Chronotype, Risk and Time Preferences, and Financial Behaviour

Abstract

:1. Introduction

2. Literature Review

2.1. Overview of Theoretical Rationale

2.2. Conceptual Model and Hypotheses Development

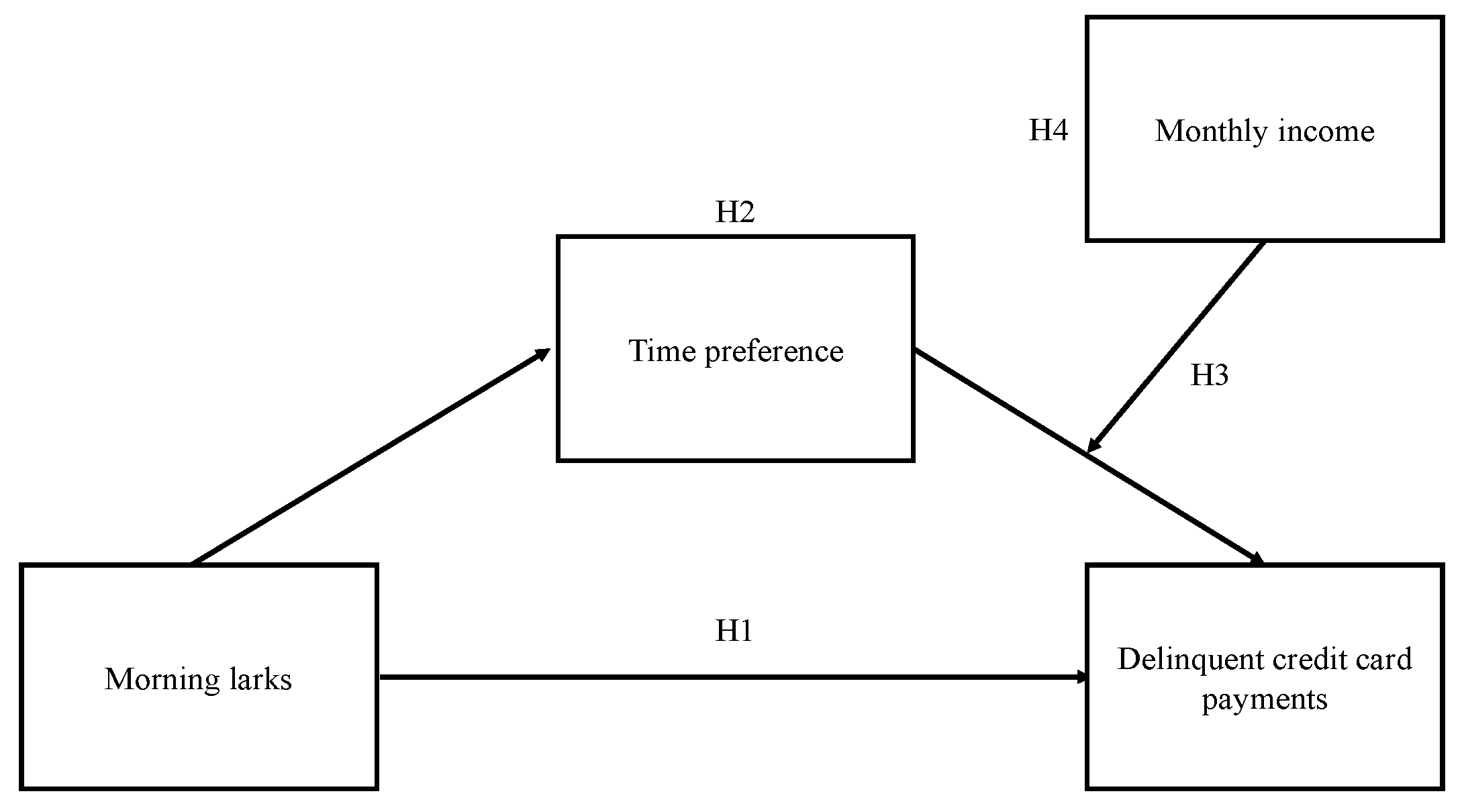

2.2.1. Morning Larks and Delinquent Credit Card Payments (H1)

2.2.2. The Mediating Role of Time Preferences (H2)

2.2.3. The Moderating Role of Monthly Income in a Second-Stage Moderated Mediation Model (H3 and H4)

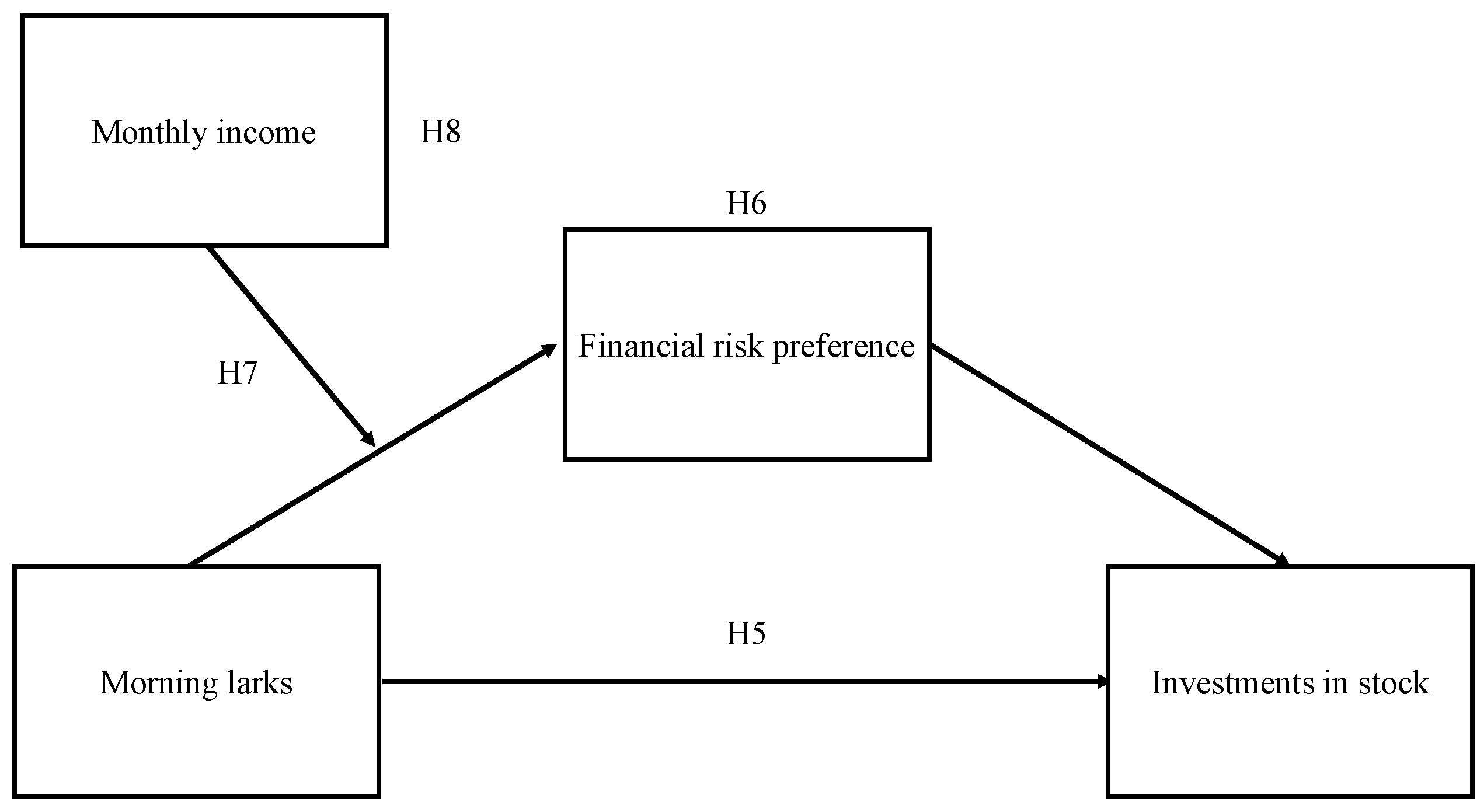

2.2.4. Morning Larks and Owning Equity (H5)

2.2.5. The Mediating Role of Financial Risk Preference (H6)

2.2.6. The Moderating Role of Monthly Income in a First-Stage Moderated Mediation Model (H7 and H8)

3. Methods

3.1. Sampling and Data Validation

3.2. Measures

3.3. Data Description

3.4. Econometrics Model

4. Results

4.1. Direct Effect of Morning Chronotype on the Likelihood of Having Revolving Credit Card Debt (H1)

4.2. The Mediating Role of Time Perspective (H2)

4.3. The Moderating Role of Income on the Indirect Effect of Morningness on Delinquent Credit Card Payments (H3 and H4)

4.4. The Direct Effect of Morningness on the Likelihood of Investments in Stock (H5)

4.5. The Mediating Role of Financial Risk Preference (H6)

4.6. The Moderating Role of Income on the Indirect Effect of Morningness on Stock Market Participation (H7 and H8)

4.7. Robustness Check

5. Discussion

5.1. Theoretical Implications

5.2. Practical Implications

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

- ○

- Yes, I am willing to joining this survey.

