Investment Decision for Long-Term Battery Energy Storage System Using Least Squares Monte Carlo

Abstract

:1. Introduction

- Development of a scheduling algorithm for the economic operation of a central dispatch ESS (10 MW/40 MWh) in the Korean electricity market.

- Using the GBM model for ESS arbitrage revenue to consider future revenue uncertainty.

- Analysis of ESS revenue and investment costs using LSMC simulations to determine optimal investment timing.

2. Problem Formulation

2.1. Optimal Investment Considering ESS’s Revenue and Investment Cost

2.2. GBM Model of Revenue Reflecting Uncertainty

2.3. LSMC Simulation to Determine the Investment Timing

3. LSMC-Based Method for ESS Investment Decision

3.1. ESS Scheduling for Arbitrage Revenue Calculation

3.2. ESS Installed Costs

3.3. Overview Diagram of the Proposed Method

- Step 1:

- This paper starts with the ESS setting. Information regarding ESS type, capacity, discharge duration, DoD, and RTE is collected and an ESS is set to conduct research using the collected information.

- Step 2:

- Perform ESS scheduling to calculate annual revenue. An objective function that maximizes the revenue from arbitrage trading is used. The constraints on the economic operation of the ESS are used. Scheduling uses the SMP and CP data.

- Step 3:

- GBM modeling is performed to stochasticize the uncertain ESS revenue. A 20-year ESS revenue process in a risk-neutral world is created. An analysis of 22 years of revenue is conducted to determine the annual volatility of the ESS revenue.

- Step 4:

- The investment value for the 20-year revenue scenario is calculated by considering the ESS investment cost. Subsequently, the estimated T−1 holding value is calculated by applying a risk-free interest rate in year T.

- Step 5:

- The investment value in T−1 is calculated using least squares regression analysis of the value in year T and the estimated holding value in year T−1. Least squares regression minimizes the sum of the residual squares between the actual and estimated values.

- Step 6:

- Determine investment decisions based on recalculated investment and holding values. If the investment value is greater than the holding value, ESS investment is carried out, and if the holding value is more significant, ESS investment is not made.

- Step 7:

- Repeating this process calculates the holding value for each revenue process. The final investment and holding values of the process are compared to determine the timing of the investment.

4. Case Study

4.1. ESS Parameter and CRF Setting

4.2. Arbitrage Revenue for Lithium-Ion Battery ESS Using Scheduling

4.3. GBM Model Reflecting ESS Revenue Uncertainty

4.4. Determining of Optimal ESS InvestmentTiming

5. Conclusions

- Analyze revenue through economic ESS operational constraints in the Korean electricity market, and consider future revenue uncertainty using GBM.

- Determine the optimal investment timing of ESSs using LSMC simulation considering the actual investment cost.

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- UN/UNFCCC. Paris Agreement. 2015. Available online: https://unfccc.int/sites/default/files/english_paris_agreement.pdf (accessed on 12 April 2024).

- IPCC. Global Warming of 1.5 °C; IPCC: Geneva, Switzerland, 2018; Available online: https://www.ipcc.ch/sr15/download/ (accessed on 12 April 2024).

- Ministry of Environment. 2030 National Greenhouse Gas Reduction Goals; Ministry of Environment: Sejong, Republic of Korea, 2021. [Google Scholar]

- Ministry of Trade, Industry and Energy. The 10th Basic Plan for Electricity Supply and Demand; Ministry of Trade, Industry and Energy: Sejong, Republic of Korea, 2023. [Google Scholar]

- Korea Institute of Energy Research. The Potential of Renewable Energy in Korea. 2024. Available online: https://kier-solar.org/user/map/map_patential.do (accessed on 14 April 2024).

- Kim, S.; Joo, S.-K. Transmission Pricing Incorporating the Impact of System Fault and Renewable Energy Uncertainty on the Transmission Margin. IEEE Access 2023, 11, 103779–103789. [Google Scholar] [CrossRef]

- Korea Energy Economics Institute. Flexibility of Power Systems for the Supply of New and Renewable Energy; Korea Energy Economics Institute: Ulsan, Republic of Korea, 2017. [Google Scholar]

- International Renewable Energy Agency (IRENA). Global Renewables Outlook: Energy Transformation 2050; International Renewable Energy Agency: Masdar City/Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- United States Department of Energy. Energy Storage Grand Challenge Roadmap. 2020. Available online: https://www.energy.gov/sites/default/files/2020/12/f81/Energy%20Storage%20Grand%20Challenge%20Roadmap.pdf (accessed on 12 April 2024).

