Energy Commodities: A Review of Optimal Hedging Strategies

Abstract

:1. Introduction

2. Hedging the Price Risk of Energy Commodities

2.1. Hedging Tools for Managing Energy Commodities’ Price Risk

2.1.1. Forward Contracts

2.1.2. Futures Contracts

2.1.3. Option Contracts

2.1.4. Swap Contracts

3. Building the Optimal Hedging Strategy

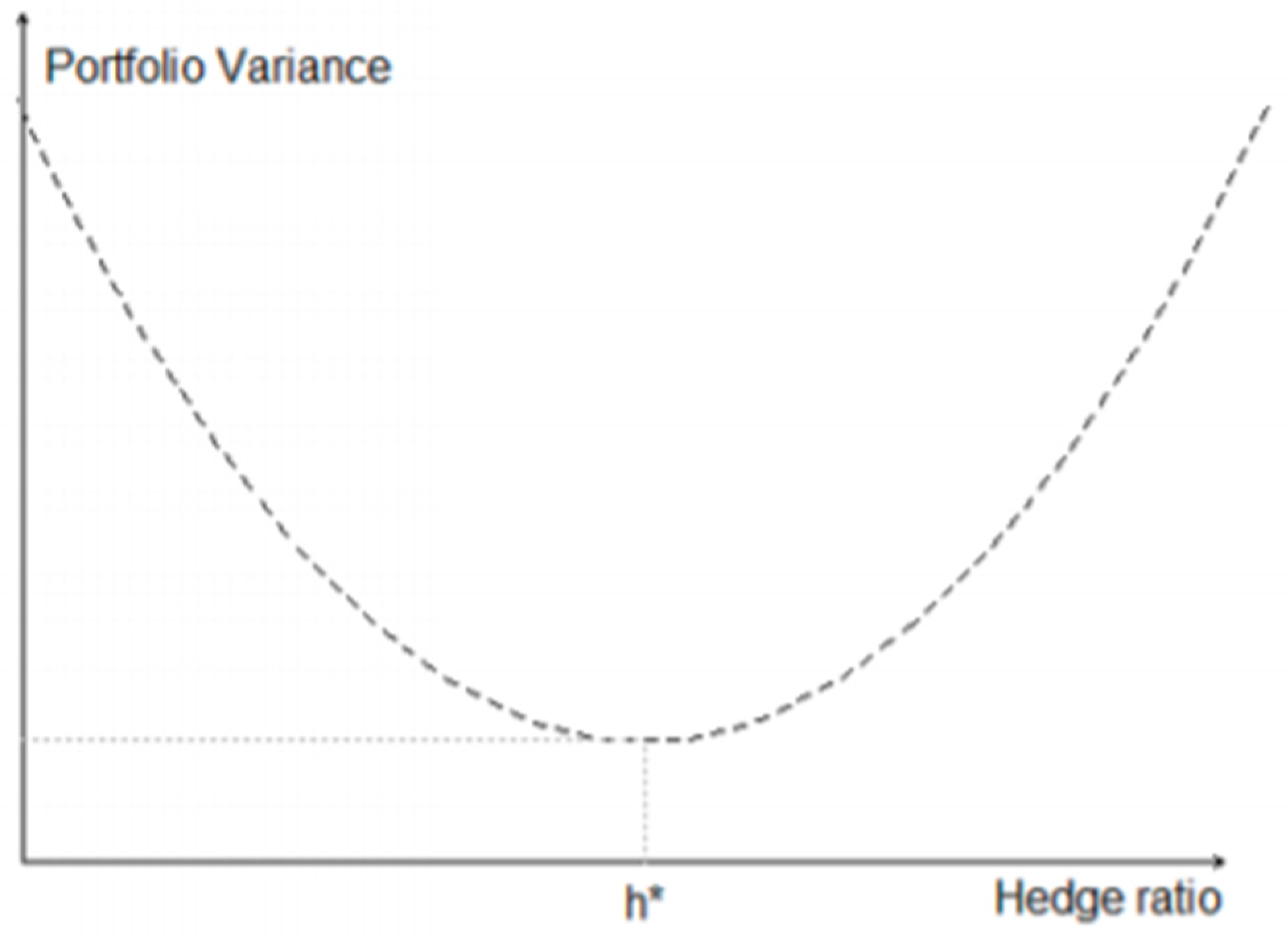

3.1. The Minimum-Variance Hedging Strategy

3.1.1. Estimation of the Minimum-Variance hedge ratio based on the OLS methodology

3.1.2. Estimation of the Minimum-Variance Hedge Ratio based on Nonlinear Multivariate Garch Models

3.2. Hedging via the Expected Utility Maximization Methodology

3.2.1. Measuring Risk Aversion

3.2.2. Optimal Hedge Ratio Estimation based on Expected Utility Theory

3.3. Alternative Hedging Strategies

4. State of the Art—Relevant Studies Using Hedging Strategies

4.1. Optimal Hedging Strategies based on the Minimum Variance Methodology

4.2. Incorporating the Elements of Risk Aversion and Expected Return into the Optimal Hedging Strategy

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- European Commission. Study on Energy Efficiency and Energy Saving Potential in Industry and on Possible Policy Mechanism; EC: Brussels, Belgium, 2015. [Google Scholar]

- Boroumand, R.H.; Goutte, S.; Porcher, S.; Porcher, T. Hedging strategies in energy markets: The case of electricity retailers. Energy Econ. 2015, 51, 503–509. [Google Scholar] [CrossRef]

- Zhang, J.; Tan, K.S.; Weng, C. Optimal hedging with basis risk under mean–variance criterion. Insur. Math. Econ. 2017, 75, 1–15. [Google Scholar] [CrossRef]

- Stulz, R.M. Optimal Hedging Policies. J. Financ. Quant. Anal. 1984, 19, 127–140. [Google Scholar] [CrossRef]

- Dewally, M.; Marriott, L. Effective Basemetal Hedging: The Optimal Hedge Ratio and Hedging Horizon. J. Risk Financ. Manag. 2008, 1, 41–76. [Google Scholar] [CrossRef]

