Financial Eco-Innovation as a Mechanism for Fostering the Development of Sustainable Infrastructure Systems

Abstract

:1. Introduction

2. Theoretical Background

3. Public-Private Partnerships and Project Finance to Develop Sustainable Infrastructure Systems Results

4. Proposed Framework

5. Trends and Research Topics

- (1)

- Proposes the optimal incorporation of new projects within the investment vehicle;

- (2)

- Conceives PF as a subset of the syndicated loan market;

- (3)

- Addresses the relation between the use of financial contracts, business risk management, and financial decision-making; and

- (4)

- Analyses PPPs compared to traditional public procurement mechanisms where the use of PF as a financing technique is frequently associated.

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Georgoulias, A.; Vidaurre-Roche, A.-M.; Rodríguez, J. Sustainable Infrastructure in Latin America: Infrastructure 360° Award. 2014. Available online: http://research.gsd.harvard.edu/wpcontent/uploads/2015/04/INF_360o_Awards_Bilingual_Publication.pdf (accessed on 3 September 2017).

- Clark, R.; Reed, J.; Sunderland, T. Bridging funding gaps for climate and sustainable development: Pitfalls, progress and potential of private finance. Land Use Policy 2018, 71, 335–346. [Google Scholar] [CrossRef]

- Cui, L.; Huang, Y. Exploring the Schemes for Green Climate Fund Financing: International Lessons. World Dev. 2018, 101, 173–187. [Google Scholar] [CrossRef]

- The Johnson Foundation. Financing Sustainable Water Infrastructure. 2012. Available online: http://www.johnsonfdn.org/sites/default/files/reports_publications/WaterInfrastructure.pdf (accessed on 5 September 2018).

- Andersen, M.M. Organising interfirm learning e as the market begins to turn Green. In Partnership and Leadership—Building Alliances for a Sustainable Future; de Bruijn, T.J.N.M., Tukker, A., Eds.; Kluwer Academic Publishers: Dordrecht, The Netherlands, 2002; pp. 103–119. [Google Scholar]

- Arundel, A.; Kemp, R. Measuring Eco-Innovation. 2009. UNU-MERIT Working Papers (Vol. #2009-017). Available online: http://collections.unu.edu/eserv/UNU:324/wp2009-017.pdf (accessed on 5 September 2017).

- Esty, B. Why Study Large Projects? An Introduction to Research on Project Finance. Eur. Financ. Manag. 2004, 10, 213–224. [Google Scholar] [CrossRef]

- Farquharson, E.; de Mästle, C.T.; Yescombe, E.R.; Encinas, J. How to Engage with the Private Sector in Public-Private Partnerships in Emerging Markets, 1st ed.; World Bank: Washington, DC, USA, 2011; ISBN 978-0-8213-7863-2. [Google Scholar] [CrossRef]

- Gatti, S. Project Finance in Theory and Practice: Designing, Structuring, and Financing Private and Public Projects. In Project Finance in Theory and Practice, 3rd ed.; Elsevier, Academic Press: London, UK, 2018; ISBN 978-0-12-39146-5. [Google Scholar]

- Yescombe, E.R. Public-Private Partnerships: Principles of Policy and Finance; Butterworth-Heinemann: Oxford, UK, 2007; ISBN 978-0-08-048957-5. [Google Scholar]

- Jefferies, M.; McGeorge, W. Using public-private partnerships (PPPs) to procure social infrastructure in Australia. Eng. Constr. Archit. Manag. 2009, 16, 415–437. [Google Scholar] [CrossRef]

- González-Ruiz, J.D.; Duque, E.A.; Arango, L. Project Finance y Capital Riesgo: Aplicación en la financiación de proyectos de infraestructura. In Finanzas y Modelación; Primera, F.I., Ed.; Universidad de Medellín: Medellín, Colombia, 2014; pp. 91–119. ISBN 978-958-8815-84-8. [Google Scholar]

- Hueskes, M.; Verhoest, K.; Block, T. Governing public-private partnerships for sustainability: An analysis of procurement and governance practices of PPP infrastructure projects. Int. J. Proj. Manag. 2017, 35, 1184–1195. [Google Scholar] [CrossRef]

- Cui, C.; Liu, Y.; Hope, A.; Wang, J. Review of studies on the public–private partnerships (PPP) for infrastructure projects. Int. J. Proj. Manag. 2018, 36, 773–794. [Google Scholar] [CrossRef]

- Wilson, C. Why should sustainable finance be given priority? Lessons from pollution and biodiversity degradation. Account. Res. J. 2010, 23, 267–280. [Google Scholar] [CrossRef]

- Schumpeter, J. Capitalism, Socialism and Democracy; Harper Row: New York, NY, USA, 1942. [Google Scholar]

