Exploring the Factors Affecting Countries’ Adoption of Blockchain-Enabled Central Bank Digital Currencies

Abstract

:1. Introduction

2. Theoretical Foundation and Hypotheses Development

2.1. Technological Factors

Technological Readiness

2.2. Environmental Factors

Sustainable Development Goals

2.3. Legal Factors

2.3.1. Corruption Perception and Control

2.3.2. Democracy Level

2.3.3. Economic Freedom and Regulatory Quality

2.4. Economic Factors

2.4.1. Income Disparity

2.4.2. Human Development and Currency Reserve

3. Materials and Methods

4. Results

5. Discussion and Directions for Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Yun, J.H.J.; Won, D.K.; Jeong, E.S.; Park, K.B.; Yang, J.H.; Park, J.Y. The relationship between technology, business model, and market in autonomous car and intelligent robot industries. Technol. Forecast. Soc. Chang. 2016, 103, 142–155. [Google Scholar] [CrossRef]

- Morkunas, V.J.; Paschen, J.; Boon, E. How blockchain technologies impact your business model. Bus. Horiz. 2019, 62, 295–306. [Google Scholar] [CrossRef]

- Behera, P.; Sethi, N. Nexus between environment regulation, FDI, and green technology innovation in OECD countries. Environ. Sci. Pollut. Res. 2022, 29, 52940–52953. [Google Scholar] [CrossRef] [PubMed]

- Hassani, H.; Huang, X.; Silva, E. Banking with blockchain-ed big data. J. Manag. Anal. 2018, 5, 256–275. [Google Scholar] [CrossRef]

- Jena, R.K. Examining the Factors Affecting the Adoption of Blockchain Technology in the Banking Sector: An Extended UTAUT Model. Int. J. Financ. Stud. 2022, 10, 90. [Google Scholar] [CrossRef]

- Demmou, L.; Sagot, Q. Central Bank Digital Currencies and payments: A review of domestic and international implications. OECD Econ. Dep. Work. Pap. 2021. [Google Scholar] [CrossRef]

- Armas, A.; Ruiz, L.; Vásquez, J.L. Assessing CBDC potential for developing payment systems and promoting financial inclusion in Peru. BIS Pap. Chapters 2022, 123, 131–151. [Google Scholar]

- Davoodalhosseini, S.M. Central bank digital currency and monetary policy. J. Econ. Dyn. Control 2022, 142, 104150. [Google Scholar] [CrossRef]

- Remittance Prices Worldwide Quarterly. 2023. Available online: https://remittanceprices.worldbank.org/ (accessed on 15 June 2023).

- Helmi, M.H.; Çatık, A.N.; Akdeniz, C. The impact of central bank digital currency news on the stock and cryptocurrency markets: Evidence from the TVP-VAR model. Res. Int. Bus. Financ. 2023, 65, 101968. [Google Scholar] [CrossRef]

- Wang, Y.; Wei, Y.; Lucey, B.M.; Su, Y. Return spillover analysis across central bank digital currency attention and cryptocurrency markets. Res. Int. Bus. Financ. 2023, 64, 101896. [Google Scholar] [CrossRef]

- Ayadi, A.; Ghabri, Y.; Guesmi, K. Directional predictability from central bank digital currency to cryptocurrencies and stablecoins. Res. Int. Bus. Financ. 2023, 65, 101909. [Google Scholar] [CrossRef]

- Kuehnlenz, S.; Orsi, B.; Kaltenbrunner, A. Central bank digital currencies and the international payment system: The demise of the US dollar? Res. Int. Bus. Financ. 2023, 64, 101834. [Google Scholar] [CrossRef]

- Gupta, S.; Pandey, D.K.; El Ammari, A.; Sahu, G.P. Do perceived risks and benefits impact trust and willingness to adopt CBDCs? Res. Int. Bus. Financ. 2023, 66, 101993. [Google Scholar] [CrossRef]

- Tian, S.; Zhao, B.; Olivares, R.O. Cybersecurity risks and central banks’ sentiment on central bank digital currency: Evidence from global cyberattacks. Financ. Res. Lett. 2023, 53, 103609. [Google Scholar] [CrossRef]

- Ngo, V.M.; Van Nguyen, P.; Nguyen, H.H.; Tram, H.X.T.; Hoang, L.C. Governance and monetary policy impacts on public acceptance of CBDC adoption. Res. Int. Bus. Financ. 2023, 64, 101865. [Google Scholar] [CrossRef]

- Li, J. Predicting the demand for central bank digital currency: A structural analysis with survey data. J. Monet. Econ. 2023, 134, 73–85. [Google Scholar] [CrossRef]

- Li, F.; Yang, T.; Du, M.; Huang, M. The development fit index of digital currency electronic payment between China and the one belt one road countries. Res. Int. Bus. Financ. 2023, 64, 101838. [Google Scholar] [CrossRef]