- ○

- No, I do not want to join

- 5:00–6:30 a.m. (5)

- 6:30–7:45 a.m. (4)

- 7:45–9:45 a.m. (3)

- 9:45–11:00 a.m. (2)

- 11:00 a.m.–12:00 (noon) (1)

- 8:00–9:00 p.m. (5)

- 9:00–10:15 p.m. (4)

- 10:15 p.m.–12:30 a.m. (3)

- 12:30–1:45 a.m. (2)

- 1:45–3:00 a.m. (1)

- Not at all easy (1)

- Slightly easy (2)

- Fairly easy (3)

- Very easy (4)

- Not at all alert (1)

- Slightly alert (2)

- Fairly alert (3)

- Very alert (4)

- Very tired (1)

- Fairly tired (2)

- Fairly refreshed (3)

- Very refreshed (4)

- Would be in good form (4)

- Would be in reasonable form (3)

- Would find it difficult (2)

- Would find it very difficult (1)

- 8:00–9:00 p.m. (5)

- 9:00–10:15 p.m. (4)

- 10:15 p.m.–12:30 a.m. (3)

- 12:30–1:45 a.m. (2)

- 1:45–3:00 a.m. (1)

- 8:00–10:00 a.m. (4)

- 11:00 a.m.–l:00 p.m. (3)

- 3:00–5:00 p.m. (2)

- 7:00–9:00 p.m. (1)

- Definitely a morning type (4)

- More a morning than an evening type (3)

- More an evening than a morning type (2)

- Definitely an evening type (1)

- Before 6:30 a.m. (4)

- 6:30–7:30 a.m. (3)

- 7:30–8:30 a.m. (2)

- 8:30 a.m. or later (1)

- Very difficult and unpleasant (1)

- Rather difficult and unpleasant (2)

- A little unpleasant but no great problem (3)

- Easy and not unpleasant (4)

- 0–10 min (4)

- 11–20 min (3)

- 21–40 min (2)

- More than 40 min (1)

- Pronounced morning active (morning alert and evening tired) (4)

- To some extent, morning active (3)

- To some extent, evening active (2)

- Pronounced evening active (morning tired and evening alert) (1)

- 18–29 (1)

- 30–44 (2)

- 45–54 (3)

- Female (0)

- Male (1)

- Others (0)

- Married (1)

- Less than High School (1)

- High school graduate (2)

- Some college (3)

- Bachelor degree (4)

- Master degree (5)

- PhD (6)

- Less than RMB3000 (1)

- RMB3000 to RMB5000 (2)

- RMB5000 to RMB7500 (3)

- RMB7500 to RMB10,000 (4)

- RMB10,000 to RMB20,000 (5)

- More than RMB20,000 (6)

- Strongly disagree (1)

- Disagree (2)

- Somewhat disagree (3)

- Neither agree nor disagree (4)

- Somewhat agree (5)

- Agree (6)

- Strongly agree (7)

- No (0)

- Yes (1)

- 0

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 0

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- I do not use credit cards for payments (0)

- Always pays off monthly (1)

- Generally pays off monthly (2)

- Occasionally pays off monthly (3)

- Seldom pays off, but tries to pay down (4)

- Generally pays minimum each month (5)

- Never (1)

- Sometimes (2)

- About half the time (3)

- Most of the time (4)

- Always (5)

- Never (5)

- Sometimes (4)

- About half the time (3)

- Most of the time (2)

- Always (1)

- Never (5)

- Sometimes (4)

- About half the time (3)

- Most of the time (2)

- Always (1)

- Never (1)

- Sometimes (2)

- About half the time (3)

- Most of the time (4)

- Always (5)

- Never (1)

- Sometimes (2)

- About half the time (3)

- Most of the time (4)

- Always (5)

- Never (5)

- Sometimes (4)

- About half the time (3)

- Most of the time (2)

- Always (1)

- Never (1)

- Sometimes (2)

- About half the time (3)

- Most of the time (4)

- Always (5)

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Dependent Variable: Delinquent Credit Card Payment | Logistic Regression | |||

|---|---|---|---|---|

| Variables | Average Marginal Effect | SE | z-Statistic | p-Value |

| Main variables | ||||

| Circadian rhythm | −0.012 *** | 0.003 | −3.47 | 0.001 |

| Control variables | ||||

| Age | 0.005 | 0.048 | 0.10 | 0.922 |

| Male | −0.030 | 0.048 | −0.63 | 0.530 |

| Married | 0.046 | 0.054 | 0.85 | 0.394 |

| Education | −0.026 | 0.044 | −0.58 | 0.565 |

| Monthly income | 0.019 | 0.024 | 0.80 | 0.425 |

| Time preference | −0.018 ** | 0.008 | −2.15 | 0.032 |

| General risk preference | 0.021 | 0.014 | 1.51 | 0.132 |

| Log pseudolikelihood | −278.827 | |||

| Pseudo R2 | 0.045 | |||

| Number of observations | 455 | |||

| Time Preference | Delinquent Credit Card Payments | |||||

|---|---|---|---|---|---|---|

| Variables | Coefficient | SE | t | Coefficient | SE | z |

| Constant | 15.630 *** | 1.522 | 10.271 | 2.716 | 1.165 | 2.331 |

| Circadian rhythm | 0.126 *** | 0.024 | 5.274 | −0.055 *** | 0.017 | −3.283 |

| Age | 0.632 ** | 0.272 | 2.325 | 0.023 | 0.222 | 0.100 |

| Male | −1.030 *** | 0.279 | −3.693 | −0.141 | 0.222 | −0.637 |

| Married | −0.381 | 0.334 | −1.141 | 0.218 | 0.257 | 0.848 |

| Education | 0.968 *** | 0.309 | 3.130 | −0.121 | 0.199 | −0.605 |

| Monthly income | −0.130 | 0.166 | −0.788 | 0.089 | 0.106 | 0.838 |

| General risk preference | 0.183 | 0.088 | 2.080 | 0.101 | 0.065 | 1.551 |

| Time preference | −0.085 ** | 0.038 | −2.239 | |||

| R2 | 0.168 | |||||

| Pseudo R2 | 0.045 | |||||

| Number of observations | 455 | 455 | ||||

| Mediator Time preference | Bootstrapping effect | Boot SE | 95% CI (LL, UL) | |||

| Indirect effect | −0.107 | 0.006 | −0.023 | −0.001 | ||

| Time Preference | Delinquent Credit Card Payments | |||||

|---|---|---|---|---|---|---|

| Variables | Coefficient | SE | t | Coefficient | SE | z |

| Constant | −9.431 *** | 1.509 | −6.251 | 0.687 *** | 1.151 | 0.597 |

| Age | 0.600 ** | 0.277 | 2.168 | 0.092 | 0.225 | 0.407 |

| Male | −1.053 *** | 0.281 | −3.747 | −0168 | 0.223 | −0.756 |

| Married | −0.429 | 0.326 | −1.317 | 0.186 | 0.260 | 0.716 |

| Education | 0.881 *** | 0.276 | 3.195 | −0.127 | 0.200 | −0.633 |

| Circadian rhythm | 0.127 *** | 0.024 | 5.316 | −0.057 *** | 0.017 | −3.372 |

| General financial preference | 0.165 * | 0.087 | 1.893 | 0.126 * | 0.067 | 1.899 |

| Monthly income | 0.120 | 0.107 | 1.124 | |||

| Time preference | −0.107 *** | 0.040 | −2.713 | |||

| Monthly income × Time preference | 0.065 ** | 0.028 | 2.343 | |||

| R2 | 0.166 | |||||

| Pseudo R2 | 0.054 | |||||

| Number of observations | 455 | 455 | ||||

| Moderator: Monthly income | Bootstrapping indirect effect | Boot SE | 95% CI (LL, UL) | |||

