Forecast of Economic Tight Oil and Gas Production in Permian Basin

Abstract

:1. Introduction

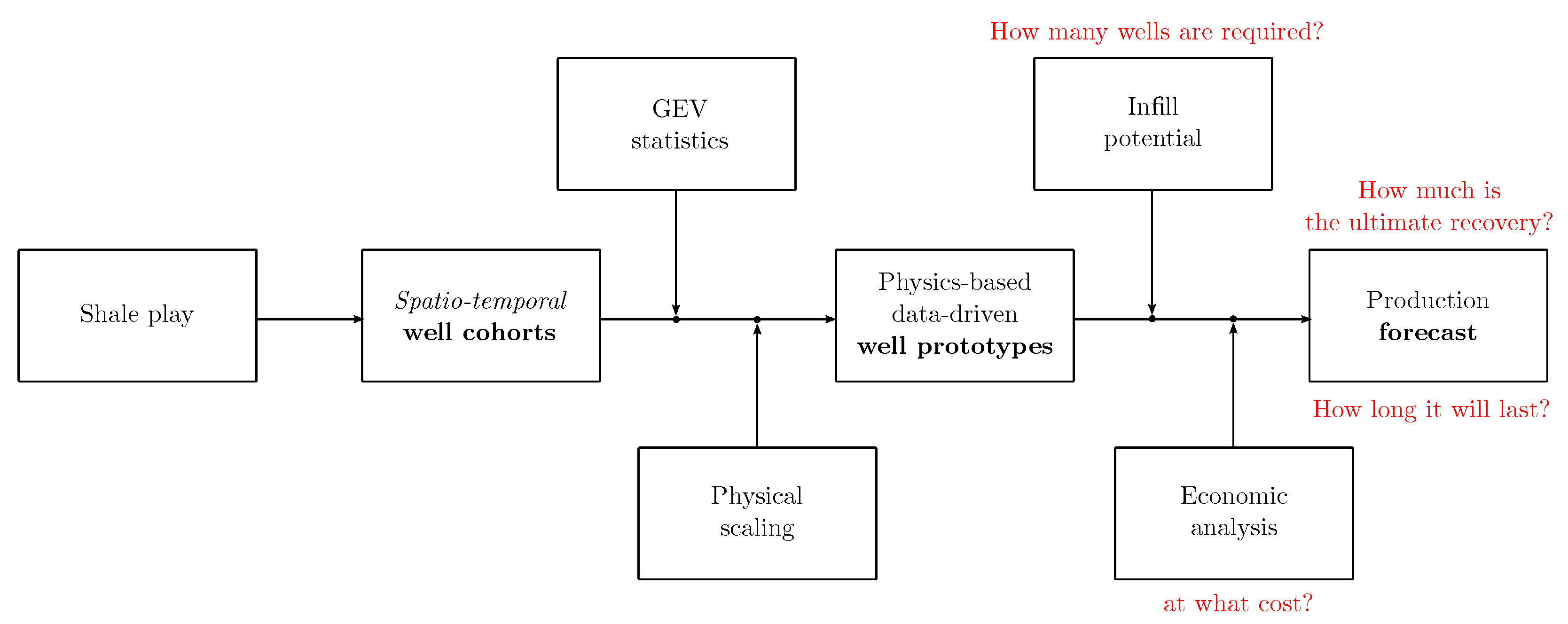

2. Results

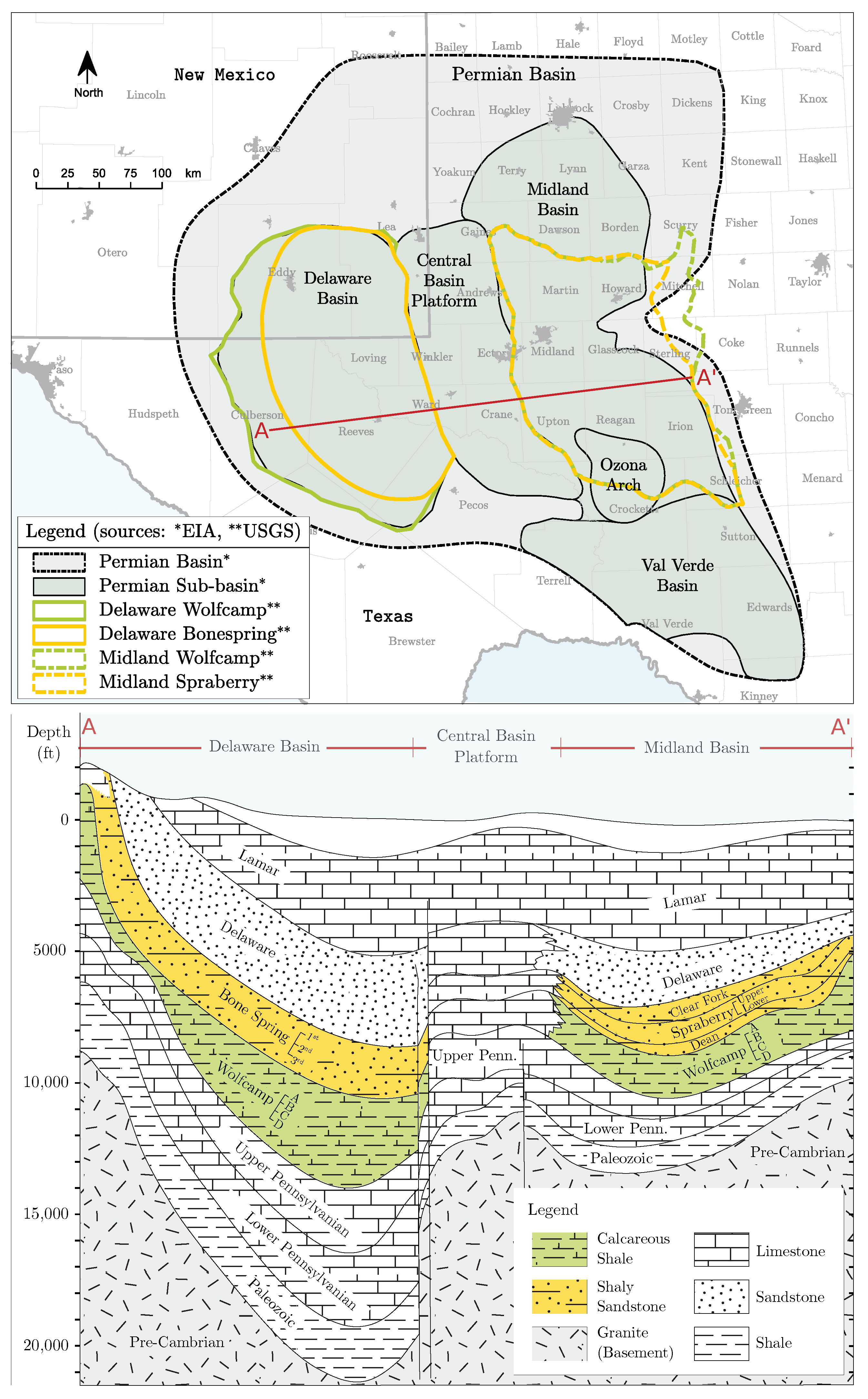

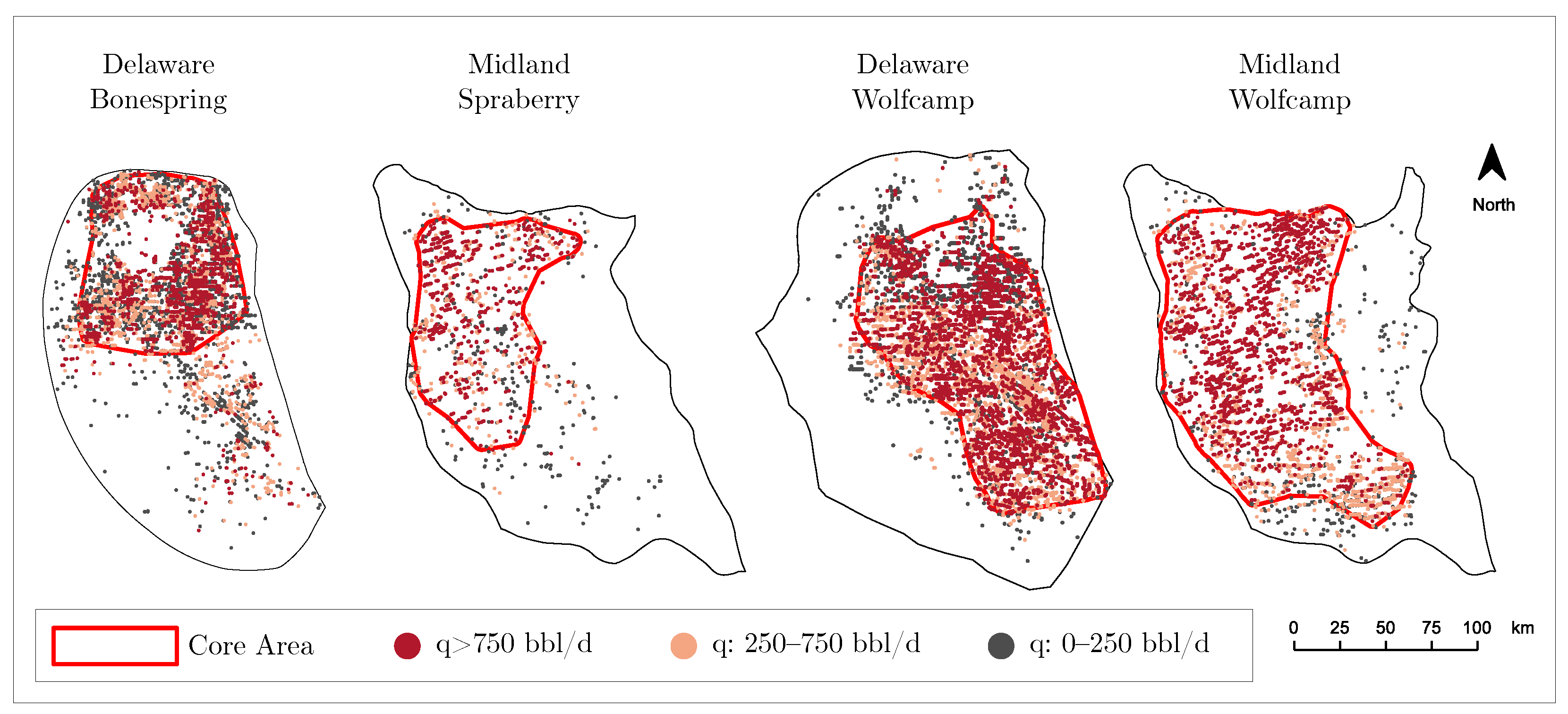