- Rehman, M.A.; Irfan, M.; Naeem, M.A.; Lucey, B.M.; Karim, S. Macro-financial implications of central bank digital currencies. Res. Int. Bus. Financ. 2023, 64, 101892. [Google Scholar] [CrossRef]

- Jabbar, A.; Geebren, A.; Hussain, Z.; Dani, S. Ul-Durar. Investigating individual privacy within CBDC: A privacy calculus perspective. Res. Int. Bus. Financ. 2023, 64, 101826. [Google Scholar] [CrossRef]

- Sethaput, V.; Innet, S. Blockchain application for central bank digital currencies (CBDC). Cluster Comput. 2023, 26, 2183–2197. [Google Scholar] [CrossRef]

- The World Bank. Financial Inclusion on the Rise, but Gaps Remain, Global Findex Database Shows; World Bank: Washington, DC, USA, 2018. [Google Scholar]

- Soilen, K.S.; Benhayoun, L. Household acceptance of central bank digital currency: The role of institutional trust. Int. J. Bank Mark. 2022, 40, 172–196. [Google Scholar] [CrossRef]

- Xin, B.; Jiang, K. Central bank digital currency and the effectiveness of negative interest rate policy: A DSGE analysis. Res. Int. Bus. Financ. 2023, 64, 101901. [Google Scholar] [CrossRef]

- Scarcella, L. The implications of adopting a European Central Bank Digital Currency: A Tax Policy Perspective. EC TAX Rev. 2021, 30, 177–188. [Google Scholar] [CrossRef]

- Radic, A.; Quan, W.; Koo, B.; Chua, B.-L.; Kim, J.J.; Han, H. Central bank digital currency as a payment method for tourists: Application of the theory of planned behavior to digital Yuan/Won/Dollar choice. J. Travel\Tour. Mark. 2022, 39, 152–172. [Google Scholar] [CrossRef]

- Roussou, I.; Stiakakis, E.; Sifaleras, A. An empirical study on the commercial adoption of digital currencies. Inf. Syst. E-Bus. Manag. 2019, 17, 223–259. [Google Scholar] [CrossRef]

- Alfar, A.J.K.; Kumpamool, C.; Nguyen, D.T.K.; Ahmed, R. The determinants of issuing central bank digital currencies. Res. Int. Bus. Financ. 2023, 64, 101884. [Google Scholar] [CrossRef]

- Koziuk, V. Confidence in digital money: Are central banks more trusted than age is matter? Investig. Manag. Financ. Innov. 2021, 18, 12–32. [Google Scholar] [CrossRef]

- Afonasova, M.A.; Panfilova, E.E.; Galichkina, M.A.; Ślusarczyk, B. Digitalization in economy and innovation: The effect on social and economic processes. Polish J. Manag. Stud. 2019, 19, 22–32. [Google Scholar] [CrossRef]

- World Economic Forum. The Global Information Technology Report. Available online: http://reports.weforum.org/global-information-technology-report-2016/ (accessed on 22 July 2023).

- Venter, I.M.; Cranfield, D.J.; Tick, A.; Blignaut, R.J.; Renaud, K.V. ‘Lockdown’: Digital and Emergency eLearning Technologies—A Student Perspective. Electronics 2022, 11, 2941. [Google Scholar] [CrossRef]

- Filho, W.L.; Vidal, D.G.; Chen, C.; Petrova, M.; Dinis, M.A.P.; Yang, P.; Rogers, S.; Álvarez-Castañón, L.; Djekic, I.; Sharifi, A.; et al. An assessment of requirements in investments, new technologies, and infrastructures to achieve the SDGs. Environ. Sci. Eur. 2022, 34, 58. [Google Scholar] [CrossRef]

- Alonso, S.L.N.; Jorge-Vazquez, J.; Forradellas, R.F.R. Detection of Financial Inclusion Vulnerable Rural Areas through an Access to Cash Index: Solutions Based on the Pharmacy Network and a CBDC. Evidence Based on Ávila (Spain). Sustainability 2020, 12, 7480. [Google Scholar] [CrossRef]

- Abbott, P.; Andersen, T.B.; Tarp, F. IMF and economic reform in developing countries. Q. Rev. Econ. Financ. 2010, 50, 17–26. [Google Scholar] [CrossRef]

- Levesque, B.; Godfrey, N.; Miller, M.; Stark, E. The Case for Financial Literacy in Developing Countries: Promoting Access to Finance by Empowering Consumers; World Bank: Washington, DC, USA, 2009. [Google Scholar]

- Ozili, P.K. CBDC, Fintech and cryptocurrency for financial inclusion and financial stability. Digit. Policy Regul. Gov. 2023, 25, 40–57. [Google Scholar] [CrossRef]