| Low (−1 SD from mean) | −0.023 | 0.009 | −0.043 | −0.008 | ||

| Average (0 SD from mean) | −0.014 | 0.006 | −0.027 | −0.004 | ||

| High (+1 SD from mean) | −0.005 | 0.006 | −0.017 | 0.007 | ||

| Index of moderated mediation | ||||||

| Mediator | Index | Boot SE | 95% CI (LL, UL) | |||

| Time preference | 0.008 | 0.004 | 0.001 | 0.018 | ||

| General Risk Preference | Stock Market Participation | |||||

|---|---|---|---|---|---|---|

| Variables | Coefficient | SE | t | Coefficient | SE | z |

| Constant | 4.534 *** | 0.924 | 4.907 | −5.454 *** | 1.293 | −4.218 |

| Circadian rhythm | 0.026 * | 0.013 | 1.959 | 0.007 | 0.018 | 0.382 |

| Age | −0.244 | 0.171 | −1.426 | 0.112 | 0.238 | 0.472 |

| Male | 0.732 *** | 0.166 | 4.412 | 0.524 ** | 0.239 | 2.196 |

| Married | 0.082 | 0.201 | 0.410 | 0.511 ** | 0.260 | 1.964 |

| Education | −0.213 | 0.144 | −1.481 | 0.659 *** | 0.218 | 3.030 |

| Monthly income | 0.389 *** | 0.085 | 4.608 | 0.072 | 0.111 | 0.646 |

| Time preference | 0.066 ** | 0.031 | 2.098 | −0.020 | 0.041 | −0.497 |

| General risk preference | 0.380 *** | 0.068 | 5.601 | |||

| R2 | 0.126 | |||||

| Pseudo R2 | 0.125 | |||||

| Number of observations | 455 | 455 | ||||

| Mediator General risk preference | Bootstrapping effect | Boot SE | 95% CI (LL, UL) | |||

| Indirect effect | 0.010 | 0.006 | 0.0002 | 0.022 | ||

References

- Piffer, D.; Ponzi, D.; Sapienza, P.; Zingales, L.; Maestripieri, D. Morningness–eveningness and intelligence among high-achieving US students: Night owls have higher GMAT scores than early morning types in a top-ranked MBA program. Intelligence 2014, 47, 107–112. [Google Scholar] [CrossRef]

- Nelson, R.J. An Introduction to Behavioral Endocrinology, 4th ed.; Sinauer: Sunderland, MA, USA, 2011. [Google Scholar]

- Andretic, R.; Franken, P.; Tafti, M. Genetics of sleep. Annu. Rev. Genet. 2008, 42, 361–388. [Google Scholar] [CrossRef] [PubMed]

- Baehr, E.K.; Revelle, W.; Eastman, C.I. Individual differences in the phase and amplitude of the human circadian temperature rhythm: With an emphasis on morningness–eveningness. J. Sleep Res. 2000, 9, 117–127. [Google Scholar] [CrossRef] [PubMed]

- Kerkhof, G.A.; Van Dongen, H.P. Morning-type and evening-type individuals differ in the phase position of their endogenous circadian oscillator. Neurosci. Lett. 1996, 218, 153–156. [Google Scholar] [CrossRef]

- Franken, P.; Dijk, D.J. Circadian clock genes and sleep homeostasis. Eur. J. Neurosci. 2009, 29, 1820–1829. [Google Scholar] [CrossRef] [PubMed]

- Natale, V.; Cicogna, P. Morningness-eveningness dimension: Is it really a continuum? Personal. Individ. Differ. 2002, 32, 809–816. [Google Scholar] [CrossRef]

- Horne, J.A.; Ostberg, O. A self-assessment questionnaire to determine morningness-eveningness in human circadian rhythms. Int. J. Chronobiol. 1976, 4, 97–110. [Google Scholar] [PubMed]

- McLaughlin, C.; Bowman, M.L.; Bradley, C.L.; Mistlberger, R.E. A Prospective Study of Seasonal Variation in Shift-Work Tolerance. Chronobiol. Int. 2008, 25, 455–470. [Google Scholar] [CrossRef] [PubMed]

- Waterhouse, J.; Edwards, B.; Nevill, A.; Carvalho, S.; Atkinson, G.; Buckley, P.; Ramsay, R. Identifying some determinants of “jet lag” and its symptoms: A study of athletes and other travellers. Br. J. Sports Med. 2002, 36, 54–60. [Google Scholar] [CrossRef] [PubMed]

- Flower, D.J.; Irvine, D.; Folkard, S. Perception and predictability of travel fatigue after long-haul flights: A retrospective study. Aviat. Space Environ. Med. 2003, 74, 173–179. [Google Scholar] [PubMed]

- Colquhoun, W.P. Circadian variations in mental efficiency. In Biological Rhythms and Human Performance; Academic Press: London, UK, 1971; pp. 39–107. [Google Scholar]

- Sternberg, R.J.; Zhang, L.F. Perspectives on Thinking, Learning, and Cognitive Styles; Routledge: New York, NY, USA, 2014. [Google Scholar]

- Antúnez, J.M.; Navarro, J.F.; Adan, A. Morningness–eveningness and personality characteristics of young healthy adults. Personal. Individ. Differ. 2014, 68, 136–142. [Google Scholar] [CrossRef]

- Martin, J.S.; Hébert, M.; Ledoux, É.; Gaudreault, M.; Laberge, L. Relationship of chronotype to sleep, light exposure, and work-related fatigue in student workers. Chronobiol. Int. 2012, 29, 295–304. [Google Scholar] [CrossRef] [PubMed]

- Levandovski, R.; Dantas, G.; Fernandes, L.C.; Caumo, W.; Torres, I.; Roenneberg, T.; Allebrandt, K.V. Depression scores associate with chronotype and social jetlag in a rural population. Chronobiol. Int. 2011, 28, 771–778. [Google Scholar] [CrossRef] [PubMed]

- Achilles, G.M. Individual differences in Morningness–eveningness and patterns of psychological functioning, social adaptation and family stress. Diss. Abstr. Int. Sect. B Sci. Eng. 2003, 64, 2954. [Google Scholar]

- Kruger, P.S. Wellbeing—The five essential elements. Appl. Res. Qual. Life 2011, 6, 325–328. [Google Scholar] [CrossRef]

- Kim, H.; DeVaney, S.A. The determinants of outstanding balances among credit card revolvers. J. Financ. Couns. Plan. 2001, 12, 67–78. [Google Scholar]

- Elliehausen, G.; Christopher, L.E.; Staten, M.E. The impact of credit counseling on subsequent borrower behaviour. J. Consum. Aff. 2007, 41, 1–28. [Google Scholar] [CrossRef]

- Almenberg, J.; Dreber, A. Gender, stock market participation and financial literacy. Econ. Lett. 2015, 137, 140–142. [Google Scholar] [CrossRef]

- Díaz-Morales, J.F.; Sánchez-Lopez, M.P. Morningness-eveningness and anxiety among adults: A matter of sex/gender? Personal. Individ. Differ. 2008, 44, 1391–1401. [Google Scholar] [CrossRef]

- Stolarski, M.; Ledzińska, M.; Matthews, G. Morning is tomorrow, evening is today: Relationships between chronotype and time perspective. Boil. Rhythm. Res. 2013, 44, 181–196. [Google Scholar] [CrossRef]

- Meier, S.; Sprenger, C. Present-biased preferences and credit card borrowing. Am. Econ. J. Appl. Econ. 2010, 2, 193–210. [Google Scholar] [CrossRef]

- Wang, L.; Chartrand, T.L. Morningness–eveningness and risk taking. J. Psychol. 2015, 149, 394–411. [Google Scholar] [CrossRef] [PubMed]

- Dohmen, T.; Falk, A.; Huffman, D.; Sunde, U.; Schupp, J.; Wagner, G.G. Individual risk attitudes: Measurement, determinants, and behavioral consequences. J. Eur. Econ. Assoc. 2011, 9, 522–550. [Google Scholar] [CrossRef]

- Calem, P.S.; Mester, L.J. Consumer behavior and the stickiness of credit card interest rates. Am. Econ. Rev. 1995, 85, 1327–1336. [Google Scholar]

- Tanaka, T.; Camerer, C.F.; Nguyen, Q. Risk and Time Preferences: Linking Experimental and Household Survey Data from Vietnam. Am. Econ. Rev. 2010, 100, 557–571. [Google Scholar] [CrossRef] [Green Version]

- Smith, C.S.; Reilly, C.; Midkiff, K. Evaluation of three circadian rhythm questionnaires with suggestions for an improved measure of morningness. J. Appl. Psychol. 1989, 74, 728–738. [Google Scholar] [CrossRef] [PubMed]

- Finke, M.S.; Huston, S.J. Time preference and the importance of saving for retirement. J. Econ. Behav. Organ. 2013, 89, 23–34. [Google Scholar] [CrossRef]

- Cavallera, G.M.; Giudici, S. Morningness and eveningness personality: A survey in literature from 1995 up till 2006. Personal. Individ. Differ. 2008, 44, 3–21. [Google Scholar] [CrossRef]

- Adan, A.; Archer, S.N.; Hidalgo, M.P.; Di Milia, L.; Natale, V.; Randler, C. Circadian typology: A comprehensive review. Chronobiol. Int. 2012, 29, 1153–1175. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Randler, C. Proactive people are morning people. J. Appl. Soc. Psychol. 2009, 39, 2787–2797. [Google Scholar] [CrossRef]

- Torsvall, L.; Åkerstedt, T. A diurnal type scale: Construction, consistency and validation in shift work. Scand. J. Work Environ. Health 1980, 6, 283–290. [Google Scholar] [CrossRef] [PubMed]

- Randler, C.; Díaz-Morales, J.F.; Rahafar, A.; Vollmer, C. Morningness–eveningness and amplitude–development and validation of an improved composite scale to measure circadian preference and stability (MESSi). Chronobiol. Int. 2016, 33, 832–848. [Google Scholar] [CrossRef] [PubMed]

