4. Discussions

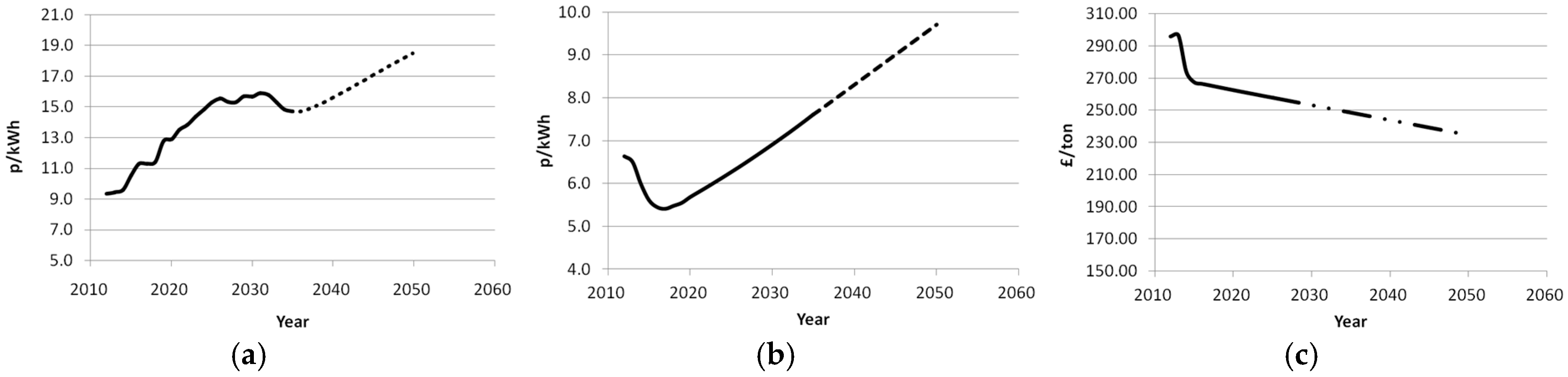

The model results show that in all cases and farm types, the production and use of biogas will increase in the period up to 2021. This is due to a combination of the price of electricity increasing over this period, but also a financial benefit for farmers to employ resources that would otherwise be wasted. The results show that the rates of FiT or RHI do not have any effects on the production rate of biogas, because irrespective of the rate, it is cost-beneficial for farmers to generate as much biogas as possible in order to benefit from the tariffs. Rather, these incentives influence the technology used to convert this biogas into useful energy, whether relatively more expensive CHP or cheaper boilers. In this regard, it was observed that in all cases, farmers invest substantially in biogas production to ensure the maximum use of the feedstocks generated on farms until 2021, after which the tariffs do not apply for new investments. This biogas is then used to either generate heat or electricity and heat, depending on the technology invested by the farms. Hence, we see that grid-fuel usage reduces gradually from 2013 until it is completely reduced in 2037. The fact that the use of all grid-fuel boilers is completely eliminated by 2037 shows that farms will not invest in such boilers from the start of the period, and instead use the residual grid-fuel boilers already in operation until the end of their lifetime of 25 years. This is the most economical way farms can proceed in all cases.

Although the trends for the period of 2013–2021 are generally similar for different rates and farm types, respectively, this period is most consequential for the later energy mix in the simulation. Depending on the electricity/heat use ratio, the energy content of the feedstock, and the tariffs’ rates, farms will determine the type of technology which is most cost-beneficial and what capacity should be installed. These technologies are then used to maximise on the returns from the tariff rates during the period 2021–2045. This is because during this latter period, the tariffs are not valid for new investments, but only for investments in technology installed before 2021, hence the relatively faster pace of most farmers to install the AD technologies prior to 2021. The capacities of the installed technologies are then used during 2021–2045 or until the end of their respective lifetimes, and thus also influence the energy mix close to 2050.

For dairy farms, it was observed that farms will only adopt CHP technologies for “FiT*2”, “FiT*4” and “FiT*4–RHI*4” cases, where the returns generated from adopting CHP technologies are adequate enough to overcome the investment and operating costs, and reduce the overall energy cost of the farms. In the case of “FiT*4”, part of the electricity generated is also exported to the grid. In the other tariff cases, investments are mainly in biogas boilers, with the electricity demand satisfied from grid-electricity supply. However, we also see from

Figure 7 that dairy farms will always need to partly depend on the grid for energy supply, as the energy potential from biogas is less than the total energy requirement of such farms.

