Simultaneous Calibration of European Option Volatility and Fractional Order under the Time Fractional Vasicek Model

Abstract

:1. Introduction

2. Pricing Formula under the Time Fractional Vasicek Model

3. Regularization Method

3.1. Existence of Solutions to Optimization Problems

3.2. ADMM Algorithm

- −

- Step 1: minimization with repect to :

- −

- Step 2: minimization with repect to :

- −

- Step 3: update the Lagrange multiplier:where is the step size.

| Algorithm 1: Particle Swarm Optimization (PSO) |

|

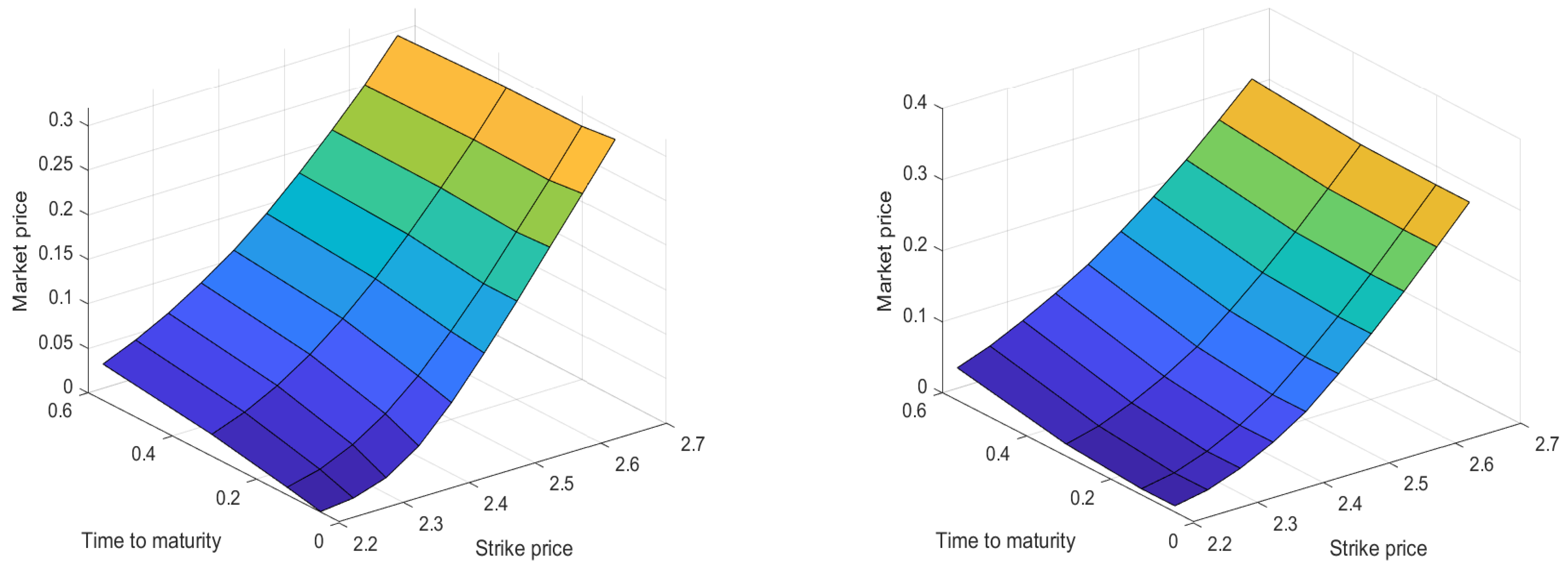

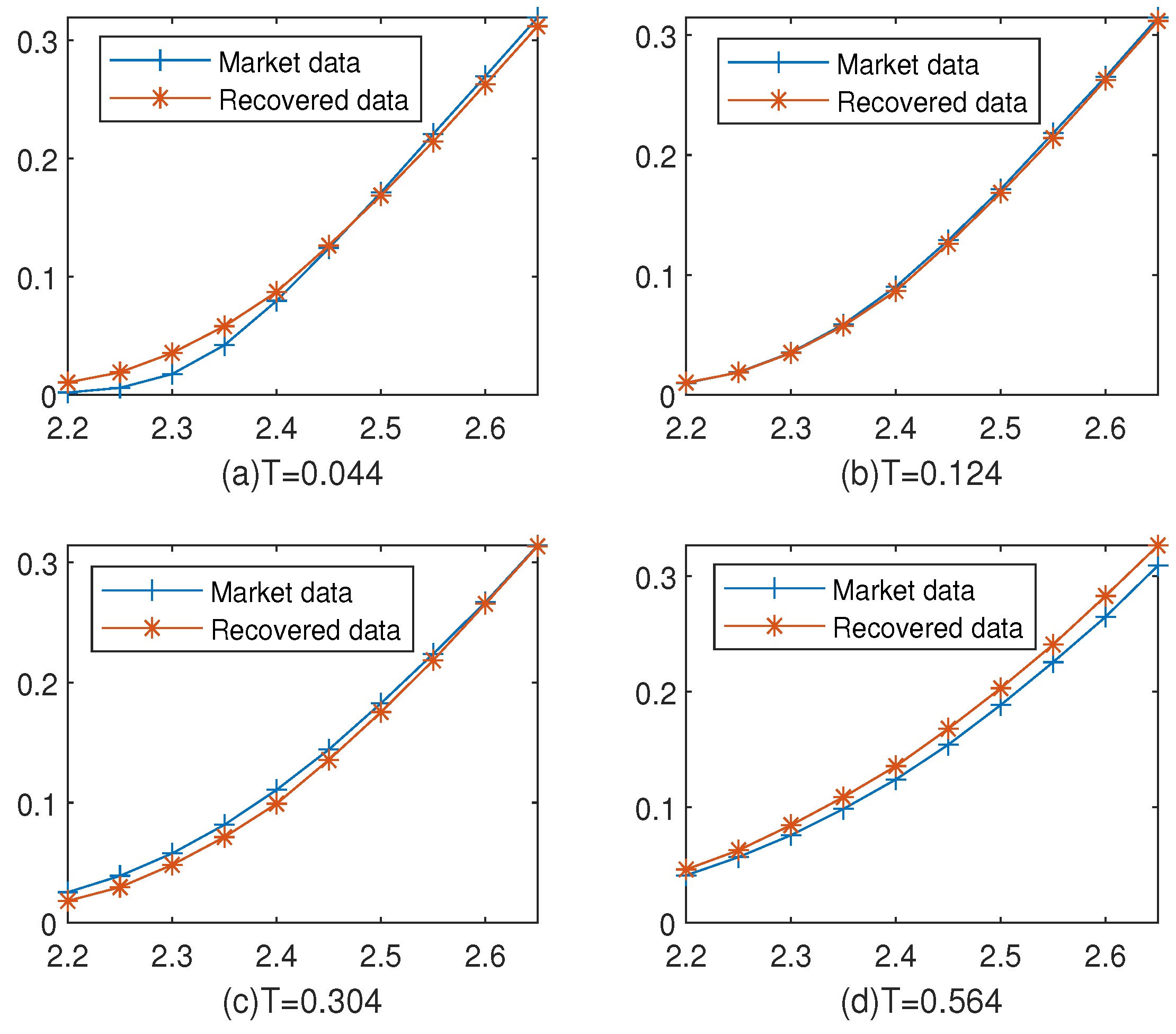

4. Numerical Experiments

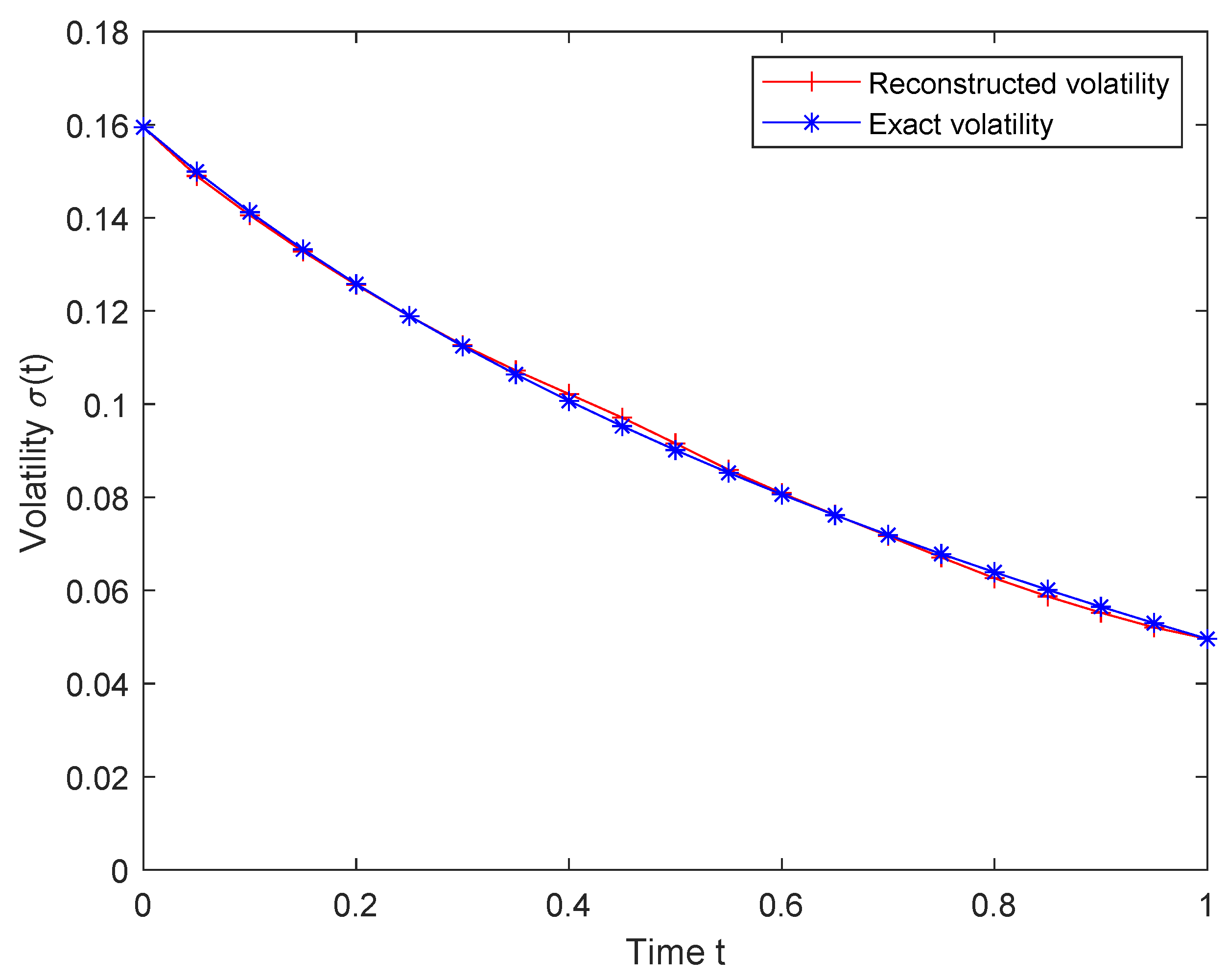

