. Board role performance and compliance with IFRS disclosure requirements among microfinance institutions in Uganda. International Journal of Law and Management 62: 47–66. [Google Scholar] [CrossRef]

- Nalukenge, Irene, Stephen Korutaro Nkundabanyanga, and Joseph Mpeera Ntayi. 2018. Corporate governance, ethics, internal controls and compliance with IFRS. Journal of Financial Reporting and Accounting 16: 764–86. [Google Scholar] [CrossRef]

- Nalukenge, Irene, Ven Tauringana, and Joseph Mpeera Ntayi. 2017. Corporate governance and internal controls over financial reporting in Ugandan MFIs. Journal of Accounting in Emerging Economies 7: 294–317. [Google Scholar] [CrossRef]

- Nkundabanyanga, Stephen K., and Augustine Ahiauzu. 2012. Board Role Performance in Uganda’s Services Sector Firms. Kampala: Uganda National Council for Science & Technology. [Google Scholar]

- Nkundabanyanga, Stephen Korutaro, Venancio Tauringana, Waswa Balunywa, and Stephen Naigo Emitu. 2013. The association between accounting standards, legal framework and the quality of financial reporting by a government ministry in Uganda. Journal of Accounting in Emerging Economies 3: 65–81. [Google Scholar] [CrossRef]

- Ogoun, Stanley, and Emmanuel Atagboro. 2020. Internal audit and creative accounting practices in ministries, departments and agencies (MDAS): An empirical analysis. Open Journal of Business and Management 8: 552. [Google Scholar] [CrossRef]

- Oino, Isaiah. 2019. Do disclosure and transparency affect bank’s financial performance? Corporate Governance: The International Journal of Business in Society 19: 1344–61. [Google Scholar] [CrossRef]

- Oussii, Ahmed Atef, and Neila Boulila Taktak. 2018a. Audit committee effectiveness and financial reporting timeliness: The case of Tunisian listed companies. African Journal of Economic and Management Studies 9: 34–55. [Google Scholar] [CrossRef]

- Oussii, Ahmed Atef, and Neila Boulila Taktak. 2018b. The impact of internal audit function characteristics on internal control quality. Managerial Auditing Journal 33: 450–69. [Google Scholar] [CrossRef]

- Pavlou, Paul A., and Mendel Fygenson. 2006. Understanding and predicting electronic commerce adoption: An extension of the theory of planned behavior. MIS Quarterly 2006: 115–43. [Google Scholar] [CrossRef]

- Rakipi, Romina, Federica De Santis, and Giuseppe D’Onza. 2021. Correlates of the internal audit function’s use of data analytics in the big data era: Global evidence. Journal of International Accounting, Auditing and Taxation 42: 100357. [Google Scholar] [CrossRef]

- Roussy, Melanie, and Marion Brivot. 2016. Internal audit quality: A polysemous notion? Accounting, Auditing & Accountability Journal 29: 714–38. [Google Scholar] [CrossRef]

- Saleh, Mousa Mohammad Abdullah, Omar Jawabreh, and Enas Fakhri Mohammad Abu-Eker. 2023. Factors of applying creative accounting and its impact on the quality of financial statements in Jordanian hotels, sustainable practices. Journal of Sustainable Finance & Investment 13: 499–515. [Google Scholar] [CrossRef]

- Saunders, Mark, Philip Lewis, and Adrian Thornhill. 2009. Research Methods for Business Students. London: Pearson Education. [Google Scholar]

- Vadasi, Christina, Michalis Bekiaris, and Andreas Andrikopoulos. 2020. Corporate governance and internal audit: An institutional theory perspective. Corporate Governance: The International Journal of Business in Society 20: 175–90. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| The Study Sample | Respondents |

|---|---|

| Sanaa Commercial Bank | 24 |

| Dhamar Commercial Bank | 27 |

| Yarim Commercial Bank | 30 |

| Commercial Bank of Ibb | 27 |

| Commercial Bank of Taiz | 24 |

| Omran Commercial Bank | 23 |

| Al Mahwit Commercial Bank | 28 |

| Marib Commercial Bank | 27 |

| TOTAL | 210 |

| EFA | CFA | ||||||

|---|---|---|---|---|---|---|---|

| PCA | Reliability | Convergent Validity | |||||

| Construct | Element | Factor Loadings | % of Variance Explained by a Factor of Unidimensionality | Cronbach’s Alpha | Factor Loading b | T Values | p Values |

