1. Introduction

Driven by a growing demand for renewable energy feedstock, chip production has expanded rapidly all over Europe providing work to logging, chipping and hauling companies that operate near the new plants. For this reason, many contractors have invested in mobile chippers, and more are prospecting the purchase of such equipment.

The acquisition of a mobile chipper involves a significant capital investment, which makes the formulation of a correct machine rate a crucial task. Machine cost is estimated using standard economic methods that divide total cost into capital and operating cost components [

1]. Capital cost is dependent on the size of the investment, the expected economic life of the machine and the interest rate charged on borrowed capital, and it is incurred whether or not the machine is working. Conversely, the operational cost depends on all the expenses incurred when the machine is actually working. To calculate a cost per unit of product (m

3 or ton), a productivity estimate is also needed. Contractors need reliable data for pricing their machines, so that they can make informed decisions when planning new investments, and offer competitive contract rates with a minimised risk of going bankrupt. Standard cost calculation methods are often assembled into dedicated spreadsheet calculators capable of returning reliable estimates of chipping productivity and cost, based on user-defined input data [

2].

Chipper productivity [

3,

4,

5] and fuel consumption [

6,

7,

8] have been documented in many studies, performed on a variety of wood chipping equipment under a wide range of work conditions. Information is also available about utilization [

9] and annual use [

6]. However, the information about annual use and fuel consumption available so far has been obtained from relatively small samples, which makes it difficult to model these figures as a function of machine type, age or use intensity. Even worse, any estimates for service life and resale value are based on older regional studies, when they do not derive from guesswork or anecdotal information. Due to the large capital investment, the assumptions made for economical service life, annual use and resale value also have a large impact on the calculation of interest charges [

10].

The combination of accurate productivity estimates coupled with largely hypothetical cost assumptions makes chipping cost predictions quite unreliable. There is a fundamental contradiction between the large amount of work invested in developing accurate chipper productivity benchmarks that can reflect machine, job and feedstock characteristics, and the limited attention paid to determining equally accurate figures for chipper cost.

Chipping emerged as an important business sector in Italy already in the late 1990s [

11]. Many contractors have now worked with chipping for almost two decades, changing several machines and gaining significant experience with this technique. Much knowledge is now available among the contractors themselves, and their records can provide a wealth of important information, because they often cover the whole life time of their machines. As this study is based on these records, it has a strong Italian bias. However, in many respects it can be generalized and extended to other countries, because the Italian chipper fleet represents a whole range of machine makes and models that are popular outside Italy, and the local business structures are similar to those found elsewhere in Europe.

Therefore, the goals of this study were to: (1) produce reliable benchmark figures for the service life and the resale value of wood chippers, which may reflect machine type, age and intensity of use, and (2) produce reliable estimates of productivity and annual use, based on long-term contractor records. This information is considered essential to estimating a correct chipper management cost, which may reflect the specific conditions encountered by each individual user. This work will enable chipping contractors to calculate fair chipping rates, which will allow them to stay competitive while accruing reasonable profits.