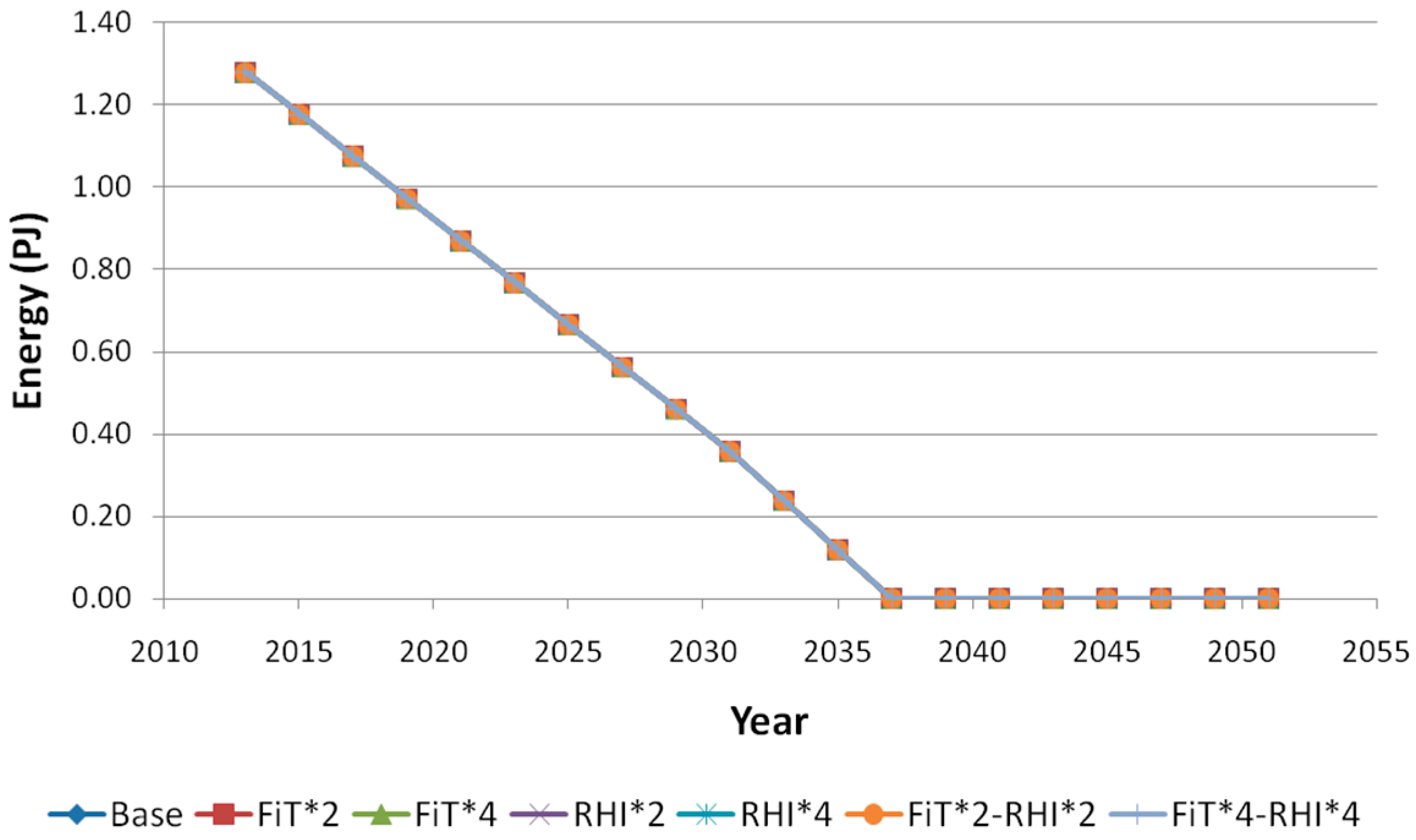

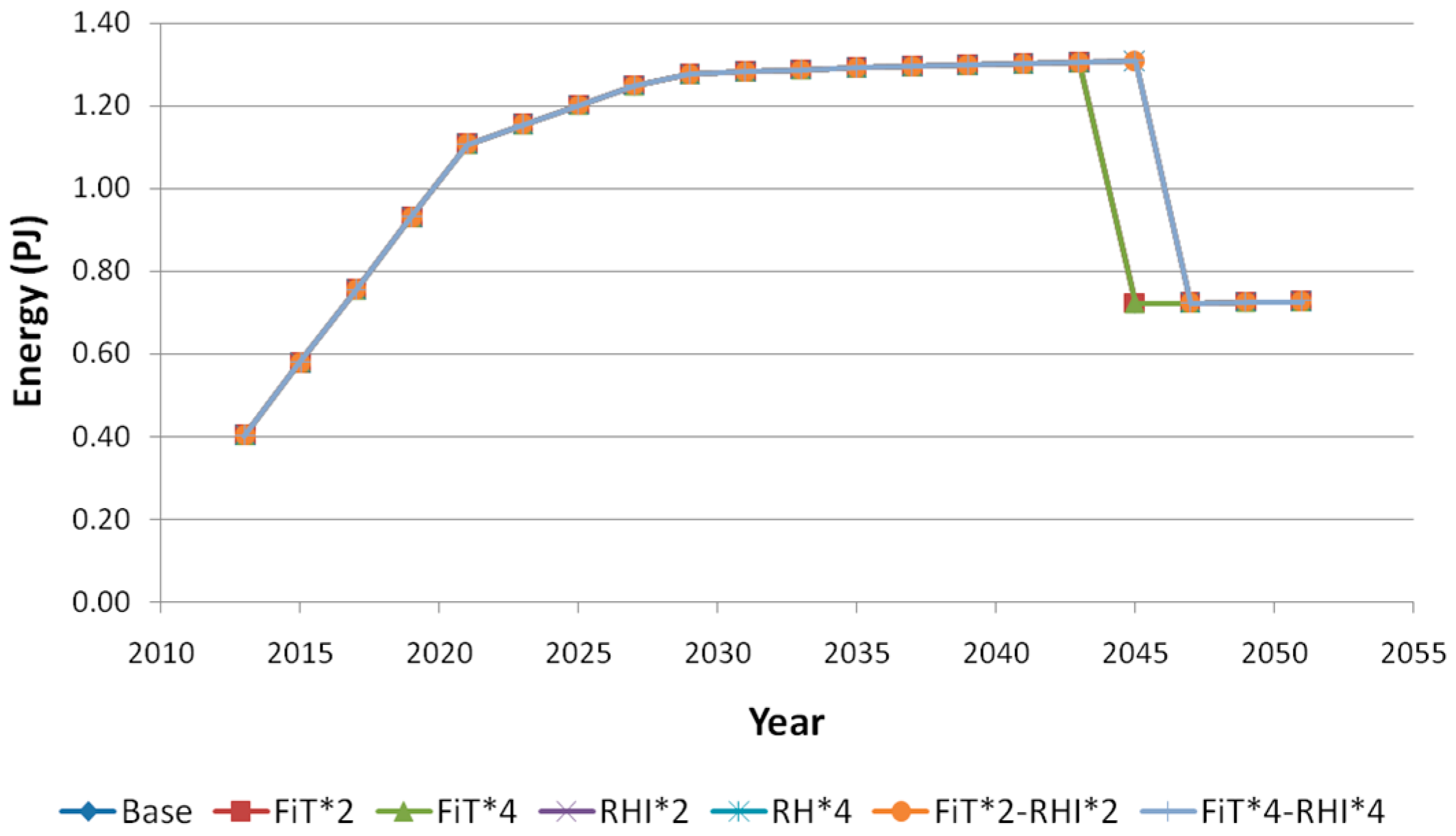

Lowlands farms, although having a pre-existing installed CHP capacity in 2013, is unlikely to sustain any further investments in CHP technology at any FiT or RHI rates. This is partly due to the relatively low electricity-heat ratio of 2.4 compared to other farms, and due to the relatively low energy content of feedstock generated mainly manure from ruminant animals (

Table 1). For this farm type, the results show that it is more cost-beneficial to use the biogas generated to produce heat from biogas boilers, and satisfy electricity demand from grid supply over the entire time-horizon. A similar situation is observed for LFA farms whereby it is generally beneficial for LFA farmers to employ the biogas generated to generate heat with biogas boilers, instead of CHP. The only exception is the case of “RHI*2” (see