- Hung, J.-C.; Chiu, C.-L.; Lee, M.-C. Hedging with zero-value at risk hedge ratio. Appl. Financ. Econ. 2006, 16, 259–269. [Google Scholar] [CrossRef]

- Halkos, G.E.; Tsirivis, A.S. Value-at-risk methodologies for effective energy portfolio risk management. Econ. Anal. Policy 2019, 62, 197–212. [Google Scholar] [CrossRef]

- Ricardo, D. On the Principles of Political Economy and Taxation; John Murray: London, UK, 1817. [Google Scholar]

- Manoilescu, M. Die Nationalen Producktivkräfte und der Aussenhandel. Theorie des Internationalen Warenaustausches, Junker und Dünnhaupt, Name? Juncker & Dünnhaupt: Berlin, Germany, 1937. [Google Scholar]

- Balassa, B. Trade Liberalisation and “Revealed” Comparative Advantage. Manch. Sch. 1965, 33, 99–123. [Google Scholar] [CrossRef]

- Porter, M.E. The Comparative Advantage of Nations. Harv. Bus. Rev. 1990, 73–91. [Google Scholar] [CrossRef]

- Dogaru, V. The expanding of constructal law in economics—A justification for crossed flows of similar macro goods. Int. J. Heat Technol. 2016, 34, 59–74. [Google Scholar] [CrossRef]

- Kuik, O.; Branger, F.; Quirion, P. Competitive advantage in the renewable energy industry: Evidence from a gravity model. Renew. Energy 2019, 131, 472–481. [Google Scholar] [CrossRef]

- Blum, J. Energy Bankruptcies Back on the Rise in 2019; Houston Chronicle: Houston, TA, USA, 2019. [Google Scholar]

- Seba, E. Bankruptcy Filings by U.S. Energy Producers Pick up Speed: Law Firm Analysis; Reuters: London, UK, 2019. [Google Scholar]

- Haushalter, G.D. Financing Policy, Basis Risk, and Corporate Hedging: Evidence from Oil and Gas Producers. J. Financ. 2000, 55, 107–152. [Google Scholar] [CrossRef]

- Haushalter, G.D. Why Hedge? Some Evidence from Oil and Gas Producers. J. Appl. Corp. Financ. 2001, 13, 87–92. [Google Scholar] [CrossRef]

- Chew, D. Energy Derivatives and the Transformation of the U.S. Corporate Energy Sector. J. Appl. Corp. Financ. 2001, 13, 50–75. [Google Scholar]