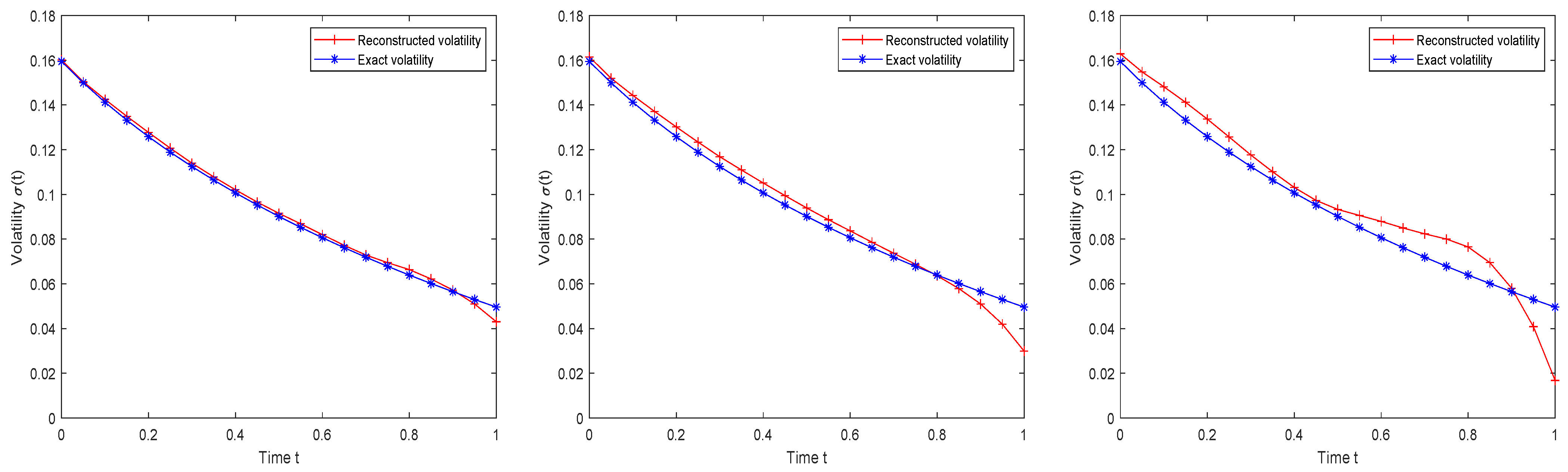

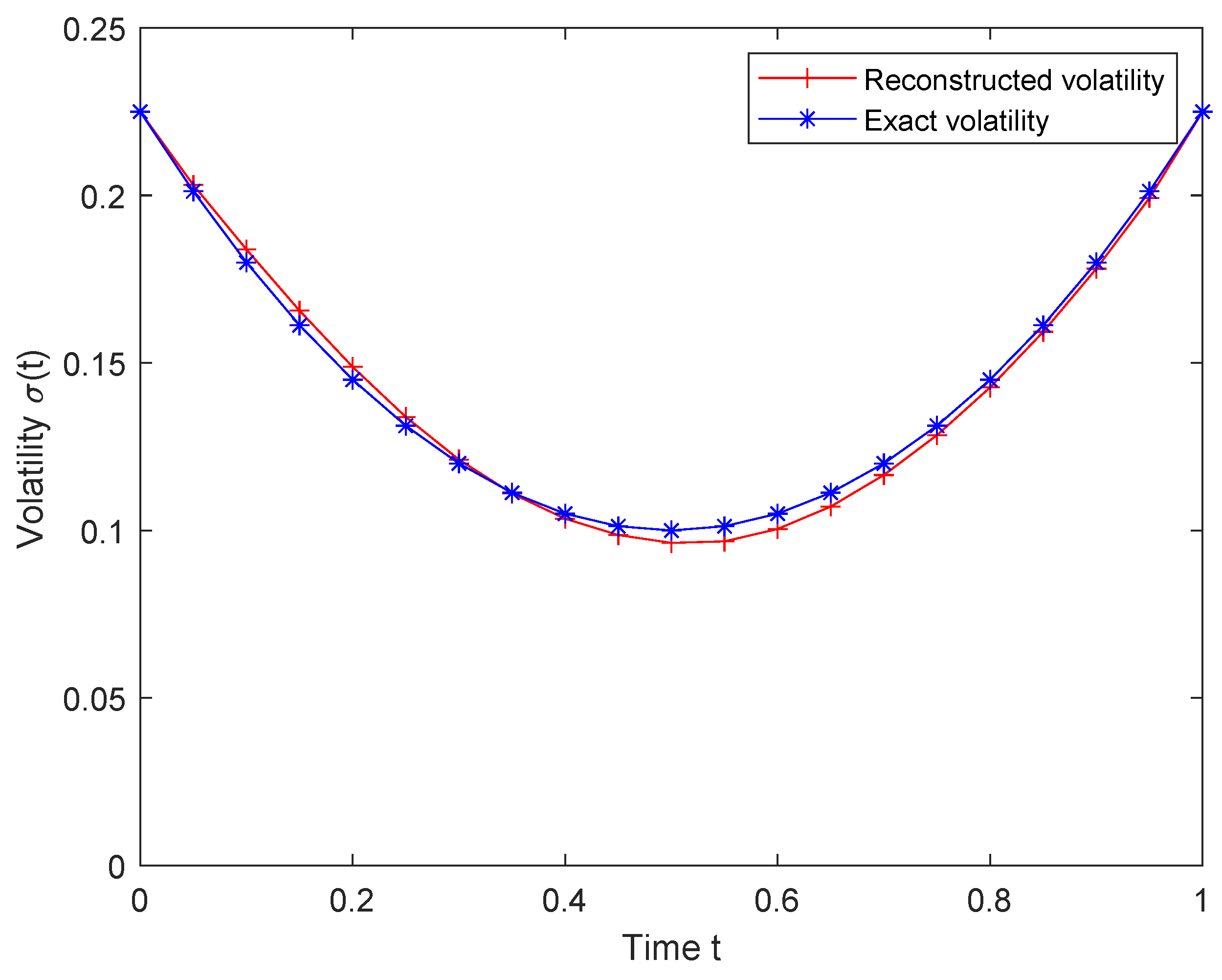

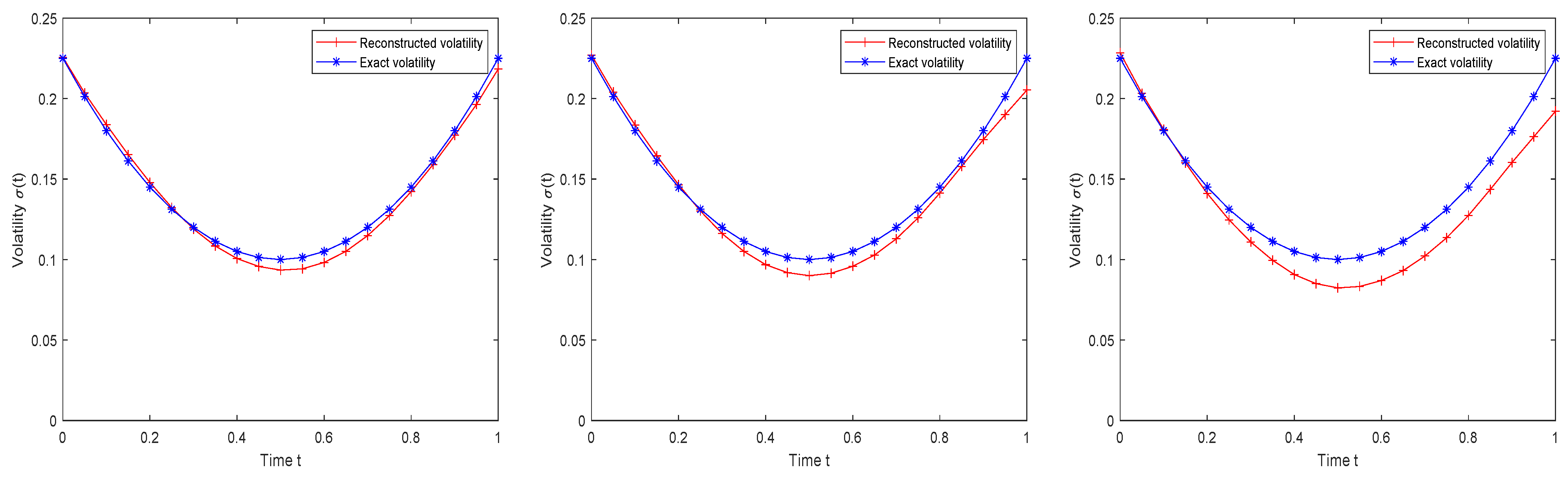

4.1. Numerical Simulation

4.2. Empirical Analysis

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Cox, J.C. The constant elasticity of variance option pricing model. J. Portf. Manag. 1996, 23, 15–17. [Google Scholar] [CrossRef]

- Cox, J.C.; Ingersoll, J.E., Jr.; Ross, S.A. A Theory of the Term Structure of Interest Rates, 2nd ed.; World Scientific: Singapore, 2005. [Google Scholar]

- Vasicek, O. An equilibrium characterization of the term structure. J. Financ. Econ. 1977, 5, 177–188. [Google Scholar] [CrossRef]

- Yao, K.; Liang, Y.S.; Zhang, F. On the connection between the order of the fractional derivative and the Hausdorff dimension of a fractal function. Chaos Soliton Fract. 2009, 41, 2538–2545. [Google Scholar] [CrossRef]

- Sene, N. Fractional model for a class of diffusion-reaction equation represented by the fractional-order derivative. Fractal Fract. 2020, 4, 15. [Google Scholar] [CrossRef]

