Modeling Intraday Markets under the New Advances of the Cross-Border Intraday Project (XBID): Evidence from the German Intraday Market

Abstract

:1. Introduction

2. Cross-Border Trading in the German Intraday Market under XBID

2.1. Market Integration in European Short-Term Energy Markets

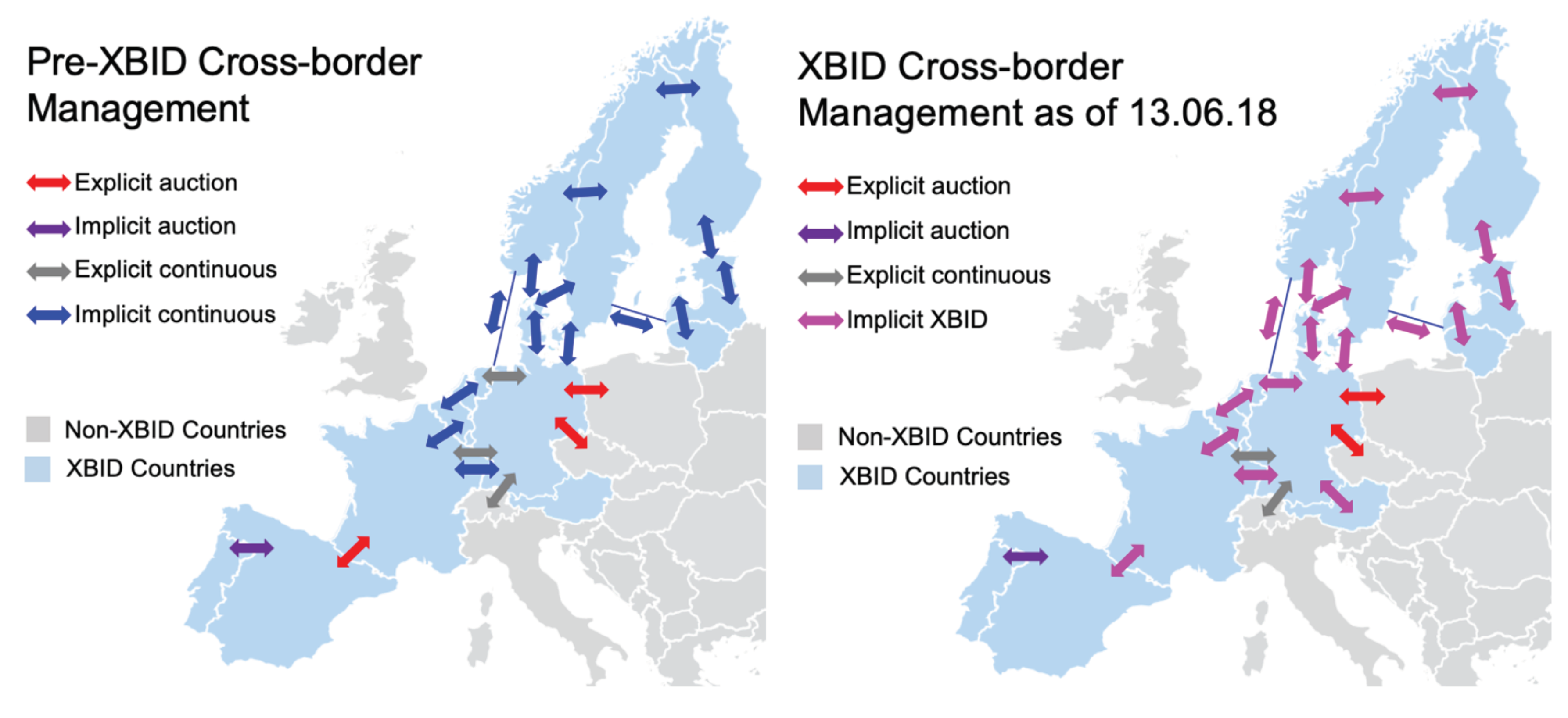

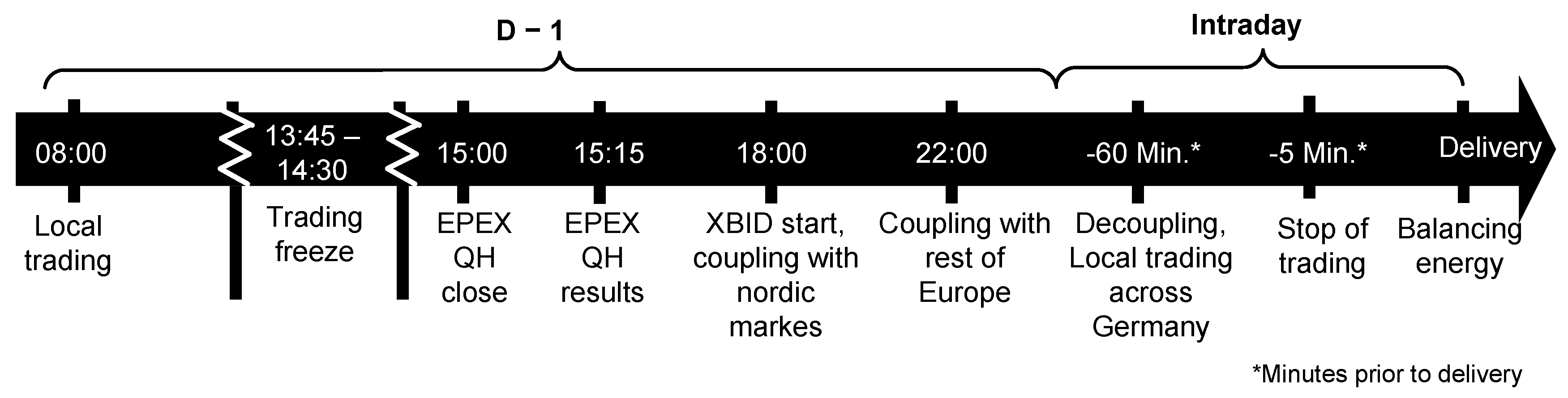

2.2. XBID as a Particular Enhancement of Market Integration

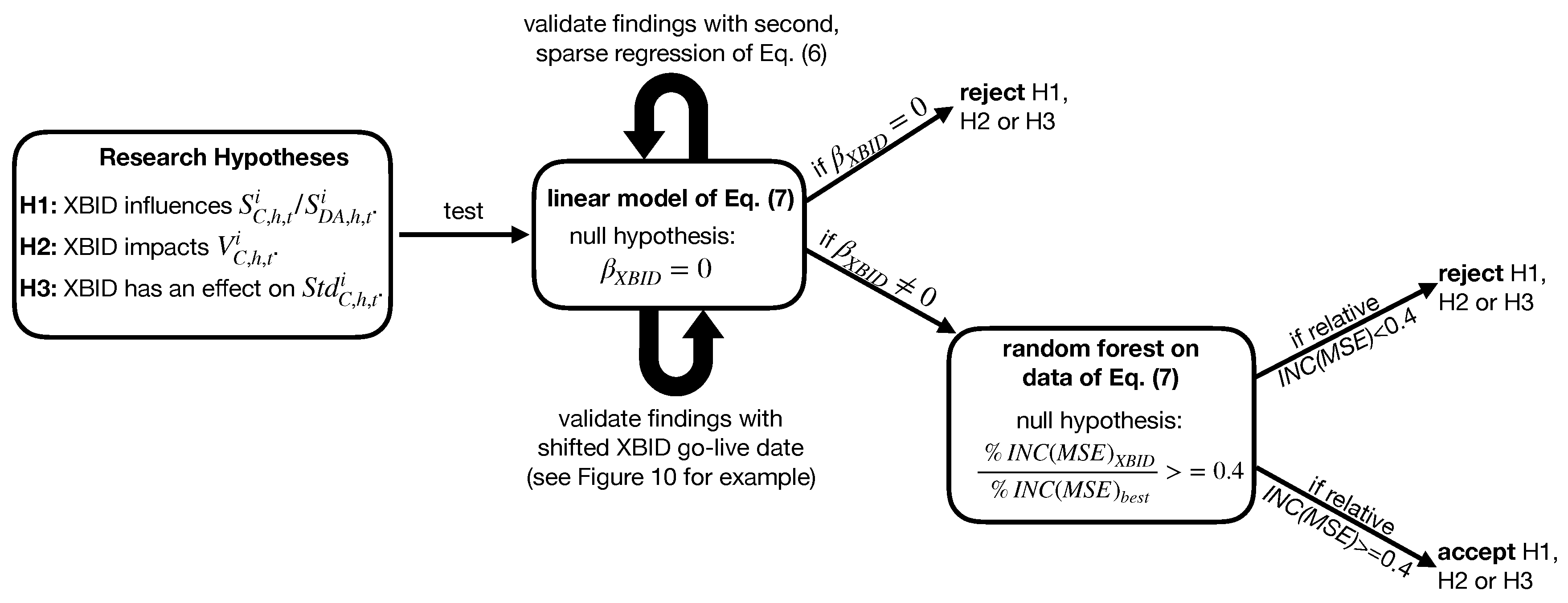

2.3. Connected Research Hypotheses and Associated Empirical Framework

3. Data and Aggregation Methodology

3.1. The Necessity to Aggregate Deal Information in Intraday Markets

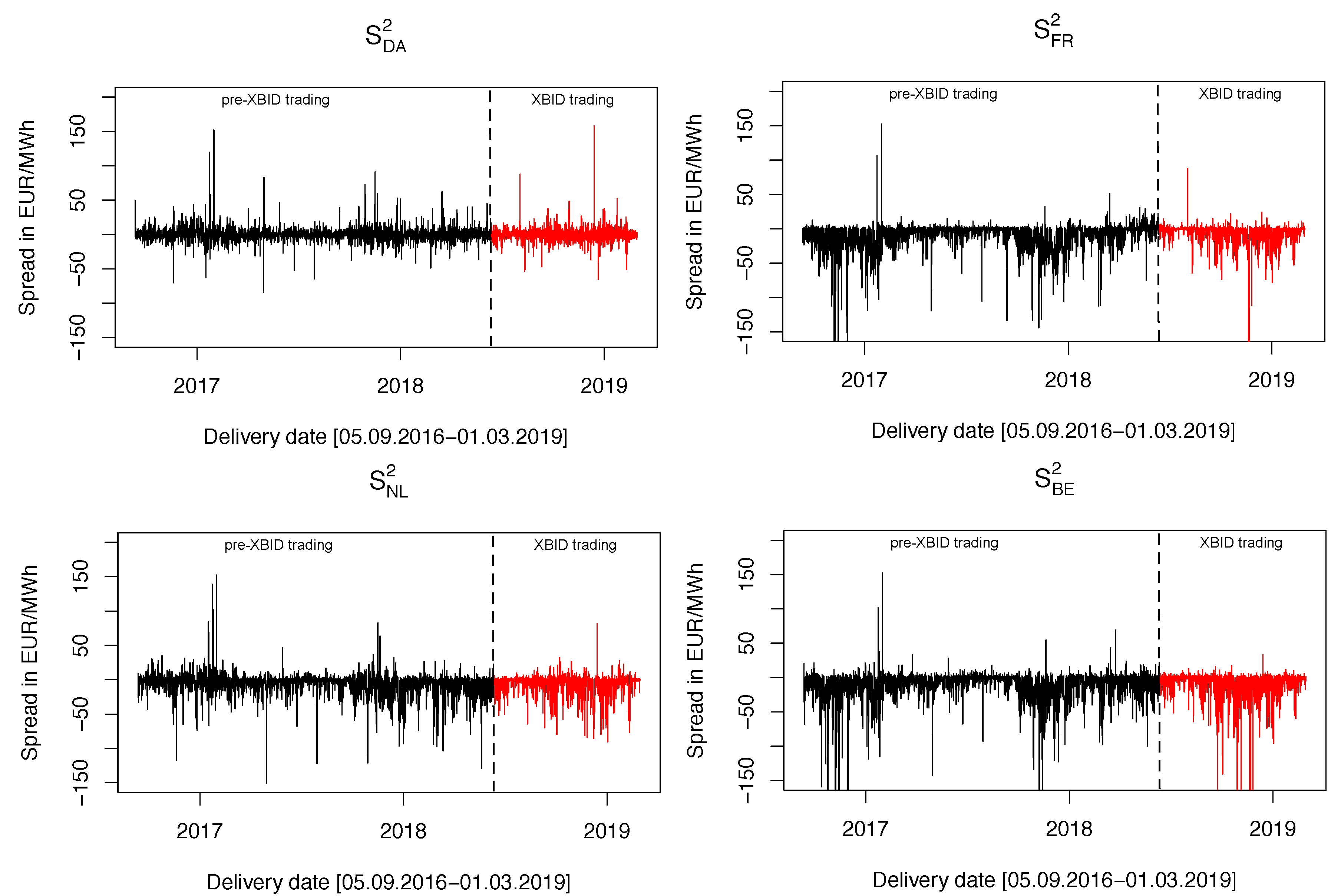

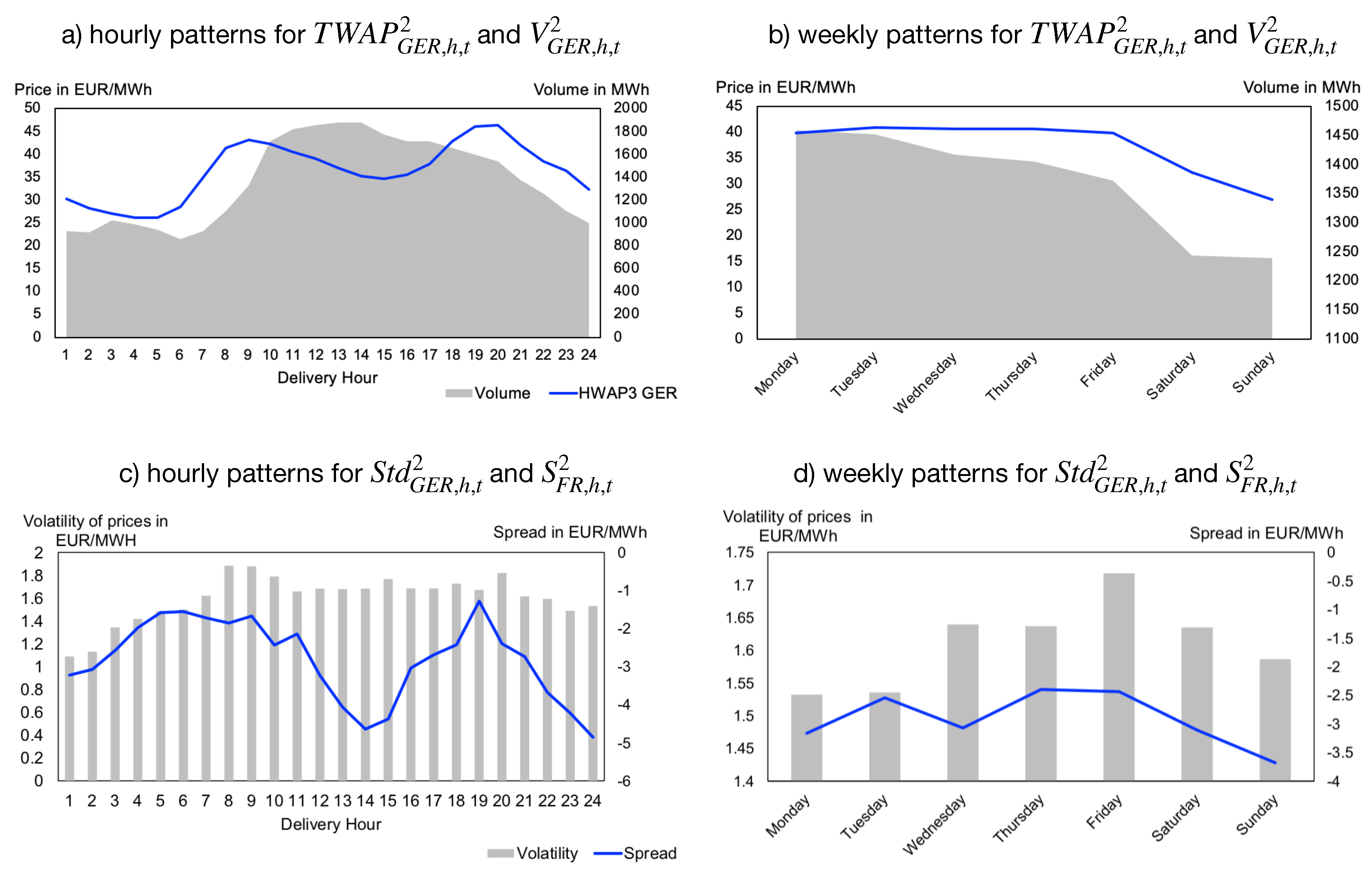

3.2. Data: Applied Intraday Prices

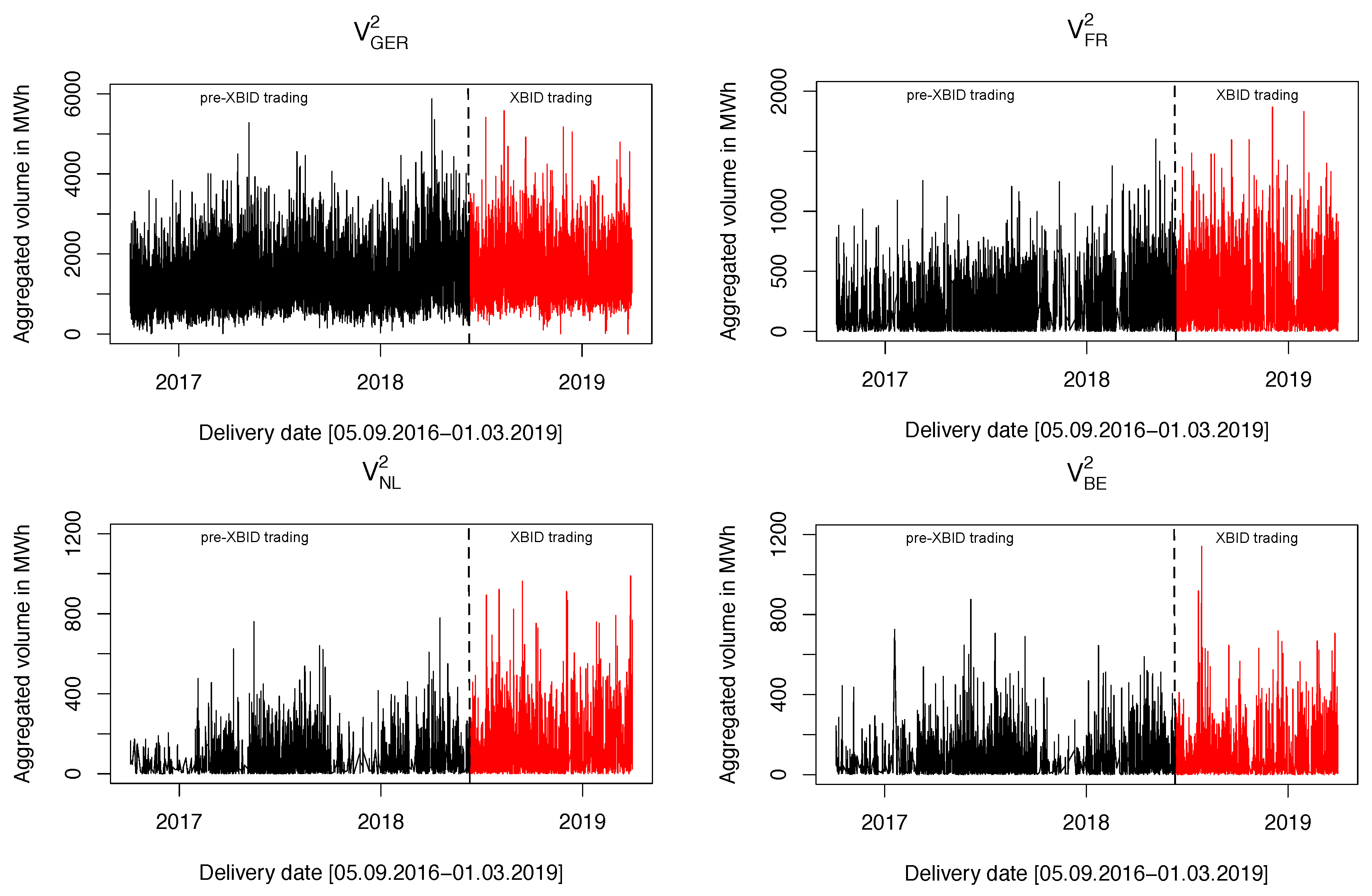

3.3. Data: Aggregated Cross-Border Volumes

3.4. Data: Intraday Volatility of Cross-Border Trades