- Korea Electrical Safery Corpotation. Statistics of Electrical Storage by Power Generation Resource. 2023. Available online: https://www.data.go.kr/data/15086616/fileData.do (accessed on 12 April 2024).

- Ministry of Trade, Industry and Energy. Energy Storage Industry Development Strategy; Ministry of Trade, Industry and Energy: Sejong, Republic of Korea, 2023. [Google Scholar]

- Filho, R.D.; Monteiro, A.C.M.; Costa, T.; Vasconcelos, A.; Rode, A.C.; Marinho, M. Strategic Guidelines for Battery Energy Storage System Deployment: Regulatory Framework, Incentives, and Market Planning. Energies 2023, 16, 7272. [Google Scholar] [CrossRef]

- Guerra, O.J. Beyond short-duration energy storage. Nat. Energy 2021, 6, 460–461. [Google Scholar] [CrossRef]

- National Grid Electricity System Operator. NOA Stability Pathfinder RFI Phase 1. 2019. Available online: https://www.nationalgrideso.com/industry-information/balancing-services/pathfinders/noa-stability-pathfinder#Phase-1-(concluded) (accessed on 12 April 2024).

- Pacific Gas and Electric Company. Mid-Term Realability RFO—Phase 2. 2022. Available online: https://www.pge.com/en/about/doing-business-with-pge/wholesale-electric-power-procurement/mid-term-reliability-rfo-phase-2.html (accessed on 12 April 2024).

- Korea Power Exchange (KPX), 2023 Jeju Long Term BESS Contract Competitive Bidding Announcement. 2023. Available online: https://www.kpx.or.kr/board.es?mid=a11201000000&bid=0042&act=view&list_no=70288 (accessed on 12 April 2024).

- Miletić, M.; Pandžić, H.; Yang, D. Operating and Investment Models for Energy Storage Systems. Energies 2020, 13, 4600. [Google Scholar] [CrossRef]

- Moon, Y. Optimal Time to Invest Energy Storage System under Uncertainty Conditions. Energies 2014, 7, 2701–2719. [Google Scholar] [CrossRef]

- Sioshansi, R.; Denholm, P.; Jenkin, T.; Weiss, J. Estimating the value of electricity storage in PJM: Arbitrage and some welfare effects. Energy Econ. 2009, 31, 269–277. [Google Scholar] [CrossRef]

- Salles, M.B.C.; Aziz, M.J.; Hogan, W.W. Potenrial Arbitrage Revenue of Energy Storage Systems in PJM during 2014. In Proceedings of the 2016 IEEE Power and Energy Society General Meeting (PESGM), Boston, MA, USA, 17–21 July 2016; pp. 1–5. [Google Scholar] [CrossRef]

- Coronel, T.; Buzarquis, E.; Blanco, G.A. Analyzing energy storage system for energy arbitrage. In Proceedings of the 2017 IEEE URUCON, Montevideo, Uruguay, 23–25 October 2017; pp. 1–4. [Google Scholar] [CrossRef]

- Nguyen, T.A.; Copp, D.A.; Byrne, R.H. Stacking Revenue from Energy Storage Providing Resilience, T&D Deferral and Arbitrage. In Proceedings of the 2019 IEEE Power & Energy Society General Meeting (PESGM), Atlanta, GA, USA, 4–8 August 2019; pp. 1–5. [Google Scholar] [CrossRef]

- Sang, L.; Xu, Y.; Long, H.; Hu, Q.; Sun, H. Electricity Price Prediction for Energy Storage System Arbitrage: A Decision-Focused Approach. IEEE Trans. Smart Grid 2022, 13, 2822–2832. [Google Scholar] [CrossRef]