- Faßl, C.; Quante, M.; Mariani, S.; Randler, C. Preliminary findings for the validity of the Morningness–Eveningness-Stability Scale improved (MESSi): Correlations with activity levels and personality. Chronobiol. Int. 2018, 1–8. [Google Scholar] [CrossRef] [PubMed]

- Kim, S.J.; Lee, Y.J.; Kim, H.; Cho, I.H.; Lee, J.Y.; Cho, S.J. Age as a moderator of the association between depressive symptoms and morningness–eveningness. J. Psychosom. Res. 2010, 68, 159–164. [Google Scholar] [CrossRef] [PubMed]

- Merikanto, I.; Kronholm, E.; Peltonen, M.; Laatikainen, T.; Lahti, T.; Partonen, T. Relation of chronotype to sleep complaints in the general Finnish population. Chronobiol. Int. 2010, 29, 311–317. [Google Scholar] [CrossRef] [PubMed]

- Adan, A.; Natale, V. Gender differences in morningness–eveningness preference. Chronobiol. Int. 2002, 19, 709–720. [Google Scholar] [CrossRef] [PubMed]

- Mongrain, V.; Paquet, J.; Dumont, M. Contribution of the photoperiod at birth to the association between season of birth and diurnal preference. Neurosci. Lett. 2006, 406, 113–116. [Google Scholar] [CrossRef] [PubMed]

- Natale, V.; Di Milia, L. Season of birth and morningness: Comparison between the northern and southern hemispheres. Chronobiol. Int. 2011, 28, 727–730. [Google Scholar] [CrossRef] [PubMed]

- Duffy, J.F.; Dijk, D.J.; Hall, E.F.; Czeisler, C.A. Relationship of endogenous circadian melatonin and temperature rhythms to self-reported preference for morning or evening activity in young and older people. J. Investig. Med. 1999, 47, 141–150. [Google Scholar] [PubMed]

- Katzenberg, D.; Young, T.; Finn, L.; Lin, L.; King, D.P.; Takahashi, J.S. A CLOCK polymorphism associated with human diurnal preference. Sleep 1998, 21, 569–576. [Google Scholar] [CrossRef] [PubMed]

- Sõõru, E.; Hein, H.; Hazak, A. Why force owls to start work early? The work schedules of R&D employees and sleep. TTU Econ. Res. Ser. 2017. Available online: www.tutecon.eu/index.php/TUTECON/article/download/25/14 (accessed on 10 October 2018).

- Carvalho, F.G.; de Souza, C.M.; Hidalgo, M.P.L. Work routines moderate the association between eveningness and poor psychological well-being. PLoS ONE 2018, 13, e0195078. [Google Scholar] [CrossRef] [PubMed]

- Roberts, R.D.; Kyllonen, P.C. Morningness–eveningness and intelligence: Early to bed, early to rise will likely make you anything but wise! Personal. Individ. Differ. 1999, 27, 1123–1133. [Google Scholar] [CrossRef]

- Natale, V.; Lorenzetti, R. Influences on Morningness–eveningness and time of day on narrative comprehension. Personal. Individ. Differ. 1997, 23, 685–690. [Google Scholar] [CrossRef]

- Di Milia, L.; Muller, H. Does impression management impact the relationship between morningness–eveningness and self-rated sleepiness? Personal. Individ. Differ. 2012, 52, 702–706. [Google Scholar] [CrossRef]

- Tankova, I.; Adan, A.; Buela-Casals, G. Circadian typology and individual differences. A review. Personal. Individ. Differ. 1994, 16, 671–684. [Google Scholar] [CrossRef]

- Garman, E.T.; Forgue, R.E. Personal Finance, 12th ed.; Houghton Mifflin Company: Boston, NY, USA, 2012. [Google Scholar]

- Hong, H.; Kubik, J.D.; Stein, J.C. Social interaction and stock-market participation. J. Financ. 2004, 59, 137–163. [Google Scholar] [CrossRef]

- Guiso, L.; Jappelli, T. Awareness and stock market participation. Rev. Financ. 2005, 9, 537–567. [Google Scholar] [CrossRef]

- Van Rooij, M.C.; Lusardi, A.; Alessie, R.J. Financial literacy and stock market participation. J. Financ. Econ. 2011, 101, 449–472. [Google Scholar] [CrossRef] [Green Version]

- Grinblatt, M.; Keloharju, M.; Linnainmaa, J. IQ and stock market participation. J. Financ. 2011, 66, 2121–2164. [Google Scholar] [CrossRef]

- Rosen, H.S.; Wu, S. Portfolio choice and health status. J. Financ. Econ. 2004, 72, 457–484. [Google Scholar] [CrossRef] [Green Version]

- Bogan, V.L.; Fertig, A.R. Portfolio choice and mental health. Rev. Financ. 2013, 17, 955–992. [Google Scholar] [CrossRef]

- Bogan, V. Stock market participation and the internet. J. Financ. Quant. Anal. 2008, 43, 191–211. [Google Scholar] [CrossRef]

- Kirby, E.G.; Kirby, S.L. Improving task performance: The relationship between morningness and proactive thinking. J. Appl. Soc. Psychol. 2006, 36, 2715–2729. [Google Scholar] [CrossRef]

- Parker, S.K.; Williams, H.M.; Turner, N. Modeling the antecedents of proactive behavior at work. J. Appl. Psychol. 2006, 91, 636–652. [Google Scholar] [CrossRef] [PubMed]

- Seibert, S.E.; Crant, J.M.; Kraimer, M.L. Proactive personality and career success. J. Appl. Psychol. 1999, 84, 416–427. [Google Scholar] [CrossRef] [PubMed]

- Kirby, E.G.; Kirby, S.L.; Lewis, M.A. A study of the effectiveness of training proactive thinking. J. Appl. Soc. Psychol. 2002, 32, 1538–1549. [Google Scholar] [CrossRef]

- Aspinwall, L.G.; Hill, D.L.; Leaf, S.L. Prospects, pitfalls, and plans: A proactive perspective on social comparison activity. Eur. Rev. Soc. Psychol. 2002, 12, 267–298. [Google Scholar] [CrossRef]

- Aspinwall, L.G.; Sechrist, G.B.; Jones, P.R. Expect the best and prepare for the worst: Anticipatory coping and preparations for Y2K. Motiv. Emot. 2005, 29, 353–384. [Google Scholar] [CrossRef]

- Hazembuller, A.; Lombardi, B.J.; Hogarth, J.M. Unlocking the risk-based pricing puzzle: Five keys to cutting credit card costs. Consum. Interests Annu. 2007, 53, 73–84. [Google Scholar]

- Milfont, T.L.; Schwarzenthal, M. Explaining why larks are future-oriented and owls are present-oriented: Self-control mediates the chronotype–time perspective relationships. Chronobiol. Int. 2014, 31, 581–588. [Google Scholar] [CrossRef] [PubMed]

- Benedetti, F.; Barbini, B.; Colombo, C.; Smeraldi, E. Chronotherapeutics in a psychiatric ward. Sleep Med. Rev. 2007, 11, 509–522. [Google Scholar] [CrossRef] [PubMed]

- Fudenburg, D.; Levine, D.K. A dual-self model of impulse control. Am. Econ. Rev. 2006, 96, 1449–1476. [Google Scholar] [CrossRef] [Green Version]

- Ando, A.; Modigliani, F. The ‘life cycle’ hypothesis of saving: Aggregate implication and tests. Am. Econ. Rev. 1963, 53, 55–84. [Google Scholar]

- Bryant, W.K. The Economic Organization of the Households; Cambridge University Press: Cambridge, UK, 1990. [Google Scholar]

- Vissing-Jorgensen, A. Towards an Explanation of Household Portfolio Choice Heterogeneity: Nonfinancial Income and Participation Cost Structures; National Bureau of Economic Research: Cambridge, MA, USA, 2002. [Google Scholar]

- Bayer, P.J.; Bernheim, B.D.; Scholz, J.K. The effects of financial education in the workplace: Evidence from a survey of employers. Econ. Inq. 2009, 47, 605–624. [Google Scholar] [CrossRef]

- Guiso, L.; Jappelli, T.; Terlizzese, D. Income risk, borrowing constraints, and portfolio choice. Am. Econ. Rev. 1996, 86, 158–172. [Google Scholar]

- Heaton, J.; Lucas, D. Portfolio choice and asset prices: The importance of entrepreneurial risk. J. Financ. 2000, 55, 1163–1198. [Google Scholar] [CrossRef]

- Guiso, L.; Sapienza, P.; Zingales, L. Trusting the stock market. J. Financ. 2008, 63, 2557–2600. [Google Scholar] [CrossRef]

- Grinblatt, M.; Keloharju, M. How distance, language, and culture influence stockholdings and trades. J. Financ. 2001, 56, 1053–1073. [Google Scholar] [CrossRef]

