1. Introduction

While the day-ahead market is the dominating electricity market, trades in more short-term markets are receiving increasing attention. A main driver for this is the growing share of production from variable renewable sources (VRES) that is hard to predict day-ahead and thereby motivates postponed trades. It is also expected that relatively more VRES will increase the value of flexible production due to increased price variation. For a flexible hydropower producer, this might correspond to a new market opportunity, and raises the question of what added value trading in multiple short-term markets can give relative to day-ahead only.

In this paper, we aim to shed light on this opportunity taking a Norwegian hydropower producer’s perspective. The Norwegian power system is dominated by regulated hydropower production, with a total share of over 95% in 2016. This gives relatively small and non-volatile short-term markets in Norway, but expectations of increasing interconnection with Europe and a larger penetration of VRES is expected to increase the liquidity and price volatility. In this paper, we analyse the potential value-creation from trading in multiple energy markets given the current market structure in Norway, Sweden and Germany. The market data from Sweden and Germany are used as a proxy for the potential market development in Norway.

Literature Review

In line with the market development, a growing amount of literature extends from day-ahead modelling into multi-market modelling of hydropower. The marginal cost is the decision base for market trade, and the literature most commonly represents these costs implicitly in a scheduling problem or bidding problem. The former seeks an optimal production schedule and the latter seeks optimal market bids [

1]. The underlying modelling of the production system and market modelling is usually similar in the two model classes. Nonlinearities, non-convexities and inflow uncertainty, due to, amongst others, the binary spinning state of generators and the decision dependent water head effects, are main challenges in modelling of the production system. In market modelling, the price and quantity uncertainty and assumptions regarding market power are the main challenges.

Closely related to the question of added value from multi-market trade is the question of co-optimization (frequently denoted “coordinated bidding”, but we use co-optimization due to its relevance also for scheduling models) as opposed to sequential optimization. While the former assumes some knowledge of subsequent markets when trading in one market, the latter trades in each market as if it was the last trading option for the given time period. Theoretically, co-optimized trade is the preferred alternative providing the larger expected profit [

2] since all options are explicitly represented, but the added complexity in properly modelling the information structure in the markets might make sequential optimization reasonable. Boomsma et al. [

2] also show that only participating in the day-ahead market gives a lower bound to co-optimized trade where multiple subsequent energy markets are included. Co-optimization versus sequential optimization is reviewed and discussed in [

3], where the main focus is put on the energy markets, the day-ahead, intra-day and balancing markets.

Most literature on multi-market scheduling or bidding does not explicitly compare day-ahead bidding with or without further market consideration, but instead focuses on the usefulness of certain modelling features and how this affect the model results. An early example is Deng et al. [

4] who focus on stochastic programming when modelling co-optimized multi-market scheduling covering the day-ahead and ancillary services markets. A case study show increased expected value with stochastic programming relative to deterministic programming on simulated price and activation quantities. Vardanyan and Hesamzadeh [

5] provide a recent example, showing how bid curves are affected when including risk measures in co-optimized bidding in the day-ahead, intra-day and real-time markets.

A few studies have sought to quantify the added value of multi-market trading relative to day-ahead trade only for hydropower producers. Boomsma et al. [

2] develop a stochastic model for the day-ahead and balancing market including imbalance settlement. For Danish market data in 2010, they find added values in the range 9.6–30.8% for different months with a median at 16.5% with co-optimized trading. Similar analysis was done for sequential trading and the numbers are 1.2–19.8% with a median at 2.7%. In the same markets using Norwegian data from 2013–2014, also using a stochastic co-optimizing model, Fodstad et al. [

6] find values up to 1.1% for representative days in October. Braun [

7] builds a deterministic model for the German markets with a price-making pumped hydropower producer. He observes a doubling of profits when allowing intra-day trade on top of the day-ahead position in the first four months of 2015. Schillinger et al. [

8] assess the added value of participating in the Swiss primary reserve, secondary reserve and balancing markets in addition to day-ahead using data from 2011–2015. Assuming perfect foresight over a year, they report added values in the range 40–90% for a small inflexible plant and 50–130% for a large flexible plant when co-optimizing the trades.

Some publications do quantify the added value of co-optimized trading relative to sequential trading. Faria and Fleten [

9] present a case study for trading in the Norwegian day-ahead and intra-day markets, and find the added value to be less than 0.65%. Multiple papers have looked into co-optimized trading in the day-ahead and balancing markets. Klæboe [

10] observes a value of less than 0.1% for co-optimized trading. Boomsma et al. [

2] report values from the Danish market ranging from 4–25% depending on the time of year and the size of the deviation between price expectations in the two markets. Kongelf and Overrein [

11] model the day-ahead, primary reserve and balancing markets, and observes a value of 0.89–1.16% for co-optimized trading over sequential trading.

To summarize, the extent to which added values from participation in multiple markets is observed is varying, and still no clear conclusion can be drawn from literature. Not too surprisingly, taking into account that European market integration is not fully reached, the values differ in different countries and markets. In addition, there are substantial differences in the modelling choices that can cause these discrepancies.

This paper will add to the literature by presenting a study of the value of trades in multiple energy markets in different price areas and with different hydropower plant properties. We approach the question of valuing multi-market trade with a simplified model assuming perfect foresight that gives an upper bound to the achievable profit. This corresponds to the approach used in, amongst others, Ref. [

8] to assess added value of multi-market hydropower trading, Ref. [

12] to assess revenue potentials for energy storages and [

13] to assess the added value of hydraulic short-circuit operation of pumped-storage in day-ahead and reserve markets. Furthermore, we aim to analyse the different components contributing to the added value, to understand under what assumptions the values might be realizable. With this approach, we avoid complicating model features that increases the computational burden, complicates the input data preparation and result analysis, and possiblyreduces generalizability of the results. Based on this upper bound, a decision can be made on whether more comprehensive tools are worth developing.