3.5. Explanatory Variables to Model Intraday Trades

3.6. Pre-Processing and Transformations of Intraday Data

3.7. The Overall Regression Matrix to Explain Intraday Transactions

4. XBID Influence Modeled in a Linear Set-Up

4.1. A Heteroscedasticity-Robust Linear Model to Capture XBID Importance

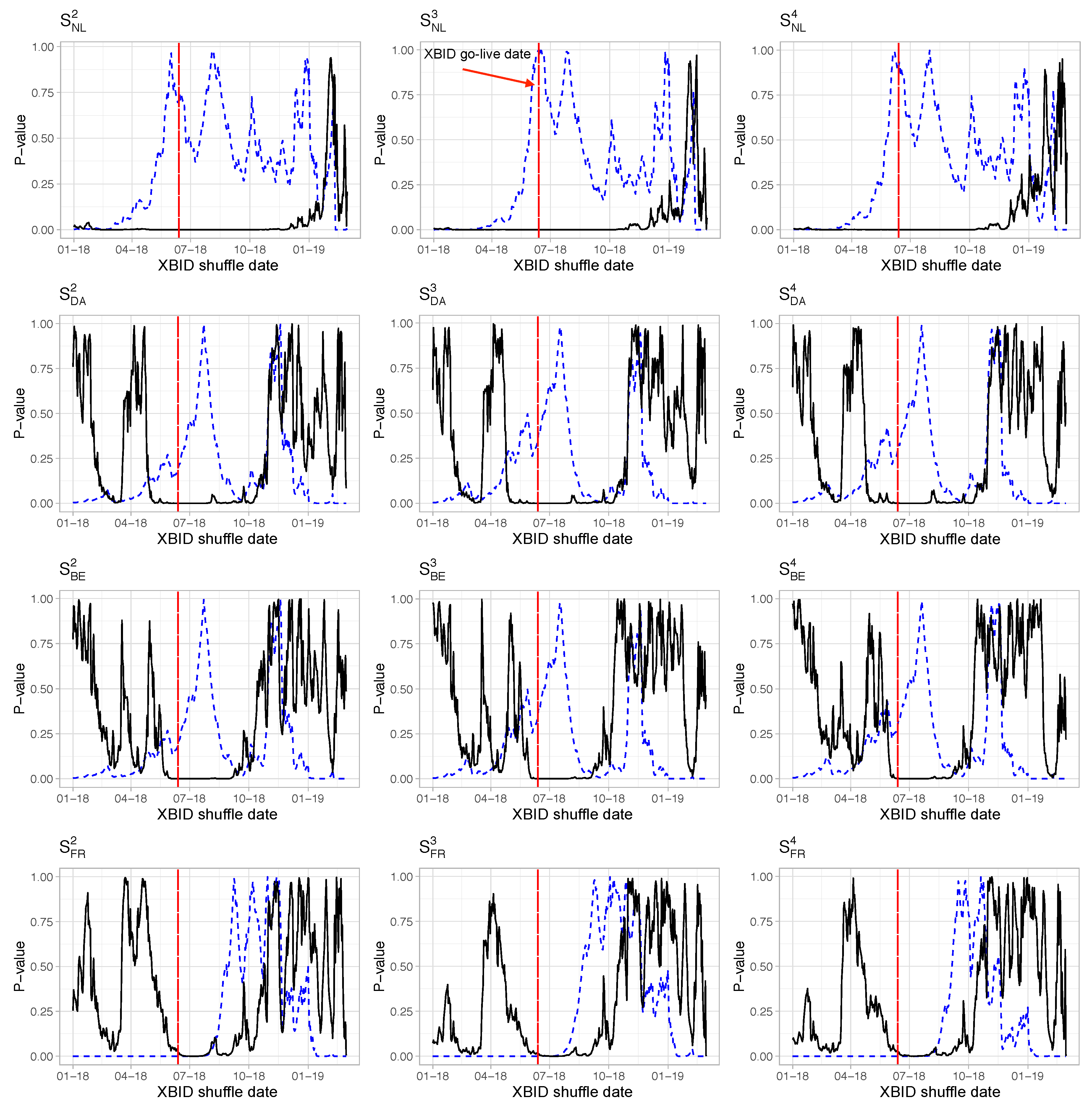

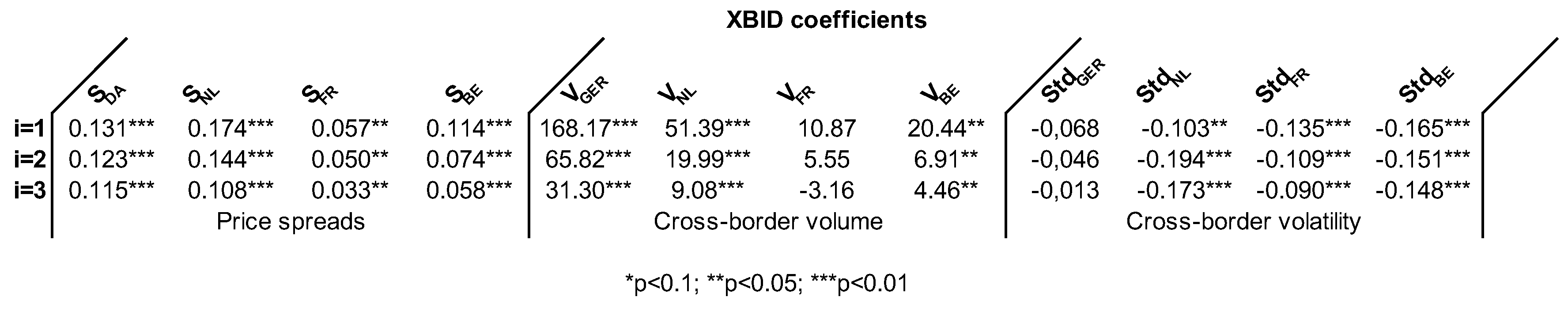

4.2. XBID Dummy Variables and their Effects in Price Spread Regression

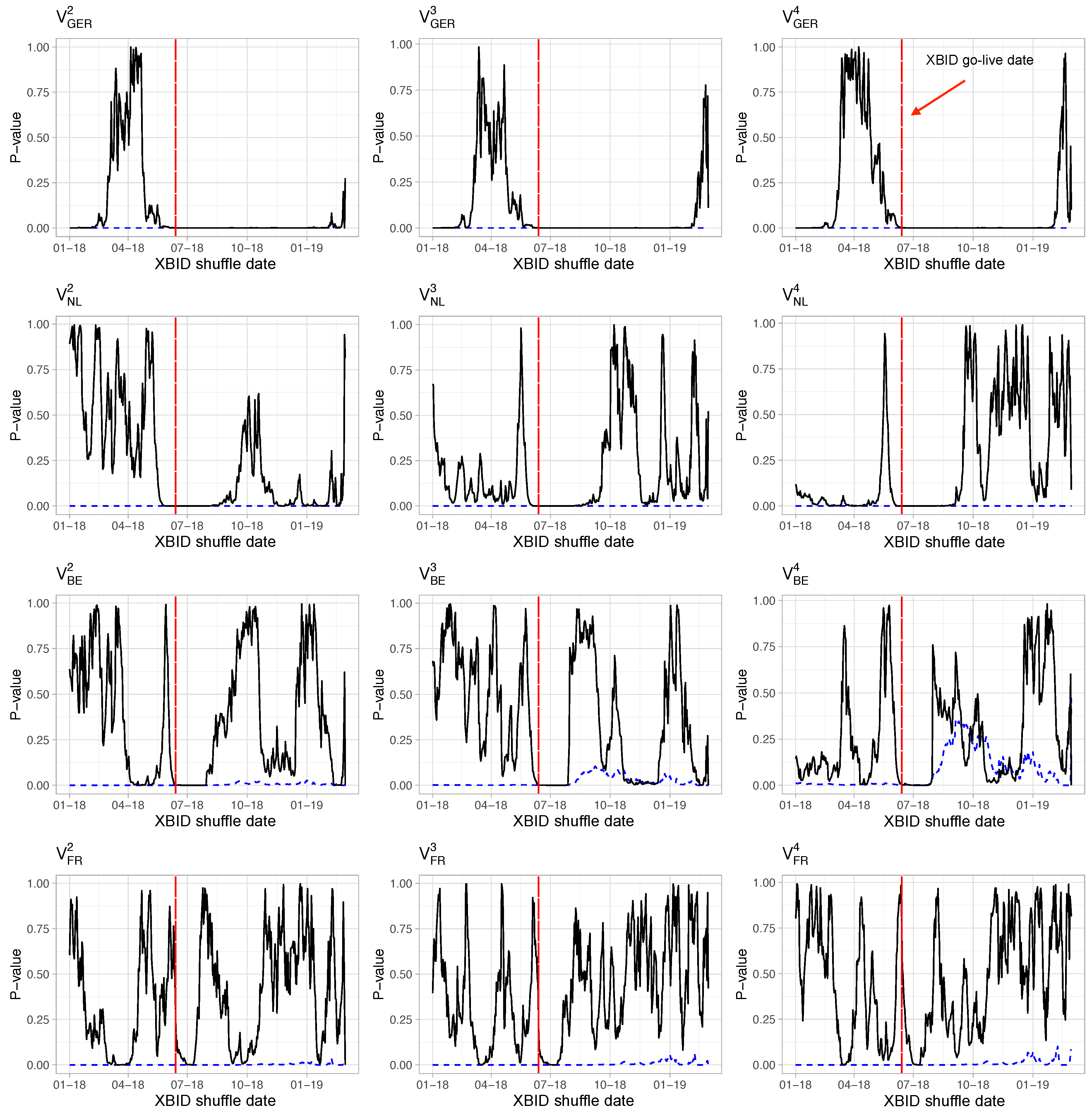

4.3. XBID Coefficients in Intraday Volume Regressions

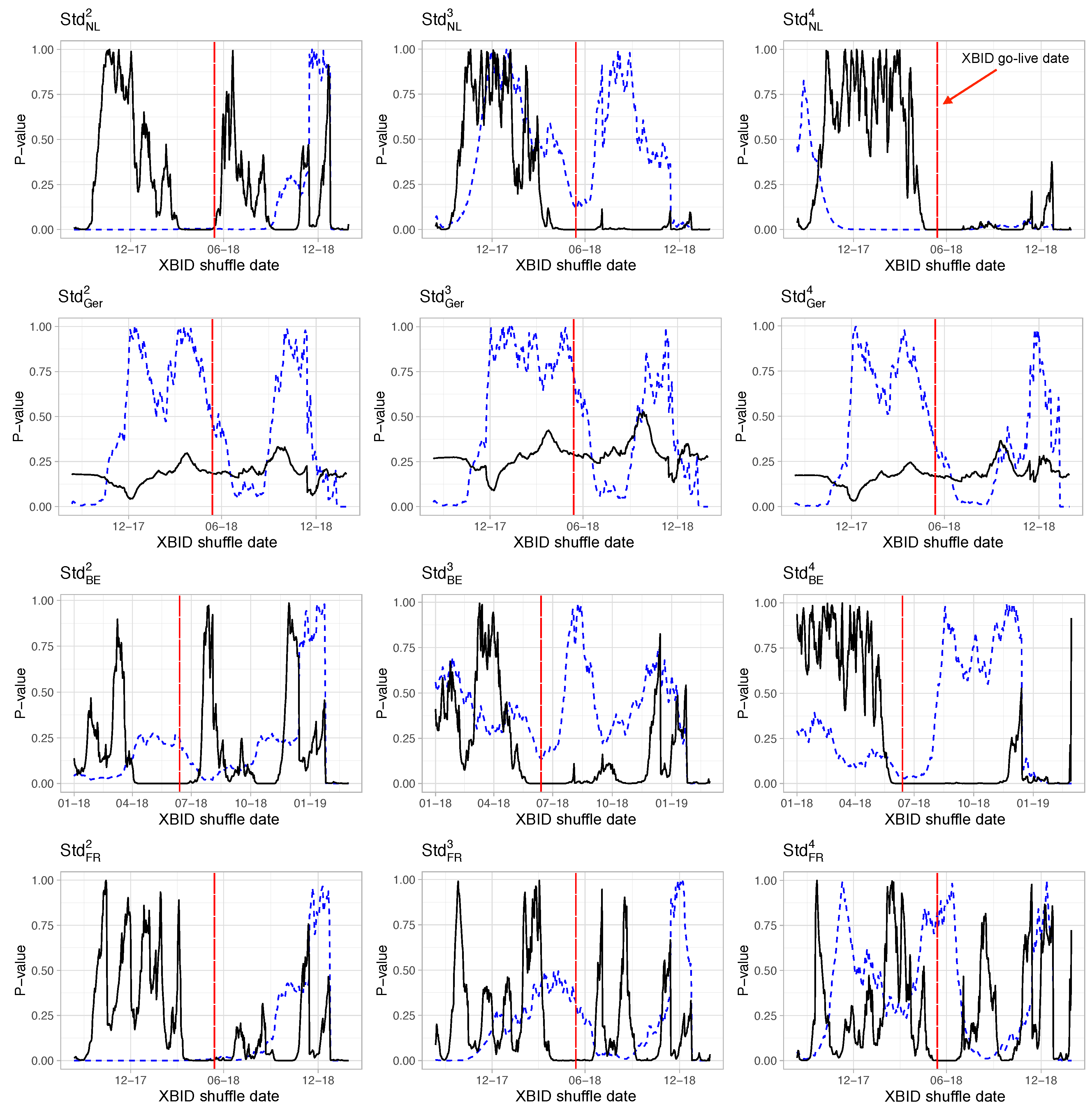

4.4. Impact on Intraday Volatility

5. XBID in a Non-Linear Variable Importance Scheme

5.1. Random Forest Permutation Importance

5.2. XBID Importance in Modeling Intraday Price Spreads

5.3. XBID Importance in Modeling Cross-Border Volumes

5.4. XBID Importance in Modeling Cross-Border Volatility

