1. Introduction

Accumulation of savings is one of the research areas undertaken in the field of financial decisions of agricultural households. Researchers take into account their various aspects, which proves the importance, topicality, complexity, and multidimensional aspect of this research area. This paper focuses on the concept of household financial energy [

1]. Taking into account the approach in which money is treated as a source of energy [

2], it was assumed that household savings are a source of financial energy necessary to launch processes related to agricultural activity [

3].

Saving is the sacrifice of current consumption, which leads to the accumulation of capital [

4]. This capital is a source of additional income that can potentially be used for future household consumption or for financing agricultural activities, including financing farm investments; therefore, it is a source of financial energy on the farm. This is confirmed by the results of research, which show that household savings can stimulate investment processes in a farm [

5]. Gikonyo et al. [

6] found that household savings were the key contributor to farm investment in rural households, being a source of financial energy on the farm.

An Important issue in the discussed area is the identification of factors influencing the accumulation of savings by agricultural households. The results of empirical research presented in the literature show that there are a number of factors determining the propensity of households to save, and they can be divided into two main groups: endogenous factors (socioeconomic, sociodemographic, and social), which are related to the characteristics of the household, and exogenous factors, independent of the household. This work fits into this current trend of research while focusing on the first, endogenous group of factors and household characteristics, as well as those related to the farm. The adopted research assumption results from the integral relationship between a household and a farm. As a result, decisions made within the agricultural household are aimed at both maximizing the satisfaction of individual and common needs of its members, i.e., fulfilling the basic goal of the household, and striving to ensure the development of the farm, which is the basic source of income of these entities [

7].

The aim of this research was to identify and evaluate the factors influencing the propensity of agricultural households to accumulate savings, which in this study are treated as a source of financial energy, taking into account socioeconomic characteristics relating to the farmer and their household, as well as farm characteristics. Classification and regression tree analysis (CRT) was used to achieve the purpose of the study.

The agricultural sector is an important part of the Polish economy; in the last 20 years, the value of exports of Polish agri-food products has increased 12-fold, to the level of 37.5 billion USD [

8]. A particular increase in agricultural production was observed after Poland’s accession to the European Union. In the years 2004–2020, the productivity of farms in Poland doubled, and the number of people working in agriculture decreased to 10% of total employment, but it remains three times higher than in the EU [

8]. According to the results of the Agricultural Census 2020 [

9], the total agricultural area in Poland was approximately 14,637 thousand ha, while the total number of farms was approximately 1317 thousand. The average agricultural area per farm was 11.1 ha. Polish agriculture has been changing in recent years, which can be confirmed by the following phenomena: the increasing specialization of farms with a progressive concentration of agricultural input, a decrease in the number of farms, an increase in the average farm area and the number of livestock per farm, and progress in farm modernization, along with farm specialization [

9]. However, the structure of Polish farms is still dominated by small farms, which determines the development of agriculture in Poland (the share of smallest farms with up to 5 ha of agricultural areas amounted to 52.5% in 2020) [

9]. Slightly more than 20% of farmers in Poland are under 40, which makes them, next to Austrians, the youngest in Europe; hence, the replacement rate is very high—over eight times higher than the EU average [

8]. Young farmers usually manage an area of 20–50 ha, have good agricultural qualifications, and often take part in further training courses [

8]. Moreover, farmers in Poland are increasingly better educated compared to 10 years ago; nevertheless, the percentage of farmers with university education is significantly higher in the case of owners of larger farms (over 50 ha) [

8]. The income situation of farms in Poland depends on their size and type of production; for some, direct payments and other financial support are the main sources of income, for others, it is only a minor addition [

8].

The remainder of this paper is organized as follows:

Section 2 provides a literature review, which is the basis for empirical research.

Section 3 presents the research methodology and data sources.

Section 4 presents the results of empirical research. First, the characteristics of the researched farms are established (

Section 4.1). Then, the results of the analyses on the savings of the surveyed agricultural households are presented, taking into account the forms, motives, and goals of saving (

Section 4.2). Next, the factors influencing the propensity to save are identified and assessed (

Section 4.3). Classification and regression tree analysis (CRT) is used for this purpose. The last section presents a summary of the obtained results and outlines directions for further research.

2. Determinants of Farm Households’ Savings—Literature Review

In general, savings are defined as the difference between income and consumption expenditure [

10,

11]; therefore, the basic factor that influences the possibility of making a decision to save is the level of total income and the level of income per capita obtained by members of an agricultural household. Previous research results showed a positive relationship between the income level and households’ propensity to save [

12]. In the case of agricultural households, the basic source of income is the income obtained from agricultural activity, which is characterized by seasonality and instability [

13]. Uncertainty about income levels due to limited ability to predict factors, such as weather, prices, and biological responses to different farming practices [

14], results in farmers taking actions aimed at limiting changes in the amount of income and for securing rural livelihoods. One of the most important strategies implemented in this area is the diversification of income sources [

15,

16,

17], which consists of obtaining income not related to agricultural activity. It is often indicated that this is a strategy primarily intended to offset risk [

18]. Taking into account the fact that this strategy makes it possible to minimize the volatility of income and guarantee a potentially high level of income for the household, having more than one source of income should have a positive impact on the household’s ability to accumulate savings. Income volatility may also encourage farmers to save as a precautionary measure [

19].

By analyzing the current research results in the field of factors influencing the savings of agricultural households, it was established that there is a relationship between the propensity to save and socioeconomic characteristics such as development phase, size and composition of the household, and gender, age, and education of the head of the household [

20,

21,

22,

23,

24]. The first group of features is related to the household composition, which is influenced by the number of people in the household, the share of people providing income to the household, and the share of children and other household dependents who generate expenses and do not provide income. On the one hand, having children may encourage saving to finance their needs (e.g., education); on the other hand, it may negatively affect the possibility of saving (lower per capita income) [

25]. With regard to household characteristics, it was also found that having a successor who will take over the farm in the future encourages farmers to invest [

26]. This is related to the expectations of continuation of agricultural activity, especially with respect to family farms [

3]. Implementation of investment processes on a farm requires the involvement of financial capital (financial energy), which may come from, among others, household savings. Therefore, having a successor should positively influence the propensity to save in order to raise capital for additional investments. Moreover, as demonstrated by Harris et al. [

27], farms with a designated successor are characterized by higher profit margins and higher returns to equity; therefore, succession planning is positively related to a farm’s business performance. As a consequence, this should result in obtaining higher income by an agricultural household, thus increasing the potential for savings.