2. Materials and Methods

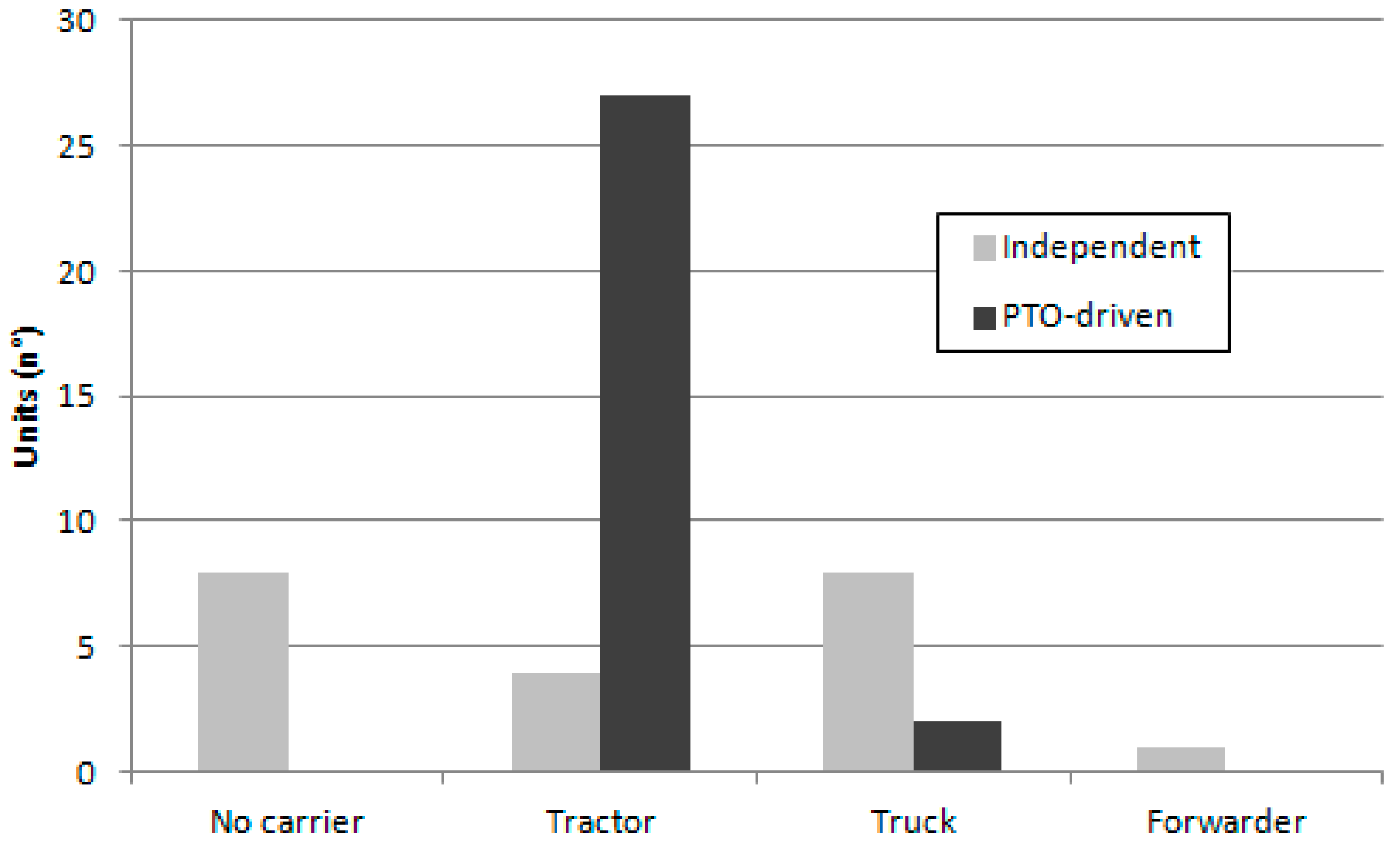

The study covered a whole range of chipping units, from light tractor-powered machines (PTO-driven, or driven through the tractor power take-off) originally designed for part-time use, to powerful independent-engine industrial units best suited to the specialized chipping contractor (

Figure 1). For the purpose of the study, the chipping unit represented a complete self-supported operation designed for mechanical feeding with a hydraulic loader. Therefore, each unit comprised of a chipper, a loader and a carrier. The loader could be integral or separate, i.e., a self-propelled loader, an adapted excavator or a farm tractor equipped with its own loader. The carrier could be a tractor, a truck or a forwarder. However, if the chipper was equipped with its own independent engine and was moved to the work site using a low-bed trailer, then no carrier was included with the chipping unit.

All machines in the survey were owned and operated by Italian entrepreneurs, and were deployed in Italy, with few exceptions of occasional cross-border activity. Despite its strong Italian character, the study covered a whole range of makes and models, both Italian and foreign. Overall, the survey included 50 units, where the chipper was powered by an engine ranging from 59 to 460 kW.

For the purpose of the study, machine owners were requested to supply data about: machine price at purchase and at the moment of the interview in 2017, or at the time of resale if the machine had already been sold; date of purchase and of the eventual resale; total machine hours (motor hours) worked from purchase to present, or to resale; total fresh tons of chips produced in the same period. Price and use data were to be provided separately for the chipper, the carrier and the loader—if one was used.

When the carrier and the loader were not permanently attached to the chipper, and thus could be used to perform other jobs, then the entrepreneurs were asked to indicate the percent of chipping work performed with this machinery, so that their total separate costs could be pro-rated in terms of chipping work only, avoiding redundant attribution. Additional cost figures were also collected, such as: insurance, fuel, lube, repair and maintenance, and labor. That was done in order to determine the proportion of fixed cost over total cost, while keeping the latter confidential not to weaken the contractors’ negotiating power.

In total, 116 operators were contacted by phone before sending the survey form. All were private entrepreneurs who performed chipping as a full-time specialized occupation, or as a part-time job complementary with a main occupation in the logging sector. Once the survey form was received, follow-up phone calls allowed clarifying any doubts and/or integrating missing data. Understandably, not all entrepreneurs had kept records of the required quality, or were willing to search their files in order to track all relevant machine use records for the whole life of their machines. For this reason, the study was based on 50 surveys only, which represented those respondents who could guarantee sufficient data quality.