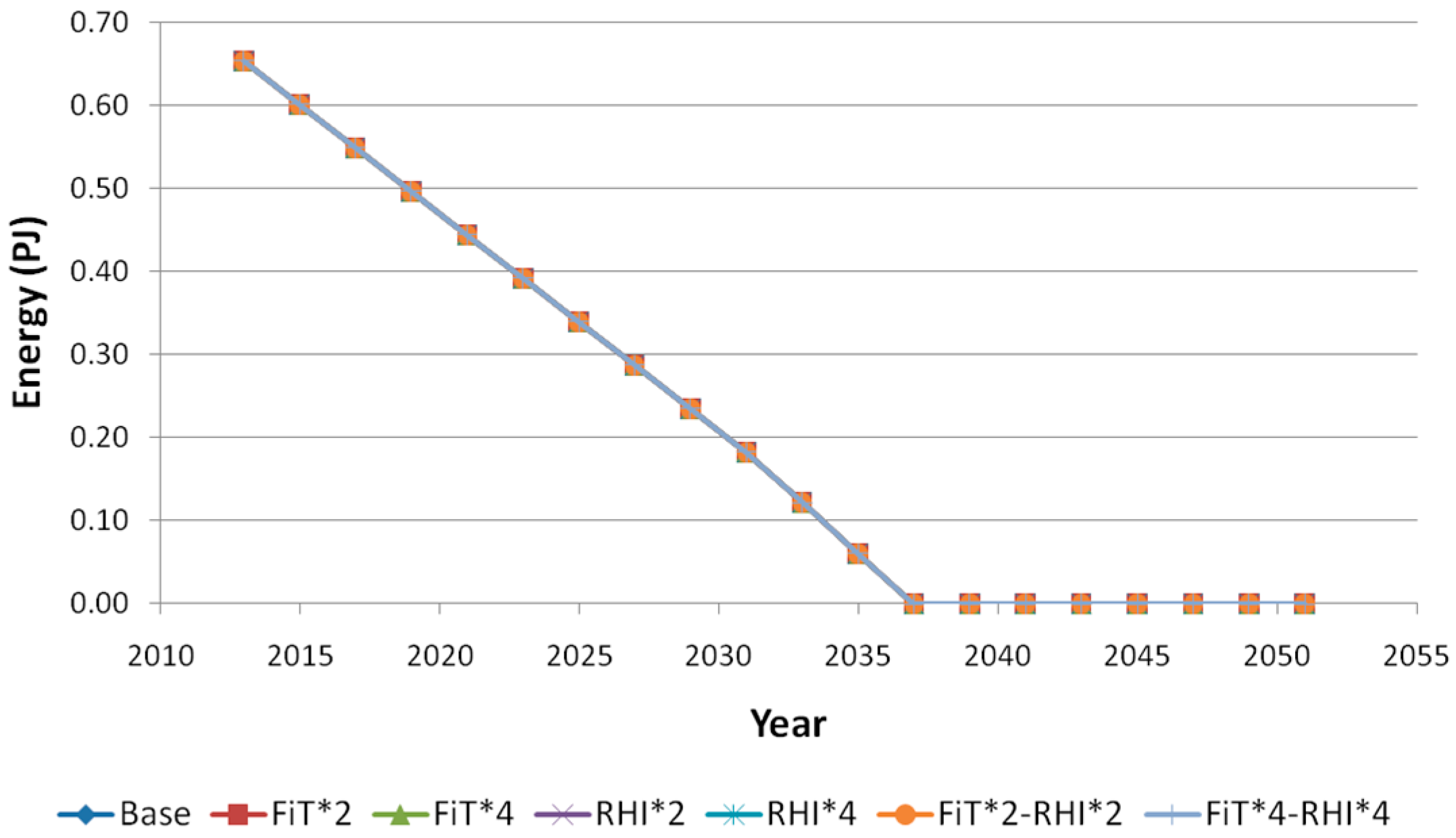

Figure 13). For this scenario, we observe partial investments in CHP technology which mitigate the demand for grid-electricity in the latter portion of the time-horizon. For LFA farms, because the electricity/heat demand ratio is also relatively low at 2.8, compared to other farms, the RHI rate has a more pronounced effect on the adoption of CHP, as opposed to FiT, as reciprocating CHP technologies produce 1.3 times more heat than electricity which enables farms to have higher return based on the generation of more heat. LFA farms, as opposed to lowlands farms, has the ability to meet its energy requirements from biogas as shown in