2. Model Description

We use a linear optimization model to maximize the profits a price-taking hydropower producer can achieve from trading electric energy. The model has a one-year horizon with hourly time resolution and includes multiple markets. A full mathematical description of the model is given in

Appendix A.

We include three separate markets in our model: the day-ahead (DA), hourly intra-day (ID) and balancing market (BM). The prices and available volumes for trading in each market are represented by historically observed values. In DA, only a sale is possible, while, in ID and BM, the producer has an option to purchase electricity. In most areas, ID is a continuously traded bilateral market, but, for simplicity, we represent the ID market with one sale and one purchase price per hour. The prices are calculated as the weighted average price from the individual ID trades in each modelled area in each hour. We include an hourly trade limit in each market as an upper bound on the sale and purchases. The limits are set according to historically traded quantities in each market. For BM, the activated energy deliveries are used as limits instead of the capacities provided to the market, since these are the quantities that are remunerated by the BM price in NordPool.

The model focuses on the business side of the hydropower production and therefore has a simplified one-reservoir description of the physical production system. The production function is linear. This implies that the efficiency is constant and that neither head effects nor generator start/stop are represented. In line with the perfect foresight assumption, the inflow is known and follows a real historical inflow profile for a Norwegian reservoir. The end reservoir level is set equal to the initial reservoir level to ease the comparison between model runs. The simplified modelling of the production system makes it possible to guarantee that the global optimum is reached within a short computation time and that the observed differences are due to market characteristics. In this study, we have focused on relative differences between model runs given different market assumptions, which we believe limits the error introduced through the simplified modelling.

3. Data

We use real historical market data from 2015 to analyse the potential value-creation from multi-market trades relative to single-market trade. This is combined with a number of different assumptions with regards to the hydro reservoir and plant specifications for our power producer. The specifications for the production system is varied to show how different production size and flexibility characteristics affect the potential for realising the values in multi-market trades.

3.1. Market Data

The analysis covers the three energy markets—DA, ID, and BM—with data from the price areas NO5 (western Norway), SE3 (middle Sweden) and GE (Germany). The DA and ID markets are operated by NordPoolSpot (NO5, SE3) and EpexSpot (GE), while BM markets are operated by the respective TSOs. For ID only the continuously traded market with hourly deliveries is included. Data for all combinations of markets and price areas was used in the study, except BM in GE due to lack of available data. The motivation for including different price areas is to observe how the price patterns from systems with different production mixes affect the results. The Norwegian power system has mainly regulated hydropower, the Swedish system a combination of hydropower (mainly run-of-river), VRES and thermal, while the German system has a relatively larger share of VRES (approximately 45% of total installed electricity generation capacity in 2015). Due to the expectations of increasing market and system integration, as well as the increasing shares of VRES, Swedish and German market data can be seen as proxies for the future market for Norwegian hydropower producers.

Table 1 shows some descriptive statistics for prices and traded quantities calculated with the market data used in the study. The historically traded quantities (Quant.) are used as limits for the position that can be taken in each market. The coefficient of variation (Coeff. of var.) measures the variability relative to the mean value, while the availability is the percentage of the hours where the traded quantity was larger than zero. For BM, the quantities used is the quantities activated by the Transmission System Operator (TSO), as opposed to the capacities kept available by the supplier. In all areas, the DA quantity exceeds the production capacity for all of our modelled plants, and the same holds true for ID quantities in Germany. This means that these quantities will not limit the trades in our analysis and therefore statistics are not presented. Purchase in DA is not included in the model and therefore not presented in the table either. For GE, we did not have access to individual trades for ID, only a single market price. To avoid model results with large zero-profit trades within this market, the ID purchase price is set 0.01 €/MWh above the sale price.

As can be observed from

Table 1, the price levels in the three areas are on average such that NO5 has the lowest prices and GE the highest prices. Furthermore, BM has the largest spread both in NO5 and SE3, which is reasonable since the price by design is equal or higher than DA for sale and equal or lower than DA for purchase. The correlation between BM prices and other market prices within each area is also weaker than between DA and ID (numbers not shown). There are indications that the price variability is larger in SE3 and GE than in NO5, but this observation is not unambiguous. It could be noted that the BM sale price in SE3 is affected by an incident with very high prices in November due to multiple simultaneously unexpected events, and removing this from the data would have lowered the mean price to 265.25 €/MWh and the coefficient of variation to 0.83. The ordering of traded quantities follows the price ordering, with GE being by far the largest market and NO5 the smallest. The three areas differ particularly in the size of the ID market where GE has trade in all hours while NO5 has trade only one fifth of the hours. While BM is the second largest market in NO5 both in mean quantity and availability, the BM market is the smallest market in SE3.

3.2. Plant Data

We have included five different production systems (plants), in our analysis (see

Table 2 for an overview). All of these plants have no reservoir or only a single reservoir. The plant characteristics are constructed to observe how the multi-market values are affected by two dimensions characterizing the plants: the size and the flexibility. Size is determined by the combination of production capacity, storage capacity and yearly inflow. For the plants

Small,

Medium and

Large, these values have the same relative size. This implies that the three plants also have the same flexibility. Flexibility covers both the ability to choose production output and the volume of water that can be stored. Flexibility can be described by the two measures Full load hours (Full load hours = Yearly inflow/(Production capacity × Hours in the year)) and Degree of regulation (Degree of regulation = Reservoir size/Yearly inflow. This corresponds to the number of years needed to fill an empty reservoir). The plants

Run-of-river,

Small and

Regulated represent the flexibility-dimension in increasing order. They have equal production capacity but different reservoir size and yearly inflow. The plants

Small,

Medium and

Large have production capacities that are within the range of real Norwegian plants.

