Quantification of VaR: A Note on VaR Valuation in the South African Equity Market

Abstract

:1. Introduction

2. Empirical Study

2.1. Empirical Data

- Merafe Resources is listed on the JSE under the General Mining sector. Merafe mines chrome, which they use to produce ferrochrome. The historical daily closing prices used for our analysis was for the period from 17 December 1999 to 1 July 2013.

- Standard Bank is listed under the Banking sector. The company provides services in personal, corporate, merchant and commercial banking, mutual fund and property fund management among other services. The daily closing prices used for analysis Standard Bank data was over the period 1 September 1997 to 31 July 2014.

- African Bank is listed under Consumer Finance. The bank provides unsecured credit, retail and financial services. We use daily closing prices over the period 29 September 1997 to 31 July 2014.

- Anglo American is listed under the General Mining sector and they mine platinum, diamonds, iron ore and thermal coal. The daily closing prices over the period from 1 September 1999 to 31 July 2014 were used.

- Pre-crisis (from 1991 January–December 2007),

- Crisis period (from January 2008–December 2009),

- Post-crisis (from January 2010–July 2014).

{kind=link}

{kind=link}

{kind=link}

| Statistical Data of the Empirical Distribution over the Period January 1991–July 2014. | |||||

| Mean | Variance | Skewness | Excess Kurtosis | No. OBS3 | |

| S & P 500 | 6170 | ||||

| FTSE/JSE TOP40 | 4770 | ||||

| Standard Bank | 4090 | ||||

| African Bank | 3944 | ||||

| Anglo American | 4162 | ||||

| Merafe Resource | 2806 | ||||

| Pre-Crisis (from January 1991–December 2007) Statistical Data. | |||||

| Mean | Variance | Skewness | Kurtosis | No. OBS | |

| S & P 500 | 0.0004 | 0.0001 | –0.0746 | 3.8997 | 4262 |

| FTSE/JSE TOP40 | 0.0006 | 0.0002 | –0.6571 | 8.1379 | 3124 |

| Standard Bank | 0.0006 | 0.0006 | –0.3163 | 4.9000 | 2463 |

