Statistical and Artificial Neural Networks Models for Electricity Consumption Forecasting in the Brazilian Industrial Sector

,

,  ,

,  , and

, and

Abstract

:1. Introduction

2. Methodology

2.1. Statistical Models

2.1.1. Holt–Winters Method

2.1.2. SARIMA

2.1.3. Dynamic Linear Model

2.1.4. Trignometric Box–Cox Transform, ARMA Errors, Trend, and Seasonal Components (TBATS)

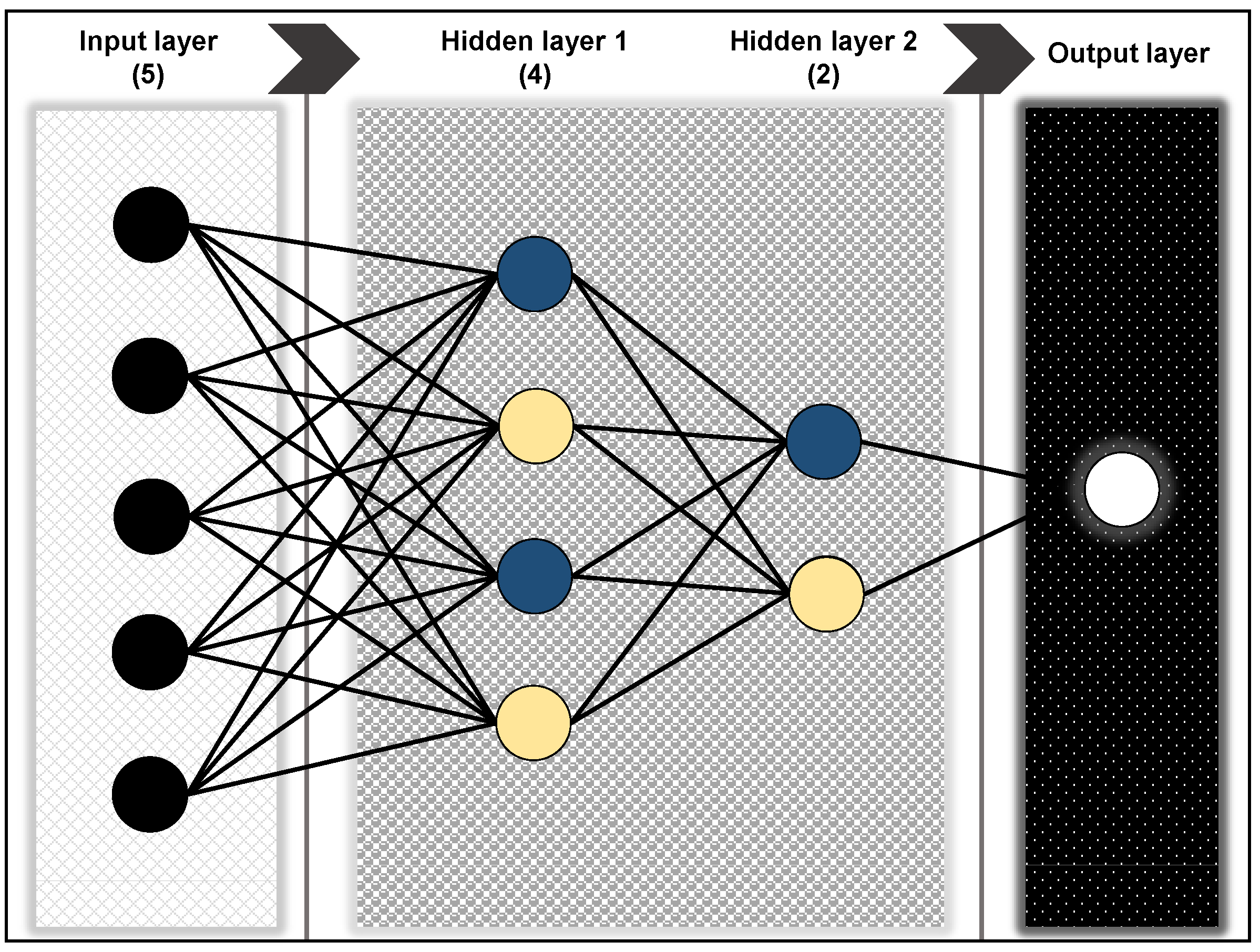

2.2. Artificial Neural Networks Approach

2.2.1. Autoregressive Neural Networks (NNAR)

2.2.2. Multilayer Perceptron (MLP)