All surveys were consolidated into a single data file for statistical analysis, which was conducted using SAS Statview (Version 5.1) [

12]. As a first step, descriptive statistics were calculated, separately for the main machine classes. The statistical significance of any differences between machine classes was checked with parametric and non-parametric tests, depending on the distribution of data. Then, regression analysis was used for establishing the significance of any relationships between purchase price, value retention, annual use, productivity and all independent variables that were expected to have some effect on these parameters. The elected significance level was α < 0.05.

3. Results

3.1. Characteristics of the Machine Pool

The 50 units included in the study represented a whole range of operations, and comprised 29 PTO-driven and 21 independent-engine machines (

Figure 2). The former were powered most often by a wheeled farm tractor, of variable size and power. Only two PTO-driven machines were powered by a truck, and could be defined as chipper trucks [

13].

Out of 50 sample units, 26 (52%) operated in Northern Italy, 20 (40%) in Central Italy and only 4 (8%) in Southern Italy. Austrian, German and Italian makes accounted for the largest proportion of the sample, offering a good representation of the current Italian fleet, which is quite international (

Figure 3). The Italian

Pezzolato was the most common brand (19 machines), immediately followed by the German

Jenz (11 machines). Other common brands were: Farmi (Nordic, 3 units), Gandini (Italian. 3 units), Heizo-hack (German, 3 units) and Mus-Max (Austrian, 3 units).

The sample showed a clear distinction between PTO-driven and independent-engine machines. Compared with PTO-driven units, independent-engine chippers were significantly more powerful, expensive and productive (

Table 1). In contrast, no significant differences between these two machine types were found concerning value retention, duration in service and intensity of use. Furthermore, use of an integral loader was twice as common among independent-engine units (60% of the cases) as among PTO-driven units (30% of the cases). Together with the possibility of de-coupling the prime mover from the chipper, that enabled about half of the PTO-driven operations to clock additional work hours on the loader and the carrier, while only 10% of the independent-engine units followed a similar strategy—largely because disconnecting the loader and/or the carrier was technically difficult and would not pay off, even when chipper use was not very intense.

None of the PTO-driven machines represented small, part-time operations: on the contrary seven among them were coupled with tractors delivering between 170 kW and 280 kW, and two were powered by large trucks with the same 350 kW engine installed on some of the most common and powerful independent-engine units in the sample.