- Smithson, C.; Simkins, B.J. Does Risk Management Add Value? A Survey of the Evidence. J. Appl. Corp. Finance 2005, 17, 8–17. [Google Scholar] [CrossRef]

- Carter, D.A.; Rogers, D.A.; Simkins, B.J. Does Hedging Affect Firm Value? Evidence from the US Airline Industry. Financ. Manag. 2006, 35, 53–86. [Google Scholar] [CrossRef]

- Geczy, C.; Minton, B.; Schrand, C. Choices among Alternative Risk Management Strategies: Evidence from the Natural Gas Industry; Working Paper Wharton School of Economics; The Rodney L. White Center for Financial Research: Pennsylvania, PA, USA, 2002. [Google Scholar]

- Jin, Y.; Jorion, P. Firm Value and Hedging: Evidence from U.S. Oil and Gas Producers. J. Financ. 2006, 61, 893–919. [Google Scholar] [CrossRef]

- Islam, M.; Chakraborti, J. Futures and forward contract as a route of hedging the risk. Risk Gov. Control. Financ. Mark. Inst. 2015, 5, 68–78. [Google Scholar] [CrossRef]

- Trafigura. Commodities Demystified: A Guide to Trading and the Global Supply Chain 2018. Available online: www.trafigura.com (accessed on 10 July 2019).

- Difiglio, C. Oil, economic growth and strategic petroleum stocks. Energy Strat. Rev. 2014, 5, 48–58. [Google Scholar] [CrossRef] [Green Version]

- Economic Consulting Associates Limited. European Electricity: Forward Markets and Hedging Products—State of Play and Elements for Monitoring 2015. Available online: www.acer.europa.eu (accessed on 10 July 2019).

- Malik, F. Risk Management: Understanding Credit Risk. Available online: www.medium.com (accessed on 10 July 2019).

- Mas, I.; Saa-Requejo, J. Using Financial Futures in Trading and Risk Management; Policy Research Working Paper; World Bank: Washington, DC, USA, 1995. [Google Scholar]

- IOSCO. Report on the International Regulation of Derivative Markets, Products and Financial Intermediaries 2012. Available online: www.trafigura.com (accessed on 15 July 2019).

- Carmona, R.; Durrleman, V. Pricing and Hedging Spread Options. SIAM Rev. 2003, 45, 627–685. [Google Scholar] [CrossRef] [Green Version]

- New York Mercantile Exchange. A guide to Energy Hedging. Available online: www.renesource.com (accessed on 5 July 2019).

- Coffman, D.; Lockley, A. Carbon dioxide removal and the futures market. Environ. Res. Lett. 2017, 12, 015003. [Google Scholar] [CrossRef]

- Keytrade Bank. Options Manual of Keytrade Bank; Keytrade Bank: Brussels, Belgium, 2017. [Google Scholar]

- Mercatus. An Introduction to Crack Spread (Refiner) Hedging 2019. Available online: www.mercatusenergy.com (accessed on 30 July 2019).

- Vitale, L. Interest Rate Swaps under the Commodity Exchange Act. Case West. Reserve Law Rev. 2001, 51, 539–591. [Google Scholar]

- Ernst & Young. Financial Reporting Developments A Comprehensive Guide Derivatives and Hedging. Available online: www.ey.com (accessed on 25 July 2019).

- Deloitte. Commodity Price Risk Management: A manual of Hedging Commodity Price Risk for Corporates 2018. Available online: www2.deloitte.com (accessed on 16 July 2019).

- Stoft, S.; Belden, T.; Goldman, C.; Pickle, S. Primer on Electricity Futures and Other Derivatives; Environmental Energy Technologies Division, Ernest Orlando Lawrence Berkeley National Laboratory, University of California Berkeley: Berkeley, CA, USA, 1998. [Google Scholar]

- Devlin, J.; Titman, S. Managing Oil Price Risk in Developing Countries. World Bank Res. Obs. 2004, 19, 119–139. [Google Scholar] [CrossRef] [Green Version]

- Ritchken, P. Hedging with Futures Contracts. Case West-ern Reserve University—Class Notes 1999. Available online: http://faculty.weatherhead.case.edu (accessed on 5 July 2019).