Referring to the assumptions of the Ando and Modigliani [

28] life-cycle hypothesis, among the factors potentially influencing savings, the age of the household head should also be indicated—which is related to the developmental phase of the household. At the same time, the results of studies presented in the literature, which take into account this research aspect, are not unambiguous. For example, Nwosu, Anumudu, and Nnamchi [

23] showed that savings increased up to a certain stage (79 years), and then decreased, at which point the household used previously accumulated savings. Brounen, Koedijk, and Pownall [

29], on the other hand, showed in the course of their research that there is a negative relationship between age and the tendency to save.

Another factor that may influence decisions on saving is the level of education of the head of the household. More educated people tend to be more knowledgeable about resource allocation and investment opportunities [

30]. A positive relationship between the level of education and household savings has been demonstrated, among others, by Çebi-Karaaslan, Oktay, and Alkan [

25]. With regard to the accumulation of savings by the household, the importance of financial literacy is also emphasized. The results of research in this area show that people with greater knowledge of finances are characterized by a greater propensity to save [

29,

31,

32]. This is related to the fact that savings decisions are complex and require significant economic knowledge and information from the decision maker [

33].

In the course of the research, it was established that the decisions of farm households in terms of savings may also be determined by factors relating to the farm used by the farmer’s family. In particular, features affecting the amount of income from agricultural activity, which is the basic source of household income and constitutes the potential for making savings decisions, should be taken into account. The production potential of a farm (land, machinery, and equipment) and the efficiency of its use are among the factors determining the amount of income from a farm [

34]. Research results prove that there is a positive relationship between the area of agricultural land and the propensity of households to save [

12,

24]. The level of income obtained from agricultural activity, which constitutes the potential for savings, is also affected by the specialization of a farm [

35,

36,

37], as well as the value of the manufactured production [

38,

39].

3. Materials and Methods

The study used primary data obtained in the course of a survey conducted in the second quarter of 2020 among farms covered by the European Farm Accountancy Data Network (FADN). The study on “financial exclusion of farm households and its importance for the development of financial services in the region of Central Pomerania” was carried out on the basis of a project financed by the Polish Ministry of Science and Higher Education. The spatial scope of the study covered the area of Central Pomerania (Poland). A total of 361 farms participated in the study, representing 88% of all entities covered by FADN agricultural accounting in the analyzed area. After substantive verification, the results concerning 348 entities were accepted for analysis. The survey was carried out by advisors from the Agricultural Advisory Centers through personal contact with the farmer and supplementary telephone contact (methods: PAPI and CATI). The obtained data concern 2019 (some of the questions also concerned the period from 2004, i.e., from the moment of Poland’s accession to the European Union). The questionnaire included a total of 69 questions, divided into three main sections: (A) general information about the household (nine questions), (B) information about financial management in the household (40 questions), and (C) information about the farm (20 questions). In the course of the research, it was assumed that a farm household is an entity that obtains income from agricultural activity.

The first part included questions relating to the head of the household. The questions concerned age, gender, level of education, household size, number of persons engaged in gainful employment in and outside the household, number of children, and the stage of development of the household.

In the second part, relating to financial management in the household, the questions related to the financial situation of the household, average monthly net income per capita, household income structure, changes in income, opinions on the amount of income in the context of expenses, the amount and structure of expenses savings (i.e., their amount, the method of allocating funds, and the purpose and motives of saving), household debt, the purpose of debt, the amount of debt, and costs related to its servicing. This part also included questions relating to financial liquidity and timely repayment of bills. In the next part, the respondents were asked about their knowledge of the concept of financial exclusion, difficulties in accessing financial services and products, and the reasons for financial exclusion. The questions also referred to financial services and/or products used by the household, detailed reference was made to the use of banking services and possible reasons for not using the services. Respondents also answered questions relating to the methods of payment for everyday purchases and various types of bills. An attempt was made to find answers to the questions relating to the reasons for the financial exclusion of farmers.

The third part of the survey referred to information on the status of a farm (self-supply/production for sale), production specialization, acreage size and structure, production value, asset structure, profitability of production (including the effect of Poland’s accession to the EU), direct payments in income from agricultural activity and their spending, methods of farm management (education, including agricultural education, age, gender of the person managing the farm, and number of years of farm management), number of people employed on the farm, and method of taking over the farm by successors.

The questionnaire made it possible to obtain data aimed at achieving the goals set in the research. In the course of the research, it was assumed that a farm household is an entity that obtains income from agricultural activity. An agricultural household is, therefore, understood as a group of people who live together and combine their income obtained from various sources, including agricultural activity. An agricultural household may also be created by a person living alone who obtains income from agricultural activity and possibly from other sources [

7].

Classification and regression tree analysis (CRT) was used to identify the key features of the farmer and his household, as well as farm-related features affecting the propensity to accumulate savings. It is one of the most popular and effective methods of data mining, very often used for prediction. The CRT method has many advantages over alternative methods such as logistic regression. Among other things, it does not require the assumption of a statistical distribution in relation to the variables used; thus, there is no need to transform the data [

40]. The classification tree method consists of the sequential division of the L-dimensional space of X

L variables into R

k subspaces (segments), until the dependent variable Y reaches the minimum level of differentiation in each of them, which is measured by the appropriate loss function [

41]. In the study, the dependent variable (Y) was the accumulation of savings in a farm household, which was defined as follows:

This dependent variable may take two values: Y = 1—when the studied agricultural household saves (191 entities), and Y = 0—in the opposite situation (218 households). The Gini index was used to assess the degree of differentiation of the R

k subspace [

42,

43,

44]. In order to obtain a simplified form of a classification and regression tree and to identify the key features affecting the accumulation of savings by a household, the recruitment division was stopped before segment homogeneity was obtained, using the FACT (fast algorithm for classification trees) direct stop rule for a given fraction of objects [

45]. Cross-validation was used in the classification and regression tree (CRT) analysis [

40,

46].