3.2. Purchase Price and Value Retention

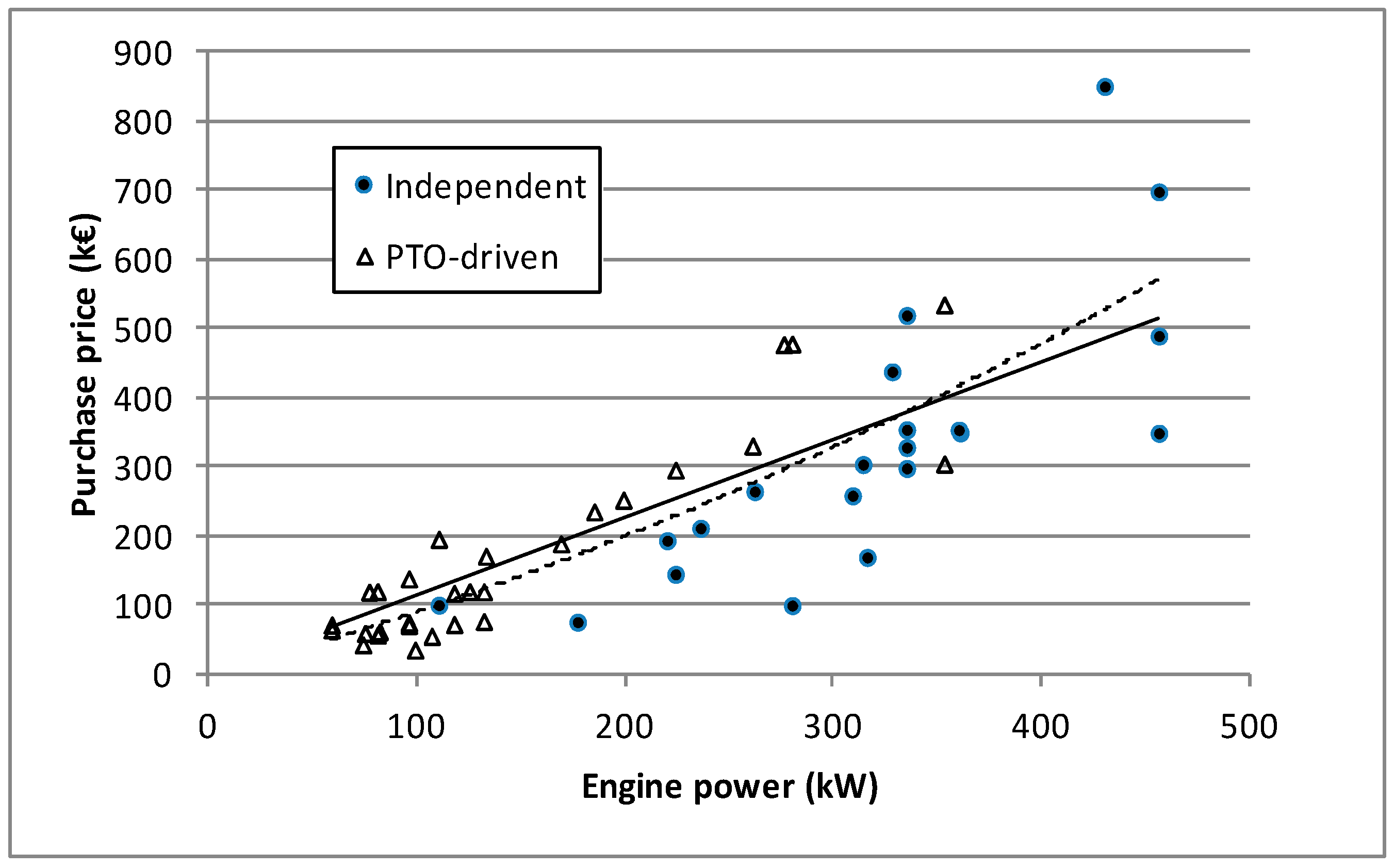

Purchase price varied from 35,000 to 850,000 €, or most commonly from 110,000 to 360,000 € (lower and upper quartile, respectively). This price was the 2017 equivalent, obtained by revaluating actual figures to 2017 currency values with the dedicated calculator provided by the Italian Statistical Agency [

14]. The purchase price included the chipper, the loader and the carrier, when one was used (all cases except for eight). If a carrier or a loader were also used in other tasks than chipping, then their revaluated purchase price was allocated to the chipping unit as a proportion of actual use with the chipper.

The distribution on the total purchase price among these main components varied significantly between chipping unit types (

Figure 4). While the price of the chipper was the dominant component for both PTO-driven and independent-engine machines, it was significantly more important for the latter (

p = 0.0003). In contrast, the proportion of total price invested in the carrier was significantly higher for PTO-driven machines, compared with independent-engine machines (

p = 0.0007). The loader accounted for ca. 20% of the total price, with no significant differences between machine types (

p = 0.6870).

Purchase price was strongly associated with engine power, which explained almost 90% of the variability in the dataset (

Table 2). The remaining variability was likely explained by differences in other machine characteristics, including optional equipment features. Furthermore, different negotiating power and capacity at the time of buying must have had their impact on price formulation [

15]. Regression analysis showed that chipper type (independent-engine or PTO-driven) had no significant effect on purchase price, indicating that on a kW by kW basis a PTO-driven chipper was as expensive to purchase as an independent-engine chipper. Of course, that accounted for the whole unit, comprised of chipper, loader and carrier—not for the chipper component only.

Regression analysis yielded two different equations for estimating purchase price as a function of engine power: a linear equation and a quadratic equation (

Table 2). The linear equation was probably the safest one, because one of the terms in the quadratic equation was not highly significant and the coefficient of determination R

2 for the quadratic equation was only marginally higher than that of the linear equation. This was most likely an effect of the increased number of variables rather than an indicator of a better capacity to represent dataset variability. However, the quadratic equation was also reported in the paper because visual analysis of the data hinted at an upward turning curve, which was best represented by a quadratic equation rather than a linear one (

Figure 5). In any case, readers are warned against extrapolating the results of these models beyond the range of variation of the independent variable: that is generally wrong and may produce incorrect estimates, especially when the curve represents a quadratic function.