| Internal audit | 74.832 | 0.907 | |||||

| IA1 | 0.827 | 0.826 | 37.976 | 0.000 | |||

| IA2 | 0.871 | 0.870 | 52.603 | 0.000 | |||

| IA3 | 0.859 | 0.859 | 46.871 | 0.000 | |||

| IA4 | 0.867 | 0.866 | 48.943 | 0.000 | |||

| IA5 | 0.788 | 0.787 | 27.507 | 0.000 | |||

| IA6 | 0.742 | 0.740 | 22.597 | 0.000 | |||

| Quality of internal audit | 76.238 | 0.903 | |||||

| QIA1 | 0.828 | 0.827 | 37.129 | 0.000 | |||

| QIA2 | 0.853 | 0.852 | 44.425 | 0.000 | |||

| QIA3 | 0.848 | 0.847 | 49.936 | 0.000 | |||

| QIA4 | 0.808 | 0.807 | 30.336 | 0.000 | |||

| QIA5 | 0.813 | 0.812 | 37.352 | 0.000 | |||

| QIA6 | 0.776 | 0.775 | 27.029 | 0.000 | |||

| Bank governance | 76.500 | 0.911 | |||||

| BG1 | 0.857 | 0.855 | 39.827 | 0.000 | |||

| BG2 | 0.845 | 0.844 | 40.500 | 0.000 | |||

| BG3 | 0.845 | 0.844 | 47.556 | 0.000 | |||

| BG4 | 0.829 | 0.827 | 37.937 | 0.000 | |||

| BG5 | 0.793 | 0.791 | 30.788 | 0.000 | |||

| BG6 | 0.820 | 0.818 | 31.649 | 0.000 | |||

| Quality of financial reports | 76.628 | 0.942 | |||||

| QFR1 | 0.822 | 0.820 | 35.296 | 0.000 | |||

| QFR2 | 0.833 | 0.832 | 39.237 | 0.000 | |||

| QFR3 | 0.835 | 0.834 | 35.089 | 0.000 | |||

| QFR4 | 0.838 | 0.837 | 36.702 | 0.000 | |||

| QFR5 | 0.876 | 0.875 | 53.095 | 0.000 | |||

| QFR6 | 0.868 | 0.867 | 53.360 | 0.000 | |||

| QFR7 | 0.856 | 0.855 | 45.290 | 0.000 | |||

| QFR8 | 0.814 | 0.812 | 33.582 | 0.000 | |||

| Study Variables | IA | QIA | BG | QFR | |

|---|---|---|---|---|---|

| Internal audit | IA1 | 0.827 | 0.686 | 0.668 | 0.775 |

| IA2 | 0.871 | 0.692 | 0.670 | 0.700 | |

| IA3 | 0.859 | 0.724 | 0.708 | 0.753 | |

| IA4 | 0.867 | 0.764 | 0.710 | 0.772 | |

| IA5 | 0.788 | 0.646 | 0.637 | 0.669 | |

| IA6 | 0.742 | 0.637 | 0.659 | 0.701 | |

| Quality of internal audit | QIA1 | 0.728 | 0.828 | 0.757 | 0.764 |