- An, J.; Kim, D.-K.; Lee, J.; Joo, S.-K. Least Squares Monte Carlo Simulation-Based Decision-Making Method for Photovoltaic Investment in Korea. Sustainability 2021, 13, 10613. [Google Scholar] [CrossRef]

- Liu, H.; Wang, L.; Li, J.; Shao, L.; Zhang, D. Research on Smart Power Sales Strategy Considering Load Forecasting and Optimal Allocation of Energy Storage System in China. Energies 2023, 16, 3341. [Google Scholar] [CrossRef]

- Chen, H.; Bo, R.; ur Rehman, W. Developing Optimal Energy Arbitrage Strategy for Energy Storage System Using Reinforcement Learning. In Proceedings of the CIRED 2021—The 26th International Conference and Exhibition on Electricity Distribution, Online, 20–23 September 2021; pp. 2266–2270. [Google Scholar] [CrossRef]

- Zubair, M.; Taina, N.; Gadotti, M.; Salles, B.C. Potential Arbitrage Revenue of Energy Storage System for MISO Energy Markets. In Proceedings of the 2023 International Conference on Clean Electrical Power (ICCEP), Terrasini, Italy, 27–29 June 2023. [Google Scholar] [CrossRef]

- Lee, D.; Lee, D.; Jang, H.; Joo, S.-K. Backup Capacity Planning Considering Short-Term Variability of Renewable Energy Resources in a Power System. Electronics 2021, 10, 709. [Google Scholar] [CrossRef]

- Yoon, Y.; Kim, Y.-H. Charge Scheduling of an Energy Storage System under Time-of-Use Pricing and a Demand Charge. Sci. World J. 2014, 2014, 937329. [Google Scholar] [CrossRef]

- Alam, M.M.; Rahman, M.H.; Nurcahyanto, H.; Jang, Y.M. Energy Management by Scheduling ESS with Active Demand Response in Low Voltage Grid. In Proceedings of the 2020 International Conference on Information and Communication Technology Convergence (ICTC), Jeju, Republic of Korea, 21–23 October 2020; pp. 683–686. [Google Scholar] [CrossRef]

- Park, J.-B.; Park, Y.-G.; Roh, J.-H.; Chang, B.-H.; Yoon, Y.-B. An Economic Assessment of Large-scale Battery Energy Storage Systems in the Energy-Shift Application to Korea Power System. Trans. Korean Inst. Electr. Eng. 2015, 64, 384–392. [Google Scholar] [CrossRef]

- Jang, M.; Jeong, H.C.; Kim, T.; Chun, H.-M.; Joo, S.-K. Analysis of Residential Consumers’ Attitudes toward Electricity Tariff and Preferences for Time-of-Use Tariff in Korea. IEEE Access 2022, 10, 26965–26973. [Google Scholar] [CrossRef]

- Hwang, H.-K.; Yoon, A.-Y.; Lee, J.-O.; Chang, J.-W.; Moon, S.-I. Optimal ESS Scheduling for the TOU Tariff based DR and Cost-saving DR. In Proceedings of the 49th Korean Institute of Electrical Engineers Summer Conference, Gangwon, Republic of Korea, 11–13 July 2018; pp. 281–282. [Google Scholar]

- Jin, Y.; Park, M.; Won, D. ESS Optimal Scheduling considering Demand Response for commercial Buildings. In Proceedings of the 2019 7th International Youth Conference on Energy (IYCE), Bled, Slovenia, 3–6 July 2019; pp. 1–6. [Google Scholar] [CrossRef]

- Ko, R.; Kong, S.; Joo, S.-K. Mixed Integer Programming (MIP)-based Energy Storage System Scheduling Method for Reducing the Electricity Purchasing Cost in an Urban Railroad System. Trans. Korean Inst. Electr. Eng. 2015, 64, 1125–1129. [Google Scholar] [CrossRef]

- Salles, M.B.C.; Huang, J.; Aziz, M.J.; Hogan, W.W. Potential Arbitrage Revenue of Energy Storage Systems in PJM. Energies 2017, 10, 1100. [Google Scholar] [CrossRef]

- Cha, H.-J.; Lee, S.-E.; Won, D. Implementation of Optimal Scheduling Algorithm for Multi-Functional Battery Energy Storage System. Energies 2019, 12, 1339. [Google Scholar] [CrossRef]

- Korea Power Exchange (KPX). System Marginal Price. Available online: https://www.kpx.or.kr/smpInland.es?mid=a10606080100&device=pc (accessed on 12 April 2024).

