Given the poor renovation-rate results achieved compared to those that are needed, in this paper, we introduce a portfolio of policy measures intended to enhance the current Italian legislation. This portfolio has four main aims: (1) Harmonize the wide range of tax rebate schemes for building interventions, linking them to actual energy-efficiency objectives; (2) Stabilize them in a long-term strategy to provide market actors with a solid framework and, at the same time, stimulate them to act as soon as possible; (3) Include decarbonization targets; (4) Act on energy poverty and equality issues.

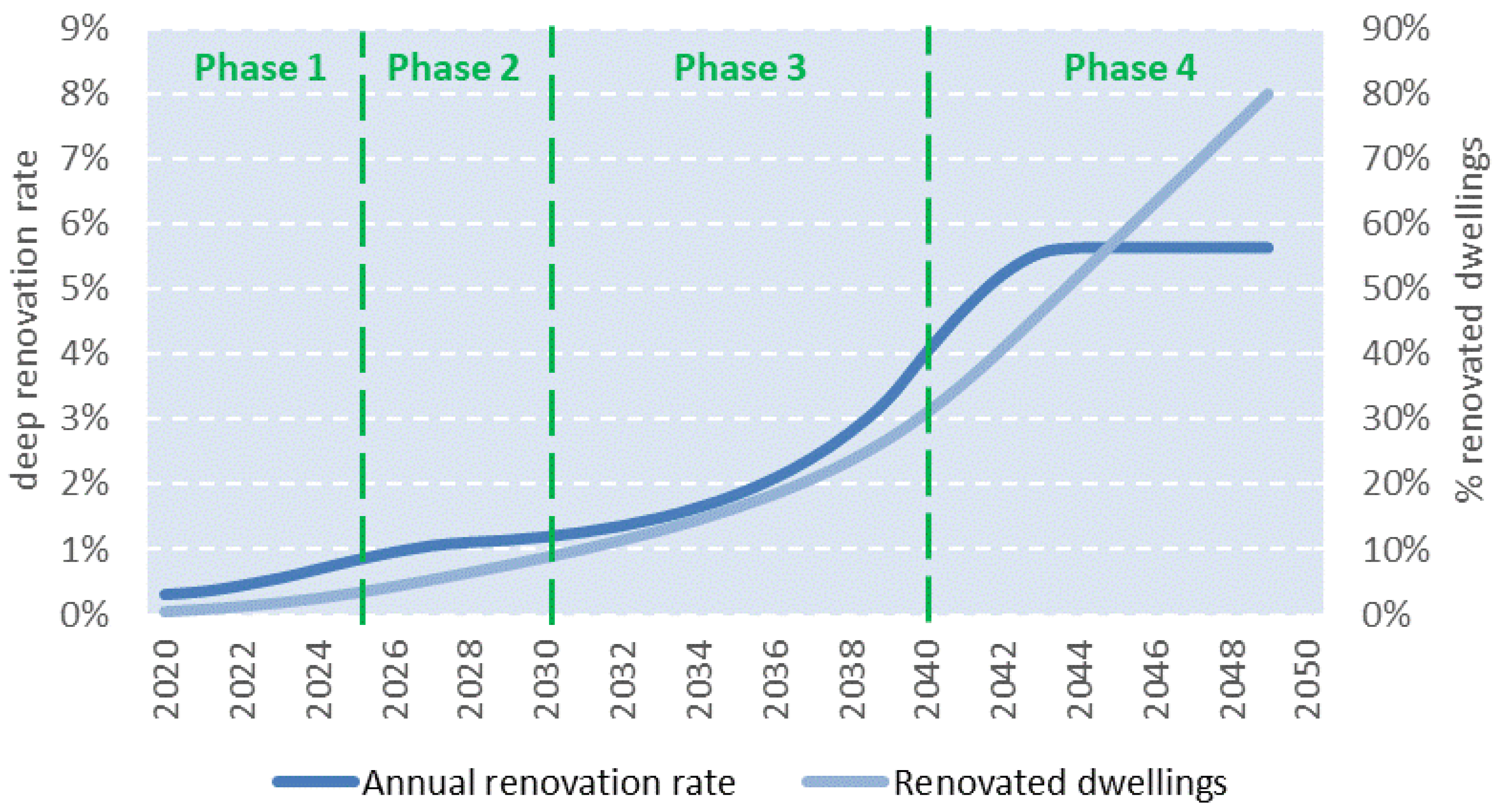

The regulatory, social, economic and technological transition should be planned in four phases, detailed as follows:

Therefore, in the following paragraphs, we present a comprehensive strategy, which walks on two legs, to have at least 80% of existing buildings deeply retrofitted by 2050. On one side, a harmonized tax rebate system that stimulates increased and accelerated deep-retrofitting rates would act on privately owned building stock. On the other side, a revolving fund mechanism would directly act on public buildings, such as schools and social housing.

