How Much Polish Consumers Know about Alternative Fuel Vehicles? Impact of Knowledge on the Willingness to Buy

Abstract

:1. Introduction

1.1. Background and Motivation

1.2. The Actual State of the Car Market in Poland

1.3. Research Goals

2. Literature Review: The Role of Socio-Economic and Attitudinal Factors in Willingness to Buy AFV

2.1. Status Quo of AFV Knowledge

2.2. The Role of Experience and Education

2.3. The Relation between AFV Knowledge and Willingness to Pay and Buy

2.4. Interest and Positive Attitudes towards New Technologies

2.5. Eco-Friendly Attitudes and Behaviors

2.6. The Role of Charging Stations

2.7. The Demographic Attributes in the Context of AFV Knowledge

3. Methods and Survey Design

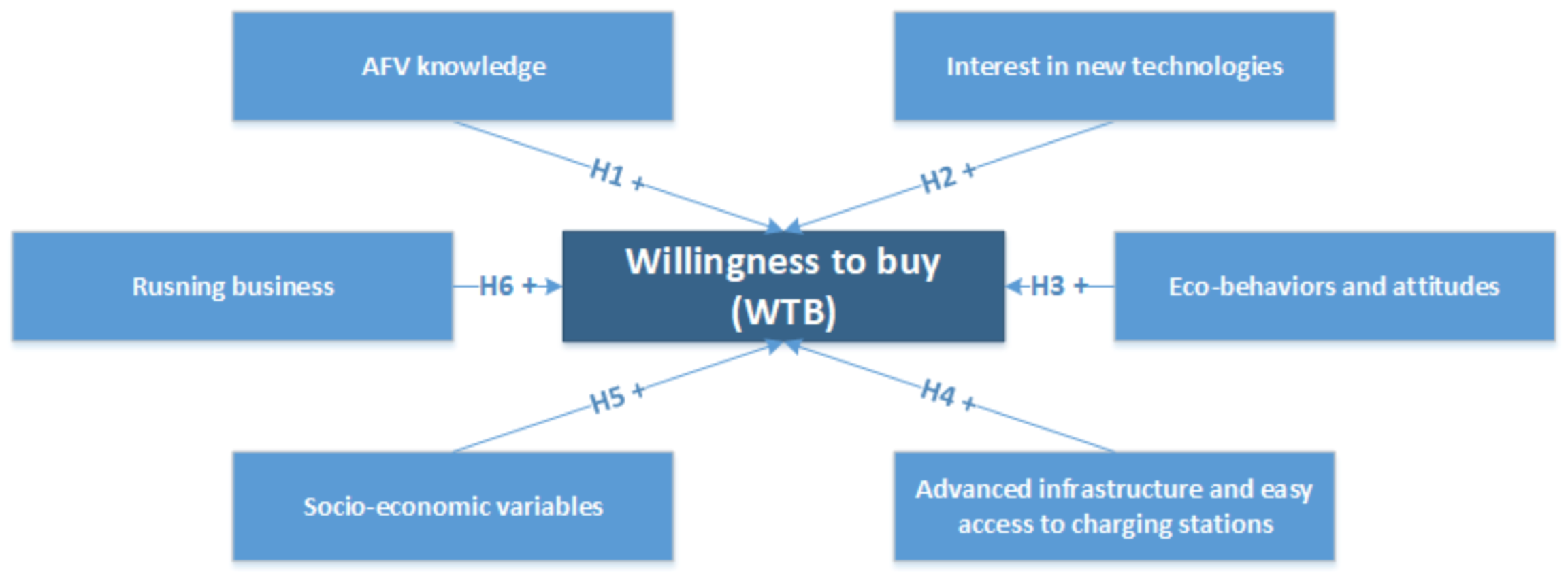

3.1. Research Framework of WTB

3.2. Data Collection and the Sample

4. Results and Discussion