- Korea Power Exchange (KPX). Capacity Payment. Available online: https://www.kpx.or.kr/board.es?mid=a10109010500&bid=0080&act=view&list_no=69918 (accessed on 12 April 2024).

- Vitlinsky, I.D.; Cho, G.C.; Smotrov, N.N.; Bitkulov, K.R.; Umurzakov, D.D. Utilization of the Energy Storage System for the Energy Arbitrage and Peak Shaving. In Proceedings of the 2022 4th International Youth Conference on Radio Electronics, Electrical and Power Engineering (REEPE), Moscow, Russia, 17–19 March 2022; pp. 1–6. [Google Scholar] [CrossRef]

- Ministry of Trade, Industry and Energy. Korea Electro-Technical Code. Available online: https://www.law.go.kr/LSW//admRulLsInfoP.do?chrClsCd=&admRulSeq=2100000232752 (accessed on 12 April 2024).

- National Renewable Energy Laboratory (NREL). Life Prediction Model for Grid Connected Li-Ion Battery Energy Storage System; National Renewable Energy Laboratory: Washington, DC, USA, 2017. [Google Scholar]

- International Renewable Energy Agency (IRENA). Electricity Storage Valuation Framewokr: Assesing System Value and Ensuring Project Viability; International Renewable Energy Agency: Masdar City/Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Montes, T.; Etxandi-Santolaya, M.; Eichman, J.; Ferreira, V.J.; Trilla, L.; Corchero, C. Procedure for Assessing the Suitability of Battery Second Life Applications after EV First Life. Batteries 2022, 8, 122. [Google Scholar] [CrossRef]

- Pacific Northwest National Laboratory (PNNL). Washing Ton Clean Energy Fund Grid Modernization Projects: Economic Analysis Final Report; Pacific Northwest National Laboratory: Washington, DC, USA, 2020. [Google Scholar]

- Pacific Gas and Electric Company (PG&E). 2019 SGIP Energy Storage Market Assessment and Cost-Effectiveness Report; Pacific Gas and Electric Company: California, MA, USA, 2019. [Google Scholar]

- Strategen Consulting. Long Duration Energy Storage for California’s Clean, Reliable Grid; Strategen Consulting: California, MA, USA, 2020. [Google Scholar]

- Korea Power Exchange (KPX). Electricity Market Operating Rules. Available online: https://new.kpx.or.kr/board.es?mid=a10205010000&bid=0030&act=view&list_no=71450 (accessed on 12 April 2024).

- Pacific Northwest National Laboratory (PNNL). 2022 Grid Energy Storage Technology Cost and Performance Assessment; Pacific Northwest National Laboratory: Washington, DC, USA, 2022. [Google Scholar]

- Korea Securities Depository (KSD). Korea Overnight Financing Repo Rate (KOFR). Available online: https://www.kofr.kr/rate/rate.jsp (accessed on 12 April 2024).

- Longstaff, F.A.; Schwartz, E.S. Valuing American Options by Simulation: A Simple Least-Squares Approach. Rev. Financ. Stud. 2001, 14, 113–147. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| ESS Duration | Capacity |

|---|---|

| Short-Term (within 30 min) | 3.66 GW |

| 4 h Long-Term | 4.22 GW |

| 6 h Long-Term | 15.58 GW |

| 8 h Long-Term | 1.05 GW |

| Pumped Storage | 1.75 GW |

| Year | Coupled with Renewable Energy [MW] | Peak Shaving [MW] | E.T.C [MW] |

|---|---|---|---|

| 2017 | 430 | 460 | 156 |

| 2018 | 1397 | 2437 | 2 |

| 2019 | 1015 | 791 | 1 |

| 2020 | 2734 | 129 | 3 |

| 2021 | 96 | 262 | 1 |

| 2022 | 2 | 231 | 22 |

| 2023 | - | 39 | 68 |

| ESS Parameter | Value |

|---|---|

| Depth of Discharge | 80% |

| Round Trip Efficiency | 85% |

| ESS Type | Lithium-ion battety |

| PCS Capacity | 10 MW |

| Duration | 4 h |

| ESS Capacity | 40 MWh |

| 10% | |

| 10% |

| ESS Installed Cost | Operating Cost | |||

|---|---|---|---|---|

| Total Installed Cost [$] | Total Installed Cost [$] | Fixed O&M [$] | Warranty [$] | |