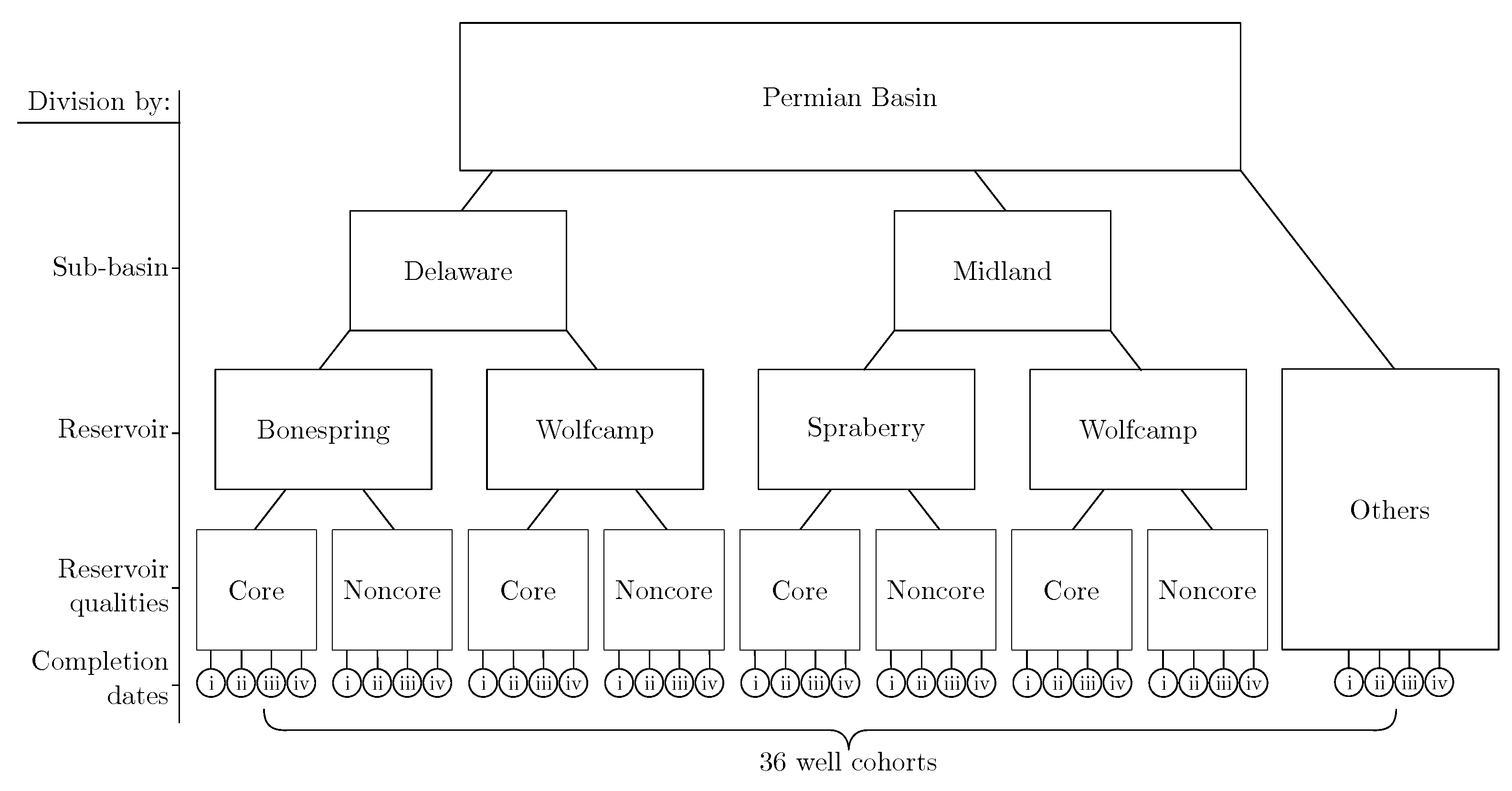

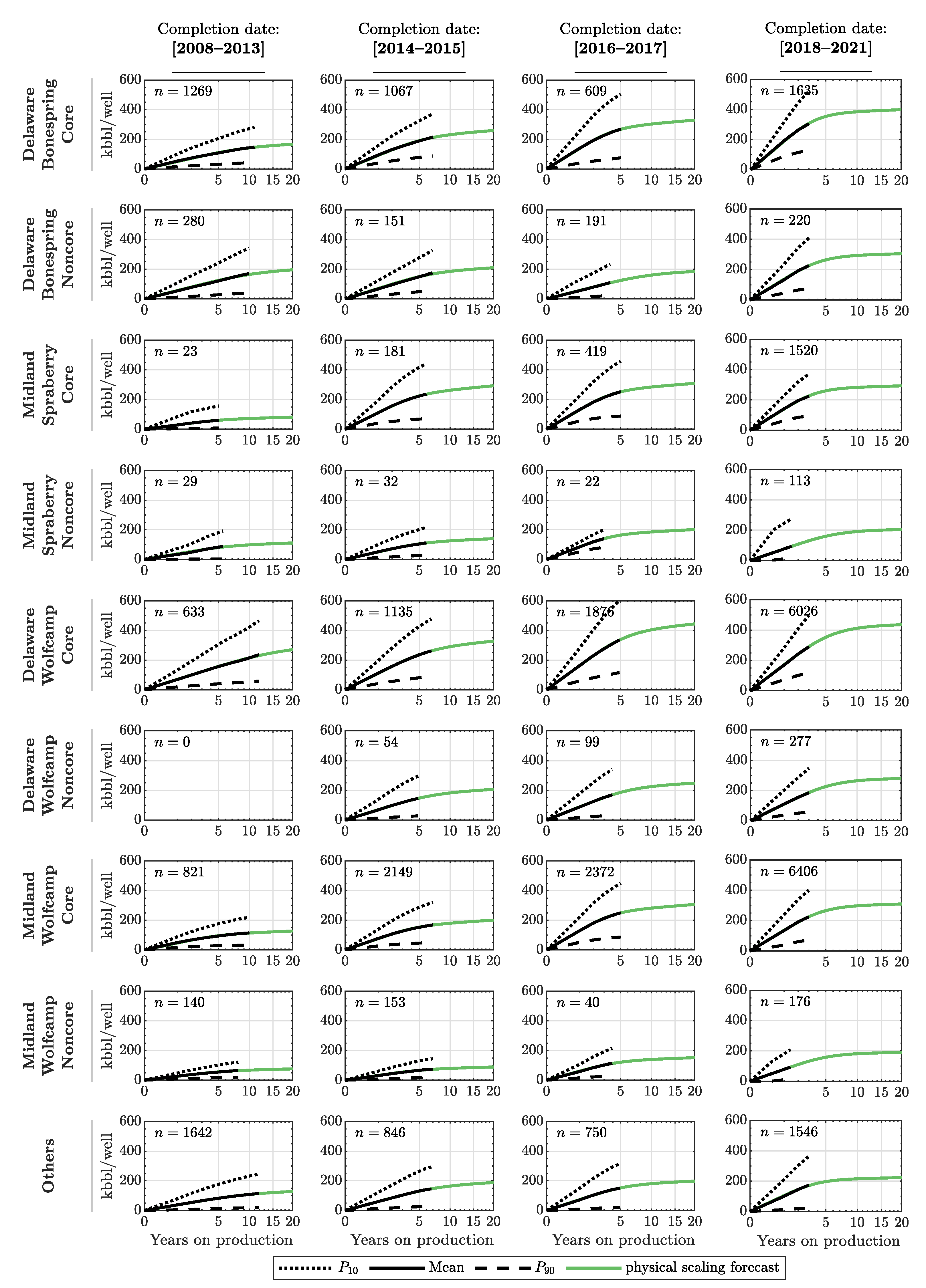

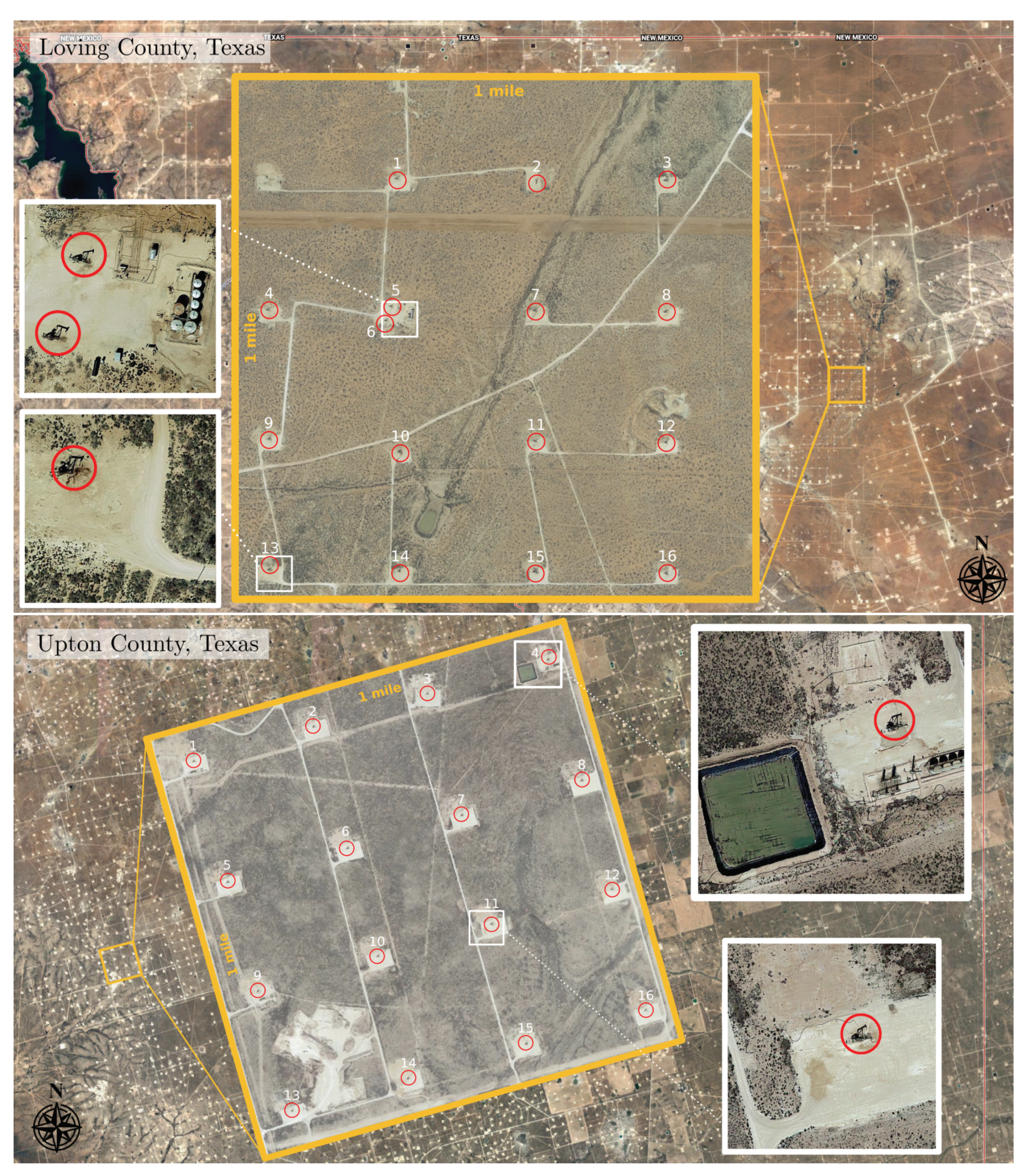

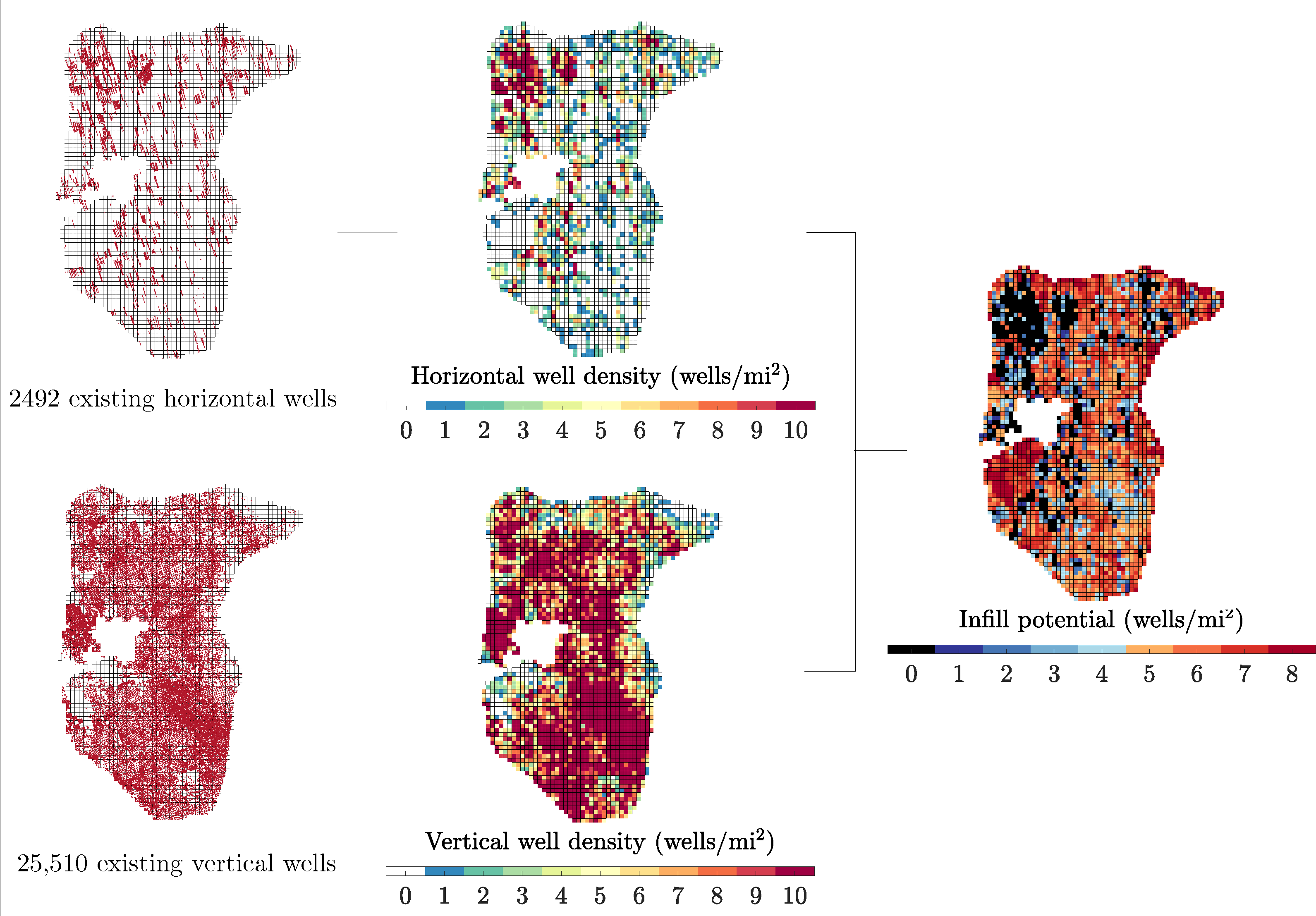

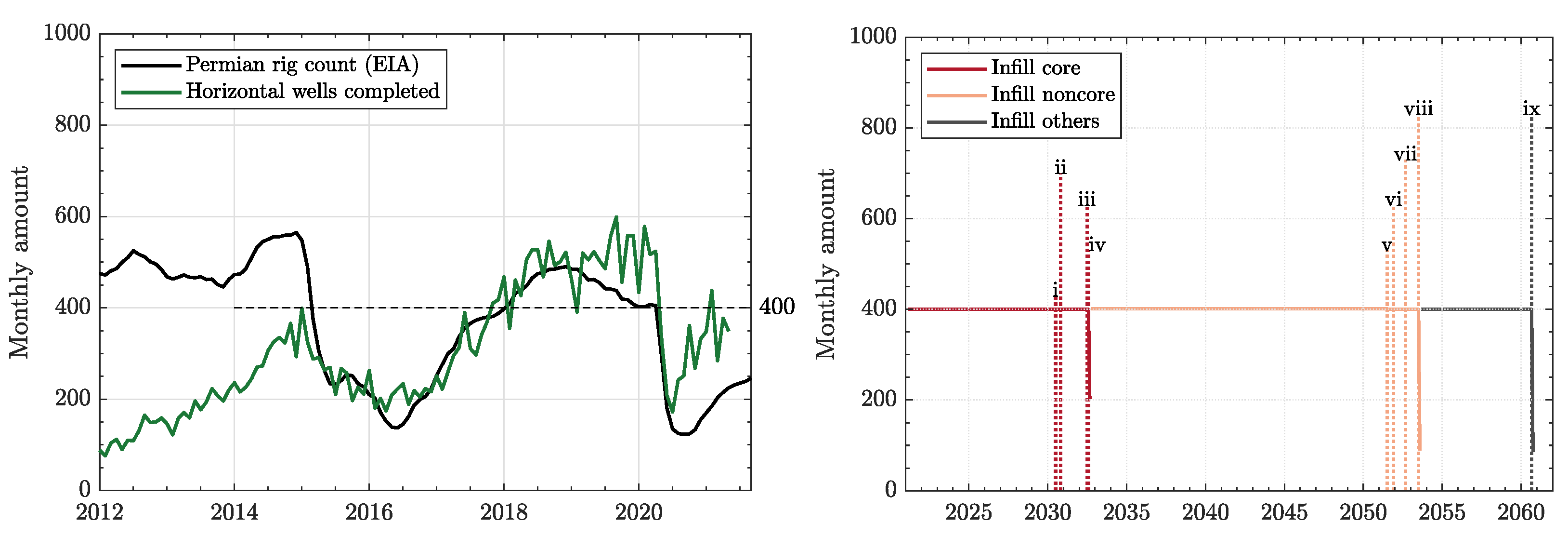