4.1. Fiscal Rebate Mechanism for NZEBs

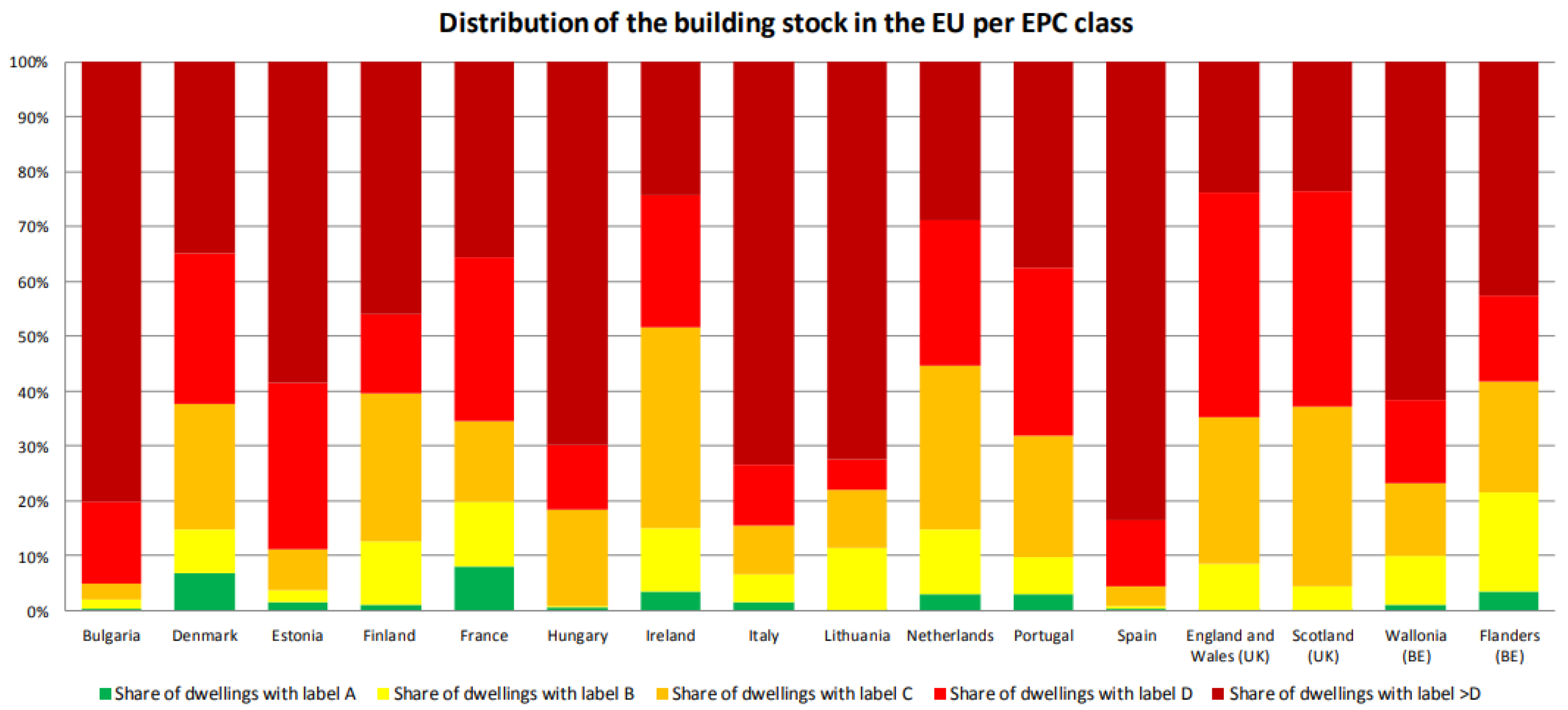

The current landscape of fiscal incentives for building interventions (see

Table 10) includes at least four different measures with different rebates (36–50%, 55–65%, 90% and 110%), different energy requirements (none, technology substitution or improvement and general building-performance improvement) and very different compliance checks (none, attestation from a certified technician for each single intervention, before-and-after building-energy certification). In this chaotic framework, major retrofits can obtain higher financial incentives (i.e., higher tax rebates) but also imply higher bureaucratic burdens and overall costs (including the cost of technical interventions and that of the professional documents needed to obtain rebates). This rather confusing situation therefore provides an unintended incentive to perform only simpler interventions with low energy-saving potential but also lower costs and complications. Seen from a public-official point of view, simpler interventions also imply a higher risk of fraud, as demonstrated through Italian Revenue Agency data. False invoices have been produced to obtain undue tax rebates without even the need of a professional to check whether the interventions were carried out.

