Infectious Diseases, Market Uncertainty and Oil Market Volatility

Abstract

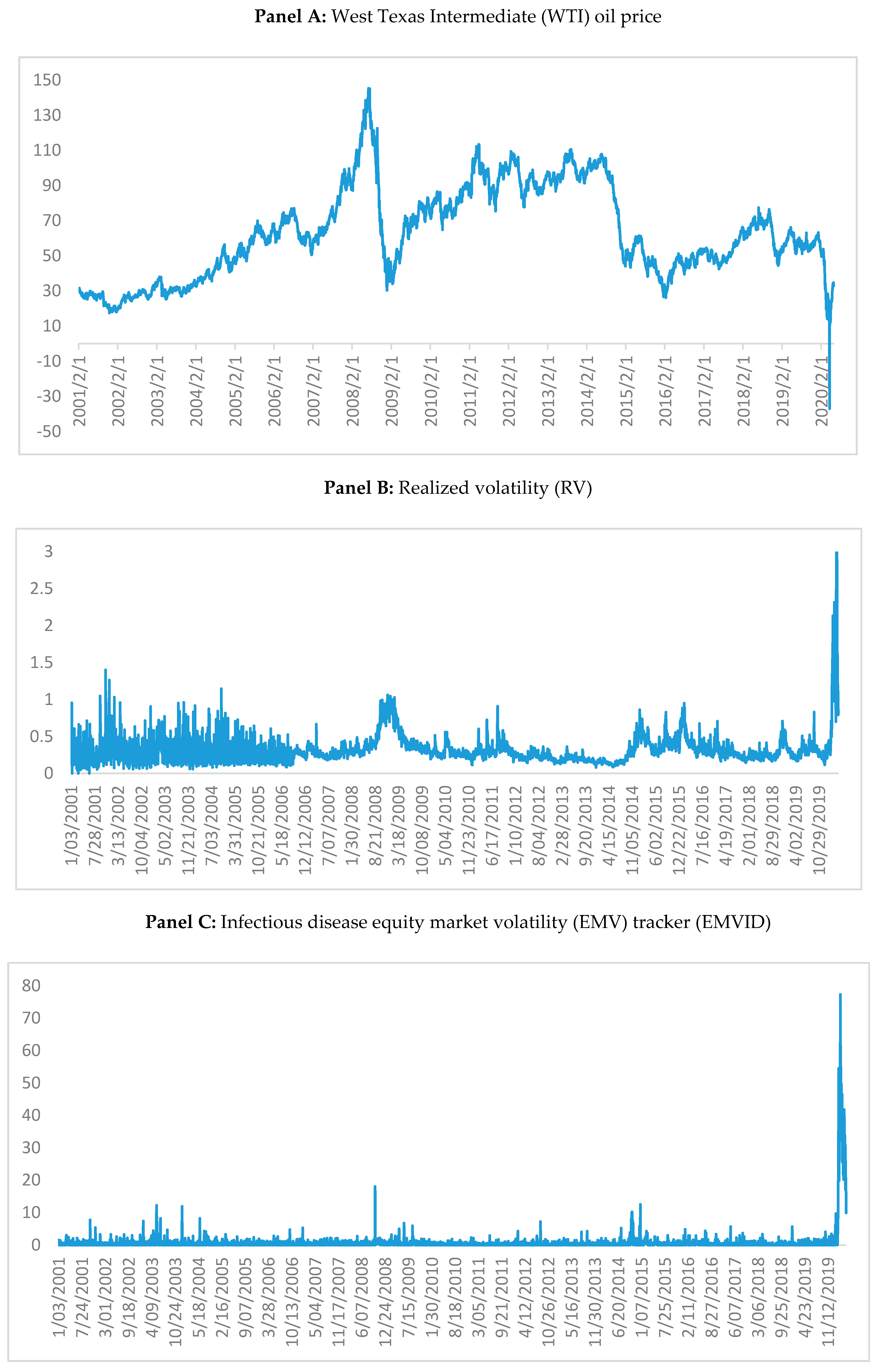

:1. Introduction

2. Data and Methodology

2.1. Data

2.2. Methodology: Heterogeneous Autoregressive Realized Volatility (HAR-RV) Model

3. Empirical Results

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Bernanke, B. The Relationship between Stocks and Oil Prices. Available online: https://www.brookings.edu/blog/ben-bernanke/2016/02/19/the-relationship-between-stocks-and-oil-prices/ (accessed on 15 February 2019).