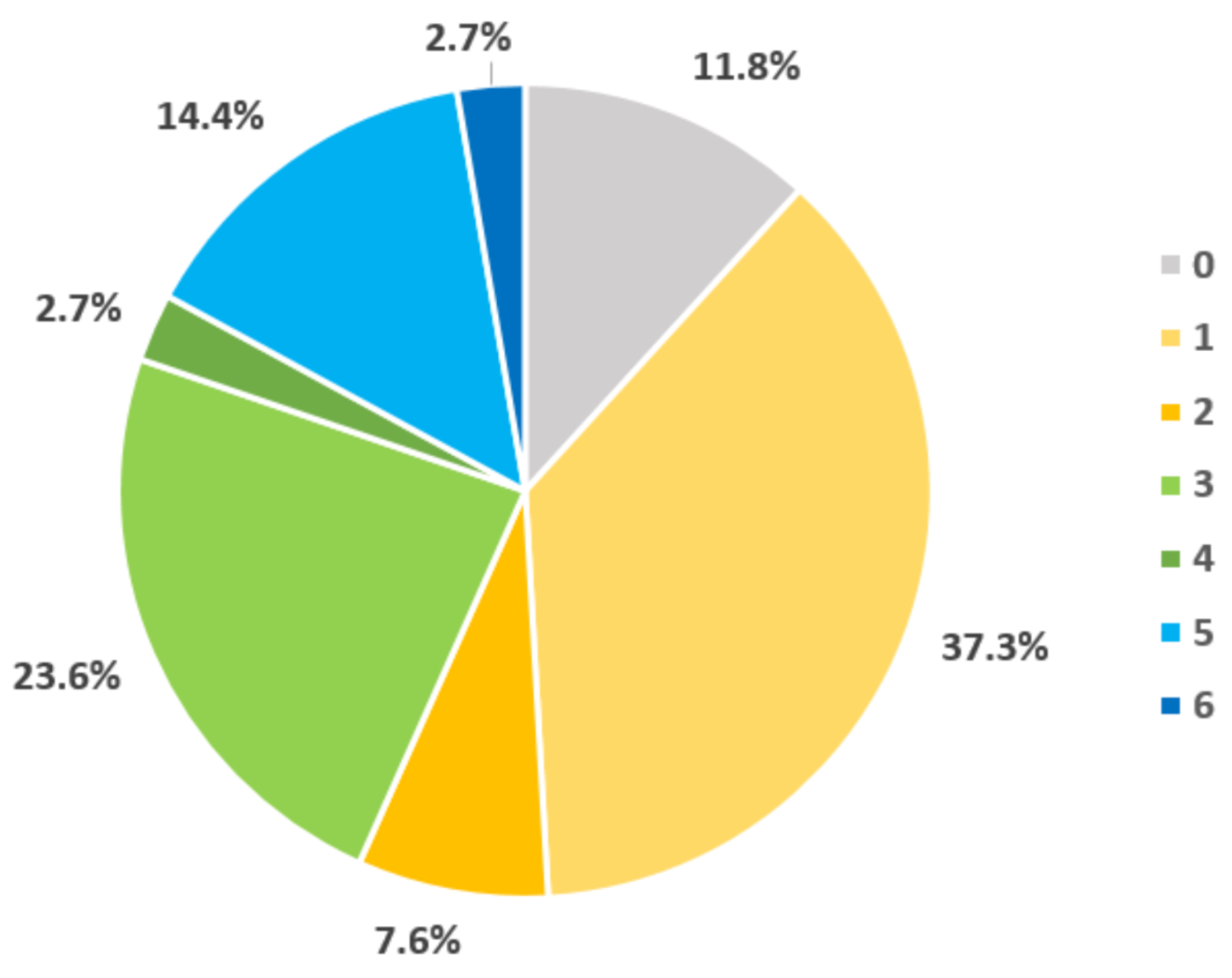

4.1. Analysis of Dependent Variable: AFV Preferences

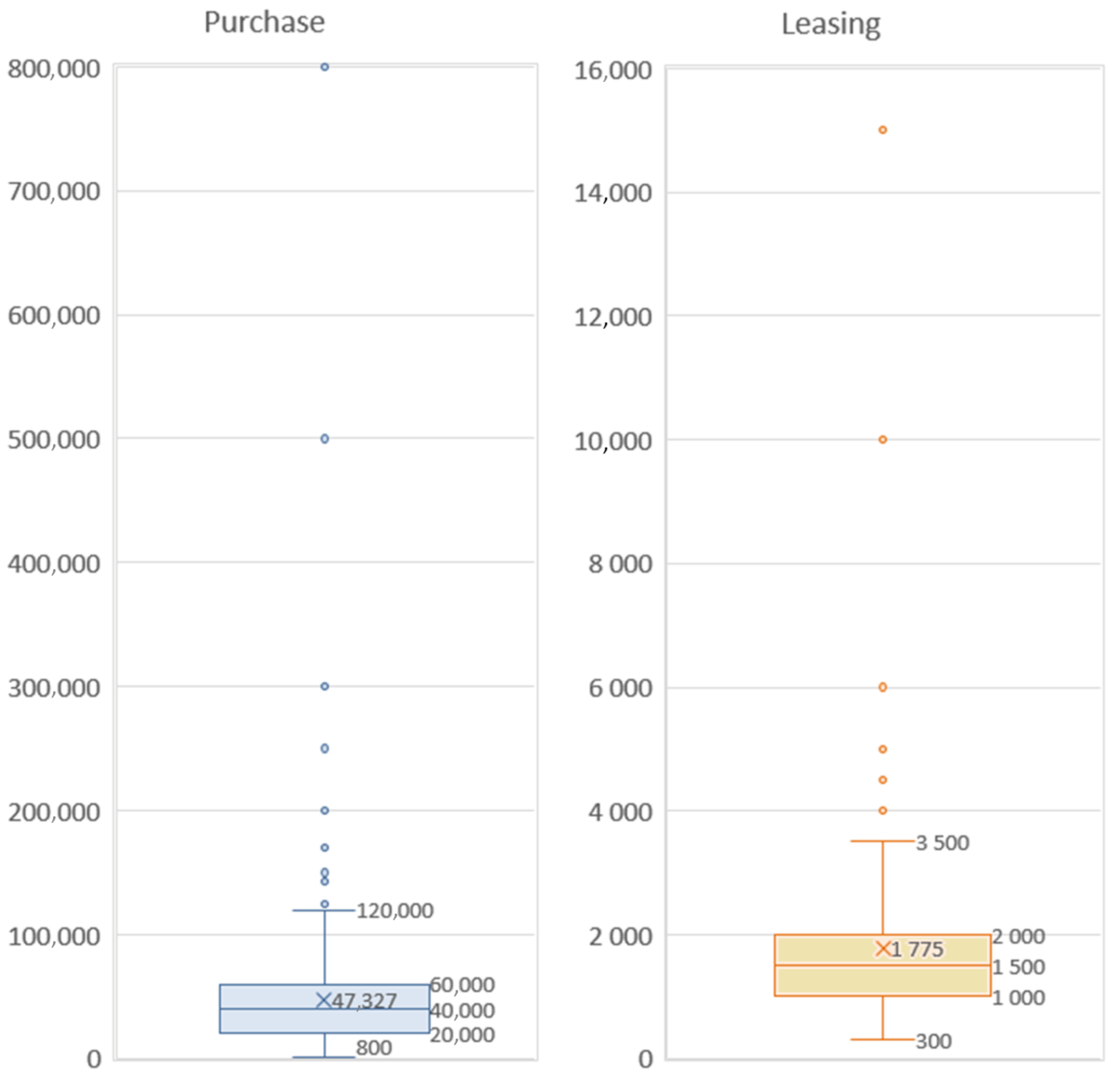

4.2. Analysis of Independent Variables

4.2.1. Environmental Attitudes and Behaviors

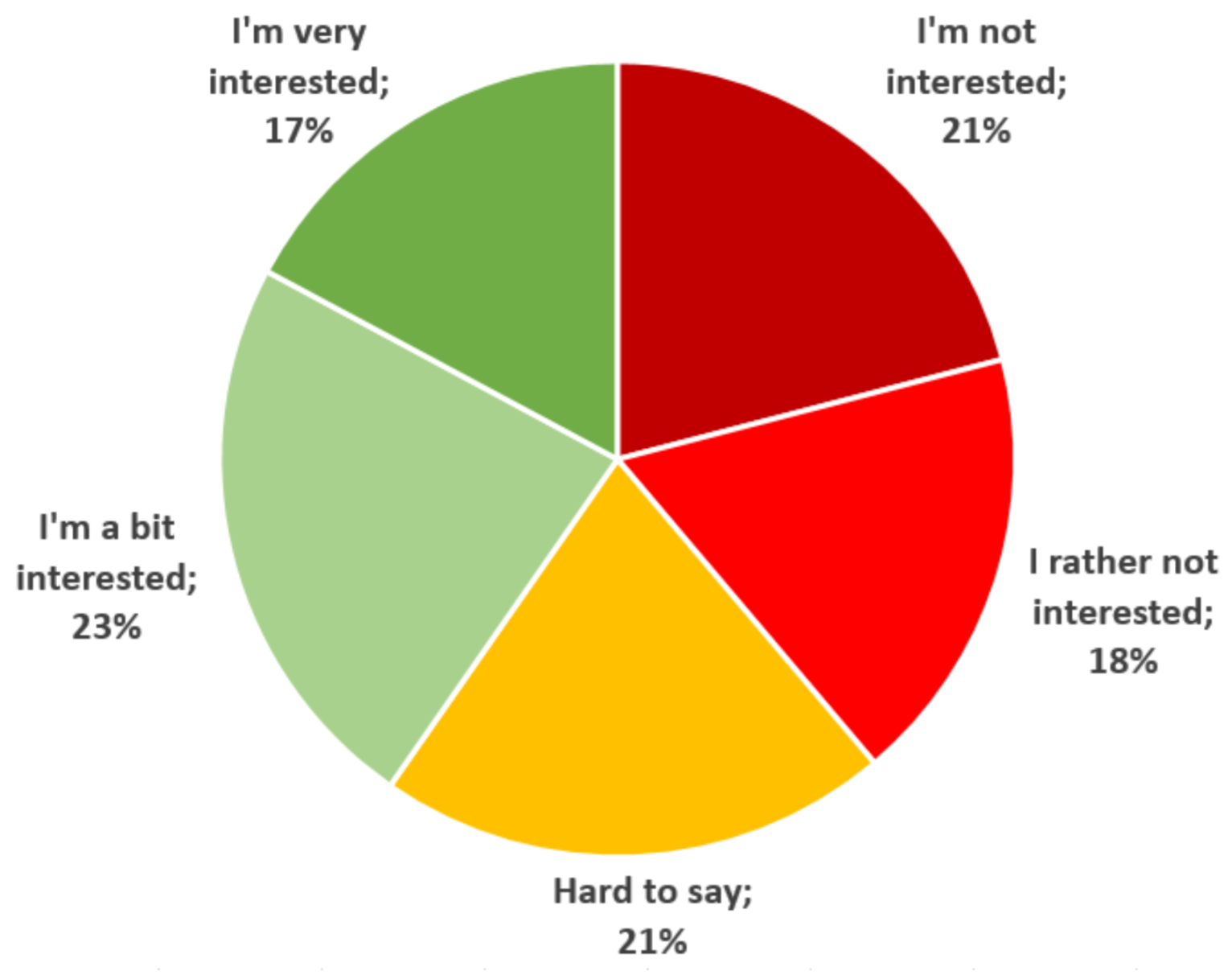

4.2.2. Interest in New Technologies

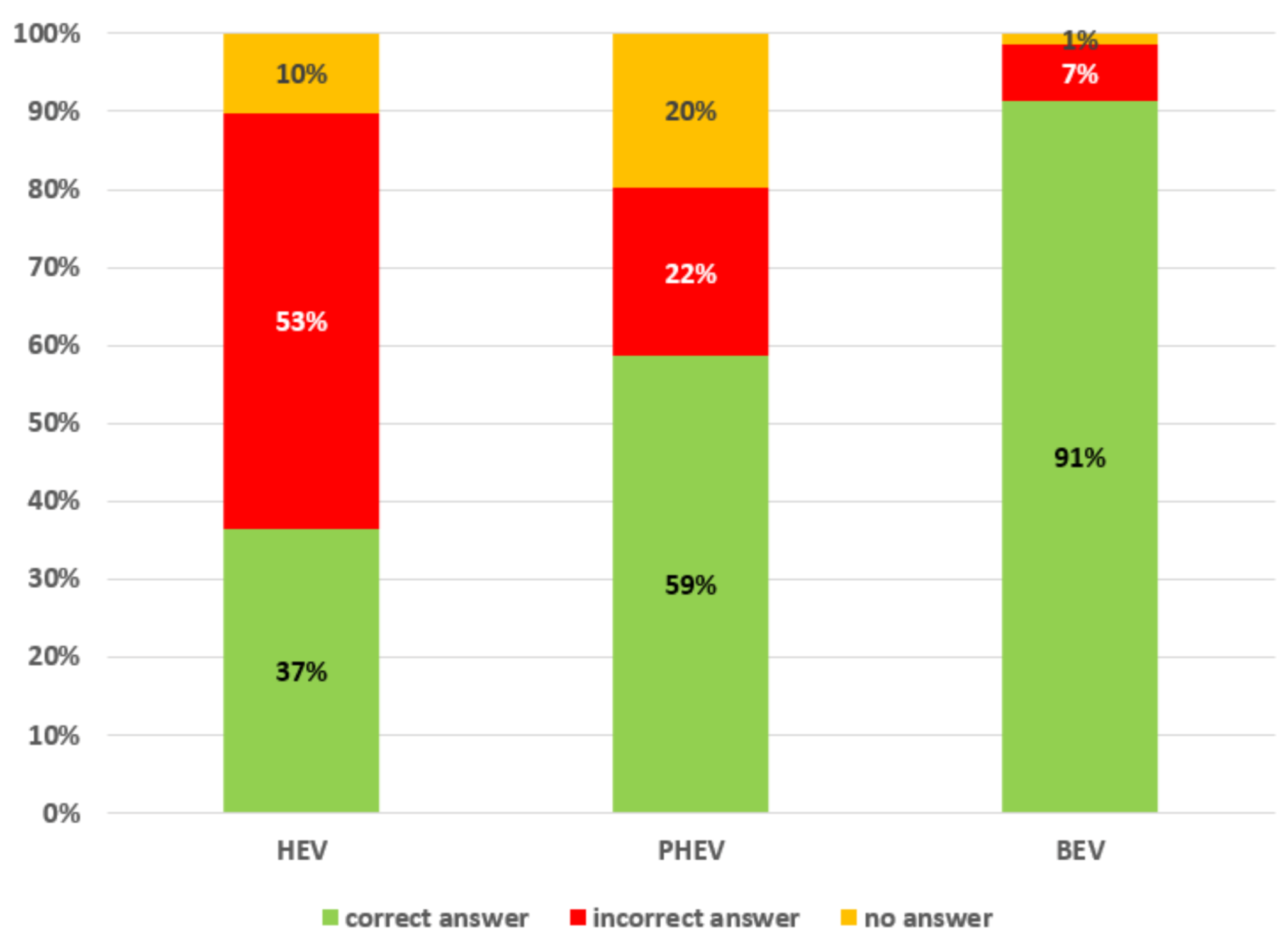

4.2.3. Knowledge Regarding Type of Fuel for AFV

4.2.4. Knowledge of AFV Brand Names

