The Linkages between Crude Oil and Food Prices

Abstract

:1. Introduction

2. Literature Review

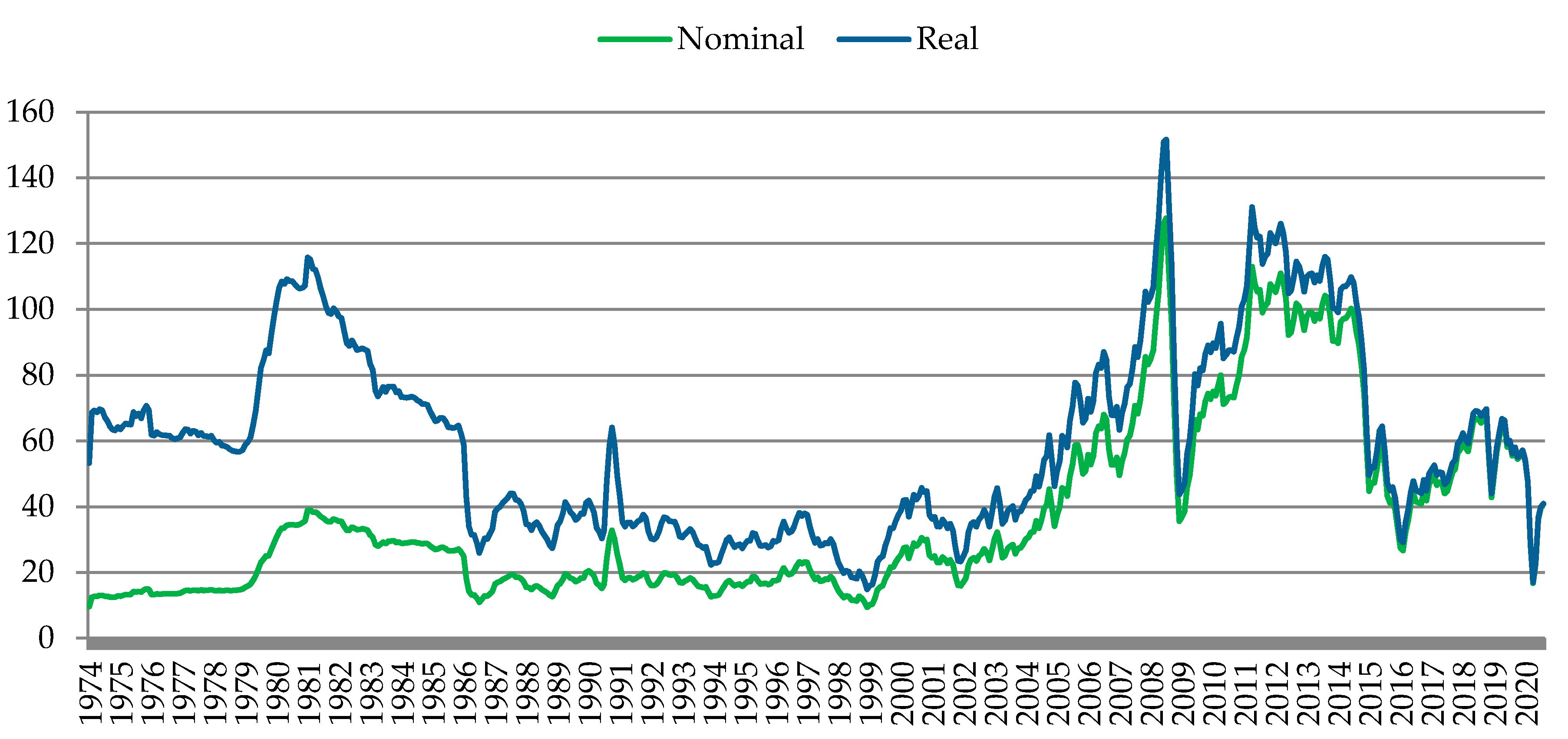

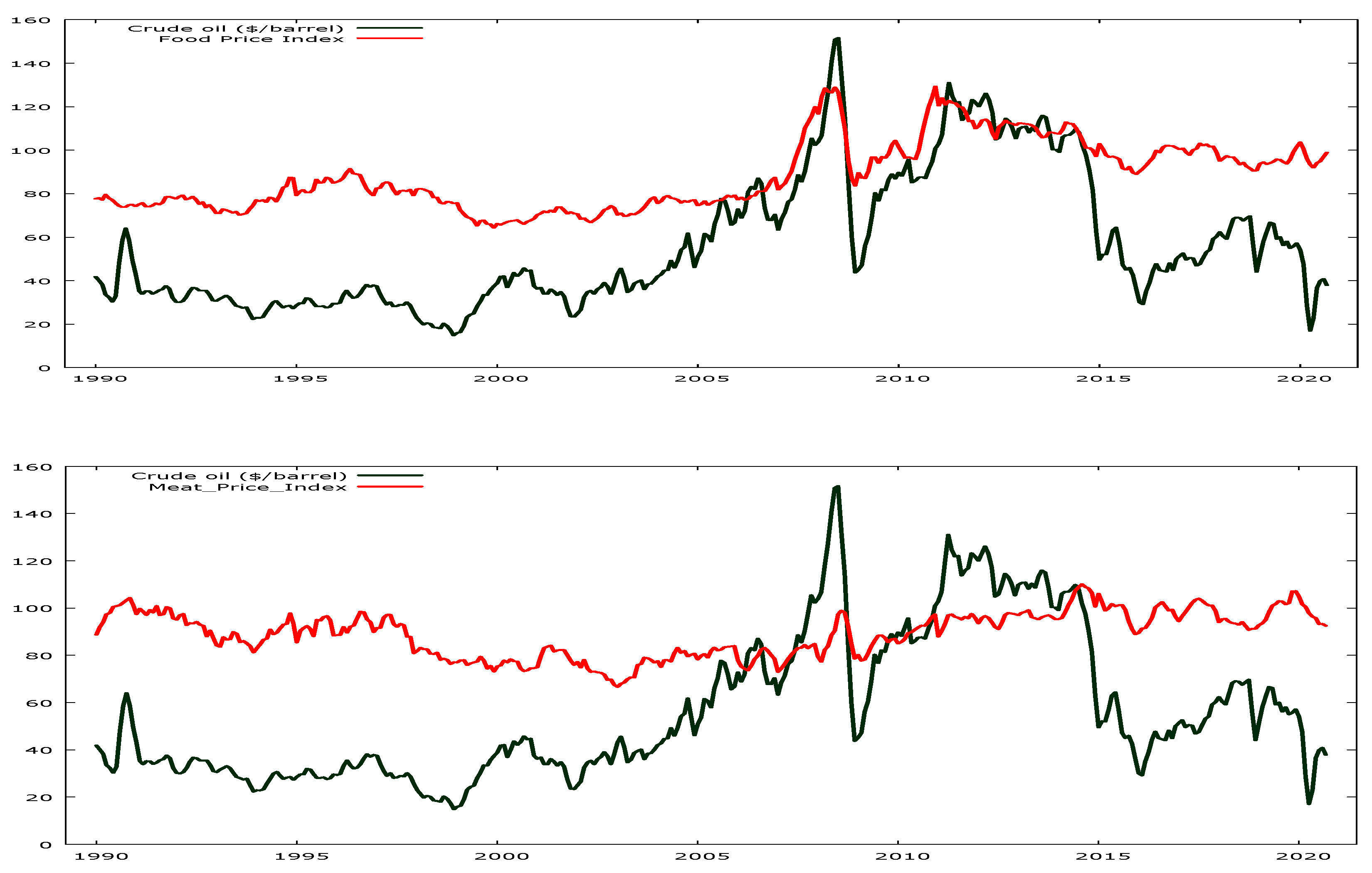

3. Materials and Methods

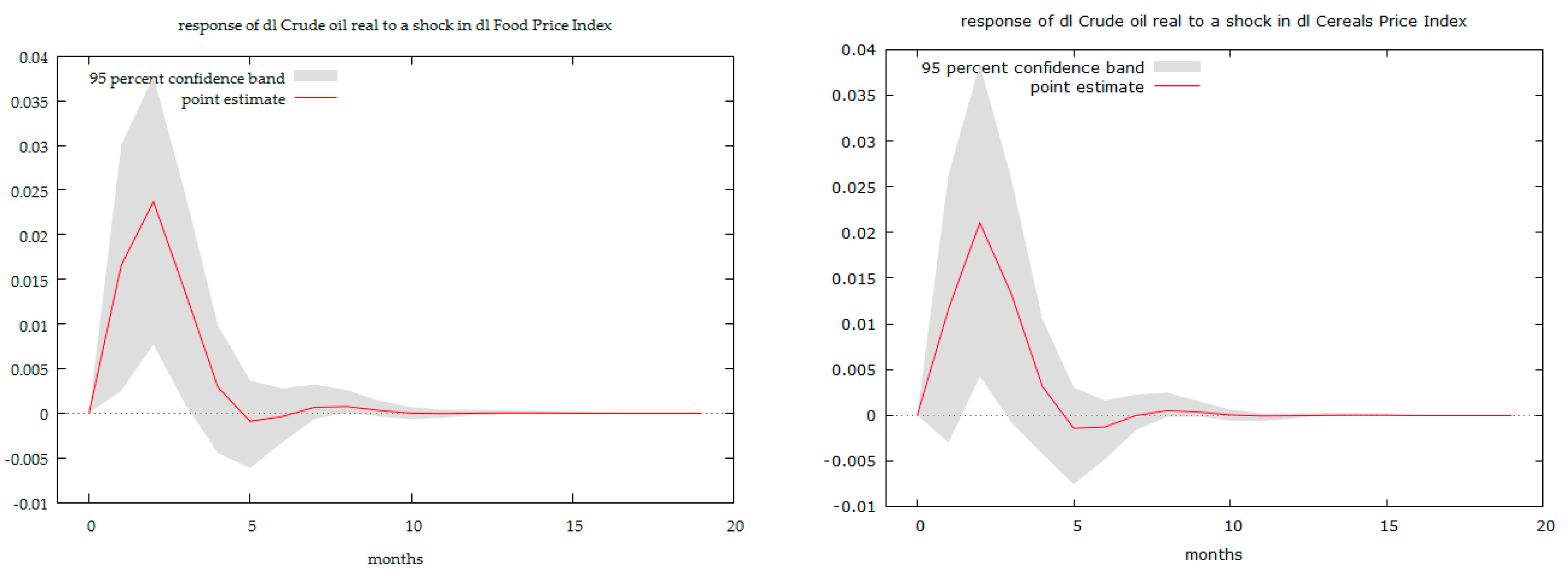

4. Results

4.1. Long-Run Analysis

4.2. Short-Run Analysis

4.3. Causal Relationship

5. Discussion and Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

| VAR(2) | Coef. | Coef. | |

|---|---|---|---|

| dl_Crude Oil | dl_Food | ||

| dl_Crude oil (−1) | 0.499 *** | dl_Crude oil (−1) | 0.001 |

| dl_Crude oil (−2) | −0.328 *** | dl_Crude oil (−2) | −0.004 |

| dl_Food (−1) | 0.6444 *** | dl_Food (−1) | 0.342 *** |

| dl_Food (−2) | 0.38 | dl_Food (−2) | 0.105 |

| Constant | −0.004 | Constant | 0.001 |

| R2 | 0.320 | R2 | 0.153 |

| dl_Crude oil | dl_Dairy | ||

| dl_Crude oil (−1) | 0.560 *** | dl_Crude oil (−1) | 0.020 |