2.1. Design of Spatio-Temporal Well Cohorts

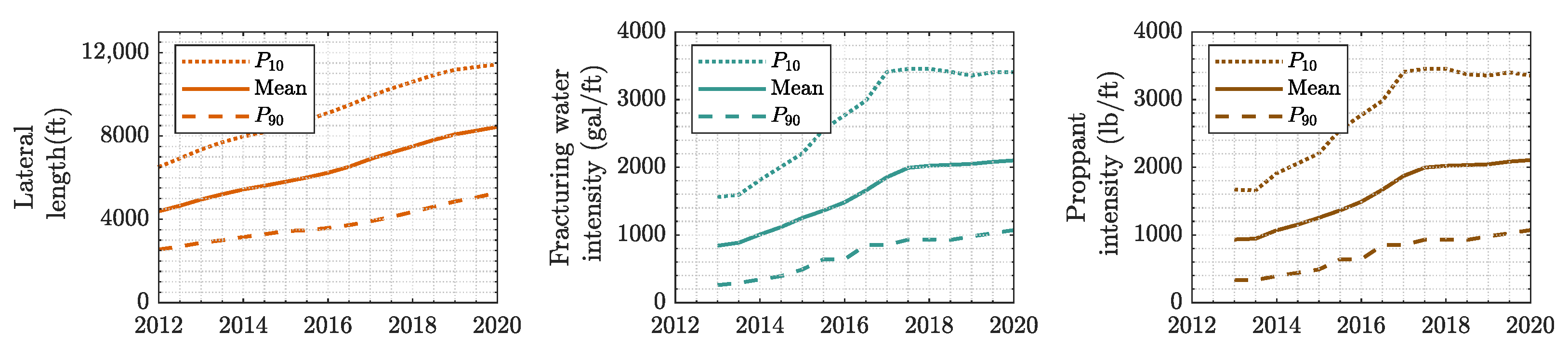

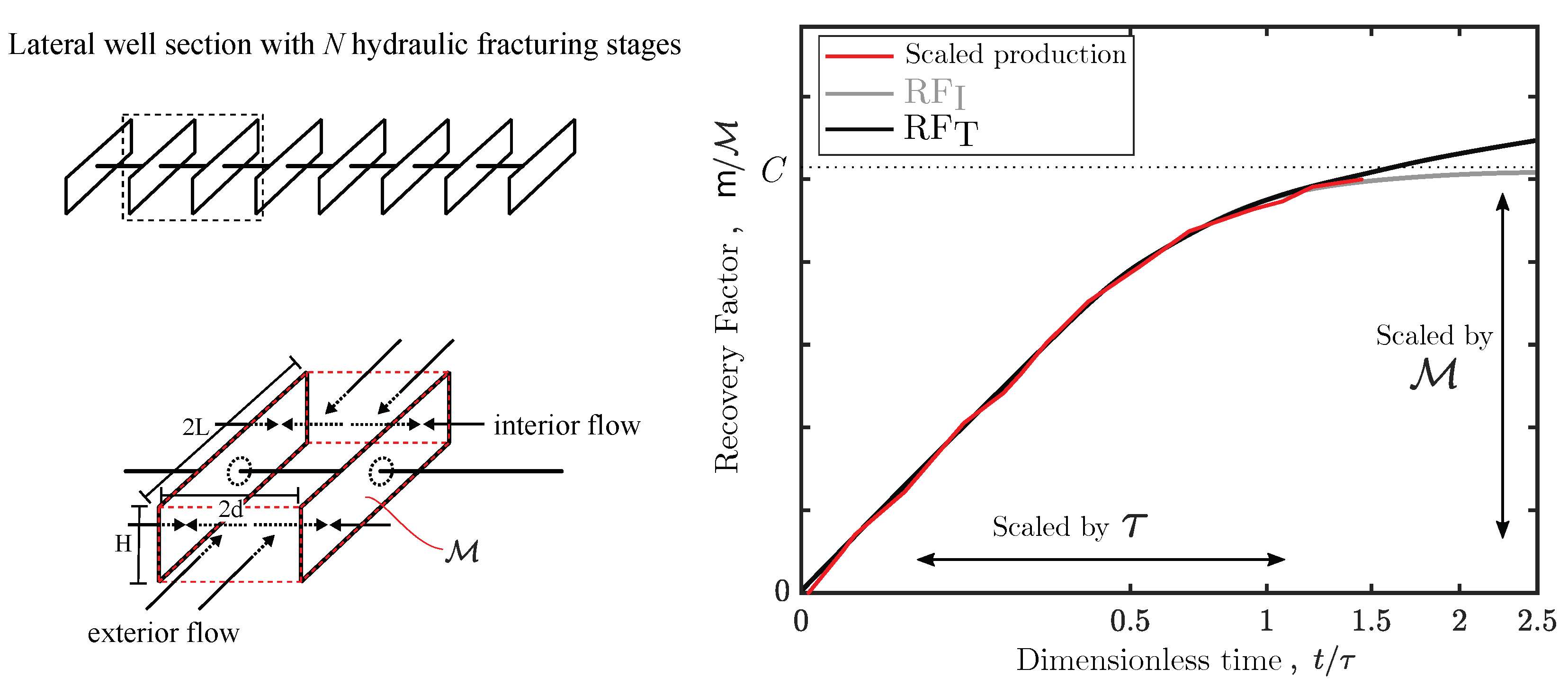

2.2. Physics-Based Data-Driven Well Prototypes

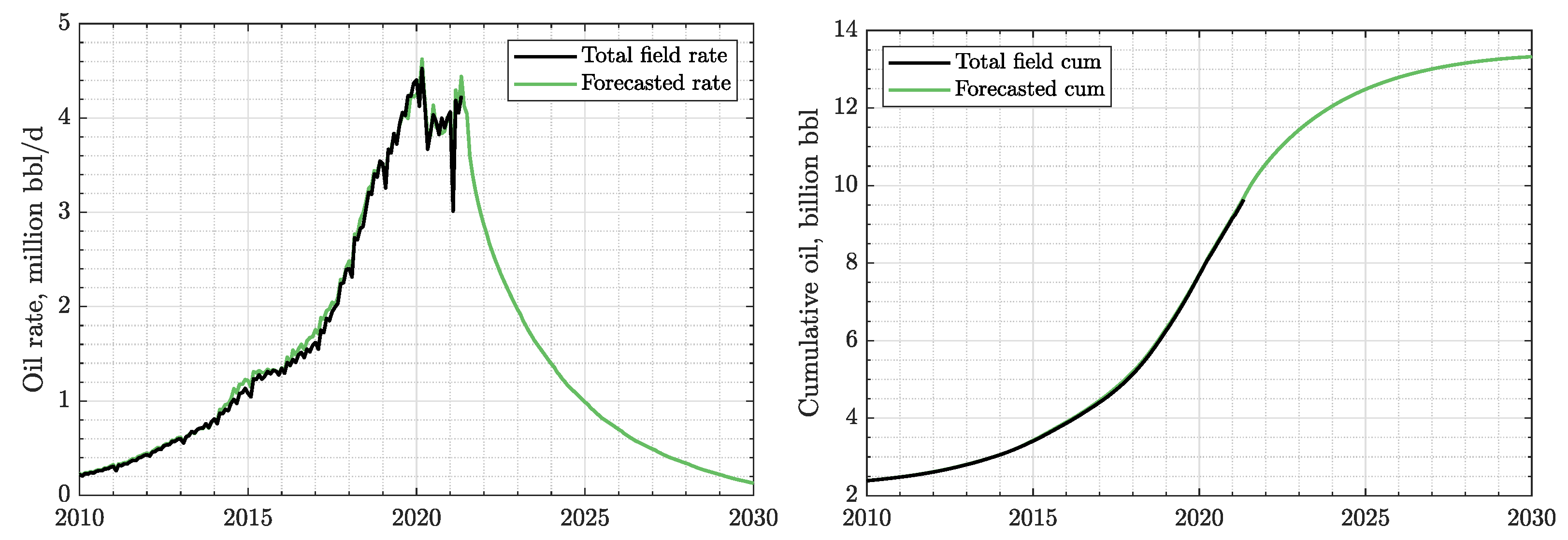

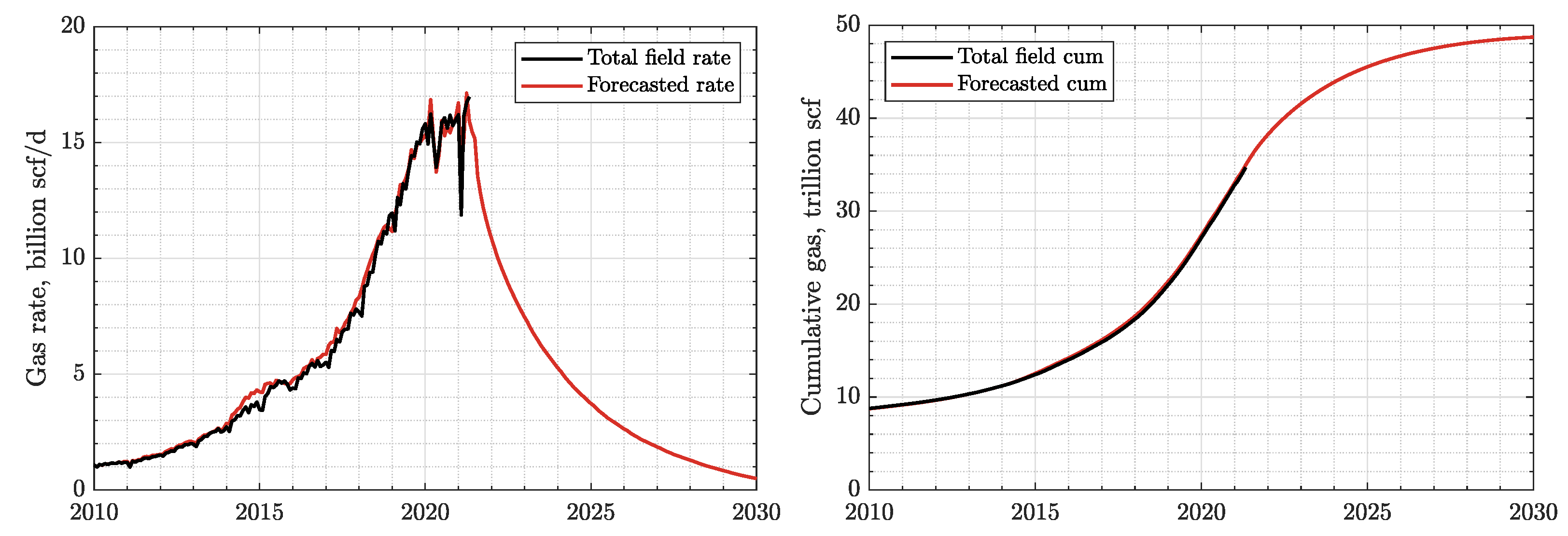