| African Bank | 0.0007 | 0.0009 | –0.4599 | 7.9791 | 2338 |

| Anglo American | 0.0008 | 0.0006 | –0.0394 | 3.0429 | 2520 |

| Merafe Resources | 0.0014 | 0.0014 | 0.4452 | 1.3903 | 1485 |

| Crisis Period (from January 2008–December 2009) Statistical Data. | |||||

| Mean | Variance | Skewness | Kurtosis | No. OBS | |

| S & P 500 | –0.0005 | 0.0005 | –0.0963 | 4.3544 | 505 |

| FTSE/JSE TOP40 | –0.0001 | 0.0005 | 0.0408 | 1.3969 | 501 |

| Standard Bank | 0.0000 | 0.0007 | 0.1997 | 1.3906 | 490 |

| African Bank | –0.0002 | 0.0009 | 0.0418 | 0.4575 | 491 |

| Anglo American | –0.0005 | 0.0016 | –0.1295 | 1.8202 | 499 |

| Merafe Resources | –0.0011 | 0.0022 | –0.6017 | 2.7368 | 457 |

| Post-Crisis (from January 2010–July 2014) Statistical Data. | |||||

| Mean | Variance | Skewness | Kurtosis | No. OBS | |

| S & P 500 | 0.0004 | 0.0001 | –3.2713 | 49.1255 | 1403 |

| FTSE/JSE TOP40 | 0.0005 | 0.0001 | –0.1593 | 1.3757 | 1145 |

| Standard Bank | 0.0003 | 0.0002 | –0.1336 | 1.1070 | 1137 |

| African Bank | –0.0014 | 0.0006 | –2.5109 | 29.7154 | 1115 |

| Anglo American | –0.0001 | 0.0003 | 0.1624 | 0.5933 | 1143 |

| Merafe Resources | –0.0000 | 0.0008 | 0.1183 | 1.8172 | 864 |

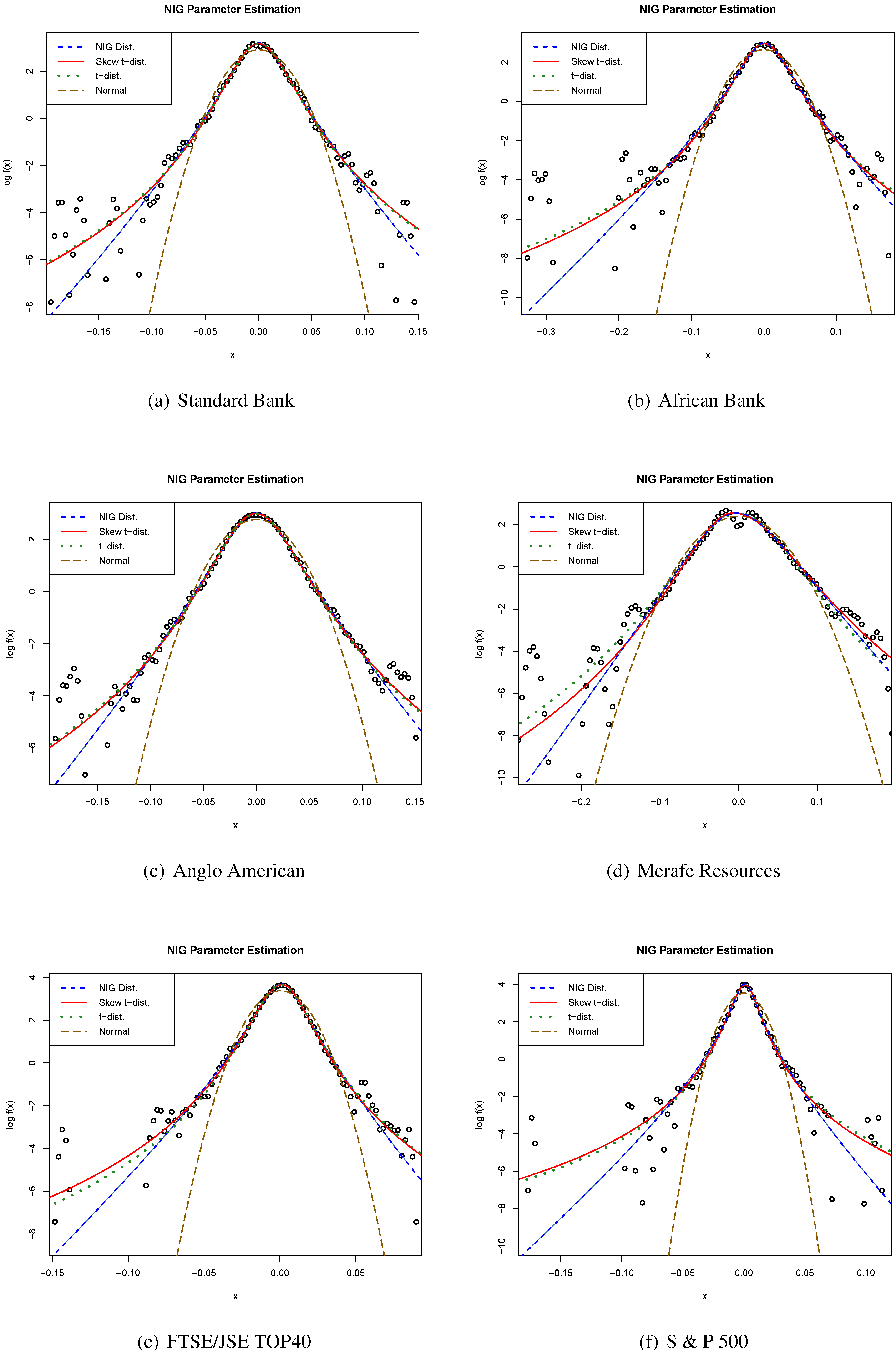

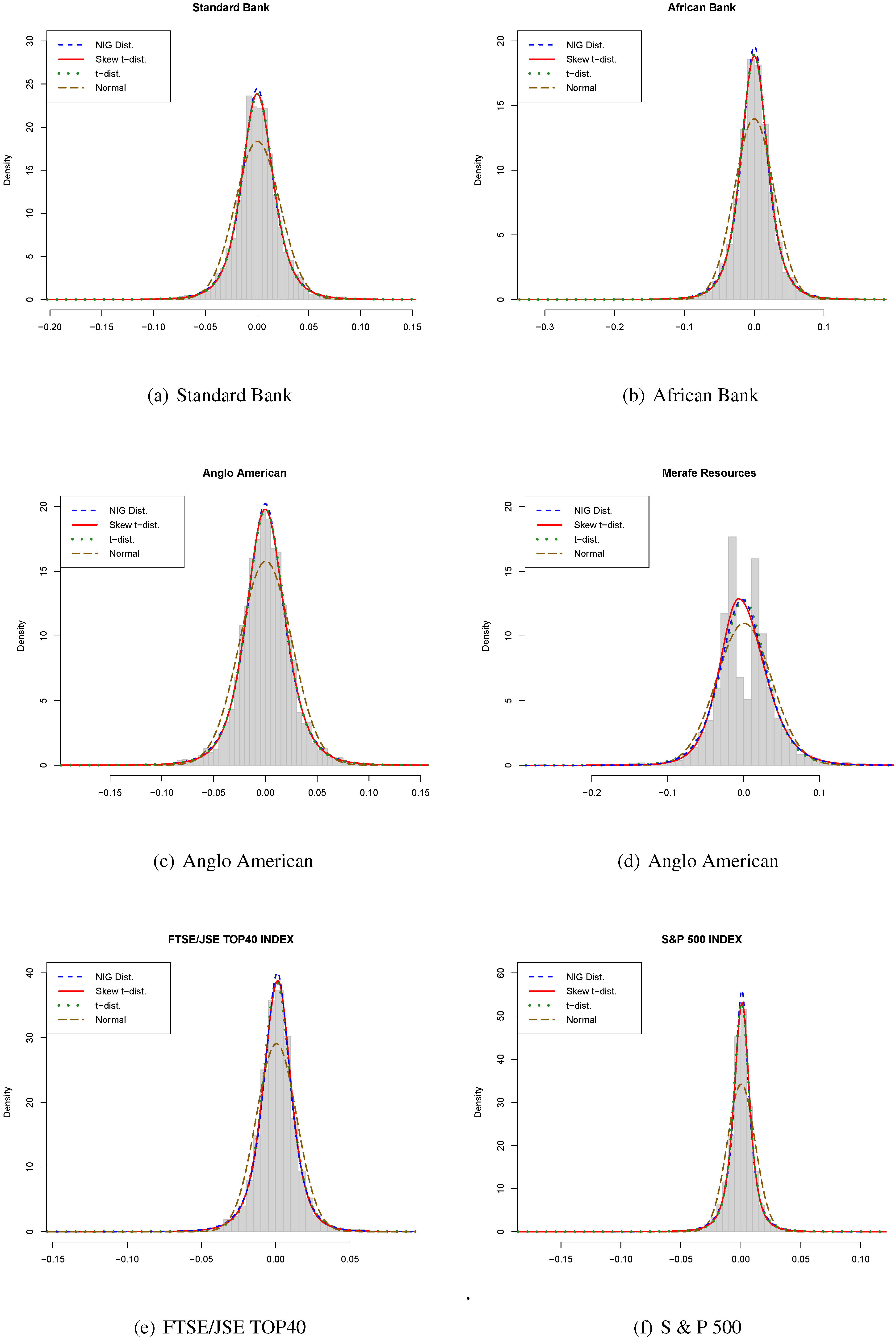

3. Fitting the Distribution

3.1. Normal Inverse Gaussian Distribution

3.2. The Student’s t-Distribution

3.3. The Skew t-Distribution

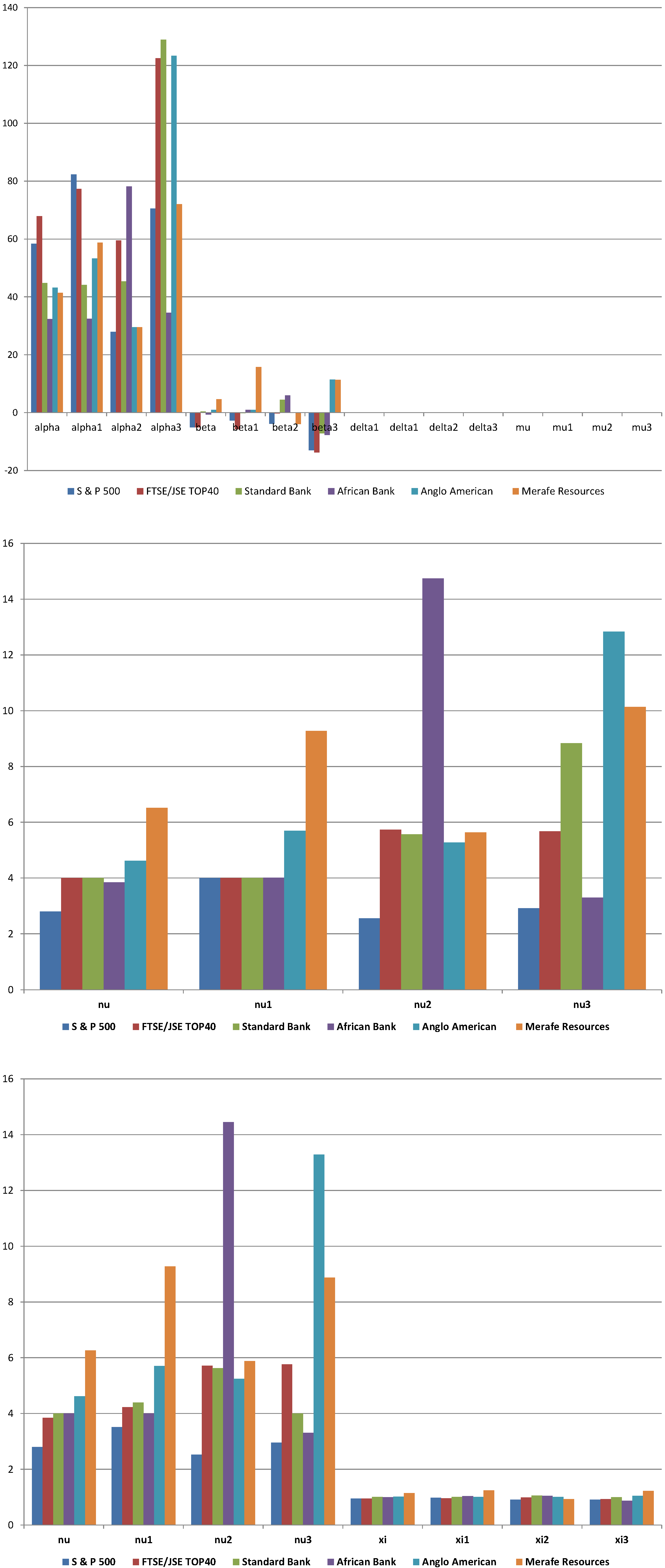

| Parameter Estimates over the Period January 1991–July 2014 | |||||||

| NIG | t-Dist. | Skew t | |||||

| S & P 500 | 58.3541 | –5.0934 | 0.0075 | 0.0009 | 2.7962 | 2.8038 | 0.9519 |

| FTSE/JSE TOP 40 | 67.8875 | –5.109 | 0.0123 | 0.0014 | 4.0000 | 3.8419 | 0.9533 |

| Standard Bank | 44.7345 | 0.3524 | 0.0208 | 0.0003 | 4.0000 | 4.0006 | 1.0145 |

| African Bank | 32.372 | –0.6613 | 0.025 | 0.0005 | 3.8414 | 4.0000 | 1.0000 |

| Anglo American | 43.1323 | 0.9557 | 0.027 | –0.0002 | 4.6143 | 4.6127 | 1.0208 |

