Emissions Trading System of the European Union: Emission Allowances and EPEX Electricity Prices in Phase III

Abstract

:1. Introduction

- Reduction of free allocation. Most notably, policy-makers reduced the free allocation of emission allowances once again. This has led to 40% of allowances being sold at auction. For instance, the entire power production sector is forced to buy allowances at auction. As such, electricity producers must buy emission allowances on the energy exchange when they have exceeded their allowance, e.g., due to higher-than-expected emissions. Additionally, in the period of 2014–2016, they reduced the number of certificates by 900 million. These certificates will be used as a market stability reverse mechanism to match demand and supply.

- Expansion to more industries and further greenhouse gases. The EU ETS now accounts for additional greenhouse gases that were not part of phase II, such as nitrous oxide (NO) and perfluorocarbons (PFCs). In addition, it adds a wider array of industry sectors, such as manufacturing industries and aircraft operators.

- EU registry. While national registries collected the names of companies qualified for emissions trading during phase II, these were replaced in phase III by a registry encompassing the full European Union, which now includes 31 countries participating in the EU ETS. The European registry was introduced in order to establish a better control mechanism throughout the member states.

2. Related Work

2.1. Long Run vs. Short Run Relationship

2.2. Asymmetric Pass-Through Rate

2.3. Directional Influence

3. Methods and Materials

3.1. Modeling of Electricity Prices

3.2. Autoregressive Time Series Model

3.3. Asymmetric Influence Via Quantile Regressions

3.4. Dataset

4. Results

4.1. Stationarity

4.2. Influence of Carbon Price during the EU ETS Regimes

Robustness Checks

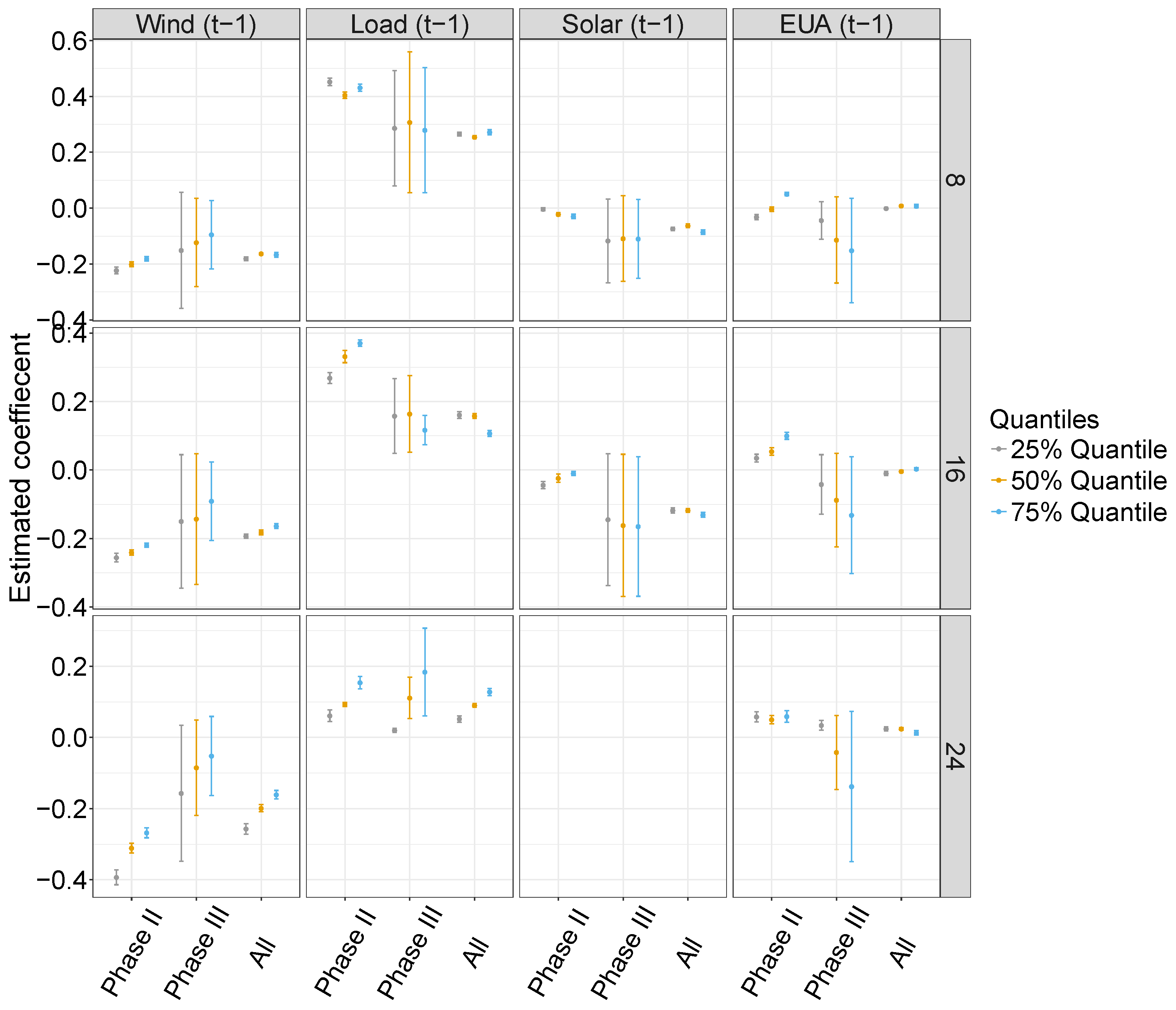

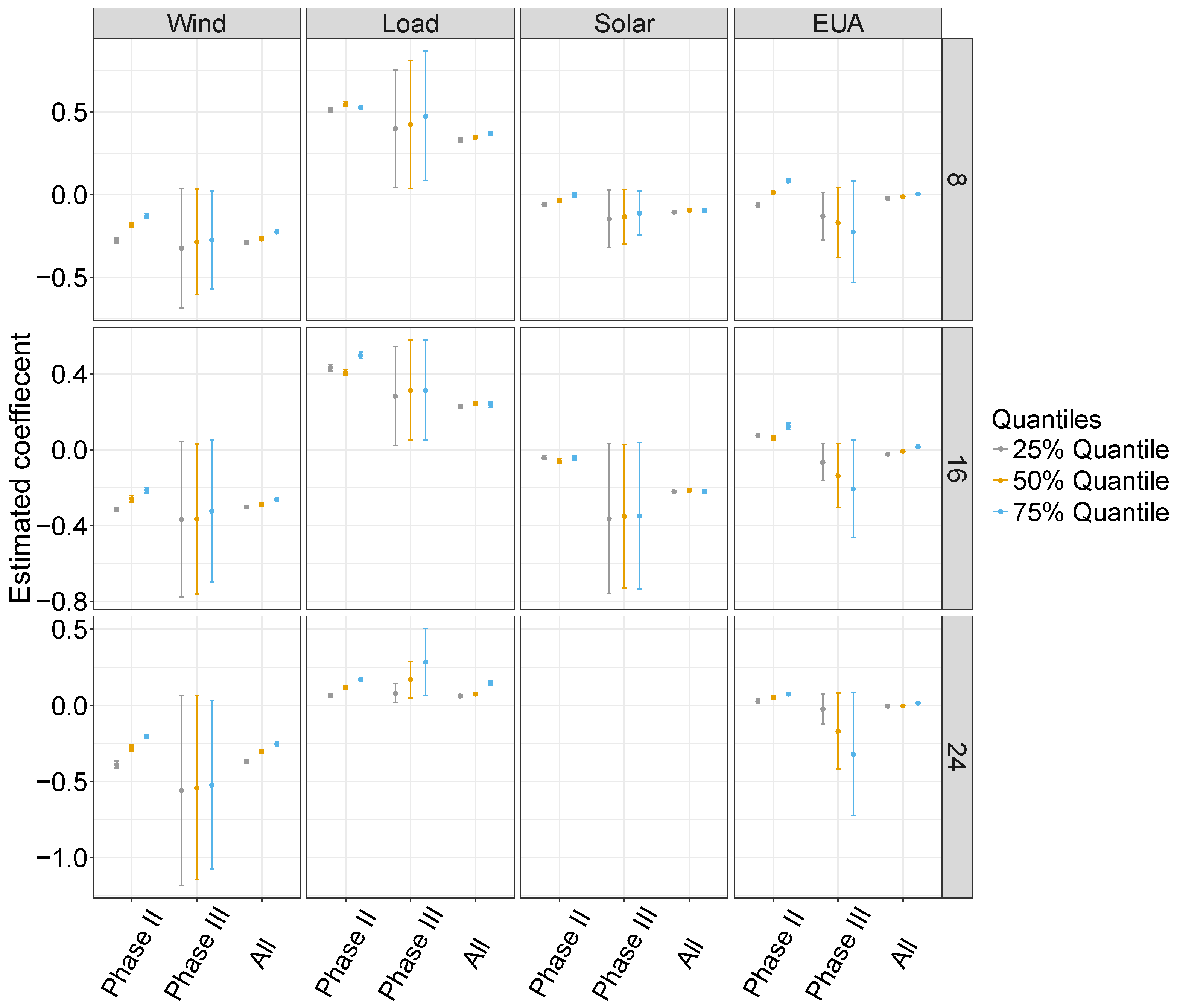

4.3. Asymmetric Influence of the Carbon Price on Electricity Prices

5. Discussion of Findings