- Castellino, M.G. Hedge effectiveness: Basis risk and minimum-variance hedging. J. Futures Mark. 2000, 20, 89–103. [Google Scholar] [CrossRef]

- Johnson, L.L. The Theory of Hedging and Speculation in Commodity Futures. Rev. Econ. Stud. 1960, 27, 139. [Google Scholar] [CrossRef]

- Ederington, L.H. The Hedging Performance of the New Futures Markets. J. Financ. 1979, 34, 157–170. [Google Scholar] [CrossRef]

- Myers, R.J.; Thompson, S.R. Generalized Optimal Hedge Ratio Estimation. Am. J. Agric. Econ. 1989, 71, 858–868. [Google Scholar] [CrossRef] [Green Version]

- Baillie, R.T.; Myers, R.J. Bivariate garch estimation of the optimal commodity futures Hedge. J. Appl. Econ. 1991, 6, 109–124. [Google Scholar] [CrossRef]

- Yu, H. The Implication of Currency Hedging Strategies for Pension Funds. Master’s Thesis, MSc Finance—Pension Track Tilburg University, Tilburg, The Netherlands, 2014. [Google Scholar]

- Arthur, J.N.; Williams, R.J.; Delfabbro, P.H. The conceptual and empirical relationship between gambling, investing, and speculation. J. Behav. Addict. 2016, 5, 580–591. [Google Scholar] [CrossRef] [Green Version]

- Benada, L. Hedging of Energy Commodities. Ph.D. Thesis, Masaryk University, Brno, Czech Republic, 2017. [Google Scholar]

- Pouliasis, P. Essays on the Empirical Analysis of Energy Risk. Ph.D. Thesis, Cass Business School, London, UK, 2011. [Google Scholar]

- Pennings, J.M.E. What Drives Actual Hedging Behaviour? Developing Risk Management Instruments. In Agribusiness and Commodity Risk: Strategies and Management; Risk Books: London, UK, 2003; pp. 63–74. [Google Scholar]

- Chen, S.S.; Lee, C.; Shrestha, K. Futures hedge ratios: A review. Quart. Rev. Econ. Financ. 2003, 43, 433–465. [Google Scholar] [CrossRef]

- Harris, R.D.F.; Stoja, E.; Tucker, J. A Simplified Approach to Modelling the Comovement of Asset Returns. J. Futures Mark. 2007, 27, 575–598. [Google Scholar] [CrossRef]

- Halkos, G.E.; Tsirivis, A.S. Effective energy commodity risk management: Econometric modeling of price volatility. Econ. Anal. Pol. 2019, 63, 234–250. [Google Scholar] [CrossRef]

- Alizadeh, A.H.; Nomikos, N.K.; Pouliasis, P.K. A Markov regime switching approach for hedging energy commodities. J. Bank. Financ. 2008, 32, 1970–1983. [Google Scholar] [CrossRef]

- Casillo, A. Model Specification for the Estimation of the Optimal Hedge Ratio with Stock Index Futures: An Application to the Italian Derivatives Market. Available online: www.luiss.it (accessed on 18 October 2019).

- Bollerslev, T.; Engle, R.F.; Wooldridge, J.M. A Capital Asset Pricing Model with Time-Varying Covariances. J. Polit. Econ. 1988, 96, 116–131. [Google Scholar] [CrossRef]

- Engle, R.F. Dynamic Conditional Correlation: A Simple Class of Multivariate Generalized Autoregressive Conditional Heteroskedasticity Models. J. Bus. Econ. Stat. 2002, 20, 339–350. [Google Scholar] [CrossRef]

- Manera, M.; McAleer, M.; Grasso, M. Modelling time-varying conditional correlations in the volatility of Tapis oil spot and forward returns. Appl. Financ. Econ. 2006, 16, 525–533. [Google Scholar] [CrossRef]

- Liu, S.D.; Jian, J.B.; Wang, Y.Y. Optimal dynamic hedging of electricity futures based on copula-GARCH models. In Proceedings of the 2010 IEEE International Conference on Industrial Engineering and Engineering Management, Macao, China, 7–10 December 2010; pp. 2498–2502. [Google Scholar]

- Zanotti, G.; Gabbi, G.; Geranio, M. Hedging with futures: Efficacy of GARCH correlation models to European electricity markets. J. Int. Financ. Mark. Inst. Money 2010, 20, 135–148. [Google Scholar] [CrossRef]