- Rao, Y.; Mei, L.; Zhu, R. Happiness and stock-market participation: Empirical evidence from China. J. Happiness Stud. 2016, 17, 271–293. [Google Scholar] [CrossRef]

- Biss, R.K.; Hasher, L. Happy as a lark: Morning-type younger and older adults are higher in positive affect. Emotion 2012, 12, 437–441. [Google Scholar] [CrossRef] [PubMed]

- Guven, C.; Hoxha, I. Rain or shine: Happiness and risk-taking. Q. Rev. Econ. Financ. 2015, 57, 1–10. [Google Scholar] [CrossRef]

- Anderson, C.; Galinsky, A.D. Power, optimism, and risk-taking. Eur. J. Soc. Psychol. 2006, 36, 511–536. [Google Scholar] [CrossRef]

- Yuen, K.S.; Lee, T.M. Could mood state affect risk-taking decisions? J. Affect. Disord. 2003, 75, 11–18. [Google Scholar] [CrossRef] [Green Version]

- Edwards, P.J.; Roberts, I.G.; Clarke, M.J. Methods to increase response rates to postal questionnaires. Cochrane Database Syst. Rev. 2009, MR000008. [Google Scholar] [CrossRef] [Green Version]

- Wjx Home Page. Available online: http://www.wjx.cn (accessed on 1 August 2017).

- Johnson, J.S. Improving online panel data usage in sales research. J. Pers. Sell. Sales Manag. 2016, 36, 74–85. [Google Scholar] [CrossRef]

- Hays, R.D.; Liu, H.; Kapteyn, A. Use of Internet panels to conduct surveys. Behav. Res. Methods 2015, 47, 685–690. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Chen, D.; Cheng, C.Y.; Urpelainen, J. Support for renewable energy in China: A survey experiment with internet users. J. Clean. Prod. 2016, 112, 3750–3758. [Google Scholar] [CrossRef]

- Liu, X.; Song, Y.; Wu, K.; Wang, J.; Li, D.; Long, Y. Understanding urban China with open data. Cities 2015, 47, 53–61. [Google Scholar] [CrossRef] [Green Version]

- Burkill, S.; Copas, A.; Couper, M.P.; Clifton, S.; Prah, P.; Datta, J.; Erens, B. Using the web to collect data on sensitive behaviours: A study looking at mode effects on the British National Survey of Sexual Attitudes and Lifestyles. PLoS ONE 2016, 11, e0147983. [Google Scholar] [CrossRef] [PubMed]

- Kreuter, F.; Presser, S.; Tourangeau, R. Social desirability bias in CATI, IVR, and web surveys: The effects of mode and question sensitivity. Public Opin. Q. 2008, 72, 847–865. [Google Scholar] [CrossRef]

- Couper, M.P. New Developments in Survey Data Collection. Annu. Rev. Sociol. 2017, 43, 121–145. [Google Scholar] [CrossRef]

- Callegaro, M.; DiSogra, C. Computing response metrics for online panels. Public Opin. Q. 2008, 72, 1008–1032. [Google Scholar] [CrossRef]

- Biemer, P.P.; Lyberg, L.E. Introduction to Survey Quality; John Wiley & Sons: Hoboken, NJ, USA, 2003. [Google Scholar]

- Saunders, M.; Lewis, P.; Thornhill, A. Research Methods for Business Students, 6th ed.; Pearson: London, UK, 2012. [Google Scholar]

- Meterko, M.; Restuccia, J.D.; Stolzmann, K.; Mohr, D.; Brennan, C.; Glasgow, J.; Kaboli, P. Response rates, nonresponse bias, and data quality: Results from a national survey of senior healthcare leaders. Public Opin. Q. 2015, 79, 130–144. [Google Scholar] [CrossRef]

- Rindfuss, R.R.; Choe, M.K.; Tsuy, N.O.; Bumpass, L.L.; Tamaki, E. Do low survey response rates bias results? Evidence from Japan. Demogr. Res. 2015, 32, 797–828. [Google Scholar] [CrossRef] [Green Version]

- Groves, R.M.; Peytcheva, E. The impact of nonresponse rates on nonresponse bias. Public Opin. Q. 2008, 72, 167–189. [Google Scholar] [CrossRef]

- Smith, H.L. Double sample to minimize bias due to non-response in a mail survey. In Survey Methods: Applications to Longitudinal Studies, to Health, to Electoral Studies and to Studies in Developing Countries; Ruiz-Gazen, P.G.A., Haziza, D., Tille, Y., Eds.; Dunod: Paris, France, 2009; pp. 334–339. [Google Scholar]

- Visser, P.S.; Krosnick, J.A.; Marquette, J.; Curtin, M. Mail surveys for election forecasting? An evaluation of the Columbus Dispatch poll. Public Opin. Q. 1996, 60, 181–227. [Google Scholar] [CrossRef]

- Curtin, R.; Presser, S.; Singer, E. The effects of response rate changes on the index of consumer sentiment. Public Opin. Q. 2000, 64, 413–428. [Google Scholar] [CrossRef] [PubMed]

- Keeter, S.; Kennedy, C.; Dimock, M.; Best, J.; Craighill, P. Gauging the impact of growing nonresponse on estimates from a national RDD telephone survey. Public Opin. Q. 2006, 70, 759–779. [Google Scholar] [CrossRef]

- Holbrook, A.; Krosnick, J.A.; Pfent, A. The causes and consequences of response rates in surveys by the news media and government contractor survey research firms. In Advances in Telephone Survey Methodology; Lepkowski, J., Harris-Kojetin, B., Lavrakas, P.J., Tucker, C., de Leeuw, E., Link, M., Brick, M., Japec, L., Sangster, R.N., Eds.; Wiley: New York, NY, USA, 2007; pp. 499–528. [Google Scholar]

- Worldometer’s Home Page Regarding China Population (Live). 2017. Available online: http://www.worldometers.info/world-population/china-population/ (accessed on 7 December 2017).

- Statista’s Home Page Regarding Number of Internet Users in China from 2015 to 2022 (in Millions). 2017. Available online: https://www.statista.com/statistics/278417/number-of-internet-users-in-china/ (accessed on 7 December 2017).

- World Development Indicator’s Home Page Regarding Gross Enrolment Ratio, Tertiary, Both Sexes (%). 2016. Available online: https://data.worldbank.org/indicator/SE.TER.ENRR (accessed on 9 December 2017).

- Paz, S.H.; Spritzer, K.L.; Morales, L.S.; Hays, R.D. Evaluation of the Patient-Reported Outcomes Information System (PROMIS®) Spanish physical functioning items. Qual. Life Res. 2013, 22, 1819–1830. [Google Scholar] [CrossRef] [PubMed]

- Community Business’s Home Page Regarding China Achieving Gender Parity and Ranks Top among 6 Asian Markets. 2014. Available online: http://www.communitybusiness.org/library/News/2014/20141028_GDBA2014_PressRelease_China.pdf (accessed on 7 December 2017).

- International Monetary Fund’s Home Page Regarding World Economic Outlook Database. 2017. Available online: http://www.imf.org/external/pubs/ft/weo/2017/01/weodata/weorept.aspx?sy=2015&ey=2022&scsm=1&ssd=1&sort=country&ds=.&br=1&c=924&s=NGDPD%2CNGDPDPC%2CPPPGDP%2CPPPPC&grp=0&a=&pr.x=75&pr.y=16 (accessed on 7 December 2017).

- China Human Capital Report’s Home Page. 2016. Available online: http://humancapital.cufe.edu.cn/en/Human_Capital_Index_Project/Project_2016/China_Human_Capital_Report.htm (accessed on 7 December 2017).