Therefore, we first of all suggest rationalization of the overall system of incentive mechanisms in order to strengthen the idea that incentives for building renovations must always guarantee application of the “energy efficiency first” principle. In line with this, our proposal is to cancel out the current tax rebate of 36% (which was temporarily raised to 50% until 2024) addressed to ordinary and extraordinary maintenance, restoration and building refurbishment that do not lead to energy savings (e.g., a corresponding tax rebate would also be provided for purchasing of furniture in connection with buildings subject to renovation). In the same perspective, the “Bonus facciate” (façade rebate, a 90% tax rebate until end of 2022) should also be permanently canceled out, since it is given out for aesthetic interventions not linked to any energy-efficiency improvements.

According to the EU’s “energy efficiency first” principle, cost-efficient alternatives should be preferred and prioritized [

43]. The aim thereof is to allocate NRRP resources more efficiently (and reach a deep-renovation rate of about 1% by 2026) and develop incentive schemes into a long-term strategy to achieve NZEB (or more ambitious) targets. The key question is: How should incentives be designed to achieve these targets?

As already mentioned, the Superbonus 110% rebate scheme includes an obligation to improve building-energy certification through scaling up of at least two classes. This provision can be considered a good starting point but needs to be improved in order to be better-aligned with long-term climate objectives. For example, in the case of a class G building, does it make sense to consider class E a good benchmark? Without improving the minimum standards and the technical conditionalities to achieve the rebates, the risk is obtaining suboptimal results at both the building and stock levels.

Our proposals are therefore: (1) To design incentive mechanisms that are proportional to their achieved energy-efficiency improvements; (2) To organize a coordinated and incremental renovation plan that guarantees that at least 80% of the existing building stock can be deeply retrofitted by 2050.

Incentive schemes for private investors should be differentiated based on the most energy-intensive buildings (in terms of energy class, dimension and climate zone). Within a long-term strategy, encouraging investors to accelerate investment decisions and choose deep renovations via giving them a premium and planning a gradual reduction in tax deduction could be a useful strategy. A price signal should reward a fuel switch toward cleaner and renewable-based technologies. Furthermore, given the need for introduction of new procedures, technologies for electrification of final energy consumption and materials that are more compatible with the criteria of a circular economy, the tax rebate formula should take into account calculation of building materials’ carbon footprints from a life-cycle-analysis point of view.

In the starting phase, the current incentive scheme could be slightly modified through changing the eligibility criteria:

Fossil-fuel boilers should be excluded, since they are not compatible with decarbonization targets.

Second homes should be excluded as well, since they are only rarely occupied; therefore, the calculated energy savings will not be ensured.

The tax deduction should be lowered to avoid an excessive unjustified increase in restructuring costs; in this regard, a rate lower than 100% would entail a minimum outlay by the household owner, representing an incentive to verify the fairness of estimates through real competition among companies.

The new and stabilized tax deduction rate should be: (1) Differentiated between single-family houses (lower) and multifamily buildings (higher); (2) Differentiated between medium retrofitting (e.g., total energy savings between 30% and 60%) and deep retrofitting (e.g., total energy savings higher than 60%); (3) Guaranteed at least until 2030, although with decreasing rates over time in order to provide an incentive to act sooner; (4) More oriented to low-income households that should be eligible to apply for special support and have their energy-saving renovations fully financed.

Table 11 shows one possible evolution of the tax deduction scheme aimed at improving energy efficiency in buildings.

The proposed scheme includes different rebate rates for medium and deep retrofits, single homes and multifamily buildings. Rates would decrease depending on the year when retrofitting is performed. Additional features of the mechanism would include deduction duration and a credit assignment possibility. The tax rebate would be reimbursed in annual installments; e.g., a 70% rebate with a 10-year duration would mean a 7% annual rebate. The credit assignment would be the possibility to assign tax rebates to the construction company or to a financial institute in exchange for an immediate discount or financing; e.g., if the cost of an intervention is 80,000 EUR and the rebate is 110%, the final customer could decide whether to keep a 88,000 EUR tax rebate and use it in the following years or to assign it to the construction company and obtain, for example, an immediate 100% discount. This may be a very important possibility for low-income families that would not be able to exploit a tax rebate (especially if they are in the no-tax area) and also may have problems financing interventions with their own resources.

