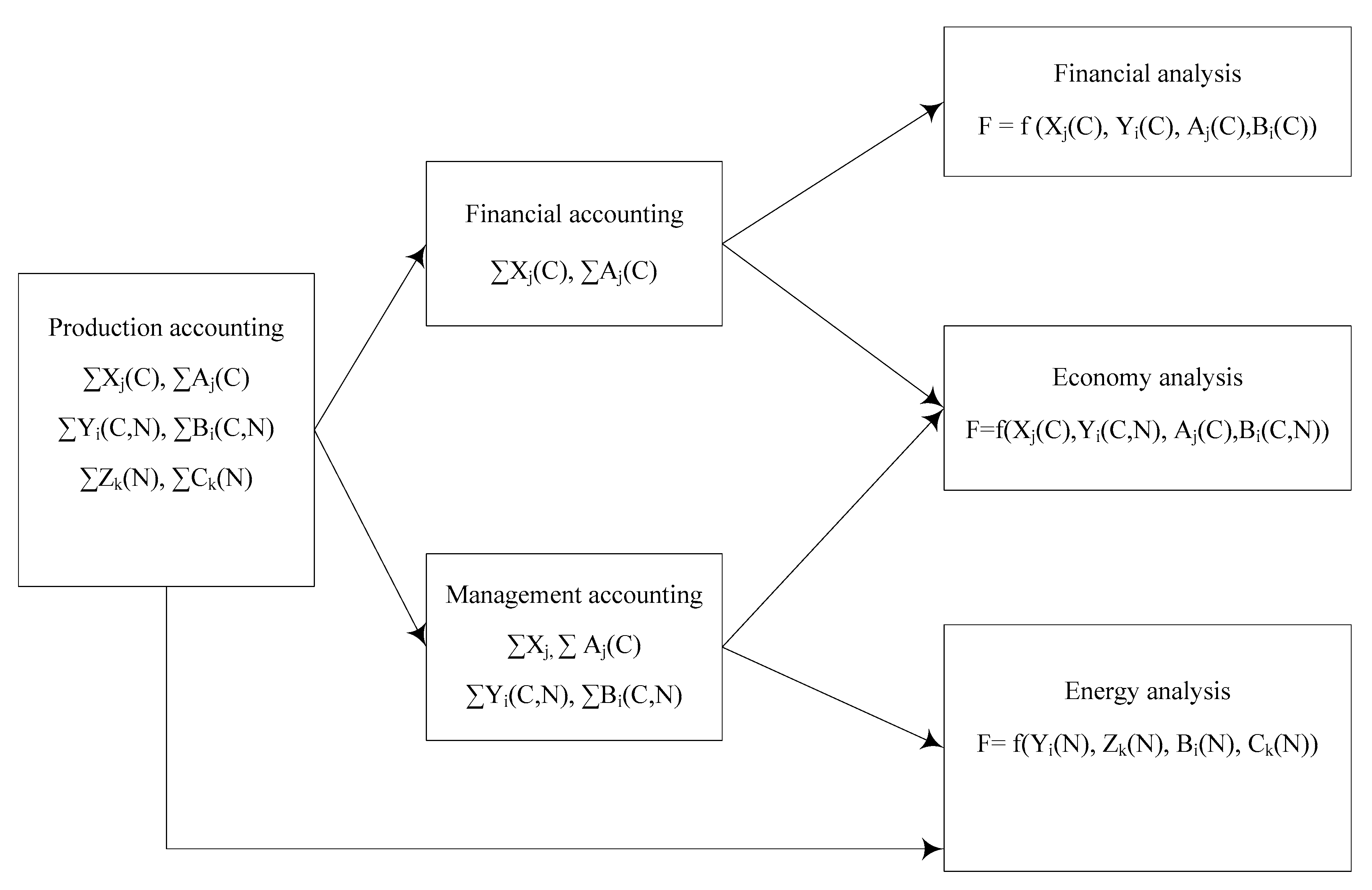

2.1. Oil and Gas Companies’ Indicators of the Energy Analysis

Data on energy consumption are provided in reports of the Russian oil and gas companies from 2005 to 2014. Typically, these data provide limited information. Only several paragraphs of text and several figures related to the consumption of electricity (kWh) and heat (Kcal) in “production” and “transportation and processing” sectors are available. A detailed report of the energy consumption involved in oil processing is not provided. In addition to the absolute values, the specific indicators of electricity consumption in production per ton of oil (kWh/t) are given. Information on energy consumption in reports is complete. The data in physical units (tons of fuels and lubricants, kWh, and tons of steel and cement) on capital investments and operational expenses divided into various production processes are necessary to conduct the energy analysis of oil production. There are three types of capital investments in oil and gas branches: (1) the establishment of newly introduced and the reconstruction of existing production assets, including operations, production, injection, and auxiliary bores; (2) the commercial development of the field, including objects in the environment (field installation and construction of well pads and wellheads); and (3) the equipment for oil and gas, not included in the construction estimates. In oil extracting, branch planning and the accounting of the operational costs of production is conducted at the level of the enterprise and its structural divisions (departments, productions, and sites) on the basis of the existing organizational structure of the enterprise [

43]. Different stages of oil and gas production are shown in

Table 2.