| dl_Crude oil (−2) | −0.323 *** | dl_Crude oil (−2) | −0.034 |

| dl_Dairy (−1) | 0.213 | dl_Dairy (−1) | 0.521 *** |

| dl_Dairy (−2) | 0.209 | dl_Dairy (−2) | −0.002 |

| Constant | −0.003 | Constant | 0.000 |

| R2 | 0.296 | R2 | 0.279 |

| dl_Crude oil | dl_Cereals | ||

| dl_Crude oil (−1) | 0.551 *** | dl_Crude oil (−1) | −0.031 |

| dl_Crude oil (−2) | −0.298 *** | dl_Crude oil (−2) | 0.024 |

| dl_Cereals (−1) | 0.283 * | dl_Cereals (−1) | 0.334 *** |

| dl_Cereals (−2) | 0.261 | dl_Cereals (−2) | 0.036 |

| Constant | −0.004 | Constant | 0.002 |

| R2 | 0.308 | R2 | 0.118 |

| dl_Crude oil | dl_Oils | ||

| dl_Crude oil (−1) | 0.488 *** | dl_Crude oil (−1) | 0.0156 |

| dl_Crude oil (−2) | −0.311 *** | dl_Crude oil (−2) | −0.046 |

| dl_Oils (−1) | 0.378 *** | dl_Oils (−1) | 0.423 *** |

| dl_Oils (−2) | 0.111 | dl_Oils (−2) | −0.041 |

| Constant | −0.004 | Constant | 0.001 |