2.3. Mean Absolute Percentage Error (MAPE)

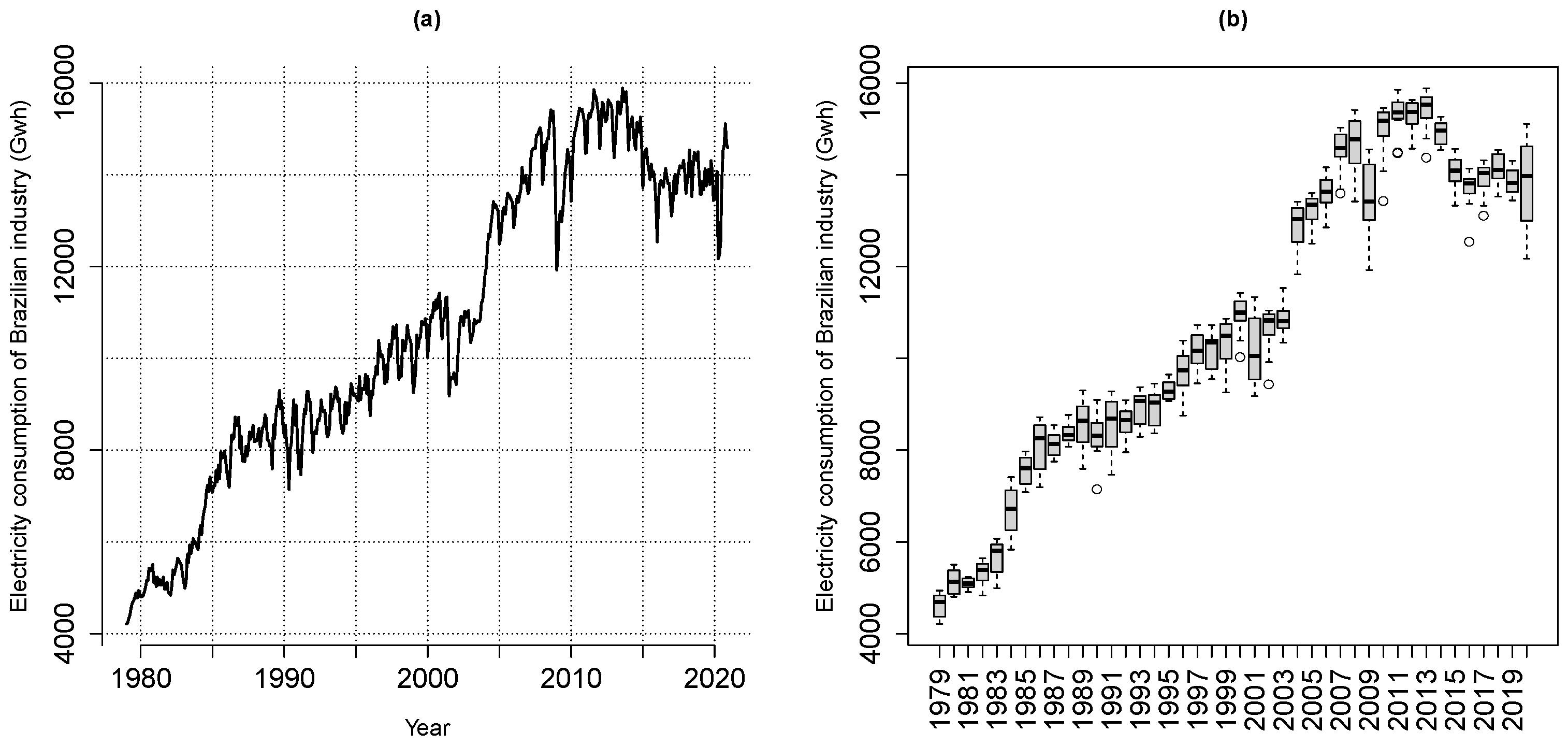

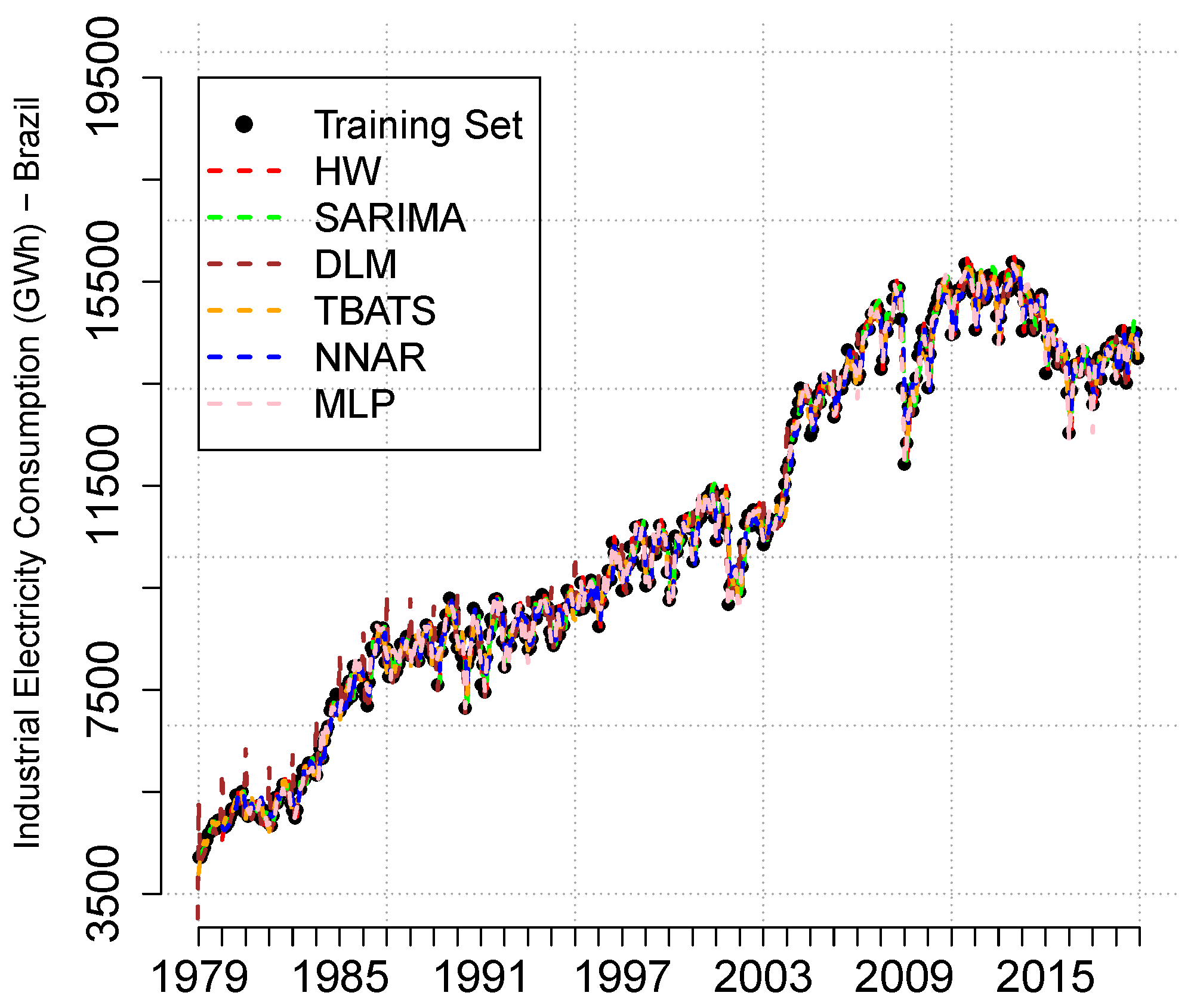

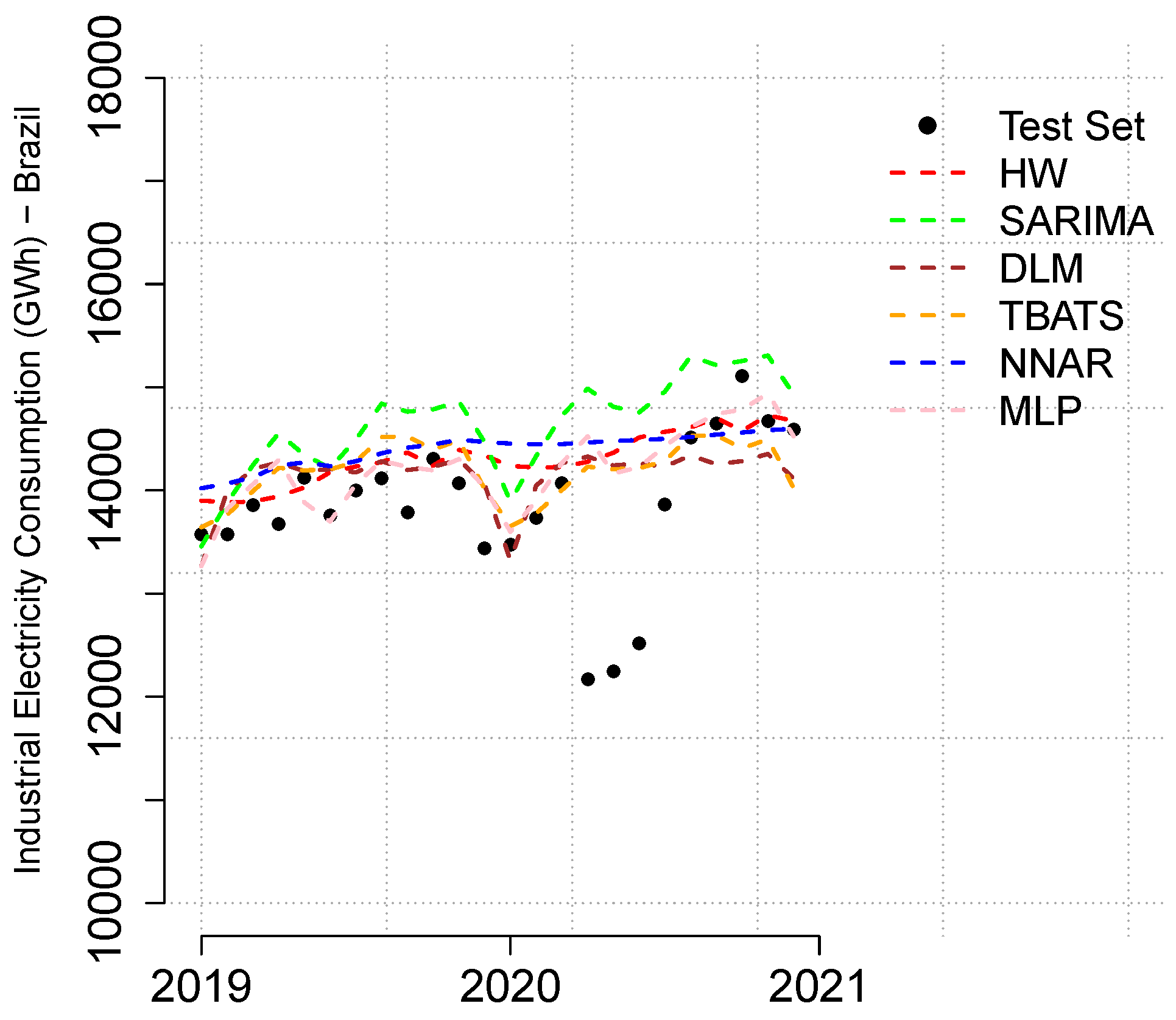

3. Results and Discussion

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Mean | Variance | St. Dev. | Amplitude | Min. | Max. |