- Chang, C.-L.; McAleer, M.; Tansuchat, R. Crude oil hedging strategies using dynamic multivariate GARCH. Energy Econ. 2011, 33, 912–923. [Google Scholar] [CrossRef] [Green Version]

- Basher, S.A.; Sadorsky, P. Hedging emerging market stock prices with oil, gold, VIX, and bonds: A comparison between DCC, ADCC and GO-GARCH. Energy Econ. 2016, 54, 235–247. [Google Scholar] [CrossRef] [Green Version]

- Heisler, A. 7 Critical Risks Impacting the Energy Industry. Risk & Insurance. Available online: www.riskandinsurance.com (accessed on 5 July 2019).

- Cotter, J.; Hanly, J. Time-varying risk aversion: An application to energy hedging. Energy Econ. 2010, 32, 432–441. [Google Scholar] [CrossRef] [Green Version]

- Al Janabi, M.A.M. Commodity price risk management: Valuation of large trading portfolios under adverse and illiquid market settings. J. Deriv. Hedge Funds 2009, 15, 15–50. [Google Scholar] [CrossRef] [Green Version]

- Georgescu-Roegen, N. Choice, Expectations and Measurability. Quart. J. Econ. 1954, 68, 503–534. [Google Scholar] [CrossRef]

- Georgescu-Roegen, N. Utility. Int. Encycl. Soc. Sci. 1968, 16, 236–267. [Google Scholar]

- Georgescu-Roegen, N. The Entropy Law and the Economic Process. East. Econ. J. 1971, 12. [Google Scholar]

- Byrne, J.; Taminiau, J. A review of sustainable energy utility and energy service utility concepts and applications: Realizing ecological and social sustainability with a community utility. WIREs Energy Environ. 2016, 5, 136–154. [Google Scholar] [CrossRef]

- Fox-Penner, P. The Smart Grid–Enabled Energy Services Utility: How Utilities Can Become Sustainable by Selling Less. Solutions 2010, 1, 42–48. [Google Scholar]

- MIT. Utility of the Future. 2016, An MIT Energy Initiative Response to an Industry in Transition. Available online: energy.mit.edu (accessed on 9 July 2019).

- Howard, C.T.; D’Antonio, L.J. A Risk-Return Measure of Hedging Effectiveness. J. Financ. Quant. Anal. 1984, 19, 101. [Google Scholar] [CrossRef]

- Kolb, R.W.; Okunev, J. An empirical evaluation of the extended mean-gini coefficient for futures hedging. J. Futures Mark. 1992, 12, 177–186. [Google Scholar] [CrossRef]

- Lien, D.; Luo, X. Estimating the extended mean-gini coefficient for futures hedging. J. Futures Mark. 1993, 13, 665–676. [Google Scholar] [CrossRef]

- Gregory-Allen, R.B.; Shalit, H. The Estimation of Systematic Risk under Differentiated Risk Aversion: A Mean-Extended Gini Approach. Rev. Quant. Financ. Account. 1999, 12, 135–158. [Google Scholar] [CrossRef]

- Kolb, R.W.; Okunev, J. Utility maximizing hedge ratios in the extended mean gini framework. J. Futures Mark. 1993, 13, 597–609. [Google Scholar] [CrossRef]

- Shalit, H. Mean-Gini hedging in futures markets. J. Futures Mark. 1995, 15, 617–635. [Google Scholar] [CrossRef]

- De Jong, A.; De Roon, F.; Veld, C. Out-of-sample hedging effectiveness of currency futures for alternative models and hedging strategies. J. Futures Mark. 1997, 17, 817–837. [Google Scholar] [CrossRef]

- Lien, D.; Tse, Y.K. Hedging time-varying downside risk. J. Futures Mark. 1998, 18, 705–722. [Google Scholar] [CrossRef]

- Lien, D.; Tse, Y.K. Hedging downside risk with futures contracts. Appl. Financ. Econ. 2000, 10, 163–170. [Google Scholar] [CrossRef]

- Chen, S.-S.; Lee, C.-F.; Shrestha, K. On a Mean—Generalized Semivariance Approach to Determining the Hedge Ratio. J. Futures Mark. 2001, 21, 581–598. [Google Scholar] [CrossRef]

- Kleindorfer, P.R.; Li, L. Multi-Period VaR-Constrained Portfolio Optimization with Applications to the Electric Power Sector. Energy J. 2005, 26, 1–26. [Google Scholar] [CrossRef]