- Excess supply of emission allowances. Since we find a weak and inconsistent influence of the emission allowance prices on the electricity price, the price must be too low to play a significant role in power generation. This is particularly evident in our autoregressive model during phase II, where we observe no direct effect. The same model evinces a statistically significant negative impact only for the day-ahead and intraday market in phase III. These findings are consistent with previous research, suggesting that the impact of low carbon prices is rather moderate [9,15] and becomes observable only above certain thresholds. Surprisingly, even though more industries are forced to engage in emissions trading in phase III of the EU ETS, actual power generation and the corresponding electricity price seem unaffected by carbon trading. Consequently, the presence of nonsignificant influences partially originate from an excess supply of emission allowances.

- Changing energy mix. The Emissions Trading System functions in a highly intricate interplay with other policies, especially the incentivized introduction of renewable energy sources. Renewables account for a growing portion of the total electricity supply. (Retrieved from http://www.bmwi-energiewende.de/EWD/Redaktion/Newsletter/2015/1/Meldung/infografik-strommix-2014-erneuerbare-auf-rekordhoch.html on 9 June 2019.) As these electricity sources replace fossil-fuel power plants, the demand for emission allowances (relative to the total electricity demand) must decrease at the same pace. Otherwise, the burgeoning share of renewables inherently results in an excess supply of emission allowances, thus counteracting one of the main advantages of renewable energies.

- Merit order effect. Large carbon prices are also linked to larger marginal costs for carbon-intensive power plants as opposed to renewable energies. This explains the differential influence of carbon prices as revealed by our quantile regressions. An additional reason is given by support schemes for renewables that sometimes grant preferential treatment. That is, wind and solar power must be consumed before power is generated via other means. Hence, carbon prices have a less significant effect on electricity prices when renewables produce a high amount of electricity, i.e., when electricity prices are low.