6. Contribution and Outlook

6.1. Conclusions

6.2. Outlook and Possible Policy Implication

Supplementary Materials

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Regression Results for

Appendix B. Regression Results for

Appendix C. Regression Results for

Appendix D. Regression Results for

References

- Garnier, E.; Madlener, R. Balancing forecast errors in continuous-trade intraday markets. Energy Syst. 2015, 6, 361–388. [Google Scholar] [CrossRef]

- Aïd, R.; Gruet, P.; Pham, H. An optimal trading problem in intraday electricity markets. Math. Financ. Econ. 2016, 10, 49–85. [Google Scholar] [CrossRef]

- Kiesel, R.; Paraschiv, F. Econometric analysis of 15-minute intraday electricity prices. Energy Econ. 2017, 64, 77–90. [Google Scholar] [CrossRef]

- Pape, C.; Hagemann, S.; Weber, C. Are fundamentals enough? Explaining price variations in the German day-ahead and intraday power market. Energy Econ. 2016, 54, 376–387. [Google Scholar] [CrossRef]

- Andrade, J.; Filipe, J.; Reis, M.; Bessa, R. Probabilistic price forecasting for day-ahead and intraday markets: Beyond the statistical model. Sustainability 2017, 9, 1990. [Google Scholar] [CrossRef]

- Monteiro, C.; Ramirez-Rosado, I.; Fernandez-Jimenez, L.; Conde, P. Short-term price forecasting models based on artificial neural networks for intraday sessions in the iberian electricity market. Energies 2016, 9, 721. [Google Scholar] [CrossRef]

- Uniejewski, B.; Marcjasz, G.; Weron, R. Understanding intraday electricity markets: Variable selection and very short-term price forecasting using LASSO. Int. J. Forecast. 2019, 35, 1533–1547. [Google Scholar] [CrossRef]

- Narajewski, M.; Ziel, F. Econometric modelling and forecasting of intraday electricity prices. arXiv 2018, arXiv:1812.09081. [Google Scholar] [CrossRef]