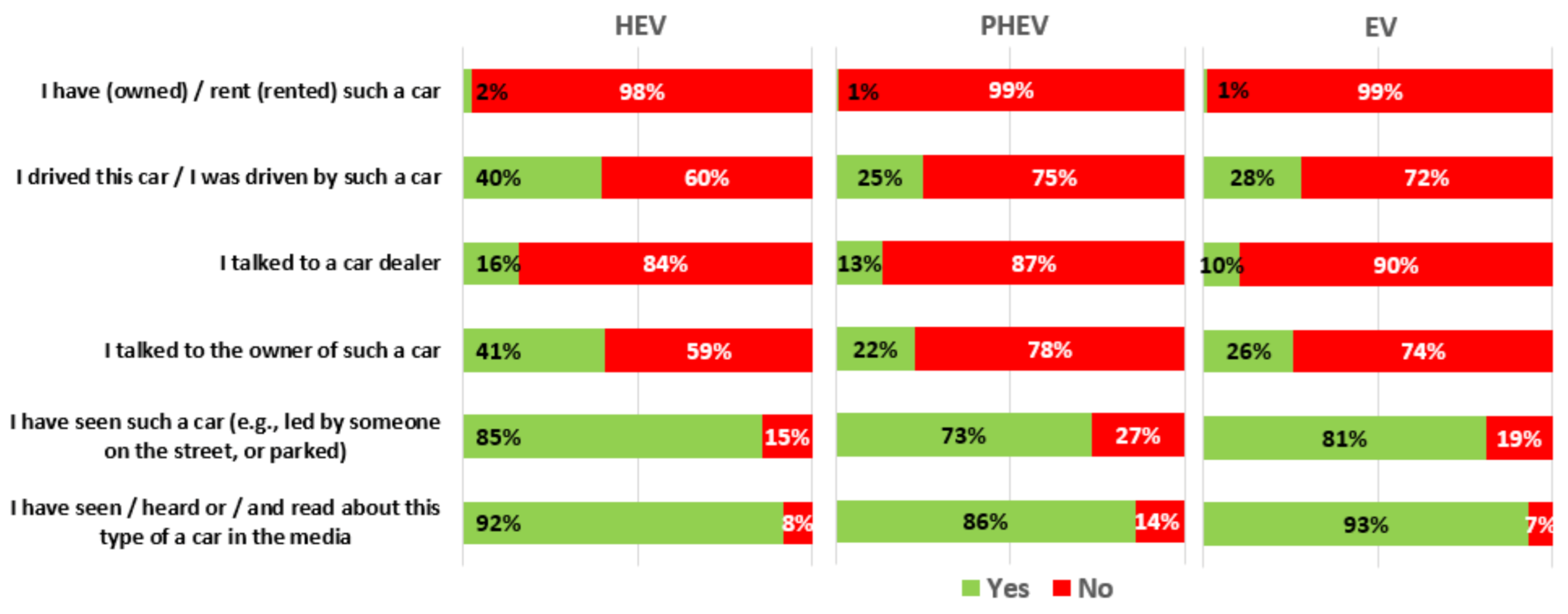

4.2.5. Sources of AFV Knowledge

4.3. Model of AFV Preferences in Terms of AFV Knowledge and Socio-Economic and Attitudinal Variables

5. Conclusions and Policy Recommendations

Future Work

Author Contributions

Funding

Informed Consent Statement

Conflicts of Interest

References

- Slocat Partnership. Available online: https://slocat.net/sustainable-development-goals-transport/ (accessed on 20 April 2020).