6. Conclusions

6.1. Summary of the Findings

6.2. Limitations and Call for Future Research

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

References

- European Commission. The EU Emissions Trading System. 2018. Available online: https://ec.europa.eu/clima/policies/ets (accessed on 29 March 2019).

- Hintermann, B.; Peterson, S.; Rickels, W. Price and Market Behavior in Phase II of the EU ETS: A Review of the Literature. Rev. Environ. Econ. Policy 2015, 10, 108–128. [Google Scholar]

- Sijm, J.; Neuhoff, K.; Chen, Y. CO2 cost pass-through and windfall profits in the power sector. Clim. Policy 2006, 6, 49–72. [Google Scholar] [CrossRef]

- Jouvet, P.A.; Solier, B. An overview of CO2 cost pass-through to electricity prices in Europe. Energy Policy 2013, 61, 1370–1376. [Google Scholar] [CrossRef]

- Cotton, D.; Mello, L.D. Econometric analysis of Australian emissions markets and electricity prices. Energy Policy 2014, 74, 475–485. [Google Scholar] [CrossRef]

- Thoenes, S. Understanding the Determinants of Electricity Prices and the Impact of the German Nuclear Moratorium in 2011. Energy J. 2014, 35, 61–78. [Google Scholar] [CrossRef]

- Bunn, D.; Fezzi, C. Interaction of European carbon trading and energy prices. J. Energy Mark. 2009, 2, 53–69. [Google Scholar] [CrossRef]

- Bello, A.; Reneses, J. Electricity price forecasting in the Spanish market using cointegration techniques. In Proceedings of the 33rd Annual International Symposium on Forecasting (ISF 2013), Seoul, Korea, 23–26 June 2013; pp. 1–7. [Google Scholar]

- Freitas, C.J.P.; da Silva, P.P. European Union emissions trading scheme impact on the Spanish electricity price during phase II and phase III implementation. Util. Policy 2015, 33, 54–62. [Google Scholar] [CrossRef]

- Fell, H. EU-ETS and Nordic electricity: A CVAR analysis. Energy J. 2010, 31, 1–25. [Google Scholar] [CrossRef]

- Jabłońska, M.; Viljainen, S.; Partanen, J.; Kauranne, T. The impact of emissions trading on electricity spot market price behavior. Int. J. Energy Sect. Manag. 2012, 6, 343–364. [Google Scholar] [CrossRef]