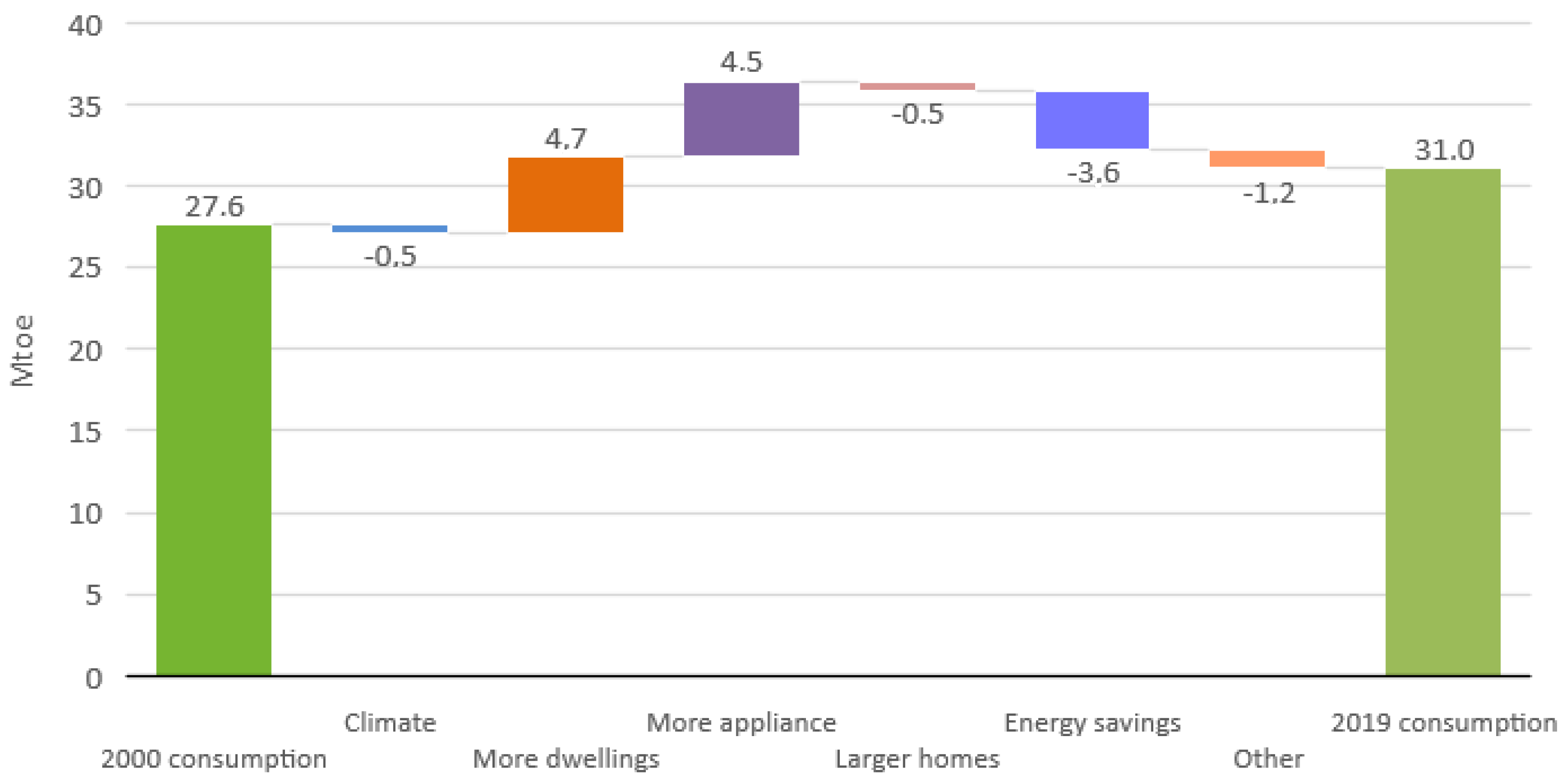

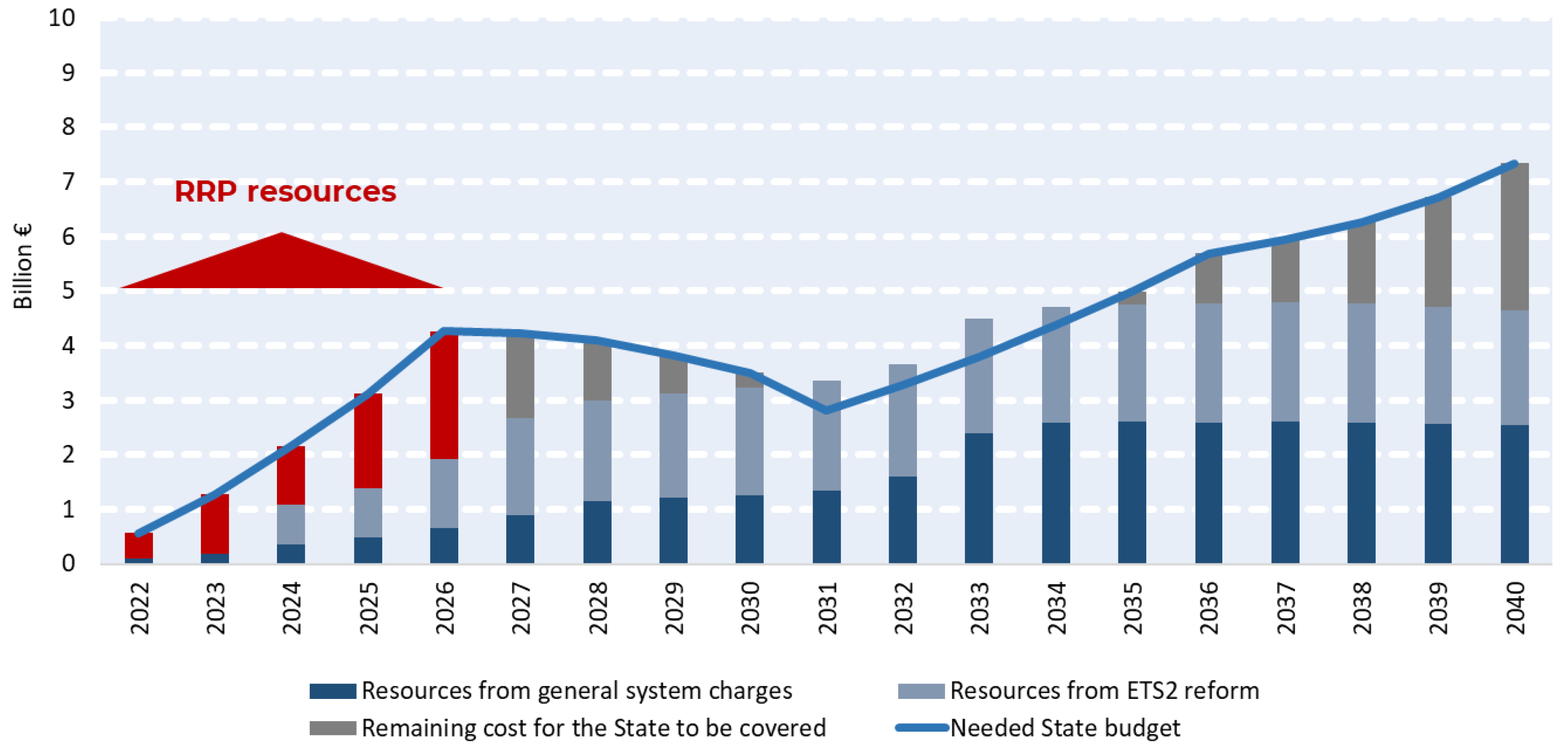

To reach the abovementioned objectives, in the short run (2022–2026), the national government should use NRRP resources as an opportunity to activate investments in energy-efficiency measures and, in turn, boost the increase in the annual deep-renovation rate (equal to about 0.3% during 2012–2016), which should be four times higher in 2030 (

Figure 5).

Through incentive mechanisms, public funds can be used as leverage for private investments in the building sector. After 2026, additional public budget should be allocated to redesign gradually incentive schemes provided to citizens at the individual level, focusing on the most energy-intensive buildings.

In the long run, rate reduction should be offset with simplified forms of funding at low rates, provided by credit institutions and guaranteed through public funds. A long-term strategy of financial framework and support schemes is needed. To calculate the costs of the proposed scheme, we applied the deep-renovation rates above to a total number of dwellings in multifamily buildings equal to 13,248,796 and a total number of single homes equal to 6,705,072. We also estimated the annual governmental budget needed to finance the incentive mechanism. As already mentioned, funds allocated by the NRRP (Mission 2—Component 3) can be used in the short run until 2026; then, other resources must be found and earmarked to cover the needed state budget. Some other possible financing sources include (

Figure 6):

Revenues from general system charges (namely ASOS components) that are currently addressed to incentivize renewables and included in the electricity tariff.