| R2 | 0.317 | R2 | 0.174 |

| dl_Crude oil | dl_Sugar | ||

| dl_Crude oil (−1) | 0.603 *** | dl_Crude oil (−1) | 0.013 |

| dl_Crude oil (−2) | −0.288 *** | dl_Crude oil (−2) | −0.031 |

| dl_Sugar (−1) | −0.052 | dl_Sugar (−1) | 0.313 *** |

| dl_Sugar (−2) | −0.074 | dl_Sugar (−2) | −0.077 |

| Constant | −0.003 | Constant | −0.001 |

| R2 | 0.283 | R2 | 0.097 |

| Selected Statistic | Stat. |

|---|---|

| AIC | −6.421 |

| BIC | −6.242 |

| Long-run relationship | 1 * ln_Crude oil − 6.164 × ln_Meat + 0.012 × time |

| EC (ln_Crude oil) | −0.008 |

| EC (ln_Meat) | 0.027 *** |

References

- Hamilton, J.D. Oil and the macroeconomy since World War II. J. Polit. Econ. 1983, 91, 228–248. [Google Scholar] [CrossRef]

- Kilian, L.; Vigfusson, R.J. Do oil prices help forecast us real GDP? The role of nonlinearities and asymmetries. J. Bus. Econ. Stat. 2013, 31, 78–93. [Google Scholar] [CrossRef]