- Caci, H.; Nadalet, L.; Staccini, P.; Myquel, M.; Boyer, P. Psychometric properties of the French version of the Composite Scale of Morningness in adults. Eur. Psychiatry 1999, 14, 284–290. [Google Scholar] [CrossRef]

- Adan, A.; Caci, H.; Prat, G. Reliability of the Spanish version of the Composite Scale of Morningness. Eur. Psychiatry 2005, 20, 503–509. [Google Scholar] [CrossRef] [PubMed]

- Randler, C. Psychometric properties of the German version of the Composite Scale of Morningness. Biol. Rhythm. Res. 2008, 39, 151–161. [Google Scholar] [CrossRef]

- Pornpitakpan, C. Psychometric properties of the composite scale of morningness: A shortened version. Personal. Individ. Differ. 1998, 25, 699–709. [Google Scholar] [CrossRef]

- Gau, S.F.; Soong, W.T.; Lee, W.Y.; Chiu, Y.N. Reliability and validity of the Chinese version of the morningness/eveningness scale. Taiwan J. Psychiatry 1998, 12, 98–109. [Google Scholar]

- Li, S.X.; Wang, X.F.; Liu, L.J.; Liu, Y.; Zhang, L.X.; Zhang, B.; Lu, L. Preliminary test for the Chinese version of the Morningness–Eveningness Questionnaire. Sleep Biol. Rhythm. 2011, 9, 19–23. [Google Scholar] [CrossRef]

- Cronbach, L.J. Coefficient alpha and the internal structure of tests. Psychometrika 1951, 16, 297–334. [Google Scholar] [CrossRef] [Green Version]

- Hinton, P.R.; Brownlow, C.; McMurray, I.; Cozens, B. SPSS Explained, 2nd ed.; Routledge Inc.: East Sussex, UK, 2014. [Google Scholar]

- Likert, R.A. A technique for the measurement of attitudes. Arch. Psychol. 1932, 140, 5–55. [Google Scholar]

- Lau, E.Y.Y.; Hui, C.H.; Lam, J.; Cheung, S.F. Sleep and optimism: A longitudinal study of bidirectional causal relationship and its mediating and moderating variables in a Chinese student sample. Chronobiol. Int. 2017, 34, 360–372. [Google Scholar] [CrossRef] [PubMed]

- Wong, M.L.; Zhang, J.; Wing, Y.K.; Lau, E.Y.Y. Sleep-related daytime consequences mediated the neuroticism–depression link. Sleep Biol. Rhythm. 2017, 15, 21–30. [Google Scholar] [CrossRef]

- Wong, M.L.; Lau, E.; Wan, J. The relationship between sleep quality and daytime sleepiness with chronotype latent constructs: An exploratory and confirmatory factor analysis in Chinese college students. Sleep 2012, 35, 191. [Google Scholar]

- Bi, Y.X. On the death penalty for drug-related crime in China. Hum. Rights Drugs 2012, 2, 29–44. [Google Scholar]

- Holt, C.A.; Laury, S.H. Risk Aversion and Incentive Effects. Am. Econ. Rev. 2002, 92, 1644–1655. [Google Scholar] [CrossRef] [Green Version]

- Eckel, C.C.; Grossman, P.J. Men, Women and Risk Aversion: Experimental Evidence. In Handbook of Experimental Economics Results; Plott, C., Smith, V., Eds.; Elsevier: New York, NY, USA, 2008; Volume 1, pp. 1061–1073. [Google Scholar]

- Mandell, L.; Klein, L.S. The impact of financial literacy education on subsequent financial behaviour. Financ. Couns. Plan. 2009, 20, 15–24. [Google Scholar]

- Fernandes, D.; Lynch, J.G., Jr.; Netemeyer, R.G. Financial literacy, financial education, and downstream financial behaviors. Manag. Sci. 2014, 60, 1861–1883. [Google Scholar] [CrossRef]

- Lawrance, E.C. Poverty and the rate of time preference: Evidence from panel data. J. Political Econ. 1991, 99, 54–77. [Google Scholar] [CrossRef]

- Rosen, A.B.; Tsai, J.S.; Downs, S.M. Variations in risk attitude across race, gender, and education. Med. Decis. Mak. 2003, 23, 511–517. [Google Scholar] [CrossRef] [PubMed]

- Borghans, L.; Golsteyn, B.; Heckman, J.; Meijers, H. Gender differences in risk aversion and ambiguity aversion. J. Eur. Econ. Assoc. 2009, 7, 649–658. [Google Scholar] [CrossRef]

- Bucciol, A.; Miniaci, R. Household portfolios and implicit risk preference. Rev. Econ. Stat. 2011, 93, 1235–1250. [Google Scholar] [CrossRef]

- Dittrich, M.; Leipold, K. Gender differences in time preferences. Econ. Lett. 2014, 122, 413–415. [Google Scholar] [CrossRef]

- Neter, J.; Kutner, M.H.; Nachtsheim, C.J.; Wasserman, W. Applied Linear Statistical Models, 4th ed.; McGraw-Hill: Boston, MA, USA, 2004; Volume 4, p. 318. [Google Scholar]

- Hayes, A.F. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach; Guilford Press: New York, NY, USA, 2013. [Google Scholar]

- Preacher, K.J.; Hayes, A.F. Asymptotic and resampling strategies for assessing and comparing indirect effects in multiple mediator models. Behav. Res. Methods 2008, 40, 879–891. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Aiken, L.S.; West, S.G.; Reno, R.R. Multiple Regression: Testing and Interpreting Interactions; Sage: London, UK, 1999. [Google Scholar]

- Hayes, A.F. An index and test of linear moderated mediation. Multivar. Behav. Res. 2015, 50, 1–22. [Google Scholar] [CrossRef] [PubMed]

- Chelminski, I.; Ferraro, F.R.; Petros, T.; Plaud, J.J. Horne and Ostberg questionnaire: A score distribution in a large sample of young adults. Personal. Individ. Differ. 1997, 23, 647–652. [Google Scholar] [CrossRef]

- Andreoni, J.; Sprenger, C. Risk preferences are not time preference. Am. Econ. Rev. 2012, 102, 3357–3376. [Google Scholar] [CrossRef]

- Killgore, W.D. Effects of sleep deprivation and morningness-eveningness traits on risk-taking. Psychol. Rep. 2007, 100, 613–626. [Google Scholar] [CrossRef] [PubMed]

- Maestripieri, D. Night owl women are similar to men in their relationship orientation, risk-taking propensities, and cortisol levels: Implications for the adaptive significance and evolution of eveningness. Evol. Psychol. 2014, 12, 130–147. [Google Scholar] [CrossRef] [PubMed]

- Gathergood, J. Self-control, financial literacy and consumer over-indebtedness. J. Econ. Psychol. 2012, 33, 590–602. [Google Scholar] [CrossRef]

- Randler, C.; Saliger, L. Relationship between morningness–eveningness and temperament and character dimensions in adolescents. Personal. Individ. Differ. 2011, 50, 148–152. [Google Scholar] [CrossRef]

- Randler, C. Morningness–eveningness, sleep–wake variables and big five personality factors. Personal. Individ. Differ. 2008, 45, 191–196. [Google Scholar] [CrossRef]

- Cinan, S.; Doğan, A. Working memory, mental prospection, time orientation, and cognitive insight. J. Individ. Differ. 2013, 34, 159–169. [Google Scholar] [CrossRef]

- Nowack, K.; van der Meer, E. Are larks future-oriented and owls present-oriented? Age-and sex-related shifts in chronotype–time perspective associations. Chronobiol. Int. 2013, 30, 1240–1250. [Google Scholar] [CrossRef] [PubMed]

- Fleig, D.; Randler, C. Association between chronotype and diet in adolescents based on food logs. Eat. Behav. 2009, 10, 115–118. [Google Scholar] [CrossRef] [PubMed]

- Nakade, M.; Takeuchi, H.; Kurotani, M.; Harada, T. Effects of meal habits and alcohol/cigarette consumption on morningness-eveningness preference and sleep habits by Japanese female students aged 18–29. J. Physiol. Anthropol. 2009, 28, 83–90. [Google Scholar] [CrossRef] [PubMed]

- Goldstein, D.; Hahn, C.S.; Hasher, L.; Wiprzycka, U.J.; Zelazo, P.D. Time of day, intellectual performance, and behavioral problems in Morning versus Evening type adolescents: Is there a synchrony effect? Personal. Individ. Differ. 2007, 42, 431–440. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Wittmann, M.; Paulus, M.; Roenneberg, T. Decreased psychological well-being in late ‘chronotypes’ is mediated by smoking and alcohol consumption. Subst. Use Misuse 2010, 45, 15–30. [Google Scholar] [CrossRef] [PubMed]

- Susman, E.J.; Dockray, S.; Schiefelbein, V.L.; Herwehe, S.; Heaton, J.A.; Dorn, L.D. Morningness/eveningness, morning-to-afternoon cortisol ratio, and antisocial behavior problems during puberty. Dev. Psychol. 2007, 43, 811–822. [Google Scholar] [CrossRef] [PubMed]

- Laibson, D. Golden eggs and hyperbolic discounting. Q. J. Econ. 1997, 112, 443–478. [Google Scholar] [CrossRef]

- Fehr, E. Behavioural science: The economics of impatience. Nature 2002, 415, 269–272. [Google Scholar] [CrossRef] [PubMed]

- Heidhues, P.; Koszegi, B. Exploiting naivete about self-control in the credit market. Am. Econ. Rev. 2010, 100, 2279–2303. [Google Scholar] [CrossRef]

- Hur, Y.M. Stability of genetic influence on morningnesseveningness: A cross-sectional examination of South Korean twins from preadolescence to young adulthood. J. Sleep Res. 2007, 16, 17–23. [Google Scholar] [CrossRef] [PubMed]

- Buschkens, J.; Graham, D.; Cottrell, D. Well-being under chronic stress: Is morningness an advantage? Stress Health 2010, 26, 330–340. [Google Scholar] [CrossRef]

- Roeser, K.; Obergfell, F.; Meule, A.; Vögele, C.; Schlarb, A.A.; Kübler, A. Of larks and hearts—Morningness/eveningness, heart rate variability and cardiovascular stress response at different times of day. Physiol. Behav. 2012, 106, 151–157. [Google Scholar] [CrossRef] [PubMed]