- Bannör, K.; Kiesel, R.; Nazarova, A.; Scherer, M. Parametric model risk and power plant valuation. Energy Econ. 2016, 59, 423–434. [Google Scholar]

- Chernyavs’ka, L.; Gullì, F. Marginal CO2 cost pass-through under imperfect competition in power markets. Ecol. Econ. 2008, 68, 408–421. [Google Scholar]

- Hintermann, B. Pass-Through of CO2 Emission Costs to Hourly Electricity Prices in Germany. J. Assoc. Environ. Resour. Econ. 2016, 3, 857–891. [Google Scholar] [CrossRef]

- Zachmann, G.; von Hirschhausen, C. First evidence of asymmetric cost pass-through of EU emissions allowances: Examining wholesale electricity prices in Germany. Econ. Lett. 2008, 99, 465–469. [Google Scholar] [CrossRef] [Green Version]

- Aatola, P.; Ollikainen, M.; Toppinen, A. Impact of the carbon price on the integrating European electricity market. Energy Policy 2013, 61, 1236–1251. [Google Scholar] [CrossRef]

- Woo, C.K.; Olson, A.; Chen, Y.; Moore, J.; Schlag, N.; Ong, A.; Ho, T. Does California’s CO2 price affect wholesale electricity prices in the Western U.S.A.? Energy Policy 2017, 110, 9–19. [Google Scholar] [CrossRef]

- Paraschiv, F.; Erni, D.; Pietsch, R. The impact of renewable energies on EEX day-ahead electricity prices. Energy Policy 2014, 73, 196–210. [Google Scholar] [CrossRef] [Green Version]

- Bierbrauer, M.; Menn, C.; Rachev, S.T.; Trück, S. Spot and derivative pricing in the EEX power market. J. Bank. Financ. 2007, 31, 3462–3485. [Google Scholar]

- Deng, S.; Oren, S.S. Electricity derivatives and risk management. Energy 2006, 31, 940–953. [Google Scholar]

- Knittel, C.R.; Roberts, M.R. An empirical examination of restructured electricity prices. Energy Econ. 2005, 27, 791–817. [Google Scholar]

- Weron, R. Modeling and Forecasting Electricity Loads and Prices: A Statistical Approach; John Wiley & Sons: Chichester, UK, 2007; Volume 403. [Google Scholar]

- Paschen, M. Dynamic analysis of the German day-ahead electricity spot market. Energy Econ. 2016, 59, 118–128. [Google Scholar] [Green Version]

- Contreras, J.; Espinola, R.; Nogales, F.J.; Conejo, A.J. ARIMA models to predict next-day electricity prices. IEEE Trans. Power Syst. 2003, 18, 1014–1020. [Google Scholar]

- Fuglerud, M.; Vedahl, K.E.; Fleten, S.E. Equilibrium simulation of the Nordic electricity spot price. In Proceedings of the 2012 9th International Conference on the European Energy Market, Florence, Italy, 10–12 May 2012; pp. 1–10. [Google Scholar]

- Ludwig, N.; Feuerriegel, S.; Neumann, D. Putting big data analytics to work: Feature selection for forecasting electricity prices using the LASSO and random forests. J. Decis. Syst. 2015, 24, 19–36. [Google Scholar]

- Weron, R. Electricity price forecasting: A review of the state-of-the-art with a look into the future. Int. J. Forecast. 2014, 30, 1030–1081. [Google Scholar] [CrossRef] [Green Version]

- Ferkingstad, E.; Løland, A.; Wilhelmsen, M. Causal modeling and inference for electricity markets. Energy Econ. 2011, 33, 404–412. [Google Scholar] [Green Version]

- Wolff, G.; Feuerriegel, S. Short-term dynamics of day-ahead and intraday electricity prices. Int. J. Energy Sect. Manag. 2017, 11, 557–573. [Google Scholar] [Green Version]

- Beran, P.; Pape, C.; Weber, C. Modelling German electricity wholesale spot prices with a parsimonious fundamental model—Validation and application. Util. Policy 2019, 58, 27–39. [Google Scholar] [CrossRef]

- Benhmad, F.; Percebois, J. Photovoltaic and wind power feed-in impact on electricity prices: The case of Germany. Energy Policy 2018, 119, 317–326. [Google Scholar] [CrossRef]

- Clò, S.; Cataldi, A.; Zoppoli, P. The merit-order effect in the Italian power market: The impact of solar and wind generation on national wholesale electricity prices. Energy Policy 2015, 77, 79–88. [Google Scholar]