- Chang, D.; Chen, S.; Hsu, C.; Hu, A.; Tzeng, G. Evaluation Framework for Alternative Fuel Vehicles: Perspective. Sustainability 2015, 7, 11570–11594. [Google Scholar] [CrossRef] [Green Version]

- Axsen, J.; Langman, B.; Goldberg, S. Confusion of innovations: Mainstream consumer perceptions and misperceptions of electric-drive vehicles and charging programs in Canada. Energy Res. Soc. Sci. 2017, 27, 163–173. [Google Scholar] [CrossRef]

- Long, Z.; Axsen, J.; Kormos, C. Consumers continue to be confused about electric vehicles: Comparing awareness among Canadian new car buyers in 2013 and 2017. Environ. Res. Lett. 2019, 14, 114036. [Google Scholar] [CrossRef]

- Wang, N.; Tang, L.; Pan, H. A global comparison and assessment of incentive policy and electric vehicle promotion. Sustain. Cities Soc. 2019, 44, 597–603. [Google Scholar] [CrossRef]

- Lopez-Carreiro, I.; Monzon, A. Evaluating sustainability and innovation of mobility patterns in Spanish cities. Analysis by size and urban typology. Sustain. Cities Soc. 2018, 38, 684–696. [Google Scholar] [CrossRef]

- Nie, Y.; Ghamami, M.; Zockaie, A.; Xiao, F. Optimization of incentive polices for plug-in electric vehicles. Transp. Res. Part B Methodol. 2016, 84, 103–123. [Google Scholar] [CrossRef]

- Kamiya, G.; Axsen, J.; Crawford, C. Modeling the GHG emissions intensity of plug-in electric vehicles using short term and long-term perspectives. Transp. Res. Part D Transp. Environ. 2019, 69, 209–223. [Google Scholar] [CrossRef]

- Requia, W.; Adams, M.; Arain, A.; Koutrakis, P.; Ferguson, M. Carbon dioxide emissions of plug-in hybrid electric vehicles: A life-cycle analysis in eight Canadian cities. Renew. Sustain. Energy Rev. 2017, 78, 1390–1396. [Google Scholar] [CrossRef]

- Peters, D.; Axsen, J.; Mallett, A. The role of environmental framing in socio-political acceptance of smart grid: The case of British Columbia, Canada. Renew. Sustain. Energy Rev. 2018, 82, 1939–1951. [Google Scholar] [CrossRef]

- Lieven, T. Policy measures to promote electric mobility—A global perspective. Transp. Res. Part A Policy Pract. 2015, 82, 78–93. [Google Scholar] [CrossRef] [Green Version]

- International Energy Agency. Global EV Outlook 2019: Towards Cross-Modal Electrification; IEA: Paris, France, 2019. [Google Scholar]

- International Energy Agency. Global EV Outlook 2020. 2020. Available online: https://webstore.iea.org/ (accessed on 12 January 2021).

- Jin, J.; Slowik, P. Literature Review of Electric Vehicle Consumer Awareness and Outreach Activities; Working Paper for the International Council of Clean Transportation; The International Council on Clean Transportation: Washington, DC, USA, 2017. [Google Scholar]

- Kurani, K.; Caparello, N.; TyreeHageman, J. New Car Buyers’ Valuation of Zero-Emission Vehicles: California; Plug-in Hybrid & Electric Vehicle Center, Institute of Transportation Studies, University of California: Davis, CA, USA, 2016. [Google Scholar]

- Browne, D.; Omahony, M.; Caulfield, B. How should barriers to alternative fuels and vehicles be classified and potential policies to promote innovative technologies be evaluated? J. Clean. Prod. 2012, 35, 140–151. [Google Scholar] [CrossRef]

- Long, Z.; Axsen, J.; Miller, I.; Kormos, C. What does Tesla mean to car buyers? Exploring the role of automotive brand in perceptions of battery electric vehicles. Transp. Res. Part A Policy Pract. 2019, 129, 85–204. [Google Scholar] [CrossRef]

- Larson, P.; Viafara, J.; Parsons, R.; Elias, A. Consumer attitudes about electric cars: Pricing analysis and policy implications. Transp. Res. Part A Policy Pract. 2014, 69, 299–314. [Google Scholar] [CrossRef]

- Kurani, K.; Axsen, J.; Caperello, N.; Davies, J.; Stillwater, T. Learning From Consumers: PHEV Demonstration and Consumer Education, Outreach, and Market Research Program; Working Paper Series qt9361r9h7; Institute of Transportation Studies: Davis, CA, USA, 2009. [Google Scholar]

- Egbue, O.; Long, S. Barriers to widespread adoption of electric vehicles: An analysis of consumer attitudes and perceptions. Energy Policy 2012, 48, 717–729. [Google Scholar] [CrossRef]

- CFA. Consumer Federation of America: Knowledge Affects Consumer Interest in EVs: New EVs Guide to Address Info Gap. 2015. Available online: http://consumerfed.org (accessed on 15 April 2020).

- Bailey, J.; Miele, A.; Axsen, J. Is awareness of public charging associated with consumer interest in plug-in electric vehicles? Transp. Res. Part D 2015, 36, 1–9. [Google Scholar] [CrossRef]

- Bunce, L.; Harris, M.; Burgess, M. Charge up then charge out? Drivers’ perceptions and experiences of electric vehicles in the UK. Transp. Res. Part A Policy Pract. 2014, 59, 278–287. [Google Scholar] [CrossRef]

- Krupa, J.; Rizzo, D.; Eppstein, M.; Lanute, D.; Gaalema, D.; Lakkaraju, K.; Warrender, C. Analysis of a consumer survey on plug-in hybrid electric vehicles. Transp. Res. Part A 2014, 64, 14–31. [Google Scholar] [CrossRef]

- CoxAutomative. Cox Automotive Evolution of Mobility Study: The Path to Electric Vehicle Adoption Study. 2019. Available online: https://www.coxautoinc.com/market-insights/cox-automotive-evolution-of-mobility-study-the-path-to-electric-vehicle-adoption-study-released/ (accessed on 5 May 2020).