| Merafe Resources | 41.3981 | 4.5965 | 0.0527 | –0.0054 | 6.5225 | 6.2649 | 1.1460 |

| Pre-crisis (from January 1991–December 2007) Parameter Estimates | |||||||

| NIG | t-Dist. | Skew t | |||||

| S & P 500 | 82.3073 | –2.7308 | 0.0084 | 0.0006 | 4.0000 | 3.5163 | 0.9765 |

| FTSE/JSE TOP40 | 77.3477 | –5.8151 | 0.0128 | 0.0015 | 4.0000 | 4.2290 | 0.9605 |

| Standard Bank | 44.1135 | –0.1645 | 0.0238 | 0.0007 | 4.0000 | 4.3920 | 1.0121 |

| African Bank | 32.4499 | 0.9420 | 0.0274 | –0.0001 | 4.0105 | 4.0001 | 1.0373 |

| Anglo American | 53.2541 | 0.9913 | 0.0306 | 0.0002 | 5.6917 | 5.6988 | 1.0134 |

| Merafe Resources | 58.7370 | 15.7660 | 0.0737 | –0.0192 | 9.2786 | 9.2746 | 1.2459 |

| Crisis Period (from January 2008–December 2009) Parameter Estimates | |||||||

| NIG | t-Dist. | Skew t | |||||

| S & P 500 | 27.9336 | –3.9019 | 0.0137 | 0.0014 | 2.5545 | 2.5254 | 0.9124 |

| FTSE/JSE TOP40 | 59.4900 | –0.3225 | 0.0270 | 0.0000 | 5.7367 | 5.7149 | 0.9874 |

| Standard Bank | 45.3549 | 4.4290 | 0.0323 | –0.0031 | 5.5645 | 5.6319 | 1.0618 |

| African Bank | 78.1936 | 5.9075 | 0.0715 | –0.0056 | 14.7400 | 14.4505 | 1.0546 |

| Anglo American | 29.5059 | –0.0252 | 0.0474 | –0.0005 | 5.2692 | 5.2457 | 1.0149 |

| Merafe Resources | 29.4521 | –4.0030 | 0.0611 | 0.0073 | 5.6407 | 5.8777 | 0.9300 |

| Post-Crisis (from January 2010–July 2014) Parameter Estimates | |||||||

| NIG | t-Dist. | Skew t | |||||

| S & P 500 | 70.5049 | –13.0538 | 0.0070 | 0.0017 | 2.9116 | 2.9563 | 0.9094 |

| FTSE/JSE TOP40 | 122.4542 | –13.7630 | 0.0132 | 0.0020 | 5.6707 | 5.7635 | 0.9264 |

| Standard Bank | 128.9099 | –7.2170 | 0.0251 | 0.0017 | 8.8356 | 4.0000 | 1.0000 |

| African Bank | 34.4911 | –7.7071 | 0.0175 | 0.0026 | 3.3022 | 3.3084 | 0.8747 |

| Anglo American | 123.3751 | 11.4136 | 0.0420 | –0.0040 | 12.8391 | 13.2898 | 1.0454 |

| Merafe Resources | 72.0322 | 11.2690 | 0.0558 | -0.0088 | 10.1389 | 8.8798 | 1.2196 |