In each of part of the report, the following expenses must be considered:

Raw materials and main materials,

Auxiliary materials,

Fuel,

Energy,

Salary fund and social responsibility funds,

Depreciation of fixed assets,

Transportation costs, and

Other expenses.

There are 13 elements (

Appendix A) described in previous articles. The first twelve items of expenditures in the list form production costs of the gross output of oil, and the last item (business expenses) represents the hollow costs of commodity oil production. The definition of the specific indicators of production efficiency is possible on the basis of those considered expenses. Traditionally, these indicators must include the following:

Costs of oil production, rub/t;

Costs of the extraction of associated gas, rub/thousand m3;

Prime costs of the pumping water in layers, rub/m3;

Costs of the preparation and pumping of oil, rub/t;

Prime costs of capital and the maintenance of wells, one thousand rub; and

Costs of the development of thermal energy and others

Therefore, we have all the information necessary for the energy analysis. The most important indicators of the financial and energy analysis in the companies are shown in

Table 3.

Before considering the calculation method for each indicator, we should examine the EROI figure and explain why it is not included on this indicators list. In this case, the indicator is an ideological mismatch between financial ROI (rate of investment) and EROI. The calculation of EROI considers the entire spectrum of materials and energy consumption. In calculating ROI, the denominator includes only the equity and long-term liabilities without the short-term liabilities. Short-term obligations, such as purchasing fuel and materials, are not considered. Moreover, the deposit can be used by several investors. Each participant will have a certain amount of investments, profit, and the board’s estimated value of the ROI depending on arrangements. For these two reasons, the assumption that is embedded in the ROI and EROI of the energy is incorrect. Meanwhile, in the financial analysis, there is a measure of the “profitability on the production costs” (while ROCS refer to return on cost of sales, in some cases, we refer to it as variable costs), calculated as the ratio of profits to the cost of goods sold. To be theoretically accurate, we should speak about the energy equivalent of increased ROCS and denote it as EROCS (energy return on cost of sales).

There are two main principles in calculating energy efficiency coefficients. First, the efficiency of extracting the primary energy resources is calculated. It is necessary to correlate the amount of primary energy spent in extracting energy. Thus, the elapsed electricity and thermal energy in the calculation must be considered based on the amount spent on the production of primary energy resources. Second, the costs of materials should also be considered based on how much primary energy has been spent on the production of a particular material. However, the definition of the energy intensity of production materials and equipment itself is a serious academic issue that should be addressed in a separate study. The coefficients of energy intensity of key construction materials (especially steel and cement) should be determined based on the results of existing studies. To compare the energy efficiency in different companies, the coefficients must be the same.

(1) ROCS and EROCS

The profitability of expenses (ROCS—return on cost of sales) refers to payments related to the sum of the pure monetary inflow (consisting of net profits and depreciation during the reporting period) considering the prime costs of the goods sold (the sum of expenses of the products sold). The coefficient ROCS characterizes repayments of production costs and shows the profits for the enterprise per ruble spent for production and product sales.

The formula for the calculation of the indicator profitability of expenses is as follows:

The energy EROCS option is the relationship between the equivalent of commodity and the costs of production:

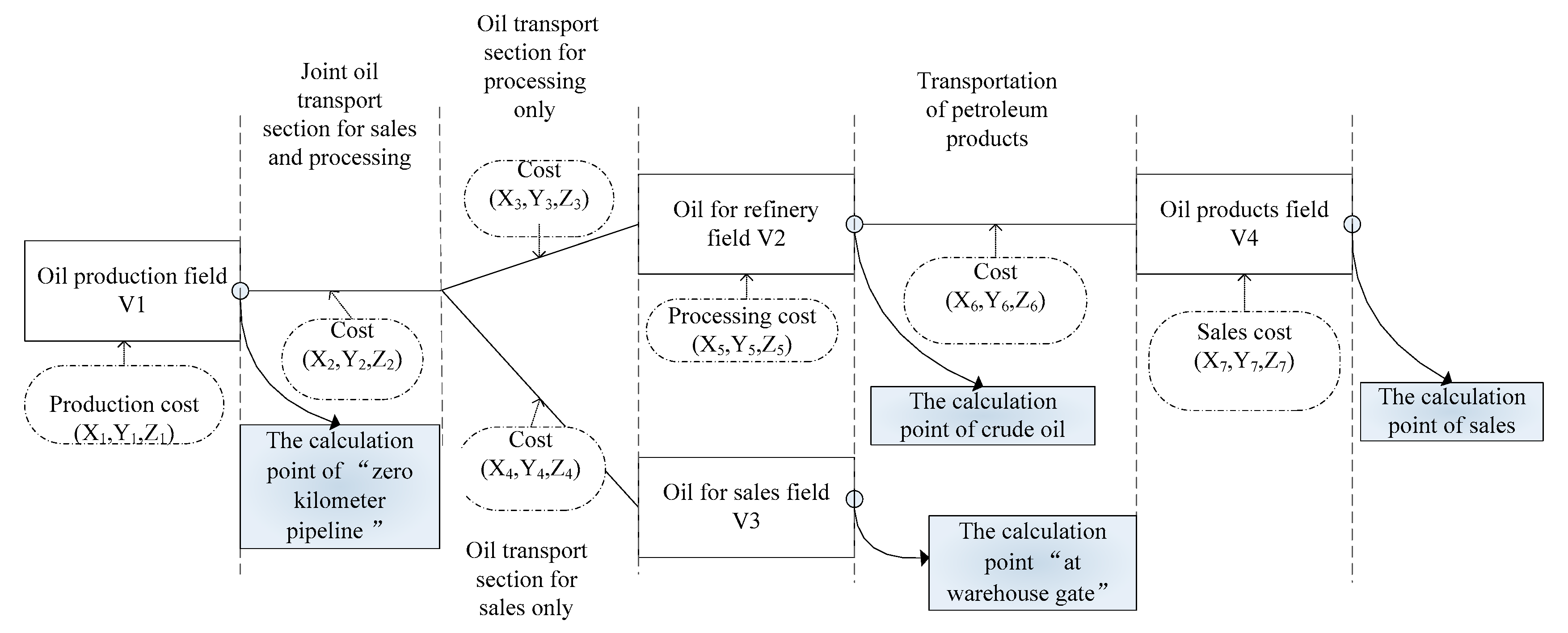

Provided that the calculation point “on zero kilometer of the main pipeline” is used, the numerator includes a volume of the commodity in energy equivalents, and the denominator includes the total volume of energy and the materials in the energy equivalent spent for production. The coefficient shows how much greater the extracted energy is than that spent for production. If EROCS is greater than 1, production is energetically favorable. If EROCS is equal to 1, production is conducted with zero net result. If EROCS is less than 1, production in the energy plan is unprofitable. Thus, all conditions being equal, a higher EROCS value indicates a more efficient energy resource.

(2) ROFA and EROFA

The profitability of non-current assets (return on fixed assets (ROFA)) is defined as the ratio of net profits to total non-current assets. The profitability of non-current assets is a relative measure of efficiency. The quotient of the net profit generated during the period is divided by the total value of non-current assets during the period. The ratio shows the ability of assets to generate profits. In other words, it measures the profits per ruble invested in fixed assets in the organization:

EROFA is calculated as the ratio of the energy equivalent of the hydrocarbon commodity to the energy equivalent of non-current assets. To calculate the energy equivalent, we must have information about non-current asset materials. Furthermore, we should consider the depreciation according to the same rules as the financial indicators’ ROFA. This figure reflects the growing (or declining because of innovation) needs of fixed assets for extracting energy resources. On the one hand, the development of heavy hydrocarbons reserves requires additional capital expenditures. On the other hand, improved technology leads to lower costs. These two trends will be reflected in the indicator EROFA. We can also conclude that increasing (or decreasing) the capital intensity of the production of hydrocarbons depends on the dynamics:

(3) The unit cost of energy and the efficiency of extraction

The unit costs of extracting hydrocarbons are calculated as the ratio of costs for the extraction of hydrocarbons (item 1) to the commercial volume of hydrocarbons. The dynamics of the indicator reflect the economic efficiency of controlling the well foundation. Energy extraction efficiency is calculated as the ratio of the trade volume of hydrocarbons to the energy expended on extraction. The dynamics of the indicator will influence the quality and the depletion of stocks and the effectiveness of controlling the well foundation. Unlike economic indicators, the energy is independent of inflation and other cost factors. Both measures will provide a more complete picture of the status in which stocks and their management are effective on the borehole foundation.

(4) The unit cost and energy efficiency of extraction and preparation

The unit costs of the extraction and preparations of hydrocarbon are calculated as the ratio of the costs of extraction and the effects on the formation, collection, transportation, and technological training on the commercial volume of hydrocarbons. The energy efficiency of the extraction and preparation of hydrocarbons is calculated as the ratio of the trade volume of hydrocarbons to the energy expended on the extraction of them and the effects on the formation, collection, transportation, and primary preparation. The dynamics of the indicator will influence the quality and degree of the depletion of reserves, the management efficiency on the borehole, the effectiveness of the stimulation, and the efficiency of the industrial infrastructure. These indicators reflect the effectiveness of the control of the main production processes in the extraction of hydrocarbons.

(5) The specific capital costs and the energy efficiency of capital expenditures in exploration and production

Specific capital costs are calculated as the ratio of the total capital costs for exploration and production to the commercial volume of hydrocarbons during the period under review. Similarly, it is possible to calculate the energy efficiency of capital expenditures as the ratio of the trade volume of hydrocarbons to the capital expenses for energy exploration and production. Considering the increasing share of tight oil reserves in the structure of mining companies, the dynamics of these indicators will reflect the growing need for additional capital expenditures.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}