| 2021 | 1,854,320 | 1,854,000 | 102,200 | 246,400 |

| 2030 | 1,399,800 | 1,400,000 | 86,800 | 160,800 |

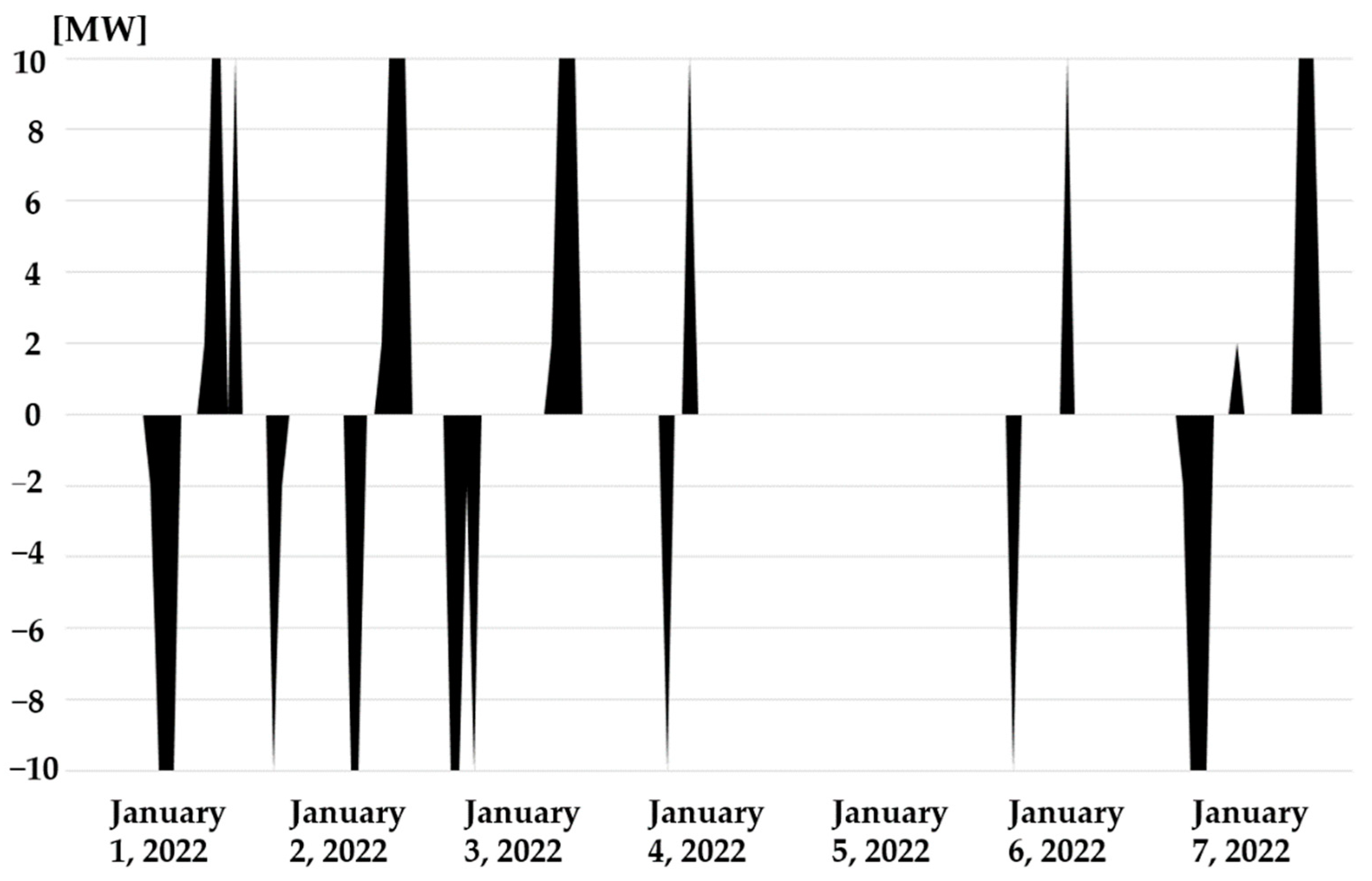

| Time [h] | Charge and Discharge Amount [MW] | Time [h] | Charge and Discharge Amount [MW] |