- Hamilton, J. Oil Prices as an Indicator of Global Economic Conditions. Available online: http://econbrowser.com/archives/2014/12/oil-prices-as-an-indicator-of-global-economic-conditions (accessed on 5 March 2020).

- Demirer, R.; Gupta, R.; Pierdzioch, C.; Shahzad, S.J.H. The Predictive Power of Oil Price Shocks on Realized Volatility of Oil: A Note; Working Paper 202044; University of Pretoria: Pretoria, South Africa, 2020. [Google Scholar]

- Badshah, I.; Demirer, R.; Suleman, M.T. The effect of economic policy uncertainty on stock-commodity correlations and its implications on optimal hedging. Energy Econ. 2019, 84, 104553. [Google Scholar] [CrossRef]

- Balcilar, M.; Bekiros, S.; Gupta, R. The role of news-based uncertainty indices in predicting oil markets: A hybrid nonparametric quantile causality method. Empir. Econ. 2017, 53, 879–889. [Google Scholar] [CrossRef] [Green Version]

- Degiannakis, S.; Filis, G. Forecasting oil price realized volatility using information channels from other asset classes. J. Int. Money Financ. 2017, 76, 28–49. [Google Scholar] [CrossRef] [Green Version]

- Bahloul, W.; Balcilar, M.; Cunado, J.; Gupta, R. The role of economic and financial uncertainties in predicting commodity futures returns and volatility: Evidence from a nonparametric causality-in-quantiles test. J. Multinatl. Financ. Manag. 2018, 45, 52–71. [Google Scholar] [CrossRef]

- Bonaccolto, M.; Caporin, M.; Gupta, R. The dynamic impact of uncertainty in causing and forecasting the distribution of oil returns and risk? Phys. A 2018, 507, 446–469. [Google Scholar] [CrossRef] [Green Version]

- Gkillas, K.; Gupta, R.; Pierdzioch, C. Forecasting realized oil-price volatility: The Role of financial stress and asymmetric loss. J. Int. Money Financ. 2020, 104, 102137. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.A.; Davis, S.J.; Terry, S.J. Covid-Induced Economic Uncertainty; Working Paper No. 26983; NBER: Cambridge, MA, USA, 2020. [Google Scholar]

- McAleer, M.; Medeiros, M.C. Realized volatility: A review. Econom. Rev. 2008, 27, 10–45. [Google Scholar] [CrossRef]

- Corsi, F. A simple approximate long-memory model of realized volatility. J. Financ. Econ. 2009, 7, 174–196. [Google Scholar] [CrossRef]

- Lux, T.; Segnon, M.; Gupta, R. Forecasting crude oil price volatility and value-at-risk: Evidence from historical and recent data. Energy Econ. 2016, 56, 117–133. [Google Scholar] [CrossRef] [Green Version]

- Bonato, M.; Gkillas, K.; Gupta, R.; Pierdzioch, C. Investor Happiness and Predictability of the Realized Volatility of Oil Price. Sustainability 2020, 12, 4309. [Google Scholar] [CrossRef]

- Xiu, D. Quasi-Maximum Likelihood Estimation of Volatility with High Frequency Data. J. Econom. 2010, 159, 235–250. [Google Scholar] [CrossRef]

- Asai, M.; Gupta, R.; McAleer, M. Forecasting Volatility and co-volatility of crude oil and gold futures: Effects of leverage, jumps, spillovers, and geopolitical risks. Int. J. Forecast. 2020, 36, 933–948. [Google Scholar] [CrossRef] [Green Version]