- Banerjee, S.; Sinha, M. Promoting Financial Inclusion through Central Bank Digital Currency: An Evaluation of Payment System Viability in India. Australas. Account. Bus. Financ. J. 2023, 17, 176–204. [Google Scholar] [CrossRef]

- Yang, Q.; Zheng, M.; Wang, Y. The Role of CBDC in Green Finance and Sustainable Development. Emerg. Mark. Financ. Trade 2023, 1–16. [Google Scholar] [CrossRef]

- Ozili, P.K. Using Central Bank Digital Currency to Achieve the Sustainable Development Goals. SSRN Electron. J. 2023, 111C, 143–153. [Google Scholar] [CrossRef]

- Rose-Ackerman, S.; Palifka, B.J. Corruption, Organized Crime, and Money Laundering. In Institutions, Governance and the Control of Corruption; Springer International Publishing: Cham, Switzerland, 2018; pp. 75–111. [Google Scholar]

- Atako, N. Privacy Beyond Possession: Solving the Access Conundrum in Digital Dollars. Vanderbilt J. Entertain. Technol. Law 2020, 23, 821. [Google Scholar]

- Zulfikri, Z.; Sa’ad, A.A.; Kassim, S.; Othman, A.H.A. Feasibility of Central Bank Digital Currency for Blockchain-Based Zakat in Indonesia. In Innovation of Businesses, and Digitalization during COVID-19 Pandemic. ICBT 2021; Lecture Notes in Networks and Systems; Springer: Cham, Switzerland, 2023; Volume 488. [Google Scholar] [CrossRef]

- Sarker, S.; Henningsson, S.; Jensen, T.; Hedman, J. Use Of Blockchain As A Resource For Combating Corruption in Global Shipping: An Interpretive Case Study. J. Manag. Inf. Syst. 2021, 38, 338–373. [Google Scholar] [CrossRef]

- Lee, D.K.C.; Yan, L.; Wang, Y. A global perspective on central bank digital currency. China Econ. J. 2021, 14, 52–66. [Google Scholar] [CrossRef]

- Dupuis, D.; Gleason, K.; Wang, Z. Money laundering in a CBDC world: A game of cats and mice. J. Financ. Crime 2022, 29, 171–184. [Google Scholar] [CrossRef]

- Abu, N.A. Keynote Paper Digital Ringgit: A New Digital Currency with Traditional Attributes. In Proceedings of the 8th International Cryptology and Information Security Conference, Putrajaya, Malaysia, 26–28 July 2022. [Google Scholar]

- Elsayed, A.H.; Nasir, M.A. Central bank digital currencies: An agenda for future research. Res. Int. Bus. Financ. 2022, 62, 101736. [Google Scholar] [CrossRef]

- Comin, D.; Hobijn, B. Cross-country technology adoption: Making the theories face the facts. J. Monet. Econ. 2004, 51, 39–83. [Google Scholar] [CrossRef]

- Milner, H.V. The Digital Divide. Comp. Polit. Stud. 2006, 39, 176–199. [Google Scholar] [CrossRef]

- Acemoglu, D. Patterns of Skill Premia. Rev. Econ. Stud. 2003, 70, 199–230. [Google Scholar] [CrossRef]

- de Vanssay, X.; Spindler, Z.A. Freedom and growth: Do constitutions matter? Public Choice 1994, 78, 359–372. [Google Scholar] [CrossRef]

- La Porta, R.; Lopez-De-Silanes, F.; Shleifer, A.; Vishny, R.W. Legal Determinants of External Finance. J. Financ. 1997, 52, 1131–1150. [Google Scholar] [CrossRef]

- de Haan, J.; Sturm, J.-E. On the relationship between economic freedom and economic growth. Eur. J. Polit. Econ. 2000, 16, 215–241. [Google Scholar] [CrossRef]

- Levine, R.; Loayza, N.; Beck, T. Financial intermediation and growth: Causality and causes. J. Monet. Econ. 2000, 46, 31–77. [Google Scholar] [CrossRef]

- Ricci, P. How economic freedom reflects on the Bitcoin transaction network. J. Ind. Bus. Econ. 2020, 47, 133–161. [Google Scholar] [CrossRef]

- Tatar, U.; Gokce, Y.; Nussbaum, B. Law versus technology: Blockchain, GDPR, and tough tradeoffs. Comput. Law Secur. Rev. 2020, 38, 105454. [Google Scholar] [CrossRef]

- Freund, G.P.; Fagundes, B.; de Macedo, D.D.J. An Analysis of Blockchain and GDPR under the Data Lifecycle Perspective. Mob. Netw. Appl. 2021, 26, 266–276. [Google Scholar] [CrossRef]

- Acemoglu, D. Technical Change, Inequality, and the Labor Market. J. Econ. Lit. 2002, 40, 7–72. [Google Scholar] [CrossRef]