| QIA2 | 0.707 | 0.853 | 0.726 | 0.731 | |

| QIA3 | 0.704 | 0.848 | 0.699 | 0.703 | |

| QIA4 | 0.660 | 0.808 | 0.648 | 0.678 | |

| QIA5 | 0.647 | 0.813 | 0.662 | 0.686 | |

| QIA6 | 0.684 | 0.776 | 0.675 | 0.678 | |

| Bank governance | BG1 | 0.668 | 0.725 | 0.857 | 0.742 |

| BG2 | 0.650 | 0.677 | 0.845 | 0.731 | |

| BG3 | 0.704 | 0.681 | 0.845 | 0.737 | |

| BG4 | 0.656 | 0.674 | 0.829 | 0.733 | |

| BG5 | 0.686 | 0.710 | 0.793 | 0.719 | |

| BG6 | 0.714 | 0.755 | 0.820 | 0.788 | |

| Quality of financial reports | QFR1 | 0.744 | 0.717 | 0.777 | 0.822 |

| QFR2 | 0.725 | 0.716 | 0.747 | 0.833 | |

| QFR3 | 0.703 | 0.721 | 0.736 | 0.835 | |

| QFR4 | 0.749 | 0.738 | 0.762 | 0.838 | |

| QFR5 | 0.760 | 0.763 | 0.782 | 0.876 | |

| QFR6 | 0.739 | 0.739 | 0.765 | 0.868 | |

| QFR7 | 0.713 | 0.714 | 0.722 | 0.856 | |

| QFR8 | 0.684 | 0.701 | 0.725 | 0.814 |

| Cronbach’s Alpha | rho_a | rho_c | AVE | |

|---|---|---|---|---|

| Internal audit | 0.907 | 0.908 | 0.928 | 0.684 |

| Quality of internal audit | 0.903 | 0.905 | 0.926 | 0.675 |

| Bank governance | 0.911 | 0.911 | 0.931 | 0.692 |

| Quality of financial reports | 0.942 | 0.942 | 0.952 | 0.711 |

| Bank Governance | BG | IA | QFR | QIA | BG × IA | BG × QIA |

|---|---|---|---|---|---|---|

| IA | 0.899 | |||||

| QFR | 0.963 | 0.932 | ||||

| QIA | 0.931 | 0.924 | 0.933 | |||

| BG × IA | 0.852 | 0.792 | 0.868 | 0.817 | ||

| BG × QIA | 0.870 | 0.794 | 0.877 | 0.825 | 0.975 |

| BG | IA | QFR | QIA | |

|---|---|---|---|---|

| BG | 0.832 | |||

| IA | 0.818 | 0.827 | ||

| QFR | 0.893 | 0.863 | 0.843 | |

| QIA | 0.847 | 0.839 | 0.862 | 0.822 |

| STDEV, T Values, p Values | ||||

|---|---|---|---|---|

| Relationship | Beta | T Statistics (|O/STDEV|) | p Values | Decision |

| BG ⟶ QFR | 0.332 | 6.227 | 0.000 | Supported |

| IA ⟶ QFR | 0.270 | 5.869 | 0.000 | Supported |