Explanatory variables for the model were selected on the basis of literature studies. Twelve independent variables relating to the socioeconomic characteristics of the farmer and their household, as well as the characteristics of the farm, were adopted to assess the studied phenomenon. Their characteristics and hypothetical impact on the propensity of the surveyed Central Pomeranian households to save, determined on the basis of research results presented in the literature, are presented in

Table 1.

When starting the construction of the classification and regression tree, all the variables included in the study were taken into account in the first stage of the analysis (

Table 1). The aim of this stage was to determine which variables (characteristics of the farmer, household, and farm) are crucial in identifying the propensity to save of the surveyed entities. The obtained results proved that, at a certain point in the classification, all characteristics of farms were similar to each other, and there were only single cases in the leaf nodes. Therefore, in order for the model to better reflect the reality and enable the identification of key factors influencing the propensity to save of the surveyed agricultural households, the model was simplified in the next stage of the analysis. For this purpose, the FACT-style direct stopping rule was used. This made it possible to obtain a simplified form of the classification and regression tree, and to identify the most important features that may affect the propensity of the surveyed entities to save.

In the course of the research, a two-tailed equality test for column proportions was also used. These tests are designed to determine the relative ordering of the categories of the categorical variable in the columns, according to the proportion of the categories of the categorical variable in the rows. For each significant pair, the category with the lower column proportion appears in the category with the larger column proportion. The significance level adopted in the study was 0.05. Tests were adjusted for all pairwise comparisons within each internal sub-table using the Bonferroni correction [

49]. This is a statistical tool to counter the problem of multiple comparisons by reducing the nominal significance level of each set of related tests in direct proportion to their total number. Statistical analyses were performed using the Statistica 13.3 package (C&RT algorithm).

4. Results

4.1. Characteristics of the Surveyed Households

Table 2 presents the descriptive statistics of the variables included in the analysis, on the basis of which the characteristics of the surveyed agricultural households were made.

In the analyzed population, the dominant group (40.22%) involved households whose average monthly income in 2019 did not exceed PLN 1500 per person, with every fifth household having less than PLN 1000 per person. Every third household had an income exceeding PLN 2000 per person. For 27.87% of the surveyed entities, the amount of this income was between PLN 1501 and PLN 2000 per person. The amount of income of the surveyed units changed most often without clear trends (40.1%); however, in every third farm, it was constantly growing. Almost one-fifth of households did not record changes in income over the last 15 years. The main source of income of the surveyed entities was agricultural activity—75.9% of total income on average. This was followed by income from hired work, which constituted 11.14% of total household income on average. The third position was occupied by income from pensions, accounting for 3.64% of income. The shares of other sources did not exceed 3% in the total income of the analyzed agricultural households.

For 28.45% of the surveyed households, farming was the only source of income. Thus, 71.55% of respondents diversified their sources of income, with 38.22% of households having income from two sources, three sources of income indicated by every fourth household, and 7.76% of entities declared having income from four or more sources. On average, 38.6% of the income of the surveyed farms from agricultural activity constituted direct subsidies. Six out of 10 of the surveyed households declared no debt.

Among the surveyed population, units where the head of the household was a man definitely dominated (82.47%). The average age of the household head was 47 years. The predominant individuals were those whose head of household had secondary education (37.07%) and basic vocational education (35.35%). One in five respondents (20.4%) declared having higher education by the head of the household. The average level of the share of children in the total number of household members was 23.48%; for half of the population, it did not exceed 20%. Nearly half of the respondents have a successor who will take over running the farm in the future.

The average farm area was 56.75 ha, of which, on average, 54.12 ha was agricultural land. In 2019, the average area of a farm in Poland was 10.95 ha; hence, the farm households included in the study had a higher average area of agricultural land than the national average [

50]. In the surveyed population, the largest group consisted of farms with a production value between PLN 32,001 and PLN 100,000 (37.8%), and the smallest group (6%) constituted farms whose production value exceeded PLN 500,000. Most of the farms were clearly focused on plant production; they accounted for almost half of the entities included in the analysis. There were 28.7% multidirectional (mixed) farms and 23.2% specializing in livestock production. In the analyzed period, the surveyed farms allocated on average 79.04% of their total agricultural production to official sale on the market. Secondly, 13.45% of the manufactured products were allocated to farm stocks. Other purposes, such as unofficial sale to the market or household consumption accounted for a small percentage of the value of agricultural production (total 7.51%).

4.2. Savings of the Surveyed Agricultural Households—Forms, Motives, and Goals

More than half (54.9%) of the surveyed agricultural households declared saving money. Using the two-tailed equality test for column proportions (

Table 1), it was found that people with higher education accumulated savings much more often (66.2%) than people with vocational or lower education (47.4%). In addition, 56.8% of people with secondary or post-secondary education declared savings. It was also established that a higher monthly net income per person in the household correlated with a greater propensity to save (

Table 3). Among the surveyed population, 60.8% of households with income of PLN 1501–2000 per person and 76.8% of households with income above PLN 2000 per person were saving. In the case of entities whose income did not exceed PLN 1500 per person, every third household declared savings.

When analyzing the saving rate of the surveyed entities, defined as the ratio of savings to total income, it was observed that the surveyed agricultural households allocated 13.9% of their total annual income on average to savings. The maximum savings rate recorded was 40% of total income, and the minimum was 1%. It was also found that every tenth household in 2019 allocated more than 20% of their total income to savings. The largest part (33.9% and 34.9% of households, respectively) allocated 6–10% or 11–20% of their annual income to savings, and every fifth household saved less than 5%. Data on the forms of collecting financial savings by the surveyed entities are presented in

Table 4.