- Aghion, P.; Howitt, P.; Violante, G.L. General Purpose Technology and Wage Inequality. J. Econ. Growth 2002, 7, 315–345. [Google Scholar] [CrossRef]

- Jaumotte, F.; Lall, S.; Papageorgiou, C. Rising Income Inequality: Technology, or Trade and Financial Globalization? IMF Econ. Rev. 2013, 61, 271–309. [Google Scholar] [CrossRef]

- Novak, M. The implications of blockchain for income inequality. In Blockchain Economics: Implications of Distributed Ledgers-Markets, Communications Networks, and Algorithmic Reality; World Scientific: Singapore, 2019. [Google Scholar]

- Lee, J.-W. Education for Technology Readiness: Prospects for Developing Countries. J. Hum. Dev. 2001, 2, 115–151. [Google Scholar] [CrossRef]

- Andriyani, K.; Marwa, T.; Adnan, N.; Muizzuddin, M. The Determinants of Foreign Exchange Reserves: Evidence from Indonesia. J. Asian Financ. Econ. Bus. 2020, 7, 629–636. [Google Scholar] [CrossRef]

- Ahmad, I.; Azam, A.; Mehmood, K.A.; Faridi, M.Z.; Aurmaghan, M. Vulnerabilities of Developing Countries to Foreign Exchange Reserves and Remittances: A Case Study of Pakistan economy. Int. J. Manag. 2020, 11, 646–659. [Google Scholar]

- CBDC Tracker. Available online: https://cbdctracker.org/timeline (accessed on 15 June 2023).

- Human Development Index. Available online: https://hdr.undp.org/data-center/human-development-index#/indicies/HDI (accessed on 15 June 2023).

- Network Readiness Index. Available online: https://networkreadinessindex.org/ (accessed on 15 June 2023).

- Sustainable Development Goal Rank. Available online: https://dashboards.sdgindex.org/ (accessed on 15 June 2023).

- Sachs, J.D.; Lafortune, G.; Fuller, G.; Drumm, E. Implementing the SDG Stimulus. In Sustainable Development Report 2023; Sustainable Development Solutions Network: Paris, France, 2023. [Google Scholar] [CrossRef]

- Gini Coefficient by Country. 2023. Available online: https://worldpopulationreview.com/ (accessed on 15 June 2023).

- GDP per Capita. Available online: https://www.worldbank.org/en/home (accessed on 15 June 2023).

- Foreign Currency Reserve per Capita. Available online: https://www.nationmaster.com/ (accessed on 15 June 2023).

- Democracy Index. Available online: https://www.eiu.com/n/ (accessed on 15 June 2023).

- Corruption Perception Index. Available online: https://www.transparency.org.uk/ (accessed on 15 June 2023).

- World Governance Indicators. Available online: https://info.worldbank.org/governance/wgi/Home/Reports (accessed on 15 June 2023).

- Economic Freedom. Available online: https://indexdotnet.azurewebsites.net/index (accessed on 15 June 2023).

- Riksbank, S. The Riksbank’s E-Krona Project. 2017. Available online: https://www.riksbank.se/en-gb/payments--cash/e-krona/e-krona-reports/e-krona-project-report-1/ (accessed on 15 June 2023).

- Centobelli, P.; Cerchione, R.; Esposito, E. Pursuing supply chain sustainable development goals through the adoption of green practices and enabling technologies: A cross-country analysis of LSPs. Technol. Forecast. Soc. Change 2020, 153, 119920. [Google Scholar] [CrossRef]

- Shahzad, U.; Radulescu, M.; Rahim, S.; Isik, C.; Yousaf, Z.; Ionescu, S. Do Environment-Related Policy Instruments and Technologies Facilitate Renewable Energy Generation? Exploring the Contextual Evidence from Developed Economies. Energies 2021, 14, 690. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Themes | Studied | References |

|---|---|---|

| Individuals and public adoption | Individuals and public perception of CBDCs | [14,20,23,26] |

| Technological characteristics | How the design of CBDCs can benefit users and nations’ financial systems | [15,17,24,25] |

| Commercial adoption | Business perception of CBDCs | [27] |

| Country adoption | Macro-financial implications of CBDC adoption | [16,18,19,28] |

| Relation of CBDCs with crypto-assets | Directional predictability between CBDC shocks and CBDC attention index on cryptocurrencies | [10,11,12,29] |