|---|---|---|---|---|---|---|

| 1979 | 4616.83 | 70,024.88 | 264.62 | 725.00 | 4215.00 | 4940.00 |

| 1980 | 5123.83 | 65,639.24 | 256.20 | 699.00 | 4806.00 | 5505.00 |

| 1981 | 5095.83 | 11,991.61 | 109.51 | 329.00 | 4906.00 | 5235.00 |

| 1982 | 5324.08 | 74,528.27 | 273.00 | 809.00 | 4836.00 | 5645.00 |

| 1983 | 5669.92 | 142,872.81 | 377.99 | 1076.00 | 4994.00 | 6070.00 |

| 1984 | 6704.58 | 254,915.17 | 504.89 | 1578.00 | 5834.00 | 7412.00 |

| 1985 | 7570.00 | 100,401.82 | 316.86 | 890.00 | 7084.00 | 7974.00 |

| 1986 | 8094.83 | 286,936.52 | 535.66 | 1529.00 | 7190.00 | 8719.00 |

| 1987 | 8116.92 | 67,643.36 | 260.08 | 797.00 | 7749.00 | 8546.00 |

| 1988 | 8377.25 | 45,443.66 | 213.18 | 695.00 | 8073.00 | 8768.00 |

| 1989 | 8583.08 | 246,853.36 | 496.84 | 1705.00 | 7595.00 | 9300.00 |

| 1990 | 8322.58 | 262,576.99 | 512.42 | 1949.00 | 7145.00 | 9094.00 |

| 1991 | 8550.08 | 391,295.36 | 625.54 | 1814.00 | 7466.00 | 9280.00 |

| 1992 | 8610.58 | 93,964.45 | 306.54 | 1139.00 | 7953.00 | 9092.00 |

| 1993 | 8915.08 | 145,204.81 | 381.06 | 1083.00 | 8290.00 | 9373.00 |

| 1994 | 8921.92 | 136,503.90 | 369.46 | 1082.00 | 8368.00 | 9450.00 |

| 1995 | 9305.50 | 44,580.09 | 211.14 | 577.00 | 9070.00 | 9647.00 |

| 1996 | 9709.67 | 217,869.70 | 466.77 | 1637.00 | 8753.00 | 10,390.00 |

| 1997 | 10,143.08 | 185,066.81 | 430.19 | 1272.00 | 9455.00 | 10,727.00 |

| 1998 | 10,164.83 | 152,053.79 | 389.94 | 1178.00 | 9545.00 | 10,723.00 |

| 1999 | 10,324.33 | 300,464.79 | 548.15 | 1607.00 | 9257.00 | 10,864.00 |

| 2000 | 10,940.00 | 163,874.18 | 404.81 | 1398.00 | 10,024.00 | 11,422.00 |

| 2001 | 10,211.50 | 609,427.18 | 780.66 | 2160.00 | 9178.00 | 11,338.00 |

| 2002 | 10,635.67 | 247,841.33 | 497.84 | 1609.00 | 9431.00 | 11,040.00 |

| 2003 | 10,852.67 | 114,157.70 | 337.87 | 1186.00 | 10,345.00 | 11,531.00 |

| 2004 | 12,846.83 | 291,560.70 | 539.96 | 1585.00 | 11,829.00 | 13,414.00 |

| 2005 | 13,217.33 | 133,968.42 | 366.02 | 1105.00 | 12,496.00 | 13,601.00 |

| 2006 | 13,598.42 | 149,381.17 | 386.50 | 1313.00 | 12,851.00 | 14,164.00 |

| 2007 | 14,530.67 | 222,010.42 | 471.18 | 1433.00 | 13,592.00 | 15,025.00 |

| 2008 | 14,652.83 | 404,200.70 | 635.77 | 1995.00 | 13,417.00 | 15,412.00 |

| 2009 | 13,483.17 | 710,177.42 | 842.72 | 2628.00 | 11,924.00 | 14,552.00 |

| 2010 | 14,956.58 | 380,298.81 | 616.68 | 2031.00 | 13,425.00 | 15,456.00 |

| 2011 | 15,298.00 | 187,278.18 | 432.76 | 1386.00 | 14,467.00 | 15,853.00 |

| 2012 | 15,285.42 | 112,891.36 | 335.99 | 1061.00 | 14,567.00 | 15,628.00 |

| 2013 | 15,390.25 | 197,482.39 | 444.39 | 1516.00 | 14,370.00 | 15,886.00 |

| 2014 | 14,925.42 | 68,056.63 | 260.88 | 723.00 | 14,537.00 | 15,260.00 |

| 2015 | 14,071.50 | 127,615.73 | 357.23 | 1238.00 | 13,327.00 | 14,565.00 |

| 2016 | 13,687.75 | 174,712.57 | 417.99 | 1598.00 | 12,538.00 | 14,136.00 |

| 2017 | 13,903.92 | 138,837.36 | 372.61 | 1211.00 | 13,105.00 | 14,316.00 |

| 2018 | 14,121.92 | 119,368.63 | 345.50 | 1014.00 | 13,525.00 | 14,539.00 |

| 2019 | 13,858.17 | 71,473.42 | 267.35 | 864.00 | 13,442.00 | 14,306.00 |

| 2020 | 13,802.42 | 1,019,275.90 | 1009.59 | 2936.00 | 12,173.00 | 15,109.00 |

References