Run-of-river,

Small and

Regulated have a very low installed effect to make the price-taker assumption more reasonable, while inflows and reservoirs are scaled to match the flexibility properties of a typical real run-of-river plant and a real plant with large flexibility.

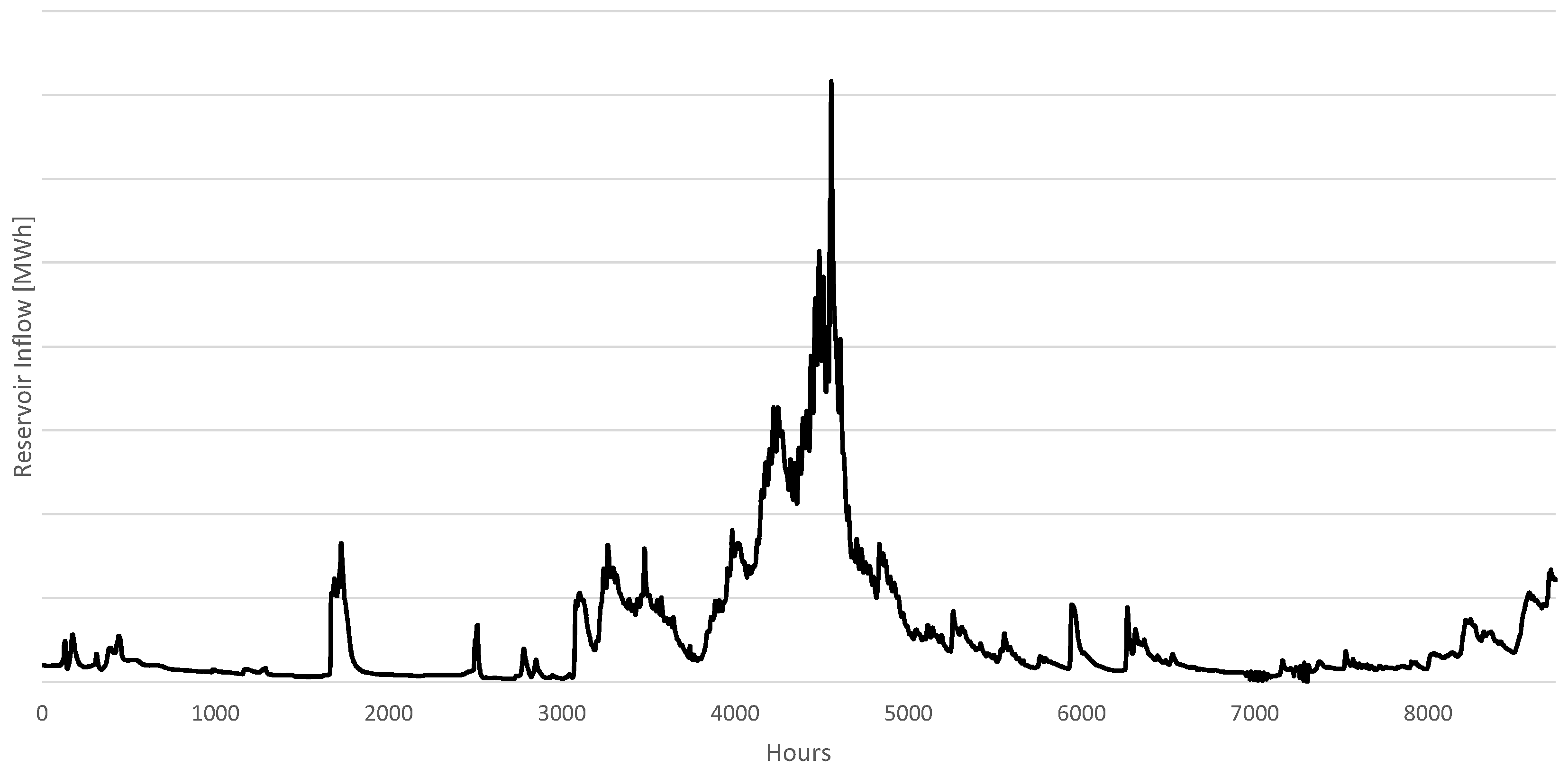

All plants have the same hourly profile for the inflow through the year, as presented in

Figure 1. The profile corresponds to the inflow profile of the catchment area Bjoreio within the NO5 area in 2015. Initial and end reservoir level is set at 70% of the capacity in all model runs, which corresponds to the average reservoir level in NO5 at entry of year 2015.

4. Test Set-Up

We run the model with a set of different assumptions that can be organized along three dimensions:

Plant,

Area, and

Market.

Plant and

Area refer to the different plant specifications and price areas presented in

Section 3.

Market describes which markets are included in the analyses. The combination of markets that we have included in our analyses is listed in

Table 3. All combinations of the dimensions are optimized, except market combinations with BM for GE. The benchmark that we compare our results with is a model run where only the DA market is included. The DA market is the dominating market at the moment and, as such, a natural benchmark for the value of including additional markets in the planning for a power producer. The following multi-market analyses will show what added values can be achieved on top of these benchmark values.

Additionally, Pure market trade model runs are conducted measuring the arbitrage potential in the market data. This is calculated as the profits from trading on the spread between purchase and sale price within the trade limits assuming a zero net position in each hour.

The linear model is implemented in Xpress Mosel 3.10 [

14] and solved with Xpress Optimizer 28.01 [

14]. A typical problem with all three markets included has 96 thousand variables, 105 thousand constraints and takes less than 2 s to solve on a laptop with Intel Core i7-3740QM @ 2.70 GHz.

5. Results and Discussion

In this section, we will present the main results from our analyses. We start by presenting the results for the benchmark, where only the DA-market is included. Next, we discuss liquidity in the markets and our price-taker assumption. We then move on to analyse the added value of participating in multiple markets, either as seller only or as both seller and buyer, and what drives these values. Lastly, we discuss how our modelling set-up affects the result interpretation and the possibility to draw conclusions from our study.