- Wang, J.; Huang, Y.; Ma, F.; Chevallier, J. Does high-frequency crude oil futures data contain useful information for predicting volatility in the US stock market? New evidence. Energy Econ. 2020, 91, 1–13. [Google Scholar] [CrossRef]

- Trench, C.J.; Miesner, T.O. The role of energy pipelines and research in the United States. In Pipeline Research Council; International Inc.: Bothell, WA, USA, 2006. [Google Scholar]

- Rahman, M. Oil and Gas: The Engine of the World Economy. In Proceedings of the Presentation as OPEC Secretary General at the Tenth International Financial and Economic Forum, Vienna, Austria, 10–11 November 2004. [Google Scholar]

- Jahangir, S.R.; Dural, B.Y. Crude oil, natural gas, and economic growth: Impact and causality analysis in Caspian Sea region. Int. J. Manag. Econ. 2018, 54, 169–184. [Google Scholar] [CrossRef] [Green Version]

- Taghizadeh-Hesary, F.; Rasoulinezhad, E.; Yoshino, N. Energy and Food Security: Linkages through Price Volatility. Energy Policy 2019, 128, 796–806. [Google Scholar] [CrossRef]

- Xu, S.; Du, Z.; Zhang, H. Can Crude Oil Serve as a Hedging Asset for Underlying Securities? Research on the Heterogenous Correlation between Crude Oil and Stock Index. Energies 2020, 13, 3139. [Google Scholar] [CrossRef]

- EIA. Short-Term Energy Outlook. Available online: https://www.eia.gov/outlooks/steo/marketreview/crude.php (accessed on 10 October 2020).

- Umar, G.; Kilishi, A.A. Oil price shocks and the Nigeria economy: A variance autoregressive (VAR) model. Int. J. Bus. Manag. 2010, 5, 39. [Google Scholar] [CrossRef]

- Benedictow, A.; Fjærtoft, D.; Løfsnæs, O. Oil dependency of the Russian economy: An econometric analysis. Econ. Model. 2013, 32, 400–428. [Google Scholar] [CrossRef] [Green Version]

- Bayraktar, Y.; Taha, E.; Yildiz, F. A causal relationship between oil prices current account deficit, and economic growth: An empirical analysis from fragile five countries. Ecoforum. J. 2016, 5, 3. [Google Scholar]

- Ftiti, Z.; Guesmi, K.; Teulon, F.; Chouachi, S. Relationship between crude oil prices and economic growth in selected OPEC countries. J. Appl. Bus. Res. 2016, 32, 11. [Google Scholar] [CrossRef] [Green Version]

- Sarwar, S.; Tivari, A. Analyzing volatility spillovers between oil market and Asian stock markets. Resour. Policy 2020, 66, 101608. [Google Scholar] [CrossRef]

- Ding, S.; Zhang, Y. Cross market predictions for commodity prices. Econ. Model. 2020, 91, 455–462. [Google Scholar] [CrossRef]

- Hau, L.; Zhu, H.; Huang, R.; Ma, X. Heterogeneous dependence between crude oil price volatility and China’s agriculture commodity futures: Evidence from quantile-on-quantile regression. Energy 2020, 213. [Google Scholar] [CrossRef]

- Fowowe, B. Do oil prices drive agricultural commodity prices? Evidence from South Africa. Energy 2016, 104, 149–157. [Google Scholar] [CrossRef]

- Ibrahim, M.H. Oil and food prices in Malaysia: A nonlinear ARDL analysis. Agric. Food Econ. 2015, 3, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Nazlioglu, S.; Soytas, U. World oil prices and agricultural commodity prices: Evidence from an emerging market. Energy Econ. 2011, 33, 488–496. [Google Scholar] [CrossRef]

- Gilbert, C.L. How to understand high food prices. J. Agric. Econ. 2010, 61, 398–425. [Google Scholar] [CrossRef]

- Zhang, Z.; Lohr, L.; Escalante, C.; Wetzstein, M. Food versus fuel: What do prices tell us? Energy Policy 2010, 38, 445–451. [Google Scholar] [CrossRef]

- Vo, D.H.; Vu, T.N.; Vo, A.T.; McAleer, M. Modeling the Relationship between Crude Oil and Agricultural Commodity Prices. Energies 2019, 12, 1344. [Google Scholar] [CrossRef] [Green Version]

- Su, C.W.; Wang, X.Q.; Tao, R.; Oana-Ramona, L. Do oil prices drive agricultural commodity prices? Further evidence in a global bio-energy context. Energy 2019, 172, 691–701. [Google Scholar] [CrossRef]

- Pal, D.; Mitra, S.K. Correlation dynamics of crude oil with agricultural commodities: A comparison between energy and food crops. Econ. Model. 2019, 82, 453–466. [Google Scholar] [CrossRef]