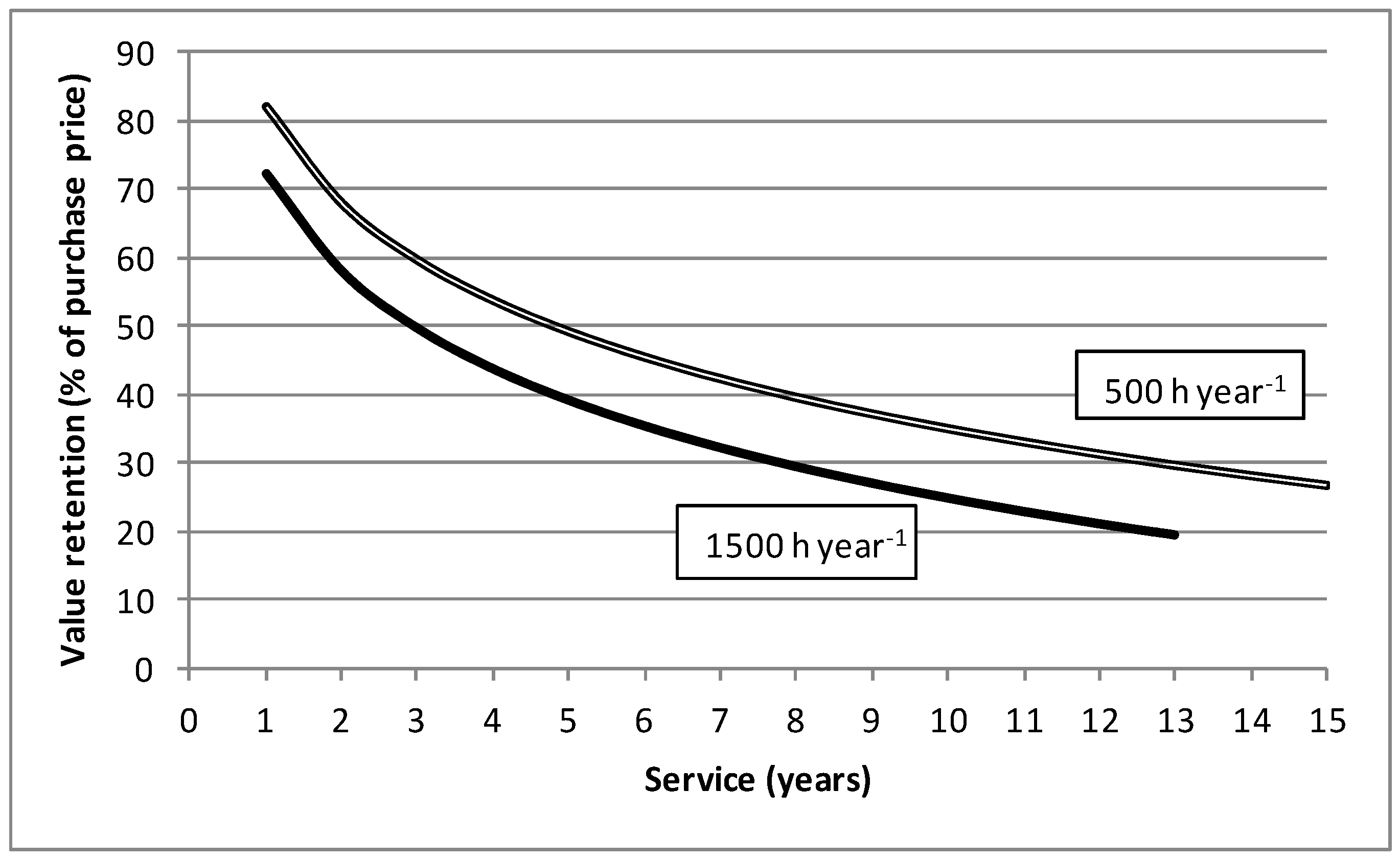

Value retention was defined as the relationship between resale price and revaluated purchase price, expressed as a percent ratio. Value retention decreased with use, as one would expect. Among the many indicators for use, number of years in service and use intensity (h year

−1) proved the best predictors (

Table 2). The total number of hours clocked in by a machine was half as good a predictor as the total number of years in service, a tendency that was already reported for harvesters and forwarders in previous studies [

16,

17]. Interestingly enough, neither engine power nor chipper type (i.e., independent-engine or PTO-driven) had any significant effect on value retention. The value losses were highest over the very first years and became increasingly smaller with extended service life (

Figure 6), as typical of most machinery [

18].

3.3. Service Life and Use Intensity

Determining reliable benchmark figures for service life was among the primary goals of this study. The average service life figures obtained from this study were not representative of total service life because they just described how old were the sample machines at the time of the survey, regardless of whether they were about to be replaced or not [

19]. The maximum value in the range or the upper quintile offered a more representative estimate, which could be taken as a proxy for the total life one may reasonably expect from a chipper. In that case, total service life could be estimated anywhere above 10 years or 6000 h, with a maximum as high as 24 years or 20,000 h (

Table 3). Similarly, the production expected over the lifetime of a chipper was likely higher than 100,000 t, with a maximum close to half a million t.