- Karakaya, E.; Hidalgo, A.; Nuur, C. Diffusion of eco-innovations: A review. Renew. Sustain. Energy Rev. 2014, 33, 392–399. [Google Scholar] [CrossRef]

- Mostafavi, A.; Abraham, D.; DeLaurentis, D. Toward Sustainable Financial Innovation Policies in Infrastructure: A Framework for Ex-Ante Analysis. Comput. Civ. Eng. 2011, 41–50. [Google Scholar] [CrossRef]

- Tan, Y.; Shen, L.; Yao, H. Sustainable construction practice and contractors’ competitiveness: A preliminary study. Habitat Int. 2011. [CrossRef]

- Wu, G.; Qiang, G.; Zuo, J.; Zhao, X.; Chang, R. What are the Key Indicators of Mega Sustainable Construction Projects?—A Stakeholder-Network Perspective. Sustainability 2018, 10, 2939. [Google Scholar] [CrossRef]

- Zhang, X. Financial Viability Analysis and Capital Structure Optimization in Privatized Public Infrastructure Projects. J. Constr. Eng. Manag. 2005, 131, 656–668. [Google Scholar] [CrossRef]

- Boons, F.; Wagner, M. Assessing the relationship between economic and ecological performance: Distinguishing system levels and the role of innovation. Ecol. Econ. 2009, 68, 1908–1914. [Google Scholar] [CrossRef]

- Przychodzen, J.; Przychodzen, W. Relationships between eco-innovation and financial performance—Evidence from publicly traded companies in Poland and Hungary. J. Clean. Prod. 2015, 90, 253–263. [Google Scholar] [CrossRef]

- Waltman, L. A review of the literature on citation impact indicators. J. Informetr. 2016, 10, 365–391. [Google Scholar] [CrossRef] [Green Version]

- Krajangsri, T.; Pongpeng, J. Effect of Sustainable Infrastructure Assessments on Construction Project Success Using Structural Equation Modeling. J. Manag. Eng. 2016, 33, 1–12. [Google Scholar] [CrossRef]

- Egler, H.-P.; Frazao, R. Sustainable Infrastructure and Finance—How to Contribute to a Sustainable Future. 2016. Available online: http://unepinquiry.org/wp-content/uploads/2016/06/Sustainable_Infrastructure_and_Finance.pdf (accessed on 10 October 2017).

- Mostafavi, A.; Abraham, D.; Mannering, F.; Vives, A.; Valentin, V. Assessment of Public Perceptions of Innovative Financing for Infrastructure. Constr. Res. Congr. 2012, 2260–2269. [Google Scholar] [CrossRef]

- Fabozzi, F.J. Accessing Capital Markets through Securitization; Wiley: Oxford, UK, 2001; ISBN 978-1-883-24992-2. [Google Scholar]

- Blanch, J. Financial Innovations and their role in the modern financial systems—Identitication and systematization of the problem. Financ. Internet Q. e-Finanse 2011, 7, 13–26. Available online: http://hdl.handle.net/10419/66758 (accessed on 3 September 2017).

- Dalberg. Innovative Financing for Development: Scalable Business Models that Produce Economic, Social, and Environmental. 2014. Available online: http://globaldevincubator.org/wp-content/uploads/2014/09/Innovative-Financing-for-Development.pdf (accessed on 3 September 2017).

- Ozusaglam, S. Environmental innovation: A concise review of the literature. Vie Sci. l’entreprise 2012, 191–192, 15. [Google Scholar] [CrossRef]

- Cui, Y.; Geobey, S.; Weber, O.; Lin, H. The Impact of Green Lending on Credit Risk in China. Sustainability 2018, 10, 2008. [Google Scholar] [CrossRef]

- Faber, A.; Frenken, K. Models in evolutionary economics and environmental policy: Towards an evolutionary environmental economics. Technol. Forecast. Soc. Chang. 2009, 76, 462–470. [Google Scholar] [CrossRef]

- Carrillo-Hermosilla, J.; del Río, P.; Könnölä, T. Diversity of eco-innovations: Reflections from selected case studies. J. Clean. Prod. 2010, 18, 1073–1083. [Google Scholar] [CrossRef]

- Hojnik, J.; Ruzzier, M. What drives eco-innovation? A review of an emerging literature. Environ. Innov. Soc. Transit. 2016, 19, 31–41. [Google Scholar] [CrossRef]

- Schiederig, T.; Tietze, F.; Herstatt, C. Green innovation in technology and innovation management—An exploratory literature review. R&D Manag. 2012, 42, 180–192. [Google Scholar] [CrossRef]

- Rennings, K. Redefining innovation—Eco-innovation research and the contribution from ecological economics. Ecol. Econ. 2000, 32, 319–332. [Google Scholar] [CrossRef]