- Gelabert, L.; Labandeira, X.; Linares, P. An ex-post analysis of the effect of renewables and cogeneration on Spanish electricity prices. Energy Econ. 2011, 33, 59–65. [Google Scholar]

- Mosquera-López, S.; Nursimulu, A. Drivers of electricity price dynamics: Comparative analysis of spot and futures markets. Energy Policy 2019, 126, 76–87. [Google Scholar] [CrossRef]

- Wooldridge, J. Introductory Econometrics: A Modern Approach, 5th ed.; Cengage Learning: Boston, MA, USA, 2012. [Google Scholar]

- Paraschiv, F.; Bunn, D.W.; Westgaard, S. Estimation and Application of Fully Parametric Multifactor Quantile Regression with Dynamic Coefficients; University of St. Gallen, School of Finance Research Paper No. 2016/07; 2016; Available online: https://ssrn.com/abstract=2741692 (accessed on 29 March 2019).

- Koenker, R.; Bassett, G. Regression Quantiles. Econometrica 1978, 46, 33–50. [Google Scholar]

- Pape, C.; Hagemann, S.; Weber, C. Are fundamentals enough? Explaining price variations in the German day-ahead and intraday power market. Energy Econ. 2016, 54, 376–387. [Google Scholar] [CrossRef] [Green Version]

- Würzburg, K.; Labandeira, X.; Linares, P. Renewable generation and electricity prices: Taking stock and new evidence for Germany and Austria. Energy Econ. 2013, 40, 159–171. [Google Scholar]

{kind=link}

{kind=link}

| Variable, Unit | Symbol | Frequency | Description | Data Source |

|---|---|---|---|---|

| Day-ahead spot price, € | Hourly | Electricity price of day-ahead auction with delivery in Germany and Austria: The auction price is set at 12 a.m. for each hour of the next day | European Power Exchange | |

| Intraday spot price, € | Hourly | Continuous intraday electricity price with delivery in Germany and (partially) Austria, where trading is possible up to 30 min before delivery | European Power Exchange | |

| Wind infeed, | Hourly | Aggregated total wind infeed from the four transmission system operators (TransnetBW, Tennet, Amprion, and 50 Hertz) in Germany | Energy Exchange (EEX) Transparency | |

| Solar infeed, | Hourly | Aggregated total photovoltaic infeed from the four transmission system operators (TransnetBW, Tennet, Amprion, and 50 Hertz) in Germany | EEX Transparency | |

| Load, | Hourly | Total hourly electricity consumption in Germany | ENTSO-E | |

| Price of EUA, € | Daily | Setting price of EEX European Emission Allowance (EUA) future that is continuously traded on the Intercontinal Exchange (ICE): one EUA entitles its holder to emit one ton of carbon dioxide or its equivalents | Thomson Reuters Datastream |

| Phase II | Phase III | Relative Change | |

|---|---|---|---|

| Time Period | Jan 2010–Dec 2012 | Jan 2013–Dec 2014 | |

| Observations | 782 | 522 | |

| Mean | 11.61 | 5.23 | −54.26% |

| Median | 12.71 | 5.13 | −59.64% |

| Min. | 5.74 | 2.70 | −52.96% |

| Max. | 17.03 | 7.37 | −56.72% |

| Std. dev. | 3.56 | 1.02 | −71.35% |

| Skew. | −0.16 | 0.01 | 106.25% |

| Kurt. | −1.57 | −0.67 | 57.32% |

| Dependent Variable: Hourly Day-Ahead Electricity Price | |||||||||

| Phase II (2010–2012) | Phase III (2013–2014) | Phases II & III (2010–2014) | |||||||

| Hour 8 | Hour 16 | Hour 24 | Hour 8 | Hour 16 | Hour 24 | Hour 8 | Hour 16 | Hour 24 | |

| −0.13 | −0.11 | −0.08 | −0.09 | −0.08 | −0.04 | −0.11 | −0.10 | −0.08 | |

| t-value | (−11.07) | (−12.97) | (−7.55) | (−4.74) | (−4.11) | (−3.22) | (−9.41) | (−9.60) | (−7.55) |

| −0.01 | −0.02 | −0.08 | −0.11 | −0.05 | −0.07 | ||||

| t-value | (−1.86) | (−2.21) | (−3.11) | (−3.99) | (−4.28) | (−5.93) | |||

| 0.85 | 0.67 | 0.30 | 1.00 | 0.92 | 0.40 | 0.72 | 0.63 | 0.30 | |

| t-value | (13.77) | (15.20) | (0.71) | (6.67) | (9.20) | (7.06) | (12.39) | (14.97) | (0.71) |