The structure of financial savings of the surveyed agricultural households was dominated by funds accumulated in savings accounts (on average 62.29%). This was followed by cash (on average 26.39% of all financial savings) and bank deposits (10.55%). Savings in the other forms account for a negligible percentage (0.77%). None of the households covered by the study had savings in the form of stocks or bonds. Then, the frequency of collecting savings by the surveyed entities was assessed, and the results obtained in this regard are presented in

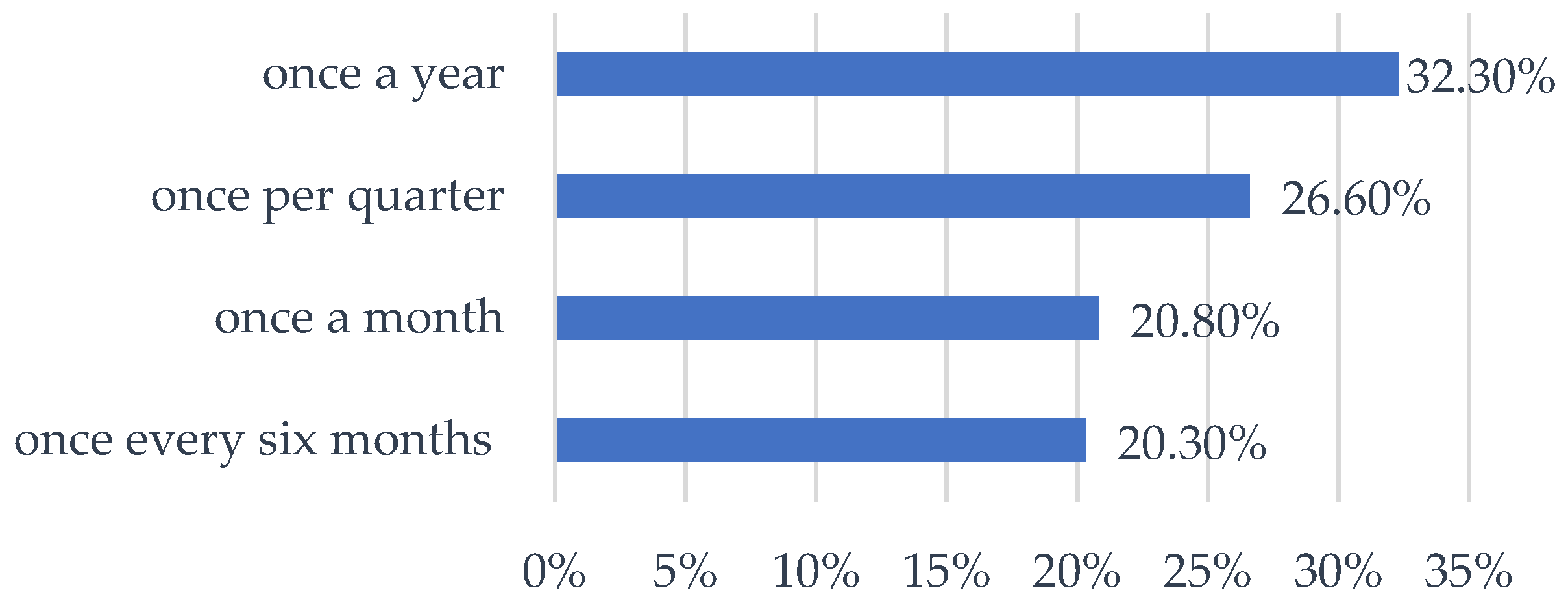

Figure 1.

One-fifth of the surveyed agricultural households declared regular monthly savings of part of their income. In turn, saving once a quarter was indicated by 26.6% of the surveyed entities, while saving once every 6 months was indicated by 20.3%. Every third household declared that they set aside part of their income for savings once a year. One of the features of agricultural households is the seasonality of their income. Income from agricultural activity, depending on the business profile, may occur, for example, once a quarter or even once a year, which may affect the household’s ability to save regularly. Subsequently, using a two-sided equality test for column proportions, it was found that the frequency of allocating income to savings was statistically significantly related to the age and level of education of the head of the household (

Table 5).

Using a two-tailed test for column proportions, it was found that younger people (up to 35 years of age) more often than other age groups regularly (monthly) set aside part of their income for savings (

Table 5). This characteristic was noted for 41.2% of respondents at this age, compared to 7.5% of people over 55 (a statistically significant difference) and 19.5–21.9% of people between 36 and 55 (a directional difference). The frequency of allocating income to savings is also statistically significantly related to the level of education of the head of the household. The results of the analyses have shown that only one in 10 people with basic vocational or lower education regularly allocated part of their income to savings every month; this is statistically significantly less than people with secondary or post-secondary education (25.3%) or with higher education (29.5%).