- Kristiansen, T. A preliminary assessment of the market coupling arrangement on the Kontek cable. Energy Policy 2007, 35, 3247–3255. [Google Scholar] [CrossRef]

- Oggioni, G.; Smeers, Y. Market failures of Market Coupling and counter-trading in Europe: An illustrative model based discussion. Energy Econ. 2013, 35, 74–87. [Google Scholar] [CrossRef]

- Hagemann, S. Price determinants in the German intraday market for electricity: An empirical analysis. J. Energy Mark. 2015, 8, 21–45. [Google Scholar] [CrossRef]

- Ziel, F.; Steinert, R.; Husmann, S. Forecasting day ahead electricity spot prices: The impact of the EXAA to other European electricity markets. Energy Econ. 2015, 51, 430–444. [Google Scholar] [CrossRef]

- Panapakidis, I.P.; Dagoumas, A.S. Day-ahead electricity price forecasting via the application of artificial neural network based models. Appl. Energy 2016, 172, 132–151. [Google Scholar] [CrossRef]

- Lago, J.; De Ridder, F.; De Schutter, B. Forecasting spot electricity prices: Deep learning approaches and empirical comparison of traditional algorithms. Appl. Energy 2018, 221, 386–405. [Google Scholar] [CrossRef]

- Lago, J.; De Ridder, F.; Vrancx, P.; De Schutter, B. Forecasting day-ahead electricity prices in Europe: The importance of considering market integration. Appl. Energy 2018, 211, 890–903. [Google Scholar] [CrossRef]

- Zachmann, G. Electricity wholesale market prices in Europe: Convergence? Energy Econ. 2008, 30, 1659–1671. [Google Scholar] [CrossRef]

- Amprion GmbH. French/German Interconnectiion Intraday Capacity Explicit Allocation Rules. 2019. Available online: https://www.amprion.net/Dokumente/Strommarkt/Engpassmanagement/XBID-Project/Sonstiges/ifd_rules.pdf (accessed on 4 April 2019).