- Pasrun, A.; Rosnawintang, R.; Saidi, L.D.; Tondi, L.; Sani, L.O.A. The Causal Relationship between Crude Oil Price, Exchange Rate and Rice Price. Int. J. Energy Econ. Policy 2018, 8, 90–94. [Google Scholar]

- Ji, Q.; Bouri, E.; Roubaud, D.; Shahzad, S.J.H. Risk spillover between energy and agricultural commodity markets: A dependence-switching CoVaR-copula model. Energy Econ. 2018, 75, 14–27. [Google Scholar] [CrossRef]

- Al-Maadid, A.; Caporale, G.M.; Spagnolo, F.; Spagnolo, N. Spillovers between food and energy prices and structural breaks. Int. Econ. 2017, 150, 1–18. [Google Scholar] [CrossRef]

- Bergmann, D.; O’Connor, D.; Thummel, A. An analysis of price and volatility transmission in butter, palm oil and crude oil markets. Agric. Food Econ. 2016, 4, 1–23. [Google Scholar] [CrossRef] [Green Version]

- Hamulczuk, M. Energy prices vs agri-food prices – energy security and food security. Humanit. Soc. Sci. 2016, 23, 37–51. [Google Scholar]

- Mawejje, J. Food prices, energy and climate shocks in Uganda. Agric. Food Econ. 2016, 4, 1–18. [Google Scholar] [CrossRef] [Green Version]

- Fernandez-Perez, A.; Frijns, B.; Tourani-Rad, A. Contemporaneous interactions among fuel, biofuel and agricultural commodities. Energy Econ. 2016, 58, 1–10. [Google Scholar] [CrossRef]

- McFarlane, L. Agricultural commodity prices and oil prices: Mutual causation. Outlook Agric. 2016, 45, 87–93. [Google Scholar] [CrossRef] [Green Version]

- Cabrera, B.L.; Schulz, F. Volatility linkages between energy and agricultural commodity prices. Energy Econ. 2016, 54, 190–203. [Google Scholar] [CrossRef] [Green Version]

- Nwoko, I.C.; Aye, G.C.; Asogwa, B.C. Effect of oil price on Nigeria’s food price volatility. Cogent Food Agric. 2016, 2, 1–14. [Google Scholar] [CrossRef]

- Zhang, C.; Qu, X. The effect of global oil price shocks on China’s agricultural commodities. Energy Econ. 2015, 51, 354–364. [Google Scholar] [CrossRef]

- Koirala, K.H.; Mishra, A.K.; D’Antoni, J.M.; Mehlhorn, J.E. Energy prices and agricultural commodity prices: Testing correlation using copulas method. Energy 2015, 81, 430–436. [Google Scholar] [CrossRef]

- Rezitis, A.N. The relationship between agricultural commodity prices, crude oil prices and US dollar exchange rates: A panel VAR approach and causality analysis. Int. Rev. Appl. Econ. 2015, 29, 403–434. [Google Scholar] [CrossRef]

- Natanelov, V.; Alam, M.J.; McKenzie, A.M.; Huylenbroeck, G.V. Is there co-movement of agricultural commodities futures prices and crude oil? Energy Policy 2011, 39, 4971–4984. [Google Scholar] [CrossRef] [Green Version]

- Chang, T.-H.; Su, H.-M. The substitutive effect of biofuels on fossil fuels in the lower and higher crude oil price periods. Energy 2010, 35, 2807–2813. [Google Scholar] [CrossRef]

- Balcombe, K.; Rapsomanikis, G. Bayesian estimation and selection of nonlinear vector error correction models: The case of the sugar-ethanol-oil nexus in Brazil. Am. J. Agric. Econ. 2008, 90, 658–668. [Google Scholar] [CrossRef]

- Nazlioglu, S. World oil and agricultural commodity prices: Evidence from nonlinear causality. Energy Policy 2011, 39, 2935–2943. [Google Scholar] [CrossRef]

- Rosa, F.; Vasciaveo, M. Agri-Commodity Price Dynamics: The Relationship between Oil and Agricultural Market. In Proceedings of the International Association of Agricultural Economists (IAAE) Triennial Conference, Foz do Iguaçu, Brazil, 18–24 August 2012; pp. 18–24. [Google Scholar]

- FAO Food Price Index. Available online: http://www.fao.org/fileadmin/templates/worldfood/Reports_and_docs/Food_price_indices_data.xls (accessed on 10 October 2020).