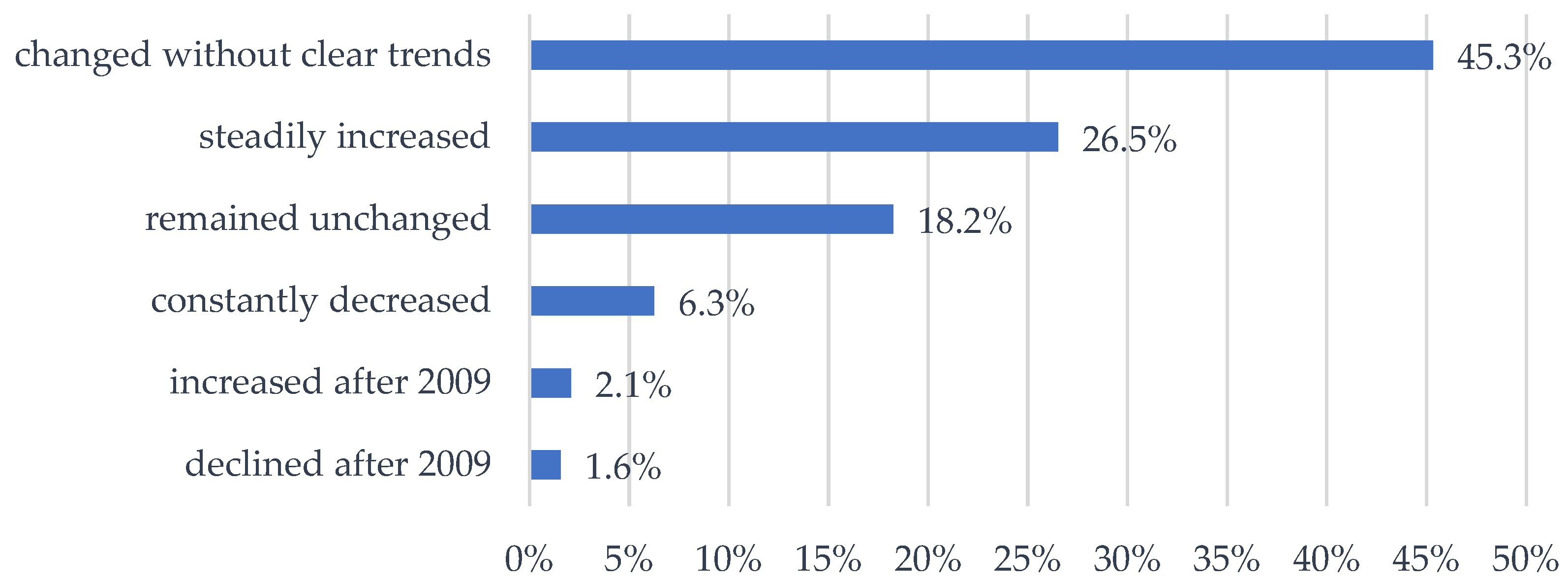

In the next stage of the analysis, changes in the level of income and savings of the surveyed entities in the years 2004–2019 were assessed. The results obtained in this regard are presented in

Figure 2.

The amount of savings accumulated in the surveyed agricultural households in the years 2004–2019 changed most often without any clear trends (45.3% of responses); however, in every fourth household, their steady increase was recorded (26.6%). It was also found that almost one-fifth of households did not change the amount of savings over the 15 year period under consideration, and 6.3% of respondents observed their steady decline. The next stage of the analyses included setting of savings goals by the surveyed agricultural households (

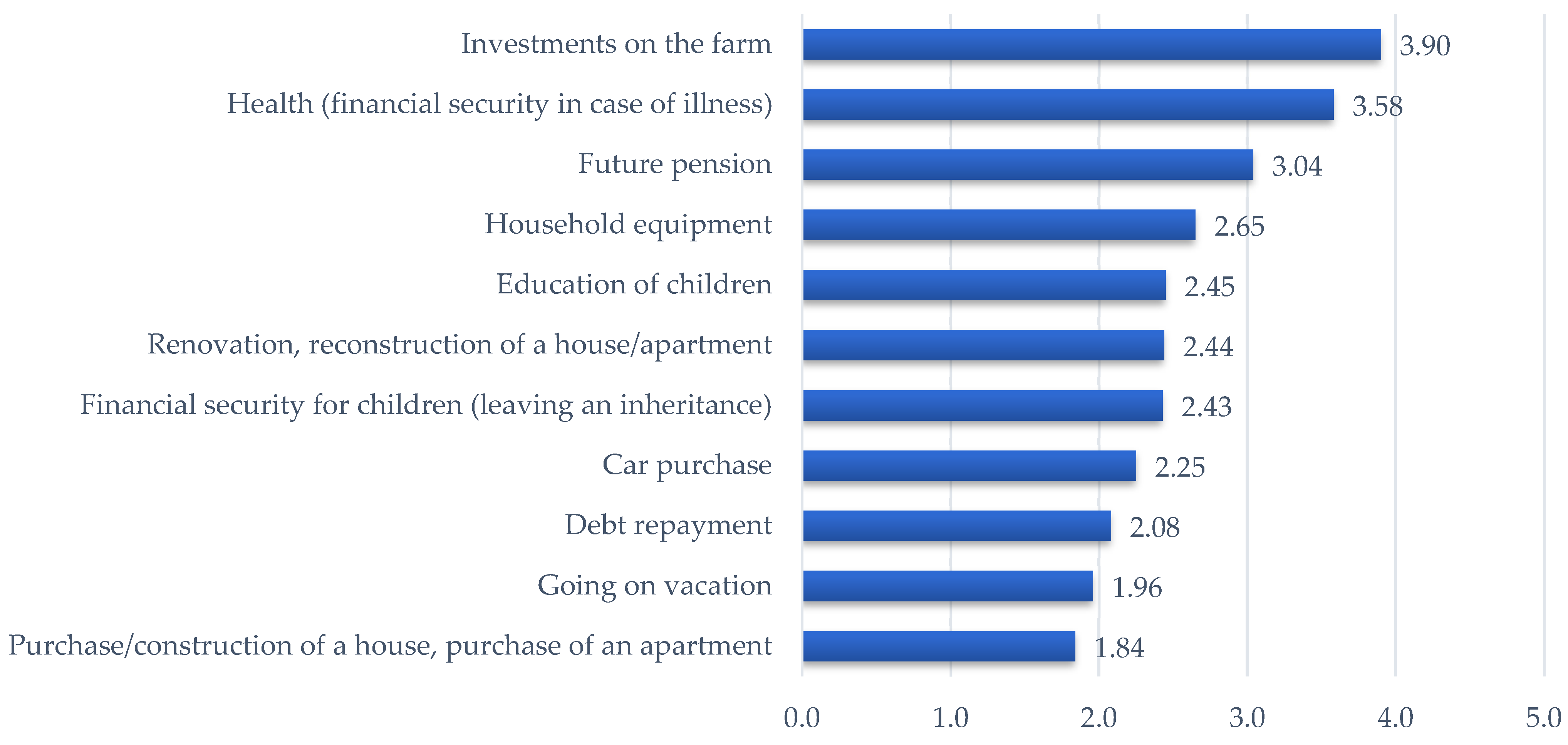

Figure 3).