- Silva, F.L.C.; Souza, R.C.; Oliveira, F.L.C.; Lourenco, P.M.; Calili, R.F. A bottom-up methodology for long term electricity consumption forecasting of an industrial sector—Application to pulp and paper sector in Brazil. Energy 2018, 144, 1107–1118. [Google Scholar] [CrossRef]

- López-Gonzales, J.L.; Castro Souza, R.; Leite Coelho da Silva, F.; Carbo-Bustinza, N.; Ibacache-Pulgar, G.; Calili, R.F. Simulation of the Energy Efficiency Auction Prices via the Markov Chain Monte Carlo Method. Energies 2020, 13, 4544. [Google Scholar] [CrossRef]

- Ardakani, F.J.; Ardehali, M.M. Novel effects of demand side management data on accuracy of electrical energy consumption modeling and long-term forecasting. Energy Convers. Manag. 2014, 78, 745–752. [Google Scholar] [CrossRef]

- Taylor, J.W.; Buizza, R. Using weather ensemble predictions in electricity demand forecasting. Int. J. Forecast. 2003, 19, 57–70. [Google Scholar] [CrossRef]

- Bianco, V.; Manca, O.; Nardini, S. Electricity consumption forecasting in italy using linear regression models. Energy 2009, 34, 1413–1421. [Google Scholar] [CrossRef]

- Taylor, J.; Mcsharry, P. Short-term load forecasting methods: An evaluation based on european data. Power Syst. IEEE Trans. 2007, 22, 2213–2219. [Google Scholar] [CrossRef] [Green Version]

- Santana, A.L.; Conde, G.B.; Rego, L.P.; Rocha, C.A.; Cardoso, D.L.; Costa, J.C.; Bezerra, U.H.; Francs, C.R. Predict decision support system for load forecasting and inference: A new undertaking for brazilian power suppliers. Electr. Power Energy Syst. 2012, 38, 33–45. [Google Scholar] [CrossRef]

- Sadownik, R.; Barbosa, E.P. Short term forecasting of industrial electricity consumption in brazil. J. Forecast. 1999, 18, 215–224. [Google Scholar] [CrossRef]

- Fan, S.; Hyndman, R.J. Short-term load forecasting based on a semi-parametric additive model. IEEE Trans. Power Syst. 2012, 27, 134–141. [Google Scholar] [CrossRef] [Green Version]

- Huang, Y.-H.; Chang, Y.-L.; Fleiter, T. A critical analysis of energy efficiency improvement potentials in taiwan’s cement industry. Energy Policy 2016, 96, 14–26. Available online: https://www.journals.elsevier.com/energy-policy (accessed on 25 November 2021). [CrossRef]

- Silva, F.L.; Oliveira, F.L.; Souza, R.C. A bottom-up bayesian extension for long term electricity consumption forecasting. Energy 2019, 167, 198–210. [Google Scholar] [CrossRef]

- Martínez-Álvarez, F.; Troncoso, A.; Asencio-Cortés, G.; Riquelme, J.C. A Survey on Data Mining Techniques Applied to Electricity-Related Time Series Forecasting. Energies 2015, 8, 13162–13193. [Google Scholar] [CrossRef] [Green Version]

- Divina, F.; García Torres, M.; Goméz Vela, F.A.; Vázquez Noguera, J.L. A Comparative Study of Time Series Forecasting Methods for Short Term Electric Energy Consumption Prediction in Smart Buildings. Energies 2019, 12, 1934. [Google Scholar] [CrossRef] [Green Version]

- Ramos, D.; Faria, P.; Vale, Z.; Mourinho, J.; Correia, R. Industrial Facility Electricity Consumption Forecast Using Artificial Neural Networks and Incremental Learning. Energies 2020, 13, 4774. [Google Scholar] [CrossRef]

- Rocha, H.R.; Honorato, I.H.; Fiorotti, R.; Celeste, W.C.; Silvestre, L.J.; Silva, J.A. An Artificial Intelligence based scheduling algorithm for demand-side energy management in Smart Homes. Appl. Energy 2021, 282, 116–145. [Google Scholar] [CrossRef]