| Parameter Estimates for the Period January 1991–July 2014 | ||||||||

| Kolmogorov-Smirnov | Critical Value | |||||||

| NIG | t-Dist. | Skew t | Normal | |||||

| S & P 500 | 0.0058 | 0.0135 | 0.0113 | 0.0875 | 0.0156 | 0.0173 | 0.0188 | 0.0207 |

| FTSE/JSE TOP40 | 0.0081 | 0.0082 | 0.0046 | 0.0580 | 0.0177 | 0.0197 | 0.0214 | 0.0236 |

| Standard Bank | 0.0201 | 0.0190 | 0.0184 | 0.0560 | 0.0191 | 0.0212 | 0.0231 | 0.0255 |

| African Bank | 0.0173 | 0.0150 | 0.0149 | 0.0657 | 0.0195 | 0.0216 | 0.0236 | 0.0259 |

| Anglo American | 0.0114 | 0.0101 | 0.0088 | 0.0443 | 0.0190 | 0.0211 | 0.0229 | 0.0252 |

| Merafe Resources | 0.0809 | 0.0862 | 0.0828 | 0.0765 | 0.0232 | 0.0257 | 0.0280 | 0.0308 |

| Pre-Crisis (from January 1991–December 2007) Parameter Estimates | ||||||||

| Kolmogorov-Smirnov | Critical Value | |||||||

| NIG | t-Dist. | Skew t | Normal | |||||

| S & P 500 | 0.0117 | 0.0187 | 0.0163 | 0.0626 | 0.0187 | 0.0208 | 0.0227 | 0.0249 |

| FTSE/JSE TOP40 | 0.0116 | 0.0103 | 0.0092 | 0.0535 | 0.0219 | 0.0243 | 0.0265 | 0.0291 |

| Standard Bank | 0.1934 | 0.0288 | 0.0272 | 0.0546 | 0.0247 | 0.0274 | 0.0298 | 0.0328 |

| African Bank | 0.0245 | 0.0247 | 0.0224 | 0.0641 | 0.0253 | 0.0281 | 0.0306 | 0.0337 |

| Anglo American | 0.0112 | 0.0104 | 0.0105 | 0.0349 | 0.0244 | 0.0271 | 0.0295 | 0.0324 |

| Merafe Resources | 0.0885 | 0.0994 | 0.0968 | 0.0982 | 0.0318 | 0.0352 | 0.0384 | 0.0422 |

| Crisis Period (from January 2008–December 2009) Parameter Estimates | ||||||||

| Kolmogorov-Smirnov | Critical Value | |||||||

| NIG | t-Dist. | Skew t | Normal | |||||

| S & P 500 | 0.0278 | 0.0369 | 0.0288 | 0.0860 | 0.0545 | 0.0604 | 0.0659 | 0.0724 |

| FTSE/JSE TOP40 | 0.0162 | 0.0177 | 0.0181 | 0.0410 | 0.0547 | 0.0607 | 0.0661 | 0.0727 |

| Standard Bank | 0.0235 | 0.0285 | 0.0287 | 0.0618 | 0.0553 | 0.0614 | 0.0669 | 0.0735 |

| African Bank | 0.0261 | 0.0297 | 0.0237 | 0.0279 | 0.0552 | 0.0613 | 0.0668 | 0.0735 |

| Anglo American | 0.0322 | 0.0342 | 0.0336 | 0.0676 | 0.0548 | 0.0608 | 0.0663 | 0.0729 |

| Merafe Resources | 0.0596 | 0.0557 | 0.0606 | 0.0594 | 0.0573 | 0.0635 | 0.0692 | 0.0761 |

| Post-Crisis (from January 2010–July 2014) Parameter Estimates | ||||||||

| Kolmogorov-Smirnov | Critical Value | |||||||

| NIG | t-Dist. | Skew t | Normal | |||||

| S & P 500 | 0.0160 | 0.0212 | 0.0165 | 0.1066 | 0.0327 | 0.0363 | 0.0395 | 0.0435 |

| FTSE/JSE TOP40 | 0.0135 | 0.0166 | 0.0171 | 0.0504 | 0.0362 | 0.0401 | 0.0437 | 0.0481 |

| Standard Bank | 0.0175 | 0.0160 | 0.0254 | 0.0293 | 0.0363 | 0.0403 | 0.0439 | 0.0483 |

| African Bank | 0.0279 | 0.0236 | 0.0152 | 0.0942 | 0.0367 | 0.0407 | 0.0443 | 0.0487 |

| Anglo American | 0.0150 | 0.0138 | 0.0142 | 0.0266 | 0.0362 | 0.0402 | 0.0438 | 0.0481 |

| Merafe Resources | 0.0945 | 0.0932 | 0.1072 | 0.0899 | 0.0416 | 0.0462 | 0.0504 | 0.0554 |

4. Value-at-Risk

4.1. Value-at-Risk Estimates

4.2. Backtesting the Model

| VaR Estimates over the Period January 1991–July 2014 | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 3.15% | 3.31% | 3.04% | 3.45% | 2.68% |

| FTSE/JSE TOP 40 | 3.79% | 3.75% | 3.56% | 3.84% | 3.11% |

| Standard Bank | 5.81% | 5.81% | 5.65% | 5.86% | 4.87% |

| African Bank | 7.35% | 7.53% | 7.73% | 7.54% | 6.37% |

| Anglo American | 6.60% | 6.38% | 6.73% | 6.46% | 5.97% |

| Merafe Resources | 9.02% | 8.98% | 9.36% | 8.13% | 8.36% |

| Pre-Crisis (from January 1991–December 2007) VaR Estimates | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 2.6213% | 2.8307% | 2.5053% | 2.8592% | 2.3426% |

| FTSE/JSE TOP40 | 3.7136% | 3.5412% | 3.5011% | 3.6038% | 2.9309% |

| Standard Bank | 6.4264% | 6.1871% | 6.0822% | 6.2585% | 5.2607% |

| African Bank | 7.6811% | 8.2170% | 7.9237% | 7.7267% | 7.0160% |

| Anglo American | 6.1856% | 6.2482% | 6.0138% | 5.9658% | 5.5577% |

| Merafe Resources | 8.0043% | 8.3464% | 9.2559% | 7.9108% | 8.3902% |

| Crisis Period (from January 2008–December 2009) VaR Estimates | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 6.2799% | 7.2567% | 6.3789% | 8.4283% | 5.1633% |