- Polish Association of Automotive Industry. Electromobility Index: Record Year 2020 on the Polish Market Electric Cars. 2021. Available online: https://www.pzpm.org.pl/pl/Rynek-motoryzacyjny/Licznik-elektromobilnosci/Rok-2020/Grudzien-2020 (accessed on 20 February 2021).

- The European Automobile Manufacturers’ Association. European Automobile Manufacturers’ Association, Alternative Fuel Vehicle Registrations. 2021. Available online: www.https://www.acea.be/statistics/tag/category/electric-and-alternative-vehicle-registrations (accessed on 20 February 2021).

- Transport&Environment-Report. How Clean Are Electric Cars? T&E’s Analysis of Electric Car Lifecycle CO2 Emissions. Transport & Environment. 2020. Available online: https://www.transportenvironment.org/sites/te/files/T%26E%E2%80%99s%20EV%20life%20cycle%20analysis%20LCA.pdf (accessed on 20 December 2020).

- Kowalska-Pyzalska, A.; Kott, J.; Kott, M. Why Polish market of alternative fuel vehicles (AFVs) is the smallest in Europe? SWOT analysis of opportunities and threats. Renew. Sustain. Energy Rev. 2020, 133, 110076. [Google Scholar] [CrossRef]

- ACEA. European Automobile Manufacturers’ Association, Making the Transition to Zero-Emission Mobility—2020 Progress Report. 2020. Available online: https://www.acea.be/publications (accessed on 14 October 2020).

- Eurostat. Road Transport Infrastructure. 2019. Available online: https://ec.europa.eu/eurostat/data/ (accessed on 6 December 2020).

- Ploetz, P.; Schneider, U.; Globisch, J.; Duetschke, E. Who will buy electric vehicles? Identifying early adopters in Germany. Transp. Res. Part A Policy Pract. 2014, 67, 96–109. [Google Scholar] [CrossRef]

- Simsekoglu, O.; Nayum, A. Predictors of intention to buy a battery electric vehicle among conventional car drivers. Transp. Res. Part F 2019, 60, 1–10. [Google Scholar] [CrossRef]

- Tsouros, I.; Polydoropoulou, A. Who will buy alternative fueled or automated vehicles: A modular, behavioral modeling approach. Transp. Res. Part A 2020, 132, 214–225. [Google Scholar] [CrossRef]

- Lin, B.; Wu, W. Why people want to buy electric vehicle: An empirical study in first-tier cities of China. Energy Policy 2018, 112, 233–241. [Google Scholar] [CrossRef]

- Ramos-Real, F.; Ramírez-Díaz, A.; Marrero, G.; Perez, Y. Willingness to pay for electric vehicles in island regions: The case of Tenerife (Canary Islands). Renew. Sustain. Energy Rev. 2018, 98, 140–149. [Google Scholar] [CrossRef]

- Humbe, C.; Wardle, J.; Humby, R.; Poskett, H.; Nourse, C. Why Consumers Buy Electric Vehicles? Starcount Observatory Platform. 2019. Available online: www.starcount.com (accessed on 20 February 2021).

- Bartczak, A.; Chilton, S.; Czajkowski, M.; Meyerhoff, J. Gain and losses of money in a choice experiment. The impact of financial loss aversion and risk preferences on willingness to pay to avoid renewable energy externalities. Energy Econ. 2017, 65, 326–334. [Google Scholar] [CrossRef]

- Frank, B.; Enkawa, T.; Schvaneveldt, S.; Torrico, B. Antecedents and consequences of innate willingness to pay for innovations: Understanding motivations and consumer preferences of prospective early adopters. Technol. Forecast. Soc. Chang. 2015, 99, 252–266. [Google Scholar] [CrossRef] [Green Version]

- Ma, C.; Rogers, A.; Kragt, M.; Zhang, F.; Polyakov, M. Consumers’ willingness to pay for renewable energy: A meta-regression analysis. Resour. Energy Econ. 2015, 42, 93–109. [Google Scholar] [CrossRef] [Green Version]

- Sundt, S.; Rehdanz, K. Consumers’ willingness to pay for green electricity: A meta-analysis of the literature. Energy Econ. 2015, 51, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Oerlemans, L.; Chan, K.Y.; Voschenk, J. Willingness to pay for green electricity: A review of the contingent valuation literature and its source of error. Renew. Sustain. Energy Rev. 2016, 66, 875–885. [Google Scholar] [CrossRef] [Green Version]

- Kowalska-Pyzalska, A. Do consumers want to pay for green electricity? A case study from Poland. Sustainability 2019, 11, 1310. [Google Scholar] [CrossRef] [Green Version]

- Hackbarth, A.; Madlener, R. Consumer Preferences for Alternative Fuel Vehicles: A Discrete Choice Analysis. Transp. Res. Part Transp. Environ. 2013, 25, 5–17. [Google Scholar] [CrossRef] [Green Version]

- Liao, F.; Molin, E.; van Wee, B. Consumer preferences for electric vehicles: A literature review. Transp. Rev. 2017, 37, 252–275. [Google Scholar] [CrossRef] [Green Version]

- Noel, L.; Carrone, A.; Jensen, A.; Zarazua de Rubens, G.; Kester, J.; Sovacool, B. Willingness to pay for electric vehicles and vehicle-to-grid applications: A Nordic choice experiment. Energy Econ. 2019, 78, 525–534. [Google Scholar] [CrossRef]

- Jensen, A.; Cherchi, E.; Mabit, S. On the stability of preferences and attitudes before and after experiencing an electric vehicle. Transp. Res. Part D 2013, 25, 24–32. [Google Scholar] [CrossRef] [Green Version]

- Qiao, Q.; Zhao, F.; Liu, Z.; Jiang, S.; Hao, H. Comparative study on life cycle C02 emissions from the production of electric and conventional vehicles in China. Energy Procedia 2017, 105, 3584–3595. [Google Scholar] [CrossRef]