| −0.05 | 0.05 | 0.00 | −0.32 | −0.26 | −0.13 | −0.01 | −0.01 | 0.00 | |

| t-value | (−1.68) | (2.56) | (0.71) | (−3.45) | (−4.54) | (−3.00) | (−0.86) | (1.42) | (0.71) |

| 0.16 | 0.22 | 0.42 | 0.19 | 0.27 | 0.50 | 0.21 | 0.27 | 0.42 | |

| t-value | (7.45) | (8.32) | (13.86) | (4.41) | (7.52) | (16.22) | (10.48) | (12.14) | (13.86) |

| 0.17 | 0.15 | 0.23 | 0.18 | 0.20 | 0.22 | 0.20 | 0.19 | 0.23 | |

| t-value | (6.18) | (6.61) | (10.74) | (4.06) | (5.45) | (5.95) | (8.13) | (10.31) | (10.74) |

| 0.15 | 0.12 | 0.15 | 0.21 | 0.17 | 0.12 | 0.21 | 0.19 | 0.15 | |

| t-value | (4.11) | (3.98) | (5.75) | (3.12) | (4.28) | (3.80) | (5.57) | (7.38) | (5.75) |

| Observations | 1089 | 1089 | 1089 | 716 | 716 | 716 | 1819 | 1819 | 1819 |

| Adjusted | 0.98 | 0.98 | 0.99 | 0.94 | 0.95 | 0.98 | 0.96 | 0.97 | 0.98 |

| F-statistic | 4661.56 | 7564.34 | 883.99 | 1148.79 | 1659.21 | 3809.93 | 4669.10 | 7051.32 | 22148.95 |

| Dependent Variable: Hourly Intraday Electricity Price | |||||||||

| Phase II (2010–2012) | Phase III (2013–2014) | Phases II & III (2010–2014) | |||||||

| Hour 8 | Hour 16 | Hour 24 | Hour 8 | Hour 16 | Hour 24 | Hour 8 | Hour 16 | Hour 24 | |

| −0.16 | −0.14 | −0.14 | −0.18 | −0.25 | −0.24 | −0.17 | −0.18 | −0.16 | |

| t-value | (−8.94) | (−11.79) | (−7.08) | (−14.26) | (−13.94) | (−14.40) | (−13.02) | (−16.51) | (−11.07) |

| −0.02 | −0.05 | −0.05 | −0.28 | −0.04 | −0.14 | ||||

| t-value | (−2.68) | (−4.00) | (−5.44) | (−11.06) | (−5.24) | (−9.07) | |||

| 1.04 | 0.86 | 0.49 | 1.16 | 1.54 | 0.97 | 0.87 | 0.88 | 0.43 | |

| t-value | (18.20) | (16.10) | (8.12) | (20.42) | (19.70) | (13.46) | (20.38) | (20.84) | (9.55) |

| −0.07 | 0.05 | 0.05 | −0.36 | −0.42 | −0.28 | −0.00 | −0.00 | 0.00 | |

| t-value | (−1.85) | (1.74) | (1.88) | (−6.25) | (−5.86) | (−5.15) | (−0.48) | (−0.07) | (0.66) |

| 0.13 | 0.21 | 0.27 | 0.11 | 0.15 | 0.16 | 0.17 | 0.23 | 0.30 | |

| t-value | (4.44) | (7.66) | (8.25) | (4.00) | (6.33) | (4.92) | (8.07) | (12.77) | (11.11) |

| 0.07 | 0.07 | 0.14 | 0.13 | 0.01 | 0.14 | 0.12 | 0.09 | 0.20 | |

| t-value | (3.03) | (3.11) | (4.01) | (4.97) | (0.49) | (4.52) | (6.45) | (4.88) | (6.51) |

| 0.05 | 0.04 | 0.13 | 0.20 | 0.09 | 0.11 | 0.15 | 0.14 | 0.19 | |

| t-value | (1.74) | (1.43) | (3.63) | (6.04) | (3.35) | (3.91) | (6.04) | (6.57) | (6.66) |

| Observations | 1089 | 1089 | 1089 | 716 | 716 | 716 | 1819 | 1819 | 1819 |

| Adjusted | 0.97 | 0.95 | 0.97 | 0.97 | 0.95 | 0.97 | 0.95 | 0.96 | 0.96 |

| F-statistic | 2359.96 | 3526.41 | 3940.32 | 2277.76 | 1485.25 | 2852.08 | 3959.73 | 4505.73 | 6164.12 |