| FTSE/JSE TOP40 | 5.3725% | 5.6579% | 5.4216% | 5.5736% | 4.8682% |

| Standard Bank | 6.5636% | 6.6214% | 6.9057% | 6.3490% | 6.1787% |

| African Bank | 6.8522% | 7.2559% | 7.6928% | 7.2836% | 6.9659% |

| Anglo American | 9.9742% | 10.5935% | 10.9597% | 10.1201% | 9.4863% |

| Merafe Resources | 13.5510% | 12.4084% | 11.6611% | 12.8104% | 10.9410% |

| Post-Crisis (from January 2010–July 2014) VaR Estimates | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 2.8858% | 2.8198% | 2.9767% | 3.2944% | 2.5355% |

| FTSE/JSE TOP40 | 2.8897% | 2.7751% | 2.8675% | 2.8675% | 2.3807% |

| Standard Bank | 3.6093% | 3.6265% | 3.3549% | 4.1969% | 3.1541% |

| African Bank | 6.8760% | 7.7128% | 6.5781% | 7.1226% | 6.1529% |

| Anglo American | 4.3435% | 4.4079% | 4.5477% | 4.4322% | 4.2903% |

| Merafe Resources | 6.4198% | 6.6560% | 7.0918% | 6.3123% | 6.3751% |

| Estimates of One-Day Expected Shortfall. | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| FTSE/JSE TOP 40 | |||||

| S & P 500 | |||||

| Standard Bank | |||||

| African Bank | |||||

| Anglo American | |||||

| Merafe Resources | |||||

| Pre-crisis (from January 1991–December 2007) Expected Shortfall Estimates. | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 3.47% | 3.64% | 3.39% | 4.19% | 2.67% |

| FTSE/JSE TOP40 | 5.21% | 4.57% | 4.85% | 4.94% | 3.39% |

| Standard Bank | 8.76% | 7.99% | 8.20% | 8.25% | 5.99% |

| African Bank | 11.35% | 10.28% | 11.17% | 10.22% | 8.01% |

| Anglo American | 7.96% | 7.79% | 8.04% | 7.44% | 6.35% |

| Merafe Resources | 9.77% | 10.01% | 11.37% | 9.51% | 9.67% |

| Crisis Period (from January 2008–December 2009) Expected Shortfall Estimates. | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 8.20% | 9.49% | 11.42% | 21.09% | 5.88% |

| FTSE/JSE TOP40 | 6.58% | 6.80% | 7.06% | 7.26% | 5.49% |

| Standard Bank | 7.96% | 8.20% | 8.94% | 8.20% | 7.11% |

| African Bank | 8.86% | 8.47% | 8.99% | 8.51% | 7.95% |

| Anglo American | 14.01% | 13.35% | 14.02% | 13.44% | 10.78% |

| Merafe Resources | 17.44% | 15.43% | 14.84% | 16.01% | 12.50% |

| Post-Crisis (from January 2010–July 2014) Expected Shortfall Estimates. | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 4.74% | 3.91% | 4.72% | 5.17% | 2.90% |

| FTSE/JSE TOP40 | 3.29% | 3.69% | 3.62% | 3.69% | 2.71% |

| Standard Bank | 4.37% | 4.37% | 4.06% | 6.01% | 3.64% |

| African Bank | 12.55% | 10.28% | 9.82% | 10.50% | 7.06% |

| Anglo American | 4.95% | 5.08% | 5.53% | 5.13% | 4.93% |

| Merafe Resources | 9.10% | 8.00% | 8.61% | 7.78% | 7.43% |

| Zone | Number of Violations | Scaling Violations |

|---|---|---|

| Green | 0 to 4 | 3 |

| Yellow | 5 | |

| 6 | ||

| 7 | ||

| 8 | ||

| 9 | ||

| Red | 10 or more | 4 |

| Backtesting Results for 99% Daily-VaR over the Most Recent 250 Days of Our Data. | ||||||