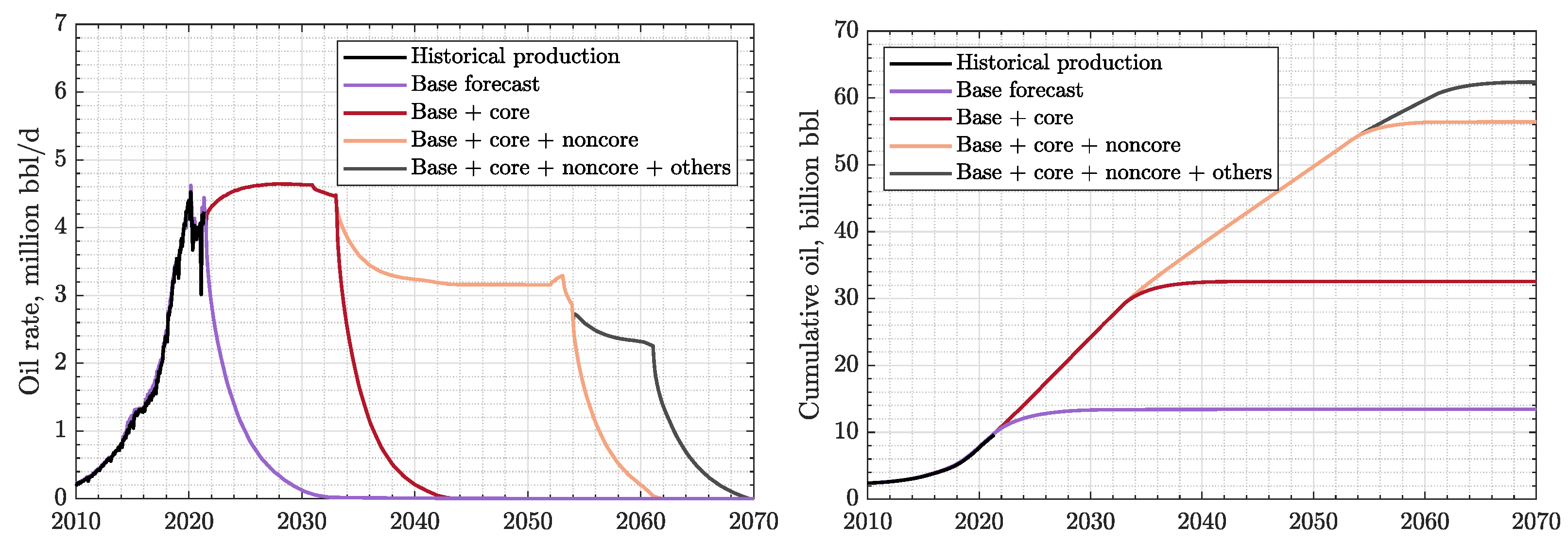

2.3. Production Forecast

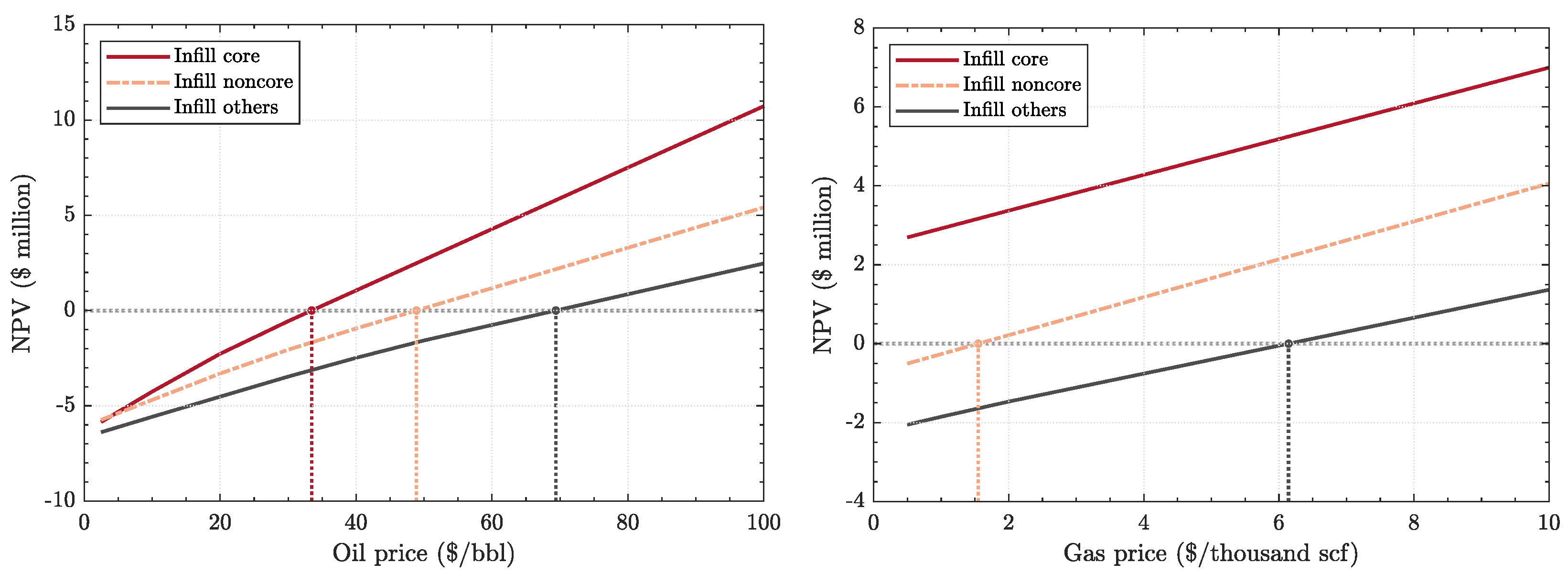

2.4. Economic Analysis

3. Discussion

4. Materials and Methods

- We divide all 53,708 horizontal hydrofractured tight oil wells in the Permian into 36 spatiotemporal well cohorts, in which oil production is statistically uniform. The number 36 is the product of nine reservoir qualities and four completion date intervals;