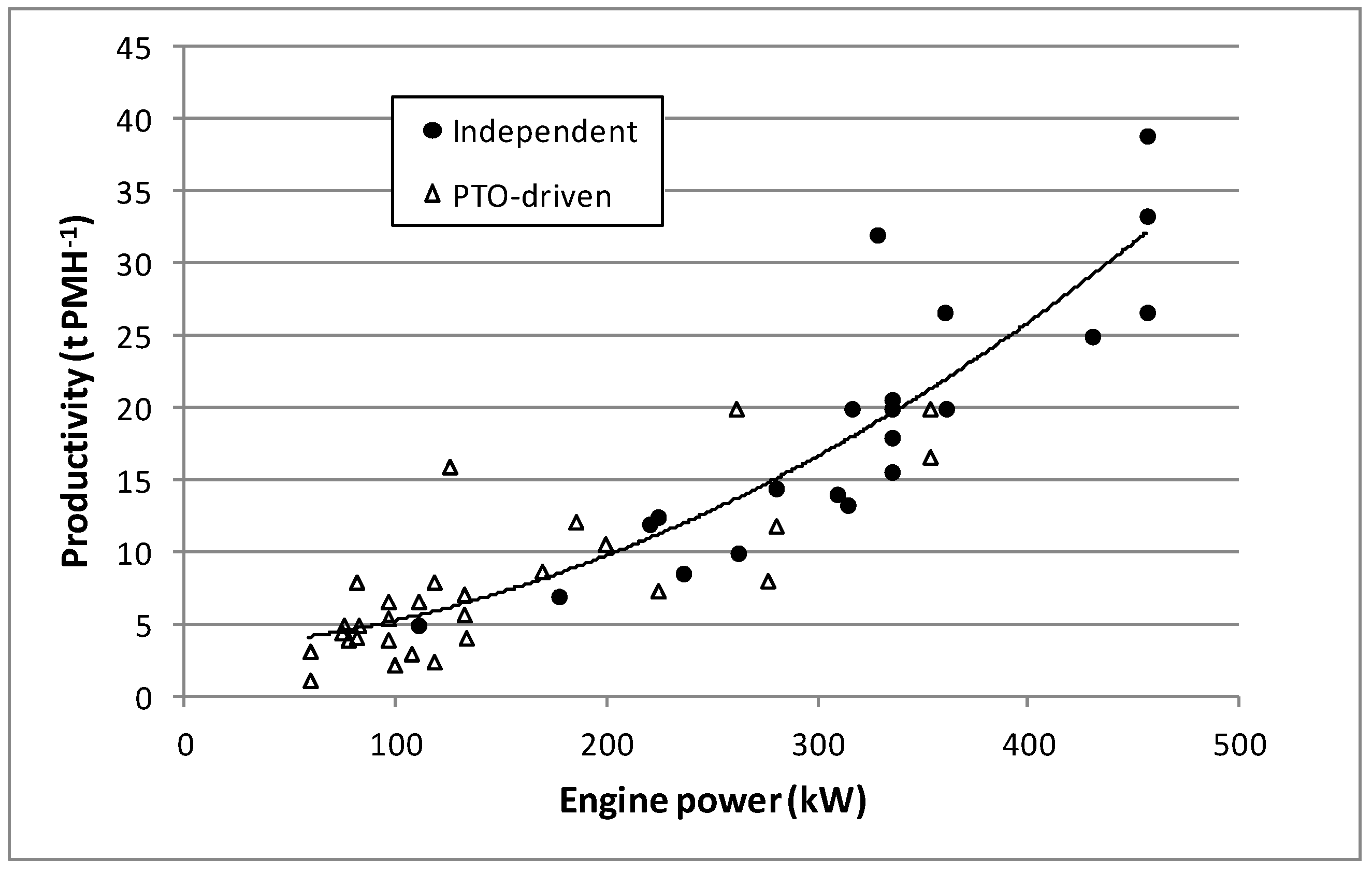

Mean use intensity was near to 600 h year

−1 or 9000 t year

−1, but a large share of the contractors easily doubled these figures, as represented in the upper quintile. As expected, use intensity increased significantly with chipping unit price, indicating that more expensive and productive units were bought by contractors with more work (

Table 4,

Figure 7).

3.4. Productivity and Cost

Long-term productivity was calculated from total production and total machine use, which was modelled as a function of relevant independent variables. Among these, engine power was the most influential and explained over 80% of the variability in the dataset. Chipper type had no significant effect on long-term productivity, supporting the notion of PTO-driven and independent-engine chippers being equally productive as long as engine power was the same. Productivity was affected by loader type and was ca. 2 t h

−1 higher for those units that used a separate loader, instead of an integral one. However, the loader variable was borderline significant (

p = 0.067) and therefore this result was suggestive, not conclusive. For this reason, the effect of loader type was not included in the final model. The final equation represented a power curve and described a clear scale effect, where engine power increments resulted in proportionally larger productivity increments (

Figure 7). Once more, readers are warned against extrapolating the results of this model beyond the range of variation spanned by the original data.

Raw chipping cost varied most commonly between 6 and 33 € t−1, and it was represented by fixed cost for approximately 40%, without any significant differences between PTO-driven and independent-engine units (p = 0.7020). Obviously, the proportion of fixed cost decreased with use intensity, since the two were tied by a strictly deterministic relationship.

4. Discussion

4.1. Limitations of the Study

Before embarking in a proper discussion, it is just fair to state upfront the limitations of the study, namely: the national character of the sample, the reliance on company records and the largely subjective way of estimating resale value.