- Kandasamy, N.; Hardy, B.; Page, L.; Schaffner, M.; Graggaber, J.; Powlson, A.S.; Coates, J. Cortisol shifts financial risk preferences. Proc. Natl. Acad. Sci. USA 2014, 111, 3608–3613. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Dallman, M.F.; Bhatnagar, S. Chronic Stress and Energy Balance: Role of the Hypothalamo-Pituitary-Adrenal Axis. In Handbook of Physiology, Section 7. The Endocrine System; McEwen, B., Ed.; Oxford University Press: New York, NY, USA, 2010; pp. 179–210. [Google Scholar]

- Lupien, S.J.; Wilkinson, C.W.; Brière, S.; Ménard, C.; Kin, N.N.Y.; Nair, N.P.V. The modulatory effects of corticosteroids on cognition: Studies in young human populations. Psychoneuroendocrinology 2002, 27, 401–416. [Google Scholar] [CrossRef]

- Cueva, C.; Roberts, R.E.; Spencer, T.; Rani, N.; Tempest, M.; Tobler, P.N.; Rustichini, A. Cortisol and testosterone increase financial risk taking and may destabilize markets. Sci. Rep. 2015, 5, 1–16. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bailey, S.L.; Heitkemper, M.M. Morningness-eveningness and early-morning salivary cortisol levels. Biol. Psychol. 1991, 32, 181–192. [Google Scholar] [CrossRef]

- Kudielka, B.M.; Federenko, I.S.; Hellhammer, D.H.; Wüst, S. Morningness and eveningness: The free cortisol rise after awakening in “early birds” and “night owls”. Biol. Psychol. 2006, 72, 141–146. [Google Scholar] [CrossRef] [PubMed]

- Griefahn, B.; Robens, S. The cortisol awakening response: A pilot study on the effects of shift work, morningness and sleep duration. Psychoneuroendocrinology 2008, 33, 981–988. [Google Scholar] [CrossRef] [PubMed]

- Randle, C.; Schaal, S. Morningness–eveningness, habitual sleep-wake variables and cortisol level. Biol. Psychol. 2010, 85, 14–18. [Google Scholar] [CrossRef] [PubMed]

- Randler, C.; Ebenhöh, N.; Fischer, A.; Höchel, S.; Schroff, C.; Stoll, J.C.; Vollmer, C. Chronotype but not sleep length is related to salivary testosterone in young adult men. Psychoneuroendocrinology 2012, 37, 1740–1744. [Google Scholar] [CrossRef] [PubMed]

- Grable, J.E.; Roszkowski, M.J. The influence of mood on the willingness to take financial risks. J. Risk Res. 2008, 11, 905–923. [Google Scholar] [CrossRef]

- Kuhnen, C.M.; Knutson, B. The influence of affect on beliefs, preferences, and financial decisions. J. Financ. Quant. Anal. 2011, 46, 605–626. [Google Scholar] [CrossRef]

- Barsky, R.B.; Juster, F.T.; Kimball, M.S.; Shapiro, M.D. Preference parameters and behavioral heterogeneity: An experimental approach in the health and retirement study. Q. J. Econ. 1997, 112, 537–579. [Google Scholar] [CrossRef]

- Charness, G.; Gneezy, U.; Imas, A. Experimental methods: Eliciting risk preferences. J. Econ. Behav. Organ. 2013, 87, 43–51. [Google Scholar] [CrossRef]

- Gafni, A.; Torrance, G.W. Risk attitude and time preference in health. Manag. Sci. 1984, 30, 440–451. [Google Scholar] [CrossRef]

- Kahneman, D.; Tversky, A. Prospect theory: An analysis of decision under risk. Econ. J. Econ. Soc. 1979, 47, 263–291. [Google Scholar]

- Zimbardo, P.G.; Boyd, J.N. Putting time in perspective: A valid, reliable individual-differences metric. J. Pers. Soc. Psychol. 1999, 77, 1271–1288. [Google Scholar] [CrossRef]

- Levin, K.A. Study design III: Cross-sectional studies. Evid.-Based Dent. 2006, 7, 24–25. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Carciofo, R.; Du, F.; Song, N.; Qi, Y.; Zhang, K. Age-related chronotype differences in Chinese, and reliability assessment of a reduced version of the Chinese Morningness–Eveningness Questionnaire. Sleep Biol. Rhythm. 2012, 10, 310–318. [Google Scholar] [CrossRef]

- Kerkhof, G.A. Inter-individual differences in the human circadian system: A review. Biol. Psychol. 1985, 20, 83–112. [Google Scholar] [CrossRef]

- Caci, H.; Adan, A.; Bohle, P.; Natale, V.; Pornpitakpan, C.; Tilley, A. Transcultural properties of the composite scale of morningness: The relevance of the “morning affect” factor. Chronobiol. Int. 2005, 22, 523–540. [Google Scholar] [CrossRef] [PubMed]

| Variables | Observations | Mean | SE | Min | Max |

|---|---|---|---|---|---|

| Morningness | 455 | 0.132 | 0.339 | 0 | 1 |

| Age | 455 | 1.378 | 0.485 | 1 | 2 |

| Male | 455 | 0.389 | 0.488 | 0 | 1 |

| Married | 455 | 0.752 | 0.432 | 0 | 1 |

| Education | 455 | 3.936 | 0.558 | 1 | 6 |

| Monthly income | 455 | 3.342 | 1.105 | 1 | 6 |

| Time preference | 455 | 25.164 | 2.959 | 13 | 32 |

| Financial risk preference | 455 | 7.569 | 1.926 | 1 | 11 |

| Stock market participation | 455 | 0.657 | 0.475 | 0 | 1 |

| Delinquent credit card payments | 455 | 0.341 | 0.474 | 0 | 1 |

| Variables | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| 1. Morningness | |||||||||

| 2. Age | 0.058 | ||||||||

| 3. Male | −0.058 | −0.036 | |||||||

| 4. Married | 0.014 | 0.291 *** | −0.105 ** | ||||||

| 5. Education | 0.033 | 0.032 | 0.010 | 0.035 | |||||

| 6. Monthly income | 0.067 | 0.152 *** | 0.112 ** | 0.183 *** | 0.354 *** | ||||

| 7. Time preference | 0.262 *** | 0.104 ** | −0.167 *** | 0.020 | 0.188 *** | 0.037 | |||

| 8. Financial risk preference | 0.131 *** | 0.002 | 0.200 *** | 0.088 | 0.042 | 0.240 *** | 0.080 | ||

| 9. Stock participation | 0.104 ** | 0.048 | 0.159 *** | 0.110 ** | 0.175 *** | 0.187 *** | 0.025 | 0.303 *** | |

| 10. Delinquent credit card payments | −0.157 *** | 0.004 | 0.016 | 0.038 | −0.043 | 0.050 | −0.156 *** | 0.053 | 0.031 |

| Dependent Variable: Delinquent Credit Card Payments | Logistic Regression | |||

|---|---|---|---|---|

| Variables | Average Marginal Effect | SE | z-Statistic | p-Value |

| Main variables | ||||

| Morningness | −0.223 *** | 0.080 | −2.80 | 0.005 |

| Control variables | ||||

| Age | 0.005 | 0.048 | 0.10 | 0.917 |

| Male | −0.016 | 0.046 | −0.37 | 0.712 |

| Married | 0.028 | 0.053 | 0.53 | 0.593 |

| Education | −0.035 | 0.043 | −0.82 | 0.412 |

| Monthly income | 0.031 | 0.023 | 1.36 | 0.174 |

| Time preference | −0.019 ** | 0.008 | −2.31 | 0.021 |

| Log pseudolikelihood | −280.78662 | |||

| Pseudo R2 | 0.038 | |||

| Number of observations | 455 | |||

| Time Preference | Delinquent Credit Card Payments | |||||

|---|---|---|---|---|---|---|

| Variables | Coefficient | SE | t | Coefficient | SE | z |

| Constant | 20.912 *** | 1.051 | 19.890 | 1.684 | 1.092 | 1.543 |

| Morningness | 2.136 *** | 0.375 | 5.701 | −1.045 *** | 0.386 | −2.704 |

| Age | 0.557 ** | 0.273 | 2.039 | 0.023 | 0.221 | 0.106 |

| Male | −0.904 *** | 0.272 | −3.324 | −0.078 | 0.214 | −0.365 |

| Married | −0.169 | 0.337 | −0.500 | 0.132 | 0.253 | 0.522 |

| Education | 1.029 *** | 0.293 | 3.511 | −0.164 | 0.196 | −0.837 |

| Monthly income | −0.110 | 0.162 | −0.682 | 0.145 | 0.102 | 1.415 |

| Time preference | −0.087 ** | 0.037 | −2.367 | |||

| R2 | 0.133 | |||||

| Pseudo R2 | 0.038 | |||||

| Number of observations | 455 | 455 | ||||

| Mediator Time preference | Bootstrapping effect | Boot SE | 95% CI (LL, UL) | |||