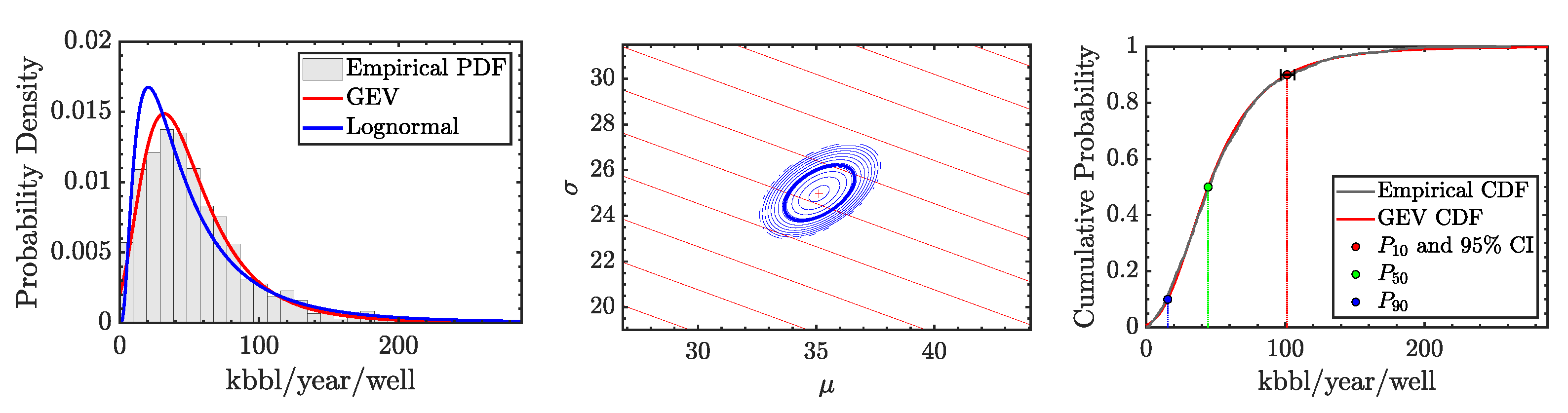

- For each cohort, we sample each oil of oil production of its wells and fit the resulting empirical distribution with a generalized extreme value (GEV) distribution, see Appendix A. We construct historical well prototypes as the expected (mean) values of the annual GEV distribution. Next, we use physical scaling to extrapolate the prototypes for several more decades, see Appendix B. We determine the data-driven well survival probabilities to make our prototypes even more realistic, see Appendix C;

- We replace the actual field production rate from all existing groups of wells in the Permian with their corresponding well prototypes. The summation of all the prototypes is now the ‘base’ or ‘do-nothing’ forecast of the Permian tight oil wells. To obtain the infill forecasts, we first calculate the probability of success and infill potential (see Appendix C). Then, we schedule future drilling programs. We calculate the net present value (NPV) (see Appendix D) to evaluate the profitability of each future drilling program.

5. Conclusions

- We have provided an optimal play-wide assessment of the Permian tight reservoirs by considering play geology, advancement of well completion technologies, physics of hydrocarbon production from the horizontal hydrofractured wells, well attrition, and economics of drilling projects;

- Our mean Generalized Extreme Value statistics well prototypes are robust and in excellent agreement with the physics-based scaling curves. Using these prototypes, we were able to match rather well the historical oil and gas production from the entire Permian Basin;

- Both the Delaware Bonespring Core and the Delaware Wolfcamp Core give the highest estimated ultimate recovery, because these two formations are thicker and more mature than those in the Midland Basin;

- The newer wells yield significantly higher EURs due to longer laterals and bigger hydraulic fractures. However, in areas of poor reservoir quality, these advancements of completion technologies do not help much;

- We estimate that the total recoverable oil in the Permian tight reservoirs is 54.4–62.4 billion bbl, and the total recoverable gas is 246–285 trillion scf;

- Operators might consider abstaining from drilling in the ‘Others’ area of the Permian, because it may be unprofitable for all scenarios we considered;

- It is most likely that Permian will continue to be the most prolific oil play in the U.S. and will surpass the declining giant Marcellus shale in producing natural gas. However, we should not assume that hydrocarbon production from the Permian will last for centuries and keep on subsidizing our energy demands.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Abbreviations

| CDF | Cumulative Distribution Function |

| DCA | Decline Curve Analysis |

| EUR | Estimated Ultimate Recovery |

| GEV | Generalized Extreme Value |

| GOR | Gas to Oil Ratio |

| NPV | Net Present Value |

| Probability Density Function | |

| RF | Recovery Factor |

| SRV | Stimulated Reservoir Volume |

| WC | Watercut |

Appendix A. Generalized Extreme Value (GEV) Distribution

Appendix B. Physical Scaling of Oil Flow towards Hydrofractured Shale Wells

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Region | Delaware Bonespring | Midland Spraberry | Delaware Wolfcamp | Midland Wolfcamp | Others |

|---|---|---|---|---|---|

| TVD (ft) | 9700 | 8700 | 11,200 | 8800 | 6300 |

| (psi) | 7760 | 5220 | 8960 | 5280 | 4410 |

| 0.44 | 0.37 | 0.44 | 0.37 | 0.37 | |

| C | 0.163 | 0.117 | 0.192 | 0.118 | 0.094 |

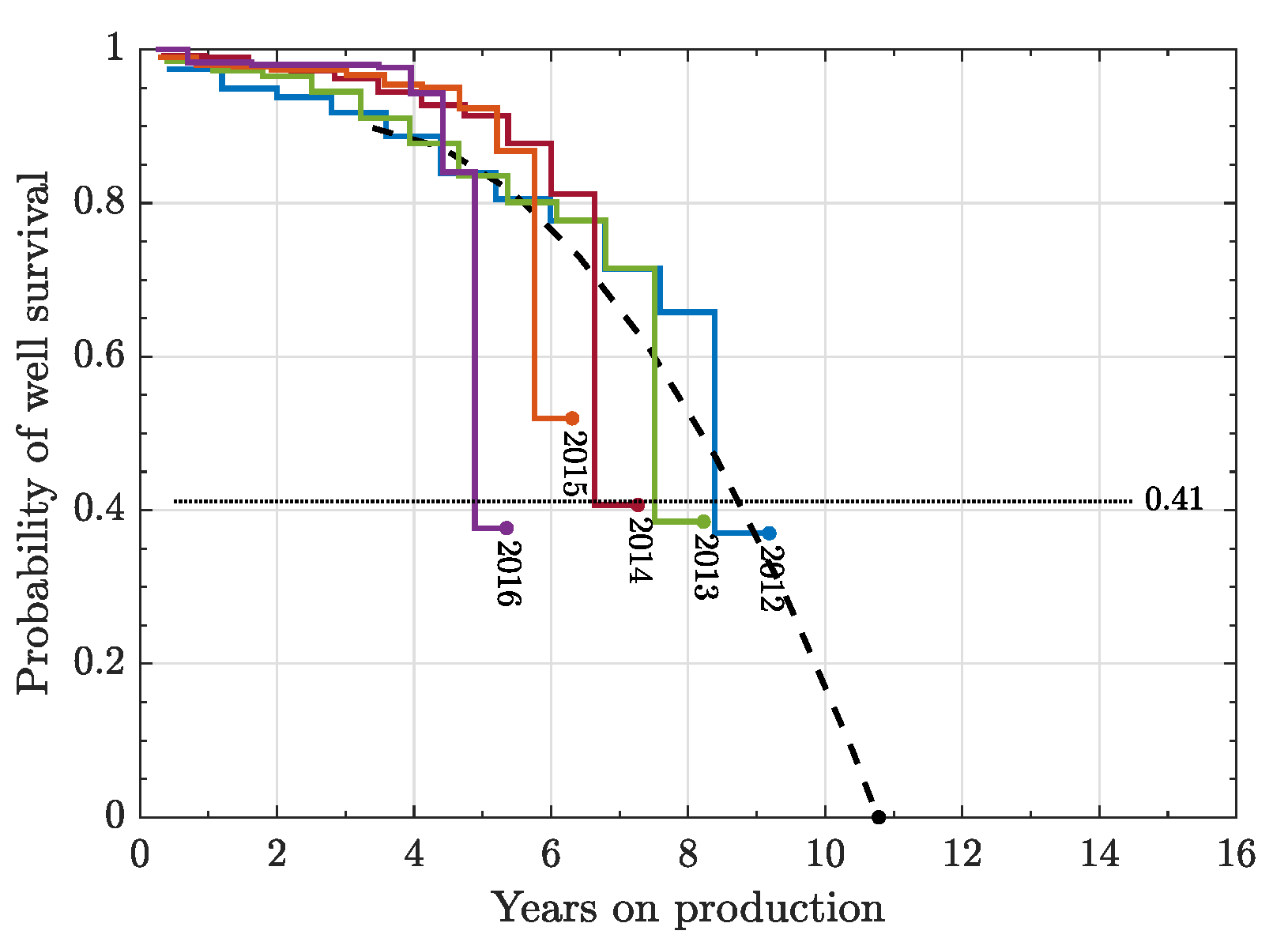

Appendix C. Calculating Probability of Well Survival, Probability of Success, and Infill Potential

Appendix D. Calculating NPV

References

- Fox, K. The Energy Crisis Couldn’t Have Come at a Worse Time for Climate. 2021. Available online: https://edition.cnn.com/2021/10/08/business/energy-crisis-climate-fossil-fuels-renewables-cop26-cmd-intl/index.html (accessed on 10 October 2021).