| Variables | Label | Effect | |

|---|---|---|---|

| 1 | Network readiness index | NRI | Positive |

| 2 | Sustainable development goal rank | SDG | Positive |

| 3 | Corruption control | CC | Positive |

| 4 | Democracy level | DeM | Positive |

| 5 | Economic freedom | EF | Negative |

| 6 | Income inequality | GiC | Negative |

| 7 | Foreign reserve | RiS | Positive |

| 8 | Human development index | HDI | Positive |

| 9 | Regulatory quality | RQ | Negative |

| 10 | Corruption perception index | CPI | Positive |

| 11 | Country CBDC adoption status | STA | Dependent Variable |

| Index | Value | Interpretation |

|---|---|---|

| Average path coefficient (APC) | APC = 0.158, p = 0.044 | |

| Average R-squared (ARS) | ARS = 0.052, p = 0.167 | |

| Average adjusted R-squared (AARS) | AARS = −0.118, p = 0.080 | |

| Average block VIF (AVIF) | AVIF = 3.316 | Acceptable if ≤ 5, ideally ≤ 3.3 |

| Average full collinearity VIF (AFVIF) | AFVIF = 5.444 | Acceptable if ≤ 5, ideally ≤ 3.3 |

| Tenenhaus GoF (GoF) | GoF = 0.227 | Small ≥ 0.1, medium ≥ 0.25, large ≥ 0.36 |

| Simpson’s paradox ratio (SPR) | SPR = 0.700 | Acceptable if ≥ 0.7, ideally = 1 |

| R-squared contribution ratio (RSCR) | RSCR = 0.585 | Acceptable if ≥ 0.9, ideally = 1 |

| Statistical suppression ratio (SSR) | SSR = 0.800 | Acceptable if ≥ 0.7 |

| Nonlinear bivariate causality direction ratio (NLBCDR) | NLBCDR = 0.400 | Acceptable if ≥ 0.7 |

| Result | |||

|---|---|---|---|

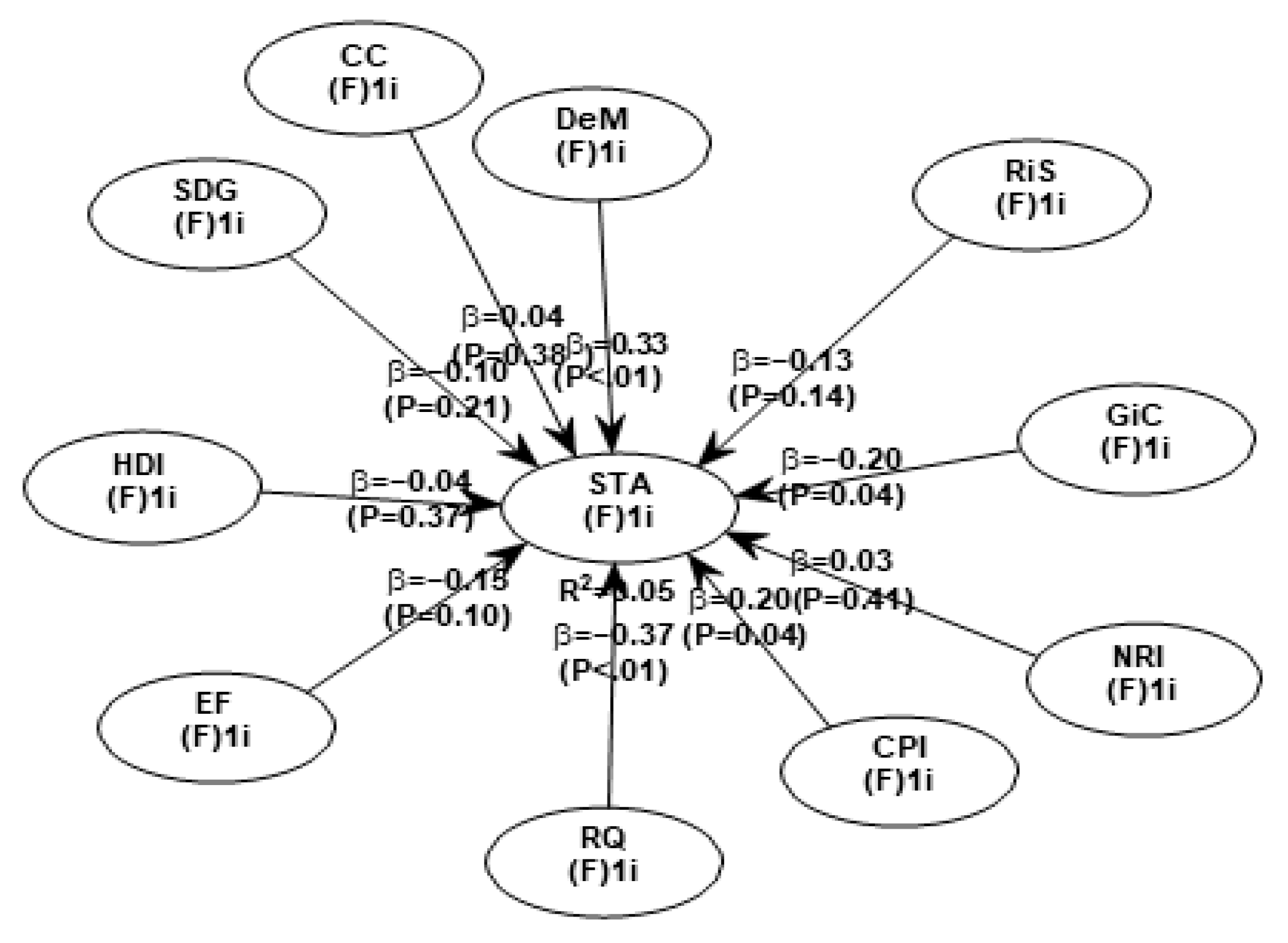

| H1 | Network readiness → Adoption status of CBDCs | (β = 0.03, p = 0.41) | Reject |