- Yang, C. Launching strategy for electric vehicles: Lessons from China and Taiwan. Technol. Forecast. Soc. Chang. 2010, 77, 831–840. [Google Scholar] [CrossRef]

- Buekers, J.; van Hoderbeke, M.; Bierkens, J.; Panis, L. Health and environmental benefits related to electric vehicle introduction in EU countries. Transp. Res. Part D 2014, 33, 26–38. [Google Scholar] [CrossRef]

- Knez, M.; Obrecht, M. Policies for Promotion of Electric Vehicles and Factors Influencing Consumers’ Purchasing Decisions of Low Emission Vehicles. J. Sustain. Dev. Energy Water Environ. Syst. 2017, 5, 151–162. [Google Scholar] [CrossRef] [Green Version]

- de Rubens, G. Who will buy electric vehicles after early adopters? Using machine learning to identify the electric vehicle mainstream market. Energy 2019, 172, 243–254. [Google Scholar] [CrossRef]

- Noel, L.; Zarazua de Rubens, G.; Kester, J.; Sovacool, B. Understanding the socio-technical nexus of Nordic electric vehicle (EV) barriers: A qualitative discussion of range, price, charging and knowledge. Energy Policy 2020, 138, 111292. [Google Scholar] [CrossRef]

- Axsen, J.; Wolinetz, M. How policy can build the plug-in electric vehicle market: Insights from the Respondent-based Preference And Constraints (REPAC) model. Technol. Forecast. Soc. Chang. 2017, 117, 238–250. [Google Scholar]

- Melton, N.; Axsen, J.; Goldberg, S. Evaluating plug-in electric vehicle policies in the context of long-term greenhouse gas reduction goals: Comparing 10 Canadian provinces using the “PEV policy report card”. Energy Policy 2017, 107, 381–393. [Google Scholar] [CrossRef]

- Kurani, K.; Tal, G. Growing PEV Markets? Notes from Recent Consumer Research. In Proceedings of the Plug-in Hybrid and Electric Vehicle Research Center of the Institute of Transportation Studies, University of California, Davis, CA, USA, 21 November 2014. [Google Scholar]

- Singer, M. Consumer Views on Plug-In Electric Vehicles: National Benchmark Report. 2015. Available online: http://www.afdc.energy.gov/uploads/publications (accessed on 7 April 2020).

- Karplus, V.; Patesev, S.; Reilly, J. Prospects for plug-in hybrid electric vehicles in the United States and Japan. Transp. Res. Part A 2010, 44, 620–641. [Google Scholar]

- Sharma, K.; Manzie, C.; Bessede, M.; Crawford, R.; Brear, M. Conventional, hybrid and electric vehicles for Australia and driving conditions. Part 2: Life cycle CO2-emissions. Transp. Res. Part C 2013, 28, 63–73. [Google Scholar] [CrossRef]

- Al-Alawi, B.; Bradley, T. Review of hybrid, plug-in hybrid and electric vehicle market modeling studies. Renew. Sustain. Energy Rev. 2013, 21, 190–203. [Google Scholar] [CrossRef]

- Gyimesi, K.; Viswanathan, R. The Shift to Electric Vehicles: Putting Consumers in the Driver’s Seat. 2011. Available online: https://www.electrive.com/study-guide/the-shift-to-electric-vehicles-putting-consumers-in-the-drivers-seat/ (accessed on 20 February 2021).

- Reiner, R.; Haas, H. Stuttgart Region—From E-Mobility Pilot Projects to Showcase Region. E-Mobility in Europe; Springer International Publishing: Berlin/Heidelberg, Germany, 2015. [Google Scholar]

- TRB. Transportation Research Board and National Research Council. Overcoming Barriers to the Deployment of Plug-In Electric Vehicles; The National Academies Press: Washington, DC, USA, 2015. [Google Scholar] [CrossRef]

- Kannstatter, T.; Meerschiff, S. Launching an E-Carsharing System in the Polycentric Area of Ruhr. E-Mobility in Europe; Springer International Publishing: Berlin/Heidelberg, Germany, 2015. [Google Scholar]

- Kahma, N.; Matschoss, K. The rejection of innovations? Rethinking technology diffusion and the non-use of smart energy services in Finland. Energy Resour. Soc. Sci. 2017, 34, 27–36. [Google Scholar] [CrossRef]

- Krishnamutri, T.; Schwartz, D.; Davis, A.; Fischoff, B.; de Bruin, W.B.; Lave, L.; Wang, J. Preparing for smart grid technologies: A behavioral decision research approach to understanding consumer expectations about smart meters. Energy Policy 2012, 41, 790–797. [Google Scholar] [CrossRef]

- Chawla, Y.; Kowalska-Pyzalska, A. Public awareness and consumer acceptance of smart meters among Polish social media users. Energies 2019, 12, 2759. [Google Scholar] [CrossRef] [Green Version]

- Chawla, Y.; Kowalska-Pyzalska, A.; Skowronska-Szmer, A. Perspectives of Smart Meters’ Roll-Out in India: An Empirical Analysis of Consumers’ Awareness and Preferences. Energy Policy 2020, 146, 111798. [Google Scholar] [CrossRef]

- Axsen, J.; Bailey, J.; Castro, M. Preference and lifestyle heterogeneity among potential plug-in electric vehicle buyers. Energy Econ. 2015, 50, 190–201. [Google Scholar] [CrossRef]

- Ruggieri, R.; Ruggeri, M.; Vinci, G.; Poponi, S. Electric Mobility in a Smart City: European Overview. Energies 2021, 14, 315. [Google Scholar] [CrossRef]

- Ingeborgrud, L.; Ryghaug, M. The role of practical, cognitive and symbolic factors in the successful implementation of battery electric vehicles in Norway. Transp. Res. Part A 2020, 130, 507–516. [Google Scholar] [CrossRef]