Appendix B provides tables summarizing the calculated market profits that form the basis for the result analysis.

5.1. DA Only—The Benchmark

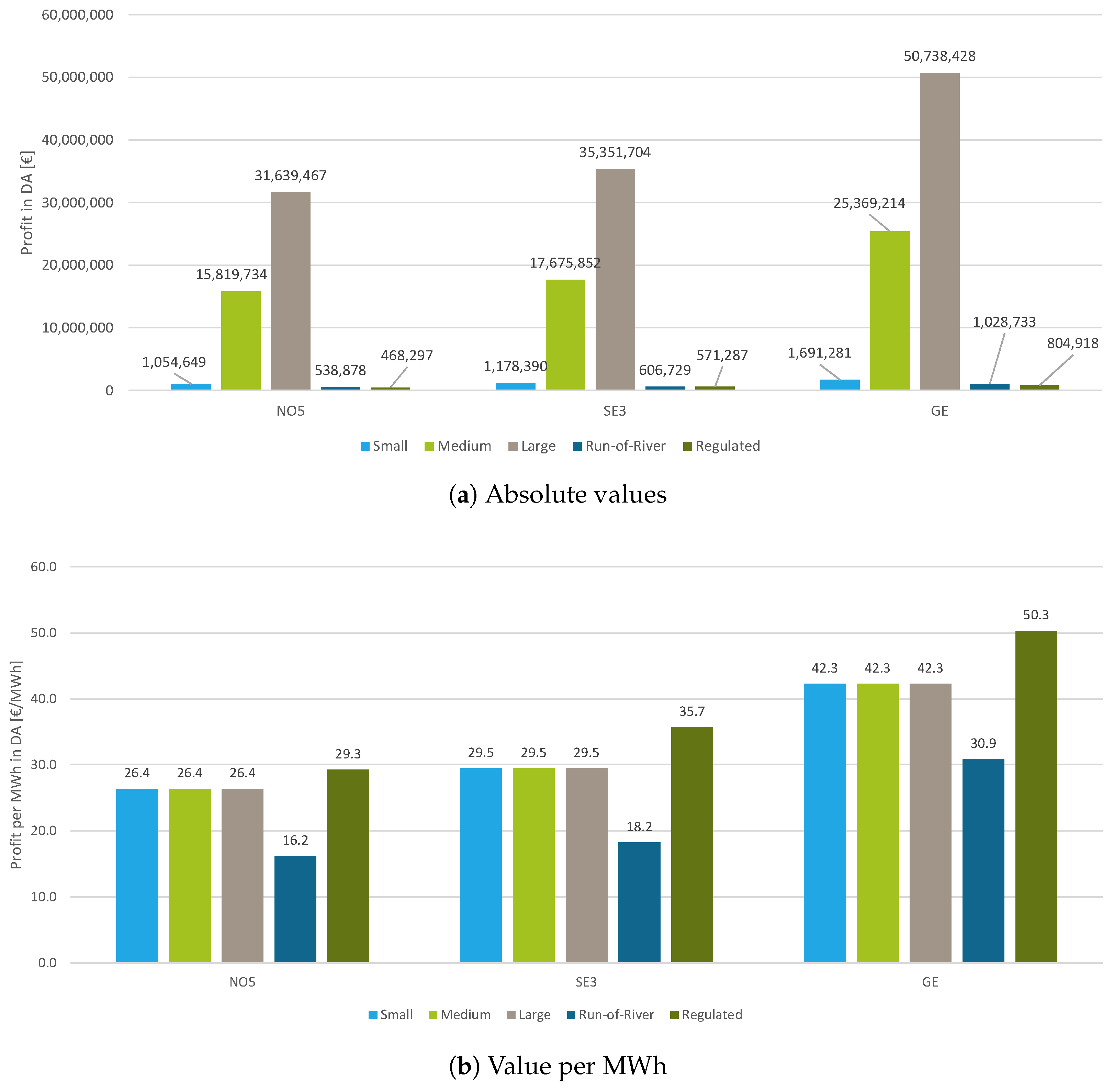

The value of optimally selling the available energy in the DA market is used as the benchmark for the analyses. Remember that also the DA only model runs have perfect foresight, which means that the benchmark is an upper bound to the real achievable value of the available energy, and thereby a tough benchmark to beat. In particular, the benchmark will, within the storage limitations, perfectly allocate the available energy over the year according to the DA price. Combined with the high correlation between prices in the markets, this means that the value of storage due to seasonal, weekly, and daily patterns are largely captured in the benchmark.

Figure 2 shows the benchmark values as total profit (upper) and average profit per MWh (lower). The on average higher price in GE and SE3 relative to NO5, as discussed in

Section 3.1, are clearly seen in the figure in terms of higher profits for the same plants. Furthermore, the figure shows some properties in the plant definitions. The three plants representing increasing sizes, i.e.,

Small,

Medium, and

Large, have increasing DA profits but equal profit per MWh. On the other hand, the three plants with increasing flexibility,

Run-of-River,

Small, and

Regulated exhibit increasing profits per MWh. The different benchmark values shown in

Figure 2 are used in the following when we refer to percentage added value relative to DA only. Since the benchmark values are different, this means that a direct comparison of percentages for different plants or areas will not be valid.