| H2 | Sustainable development goals → Adoption status of CBDCs | (β = −0.10, p = 0.21) | Reject |

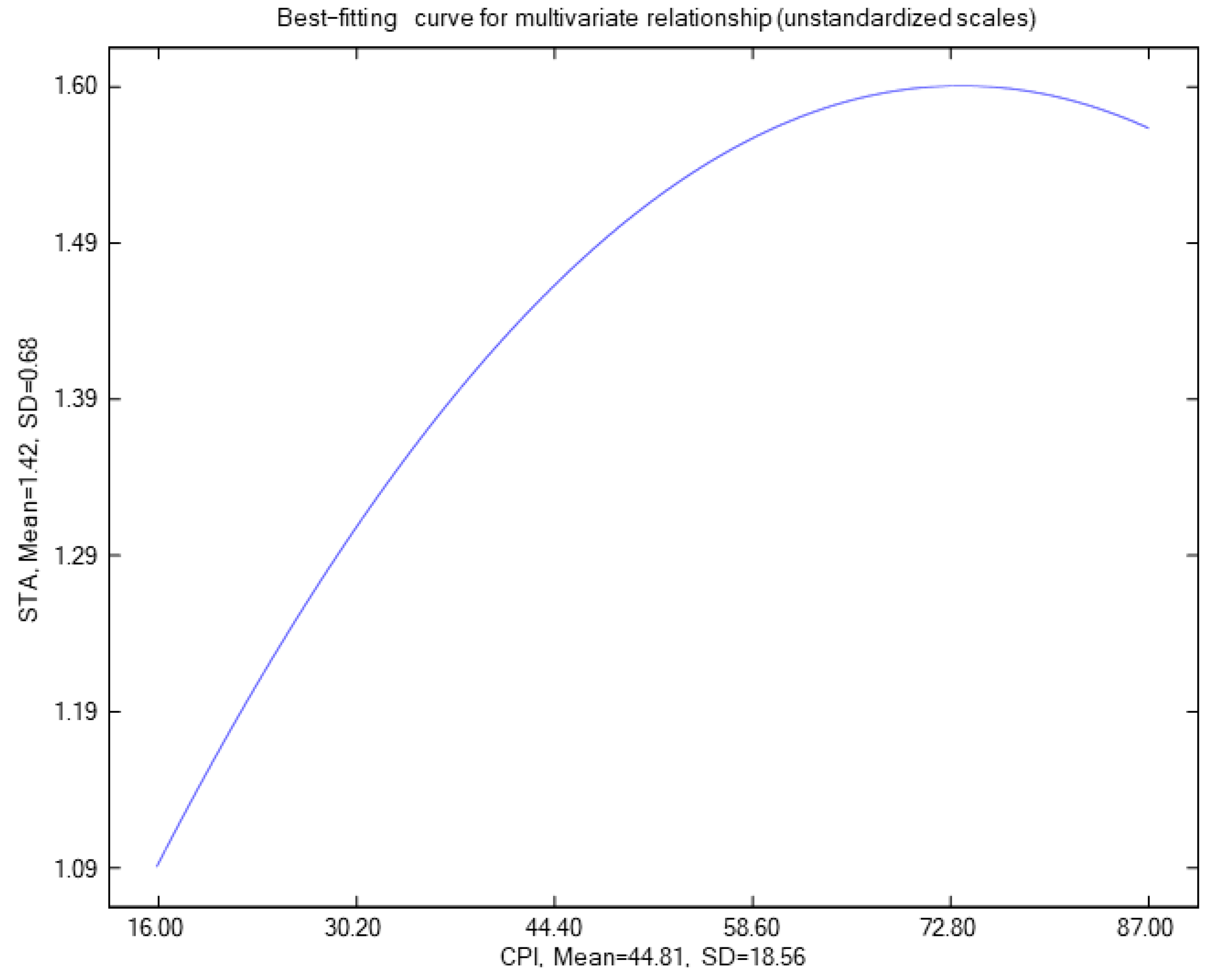

| H3 | Corruption perception → Adoption status of CBDCs | (β = 0.20, p = 0.04) | Pass |

| H4 | Corruption control → Adoption status of CBDCs | (β = 0.04, p = 0.38) | Reject |

| H5 | Democracy level → Adoption status of CBDCs | (β = 0.33, p < 0.01) | Pass |