- Dickey, D.A.; Fuller, W.A. Distribution of the estimators for autoregressive time series with a unit root. J. Am. Stat. Assoc. 1979, 74, 427–431. [Google Scholar]

- Engle, R.F.; Granger, C.W.J. Co-integration and error correction: Representation, estimation and testing. Econometrica 1987, 55, 251–276. [Google Scholar] [CrossRef]

- Lutkepohl, H. Vector Autoregressive and Vector Error Correction Models. In Book Applied Time Series Econometrics; Lutkepohl, H., Kratzig, M., Eds.; Cambridge University Press: New York, NY, USA, 2004; pp. 86–108. [Google Scholar]

- Neusser, K. Time Series Econometrics; Springer International Publishing: Cham, Switzerland, 2016; pp. 305–310. [Google Scholar]

- Kusideł, E. Modelowanie Wektorowo-Autoregresyjne VAR. Metodologia i Zastosowanie w Badaniach Ekonomicznych; Absolwent: Łódź, Poland, 2000; pp. 40–55. [Google Scholar]

- Granger, C.W.J. Investigating Causal Relations by Econometric Models and Cross-spectral Methods. Econometrica 1969, 37, 424–438. [Google Scholar] [CrossRef]

- Baumeister, C.; Kilian, L. Do oil price increases cause higher food prices? Econ. Policy 2014, 29, 691–747. Available online: https://www.jstor.org/stable/24030050 (accessed on 11 December 2020). [CrossRef] [Green Version]

- Coronado, S.; Rojas, O.; Romero-Meza, R.; Serletis, A.; Chiu, L.V. Crude oil and Biofuel Agricultural Commodity Prices. In Expectations, Uncertainty and Asset Price Dynamics; Fredj, J., Ed.; Springer: Berlin/Heidelberg, Germany, 2018. [Google Scholar]

- Vacha, L.; Janda, K.; Kristoufek, L.; Zilberman, D. Time-frequency dynamics of biofuel-fuel-food system. Energy Econ. 2013, 40, 233–241. [Google Scholar] [CrossRef] [Green Version]

- Nazlioglu, S.; Erdem, C.; Soytas, U. Volatility spillover between oil and agricultural commodity markets. Energy Econ. 2013, 36, 658–665. [Google Scholar] [CrossRef]

- Reboredo, J.C. Do food and oil prices co-move? Energy Policy 2012, 49, 456–467. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Authors, Year | Methods | Data (Source) | Time/Geographical Coverage | Results | |

|---|---|---|---|---|---|

| Neutrality Hypothesis | Crude Oil/Energy Prices Driving Prices of Agricultural/Food Goods | ||||

| Ding, Zhang (2020) [15] | Spread CRB Index, Dickey–Fuller test | Crude oil, corn, cattle gold, and copper prices daily data (Thomson Datastream) | 2005–2018 | + | |

| Hau, Zhu, Huang, Ma (2020) [16] | Model TVP-SVM, Model MCMC estimation | Corn, soybean, bean, strong wheat, cotton, pulp, natural rubber; weekly data | 2003–2004, 2007–2011, China | + | |

| Fowowe (2016) [17] | ECM, Nonlinear causality tests | Maize, sunflower, and soybeans; weekly data (the EIA, the Johannesburg Stock Exchange) | 2001–2014, South Africa | + | |

| Ibrahim (2015) [18] | NARDL model | Food and oil prices annual data | 1971–2012, Malaysia | + | |

| Nazlioglu, Soytas (2011) [19] | Toda and Yamamoto causality test | Monthly data | 1994–2010, Turkey | + | |

| Gilbert (2010) [20] | Granger causality test, 2SLS, 3SLS OLS, | Quarterly data | 1971–2008 | + | |

| Zhang, Lohr, Escalante, Wetzstein (2010) [21] | VECM | Crude oil, soybean, corn, wheat prices, monthly data | 1989–2008 | + | |

| Vo, Vu, Vo (2019) [22] | SVAR model IRF model, variance decomposition technique | Crude oil prices, corn, wheat, sugarcane, soybeans, coconut, soybean and palm oil, palm kernel oil, barley, coffee, cocoa, rice, tea, cotton prices; monthly data; WB | January 2000–July 2018, 2000–2006, 2006–2013, 2013–2018 | + | |

| Taghizadeh-Hesary, Rasoulinezhad, Yoshino (2019) [7] | Panel-VAR model | Food prices, crude oil and biofuel price, inflation and real interest rate, agricultural land, employment in the agriculture sector, GDP (World Development Indicators, the FAO, the BP, the EIA, Statistical Review of World Energy) | 2000–2016, 8 Asian countries | + | |

| Su, Wang, Tao, Oana-Ramona (2019) [23] | Vertical market integration model Ciaian and Kancs, bootstrap full-sample causality test, Granger causality test, bivariate VAR models | Crude oil spot price Worldwide; maize and soybeans, tea and cocoa beans, monthly data, (WTI) | 1990–2017 | + | |

| Pal, Mitra (2019) [24] | DCC model, Pearson correlations | Crude oil, corn, soybeans, wheat, and oat prices, daily spot closing prices, (WTI) | 2000–2018; U.S. | + | |