The primary purpose of collecting savings by the surveyed agricultural households was to finance investments in the farm (M = 3.90). Nearly 40% of entities indicated this goal as the most important (5 on a five-point Likert scale), and another 30% as a very important goal (4). This confirms the research assumption that household savings are a source of financial energy for a farm. Subsequently, the surveyed entities saved as an insurance in case of illness (health, M = 3.58) and for the period after the end of professional activity (future retirement, M = 3.04). The three least important goals, buying or building a house or an apartment (M = 1.84), going on holiday (M = 1.96), and repaying debt (M = 2.08), were characterized by low variability of responses (SD = 1.242, 1.146, and 1.465, respectively), which means that their low significance is constant between the surveyed farms.

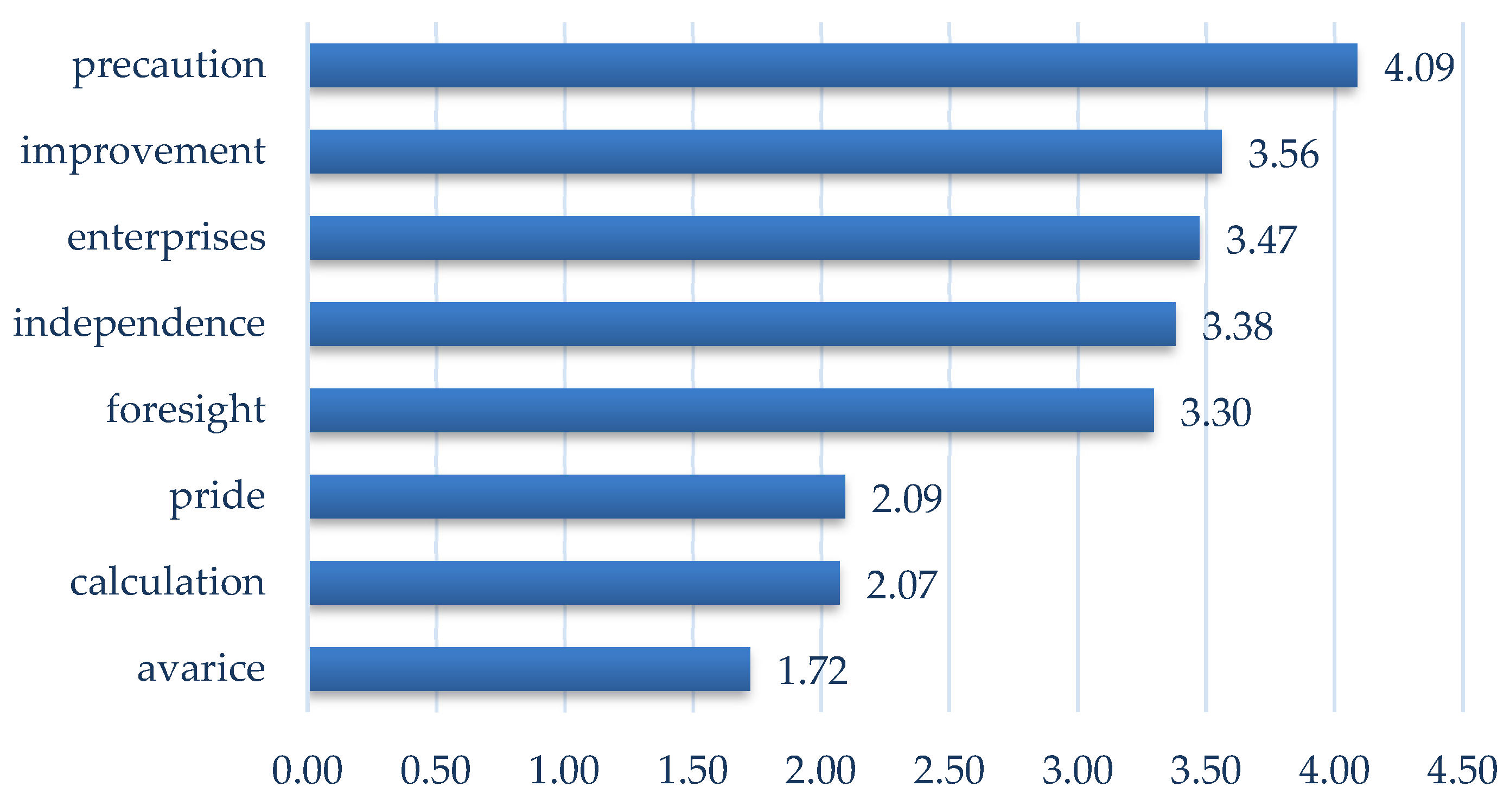

In the course of the research, the motives for saving were also established, referring to the catalog of motives proposed by Keynes [

8]. The results obtained in this regard are presented in

Figure 4.

Among the surveyed farm households, the dominant motive was the desire to protect themselves against unforeseen events (precaution, M = 4.09). Half of the respondents indicated that this was the most important theme (5 on a five-point Likert scale), and another 30% indicated it as very important (4). The second most important motive for saving money was the desire to improve one’s living conditions (improvement, M = 3.56). Respondents also indicated that they save to have capital for investment (enterprises, M = 3.47), to have a sense of independence and the ability to carry out plans (independence, M = 3.38), and to meet the future needs of the household (foresight, M= 3.30). Among the least important saving goals of the surveyed households were the desire to leave an inheritance (pride, M = 2.09), obtaining additional income, e.g., in the form of interest (calculation, M = 2.07), or simply unwillingness to spend money (avarice, M = 1.72).