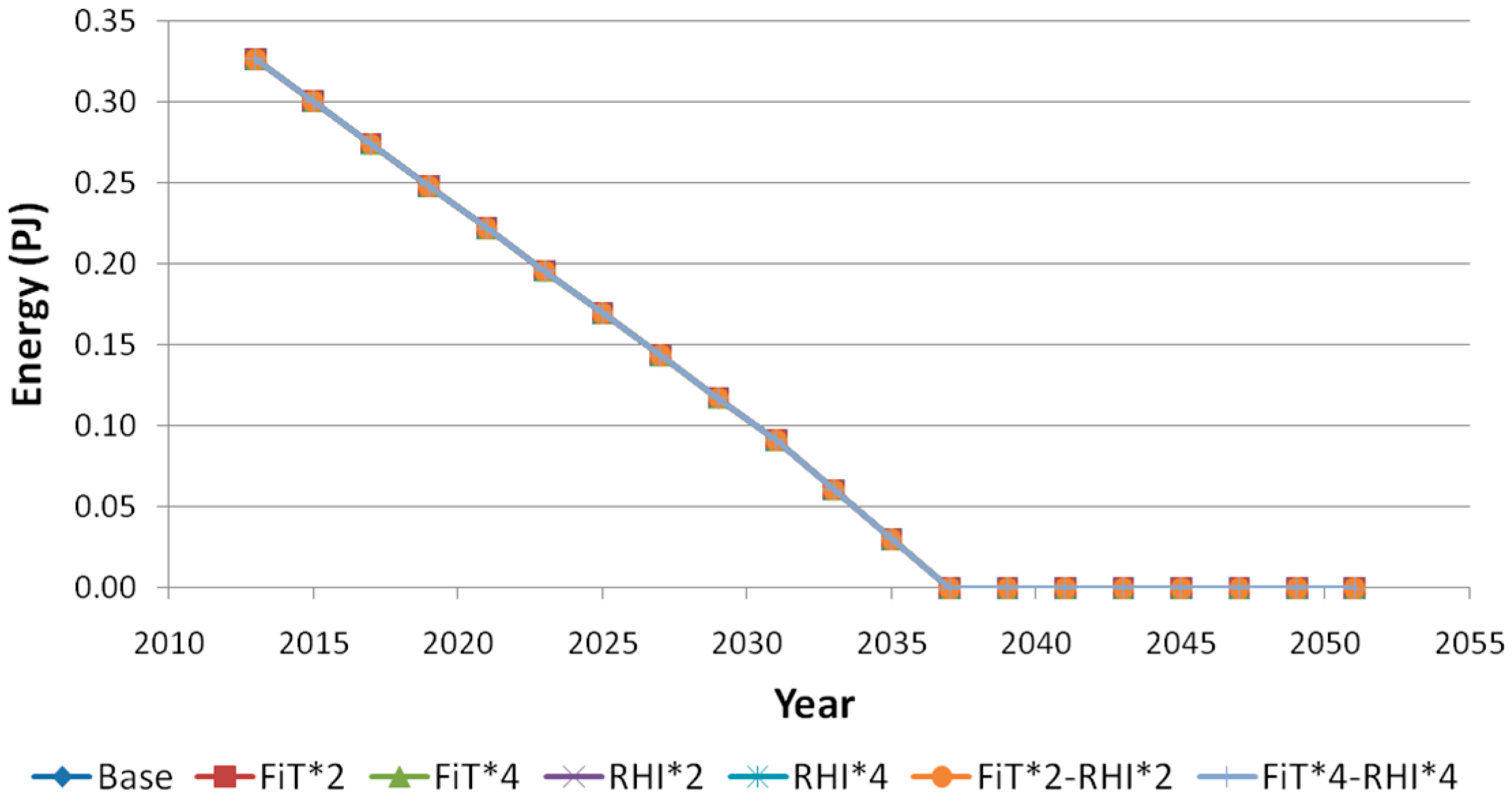

Figure 12,

Figure 13 and

Figure 14, where the embedded energy in biogas generated is higher than the total energy demand of LFA farms.