| Pasrun, Rosnawintang, La Ode, La, La Ode (2018) [25] | VAR model, Granger causality test | Crude oil price, rice price, monthly data | January 2000–September 2017 | + | |

| Ji, Bouri, Roubaud, Shahzad (2018) [26] | Copula model | Daily data, | 2000–2017 | + | |

| Al-Maadid, Caporale, Spagnolo, Spagnolo (2017) [27] | Bivariate VAR-GARCH(1,1) model | Crude oil and ethanol prices and coffee, cacao, corn, sugar, soybeans, and wheat prices, daily data (Bloomberg) | January 1st, 2003 to June 6th, 2015 | + | |

| Bergmann, O’Connor, Thummel (2016) [28] | VAR model, multivariate GARCH model | Palm oil, butter, and crude oil prices | January 1995–December 2005; EU and World | + | |

| Hamulczuk (2016) [29] | Correlation coefficient | Energy prices and agrifood prices | 1995–2015, | + | |

| Mawejje (2016) [30] | Cointegration techniques | Energy, meat, dairy, cereal, edible oil, sugar prices, monthly data; the Uganda Bureau of Statistics, Bank of Uganda, FAO | 2000–2011 | + | |

| Fernandez-Perez, Frijns, Tourani-Rad (2016) [31] | SVAR | Daily data | 2006–2016 | + | |

| McFarlane (2016) [32] | Dickey–Fuller test, Johansen tests, VAR | Corn, sugar, wheat, and crude oil prices, weekly data | 1999–2005, 2006–2012, The U.S | + | |

| Cabrera, Schulz (2016) [33] | Correlation GARCH model, multivariate multiplicative volatility model | Energy, agricultural product prices | 2003–2012, Germany | + | |

| Nwoko, Aye, Asogwa (2016) [34] | GARCH (1, 1) model, Dickey–Fuller test, Phillip–Perron test, Granger causality test, VAR model | Oil price (food crop prices (US EIA, Federal Ministry of Agriculture), annual data | 2000–2013, Nigeria | + | |

| Zhang, Qu (2015) [35] | ARMA-GARCH | Daily data | 2004–2014 | + | |

| Koirala, Mishra, D’Antoni, Mehlhorn (2015) [36] | Copula model | Daily data | 2011–2012 | + | |

| Rezitis (2015) [37] | Panel-VAR model, Granger causality tests | US dollar exchange rates, crude oil prices, 5 fertilizer prices, 30 selected agricultural prices, monthly data | June 1983–June 2013 | + | |

| Natanelov, Alam, McKenzie, Huylenbroeck (2011) [38] | VECM, TVECM | Monthly data | 1989–2010 | + | |

| Chang, Su (2010) [39] | EGARCH | Daily data | 2004–2008 | + | |

| Balcombe, Rapsomanikis (2008) [40] | VECM, AVECM, TVECM | Weekly data | 2000–2006 | + | |

| L_Crude Oil | Dl_Crude Oil | ||||||

|---|---|---|---|---|---|---|---|

| 1999–2020 | 1990–2005 | 2006–2020 | 1999–2020 | 1990–2005 | 2006–2020 | ||

| l_Food | 0.742 | −0.125 | 0.603 | dl_Food | 0.195 | −0.174 | 0.393 |

| l_Meat | 0.275 | −0.025 | −0.085 | dl_Meat | 0.159 | 0.007 | 0.282 |

| l_Dairy | 0.783 | 0.341 | 0.557 | dl_Dairy | 0.124 | −0.095 | 0.293 |

| l_Cereals | 0.732 | −0.121 | 0.595 | dl_Cereals | −0.001 | −0.223 | 0.137 |

| l_Oils | 0.592 | −0.353 | 0.603 | dl_Oils | 0.202 | −0.141 | 0.436 |

| l_Sugar | 0.509 | −0.072 | 0.321 | dl_Sugar | 0.169 | −0.011 | 0.308 |

| 1990–2020 | 1990–2005 | 2006–2020 | |

|---|---|---|---|

| l_Food | −2.769 | −1.768 | −2.873 |

| dl_Food | −14.449 *** | −12.984 *** | −8.507 *** |

| l_Meat | −2.141 | −2.525 | −2.947 |

| dl_Meat | −10.460 *** | −4.214 *** | −10.082 *** |

| l_Dairy | −3.021 | −2.694 | −3.048 |

| dl_Dairy | −14.612 *** | −13.606 *** | −7.020 *** |

| l_Cereals | −3.260 | −3.044 | −3.166 |

| dl_Cereals | −13.326 *** | −7.387 *** | −8.957 *** |

| l_Oils | −3.120 | −2.267 | −2.989 |

| dl_Oils | −8.043 *** | −5.743 *** | −5.948 *** |

| l_Sugar | −3.568 ** | −2.676 | −2.477 |

| dl_Sugar | −12.747 *** | −9.406 *** | −9.494 *** |

| l_Crude oil | −2.430 | −2.335 | −2.556 |

| dl_Crude oil | −13.048 *** | −8.923 *** | −9.247 *** |

| Rank | 1990–2005 | 2006–2020 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| LRtrace | LRmax | LRtrace | LRmax | ||||||