- Looney, B. Statistical Review of World Energy 2021, 70th ed.; BP Statistical Review: London, UK, 2021; Volume 70, p. 66. [Google Scholar]

- Nalley, S.; LaRose, A.; Energy Information Administration (EIA). International Energy Outlook 2021 (IEO2021); Energy Information Administration (EIA): Washington, DC, USA, 2021; Volume 10, p. 9. [Google Scholar]

- Nalley, S.; LaRose, A.; Energy Information Administration (EIA). Annual Energy Outlook 2021(AEO2021): Petroleum and other liquids. In Annual Energy Outlook; US Energy Information Administration: Washington, DC, USA, 2021; Volume 2, p. 4. [Google Scholar]

- Saputra, W.; Kirati, W.; Patzek, T.W. Generalized extreme value statistics, physical scaling and forecasts of oil production from all vertical wells in the Permian Basin. Energies 2021. submitted. [Google Scholar]

- Gaswirth, S.B.; French, K.L.; Pitman, J.K.; Marra, K.R.; Mercier, T.J.; Leathers-Miller, H.M.; Schenk, C.J.; Tennyson, M.E.; Woodall, C.A.; Brownfield, M.E.; et al. Assessment of Undiscovered Continuous Oil and Gas Resources in the Wolfcamp Shale and Bone Spring Formation of the Delaware Basin, Permian Basin Province, New Mexico and Texas, 2018; US Geological Survey: Reston, VA, USA, 2018. [Google Scholar] [CrossRef]

- Nalley, S.; LaRose, A.; Energy Information Administration. Assumptions to the Annual Energy Outlook 2021: Oil and Gas Supply Module. In Annual Energy Outlook; US Energy Information Administration: Washington, DC, USA, 2021; p. 4. [Google Scholar]

- Patzek, T.W.; Saputra, W.; Kirati, W.; Marder, M. Generalized Extreme Value Statistics, Physical Scaling, and Forecasts of Gas Production in the Barnett Shale. Energy Fuels 2019, 33, 12154–12169. [Google Scholar] [CrossRef]

- Saputra, W.; Kirati, W.; Patzek, T. Generalized Extreme Value Statistics, Physical Scaling and Forecasts of Oil Production in the Bakken Shale. Energies 2019, 12, 3641. [Google Scholar] [CrossRef] [Green Version]

- Saputra, W.; Kirati, W.; Patzek, T.W. Generalized extreme value statistics, physical scaling and forecasts of gas production in the Haynesville shale. J. Nat. Gas Sci. Eng. 2021, 94, 104041. [Google Scholar] [CrossRef]

- Saputra, W.; Kirati, W.; Hughes, D.; Patzek, T.W. Forecast of Economic Gas production in the Marcellus. AAPG Bull. 2021. accepted. [Google Scholar]

- Fréchet, M. Sur la loi de probabilité de l’écart maximum. Ann. Soc. Math. Polon. 1927, 6, 93–116. [Google Scholar]

- Gumbel, E.J. Statistical theory of extreme values and some practical applications. NBS Appl. Math. Ser. 1954, 33., 19–33. [Google Scholar]

- Weibull, W. A statistical distribution function of wide applicability. J. Appl. Mech. 1951, 18, 293–297. [Google Scholar] [CrossRef]

- Patzek, T.W.; Male, F.; Marder, M. From the Cover: Cozzarelli Prize Winner: Gas production in the Barnett Shale obeys a simple scaling theory. Proc. Natl. Acad. Sci. USA 2013, 110, 19731–19736. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Patzek, T.W.; Male, F.; Marder, M. A simple model of gas production from hydrofractured horizontal wells in shales. AAPG Bull. 2014, 98, 2507–2529. [Google Scholar] [CrossRef]

- Patzek, T.W.; Saputra, W.; Kirati, W. A Simple Physics-Based Model Predicts Oil Production from Thousands of Horizontal Wells in Shales. In Proceedings of the SPE Annual Technical Conference and Exhibition, San Antonio, TX, USA, 9–11 October 2017. [Google Scholar]

- Saputra, W.; Kirati, W.; Patzek, T. Physical Scaling of Oil Production Rates and Ultimate Recovery from All Horizontal Wells in the Bakken Shale. Energies 2020, 13, 2052. [Google Scholar] [CrossRef] [Green Version]

- Arps, J. Analysis of Decline Curves. Trans. AIME 1945, 160, 228–247. [Google Scholar] [CrossRef]

- Saputra, W.; Albinali, A.A. Validation of the Generalized Scaling Curve Method for EUR Prediction in Fractured Shale Oil Wells. In Proceedings of the SPE Kingdom of Saudi Arabia Annual Technical Symposium and Exhibition, Dammam, Saudi Arabia, 23–26 April 2018. [Google Scholar]

- EIA. Maps: Oil and Gas Exploration, Resources, and Production; US Energy Information Administration: Washington, DC, USA, 2021. [Google Scholar]

- Male, F. Using a segregated flow model to forecast production of oil, gas, and water in shale oil plays. J. Pet. Sci. Eng. 2019, 180, 48–61. [Google Scholar] [CrossRef]

- Berman, A. Giant Wolfcamp Oil Field Would Lose $500 Billion at Today’s Prices. 2016. Available online: https://www.forbes.com/sites/arthurberman/2016/11/20/permian-giant-oil-field-would-lose-500-billion-at-todays-prices/ (accessed on 1 October 2021).

- Xiong, H.; Ramanthan, R.; Nguyen, K. Maximizing Asset Value by Full Field Development—Case Studies in the Permian Basin. In Proceedings of the 7th Unconventional Resources Technology Conference, Brisbane, Australia, 18–19 November 2019; American Association of Petroleum Geologists: Tulsa, OK, USA, 2019. [Google Scholar]

- Equity, O.G. Drilling & Completion Facts. 2021. Available online: https://www.oilgasequity.com/resources/drilling-completion-facts/ (accessed on 1 October 2021).

- EIA. Trends in US Oil and Natural Gas Upstream Costs; US Energy Information Administration: Washington, DC, USA, 2016. [Google Scholar]

- Observer, G. Abandoned Oil Gas Wells Permian Texas-New Mexico. 2021. Available online: https://grist.org/abandoned-oil-gas-wells-permian-texas-new-mexico/ (accessed on 1 October 2021).

- Gentile, N. Federal Oil and Gas Royalty and Revenue Reform. 2021. Available online: https://www.americanprogress.org/issues/green/reports/2015/06/19/115580/federal-oil-and-gas-royalty-and-revenue-reform/ (accessed on 1 October 2021).

- Eftekhari, B.; Marder, M.; Patzek, T.W. Field data provide estimates of effective permeability, fracture spacing, well drainage area and incremental production in gas shales. J. Nat. Gas Sci. Eng. 2018, 56, 141–151. [Google Scholar] [CrossRef]

| Region | (Years) | EUR (kbbl/well) | ||||||

|---|---|---|---|---|---|---|---|---|

| (i) | (ii) | (iii) | (iv) | (i) | (ii) | (iii) | (iv) | |

| Delaware Bonespring Core | 11.9 | 7.8 | 5.3 | 5.0 | 178 | 277 | 349 | 407 |

| Delaware Bonespring Noncore | 13.7 | 8.9 | 12.3 | 5.8 | 210 | 224 | 195 | 311 |