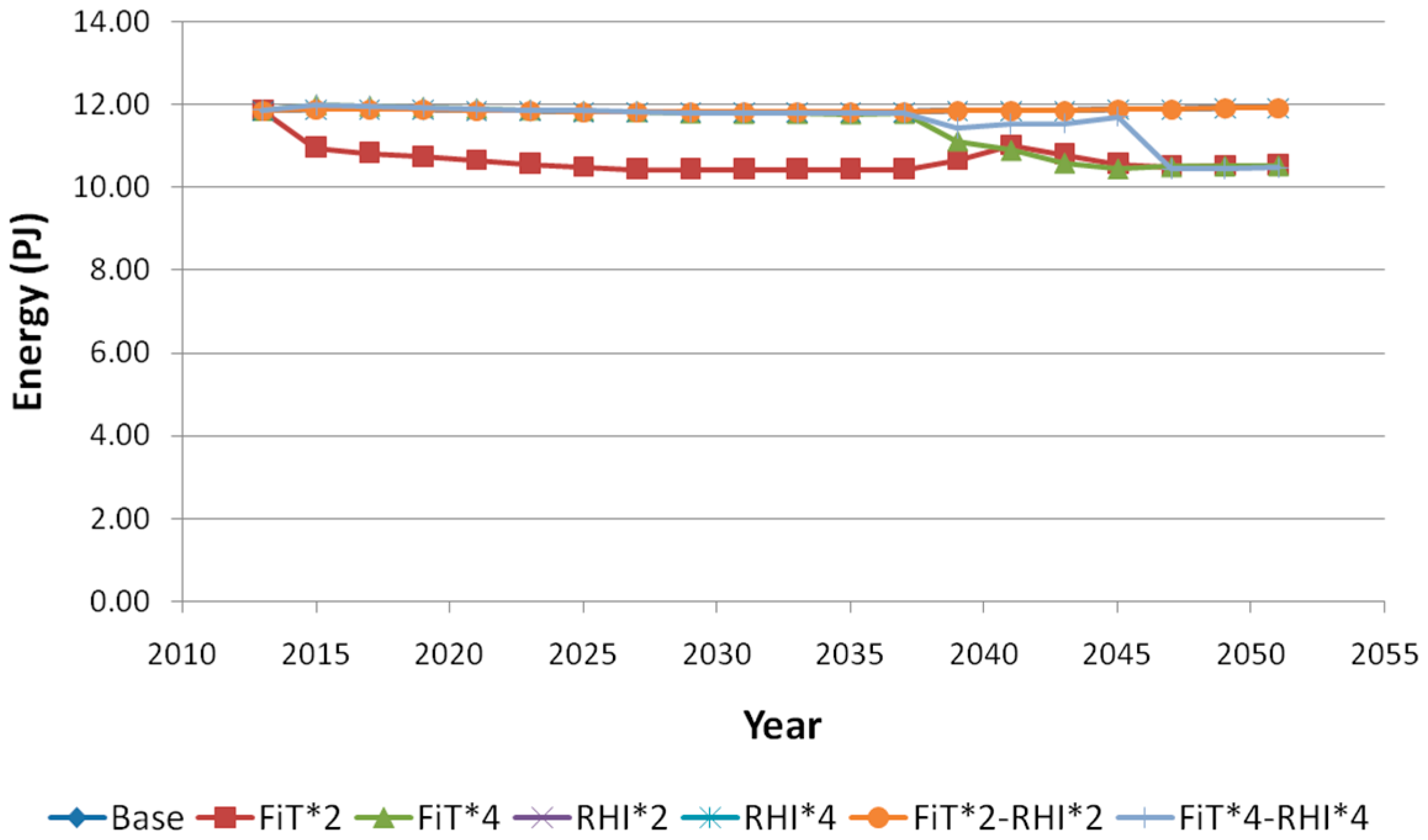

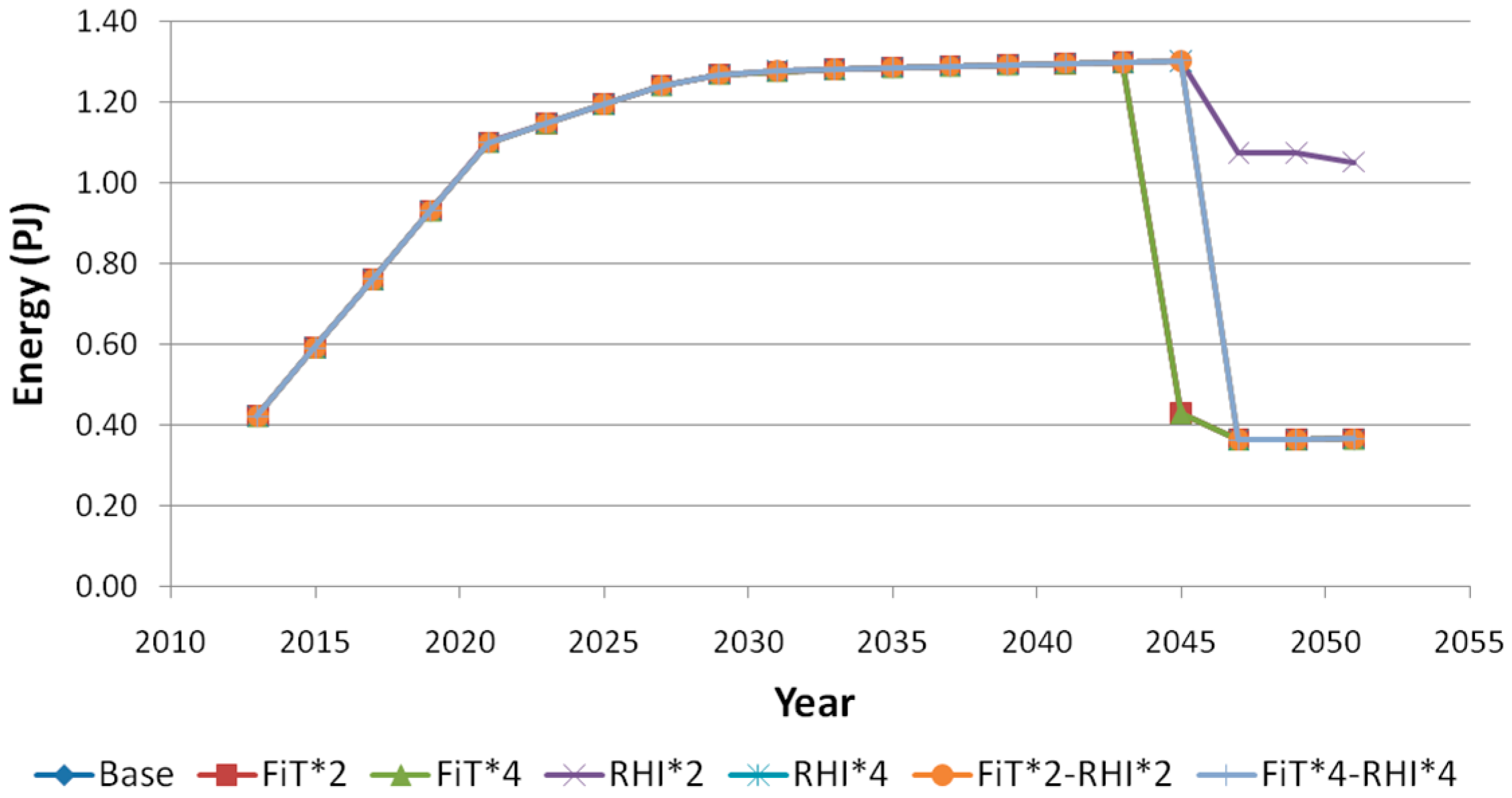

Pig farms were found to have erratic trends with respect to the different FiT and RHI rates studied. These farms have the highest electricity/heat ratio at 127, and for all cases, investing in CHP units will reduce the energy costs of pig farms. The electricity generated will be primarily consumed on-site, although at high “FiT*4” rates, approximately 50%–90% is exported during the period of 2015–2037, to maximise on returns from the tariff. In general, it is beneficial for pig farms to invest in CHP technologies even without any subsidy, however as shown in

Figure 16 and

Figure 17, under the current high energy demands for electricity and heat, it is impossible for pig farms to become self-sufficient in energy without significant process-efficiency improvement measures.