- EPEX Spot SE. Cross-Border Intraday: Questions and Answers. 2018. Available online: https://www.epexspot.com/document/40068/XBID%20Q%26A (accessed on 4 April 2019).

- ENTSO-E. First Edition of the Bidding Zone Review. 2018. Available online: https://docstore.entsoe.eu/Documents/News/bz-review/2018-03_First_Edition_of_the_Bidding_Zone_Review.pdf (accessed on 6 April 2019).

- Commission, E. COMMISSION REGULATION (EU) 2015/1222 Establishing a Guideline on Capacity Allocation and Congestion Management. 2015. Available online: https://eur-lex.europa.eu/legal-content/DE/TXT/?uri=CELEX%3A32015R1222 (accessed on 4 April 2019).

- Popper, K.R. Science as falsification. Conjectures Refutations 1963, 1, 33–39. [Google Scholar]

- Hagemann, S.; Weber, C. Trading Volumes in Intraday Markets: Theoretical Reference Model and Empirical Observations in Selected European Markets; Technical Report, HEMF Working Papers, Chair for Management Science and Energy Economics, House of Energy Markets & Finance; University of Duisburg-Essen: Essen, Germany, 2015. [Google Scholar]

- Weber, C. Adequate intraday market design to enable the integration of wind energy into the European power systems. Energy Policy 2010, 38, 3155–3163. [Google Scholar] [CrossRef]

- Janke, T.; Steinke, F. Forecasting the Price Distribution of Continuous Intraday Electricity Trading. Energies 2019, 12, 4262. [Google Scholar] [CrossRef]

- Bundesnetzagentur. Kraftwerksliste der Bundesnetzagentur- March 2019. Available online: https://www.bundesnetzagentur.de/DE/Sachgebiete/ElektrizitaetundGas/Unternehmen_Institutionen/Versorgungssicherheit/Erzeugungskapazitaeten/Kraftwerksliste/kraftwerksliste-node.html (accessed on 9 May 2019).

- De Vos, K. Negative wholesale electricity prices in the German, French and Belgian day-ahead, intra-day and real-time markets. Electr. J. 2015, 28, 36–50. [Google Scholar] [CrossRef]

- Uniejewski, B.; Weron, R.; Ziel, F. Variance stabilizing transformations for electricity spot price forecasting. IEEE Trans. Power Syst. 2018, 33, 2219–2229. [Google Scholar] [CrossRef]

- Hoaglin, D.C.; John, W. Tukey and data analysis. Stat. Sci. 2003, 18, 311–318. [Google Scholar]

- Buuren, S.; Groothuis-Oudshoorn, K. mice: Multivariate imputation by chained equations in R. J. Stat. Softw. 2011, 45, 1–67. [Google Scholar] [CrossRef]

- Weron, R. Modeling and Forecasting Electricity Loads and Prices: A Statistical Approach; John Wiley & Sons: Hoboken, NJ, USA, 2007; Volume 403. [Google Scholar]

- Ziel, F.; Weron, R. Day-ahead electricity price forecasting with high-dimensional structures: Univariate vs. multivariate modeling frameworks. Energy Econ. 2018, 70, 396–420. [Google Scholar] [CrossRef]

- Chow, G.C. Tests of equality between sets of coefficients in two linear regressions. Econom. J. Econom. Soc. 1960, 28, 591–605. [Google Scholar] [CrossRef]

- Binder, J. The event study methodology since 1969. Rev. Quant. Financ. Account. 1998, 11, 111–137. [Google Scholar] [CrossRef]

- Valitov, N. Risk premia in the German day-ahead electricity market revisited: The impact of negative prices. Energy Econ. 2018. in Press. [Google Scholar] [CrossRef]

- Newey, W.K.; West, K.D. Automatic lag selection in covariance matrix estimation. Rev. Econ. Stud. 1994, 61, 631–653. [Google Scholar] [CrossRef]

- Newey, W.K.; West, K.D. A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 1987, 55, 703–708. [Google Scholar] [CrossRef]

- Zeileis, A. Econometric computing with HC and HAC covariance matrix estimators. J. Stat. Softw. 2004, 11, 1–17. [Google Scholar] [CrossRef]

- Dickey, D.A.; Fuller, W.A. Distribution of the estimators for autoregressive time series with a unit root. J. Am. Stat. Assoc. 1979, 74, 427–431. [Google Scholar]

- Kwiatkowski, D.; Phillips, P.C.; Schmidt, P.; Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? J. Econom. 1992, 54, 159–178. [Google Scholar] [CrossRef]

- Durbin, J.; Watson, G.S. Testing for serial correlation in least squares regression. III. Biometrika 1971, 58, 1–19. [Google Scholar] [CrossRef]

- Breusch, T.S.; Pagan, A.R. A simple test for heteroscedasticity and random coefficient variation. Econ. J. Econ. Soc. 1979, 47, 1287–1294. [Google Scholar] [CrossRef]

- Nathans, L.L.; Oswald, F.L.; Nimon, K. Interpreting multiple linear regression: A guidebook of variable importance. Pract. Assess. Res. Eval. 2012, 17, 1–19. [Google Scholar]

- Breiman, L. Random forests. Mach. Learn. 2001, 45, 5–32. [Google Scholar] [CrossRef] [Green Version]

- Liaw, A.; Wiener, M. Classification and regression by randomForest. R News 2002, 2, 18–22. [Google Scholar]