| QIA ⟶ QFR | 0.160 | 3.077 | 0.002 | Supported |

| BG × IA ⟶ QFR | −0.048 | 0.868 | 0.385 | Not Supported |

| BG × QIA ⟶ QFR | −0.073 | 1.328 | 0.184 | Not Supported |

| Error | 2.5% | 97.5% | R | F | Q2 | Decision | |

|---|---|---|---|---|---|---|---|

| BG → QFR | −0.001 | 0.224 | 0.435 | 0.175 | Supported | ||

| IA → QFR | 0.001 | 0.177 | 0.359 | 0.149 | Supported | ||

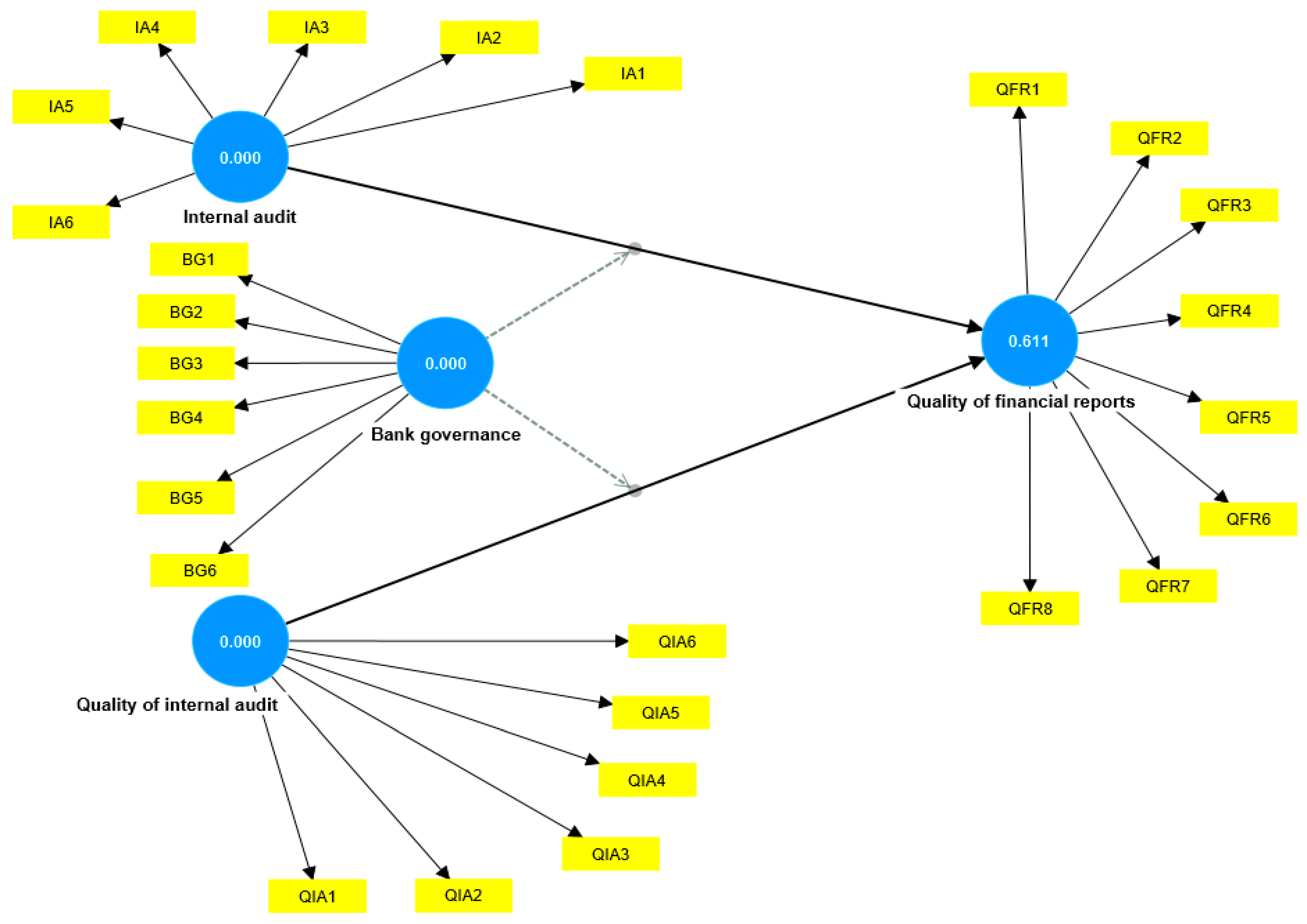

| QIA → QFR | 0.001 | 0.060 | 0.266 | 0.877 | 0.044 | 0.611 | Supported |

| BG × IA → QFR | 0.003 | −0.156 | 0.061 | 0.004 | Not Supported | ||

| BG × QIA → QFR | −0.002 | −0.185 | 0.031 | 0.008 | Not Supported |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Senan, N.A.M. The Moderating Role of Corporate Governance on the Associations of Internal Audit and Its Quality with the Financial Reporting Quality: The Case of Yemeni Banks. J. Risk Financial Manag. 2024, 17, 124. https://doi.org/10.3390/jrfm17030124

Senan NAM. The Moderating Role of Corporate Governance on the Associations of Internal Audit and Its Quality with the Financial Reporting Quality: The Case of Yemeni Banks. Journal of Risk and Financial Management. 2024; 17(3):124. https://doi.org/10.3390/jrfm17030124

Chicago/Turabian StyleSenan, Nabil Ahmed Mareai. 2024. "The Moderating Role of Corporate Governance on the Associations of Internal Audit and Its Quality with the Financial Reporting Quality: The Case of Yemeni Banks" Journal of Risk and Financial Management 17, no. 3: 124. https://doi.org/10.3390/jrfm17030124

APA StyleSenan, N. A. M. (2024). The Moderating Role of Corporate Governance on the Associations of Internal Audit and Its Quality with the Financial Reporting Quality: The Case of Yemeni Banks. Journal of Risk and Financial Management, 17(3), 124. https://doi.org/10.3390/jrfm17030124