5.2. Market and Plant Size

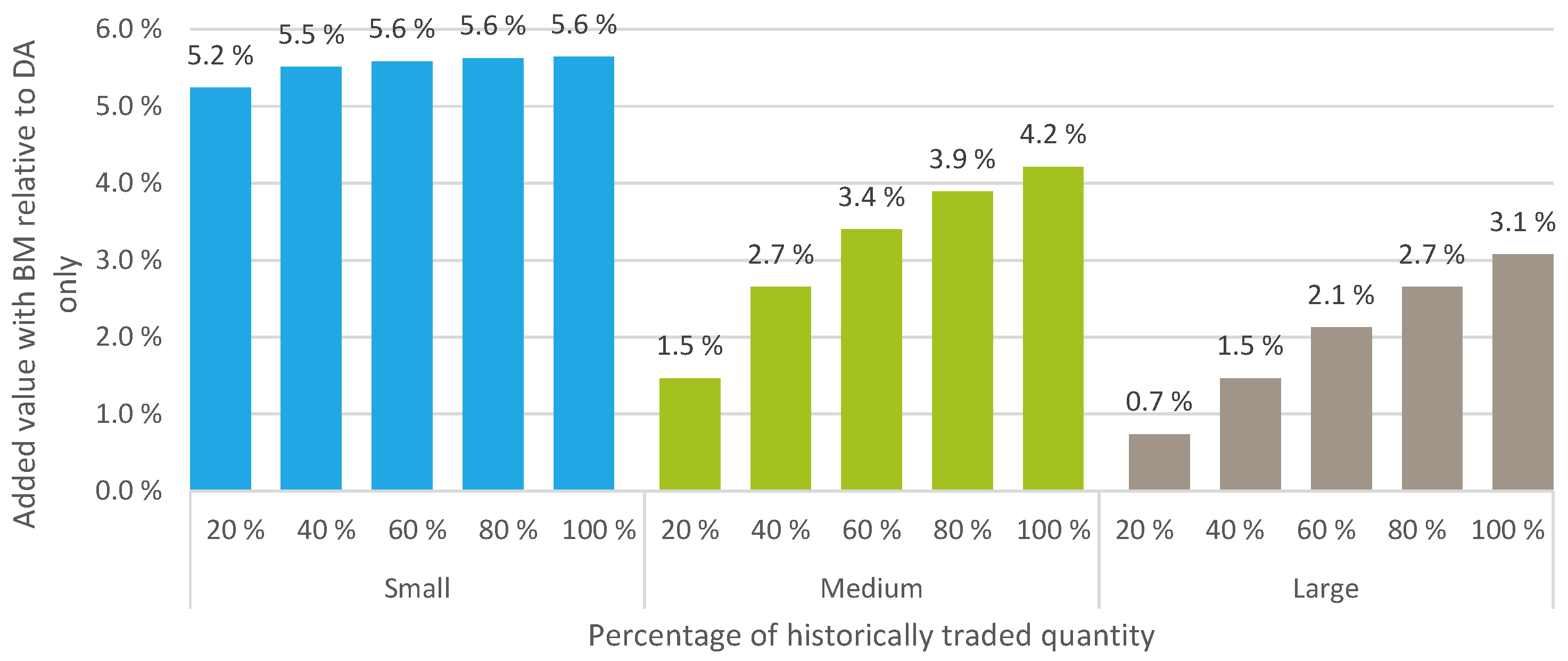

ID and BM are given trade limits in line with historically traded quantities. The motivation for including trade limits is the relatively small quantities that currently are traded in these markets.

Figure 3 show how the added value from allowing BM-sale in NO5 is reduced as these limits are reduced stepwise down to 20% of the historically traded quantities. The figure clearly shows that the plants

Medium and

Large have capacities that exceeds the BM upregulation quantities, while

Small is more robust towards the limits. The mean quantity and availability values from the market data given in

Table 1 indicate an even stronger sensitivity to trade limits for ID in NO5 and for BM in SE3, and somewhat weaker for ID in SE3, while DA and the German markets do not give trade limit sensitivity. These results show the same trend as those found by [

8] modelling the Swiss market, who observe that big and medium sized plants are largely affected by limitations in the market size. In addition, a small plant of 22 MW sees a revenue reduction of approximately 10% relative to the unlimited trade when market limits reaches 2.5% of the traded quantities.

From this, the price-taker assumption can clearly be criticized. A natural alternative would be to choose a price-maker assumption, so that large positions would be less profitable due to the price response, as done for instance in [

7]. Our reasons for not doing this is twofold: (1) the price-taker assumption makes the analyses independent of price-elasticity assumptions that are usually hard to quantify and (2) we prefer to not give the producer any incentives for strategically affecting the price. Our modelling choice is in line with the upper bound approach previously discussed. An alternative approach, as presented in [

11], could be to model the trade limits as stochastic parameters, but this would contradict the perfect foresight assumption of our study.