- Asai, M.; Gupta, R.; McAleer, M. The Impact of Jumps and Leverage in Forecasting the Co-Volatility of Oil and Gold Futures. Energies 2019, 12, 3379. [Google Scholar] [CrossRef] [Green Version]

- Campbell, J.Y. Viewpoint: Estimating the equity premium. Can. J. Econ. 2008, 41, 1–21. [Google Scholar] [CrossRef] [Green Version]

- Bai, J.; Perron, P. Computation and analysis of multiple structural change models. J. Appl. Econom. 2003, 18, 1–22. [Google Scholar] [CrossRef] [Green Version]

- McCracken, M.W. Asymptotics for out of sample tests of Granger causality. J. Econom. 2007, 140, 719–752. [Google Scholar] [CrossRef]

- Mensi, W.; Hammoudeh, S.; Yoon, S.-M. How do OPEC news and structural breaks impact returns and volatility in crude oil markets? Further evidence from a long memory process. Energy Econ. 2014, 42, 343–354. [Google Scholar] [CrossRef]

- Gupta, R.; Yoon, S.-M. OPEC news and predictability of oil futures returns and volatility: Evidence from a nonparametric causality-in-quantiles approach. North Am. J. Econ. Financ. 2018, 45, 206–214. [Google Scholar] [CrossRef]

- Plante, M.D. OPEC in the News. Energy Econ. 2019, 80, 163–172. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.A.; Davis, S.J. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- van Eyden, R.; Difeto, M.; Gupta, R.; Wohar, M.E. Oil price volatility and economic growth: Evidence from advanced OECD countries using over one century of data. Appl. Energy 2019, 233–234, 612–621. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| RV | EMVID | |

|---|---|---|

| Mean | 0.3155 | 0.8036 |

| Median | 0.2731 | 0.0000 |

| Maximum | 3.0000 | 77.3500 |

| Minimum | 0.0014 | 0.0000 |

| Std. Dev. | 0.2009 | 3.8074 |

| Skewness | 4.4032 | 11.0178 |

| Kurtosis | 40.3062 | 143.1851 |

| Jarque-Bera | 285,596.7000 | 3,914,214.0000 |

| p-value | 0.0000 | 0.0000 |

| Observations | 4665 | |

| Horizon | θ | ||||

|---|---|---|---|---|---|

| h = 1 | 0.0262 * | 0.2624 * | 0.3238 * | 0.3175 * | 0.0067 * |

| h = 5 | 0.0342 * | 0.5919 * | 4.1655 * | 0.1184 * | 0.0073 * |

| h = 22 | 0.0041 | 0.2121 * | 0.8090 * | 20.9508 * | 0.0102 * |

| Horizon | MSFE0 | MSFE1 | FG |

|---|---|---|---|

| h = 1 | 0.0148 | 0.0120 | 23.3122 * |

| h = 5 | 0.0218 | 0.0181 | 20.2231 * |

| h = 22 | 0.0204 | 0.0159 | 28.3408 * |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bouri, E.; Demirer, R.; Gupta, R.; Pierdzioch, C. Infectious Diseases, Market Uncertainty and Oil Market Volatility. Energies 2020, 13, 4090. https://doi.org/10.3390/en13164090

Bouri E, Demirer R, Gupta R, Pierdzioch C. Infectious Diseases, Market Uncertainty and Oil Market Volatility. Energies. 2020; 13(16):4090. https://doi.org/10.3390/en13164090

Chicago/Turabian StyleBouri, Elie, Riza Demirer, Rangan Gupta, and Christian Pierdzioch. 2020. "Infectious Diseases, Market Uncertainty and Oil Market Volatility" Energies 13, no. 16: 4090. https://doi.org/10.3390/en13164090

APA StyleBouri, E., Demirer, R., Gupta, R., & Pierdzioch, C. (2020). Infectious Diseases, Market Uncertainty and Oil Market Volatility. Energies, 13(16), 4090. https://doi.org/10.3390/en13164090