4.3. Savings and the Features of Household and Farm—A CRT Analysis

The results of the classification (savings accumulation criterion) of the surveyed agricultural households based on classification and regression trees (CRT) and the importance of independent variables included in the analysis are presented in

Scheme 1 and

Figure 5.

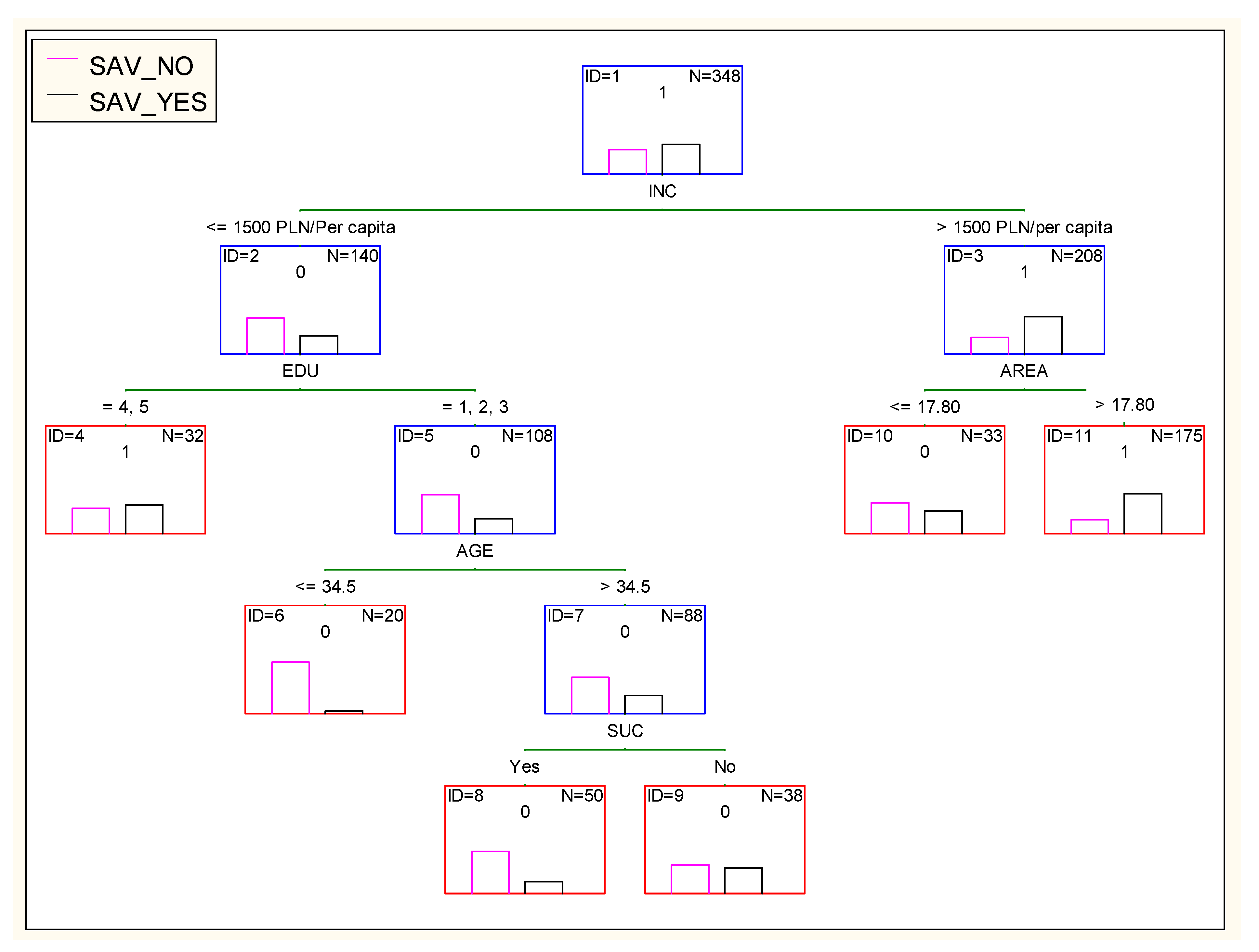

Decision rules are designed in root (ID 1), branch (IDs 2, 3, 5, and 7), and leaf (IDs 4, 6, 8, 9, 10, and 11) views. The tree consists of five split nodes and six terminal nodes. The certainty of the forecast is 74.7%. The divisions result from the algorithm that searches for the classification of the population into possibly homogeneous subsets.

The first division of the surveyed population of agricultural households was made on the basis of the INC variable. As a result of the classification, two groups were obtained: agricultural households with an average annual income per person up to PLN 1500 (ID 2) and households with an income exceeding PLN 1500 per person (ID 3). It was found that among entities characterized by a lower level of income, the majority (66.43%) did not save. On the other hand, among households with an income exceeding PLN 1500 per person, 69.2% of entities declared that they accumulate savings. The most important variable differentiating farms characterized by a higher level of income (ID 3) was the farm area (AREA). The obtained results prove that users of farms with an area exceeding 17.8 ha (ID 11) are more willing to accumulate savings than users of farms with a smaller area (ID 10); 74.29% of units from node 11 were characterized by savings, while, in node 10, less than half of the farms had this feature (42.42%). Then, the entities from node 2 (ID 2) were further divided on the basis of the education level of the head of the household (EDU). As a result of the classification, two groups were obtained: entities whose head of household had post-secondary or higher education (ID 4), more than half of which (53.13%) allocated part of their income to savings, and those whose head of household had at most secondary education (ID 5), of which 27.78% of households declared that they were saving. Next, households from node 5 (ID 5) were divided on the basis of the AGE variable. As a result of the classification taking into account the age of the head of the household, two groups were obtained: farmers aged up to 34.5 inclusive (ID 6), among whom the vast majority (95%) did not save, and farmers aged over 34.5 (ID 7), where every third respondent (32.95%) declared that their household allocates part of their income to savings. Subsequently, the entities from node 7 (ID 7) were further divided using the SUC variable. It was found that among farmers with a successor who will take over the farm in the future (ID 8), the vast majority (78%) declared that they did not save. In the second group (without a successor, ID 9), nearly half (47.37%) of the respondents indicated that they set aside part of their income for savings.