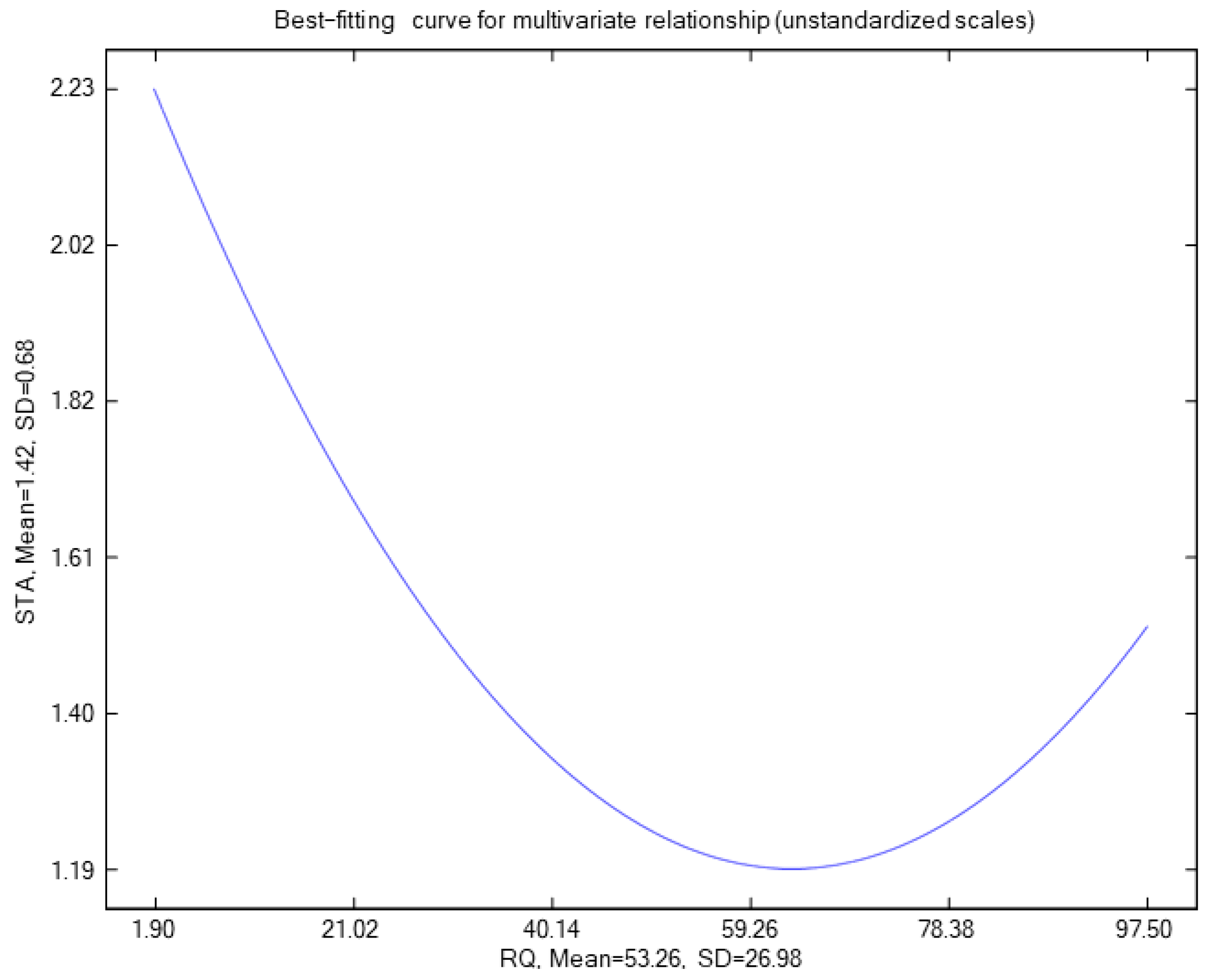

| H6 | Regulatory quality → Adoption status of CBDCs | (β = −0.37, p < 0.01) | Pass |

| H7 | Economic freedom → Adoption status of CBDCs | (β = −0.15, p < 0.10) | Reject |