The sample certainly offers a good representation of Italian chipping business but may fall short of correctly representing the situation in other countries. However, it includes a wide range of machine types that are used throughout Europe, and may offer a good picture of biomass operations in general. In that regard, it is worth stressing that biomass chipping is a relatively simple process, which is less affected by terrain and forest characteristics than other steps in the forest value chain, such as felling, extraction or merchandising [

20]. Certainly, the results of this study are valid for biomass operations only, and may not extend to pulp chip harvesting without much caution, because the technology used in America or Australia for producing pulp chips is different from that applied to European biomass operations [

21].

The reliance on company records is another limitation, given the inherent variability of these records for what concerns accuracy and resolution. However, contractors were only asked to provide basic figures, generally recorded in a common way or easily calculated from more detailed records. Furthermore, contractors who did not have good records or felt uneasy about allowing access to their data could simply excuse themselves, which many actually did. Therefore, respondents had little reason to provide inaccurate or deceitful figures. The general consistency of the dataset and of derived figures, such as productivity, indicates that contractor responses are accurate. Gross inaccuracy would have been denounced by recurring outliers and by a low explanatory capacity of regression equations, neither of which did materialize.

Probably, the weakest element in this study was the estimate for resale value, which was often based on the individual appraisal of machine owners, since few of the machines in the sample had been actually sold back. Owners’ appraisals are based on their subjective views of the market and the machines, and may reflect owner’s expectations rather than an actual market value. However, owner figures were checked against market values for similar equipment reported on the most popular second-hand machinery on-line shops, which offer numerous quotes especially for loaders and carriers. Figures generally matched, corroborating the estimates provided by machine owners.

In any case, the knowledge gathered in this study is unique in its capacity to reflect chipping entrepreneurship. To our knowledge, there are no other studies that have gathered long-term data from so many chipping contractors, and the few available studies tap into the records of State companies and cooperatives, which often benefit from the existence of a formal administration office and a centralized infrastructure [

22].

4.2. Long Live the Chipper

Chipping is hard work, and for this reason one may assume chippers to be short-lived, as they succumb to fatigue and rapid wear. This study contradicts the gloomiest expectations and points at a surprisingly long service life for a machine that receives so much punishment. The figures reported in this study are only marginally smaller than reported for harvesters and forwarders [

16,

17], and can easily exceed the 10,000 h threshold. However, the reported figures represent a technical service life and not an expected economical lifetime, which may be shorter (or longer yet).

If chipping is indeed brutal work, it is also true that modern chippers are designed for it by skilled manufacturers, who know how to build an efficient and durable piece of equipment. Furthermore, chippers are relatively simple machines, which supports longevity and facilitates maintenance. In fact, the study did not quantify maintenance cost, and therefore it could not establish if the exceptionally long service life of some machines in the sample pool was associated with an excessive increase of maintenance cost. If so, one would simply be observing a case of belated replacement, past optimum service life [

23]. Evidence of increasing maintenance costs may be observed as a faster drop in value retention, compared with other machine types, but that is not the case either; in fact, used chipping units seem to have better value retention than dedicated cut-to-length equipment, such as harvesters and forwarders [

16,

17]. As far as one can tell, chippers are solid, durable machines.

On the other hand, the extremely simple design of most chippers may justify extending service life through the iterative renewal of worn parts, much like in Theseus’ paradox [

24]. In that case, the machine would be finally replaced only due to obsolescence, non-conformity with new safety regulations or changes in the owner’s production target that would require purchasing a new machine. In the absence of direct evidence for the maximum rational service life of wood chippers, one has to fall back on indirect stochastic indicators, such as the quintile group. The number of respondents above the 4th quintile is large enough to mitigate the effect of the odd irrational owner, if any such owners exists in a group of experienced professionals. Further studies should aim at refining the current estimates for service life, addressing the issue of its interaction with maintenance cost.

Finally, the annual use figures reported in this study are significantly lower than those previously reported in a similar study of six Italian contractors [

6]. In particular the present study estimates an annual use of 500 h for PTO-driven chippers and 700 h for independent-engine chippers, whereas previously published data are 900 h and 1200 h, respectively. This can be explained by differences in the respective samples: this study contains a wide sample that comprises both part-time chipping contractors and specialized full-time chipping contractors, while the previous study only includes the latter group.