- Oum, Y.; Oren, S. VaR constrained hedging of fixed price load-following obligations in competitive electricity markets. Risk Dec. Anal. 2009, 1, 43–56. [Google Scholar] [Green Version]

- Jalali-Naini, A.R.; Manesh, M.K. Price volatility, hedging and variable risk premium in the crude oil market. OPEC Rev. 2006, 30, 55–70. [Google Scholar] [CrossRef]

- Ji, Q.; Fan, Y. A dynamic hedging approach for refineries in multiproduct oil markets. Energy 2011, 36, 881–887. [Google Scholar] [CrossRef]

- Ghoddusi, H.; Emamzadehfard, S. Optimal hedging in the US natural gas market: The effect of maturity and cointegration. Energy Econ. 2017, 63, 92–105. [Google Scholar] [CrossRef]

- Cotter, J.; Hanly, J. Performance of utility based hedges. Energy Econ. 2015, 49, 718–726. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Commodity Name | Monthly Volatility (Normal Market) (%) | Monthly Volatility (Crisis Market) (%) | Annual Volatility (Normal Market) (%) | Annual Volatility (Crisis Market) (%) | Sensitivity Factors |

|---|---|---|---|---|---|

| Petroleum: average crude price | 8.1 | 24.6 | 28.1 | 85.2 | 1.72 |

| Gasoline | 10.4 | 25.4 | 30.4 | 87.2 | 1.88 |

| Natural gas | 5.8 | 20.6 | 20.0 | 71.2 | 0.14 |

| Coal | 4.0 | 13.5 | 13.9 | 46.9 | 0.26 |

| Gold | 3.3 | 12.5 | 11.3 | 43.2 | 0.18 |

| Silver | 5.4 | 21.6 | 18.7 | 75.0 | 0.18 |

| Copper | 6.2 | 20.0 | 21.5 | 69.2 | 0.48 |

| Zinc | 6.1 | 24.9 | 21.3 | 86.4 | 0.34 |

| Lead | 6.3 | 23.8 | 21.9 | 82.3 | 0.15 |

| Aluminum | 5.8 | 32.6 | 20.0 | 133.1 | 0.31 |

| Nickel | 8.9 | 22.2 | 30.7 | 76.9 | 0.54 |

| Iron ore | 4.4 | 12.9 | 15.2 | 44.7 | 0.18 |

| Phosphate rock | 2.3 | 21.7 | 8.1 | 75.2 | 0.01 |

| Wheat | 5.1 | 15.1 | 17.7 | 52.3 | 0.08 |

| Cotton | 4.9 | 12.6 | 17.0 | 43.5 | 0.14.9 |

| Sugar | 2.1 | 11.0 | 7.3 | 38.2 | −0.05 |

| Maize | 5.3 | 25.2 | 18.4 | 87.2 | −0.08 |

| Tobacco | 1.8 | 4.9 | 6.2 | 16.8 | 0.01 |

| Coffee | 8.0 | 37.1 | 27.6 | 128.6 | 0.04 |

| Tea | 7.7 | 23.6 | 26.8 | 81.8 | 0.11 |

| Rubber | 6.0 | 18.1 | 20.8 | 62.7 | 0.37 |

| Wool | 4.7 | 16.5 | 16.4 | 57.3 | −0.02 |

| All commodities | 3.6 | 12.3 | 12.5 | 42.5 | 1.00 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Halkos, G.E.; Tsirivis, A.S. Energy Commodities: A Review of Optimal Hedging Strategies. Energies 2019, 12, 3979. https://doi.org/10.3390/en12203979

Halkos GE, Tsirivis AS. Energy Commodities: A Review of Optimal Hedging Strategies. Energies. 2019; 12(20):3979. https://doi.org/10.3390/en12203979

Chicago/Turabian StyleHalkos, George E., and Apostolos S. Tsirivis. 2019. "Energy Commodities: A Review of Optimal Hedging Strategies" Energies 12, no. 20: 3979. https://doi.org/10.3390/en12203979

APA StyleHalkos, G. E., & Tsirivis, A. S. (2019). Energy Commodities: A Review of Optimal Hedging Strategies. Energies, 12(20), 3979. https://doi.org/10.3390/en12203979