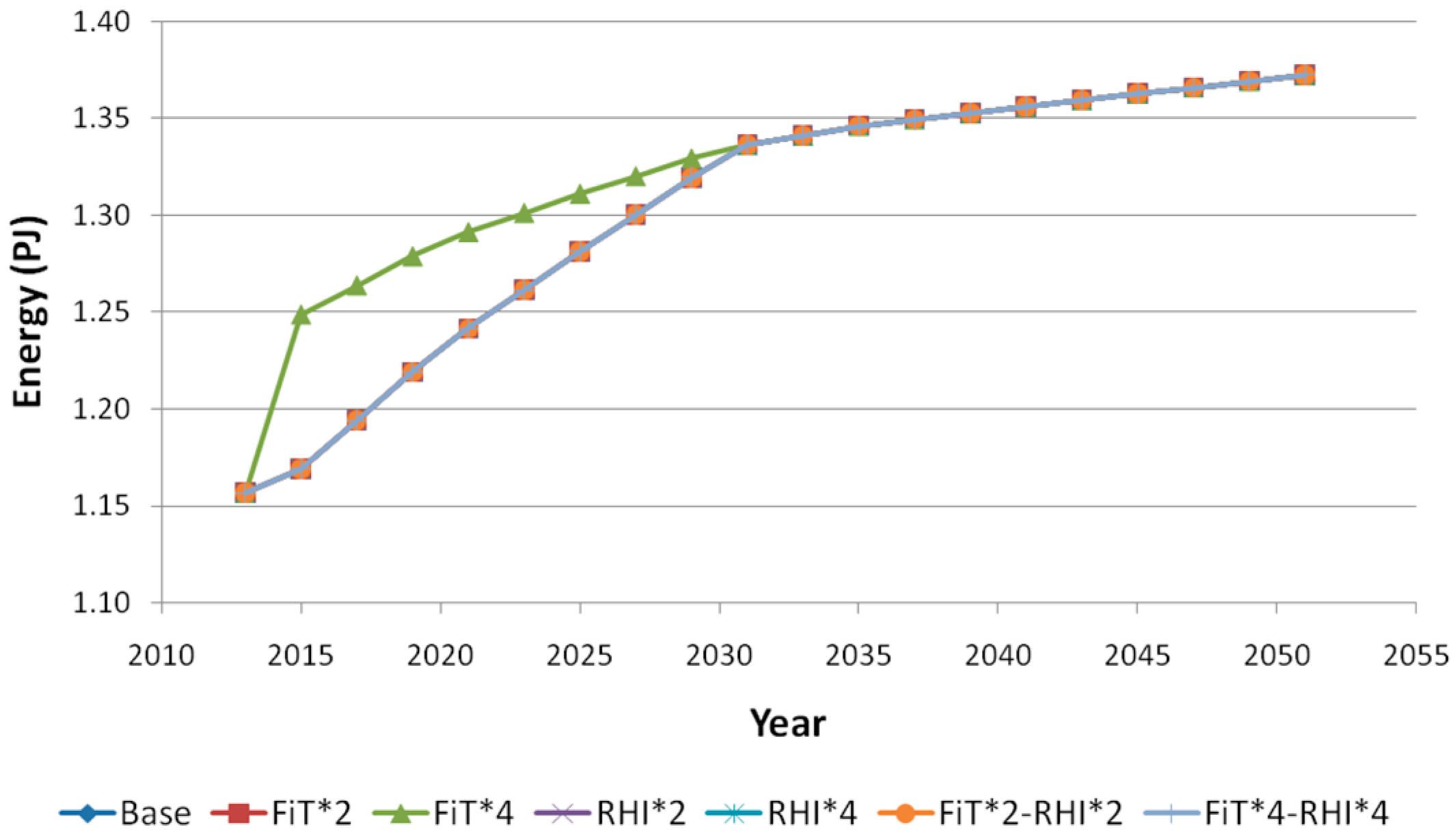

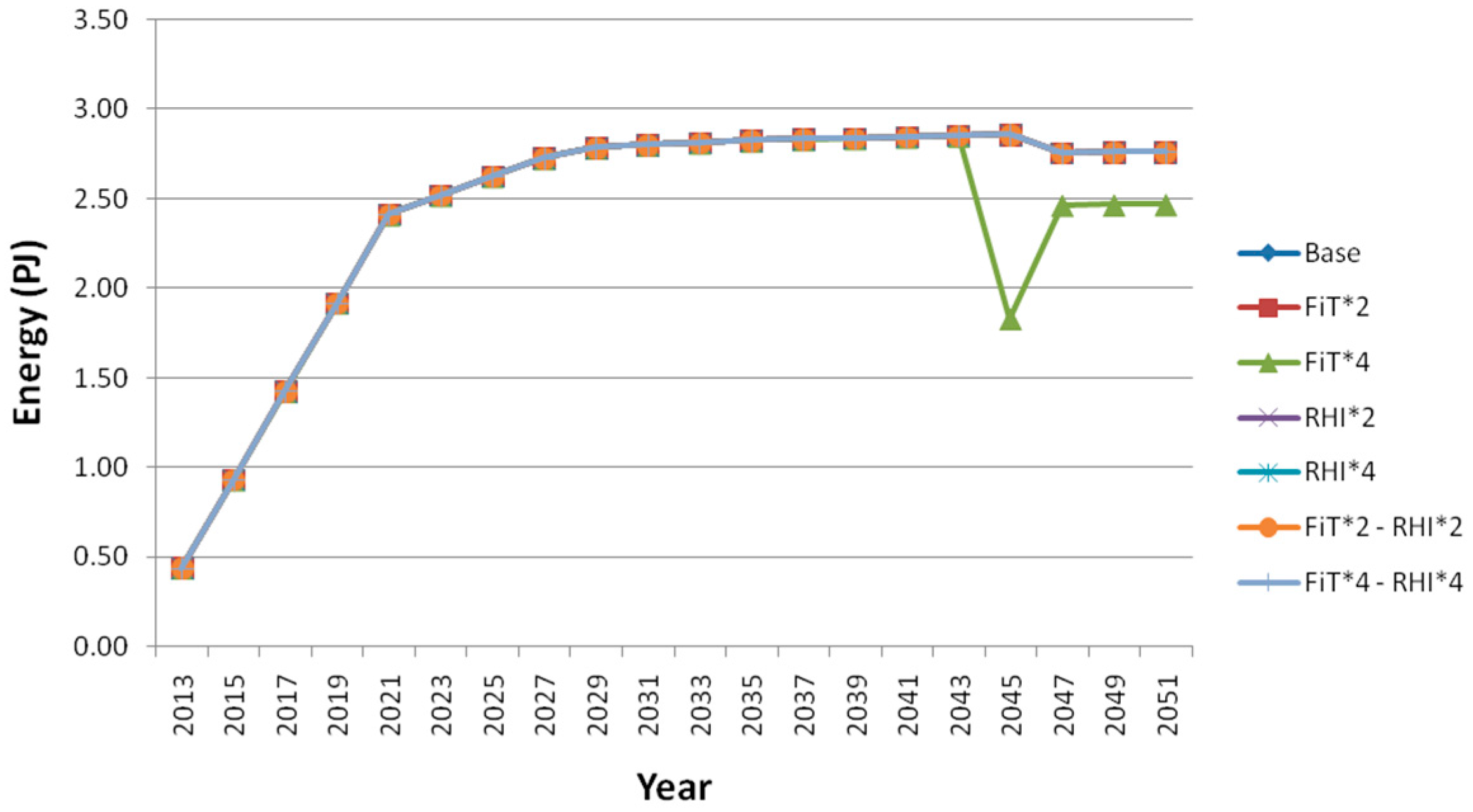

Poultry farms were found to be more prone to adopting biogas for generating electricity from CHP instead of heat from biogas boilers. Grid electricity demand is seen to reduce to its lowest in 2021, displaced by electricity from CHP, whilst heat demand is satisfied through combinations of biogas boilers and heat generated from CHP. The only exceptions occur at high RHI rates where investments in biogas boilers are more prominent up to 2037, enabling farms to maximise on returns from RHI. Ultimately, however, all FiT and RHI rates favour investments in CHP technology mainly because of the disparity in energy generation potential from biogas (due to high energy content in poultry litter) and the energy demand of farms, and hence the high potential of poultry farms to benefit from the RHI and FiT schemes.

In general, high electricity prices will promote the use of CHP in farms but the degree of adoption will vary depending on the farm type. Farms with high electricity/heat ratio will more easily implement such technologies, whilst other farms may need higher incentives. However, as shown in the cases of pig, poultry, LFA and dairy farms, increasing the FiT rate to high level may lead to the maximisation of generation and export of electricity to the grid, and re-purchasing grid electricity at a relatively cheaper price. The RHI scheme is seen to mainly influence and enhance the competitiveness of biogas boilers, which are already a cheaper investment and operates a higher heat-generating efficiency than CHP technologies. The model generally portrays that the RHI is the main driver behind the adoption of AD in farms and the use of the generated biogas for the production of heat in biogas boilers. In many cases, the heat generation potential is higher than the heat demand of the farm and because of the attractiveness of the incentive; more heat can be generated than is needed. With the unavailability of opportunities to export either heat or biomethane to the grid due to the remote nature of UK farms, the excess heat is wasted and this represents a drawback of the current RHI policy, particularly for farms where the embedded AD feedstock energy may well exceed the energy requirements of the farms, resulting in incentive payments for wasted heat.