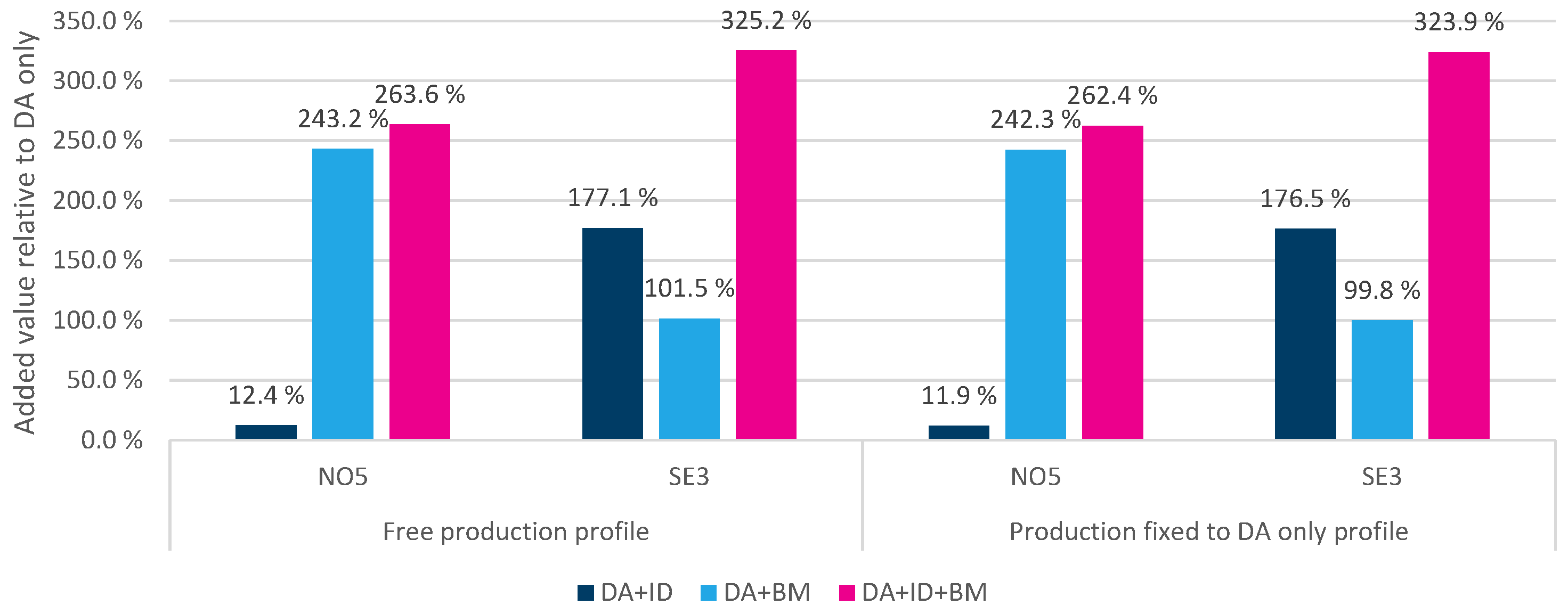

5.3. Sale in Multiple Markets

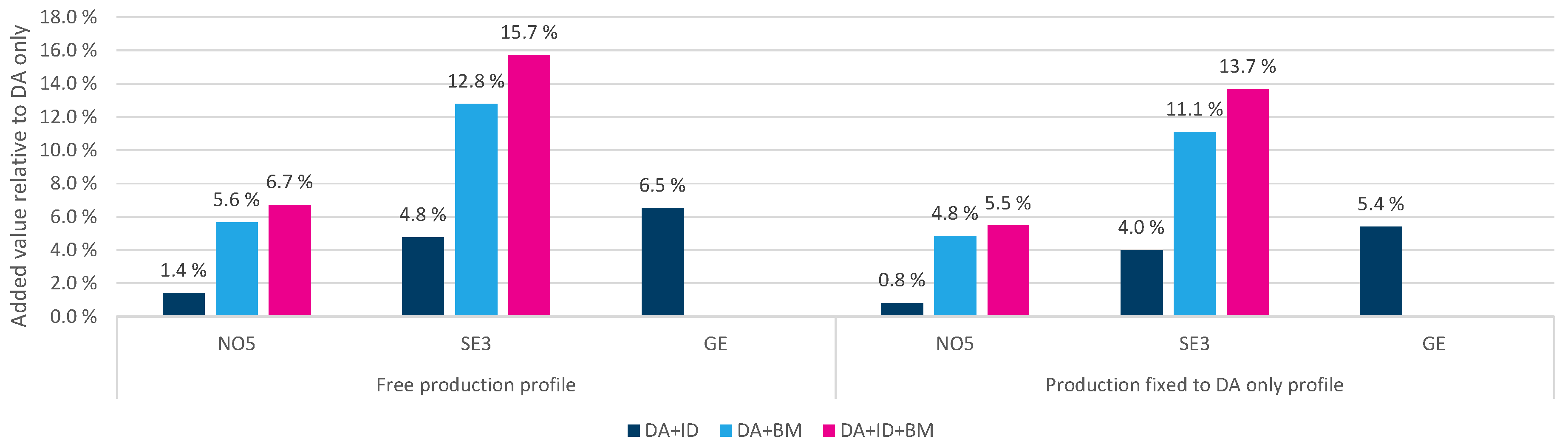

In this analysis, we give the producer the opportunity to sell power in multiple markets.

Figure 4 shows the relative added profits for the different case runs for the

Small plant. The numbers show the percentage increase with multi-market sale compared to the benchmark solution. As expected, the relative profits increase when we add additional markets. Each new market provides a new opportunity for trades without invalidating the benchmark solution. The results indicates a general increasing value of multi-market sale going from NO5 to SE3, and a further increase in GE for DA + ID. The result is strengthened by the fact that GE has 100% availability in the ID market and large traded quantities (more than 100 times the capacity of

Small in 96% of the hours). This implies that the observed value potential is not limited to small markets where market imperfections might challenge the validity of the observations.

The chart to the right in

Figure 4 shows the results when the production profile is fixed to the production profile from the DA only run (same hourly production throughout the year), while the chart to the left shows the results when the production profile is freely optimized in the multi-market analysis. As can be seen from the charts, the values in the right chart are only slightly below those to the left. This is mainly due to the strong correlation between the market prices. This has two implications: firstly, the producer do not need perfect foresight through a whole year to have the potential for a substantial multi-market sales value. Most of the potential added value requires only perfect foresight, or more realistically a good forecast for each market at the time of DA bidding, to be able to decide how much to offer in DA and how much to sell in subsequent markets. Secondly, a substantial part of the multi-market sales value can be achieved independent of the ability, and cost, related to within hour production changes.

Still, the results indicates that the properties of the plant do affect the multi-market sales value, as shown in

Figure 5. The figure shows the increase in average price obtained in the multi-market analysis in SE3 for the three plants with different flexibility characteristics. Remember that the reference price for these plants are varying, as shown in

Figure 2b, and also that the delivered quantity is different for the different plants. The results indicate that the trend from DA is strengthened when multiple markets are available. That is, the flexible plants see a larger price increase on the already higher average price from DA than the less flexible plants. This implies that the access to multiple markets has a larger value potential for producers who can control their production output by utilizing the reservoir than producers with intermittent production. These results match the observations [

8] do in their similar analysis using Swiss historical prices.