- Little, A.D. How Leading Companies Are Using Sustainability-Driven Innovation to Win Tomorrow’s Customers; World Business Council for Sustainab le Development (WBCSD): Geneva, Switzerland, 2005. [Google Scholar]

- Porter, M.E.; van der Linde, C. Toward a New Conception of the Environment-Competitiveness Relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef] [Green Version]

- Yang, F.; Yang, M. Analysis on China’s eco-innovations: Regulation context, intertemporal change and regional differences. Eur. J. Oper. Res. 2015, 247, 1003–1012. [Google Scholar] [CrossRef]

- Polzin, F.; von Flotow, P.; Klerkx, L. Addressing barriers to eco-innovation: Exploring the finance mobilisation functions of institutional innovation intermediaries. Technol. Forecast. Soc. Chang. 2016, 103, 34–46. [Google Scholar] [CrossRef]

- King, A.A.; Lenox, M.J. Does It Really Pay to Be Green? An Empirical Study of Firm Environmental and Financial Performance. J. Ind. Ecol. 2001, 5, 105–116. Available online: http://mitpress.mit.edu/JIE (accessed on 5 September 2017). [CrossRef]

- Renneboog, L.; Ter, J.; Zhang, C. Socially responsible investments: Institutional aspects, performance, and investor behavior. J. Bank. Financ. 2008, 32, 1723–1742. [Google Scholar] [CrossRef]

- Linnenluecke, M.K.; Chen, X.; Ling, X.; Smith, T.; Zhu, Y. Emerging trends in Asia-Pacific finance research: A review of recent influential publications and a research agenda. Pac. Basin Financ. J. 2016, 36, 66–76. [Google Scholar] [CrossRef] [Green Version]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Does it really pay to be green? Determinants and consequences of proactive environmental strategies. J. Account. Public Policy 2011, 30, 122–144. [Google Scholar] [CrossRef]

- Govindan, K.; Diabat, A.; Madan, K. Analyzing the drivers of green manufacturing with fuzzy approach. J. Clean. Prod. 2015, 96, 182–193. [Google Scholar] [CrossRef]

- Bolton, B. Sustainable Financial Invesment. Maximizing Corporate Profits and Long-Term Economic Value Creation, 1st ed.; Palgrave Macmillan: New York, NY, USA, 2015; ISBN 978-1-137-41199-0. [Google Scholar]

- Fatemi, A.M.; Fooladi, I.J. Sustainable finance: A new paradigm. Glob. Financ. J. 2013, 24, 101–113. [Google Scholar] [CrossRef]

- Martens, M.L.; Carvalho, M.M. Key factors of sustainability in project management context: A survey exploring the project managers’ perspective. Int. J. Proj. Manag. 2016, 2016, 1–19. [Google Scholar] [CrossRef]

- Meltzer, J.P. Financing Low Carbon, Climate Resilient in Frastructure: The Role of Climate Finance and Green Financial Systems. 2016. Available online: https://ssrn.com/abstract=2841918 (accessed on 26 November 2018). [CrossRef]

- Elkington, J. Cannibals with Forks: The Triple Bottom Line of 21st Century Business, 6th ed.; New Society Publishers: Gabriola, BC, Canada, 1998. [Google Scholar]

- Foxon, T.J.; Bale, C.S.E.; Busch, J.; Bush, R.; Hall, S.; Roelich, K. Low carbon infrastructure investment: Extending business models for sustainability. Infrastruct. Complex. 2015, 2, 4. [Google Scholar] [CrossRef]

- Rizzi, F.; Pellegrini, C.; Battaglia, M. The structuring of social finance: Emerging approaches for supporting environmentally and socially impactful projects. J. Clean. Prod. 2018, 170, 805–817. [Google Scholar] [CrossRef]

- Kivleniece, I.; Quelin, B.V. Creating and Capturing Value in Public-Private Ties: A Private Actor’s Perspective. Acad. Manag. Rev. 2012, 37, 272–299. [Google Scholar] [CrossRef]

- Laszlo, C. The Sustainable Company: How to Create Lasting Value through Social and Environmental Performance; Island Press: Washington, DC, USA, 2003. [Google Scholar]

- Gupta, R.; Morris, J.W.F.; Espinoza, D. Financial Sustainability as a Metric for Infrastructure Projects. In Proceedings of the Geo-Chicago 2016, Chicago, IL, USA, 14–18 August 2016; pp. 653–662. [Google Scholar] [CrossRef]

- González-Ruiz, J.D.; Arboleda, C.; Botero, S. A Proposal for Green Financing as a Mechanism to Increase Private Participation in Resilient Water Infrastructure Systems: The Colombian Case. Procedia Eng. 2016, 145, 180–187. [Google Scholar] [CrossRef]

- Gollier, C. Pricing the Planet’s Future: The Economics of Discounting in an Uncertain World; Princeton University Press: Princeton, NJ, USA, 2013; Available online: https://press.princeton.edu/titles/9894.html (accessed on 5 September 2017).