- Sulandari, W.; Subanar, S.; Lee, M.H.; Rodrigues, P.C. Time series forecasting using singular spectrum analysis, fuzzy systems and neural networks. MethodsX 2020, 7, 101015. [Google Scholar] [CrossRef] [PubMed]

- Sulandari, W.; Subanar, S.; Suhartono, S.; Utami, H.; Lee, M.H.; Rodrigues, P.C. SSA-based hybrid forecasting models and applications. Bull. Electr. Eng. Inform. 2020, 9, 2178–2188. [Google Scholar] [CrossRef]

- Sulandari, W.; Lee, M.H.; Rodrigues, P.C. Indonesian electricity load forecasting using singular spectrum analysis, fuzzy systems and neural networks. Energy 2020, 190, 116408. [Google Scholar] [CrossRef]

- Makridakis, S.; Hibon, M. The m3-competition: Results, conclusions and implications. Int. J. Forecast. 2000, 16, 451–476. [Google Scholar] [CrossRef]

- Makridakis, S.; Spiliotis, E.; Assimakopoulos, V.; Chen, Z.; Gaba, A.; Tsetlin, I.; Winkler, R. The m5 Uncertainty Competition: Results, Findings and Conclusions. 2020. Available online: https://www.researchgate.net/publication/346493740_The_M5_Uncertainty_competition_Results_findings_and_conclusions (accessed on 15 November 2021).

- Makridakis, S.; Fry, C.; Petropoulos, F.; Spiliotis, E. The Future of Forecasting Competitions: Design Attributes and Principles. 2021. Available online: https://arxiv.org/abs/2102.04879 (accessed on 1 November 2021).

- Du Preez, J.; Witt, S. Univariate versus multivariate time series forecasting: An application to international tourism demand. Int. J. Forecast. 2003, 19, 435–451. Available online: https://www.sciencedirect.com/science/article/pii/S0169207002000572 (accessed on 1 December 2021). [CrossRef]

- Todorov, H.; Searle-White, E.; Gerber, S. Applying univariate vs. multivariate statistics to investigate therapeutic efficacy in (pre)clinical trials: A Monte Carlo simulation study on the example of a controlled preclinical neurotrauma trial. PLoS ONE 2020, 15, 798. [Google Scholar] [CrossRef]

- Rana, M.; Koprinska, I.; Agelidis, V. Univariate and multivariate methods for very short-term solar photovoltaic power forecasting. Energy Convers. Manag. 2021, 121, 380–390. Available online: https://www.sciencedirect.com/science/article/pii/S0196890416303934 (accessed on 2 December 2021). [CrossRef]

- Ivanova, M.; Herron, T.; Dronkers, N.; Baldo, J. An empirical comparison of univariate versus multivariate methods for the analysis of brain–behavior mapping. Hum. Brain Mapp. 2021, 42, 1070–1101. Available online: https://onlinelibrary.wiley.com/doi/abs/10.1002/hbm.25278 (accessed on 4 December 2021). [CrossRef] [PubMed]

- Lütkepohl, H. Introduction to Multiple Time Series Analysis; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2013. [Google Scholar]

- Central Bank of Brazil. Time Series Management System—v2.1. 2021. Available online: https://www3.bcb.gov.br/sgspub/localizarseries/localizarSeries.do?method=prepararTelaLocalizarSeries (accessed on 10 November 2021).

- R Core Team. R: A Language and Environment for Statistical Computing; R Foundation for Statistical Computing: Vienna, Austria, 2021; Available online: https://www.R-project.org/ (accessed on 9 November 2021).

- Holt, C.C. Forecasting seasonals and trends by exponentially weighted moving averages. Int. J. Forecast. 1957, 20, 5–10. [Google Scholar] [CrossRef]

- Winters, P.R. Forecasting sales by exponentially weighted moving averages. Manag. Sci. 1960, 6, 324–342. [Google Scholar] [CrossRef]

- Box, G.E.P.; Jenkins, G.M.; Reinsel, G.C.; Ljung, G.M. Time Series Analysis: Forecasting and Control; Wiley: Hoboken, NJ, USA, 2015. [Google Scholar]

- West, M.; Harrison, J. Bayesian Forecasting and Dynamic Models; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2006. [Google Scholar]

- Livera, A.M.D.; Hyndman, R.J.; Snyder, R.D. Forecasting time series with complex seasonal patterns using exponential smoothing. J. Am. Stat. Assoc. 2011, 106, 1513–1527. [Google Scholar] [CrossRef] [Green Version]

- Hyndman, R.J.; Athanasopoulos, G. Forecasting: Principles and Practice; OTexts: Melbourne, Australia, 2018. [Google Scholar]

- Veloz, A.; Salas, R.; Allende-Cid, H.; Allende, H.; Moraga, C. Identification of lags in nonlinear autoregressive time series using a flexible fuzzy model. Neural Process. Lett. 2016, 43, 641–666. [Google Scholar] [CrossRef]

- Hyndman, R.; Athanasopoulos, G.; Bergmeir, C.; Caceres, G.; Chhay, L.; O’Hara-Wild, M.; Petropoulos, F.; Razbash, S.; Wang, E.; Yasmeen, F. Forecast: Forecasting Functions for Time Series and Linear Models. R Package Version 8.15. 2021. Available online: https://pkg.robjhyndman.com/forecast/ (accessed on 10 November 2021).