In Italy, the electricity price is composed of the following components: (i) Procurement costs that cover the costs of purchasing electricity from the wholesale market, plus other marketing, dispatching and imbalance costs; (ii) Network costs, i.e., costs paid for transmission, distribution and measurement of electricity; (iii) The system charges tariff, i.e., the costs of supporting activities of general interest for the electric system, including those incurred to purchase and incentivize electricity from renewable sources (namely “ASOS” components); (iv) Taxes, i.e., VAT and excise duties. ASOS components are expected to decrease over time due to expiration of incentives for renewables. Our suggestion is to maintain and reallocate this tariff component to all energy carriers (gas, electricity, transport) according to their environmental impact so as to ensure minimum resources for financing energy-efficiency measures. This reform could also solve the existing imbalance among the electric and gas tariff with respect to the amount paid for incentivizing renewable energies. Currently, the gas tariff pays for fewer tax components and parafiscal charges (i.e., general system charges) compared to the electric tariff, disadvantaging electrification of the final energy consumption. Therefore, it is necessary to review and counterbalance the taxation of electricity and natural gas via taking into consideration (i) energy content, (ii) environmental impact (negative externalities) and (iii) stability over time.

Resources from anticipation of the Commission proposal that will introduce a new emission trading system (ETS) for buildings.

Within the Fit For 55 package, the European Commission proposed to create a new system (called ETS2) to cap and trade carbon emissions from two major laggard sectors, i.e., road transport and buildings, in order to accelerate their decarbonization pathways. Manufacturing and energy industries, already covered by the old EU ETS, have, in fact, cut GHG emissions by more than 40% since 1990. Designed to start in 2026, the new ETS2 will put a price on emissions from the building and road-transport sectors. Suppliers (rather than households or car drivers) will be responsible for monitoring and reporting the quantities of fuel they place on the market and surrendering emission allowances each calendar year depending on the carbon intensities of these fuels. This approach aims to incentivize fuel suppliers to decarbonize their products, as this will reduce costs of compliance with the emissions trading system. In any case, under the new system, fuel retailers will largely pass the carbon price onto their customers, so final consumers will face higher prices for fossil fuels for transport and heating. Thus, the EC also introduced a Social Climate Fund of 72 billion EUR, aimed at addressing the social challenges that vulnerable groups in society may face. Our suggestion is to introduce carbon pricing on heating before 2026 and use the revenue thereof to cover the costs of energy-efficiency measures in buildings.

Added VAT revenues due to the increase in the construction industry’s value. The proposed mechanism could favor productivity growth in the construction sector, which would in turn generate higher revenues related to value-added taxes. According to experts, 25–30% of the public expenditure allocated to cover this mechanism would return to the public budget in the form of VAT revenues.

Resources from incentive schemes that are removed or lowered by this proposal. The abolishment of the current tax rebate for ordinary and extraordinary maintenance, restoration and building refurbishment (which do not regard energy-efficient renovations) could release resources that could instead be used for financing energy-efficiency measures.

4.2. A Revolving Fund for Schools and Public Housing Renovations

Although public authorities do not pay income taxes, the 110% Superbonus rebate has also financed public-house-renovation plans thanks to the credit-assignment mechanism. In this way, some local social housing bodies and associations have developed very interesting interventions. However, in our perspective, deep energy retrofitting of public buildings such as schools and social housing should be financed through a specific revolving scheme. According to our estimates (Chapter 3), the total size of the fund should be equal to 17 billion EUR in order to renovate about 1600 schools per year (a school renovation rate equal to 3%).