| Dependent Variable: Hourly Day-Ahead Electricity Price | |||||||||

| Phase II (2010–2012) | Phase III (2013–2014) | Phases II & III (2010–2014) | |||||||

| Hour 8 | Hour 16 | Hour 24 | Hour 8 | Hour 16 | Hour 24 | Hour 8 | Hour 16 | Hour 24 | |

| −0.28 | −0.20 | −0.21 | −0.15 | −0.12 | −0.05 | −0.22 | −0.16 | −0.13 | |

| t-value | (−11.56) | (−14.51) | (−9.39) | (−5.09) | (−5.37) | (−3.36) | (−10.39) | (−11.75) | (−8.14) |

| −0.69 | −0.07 | −1.07 | −0.10 | −1.07 | −0.11 | ||||

| t-value | (−3.68) | (−3.59) | (−2.90) | (−4.66) | (−5.17) | (−7.81) | |||

| 0.68 | 0.51 | 0.32 | 0.66 | 0.47 | 0.20 | 0.55 | 0.41 | 0.21 | |

| t-value | (14.09) | (12.86) | (7.88) | (5.59) | (5.60) | (3.20) | (12.09) | (13.65) | (8.16) |

| −0.12 | −0.15 | 1.86 | −2.20 | −1.25 | −0.34 | −1.03 | −1.37 | 0.38 | |

| t-value | (−0.15) | (−0.20) | (2.38) | (−2.82) | (−2.36) | (−0.84) | (−0.97) | (−1.41) | (0.54) |

| −0.16 | −0.13 | −0.09 | −0.57 | −0.02 | 0.25 | −0.14 | −0.02 | 0.07 | |

| t-value | (−0.71) | (−0.73) | (−0.60) | (−0.83) | (−0.03) | (0.60) | (−0.72) | (−0.10) | (0.51) |

| 0.03 | −0.02 | 0.05 | −0.08 | −0.06 | −0.04 | 0.05 | 0.04 | 0.02 | |

| t-value | (0.30) | (−0.22) | (0.68) | (−0.33) | (−0.32) | (−0.29) | (0.53) | (0.50) | (0.38) |

| 0.40 | 0.26 | 0.25 | 0.46 | 0.48 | 0.28 | 0.41 | 0.38 | 0.23 | |

| t-value | (3.74) | (2.60) | (3.89) | (3.35) | (3.81) | (3.49) | (5.80) | (5.68) | (4.41) |

| 16.74 | −13.82 | 10.15 | 67.93 | 45.04 | 11.23 | 27.65 | 3.24 | 13.60 | |

| t-value | (26.84) | (−0.64) | 0.69 | (0.89) | (0.75) | 0.26 | (1.03) | (0.14) | (0.88) |

| 0.17 | 0.22 | 0.27 | 0.19 | 0.26 | 0.49 | 0.20 | 0.26 | 0.40 | |

| t-value | (7.84) | (8.31) | (7.73) | (4.76) | (8.21) | (16.13) | (10.80) | (12.24) | (13.30) |

| 0.15 | 0.15 | 0.21 | 0.17 | 0.17 | 0.21 | 0.18 | 0.17 | 0.22 | |

| t-value | (6.50) | (6.34) | (9.92) | (4.32) | (6.00) | (5.58) | (8.33) | (10.13) | (10.69) |

| 0.12 | 0.13 | 0.12 | 0.16 | 0.12 | 0.09 | 0.18 | 0.17 | 0.13 | |

| t-value | (3.40) | (4.08) | (2.92) | (3.03) | (3.04) | (2.89) | (5.50) | (6.43) | (4.97) |

| Observations | 1089 | 1089 | 1089 | 716 | 716 | 716 | 1819 | 1819 | 1819 |

| Adjusted | 0.97 | 0.99 | 0.99 | 0.94 | 0.96 | 0.98 | 0.96 | 0.97 | 0.98 |

| F-statistic | 3610 | 6066 | 6919 | 857.3 | 1282 | 2739 | 3548 | 5430 | 7760 |

| Dependent Variable: Hourly Intraday Electricity Price | |||||||||

| Phase II (2010–2012) | Phase III (2013–2014) | Phases II & III (2010–2014) | |||||||

| Hour 8 | Hour 16 | Hour 24 | Hour 8 | Hour 16 | Hour 24 | Hour 8 | Hour 16 | Hour 24 | |