- Goodfellow, I.; Bengio, Y.; Courville, A. Deep Learning; MIT Press: Cambridge, MA, USA, 2016. [Google Scholar]

- Ahmed, N.K.; Atiya, A.F.; Gayar, N.E.; El-Shishiny, H.E. An Empirical Comparison of Machine Learning Models for Time Series Forecasting. Econom. Rev. 2010, 29, 594–621. [Google Scholar] [CrossRef]

- Petris, G. An R Package for Dynamic Linear Models. J. Stat. Softw. Artic. 2020, 36, 1–16. Available online: https://www.jstatsoft.org/v036/i12 (accessed on 3 November 2021).

- Vivas, E.; Allende-Cid, H.; Salas, R. A systematic review of statistical and machine learning methods for electrical power forecasting with reported mape score. Entropy 2020, 22, 1412. [Google Scholar] [CrossRef] [PubMed]

- Cordova, C.H.; Portocarrero, M.N.L.; Salas, R.; Torres, R.; Rodrigues, P.C.; López-Gonzales, J.L. Air quality assessment and pollution forecasting using artificial neural networks in Metropolitan Lima-Peru. Sci. Rep. 2021, 11, 24232. [Google Scholar] [CrossRef] [PubMed]

| Equations | Additive Method | Multiplicative Method |

|---|---|---|

| Level () | ||

| Trend () | ||

| Seasonal () | ||

| Forecast () |

| Model | Fitted | Forecast |

|---|---|---|

| Holt–Winters | 2.51 | 4.09 |

| SARIMA | 1.88 | 6.17 |

| TBATS | 1.99 | 3.77 |

| DLM | 1.87 | 4.09 |

| NNAR | 2.40 | 4.77 |

| MLP | 1.48 | 3.41 |

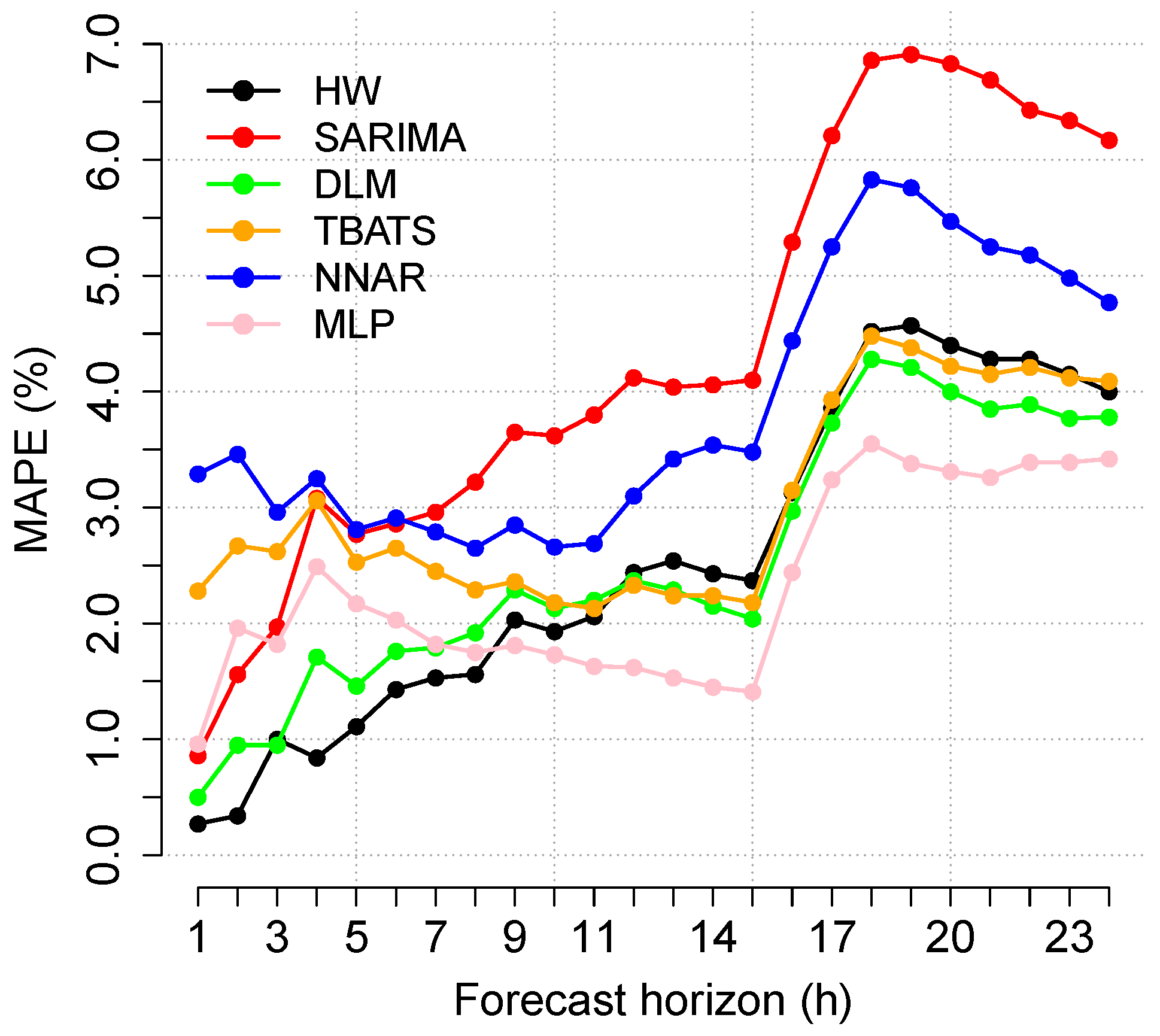

| Step | HW | SARIMA | TBATS | DLM | NNAR | MLP |

|---|---|---|---|---|---|---|

| 1 | 0.27 | 0.86 | 0.50 | 2.28 | 3.29 | 0.96 |

| 2 | 0.34 | 1.56 | 0.95 | 2.67 | 3.46 | 1.96 |

| 3 | 1.00 | 1.97 | 0.95 | 2.62 | 2.96 | 1.82 |

| 4 | 0.84 | 3.08 | 1.71 | 3.06 | 3.25 | 2.49 |

| 5 | 1.11 | 2.77 | 1.46 | 2.53 | 2.81 | 2.17 |

| 6 | 1.43 | 2.86 | 1.76 | 2.65 | 2.91 | 2.03 |

| 7 | 1.53 | 2.96 | 1.79 | 2.45 | 2.79 | 1.82 |

| 8 | 1.56 | 3.22 | 1.92 | 2.29 | 2.65 | 1.75 |

| 9 | 2.03 | 3.65 | 2.29 | 2.36 | 2.85 | 1.81 |

| 10 | 1.93 | 3.62 | 2.13 | 2.18 | 2.66 | 1.73 |