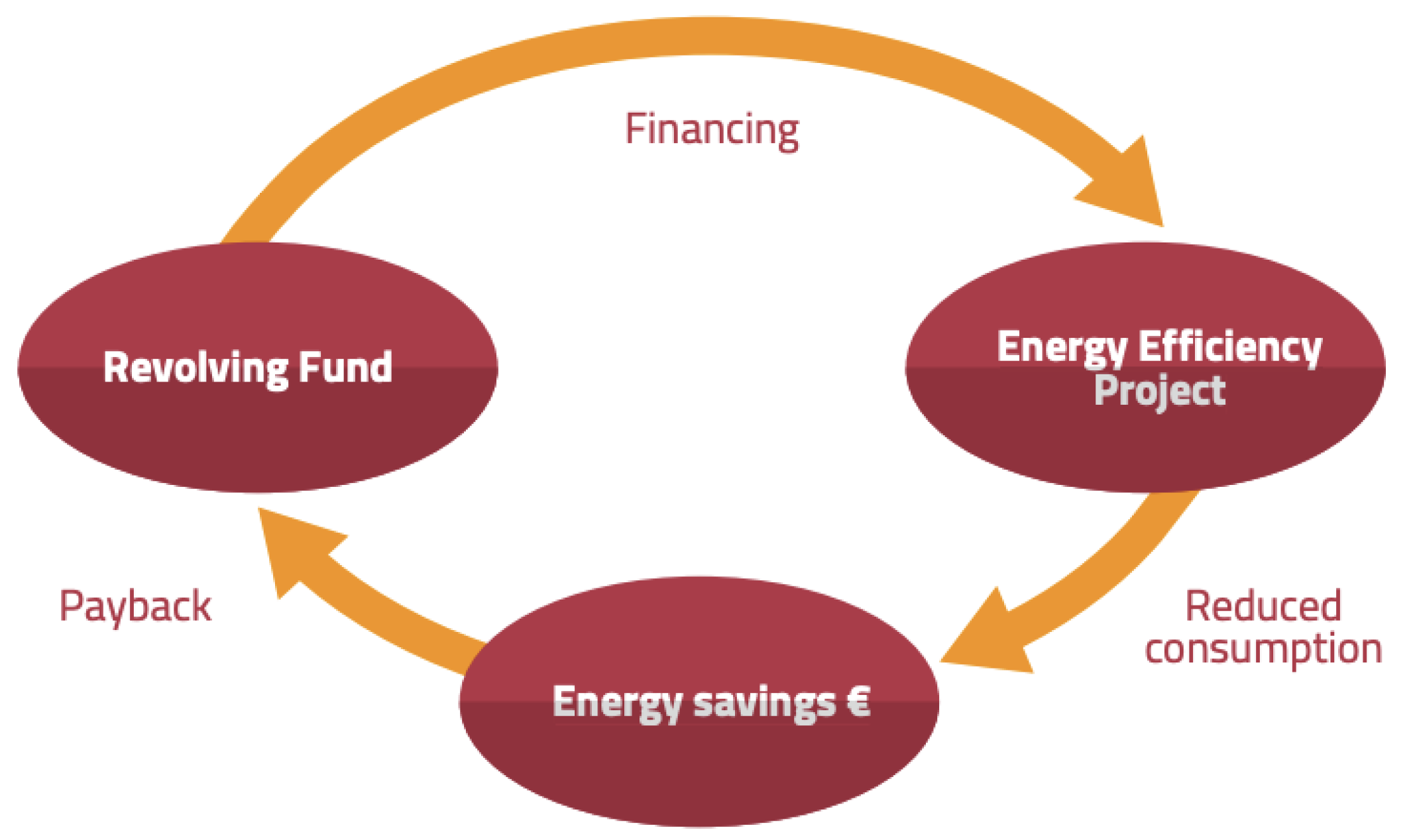

An energy-efficiency revolving fund is a type of fund that is dedicated to scaling up energy-efficiency investments using a revolving mechanism. A portion of the savings generated via supported investments is used to partially replenish the fund (i.e., revolved), allowing for reinvestments in future projects of similar value. This represents a promising support mechanism, as it acts as an ongoing funding vehicle that helps drive more energy-efficiency investments over time while generating cost savings and ensuring that capital is available for further projects [

44]. To ensure that this support mechanism will deliver, it is necessary to allocate sufficient funds in the revolving fund. In addition, the rate of return of supported energy-efficiency interventions must balance the risks associated with this type of fund, which means that projects must be closely monitored to accurately calculate energy savings (and thereby rates of return) [

44].

Some examples of revolving funds are the following: The Energy Efficiency and Renewable Sources Fund in Bulgaria; The Kredex Fund in Estonia; The National Revolving Fund for Energy Saving in the Netherlands; The SALIX scheme in the UK [

44]. For example, in the last case, the government funded a private company called Salix Finance Ltd. to establish energy-efficiency revolving-loan schemes in the public sector. This company developed an innovative spend-to-save program to overcome barriers in the public sector. Salix provided interest-free loans to organizations that were required to provide matched funding and establish an ongoing ring-fenced energy-saving fund within the organization. The energy or estates team would then (typically) use this fund to support projects across the estate that would pay back into the loan fund using the energy savings they generated. These loans, once established, would continue to deliver energy savings over time, with recycled savings used to repay each individual project loan and then released for frontline services.

An example of a revolving fund in Italy is the “Fondo rotativo per il sostegno alle imprese e agli investimenti in ricerca" (revolving fund to support business and investment in research), which is addressed to companies that invest in the following sectors: Research and development; Technological innovation; Industry; Tourism, Trade; Craft; Agriculture; Service. The national Deposits and Loans Fund (“Cassa Depositi e Prestiti”, CDP) provides medium–long-term finance, pooled with the banking system, for entities that make investments that are eligible for public subsidies on various measures, at favorable economic conditions. Subsidized financing normally covers 50% of a loan, reaching a maximum value of 90% for research, development and innovation programs. The entity eligible for the loan (i.e., the beneficiary subject) enters a single loan contract, composed of a quota granted by the CDP at a subsidized rate and a quota granted by a bank at the market rate.