| Stat. | p-Value | Stat. | p-Value | Stat. | p-Value | Stat. | p-Value | ||

| l_Food | 0 | 8.990 | 0.171 | 8.900 | 0.126 | 22.300 | 0.131 | 11.285 | 0.497 |

| 1 | 0.091 | 0.828 | 0.091 | 0.819 | 11.014 | 0.088 | 11.014 | 0.088 | |

| l_Meat | 0 | 20.513 | 0.204 | 15.769 | 0.159 | 32.632 | 0.005 | 21.617 | 0.020 |

| 1 | 4.744 | 0.639 | 4.744 | 0.640 | 11.015 | 0.088 | 11.015 | 0.088 | |

| l_Dairy | 0 | 23.120 | 0.106 | 15.788 | 0.158 | 22.398 | 0.128 | 13.481 | 0.301 |

| 1 | 7.332 | 0.321 | 7.332 | 0.321 | 8.916 | 0.190 | 8.916 | 0.190 | |

| l_Cereals | 0 | 21.006 | 0.182 | 14.256 | 0.246 | 24.618 | 0.070 | 14.345 | 0.240 |

| 1 | 6.749 | 0.382 | 6.749 | 0.383 | 10.273 | 0.117 | 10.273 | 0.117 | |

| l_Oils | 0 | 9.395 | 0.941 | 5.186 | 0.973 | 22.431 | 0.127 | 14.123 | 0.255 |

| 1 | 4.209 | 0.713 | 4.209 | 0.715 | 8.308 | 0.234 | 8.308 | 0.234 | |

| l_Sugar | 0 | 23.177 | 0.104 | 13.759 | 0.280 | 19.150 | 0.278 | 11.936 | 0.434 |

| 1 | 9.417 | 0.160 | 9.417 | 0.160 | 7.214 | 0.332 | 7.214 | 0.333 | |

| 1990–2005 | 2006–2020 | |||||

|---|---|---|---|---|---|---|

| Stat. | p-Value | Stat. | p-Value | |||

| dl_Crude oil ≠ > dl_Food | 1.151 | 0.333 | Crude oil←Food | 0.020 | 0.980 | Crude oil←Food |

| dl_Food ≠ > dl_Crude oil | 3.359 | 0.010 | 5.277 | 0.006 | ||

| dl_ Crude oil ≠ > dl_Meat | 3.344 | 0.011 | Crude oil→Meat | 5.185 | 0.007 | Crude oil→Meat |

| dl_Meat ≠ > dl_ Crude oil | 1.628 | 0.167 | 1.020 | 0.363 | ||

| dl_ Crude oil ≠ > dl_Dairy | 1.866 | 0.173 | Crude oil←Dairy | 0.732 | 0.482 | Crude oil x Dairy |

| dl_Dairy ≠ > dl_ Crude oil | 4.697 | 0.031 | 2.140 | 0.121 | ||

| dl_ Crude oil ≠ > dl_Cereals | 1.176 | 0.322 | Crude oil←Cereals | 0.497 | 0.609 | Crude oil←Cereals |

| dl_Cereals ≠ > dl_ Crude oil | 2.533 | 0.041 | 3.704 | 0.027 | ||

| dl_ Crude oil ≠ > dl_Oils | 2.137 | 0.061 | Crude oil x Oils | 0.571 | 0.566 | Crude oil←Oils |

| dl_Oils ≠ > dl_ Crude oil | 1.237 | 0.292 | 4.853 | 0.009 | ||

| dl_ Crude oil ≠ > dl_Sugar | 0.250 | 0.617 | Crude oil x Sugar | 0.142 | 0.867 | Crude oil x Sugar |

| dl_Sugar ≠ > dl_ Crude oil | 0.751 | 0.387 | 0.548 | 0.579 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Roman, M.; Górecka, A.; Domagała, J. The Linkages between Crude Oil and Food Prices. Energies 2020, 13, 6545. https://doi.org/10.3390/en13246545

Roman M, Górecka A, Domagała J. The Linkages between Crude Oil and Food Prices. Energies. 2020; 13(24):6545. https://doi.org/10.3390/en13246545

Chicago/Turabian StyleRoman, Monika, Aleksandra Górecka, and Joanna Domagała. 2020. "The Linkages between Crude Oil and Food Prices" Energies 13, no. 24: 6545. https://doi.org/10.3390/en13246545

APA StyleRoman, M., Górecka, A., & Domagała, J. (2020). The Linkages between Crude Oil and Food Prices. Energies, 13(24), 6545. https://doi.org/10.3390/en13246545