4.3. Engine Power as the Main Predictor

One of the most important findings of this study is the strong association of engine power with the main figures of interest: purchase price, productivity and annual use. These relationships are logical and are already reported in previous chipper studies, at least for what concerns productivity [

11]. What is surprising is rather the capacity of the variable “engine power” to displace all other predictors, despite the undeniable effect of other factors on the dependent variables of interest. That is largely due to the lack of information about these other variables, such as job characteristics (for productivity) or optional features (for purchase price). However, one may expect that the lack of such details would result in a much lower explanatory capacity for the estimated models: that it is not the case is a great comfort, and opens the possibility of issuing “quick and (not so) dirty” estimates based on simple fundamental information that should be easily available to any user. Engine power is a unifying predictor, capable of summarizing the most important effects recorded: the identification of a single powerful predictor lends additional merit to this study, and points at its capacity to dig deep into the fundamentals. For this same reason, the models in the study may return principal estimates of long-term performance but may not reflect as accurately specific work conditions, which makes them more suitable for strategic planning than for tactical planning.

4.4. Robust Productivity Model

The study yielded a simple and robust productivity model, which can be used as a benchmark for chipper productivity even in the absence of additional detail about piece size and job type. This model has a very high predicting capacity and offers a good match with previously published models, with the additional benefit of being simpler to use.

In that regard, it is important to stress that the time used as a denominator in the productivity equation is engine run time (hour meter), which deviates in some measure from both productive machine time (excluding all delays) and scheduled time (including all delays) [

25]. The machine clock runs whenever the machine engine is on, and it will include the wide range of shorter delay events during which the operator does not deem practical to turn off the engine. In contrast, the operator is much likely to turn off the engine when the interruption is expected to last for a longer time, and certainly when performing machine maintenance. For this reason, the productivity estimates obtained from the model should best compare to the PSH

15 productivity figures reported in many German studies. PSH

15 stands for productive system hours, consisting of productive work time and all delay events lasting no more than 15 min. That seems the closest match to the description provided above, and should offer a viable proxy. Previous studies of chipper delays indicate that delay events with a maximum duration of 15 min account for only one-third of total delay time, and therefore the productivity estimates returned by the model are substantially higher than the actual productivity calculated on the basis of total scheduled time [

9]. In that regard, one must notice that different machine meters record time in different ways: some simply measure the time when the engine is on—even if idle—while others only record the time when the engine runs above a certain rotational regime, thus excluding idle time. With so many different machine models from so many different manufacture years, the study sample is likely to contain a mix of both hour meter types, which certainly contributes to random variability. Nevertheless, this variability is not as large as to prevent building strong models and disclosing highly significant differences, as the study results demonstrate.

Finally, it is worth highlighting the form of the productivity curve estimated in this study. Since the exponent is larger than 1, the curve bends upwards and describes the typical phenomenon of increasing returns, which in this specific case has been interpreted as the scale effect of engine power. Conversely, curves relating productivity to piece size use exponents smaller than 1 and bend downwards, indicating diminishing returns as piece size increases [

26]. That is important to notice, because it demonstrates that productivity is directly proportional to both engine power and piece size, and yet investments in engine power are more productive, as returns are higher and may easily offset limitations in piece size.

4.5. Chipper Type Is Indifferent

Another interesting result of this study is the lack of any principle differences between PTO-driven and independent-engine chippers. In fact, the only major difference is power, because PTO-driven chippers are limited by the power of existing farm tractors. However, for the same engine power, PTO-driven machines are as productive, durable and expensive as independent-engine machines. Of course, price equality is only true for the whole chipping unit, including loader and carrier: the chipper component alone is less expensive when no own engine is provided.

If the two unit types are technically and financially equivalent, one may wonder about what drives the choice towards one or the other option. Power availability is again a pivotal factor: if one needs a larger machine than a tractor can support, then an independent-engine chipper is the only solution. If power is not an issue, the data point at equipment flexibility as a main driver. Approximately half of the PTO-driven units make use of the carrier and the loader for additional tasks than just chipping. In those cases, a PTO-driven chipper allows disconnecting the tractor when it is needed for other jobs, and contributes to a better utilization of the tractor itself [

27]. Even so, the question remains unanswered for the other half of the cases, where a tractor is permanently coupled with the chipper. Further research may address the decision factors leading to specific technology choices, which could improve our understanding of this business and help prospective users with their plans [

28].

5. Conclusions

This study is currently the only one offering updated empirical data on the purchase price, value retention, economic life and annual use of chipping units used in biomass operations. Such data have been obtained from a large group of chipping contractors, representing the small and medium-scale enterprises that support the European chipping contracting sector. The information obtained from the study is essential to formulating reliable machine rate estimates. Results highlight a longer economic life and a better value retention than previously assumed for this equipment type, which may result from skilled machine design and professional use—both deriving from the experience gained over the years in this crucial sector. The study also reveals that engine power can be used as the main predictor for most of the parameters investigated in the study. Furthermore, it points at the basic equivalence between PTO-driven and independent-engine chippers, once differences in engine power are accounted for. Finally, the study offers a robust and simple productivity benchmark, which can be used for extracting fast and reliable estimates of expected long-term performance.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}