| Midland Spraberry Core | 7.2 | 6.1 | 5.2 | 5.0 | 87 | 314 | 327 | 299 |

| Midland Spraberry Noncore | 8.3 | 7.0 | 5.2 | 8.6 | 119 | 150 | 214 | 208 |

| Delaware Wolfcamp Core | 19.8 | 8.5 | 7.6 | 7.7 | 295 | 350 | 467 | 445 |

| Delaware Wolfcamp Noncore | - | 8.9 | 8.3 | 7.7 | - | 220 | 261 | 286 |

| Midland Wolfcamp Core | 6.7 | 6.2 | 5.2 | 6.0 | 137 | 215 | 325 | 316 |

| Midland Wolfcamp Noncore | 7.7 | 7.1 | 6.0 | 6.9 | 82 | 95 | 161 | 194 |

| Others | 12.9 | 10.1 | 7.5 | 5.2 | 137 | 201 | 209 | 229 |

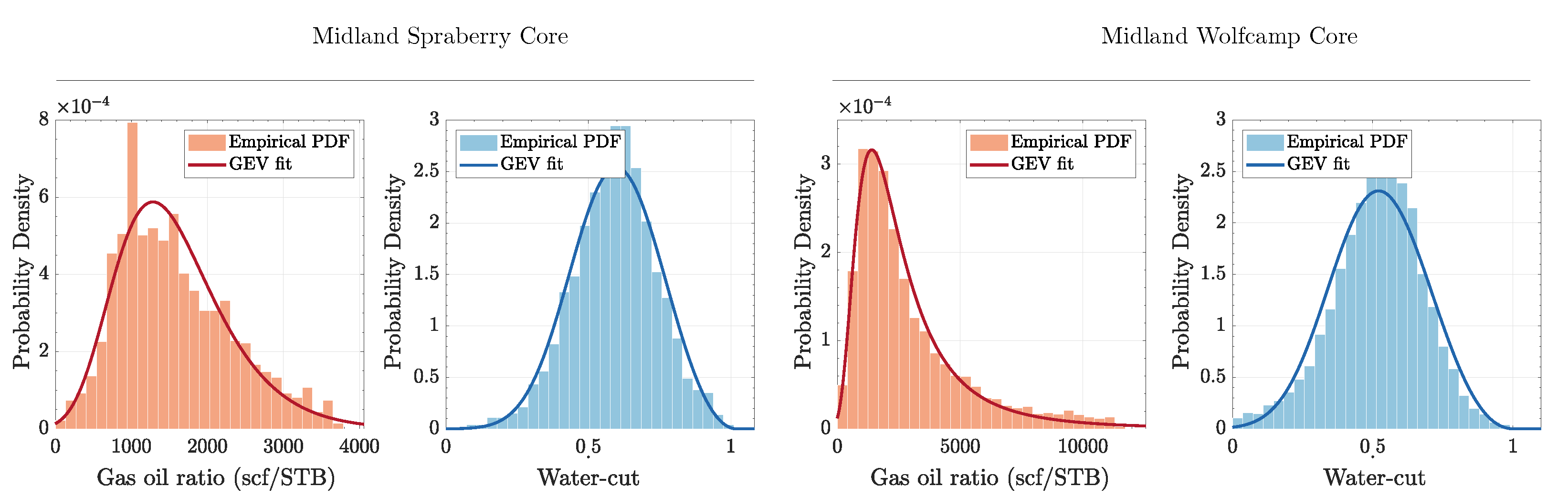

| Region | Gas Oil Ratio (scf/stb) | Water Cut |

|---|---|---|

| Delaware Bonespring Core | 3058 | 0.54 |

| Delaware Bonespring Noncore | 2809 | 0.64 |

| Midland Spraberry Core | 1574 | 0.59 |

| Midland Spraberry Noncore | 3949 | 0.51 |

| Delaware Wolfcamp Core | 3285 | 0.67 |

| Delaware Wolfcamp Noncore | 6965 | 0.70 |

| Midland Wolfcamp Core | 3019 | 0.52 |

| Midland Wolfcamp Noncore | 4430 | 0.57 |

| Others | 4385 | 0.63 |

| Region | Survival Time (Years) | Probability of Success | Max. Density (wells/mi2) | Infill Potential |

|---|---|---|---|---|

| Delaware Bonespring Core | 10.8 | 0.82 | 12 | 6946 |

| Delaware Bonespring Noncore | 8.7 | 0.82 | 12 | 28,425 |

| Midland Spraberry Core | 8.7 | 0.72 | 8 | 4712 |

| Midland Spraberry Noncore | 7.3 | 0.76 | 8 | 18,681 |

| Delaware Wolfcamp Core | 11.0 | 0.79 | 16 | 17,550 |

| Delaware Wolfcamp Noncore | 9.7 | 0.79 | 12 | 32,780 |

| Midland Wolfcamp Core | 10.0 | 0.87 | 16 | 26,195 |

| Midland Wolfcamp Noncore | 9.2 | 0.75 | 12 | 20,429 |

| Others | 8.6 | 0.33 | 4 | 34,086 |

| Parameters | Notations | Units | Values | Notes |

|---|---|---|---|---|

| Drilling & comp. cost | DRILL | $ million | 6.0 | Delaware Bonespring |

| 6.4 | Midland Spraberry | |||

| 8.9 | Delaware Wolfcamp | |||

| 7.0 | Midland Wolfcamp | |||

| 6.9 | Others | |||

| Land acquisition cost | LAND | $ million | 0.5 | |

| Plug & abandon. cost | PLUG | $ million | 0.3 | |

| Operating cost | OPEX | $/bbl | 0.7 | Oil |

| $/bbl | 0.5 | Water | ||

| $/kscf | 0.1 | Gas | ||

| Severance tax rate | TAXS | $/kscf | 0.05 | |

| Corporate tax rate | TAXC | frac./year | 0.25 | |

| Intangible expend. | INTAN | frac./year | 0.5 | |

| Royalty rate | ROY | frac./year | 0.15 | |

| Discount rate | DIS | frac./year | 0.08 |

| Region | Existing | Remaining Resources | Est. Ultimate Recovery | ||||

|---|---|---|---|---|---|---|---|

| Wells | Mean | Mean | |||||

| (Gbbl) | (Gbbl) | (Gbbl) | (Gbbl) | (Gbbl) | (Gbbl) | (Gbbl) | |

| Delaware Bonespring Core | 1.0 | 4.6 | 3.0 | 1.1 | 5.6 | 4.0 | 2.1 |

| Delaware Bonespring Noncore | 0.2 | 14.8 | 8.3 | 2.7 | 15.0 | 8.5 | 2.9 |

| Midland Spraberry Core | 1.6 | 2.2 | 1.6 | 0.5 | 3.8 | 3.2 | 2.2 |

| Midland Spraberry Noncore | 0.6 | 9.8 | 3.4 | 0.6 | 10.4 | 3.9 | 1.2 |

| Delaware Wolfcamp Core | 2.4 | 12.5 | 8.8 | 3.0 | 14.9 | 11.2 | 5.3 |

| Delaware Wolfcamp Noncore | 0.1 | 16.2 | 8.7 | 2.7 | 16.3 | 8.8 | 2.7 |

| Midland Wolfcamp Core | 2.3 | 13.8 | 8.7 | 2.5 | 16.1 | 11.0 | 4.8 |

| Midland Wolfcamp Noncore | 0.1 | 8.2 | 3.7 | 0.6 | 8.3 | 3.8 | 0.7 |

| Others | 1.6 | 12.5 | 6.3 | 0.8 | 14.1 | 7.9 | 2.4 |

| TOTAL | 9.9 | 94.6 | 52.5 | 14.5 | 104.5 | 62.4 | 24.4 |

| TOTAL Core + Noncore | 8.3 | 82.2 | 46.2 | 13.7 | 90.4 | 54.4 | 22.0 |

| Region | Existing | Remaining Resources | Est. Ultimate Recovery | ||||

|---|---|---|---|---|---|---|---|

| Wells | Mean | Mean | |||||

| (Tscf) | (Tscf) | (Tscf) | (Tscf) | (Tscf) | (Tscf) | (Tscf) | |

| Delaware Bonespring Core | 4.0 | 16.8 | 10.5 | 4.2 | 20.8 | 14.5 | 8.1 |

| Delaware Bonespring Noncore | 0.5 | 50.0 | 27.8 | 9.2 | 50.4 | 28.3 | 9.7 |

| Midland Spraberry Core | 3.7 | 4.1 | 3.1 | 1.0 | 7.8 | 6.8 | 4.7 |

| Midland Spraberry Noncore | 2.4 | 46.5 | 16.0 | 2.9 | 48.9 | 18.4 | 5.2 |

| Delaware Wolfcamp Core | 11.0 | 49.4 | 33.9 | 11.7 | 60.4 | 44.9 | 22.6 |

| Delaware Wolfcamp Noncore | 0.8 | 135.4 | 72.6 | 22.2 | 136.2 | 73.4 | 23.0 |

| Midland Wolfcamp Core | 7.0 | 50.1 | 32.5 | 9.0 | 57.1 | 39.5 | 16.0 |

| Midland Wolfcamp Noncore | 0.5 | 43.4 | 19.8 | 3.0 | 43.9 | 20.3 | 3.6 |

| Others | 5.9 | 65.7 | 33.1 | 4.3 | 71.5 | 39.0 | 10.2 |

| TOTAL | 35.7 | 461.5 | 249.3 | 67.5 | 497.2 | 285.0 | 103.2 |

| TOTAL Core + Noncore | 29.8 | 395.8 | 216.2 | 63.2 | 425.6 | 246.1 | 93.0 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Saputra, W.; Kirati, W.; Patzek, T. Forecast of Economic Tight Oil and Gas Production in Permian Basin. Energies 2022, 15, 43. https://doi.org/10.3390/en15010043

Saputra W, Kirati W, Patzek T. Forecast of Economic Tight Oil and Gas Production in Permian Basin. Energies. 2022; 15(1):43. https://doi.org/10.3390/en15010043

Chicago/Turabian StyleSaputra, Wardana, Wissem Kirati, and Tadeusz Patzek. 2022. "Forecast of Economic Tight Oil and Gas Production in Permian Basin" Energies 15, no. 1: 43. https://doi.org/10.3390/en15010043

APA StyleSaputra, W., Kirati, W., & Patzek, T. (2022). Forecast of Economic Tight Oil and Gas Production in Permian Basin. Energies, 15(1), 43. https://doi.org/10.3390/en15010043