- Pettifor, H.; Wilson, C.; Axsen, J.; Abrahamse, W.; Anable, J. Social influence in the global diffusion of alternative fuel vehicles—A meta-analysis. J. Transp. Geogr. 2017, 62, 247–261. [Google Scholar] [CrossRef]

- Gnann, T.; Ploetz, P. A review of combined models for market diffusion of alternative fuel vehicles and their refueling infrastructure. Renew. Sustain. Energy Rev. 2015, 47, 783–793. [Google Scholar] [CrossRef]

- Bjerkana, Y.; Norbech, T.; Nordtomme, M. Incentives for promoting Battery Electric Vehicle (BEV) adoption in Norway. Transp. Res. Part D Transp. Environ. 2016, 43, 169–180. [Google Scholar] [CrossRef] [Green Version]

- Skowrońska-Szmer, A.; Kowalska-Pyzalska, A. Key factors of development of electromobility among microentrepreneurs: A case study from Poland. Energies 2021, 14, 764. [Google Scholar] [CrossRef]

- PSPA. Polish Alternative Fuels Association: Barometr Nowej Mobilnosci 2020/21. 2020. Available online: https://pspa.com.pl/media/2020/11/RAPORT_Barometr_Nowej_Mobilnosci_2020.pdf (accessed on 20 December 2020).

- Golas, Z.; Kurzawa, I. The application of ordered logit model in analysis of profitability of food industry sectors. Probl. Agric. Econ. 2014, 1, 78–96. [Google Scholar]

- Grilli, L.; Rampichini, C. Ordered Logit Model. In Book: Encyclopedia of Quality of Life and Well-Being; Michalos, A.C., Ed.; Springer: Berlin/Heidelberg, Germany, 2014. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Frequencies for the Sample |

|---|---|

| Gender | female 40% male 60% |

| Age | M = 36.26, SD = 11.15 |

| Education | primary school 1.0% basic vocational 4.6% secondary vocational 21.2% secondary education 14.5% higher education 56.7% |

| Material situation | very bad or rather bad 2.0% moderate 33.8% rather good or very good 63.4% |

| Place of a living | village 32.4% city up to 30,000 inh. 18.6% city 30,000 to 100,000 inh. 15.6% city 100,000 to 500,000 inh. 10.9% city more than 500,000 inh. 21.8% |

| Household size | M = 3.36, SD = 1.54 (where the integer number indicates the number of family members) |

| Driving license | M = 2.15, SD = 0.97 |

| Running business | M = 0.19, SD = 0.40 (where 1 indicates running a business and 0 representing a household) |

| Number of employees | M = 3.9, SD = 12.74 |

| How long the company exists | M = 8.8, SD = 7.13 |

| Mean | SD | |

|---|---|---|

| Environmental Attitudes and Behaviors: | ||

| Do you segregate waste? | 4.63 | 0.81 |

| Do you use reusable shopping bags? | 4.41 | 1.04 |

| Do you turn off the light while leaving the room? | 4.59 | 0.83 |

| Do you financially support any pro-environmental institutions? | 1.74 | 1.19 |

| Do you limit the usage of water in your household | 4.19 | 1.03 |

| I am satisfied with the fact that climate and environmental protection play an important role in politics | 3.87 | 1.28 |

| I would be willing to pay higher taxes to better protect the environment | 3.05 | 1.38 |

| I believe that everyone has an influence on the environment protection by one’s actions | 4.70 | 0.74 |

| I believe that the reports about the ecological crisis are exaggerated | 3.35 | 1.41 |

| HEV | PHEV | BEV |

|---|---|---|

| 1. Toyota 60.9% 2. Lexus 10.2% 3. BMW 8.0% 4. VW 5.6% 5. Honda 5.5% | 1. Toyota 41.3%. 2. BMW 7.3% 3. VW 5.4% 4. Skoda * 3.7% 5. Volvo 3.6% | 1. Tesla 36.8% 2. Toyota ** 22.7% 3. BMW 14.9% 4. Renault 14.8% 5. Nissan 14.4% |

| Ordered Logit Model | |

|---|---|

| gender | * (0.15) |

| age | (0.01) |

| education | (0.04) |

| place of living | (0.15) |

| running business | (0.15) |

| interest in technologies | * (0.05) |

| eco-behaviors and attitudes | ** (0.01) |

| knowledge of fueling HEV | (0.12) |

| knowledge of fueling PHEV | (0.12) |

| knowledge of fueling BEV | (0.21) |

| brand recognition | ** (0.07) |

| access to the charging stations | ** (0.11) |

| cut1 | (0.65) |

| cut2 | * (0.66) |

| cut3 | ** (0.67) |

| cut4 | *** (0.66) |

| cut5 | *** (0.66) |

| cut6 | *** (0.69) |

| LL | −1588.85 |

| (12) | 302.68 *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kowalska-Pyzalska, A.; Kott, M.; Kott, J. How Much Polish Consumers Know about Alternative Fuel Vehicles? Impact of Knowledge on the Willingness to Buy. Energies 2021, 14, 1438. https://doi.org/10.3390/en14051438

Kowalska-Pyzalska A, Kott M, Kott J. How Much Polish Consumers Know about Alternative Fuel Vehicles? Impact of Knowledge on the Willingness to Buy. Energies. 2021; 14(5):1438. https://doi.org/10.3390/en14051438

Chicago/Turabian StyleKowalska-Pyzalska, Anna, Marek Kott, and Joanna Kott. 2021. "How Much Polish Consumers Know about Alternative Fuel Vehicles? Impact of Knowledge on the Willingness to Buy" Energies 14, no. 5: 1438. https://doi.org/10.3390/en14051438

APA StyleKowalska-Pyzalska, A., Kott, M., & Kott, J. (2021). How Much Polish Consumers Know about Alternative Fuel Vehicles? Impact of Knowledge on the Willingness to Buy. Energies, 14(5), 1438. https://doi.org/10.3390/en14051438