In the right-hand side of

Figure 5, the production profile is fixed according to the optimal profile for DA sale, while, on the left side, the production is freely optimized. Comparing the two sides of the figure gives similar observations as in

Figure 4. That is, most of the price increase potential is kept even when the production profile is fixed. The trend, though, is that the larger the flexibility in the plant, the more valuable it is to adapt the production profile.

Run-of-River represents an extreme case, since it, per design, does not have any ability to adapt the production, giving equal values on both sides of the figure.

Small reaches a smaller price increase than

Run-of-River in DA + ID when the production profile is fixed. This is because

Small sells a larger quantity, which gives a smaller average price, despite obtaining a larger added value in absolute terms than

Run-of-River.

5.4. Bidirectional Trade in Multiple Markets

The hydropower producers can, in addition to selling their production in the markets, also participate in the markets by purchasing power. This possibility provides the producers with additional flexibility in their production planning.

Figure 6 shows the resulting additional profits when we add purchase liquidity in the markets. As we can see from these numbers, the effect on profits is substantial—for SE3, the added value is more than three times the value of

Small in DA.

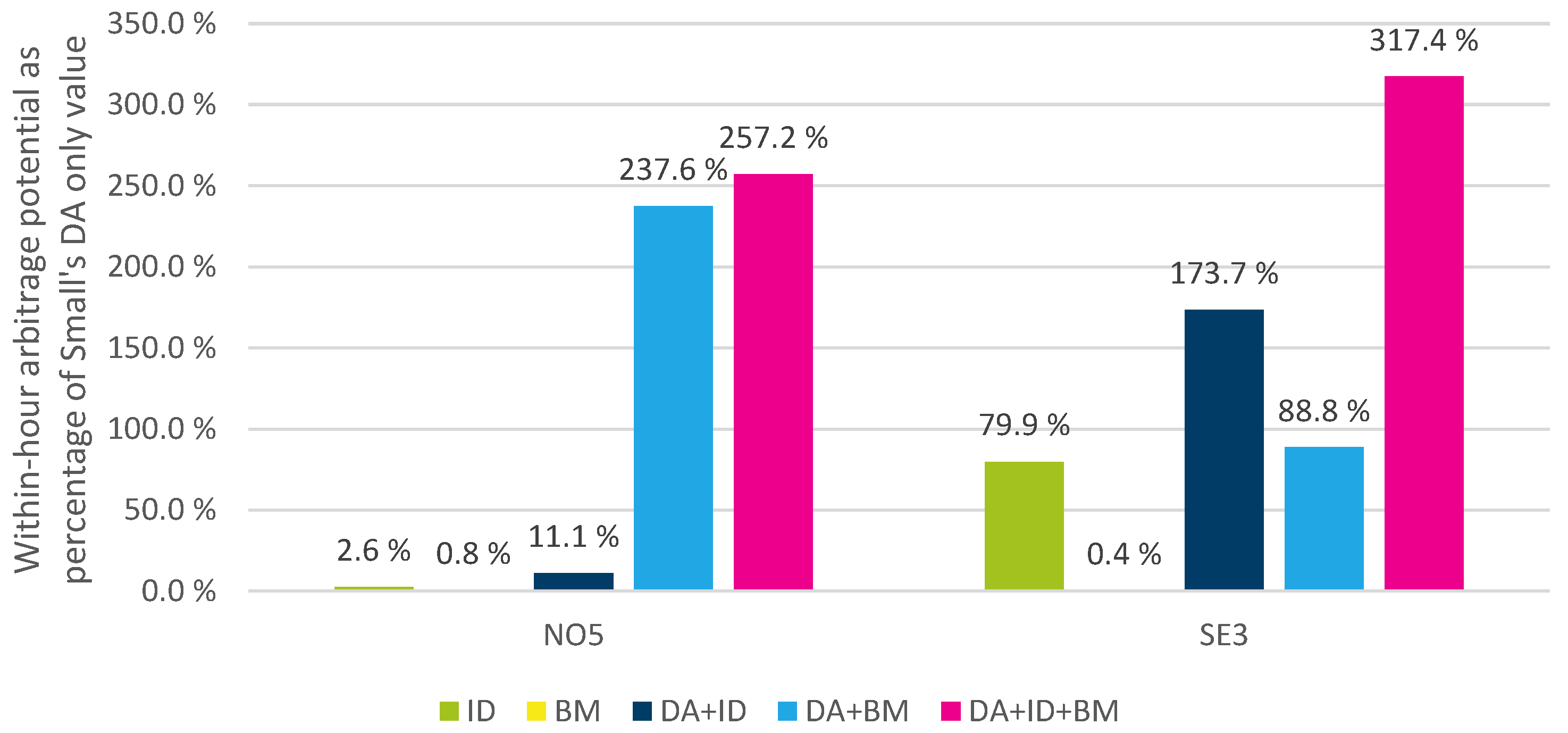

In order to understand why the effects from introducing purchase liquidity in the markets are so large, we have isolated the profits from within-hour arbitrage running the model with

Pure market trade. The values identified as arbitrage values are shown in

Figure 7. The figure shows that the main part of the added value comes from pure market trades between and within the markets. When removing this arbitrage value from our results, there is no added value beyond what is achieved with only a sale (see

Figure 4). This means that adding purchase liquidity to the markets does not increase the value of the water resources available to the hydropower producer in our setting. If the power producer does purchase one unit of power in a market in a given hour, he will have no means of utilizing this power unit other than selling it in a different market within the same hour. If the power producer had access to a pumping storage facility, or had contractual delivery commitments, this could have changed the analysis. Additionally, if we had included uncertainty, the purchase liquidity could have been used to avoid production costs or imbalance costs in non-favourable market clearing situations.