| 11 | 2.06 | 3.80 | 2.20 | 2.13 | 2.69 | 1.63 |

| 12 | 2.44 | 4.12 | 2.37 | 2.33 | 3.10 | 1.62 |

| 13 | 2.54 | 4.04 | 2.29 | 2.24 | 3.42 | 1.53 |

| 14 | 2.43 | 4.06 | 2.15 | 2.24 | 3.54 | 1.45 |

| 15 | 2.37 | 4.10 | 2.04 | 2.18 | 3.48 | 1.41 |

| 16 | 3.13 | 5.29 | 2.97 | 3.15 | 4.44 | 2.44 |

| 17 | 3.86 | 6.21 | 3.73 | 3.93 | 5.25 | 3.24 |

| 18 | 4.52 | 6.86 | 4.28 | 4.48 | 5.83 | 3.55 |

| 19 | 4.57 | 6.91 | 4.21 | 4.38 | 5.76 | 3.38 |

| 20 | 4.40 | 6.83 | 4.00 | 4.22 | 5.47 | 3.31 |

| 21 | 4.28 | 6.69 | 3.85 | 4.15 | 5.25 | 3.26 |

| 22 | 4.28 | 6.43 | 3.89 | 4.21 | 5.18 | 3.39 |

| 23 | 4.15 | 6.34 | 3.77 | 4.12 | 4.98 | 3.39 |

| 24 | 4.00 | 6.17 | 3.78 | 4.09 | 4.77 | 3.42 |

| Average | 2.54 | 4.35 | 2.54 | 3.04 | 3.87 | 2.32 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Leite Coelho da Silva, F.; da Costa, K.; Canas Rodrigues, P.; Salas, R.; López-Gonzales, J.L. Statistical and Artificial Neural Networks Models for Electricity Consumption Forecasting in the Brazilian Industrial Sector. Energies 2022, 15, 588. https://doi.org/10.3390/en15020588

Leite Coelho da Silva F, da Costa K, Canas Rodrigues P, Salas R, López-Gonzales JL. Statistical and Artificial Neural Networks Models for Electricity Consumption Forecasting in the Brazilian Industrial Sector. Energies. 2022; 15(2):588. https://doi.org/10.3390/en15020588

Chicago/Turabian StyleLeite Coelho da Silva, Felipe, Kleyton da Costa, Paulo Canas Rodrigues, Rodrigo Salas, and Javier Linkolk López-Gonzales. 2022. "Statistical and Artificial Neural Networks Models for Electricity Consumption Forecasting in the Brazilian Industrial Sector" Energies 15, no. 2: 588. https://doi.org/10.3390/en15020588

APA StyleLeite Coelho da Silva, F., da Costa, K., Canas Rodrigues, P., Salas, R., & López-Gonzales, J. L. (2022). Statistical and Artificial Neural Networks Models for Electricity Consumption Forecasting in the Brazilian Industrial Sector. Energies, 15(2), 588. https://doi.org/10.3390/en15020588