|---|---|---|---|---|---|---|

| Historical | NIG | Skew t | t-Dist. | Normal | ||

| Standard Bank | No. of ex | 0 | 0 | 0 | 0 | 0 |

| Zone | Green | Green | Green | Green | Green | |

| African Bank | No. of ex | 6 | 6 | 6 | 6 | 11 |

| Zone | Yellow | Yellow | Yellow | Yellow | Red | |

| Anglo American | No. of ex | 0 | 0 | 0 | 0 | 0 |

| Zone | Green | Green | Green | Green | Green | |

| Merafe Resource | No. of ex | 0 | 0 | 0 | 0 | 0 |

| Zone | Green | Green | Green | Green | Green | |

| FTSE/JSE Top40 | No. of ex | 0 | 0 | 0 | 0 | 0 |

| Zone | Green | Green | Green | Green | Green | |

| S & P 500 | No. of ex | 1 | 1 | 1 | 1 | 1 |

| Zone | Green | Green | Green | Green | Green | |

| Number of Violations for 99% Daily-VaR. | ||||||

| Historical | NIG | t-Dist. | Skew t | Normal | Expected Violations | |

| S & P 500 | 63 | 54 | 72 | 51 | 102 | 62 |

| FTSE/JSE TOP 40 | 49 | 51 | 56 | 43 | 98 | 48 |

| Standard Bank | 41 | 41 | 46 | 39 | 72 | 41 |

| African Bank | 40 | 37 | 37 | 37 | 60 | 39 |

| Anglo American | 42 | 48 | 38 | 45 | 63 | 42 |

| Merafe Resources | 28 | 30 | 25 | 36 | 34 | 28 |

| Pre-Crisis (from January 1991–December 2007) Number of Violations. | ||||||

| Historical | NIG | t-Dist. | Skew t | Normal | Expected Violations | |

| S & P 500 | 43 | 32 | 56 | 30 | 74 | 43 |

| FTSE/JSE TOP40 | 32 | 35 | 36 | 34 | 63 | 31 |

| Standard Bank | 25 | 27 | 28 | 27 | 45 | 25 |

| African Bank | 24 | 17 | 22 | 24 | 29 | 23 |

| Anglo American | 26 | 24 | 28 | 28 | 37 | 25 |

| Merafe Resources | 17 | 13 | 8 | 18 | 13 | 15 |

| Crisis Period (from January 2008–December 2009) Number of Violations. | ||||||

| Historical | NIG | t-Dist. | Skew t | Normal | Expected Violations | |

| S & P 500 | 6 | 4 | 5 | 3 | 11 | 5 |

| FTSE/JSE TOP40 | 6 | 5 | 5 | 5 | 9 | 5 |

| Standard Bank | 5 | 5 | 4 | 6 | 7 | 5 |

| African Bank | 5 | 5 | 4 | 4 | 5 | 5 |

| Anglo American | 5 | 4 | 4 | 5 | 7 | 5 |

| Merafe Resources | 5 | 8 | 9 | 7 | 9 | 5 |

| Post-Crisis (from January 2010–July 2014) Number of Violations. | ||||||

| Historical | NIG | t-Dist. | Skew t | Normal | Expected Violations | |

| S & P 500 | 15 | 17 | 13 | 8 | 20 | 14 |

| FTSE/JSE TOP40 | 12 | 15 | 12 | 12 | 26 | 11 |

| Standard Bank | 12 | 12 | 17 | 5 | 23 | 11 |

| African Bank | 12 | 9 | 14 | 10 | 17 | 11 |

| Anglo American | 12 | 10 | 8 | 10 | 12 | 11 |

| Merafe Resources | 9 | 8 | 7 | 9 | 9 | 9 |

| Kupiec LR Test Statistic. | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 0.0275 | 1.0133 | 1.6484 | 1.9920 | 22.2150 |

| FTSE/JSE TOP 40 | 0.0355 | 0.2255 | 1.3817 | 0.4838 | 41.0648 |

| Standard Bank | 0.0002 | 0.0002 | 0.6175 | 0.0906 | 19.4767 |

| African Bank | 0.0080 | 0.1557 | 0.1557 | 0.1557 | 9.3361 |

| Anglo American | 0.0035 | 0.9414 | 0.3276 | 0.2701 | 9.5849 |

| Merafe Resources | 0.0001 | 0.1325 | 0.3499 | 2.0832 | 1.1898 |

| Pre-Crisis (from January 1991–December 2007) Kupiec LR Test Statistic. | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 0.0034 | 2.9251 | 3.8616 | 4.2101 | 19.1317 |

| FTSE/JSE TOP40 | 0.0185 | 0.4400 | 0.6983 | 0.2394 | 25.1881 |

| Standard Bank | 0.0056 | 0.2234 | 0.4461 | 0.2234 | 13.6734 |

| African Bank | 0.0165 | 1.9429 | 0.0839 | 0.0165 | 1.2677 |

| Anglo American | 0.0254 | 0.0586 | 0.3033 | 0.3033 | 4.8774 |

| Merafe Resources | 0.3004 | 0.2430 | 3.8349 | 0.6321 | 0.2430 |

| Crisis Period (from January 2008–December 2009) Kupiec LR Test Statistic. | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 0.1703 | 0.2375 | 0.0005 | 0.9837 | 5.2982 |

| FTSE/JSE TOP40 | 0.1859 | 0.0000 | 0.0000 | 0.0000 | 2.5964 |

| Standard Bank | 0.0020 | 0.0020 | 0.1781 | 0.2328 | 0.8026 |

| African Bank | 0.0017 | 0.0017 | 0.1819 | 0.1819 | 0.0017 |

| Anglo American | 0.0000 | 0.2129 | 0.2129 | 0.0000 | 0.7268 |

| Merafe Resources | 0.0397 | 2.1249 | 3.3823 | 1.1226 | 3.3823 |

| Post-Crisis (from January 2010–July 2014) Kupiec LR Test Statistic. | |||||

| Historical | NIG | t-Dist. | Skew t | Normal | |

| S & P 500 | 0.0662 | 0.5949 | 0.0783 | 3.0980 | 2.2671 |

| FTSE/JSE TOP40 | 0.0263 | 1.0129 | 0.0263 | 0.0263 | 13.7331 |

| Standard Bank | 0.0346 | 0.0346 | 2.4442 | 4.5606 | 9.2683 |

| African Bank | 0.0639 | 0.4483 | 0.6807 | 0.1241 | 2.6714 |

| Anglo American | 0.0283 | 0.1887 | 1.1616 | 0.1887 | 0.0283 |

| Merafe Resources | 0.0149 | 0.0491 | 0.3362 | 0.0149 | 0.0149 |

| Interval (Decreases) | The Likelihood of Decreases on the Given Interval Likely to Be Realised Once Every Number of Years for the Period Ending 31 July 2014 | ||||

|---|---|---|---|---|---|

| FTSE/JSE Top40 | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0084 | 0.0091 | 0.0091 | 0.0090 | 0.0084 |

| 2.5% to 5% | 0.1176 | 0.1267 | 0.1411 | 0.1564 | 0.1010 |

| 5% to 10% | 18.9286 | 38.2812 | 17.8197 | 24.2281 | 1.68E+07 |

| 10% to 15% | 18.9286 | 63.0238 | 14.3920 | 20.4024 | 7.44E+09 |

| 15% to 20% | - | 2.51E+03 | 76.3979 | 115.7666 | - |

| S & P 500 | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0109 | 0.0089 | 0.0089 | 0.0088 | 0.0081 |

| 2.5% to 5% | 0.1521 | 0.1905 | 0.2246 | 0.2507 | 0.2335 |

| 5% to 10% | 24.4841 | 37.6071 | 15.2851 | 17.7828 | 1.08E+11 |

| 10% to 15% | 24.4841 | 51.8338 | 10.0172 | 11.6906 | - |

| 15% to 20% | - | 1.30E+03 | 37.5097 | 4.39E+1 | - |

| Standard Bank | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0081 | 0.0100 | 0.0099 | 0.0100 | 0.0105 |

| 2.5% to 5% | 0.0434 | 0.0524 | 0.0543 | 0.0536 | 0.0335 |

| 5% to 10% | 2.7050 | 4.6775 | 4.3308 | 4.1112 | 136.4962 |

| 10% to 15% | 4.0575 | 5.3219 | 3.4828 | 3.2886 | 1.68E+03 |

| 15% to 20% | 8.1151 | 85.8005 | 18.8816 | 17.7106 | - |

| African Bank | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0080 | 0.0111 | 0.0110 | 0.0110 | 0.0125 |

| 2.5% to 5% | 0.0293 | 0.0387 | 0.0378 | 0.0381 | 0.0269 |

| 5% to 10% | 0.6260 | 1.4867 | 1.8286 | 1.7623 | 6.1621 |

| 10% to 15% | 1.0434 | 1.2498 | 1.3973 | 1.3133 | 25.6393 |

| 15% to 20% | 3.1302 | 10.2350 | 7.1777 | 6.4388 | 1.26E+05 |

| Anglo American | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0080 | 0.0107 | 0.0106 | 0.0107 | 0.0116 |