A hypothetical way to replenish the initial fund is for newly renovated buildings to pay, for a fixed number of years, the same energy bills despite their energy savings (a small reduction could also be considered) so as to feed the revolving-fund budget, which could then be used for other retrofitting interventions (

Figure 7).

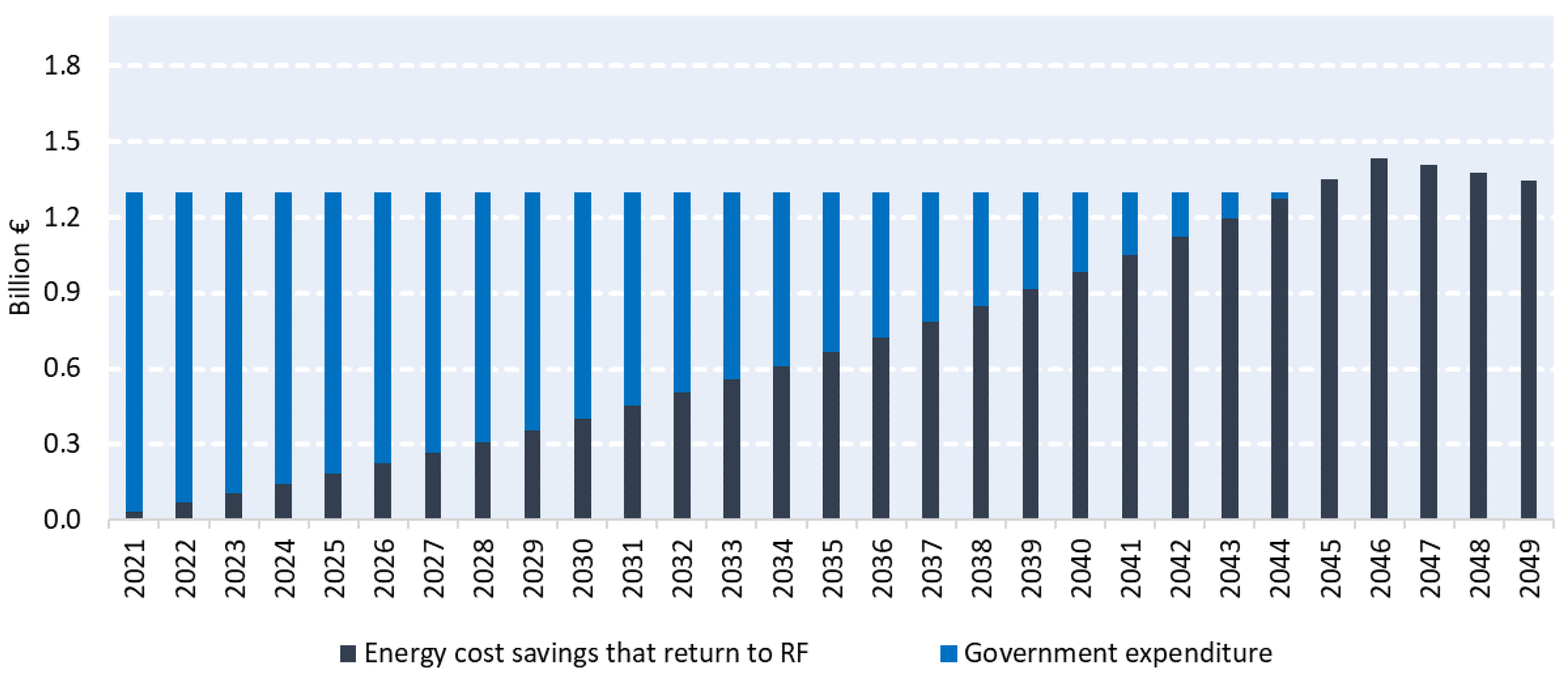

The revolving fund could be financed with the public budget and particularly with resources consistent with Directive 108/2018 targets. NRRP resources for renovation of schools should be better allocated through setup of a revolving fund to involve a greater number of buildings and create the opportunity to continuously finance new investments.

According to our estimates, every year, the fund should consist of about 1.3 billion EUR to renovate 1600 schools and reduce their energy consumption by about 60 kWh/m

2. This fund would be partially financed via energy cost savings obtained by renovated schools, as reported in

Figure 8.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}