The results of our analysis highlights the importance of dealing with unwanted arbitrage options that might be available when modelling both purchase and sale. This is true both for deterministic and stochastic models, although the effects are easier to identify in deterministic models. We must be aware of these values as a source of disturbance, since an optimization model will aim to utilize any profit potential, including arbitrage, not differentiating between pure market speculation and rebalancing motivated by properties in the production system. In our stylized model, with a highly simplified description of the production technology, no price response, and known prices across multiple markets, this property becomes very visible. In more complex models with stricter assumptions, the arbitrage values are usually relatively smaller and thereby harder to observe, but that does not necessarily mean they are not there.

In order to limit unrealistic arbitrage profits in analyses with bidirectional multi-market trade, two approaches are often used: rolling-horizon and stochastic programming. By using a rolling-horizon set-up, perfect foresight over the full analysis horizon is avoided. This can reduce the possibility of intertemporal arbitrage trades. However, in our analysis, the arbitrage values can be achieved by bidirectional trading within the same hour. That is, given the assumptions and data used in our analysis, a rolling-horizon set-up would not influence our results in terms of arbitrage values. With stochastic programming, however, the problem of unrealistic arbitrage values may be reduced or eliminated completely. To what extent arbitrage potentials are present in a stochastic model is determined by the scenario generation method and scenario tree size. For instance, if the scenario tree is constructed such that all markets trading the same product have the same expected price in the scenario tree, this will remove all arbitrage options. However, in reality, different markets trading the same product typically have different conditions, e.g., the closing time. Such differing conditions can cause price differences, which, again, give rise to potentials for pure financial gains. To realistically represent this, the real information structure and data properties must be replicated at a very high level of detail in the scenario tree. It is also worthwhile to notice that such financial gains in a stochastic model, and in reality, will be subject to uncertainty and risk.

5.5. Results Discussion

In our analyses, we have identified a value-creation potential for hydropower producers from participating in multiple-markets. This potential depends on the plants’ characteristics (size and flexibility), the number of markets that the producer participates in, as well as the geographical area in which the producer is located. To quantify the potential, we have used a simplified model of the physcial production system and perfect foresight for all uncertain parameters. It is important to note that while these assumptions provide an upper bound on the profits obtained by the producer, it is not necessarily an upper bound on the added value of participating in multiple markets, which we have calculated as the difference between the multi-market profits and the profits from DA only.

There are several elements that might increase the added value-creation potential for hydropower producers that do not show up in our results. Firstly, the assumption of perfect foresight might negatively affect the value of multiple markets. The access to multiple markets provides the producers with addititional flexibility when selling their production. With perfect foresight, they can use this flexibility to maximize their profits by choosing the market with the highest price. When the producers have to take into account uncertainty in prices, tradeable quantity and inflow; however, this flexibility can provide value through improved recourse decisions. The access to this flexibility can also improve the decisions that the producers take for the upcoming period. That is, the value of recourse decisions can increase due to the added flexibility provided by the multiple markets, while the first-stage decisions may improve when the producer realize that this flexibility is available at a later stage in time. By removing the perfect foresight for the producers, the absolute value of their production over the year would certainly not increase, but the relative value of access to multiple markets may increase. Secondly, by including a combination of uncertainty and a more sophisticated modelling of the physical production system, the access to multiple markets may provide the producers with sufficient flexibility to avoid high production costs due to unfavourable market clearings. This will typically have the largest value for inflexible producers, such as Run-of-river and other VRES, who can seek to adjust their position in the market as production forecasts improve closer to the time of operation, and thereby avoid costly imbalance settlements.

Our analyses do not, however, provide a lower bound on the value of trading in multiple markets either, and there are several factors that may contribute to reducing the values that we have identified. Firstly, the assumption of perfect foresight and co-optimized trading increases the potential of the producer to exploit any price differences between the markets such that the highest available price is always obtained. Secondly, the simplified production system modelling may obscure important production costs that could reduce the value of multiple-market trading, for instance, additional costs of changing production plans at short notice. Finally, our analysis of the influence of liquidity in the markets illustrate that for some of the markets the liquidity limits are too liberal.

In summary, what we can conclude is that our analyses illustrate that there is an added value-creation potential with multi-market trading given our assumptions. There is also a vast potential for further research in order to detail how different assumptions will influence this value-creation.

6. Conclusions

In this paper, we have presented a case analysis to illustrate the potential value creation from multi-market trading for a price-taking hydropower producer with perfect foresight. The studied markets are the day-ahead, intra-day and balancing markets, represented by historical data from Norway (NO5), Sweden (SE3) and Germany in 2015. We have used a stylized model for the physcial production system to focus on the implications of market availability and properties.

Based on our results, we conclude that there is a theoretical potential for added value creation from selling in multiple markets compared to the benchmark of just selling in the dominating day-ahead market. For example, in the most liquid market, Germany, the calculated added value with day-ahead and intra-day relative to day-ahead only is in the range 6.4–7.9% depending on the plant’s flexibility. The major part of this added value is also achieved when the perfect foresight is limited to the horizon from day-ahead bidding until the time of operation, observing values in the range 4.7–7.8% with the German day-ahead and intra-day market.

Plants with different flexibility properties in terms of number of full load hours and degree of regulation are studied. The results show that added values are largest for the most flexible plants and flexible plants also have the largest benefit from a long perfect foresight horizon.

To improve the assessment of multi-market trading values, we suggest several lines of research. A more realistic modelling of market uncertainties (prices, liquidity limits and balancing activation), in particular within the day-ahead horizon, is preferable. Furthermore, when analysing small markets, the inclusion of market power and possibly also stochastic liquidity limits are suggested. Moreover, improved modelling of the production system, both production function and inflow uncertainty, would give a more realistic description of production cost and recourse value from rebalancing trade options.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}