| 2.5% to 5% | 0.0341 | 0.0404 | 0.0405 | 0.0402 | 0.0283 |

| 5% to 10% | 1.2705 | 2.7994 | 2.8792 | 2.6915 | 16.2080 |

| 10% to 15% | 2.0645 | 3.0635 | 2.4844 | 2.2990 | 97.0204 |

| 15% to 20% | 5.5053 | 45.9263 | 15.7555 | 14.3929 | 2.41E+06 |

| Merafe Resources | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0079 | 0.0137 | 0.0132 | 0.0140 | 0.0157 |

| 2.5% to 5% | 0.0184 | 0.0265 | 0.0255 | 0.0272 | 0.0242 |

| 5% to 10% | 0.3840 | 0.8528 | 1.0562 | 0.7564 | 0.7074 |

| 10% to 15% | 0.5302 | 0.8699 | 1.0229 | 0.6556 | 1.1668 |

| 15% to 20% | 11.1349 | 12.3783 | 9.2258 | 5.0981 | 164.3330 |

| Interval (Decreases) | The Likelihood of Decreases on the Given Interval Likely to be Realised Once Every Number of Years for the Period Ending 31 July 2014, Using Half the Original Data. | ||||

|---|---|---|---|---|---|

| FTSE/JSE Top40 | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0086 | 0.0088 | 0.0087 | 0.0087 | 0.0083 |

| 2.5% to 5% | 0.0977 | 0.1423 | 0.1769 | 0.1664 | 0.1221 |

| 5% to 10% | - | 65.4568 | 29.6196 | 26.6067 | 1.16E+8 |

| 10% to 15% | - | 122.7782 | 25.0948 | 22.3691 | 9.14E+10 |

| 15% to 20% | - | 6.90E+03 | 143.3808 | 126.2540 | - |

| S & P 500 | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0112 | 0.0086 | 0.0085 | 0.0085 | 0.0079 |

| 2.5% to 5% | 0.1262 | 0.2335 | 0.2824 | 0.2927 | 0.3526 |

| 5% to 10% | - | 148.6019 | 55.9240 | 58.3445 | - |

| 10% to 15% | - | 301.0705 | 47.8661 | 4.99E+01 | - |

| 15% to 20% | - | 2.07E+04 | 276.4179 | 2.88E+02 | - |

| Standard Bank | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0080 | 0.0106 | 0.0104 | 0.0105 | 0.0111 |

| 2.5% to 5% | 0.0511 | 0.0460 | 0.0476 | 0.0473 | 0.0293 |

| 5% to 10% | 8.1230 | 3.1012 | 3.4007 | 2.9952 | 30.1740 |

| 10% to 15% | 8.1230 | 3.2491 | 2.7744 | 2.3480 | 226.2969 |

| 15% to 20% | - | 43.5798 | 15.6583 | 12.3680 | - |

| African Bank | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0080 | 0.0116 | 0.0114 | 0.0117 | 0.0135 |

| 2.5% to 5% | 0.0303 | 0.0362 | 0.0361 | 0.0355 | 0.0247 |

| 5% to 10% | 0.7825 | 1.2700 | 1.5678 | 1.3555 | 2.1725 |

| 10% to 15% | 1.9563 | 1.0481 | 1.1645 | 0.9859 | 6.0698 |

| 15% to 20% | 2.6085 | 8.2802 | 5.6955 | 4.7072 | 5.88E+03 |

| Anglo American | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0079 | 0.0108 | 0.0106 | 0.0108 | 0.0113 |

| 2.5% to 5% | 0.0336 | 0.0402 | 0.0414 | 0.0400 | 0.0287 |

| 5% to 10% | 0.9175 | 3.7993 | 4.1050 | 3.4787 | 23.3041 |

| 10% to 15% | 1.6516 | 4.8608 | 4.0876 | 3.3942 | 159.6729 |

| 15% to 20% | 4.1290 | 107.7421 | 34.2507 | 27.6963 | 7.42E+06 |

| Merafe Resources | Observed | NIG | Skew t | t-Dist. | Normal |

| 0 to 2.5% | 0.0079 | 0.0146 | 0.0140 | 0.0152 | 0.0161 |

| 2.5% to 5% | 0.0199 | 0.0238 | 0.0228 | 0.0261 | 0.0239 |

| 5% to 10% | 0.3095 | 0.9944 | 1.1995 | 0.6216 | 0.5675 |

| 10% to 15% | 0.3980 | 1.4715 | 1.5565 | 0.5916 | 0.8433 |

| 15% to 20% | 5.5714 | 65.5644 | 29.7320 | 6.5581 | 84.4776 |

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- RiskMetrics. Technical Report, 4th ed. New York, NY, USA: J.P. Morgan/Reuters, 1996. [Google Scholar]

- P. Jorion. Value at Risk: The New Benchmark for Measuring Financial Risk, 2nd ed. New York, NY, USA: McGraw-Hill, 2001. [Google Scholar]

- Basel Committee on Bank Supervision. Amendment to the Capital Accord to Incorporate Market Risks. Basel, Switzerland, 1996. [Google Scholar]

- J. Hull. Risk Management and Financial Institutions, 2nd ed. Upper Saddle River, NJ, USA: Pearson Education, 2010. [Google Scholar]

- A.J. McNeil, P. Embrechts, and R. Frey. Quantitative Risk Management: Concepts, Techniques and Tools. Princeton, NJ, USA: Princeton University Press, 2005. [Google Scholar]

- B. Mandelbrot. “The variation of certain speculative prices.” J. Bus. 36 (1963): 394–419. [Google Scholar] [CrossRef]

- F.E. Fama. “THe Behavior of Stock-Market Prices.” J. Bus. 38 (1965): 34–105. [Google Scholar] [CrossRef]

- C. Alexander. Market Risk Analysis Value-at-Risk Models. Volume IV, Hoboken, NJ, USA: John Wiley & Sons Ltd, England, 2008. [Google Scholar]

- T.H. Rydberg. “Realistic Statistical Modelling of Financial Data.” Int. Stat. Rev. 68 (2000): 233–258. [Google Scholar] [CrossRef]

- R. Huisman, K. Koedijk, and R. Pownall. “VaR-x: Fat tails in financial risk management.” J. Risk 1 (1998): 47–60. [Google Scholar]

- C. Milwidsky, and E. Maré. “Value-at-Risk in the South African Equity Market: A view from the tails.” SAJEMS NS 13 (2010): 345–361. [Google Scholar]