5. Conclusions and Policy Implications

The results of this study show that the impact of different rates of the RHI and FiT schemes on different farm types can vary according to the electricity/heat use ratio and the energy content of the feedstock. The analysis showed that for all cases investigated, the adoption of AD can generally be economically attractive to farms. The different rates of the schemes do not consequentially influence the generation of biogas directly, but rather impacts on the competitiveness between the adoption of CHP units and biogas boilers to generate useful energy from the produced biogas. Pig farms which have high electricity/heat ratios will tend to more easily adopt CHP technologies which generate both electricity and heat, whilst other farms will be more inclined towards implementing a mix of technologies, from which biogas boilers will predominate. Although the FiT rates are currently relatively higher per unit energy generated than the RHI, the RHI scheme will generally be more attractive for most farms during the period when the incentives are paying returns. This is due to the cheaper capital and operating costs, as well as the higher heat generation efficiency of boilers compared to CHP, which makes boilers a more cost-competitive technology.

As expected, increasing the FiT rate favours the implementation of CHP units, but excessively high values of four times the current rate may lead to farmers to instead export the generated electricity and re-purchase cheaper electricity from the grid. The higher projected BEIS (former DECC) electricity price will also favour CHP. Increasing the RHI rate simply promotes an already cheap and effective biogas boiler, and is likely to increase heat wastage due to the non-possibility of heat/biomethane export to the grid. Furthermore, even though the schemes are set to end for new applications in 2021, the inertia of their residual effects will be felt until 2041, the end of the tariffs’ lifetime. The type and capacity of technology installed prior to 2021 will likely influence later re-investments by farms between the periods of 2041 and 2050, and therefore impact the energy mix in 2050.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}