- TGE. Single Intraday Coupling (SIDC). 2019. Available online: https://tge.pl/pub/TGE/files/MC/SIDC_XBID_2nd_Wave_Pre_Launch.2019.pdf (accessed on 8 November 2019).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | AT | FR | NL | CZ | CH | DK | PL | SWE |

|---|---|---|---|---|---|---|---|---|

| Import from GER in GWh | 36.760 | 14.784 | 15.162 | 6.002 | 9.534 | 6.289 | 1.885 | 0.468 |

| Import to GER in GWh | 11.583 | 6.445 | 0.628 | 8.181 | 5.255 | 6.413 | 1.003 | 1.308 |

| Dimension | Data Selection | Condition |

|---|---|---|

| Intraday spreads | price, volume | |

| Cross-border volumes | volume | |

| Cross-border volatility | price, volume |

| Min | 1st Quantile | Mean | 3rd Quantile | Max | Std.Dev. | |

|---|---|---|---|---|---|---|

| −83.99 | 0 | 0.09 | 3.58 | 158.21 | 8.54 | |

| −650.02 | −15.97 | −10.82 | 0.03 | 158.46 | 20.4 | |

| −150.51 | −9.16 | −5.71 | 0.43 | 152.46 | 13.6 | |

| −820.18 | −14.42 | −9.11 | 0.06 | 152.46 | 18.3 |

| Determinant | Unit/granularity | Description | Data Source | Transformation |

|---|---|---|---|---|

| EPEX day-ahead auction price | EUR/MWh, hourly | Market clearing price of the EPEX day-ahead auction | European Power Exchange (EPEX), https://www.epexspot.com/en/ | mlog |

| foreign day-ahead price | EUR/MWh, hourly | Market clearing price for Denmark, Poland, France, Belgium, Switzerland, Czech Republic and Sweden. All prices obtained in a day-ahead auction | European Network of Transmission System Operators (ENTSO-E), https://transparency.entsoe.eu/ | mlog |

| EPEX intraday transactions | EUR/MWh, hourly | EPEX public trades to derive TWAPs, volume or volatility from | European Power Exchange (EPEX), https://www.epexspot.com/en/ | mlog |

| ENTSO-E flow | EUR/MWh, hourly | Scheduled commercial exchanges per country, published ex-post | European Network of Transmission System Operators (ENTSO-E), https://transparency.entsoe.eu/ | - |

| ENTSO-E load | MW, quarter-hourly | Vertical system load for bidding zone Germany/Austria, published around 10:00 d-1 | European Network of Transmission System Operators (ENTSO-E), https://transparency.entsoe.eu/ | mlog, sum of QH for one hour |

| TSO PV and wind forecast | MW, hourly | Photovoltaics (PV) and wind production forecast for Germany published by transmission system operators (TSO) at 8:00 d-1 | European Energy Exchange (EEX), https://www.eex-transparency.com/ | mlog |

| EUA future price | EUR/ton, daily | EEX EUA front-year future, closing price of each day | European Energy Exchange (EEX), https://www.eex.com/de/ | mlog |

| Coal future price | USD/ton, daily | ICE API2 Rotterdam front-month coal future, settlement price | Intercontinental Exchange (ICE), https://www.theice.com/index | mlog |

| Gas future price | EUR/MWh, daily | EEX Gaspool front-month gas future, settlement price | PEGAS https://www.powernext.com/ | mlog |

| ADF test | 0.01 | <0.01 | <0.01 | <0.001 | 0.01 | 0.01 |

| KPSS test | 0.1 | 0.01 | <0.01 | 0.01 | <0.001 | <0.001 |

| Durbin-Watson test | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 |

| Breusch-Pagan test | <0.001 | <0.001 | 0.005 | 0.008 | <0.001 | <0.001 |

| F-Statistics | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 |

| Rank (x of 46) | ||||

|---|---|---|---|---|

| 1 | GER DA PRC (26%) | NL DA PRC (117%) | FR DA PRC (154%) | BE DA PRC (427%) |

| 2 | DK–>GER (22%) | GER DA PRC (108%) | FR–>GER (102%) | FR–>GER (79%) |

| 3 | CH DA PRC (20%) | CZ DA PRC (30%) | CH DA PRC (55%) | GER DA PRC (74%) |

| 4 | GER–>DK (20%) | Wind FC (29%) | BE DA PRC (53%) | FR DA PRC (66%) |

| 5 | BE DA PRC (13%) | lagged PV FC (27%) | GER DA PRC (41%) | CH DA PRC (60%) |

| rank XBID | 46/(0.3%) | 45/(1.3%) | 39/(2.1%) | 45/(0.8%) |

| Rank (x of 46) | ||||

|---|---|---|---|---|

| 1 | FR–>GER (66 512%) | XBID (1 841%) | NL–>GER 1 759%) | FR–>GER (26 997%) |

| 2 | CH–>GER (31 341%) | EUA PRC (1 779%) | Load BE (1 010%) | CH–>GER (6 114%) |

| 3 | EUA PRC (21 4229%) | NL–>GER 1 750%) | DK DA PRC (851%) | GER DA PRC (75 244%) |

| 4 | AT–>GER (19 537%) | FR–>GER (19 537%) | BE DA PRC (762%) | FR DA PRC (4 556%) |

| 5 | DK DA PRC (15 921%) | GER DA PRC (1 218%) | GER DA PRC (729%) | DK DA PRC (4 190%) |

| rank XBID | 7/(14 447%) | 1/(1 841%) | 39/(653%) | 37/(132%) |

| Rank (x of 46) | ||||

|---|---|---|---|---|

| 1 | FR–>GER (3.3%) | GER DA PRC (0.9%) | GER DA PRC (1.2%) | GER DA PRC (0.6%) |

| 2 | CH–>GER (2.1%) | CZ DA PRC (0.8%) | BE DA PRC (0.7%) | Load DK (0.4%) |

| 3 | EUA PRC (1.6%) | Load CZ (0.7%) | FR DA PRC (0.6%) | BE DA PRC (0.4%) |

| 4 | Wind FC(1.1%) | Load DK (0.6%) | CH DA PRC (0.4%) | FR DA PRC (0.3%) |

| 5 | lagged PV Forecast FC (1%) | DK DA PRC (0.4%) | FR–>GER (0.3%) | CH DA PRC (0.2%) |

| rank XBID | 44/(0.3%) | 41/(0.01%) | 29/(0.03%) | 35/(0.02%) |

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kath, C. Modeling Intraday Markets under the New Advances of the Cross-Border Intraday Project (XBID): Evidence from the German Intraday Market. Energies 2019, 12, 4339. https://doi.org/10.3390/en12224339

Kath C. Modeling Intraday Markets under the New Advances of the Cross-Border Intraday Project (XBID): Evidence from the German Intraday Market. Energies. 2019; 12(22):4339. https://doi.org/10.3390/en12224339

Chicago/Turabian StyleKath, Christopher. 2019. "Modeling Intraday Markets under the New Advances of the Cross-Border Intraday Project (XBID): Evidence from the German Intraday Market" Energies 12, no. 22: 4339. https://doi.org/10.3390/en12224339

APA StyleKath, C. (2019). Modeling Intraday Markets under the New Advances of the Cross-Border Intraday Project (XBID): Evidence from the German Intraday Market. Energies, 12(22), 4339. https://doi.org/10.3390/en12224339