- A.J. McNeil, and R. Frey. “Estimation of tail-related risk measures for heteroscedastic finance time series: An extreme value approach.” J. Empir. Financ. 7 (2000): 271–300. [Google Scholar] [CrossRef]

- E. Platen, and R. Rendek. “Empirical Evidence on Student-t Log-Returns of Diversified World Stock Indices.” J. Stat. Theory Pract. 2 (2008): 233–251. [Google Scholar] [CrossRef]

- B.E. Hansen. “Autoregressive conditional density estimation.” Int. Econ. Rev. 35 (1994): 705–730. [Google Scholar] [CrossRef]

- A. Azzalini, and A. Capitanio. “Distributions generated by pertubation of symmetry with emphasis on a multivariate skew t distribution.” J. R. Stat. Soc. 65 (2003): 367–389. [Google Scholar] [CrossRef]

- K. Aas, and D.H. Haff. “The generalised hyperbolic skew Student’s t-distribution.” J. Financ. Econ. 4 (2006): 275–309. [Google Scholar]

- C.M. Jones, and M.J. Faddy. “A skew extension of the t-distribution, with applications.” J. R. Stat. Soc. 65 (2003): 159–174. [Google Scholar] [CrossRef]

- F. Longin. “The choice of the distribution of asset returns: How extreme value theory can help? ” J. Bank. Financ. 29 (2005): 1017–1035. [Google Scholar] [CrossRef]

- J. Danielsson, and C.G. de Vries. “Value-at-risk and extreme returns.” Ann. Econ. Stat. 60 (2000): 239–270. [Google Scholar]

- P. Embrechts, C. Klüppelberg, and T. Mikosch. Modelling Extremal Events for Insurance and Finance. Berlin/Heidelberg, Germany: Springer, 1997. [Google Scholar]

- R. Gençay, F. Selçuk, and A. Ulugülyağci. “High volatility, thick tails and extreme value theory in value-at-risk estimation.” Insur. Math. Econ. 33 (2003): 337–356. [Google Scholar] [CrossRef]

- C. Wentzel, and E. Maré. “Extreme value theory—An application to the South African Equity Market.” Invest. Anal. J. 66 (2007): 73–77. [Google Scholar]

- M. Bhattachariya, and S. Madhav. “A Comparison of VaR Estimation Procedures for Leptokurtic Equity Index Returns.” J. Math. Financ. 3 (2012): 13–30. [Google Scholar] [CrossRef]

- J. Schaumburg. “Predicting extreme value at risk: Nonparametric quantile-regression with refinements from extreme value theory.” Comput. Stat. Data Anal. 56 (2012): 4081–4096. [Google Scholar] [CrossRef]

- K. Kuester, S. Mittnik, and M.S. Paolella. “Value-at-Risk Prediction: A Comparison of Alternative Strategies.” J. Financ. Econo. 4 (2006): 53–89. [Google Scholar] [CrossRef]

- E. Bølviken, and F.E. Benth. “Quantification of risk in Norwegian stocks via the Normal Inverse Gaussian Distribution.” In Proceedings of the 10th AFIR Colloquium, Tromso, Norway; 2000, pp. 87–98. [Google Scholar]

- C.K. Huang, K. Chinhamu, C.-S. Huang, and J. Hammujuddy. “Generalized Hyperbolic Distributions and Value-at-Risk Estimation for The South African Mining Index.” Int. Bus. Econ. Res. J. 13 (2014): 320–328. [Google Scholar]

- J. Lillestøl. “Risk analysis and the NIG distribution.” J. Risk 2 (2000): 41–56. [Google Scholar]

- K. Prause. “The Generalized Hyperbolic Model: Estimation, Financial Derivatives, and Risk Measures.” PhD Thesis, University of Freiburg, 1999. [Google Scholar]

- O.E. Barndorff-Nielsen. “Normal Inverse Gaussian Processes and the Modelling of Stock Returns.” Res. Rep. 300, Department of Theoretical Statistics, Aarhus University, 1995. [Google Scholar]

- J.H. Venter, and P.J. de Jongh. “Risk estimation using the normal inverse Gaussian distribution.” J. Risk 4 (2001): 1–24. [Google Scholar]

- C. Capital. “Jse Top 40 shares.” Available online: www.courtneycapital.co.za/jse-top-40-shares/ (accessed on 12 February 2014).

- O.E. Barndorff-Nielsen. “Normal Inverse Gaussian Distributions and Stochastic Volatility Modelling.” Board Found. Scand. J. Stat. 24 (1997): 1–13. [Google Scholar] [CrossRef]

- R.C. Blattberg, and N.J. Gonedes. “A Comparison of the Stable and Student Distribution as Statistical Models for Stock Prices.” J. Bus. 47 (1974): 244–280. [Google Scholar] [CrossRef]

- D. Wuertz, and et al. THE fBasics Package: Rmetrics–Markets and Basic Statistics. 1996-2006. [Google Scholar]

- Basel Committe on Bank Supervision. Supervisory Framework for the Use of “Backtesting” in Conjunction with the Internal Models Approach to Market Risk Capital Requirements. Basel, Switzerland, 1996. [Google Scholar]

- P.H. Kupiec. “Techniques for verifying the accuracy of risk measurement models.” J. Deriv. 3 (1995): 73–84. [Google Scholar] [CrossRef]

- 1Also referred to as percentile.

- 2The Basel Committee imposing minimum capital requirements for market risk in the “1996 Amendment" [3].

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mabitsela, L.; Maré, E.; Kufakunesu, R. Quantification of VaR: A Note on VaR Valuation in the South African Equity Market. J. Risk Financial Manag. 2015, 8, 103-126. https://doi.org/10.3390/jrfm8010103

Mabitsela L, Maré E, Kufakunesu R. Quantification of VaR: A Note on VaR Valuation in the South African Equity Market. Journal of Risk and Financial Management. 2015; 8(1):103-126. https://doi.org/10.3390/jrfm8010103

Chicago/Turabian StyleMabitsela, Lesedi, Eben Maré, and Rodwell Kufakunesu. 2015. "Quantification of VaR: A Note on VaR Valuation in the South African Equity Market" Journal of Risk and Financial Management 8, no. 1: 103-126. https://doi.org/10.3390/jrfm8010103

APA StyleMabitsela, L., Maré, E., & Kufakunesu, R. (2015). Quantification of VaR: A Note on VaR Valuation in the South African Equity Market. Journal of Risk and Financial Management, 8(1), 103-126. https://doi.org/10.3390/jrfm8010103