- Cruz-Duarte, J.M.; Rosales-Garcia, J.; Correa-Cely, C.R.; Garcia-Perez, A.; Avina-Cervantes, J.G. A closed form expression for the Gaussian-based Caputo-Fabrizio fractional derivative for signal processing applications. Commun. Nonlinear Sci. 2018, 61, 138–148. [Google Scholar] [CrossRef]

- Nourian, F.; Lakestani, M.; Sabermahani, S.; Ordokhani, Y. Touchard wavelet technique for solving time-fractional Black-Scholes model. Comput. Appl. Math. 2022, 41, 150. [Google Scholar] [CrossRef]

- Roul, P. Design and analysis of a high order computational technique for time-fractional Black-Scholes model describing option pricing. Math. Method Appl. Sci. 2022, 45, 5592–5611. [Google Scholar] [CrossRef]

- Chen, C.; Wang, Z.; Yang, Y. A new operator splitting method for American options under fractional Black-Scholes models. Comput. Math. Appl. 2019, 77, 2130–2144. [Google Scholar] [CrossRef]

- Cao, J.; Li, C. Finite difference scheme for the time-space fractional diffusion equations. Open Phys. 2013, 11, 1440–1456. [Google Scholar] [CrossRef]

- Li, C.; Chen, A.; Ye, J. Numerical approaches to fractional calculus and fractional ordinary differential equation. J. Comput. Phys. 2011, 230, 3352–3368. [Google Scholar] [CrossRef]

- Gao, G.; Sun, Z.; Zhang, H. A new fractional numerical differentiation formula to approximate the Caputo fractional derivative and its applications. J. Comput. Phys. 2014, 259, 33–50. [Google Scholar] [CrossRef]

- Alikhanov, A.A. A new difference scheme for the time fractional diffusion equation. J. Comput. Phys. 2015, 280, 424–438. [Google Scholar] [CrossRef]

- Cao, J.; Xu, C.; Wang, Z. A High Order Finite Difference/Spectral Approximations to the Time Fractional Diffusion Equations. Adv. Mater. Res. 2014, 875, 781785. [Google Scholar] [CrossRef]

- Cao, J.; Li, C.; Chen, Y.Q. High-order approximation to Caputo derivatives and Caputo-type advection-diffusion equations (II). Adv. Mater. Res. 2015, 18, 735–761. [Google Scholar] [CrossRef]

- Mokhtari, R.; Mostajeran, F. A High Order Formula to Approximate the Caputo Fractional Derivative. Com. Appl. Math. Comput. 2020, 2, 1–29. [Google Scholar] [CrossRef]

- Li, D.; Wu, C.; Zhang, Z. Linearized Galerkin FEMs for nonlinear time fractional parabolic problems with non-smooth solutions in time direction. J. Sci. Comput. 2019, 80, 403–419. [Google Scholar] [CrossRef]

- Zhang, H.; Zeng, F.; Jiang, X.; Karniadakis, G.E. Convergence analysis of the time-stepping numerical methods for time-fractional nonlinear subdiffusion equations. Fract. Calc. Appl. Anal. 2022, 25, 453–487. [Google Scholar] [CrossRef]

- Yuan, W.; Zhang, C.; Li, D. Linearized fast time-stepping schemes for time-space fractional Schrödinger equations. Phys. D 2023, 454, 133865. [Google Scholar] [CrossRef]

- Zhang, H.; Jiang, X. Convergence analysis of a fast second-order time-stepping numerical method for two-dimensional nonlinear time-space fractional Schrödinger equation. Numer. Methods Partial Differ. Equations 2023, 39, 657–677. [Google Scholar] [CrossRef]

- Dupire, B. Pricing with a smile. Risk 1994, 7, 525–546. [Google Scholar]

- Xu, Z.; Jia, X. The calibration of volatility for option pricing models with jump diffusion processes. Appl. Anal. 2019, 98, 810–827. [Google Scholar] [CrossRef]

- Jiang, L.; Chen, Q.; Wang, L.; Zhang, J. A new well-posed algorithm to recover implied local volatility. Quant. Financ. 2003, 3, 451. [Google Scholar] [CrossRef]