5. Discussion and Conclusions

The aim of the research was to identify and evaluate the factors influencing the propensity of farm households to accumulate savings, which, in this work, were treated as a source of financial energy, taking into account socioeconomic characteristics relating to the farmer and their household, as well as farm characteristics. Classification and regression tree analysis (CRT) was used to achieve the goal. The study was conducted on a group of farms in Central Pomerania (Poland) participating in the system of collecting and using data from farms (FADN). Data on 348 farms, obtained through a survey carried out in 2020 using a direct survey questionnaire, were used for the analyses.

On the basis of the analysis of the research results presented in the literature, 12 independent variables were adopted to identify the characteristics affecting the propensity of the surveyed agricultural households to save—those relating to the characteristics of the farmer’s household (AGE, GEND, EDU, EDU-EC, SHARE_CHILD, SUC, INC, DIV, DEBT) and of the farm (PROD_VALUE, AREA, SPEC).

During the research, it was established that more than half of the surveyed entities declared savings, allocating on average 13.9% of their total annual income for this purpose. The main purpose of collecting savings was to finance investments in a farm, which confirms the research assumption that household savings are a source of financial energy for a farm. When considering the motives for saving, it was found that the surveyed entities set aside part of their income primarily guided by the motive of precaution, i.e., the desire to protect themselves against unforeseen events. This is consistent with the research results presented in the literature so far [

51]. As indicated by Andnan et al. [

19], precautionary saving is one of the farm’s risk management strategies, used when future income is uncertain. Agricultural activity is exposed to various types of risk, including climatic risk, which affects changes in the amount of income obtained. In a situation where the income resulting from agricultural activity is lower than planned, the source of financial energy on the farm may be household savings. They can be used to finance both expenses related to current agricultural activity and investments in a farm.

Taking into account the forms of saving, it can be noted that the surveyed agricultural households invested their savings primarily in the bank. Four out of five respondents indicated that they put their savings on a savings bank account, and every fifth respondent preferred bank deposits. It was also established that savings accumulated on bank accounts accounted for an average of 62.29% of the financial assets of the surveyed entities, and funds on bank deposits accounted for 10.55% on average. Keeping savings in the form of cash was declared by more than half of the respondents (55.5%), with its average share in the structure of financial assets amounting to 26.39% on average. The obtained results indicate that farmers decide to accumulate money to a greater extent than to multiply it on the basis of financial products and services. Kozera et al. [

52] obtained similar results in terms of the forms of saving preferred by farmers in Poland. They found out that households of farmers are characterized by conservative attitudes to savings; thus, they do not diversify their savings portfolio. The basic forms of savings in studied households were bank deposits (in PLN) and cash [

52]. The results of our research have also shown that an important role in this respect is played by the reluctance to use financial services and products, as well as the lack of knowledge of the surveyed entities about the existing possibilities of using financial services and products. This confirms the need to take action in the field of financial education in rural areas, as well as striving to increase farmers’ access to financial products and services. This seems to be crucial for creating rural development strategies, especially in the context of eliminating the phenomenon of farmers’ financial exclusion. Financial education programs should include, among others, knowledge about various financial assets and the advantages/disadvantages of investing savings in the available forms of financial assets [

31].

On the basis of the application of the classification and regression tree method, it was found that the key factor differentiating the studied population in terms of savings is the level of the average monthly net income per person in the household (

INC). Next, the agricultural area (

AREA) and the level of education of the head of the household (

EDU) were of significant importance. The direction of influence of these variables turned out to be consistent with the assumed one, which confirms the results of previous studies (e.g., Deksisa and Bayissa [

12], Lidi, Bedemo, and Belina [

24], and Çebi-Karaaslan, Oktay, and Alkan [

25]). It was also established that, in a situation where the level of average income per person does not exceed PLN 1500, and the head of the household has at most secondary education, the vast majority (95%) of respondents aged 34.5 did not save, while, in the second age group (above 34.5 years), every third respondent declared that part of their household income is allocated to savings. This demonstrates that the age of the head of the household (

AGE) is also a factor influencing the accumulation of savings, and the direction of this relationship is positive. Our results serve as a confirmation of the research results of Obalola et al. [

53]. Further analyses have shown that, in the case of households representing a lower income class (up to PLN 1500 per person), when the head of the household has at most secondary education and is over 34.5 years of age, having a successor (

SUC) is also a factor influencing the accumulation of savings; however, the direction of this relationship is negative.

The obtained results contribute to the theory of science, constituting a thread in the discussion on the factors determining the financial decisions of farm households. In practical terms, the obtained results may contribute to the formulation of postulates regarding the creation and effective implementation of measures by institutions, including financial institutions, which are interested in supporting the development of farm households and local development, as well as entities supporting the reduction in poverty and financial exclusion among farm households. The research results can also be an important source of information for financial institutions that are interested in the best possible adaptation of financial services and products for households and acquiring new customers.

The limitation of the study is that the results of our research concern the period before the COVID-19 pandemic. Therefore, in the next stage, financial decisions of agricultural households under conditions of uncertainty will be taken into account. Changes in the economic environment—as a result of the global COVID-19 pandemic, unstable geopolitical situation, and high inflation—caused the conditions of financial decisions of households to change overnight, increasing the risk and uncertainty of actions and decisions taken by these entities related to the financial management of the household. Current research results show that, during the pandemic, households reduced consumption (although, in the first months, there was an increase in consumption expenditure) [

54], showed a higher propensity to save [

55], and presented higher risk aversion [

56]. Attention should also be paid to behavioral (psychological) and cultural factors, because, as research results show, the behavior of individuals in the sphere of finance depends only to a certain extent on their financial resources [

57]. All the abovementioned aspects will be taken into account in the next stage of research. The timeliness and importance of the indicated research issues make it justified to continue research in the field of savings accumulation processes by farm households.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}