| Indirect effect | −0.186 | 0.090 | −0.381 | −0.029 | ||

| Dependent Variables: Delinquent Credit Card Payments | Monthly Income as a Moderator in Logistic Regression | |||

|---|---|---|---|---|

| Variables | Coefficients | SD | z-Statistic | p-Value |

| Constant | −0.047 | 0.874 | −0.05 | 0.957 |

| Age | 0.084 | 0.226 | 0.37 | 0.711 |

| Male | −0.088 | 0.213 | −0.41 | 0.680 |

| Married | 0.096 | 0.253 | 0.38 | 0.704 |

| Education | −0.174 | 0.198 | −0.88 | 0.379 |

| Morningness | −1.118 *** | 0.394 | −2.84 | 0.005 |

| Monthly income | 0.190 * | 0.107 | 1.78 | 0.075 |

| Time preference | −0.106 *** | 0.038 | −2.78 | 0.005 |

| Monthly income × Time preference | 0.062 ** | 0.026 | 2.37 | 0.018 |

| Log pseudolikelihood | −278.24058 | |||

| Pseudo R2 | 0.047 | |||

| Number of observations | 455 | |||

| Time Preference | Delinquent Credit Card Payment | |||||

|---|---|---|---|---|---|---|

| Variables | Coefficient | SE | t | Coefficient | SE | z |

| Constant | −4.245 *** | 1.053 | −4.033 | −0.047 | 0.866 | −0.054 |

| Age | 0.532 * | 0.278 | 1.912 | 0.084 | 0.223 | 0.376 |

| Male | −0.936 *** | 0.274 | −3.413 | −0.088 | 0.215 | −0.410 |

| Married | −0.213 | 0.328 | −0.649 | 0.096 | 0.255 | 0.376 |

| Education | 0.954 *** | 0.262 | 3.643 | −0.174 | 0.197 | −0.884 |

| Morningness | 2.116 *** | 0.368 | 5.745 | −1.118 *** | 0.392 | −2.858 |

| Monthly income | 0.191 * | 0.105 | 1.817 | |||

| Time preference | −0.106 *** | 0.038 | −2.765 | |||

| Monthly income × Time preference | 0.062 ** | 0.028 | 2.228 | |||

| R2 | 0.131 | |||||

| Pseudo R2 | 0.047 | |||||

| Number of observations | 455 | 455 | ||||

| Moderator: Monthly income | Bootstrapping indirect effect | Boot SE | 95% CI (LL, UL) | |||

| Low (−1 SD from mean) | −0.368 | 0.138 | −0.666 | −0.139 | ||

| Average (0 SD from mean) | −0.224 | 0.094 | −0.430 | −0.062 | ||

| High (+1 SD from mean) | −0.079 | 0.097 | −0.283 | 0.104 | ||

| Index of moderated mediation | ||||||

| Mediator | Index | Boot SE | 95% CI (LL, UL) | |||

| Time preference | 0.131 | 0.067 | 0.012 | 0.270 | ||

| Dependent Variables: Stock Market Participation | Logistic Regression | |||

|---|---|---|---|---|

| Variables | Average Marginal Effect | SE | z-Statistic | p-Value |

| Main variables | ||||

| Morningness | 0.105 * | 0.063 | 1.66 | 0.098 |

| Control variables | ||||

| Age | 0.011 | 0.044 | 0.24 | 0.812 |

| Male | 0.111 ** | 0.045 | 2.49 | 0.013 |

| Married | 0.088 * | 0.047 | 1.83 | 0.067 |

| Education | 0.121 *** | 0.037 | 3.24 | 0.001 |

| Monthly income | 0.018 | 0.021 | 0.86 | 0.389 |

| Financial risk preference | 0.056 ** | 0.011 | 5.24 | 0.001 |

| Log pseudolikelihood | −258.340 | |||

| Pseudo R2 | 0.117 | |||

| Number of observation | 455 | |||

| Financial Risk Preference | Stock Market Participation | |||||

|---|---|---|---|---|---|---|

| Variables | Coefficient | SE | t | Coefficient | SE | z |

| Constant | 6.514 *** | 0.654 | 9.953 | −4.978 *** | 0.962 | −5.175 |

| Morningness | 0.745 *** | 0.277 | 2.688 | 0.543 | 0.351 | 1.551 |

| Age | −0.225 | 0.189 | −1.192 | 0.055 | 0.234 | 0.233 |

| Male | 0.750 *** | 0.179 | 4.186 | 0.577 ** | 0.234 | 2.471 |

| Married | 0.375 | 0.232 | 1.619 | 0.455 * | 0.258 | 1.768 |

| Education | −0.147 | 0.164 | −0.896 | 0.629 *** | 0.212 | 2.976 |

| Monthly income | 0.381 *** | 0.093 | 4.080 | 0.095 | 0.109 | 0.869 |

| Financial risk preference | 0.293 *** | 0.059 | 4.934 | |||

| R2 | 0.113 | |||||

| Pseudo R2 | 0.117 | |||||

| Number of observations | 455 | 455 | ||||

| Mediator Financial preference | Bootstrapping effect | Boot SE | 95% CI (LL, UL) | |||

| Indirect effect | 0.219 | 0.095 | 0.067 | 0.435 | ||

| Dependent Variables: Financial Risk Preference | Monthly Income as a Moderator in Ordinary Least Squares Regression | |||

|---|---|---|---|---|

| Variables | Coefficients | SD | t-Statistic | p-Value |

| Constant | 7.772 *** | 0.702 | 11.08 | 0.001 |

| Age | −0.232 | 0.186 | −1.25 | 0.214 |

| Male | 0.766 *** | 0.180 | 4.25 | 0.001 |

| Married | 0.381 * | 0.228 | 1.67 | 0.095 |

| Education | −0.144 | 0.160 | −0.90 | 0.369 |

| Morningness | 0.713 *** | 0.269 | 2.64 | 0.008 |

| Monthly income | 0.352 *** | 0.095 | 3.70 | 0.001 |

| Monthly income × Morningness | 0.209 | 0.286 | 0.73 | 0.463 |

| R2 | 0.115 | |||

| The Number of Observations | 455 | |||

| Financial Risk Preference | Stock Market Participation | |||||

|---|---|---|---|---|---|---|

| Variables | Coefficient | SE | t | Coefficient | SE | z |

| Constant | 7.866 *** | 0.722 | 10.899 | −4.974 *** | 0.962 | −5.168 |

| Age | −0.232 | 0.188 | −1.231 | 0.077 | 0.233 | 0.330 |

| Male | 0.766 *** | 0.183 | 4.180 | 0.600 *** | 0.232 | 2.587 |

| Married | 0.381 | 0.232 | 1.647 | 0.487 * | 0.255 | 1.912 |

| Education | −0.144 | 0.164 | −0.876 | 0.693 *** | 0.199 | 3.474 |

| Morningness | 0.713 ** | 0.280 | 2.545 | 0.549 | 0.351 | 1.566 |

| Monthly income | 0.379 *** | 0.093 | 4.070 | |||

| Financial preference | 0.303 *** | 0.059 | 5.174 | |||

| Monthly income × Morning type | 0.210 | 0.305 | 0.688 | |||

| R2 | 0.115 | |||||

| Pseudo R2 | 0.116 | |||||

| Number of observations | 455 | 455 | ||||

| Moderator: Monthly income | Bootstrapping indirect effect | Boot SE | 95% CI (LL, UL) | |||

| Low (−1 SD from mean) | 0.146 | 0.136 | −0.100 | 0.444 | ||

| Average (0 SD from mean) | 0.216 | 0.095 | 0.054 | 0.422 | ||

| High (+1 SD from mean) | 0.286 | 0.147 | 0.047 | 0.620 | ||

| Index of moderated mediation | ||||||

| Mediator | Index | SE (Boot) | 95% CI (LL, UL) | |||

| Financial preference | 0.064 | 0.095 | −0.107 | 0.279 | ||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, D.; McGroarty, F.; Cheah, E.-T. Chronotype, Risk and Time Preferences, and Financial Behaviour. Algorithms 2018, 11, 153. https://doi.org/10.3390/a11100153

Wang D, McGroarty F, Cheah E-T. Chronotype, Risk and Time Preferences, and Financial Behaviour. Algorithms. 2018; 11(10):153. https://doi.org/10.3390/a11100153

Chicago/Turabian StyleWang, Di, Frank McGroarty, and Eng-Tuck Cheah. 2018. "Chronotype, Risk and Time Preferences, and Financial Behaviour" Algorithms 11, no. 10: 153. https://doi.org/10.3390/a11100153

APA StyleWang, D., McGroarty, F., & Cheah, E. -T. (2018). Chronotype, Risk and Time Preferences, and Financial Behaviour. Algorithms, 11(10), 153. https://doi.org/10.3390/a11100153