|---|---|---|---|

| 1:00 | - | 13:00 | −10 |

| 2:00 | - | 14:00 | −10 |

| 3:00 | - | 15:00 | −10 |

| 4:00 | - | 16:00 | - |

| 5:00 | - | 17:00 | - |

| 6:00 | - | 18:00 | - |

| 7:00 | - | 19:00 | 2 |

| 8:00 | - | 20:00 | 10 |

| 9:00 | - | 21:00 | 10 |

| 10:00 | - | 22:00 | - |

| 11:00 | - | 23:00 | 10 |

| 12:00 | - 2 | 24:00 | - |

| Year | Annual Revenue [$] | Year | Annual Revenue [$] |

|---|---|---|---|

| 2002 | 227,039.90 | 2013 | 165,752.31 |

| 2003 | 235,138.02 | 2014 | 95,398.56 |

| 2004 | 201,955.34 | 2015 | 68,352.95 |

| 2005 | 225,728.24 | 2016 | 54,903.17 |

| 2006 | 261,268.71 | 2017 | 94,886.42 |

| 2007 | 200,328.90 | 2018 | 67,515.76 |

| 2008 | 353,412.06 | 2019 | 78,605.08 |

| 2009 | 248,704.85 | 2020 | 101,959.41 |

| 2010 | 403,451.64 | 2021 | 80,359.08 |

| 2011 | 258,419.64 | 2022 | 256,380.77 |

| 2012 | 282,986.01 | 2023 | 349,631.05 |

| Year | ESS Log Return | Year | ESS Log Return |

|---|---|---|---|

| 2003 | 3.50% | 2014 | −55.24% |

| 2004 | −15.21% | 2015 | −33.34% |

| 2005 | 11.13% | 2016 | −21.91% |

| 2006 | 14.62% | 2017 | 54.71% |

| 2007 | −26.56% | 2018 | −34.03% |

| 2008 | 56.77% | 2019 | 15.21% |

| 2009 | −35.14% | 2020 | 26.01% |

| 2010 | 48.38% | 2021 | −23.81% |

| 2011 | −44.55% | 2022 | 116.02% |