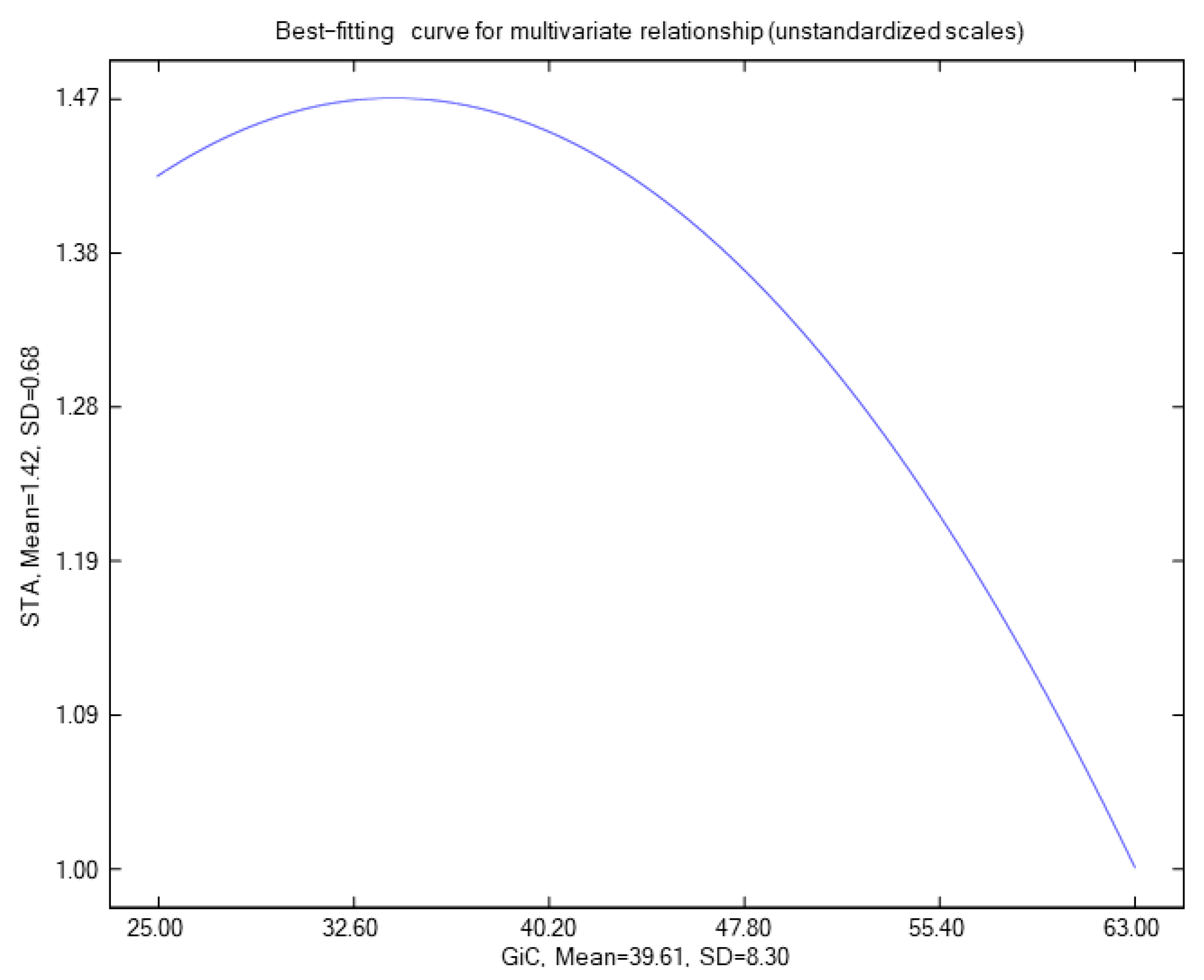

| H8 | Gini coefficient → Adoption status of CBDCs | (β = −0.20, p = 0.04) | Pass |

| H9 | Human development → Adoption status of CBDCs | (β = −0.04, p = 0.37) | Reject |

| H10 | Foreign currency reserve →Adoption status of CBDCs | (β = −0.13, p = 0.14) | Reject |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mohammed, M.A.; De-Pablos-Heredero, C.; Montes Botella, J.L. Exploring the Factors Affecting Countries’ Adoption of Blockchain-Enabled Central Bank Digital Currencies. Future Internet 2023, 15, 321. https://doi.org/10.3390/fi15100321

Mohammed MA, De-Pablos-Heredero C, Montes Botella JL. Exploring the Factors Affecting Countries’ Adoption of Blockchain-Enabled Central Bank Digital Currencies. Future Internet. 2023; 15(10):321. https://doi.org/10.3390/fi15100321

Chicago/Turabian StyleMohammed, Medina Ayta, Carmen De-Pablos-Heredero, and José Luis Montes Botella. 2023. "Exploring the Factors Affecting Countries’ Adoption of Blockchain-Enabled Central Bank Digital Currencies" Future Internet 15, no. 10: 321. https://doi.org/10.3390/fi15100321

APA StyleMohammed, M. A., De-Pablos-Heredero, C., & Montes Botella, J. L. (2023). Exploring the Factors Affecting Countries’ Adoption of Blockchain-Enabled Central Bank Digital Currencies. Future Internet, 15(10), 321. https://doi.org/10.3390/fi15100321