| −0.35 | −0.26 | −0.25 | −0.29 | −0.31 | −0.26 | −0.33 | −0.28 | −0.23 | |

| t-value | (−9.44) | (−12.94) | (−7.41) | (−13.82) | (−14.25) | (−14.95) | (−13.81) | (−17.07) | (−11.14) |

| −0.96 | −0.14 | −0.64 | −0.23 | −0.95 | −0.20 | ||||

| t-value | (−3.84) | (−5.35) | (−4.84) | (−11.16) | (−6.94) | (−10.53) | |||

| 0.86 | 0.65 | 0.42 | 0.78 | 0.87 | 0.45 | 0.70 | 0.59 | 0.32 | |

| t-value | (17.16) | (15.26) | (7.62) | (15.75) | (14.44) | (8.95) | (18.06) | (17.30) | (8.01) |

| −0.88 | −0.69 | 1.25 | −2.53 | −2.37 | −0.79 | −0.58 | −0.24 | 0.62 | |

| t-value | (−0.82) | (−0.59) | (1.13) | (−5.17) | (−4.68) | (−2.28) | (−0.62) | (−0.21) | (0.75) |

| 0.01 | −0.04 | −0.43 | −0.39 | −0.59 | −0.14 | −0.03 | −0.09 | −0.30 | |

| t-value | (0.02) | (−0.16) | (−2.10) | (−0.78) | (−0.88) | (−0.39) | (−0.08) | (−0.39) | (−1.81) |

| −0.03 | 0.01 | 0.02 | −0.07 | 0.29 | 0.05 | 0.12 | 0.18 | 0.11 | |

| t-value | (−0.26) | (0.06) | (0.27) | (−0.37) | (1.34) | (0.38) | (1.14) | (1.44) | (1.51) |

| 0.41 | 0.44 | 0.25 | 0.38 | 0.28 | 0.31 | 0.33 | 0.37 | 0.11 | |

| t-value | (2.55) | (3.13) | (3.16) | (4.97) | (2.88) | (5.66) | (4.65) | (5.04) | (2.45) |

| −2.99 | 34.27 | 22.80 | 84.03 | −10.93 | −3.62 | 15.34 | 25.36 | 14.47 | |

| t-value | (−0.08) | (1.18) | (0.83) | (1.12) | (−0.14) | (−0.09) | (0.46) | (0.86) | (0.58) |

| 0.14 | 0.21 | 0.27 | 0.12 | 0.15 | 0.14 | 0.17 | 0.23 | 0.30 | |

| t-value | (4.80) | (8.00) | (7.69) | (4.30) | (6.45) | (4.02) | (8.41) | (12.48) | (10.95) |

| 0.06 | 0.07 | 0.14 | 0.12 | 0.01 | 0.13 | 0.12 | 0.08 | 0.20 | |

| t-value | (2.98) | (2.86) | (4.41) | (4.90) | (0.37) | (4.29) | (6.41) | (4.61) | (6.57) |

| 0.04 | 0.04 | 0.13 | 0.16 | 0.07 | 0.09 | 0.13 | 0.12 | 0.18 | |

| t-value | 1.19 | (1.43) | (4.00) | (4.66) | (2.88) | (3.29) | (5.67) | (5.94) | (6.75) |

| Observations | 1089 | 1089 | 1089 | 716 | 716 | 716 | 1819 | 1819 | 1819 |

| Adjusted | 0.95 | 0.97 | 0.97 | 0.97 | 0.95 | 0.97 | 0.96 | 0.96 | 0.97 |

| F-statistic | 1719 | 2687 | 2923 | 1713 | 1084 | 2005 | 3034 | 3622 | 4816 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wolff, G.; Feuerriegel, S. Emissions Trading System of the European Union: Emission Allowances and EPEX Electricity Prices in Phase III. Energies 2019, 12, 2894. https://doi.org/10.3390/en12152894

Wolff G, Feuerriegel S. Emissions Trading System of the European Union: Emission Allowances and EPEX Electricity Prices in Phase III. Energies. 2019; 12(15):2894. https://doi.org/10.3390/en12152894

Chicago/Turabian StyleWolff, Georg, and Stefan Feuerriegel. 2019. "Emissions Trading System of the European Union: Emission Allowances and EPEX Electricity Prices in Phase III" Energies 12, no. 15: 2894. https://doi.org/10.3390/en12152894

APA StyleWolff, G., & Feuerriegel, S. (2019). Emissions Trading System of the European Union: Emission Allowances and EPEX Electricity Prices in Phase III. Energies, 12(15), 2894. https://doi.org/10.3390/en12152894