| 2012 | 9.08% | 2023 | 31.02% |

| 2013 | −53.49% |

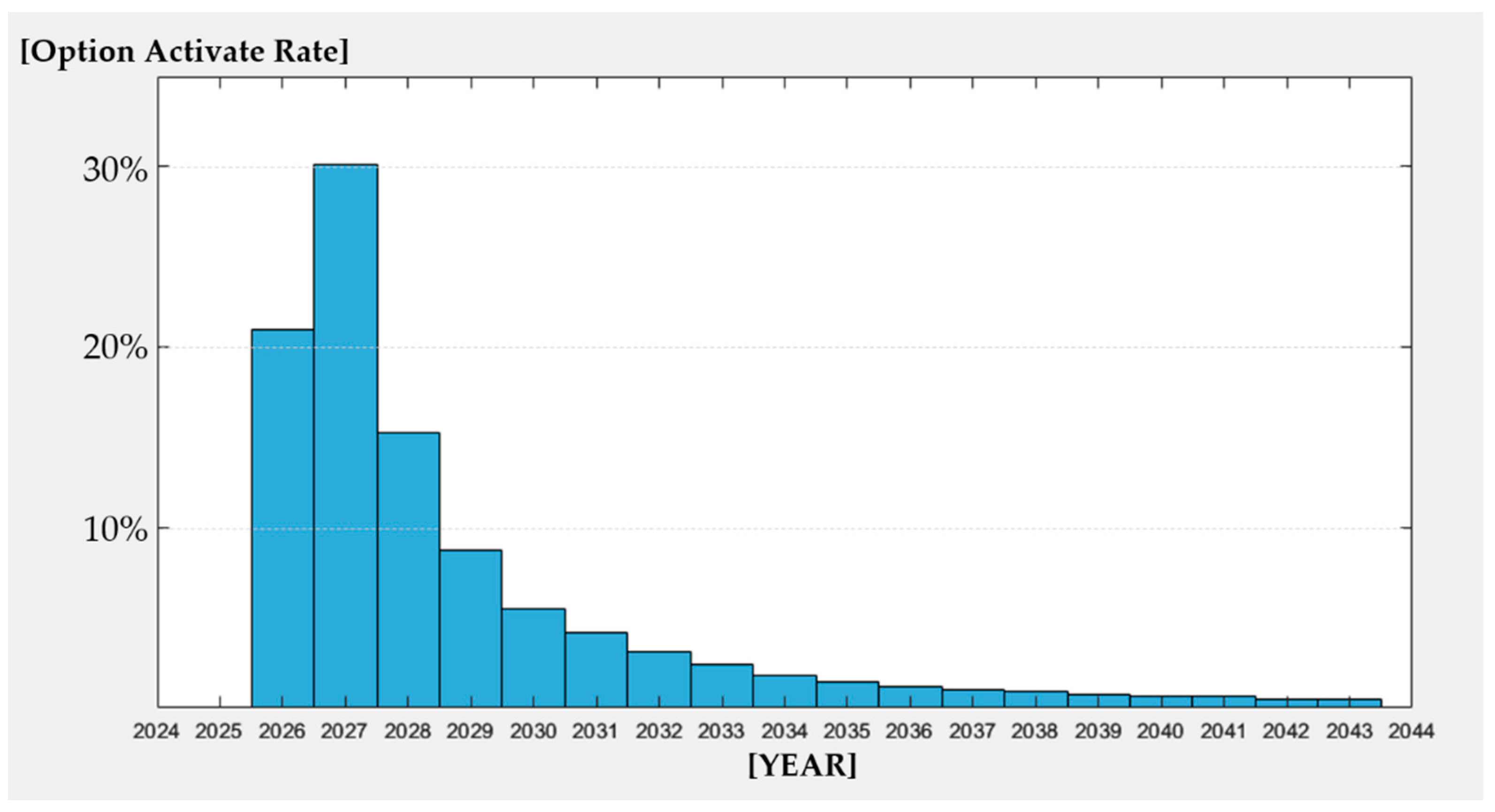

| Year | Option Active Rate | Year | Option Active Rate |

|---|---|---|---|

| 2024 | 0% | 2034 | 1.8% |

| 2025 | 0% | 2035 | 1.5% |

| 2026 | 21.0% | 2036 | 1.2% |

| 2027 | 30.1% | 2037 | 1.0% |

| 2028 | 15.3% | 2038 | 0.9% |

| 2029 | 8.8% | 2039 | 0.8% |

| 2030 | 5.5% | 2040 | 0.7% |

| 2031 | 4.2% | 2041 | 0.6% |

| 2032 | 3.1% | 2042 | 0.5% |

| 2033 | 2.4% | 2043 | 0.4% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shin, K.; Lee, J. Investment Decision for Long-Term Battery Energy Storage System Using Least Squares Monte Carlo. Energies 2024, 17, 2019. https://doi.org/10.3390/en17092019

Shin K, Lee J. Investment Decision for Long-Term Battery Energy Storage System Using Least Squares Monte Carlo. Energies. 2024; 17(9):2019. https://doi.org/10.3390/en17092019

Chicago/Turabian StyleShin, Kyungcheol, and Jinyeong Lee. 2024. "Investment Decision for Long-Term Battery Energy Storage System Using Least Squares Monte Carlo" Energies 17, no. 9: 2019. https://doi.org/10.3390/en17092019

APA StyleShin, K., & Lee, J. (2024). Investment Decision for Long-Term Battery Energy Storage System Using Least Squares Monte Carlo. Energies, 17(9), 2019. https://doi.org/10.3390/en17092019