- Li, S.; Zhou, Z. Legendre pseudo-spectral method for optimal control problem governed by a time-fractional diffusion equation. Int. J. Comput. Math. 2017, 95, 1308–1325. [Google Scholar] [CrossRef]

- Zhao, J.; Xu, Z. Simultaneous identification of volatility and mean-reverting parameter for European option under fractional CKLS model. Fractal Fract. 2022, 6, 344. [Google Scholar] [CrossRef]

- Yimamu, Y.; Deng, Z. Convergence of Inverse Volatility Problem Based on Degenerate Parabolic Equation. Mathematics 2022, 10, 2608. [Google Scholar] [CrossRef]

- Jiang, L.; Li, C. Mathematical Modeling and Methods of Option Pricing, 1st ed.; World Scientific: Singapore, 2005. [Google Scholar]

- Zhang, H.; Liu, F.; Turner, I.; Yang, Q. Numerical solution of the time fractional black-scholes model governing European options. Comput. Math. Appl. 2016, 71, 1772–1783. [Google Scholar] [CrossRef]

- Tikhonov, A.N. On the solution of ill-posed problems and the method of regularization. Russ. Acad. Sci. 1963, 151, 501–504. [Google Scholar]

- Lagnado, R.; Osher, S. A technique for calibrating derivative security pricing models: Numerical solution of an inverse problem. J. Comput. Financ. 1997, 1, 13–25. [Google Scholar] [CrossRef]

- Kharrat, M.; Arfaoui, H. A new stabled relaxation method for pricing European options under the time-fractional Vasicek model. Comput. Econ. 2023, 61, 1745–1763. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| RMSE | |||||

|---|---|---|---|---|---|

| 9.4106 × | 9.4772 × | 1.836 × | 0.700 | 1.07 × | |

| 9.8816 × | 0.0026 | 6.565 × | 0.700 | 1.249 × | |

| 9.9998 × | 0.0052 | 1.9694 × | 0.697 | 9.465 × | |

| 1.0000 × | 0.0090 | 3.2824 × | 0.696 | 1.309 × |

| 9.9770 × | 0.0030 | 4.621 × | 0.364 | 2.855 × | |

| 9.9975 × | 0.0044 | 7.820 × | 0.367 | 5.162 × | |

| 9.9999 × | 0.0073 | 1.9694 × | 0.372 | 1.9478 × | |

| 4.8906 × | 0.0156 | 3.2824 × | 0.359 | 3.4620 × |

| K | ||||

|---|---|---|---|---|

| 0.0021 | 0.0099 | 0.0255 | 0.0411 | |

| 0.0060 | 0.0189 | 0.0391 | 0.0569 | |

| 0.0177 | 0.0353 | 0.0578 | 0.0759 | |

| 0.0421 | 0.0588 | 0.0816 | 0.0986 | |

| 0.0796 | 0.0902 | 0.1107 | 0.1241 | |

| 0.1241 | 0.1290 | 0.1442 | 0.1542 | |

| 0.1712 | 0.1714 | 0.1827 | 0.1885 | |

| 0.2206 | 0.2182 | 0.2238 | 0.2256 | |

| 0.2695 | 0.2651 | 0.2668 | 0.2648 | |

| 0.3191 | 0.3145 | 0.3140 | 0.3092 |

| 9.9351 × | 0.120 | 1.810 × |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Du, Y.; Xu, Z. Simultaneous Calibration of European Option Volatility and Fractional Order under the Time Fractional Vasicek Model. Algorithms 2024, 17, 54. https://doi.org/10.3390/a17020054

Du Y, Xu Z. Simultaneous Calibration of European Option Volatility and Fractional Order under the Time Fractional Vasicek Model. Algorithms. 2024; 17(2):54. https://doi.org/10.3390/a17020054

Chicago/Turabian StyleDu, Yunkang, and Zuoliang Xu. 2024. "Simultaneous Calibration of European Option Volatility and Fractional Order under the Time Fractional Vasicek Model" Algorithms 17, no. 2: 54. https://doi.org/10.3390/a17020054

APA StyleDu, Y., & Xu, Z. (2024). Simultaneous Calibration of European Option Volatility and Fractional Order under the Time Fractional Vasicek Model. Algorithms, 17(2), 54. https://doi.org/10.3390/a17020054