- García, E. Los Instrumentos Financieros Innovadores, una Alternativa Eficaz Combatir para el Cambio Climático—Noticias | iAgua. 2016. Available online: https://www.iagua.es/noticias/caf/16/09/23/instrumentos-financieros-innovadores-alternativa-eficaz-combatir-cambio (accessed on 10 October 2017).

- Kern, F.; Gaede, J.; Meadowcroft, J.; Watson, J. The political economy of carbon capture and storage: An analysis of two demonstration projects. Technol. Forecast. Soc. Chang. 2016, 102, 250–260. [Google Scholar] [CrossRef]

- Gherghina, Ş.; Onofrei, M.; Vintilă, G.; Armeanu, D. Empirical Evidence from EU-28 Countries on Resilient Transport Infrastructure Systems and Sustainable Economic Growth. Sustainability 2018, 10, 2900. [Google Scholar] [CrossRef]

- Marcus, A.; Malen, J.; Ellis, S. The Promise and Pitfalls of Venture Capital as an Asset Class for Clean Energy Investment: Research Questions for Organization and Natural Environment Scholars. Organ. Environ. 2013, 26, 31–60. [Google Scholar] [CrossRef]

- González-Ruiz, J.D.; Rojas, M.; Arboleda, C.; Botero, S. Project Finance y Asociaciones Público-Privada para la provisión de servicios de infraestructura en Colombia Introducción. Obras y Proy. 2014, 16, 61–82. [Google Scholar] [CrossRef]

- Foxon, T.; Pearson, P. Overcoming barriers to innovation and diffusion of cleaner technologies: Some features of a sustainable innovation policy regime. J. Clean. Prod. 2008, 16, S148–S161. [Google Scholar] [CrossRef]

- Czarnitzki, D.; Hanel, P.; Rosa, J.M. Evaluating the impact of R&D tax credits on innovation: A microeconometric study on Canadian firms. Res. Policy 2011, 40, 217–229. [Google Scholar] [CrossRef] [Green Version]

- Barbero, J.; Forteza, J.H.; Skerk, C.; Mejía, A.; Katz, R.; García, R.; Gómez, M. IDEAL 2014. La Infraestructura en el Desarrollo de América Latina (Main Document); CAF: Bogotá DC, Colombia, 2015; Available online: http://scioteca.caf.com/handle/123456789/746 (accessed on 7 October 2017).

- Mostafavi, A.; Abraham, D.; Vives, A. Exploratory analysis of public perceptions of innovative financing for infrastructure systems in the U.S. Transp. Res. Part A Policy Pract. 2014, 70, 10–23. [Google Scholar] [CrossRef]

- Weber, K.M.; Rohracher, H. Legitimizing research, technology and innovation policies for transformative change: Combining insights from innovation systems and multi-level perspective in a comprehensive ‘failures’ framework. Res. Policy 2012, 41, 1037–1047. [Google Scholar] [CrossRef]

- Haley, U.C.V.; Schuler, D.A. Government policy and firm strategy in the solar photovoltaic industry. Calif. Manag. Rev. 2011, 54, 17–38. [Google Scholar] [CrossRef]

- Hendry, C.; Harborne, P.; Brown, J. So what do innovating companies really get from publicly funded demonstration projects and trials? innovation lessons from solar photovoltaics and wind. Energy Policy 2010, 38, 4507–4519. [Google Scholar] [CrossRef]

- Pauw, W.P. Not a panacea: Private-sector engagement in adaptation and adaptation finance in developing countries. Clim. Policy 2015, 15, 583–603. [Google Scholar] [CrossRef]

- Lee, S.; Lee, B.; Kim, J.; Kim, J. A financing model to solve financial barriers for implementing green building projects. Sci. World J. 2013, 2013. [Google Scholar] [CrossRef] [PubMed]

- Ozorhon, B. Analysis of Construction Innovation Process at Project Level. J. Manag. Eng. 2013, 29, 455–463. [Google Scholar] [CrossRef]

- Leete, S.; Xu, J.; Wheeler, D. Investment barriers and incentives for marine renewable energy in the UK: An analysis of investor preferences. Energy Policy 2013, 60, 866–875. [Google Scholar] [CrossRef]

- Moore, M.-L.; Westley, F.R.; Nicholls, A. The Social Finance and Social Innovation Nexus. J. Soc. Entrep. 2012, 3, 115–132. [Google Scholar] [CrossRef]

- Bielenberg, A.; Kerlin, M.; Oppenheim, J.; Roberts, M. Financing Change: How to Mobilize Private-Sector Financing for Sustainable Infrastructure; Mckinsey & Company: Washington, DC, USA, 2016; Available online: http://newclimateeconomy.report/2015/wp-content/uploads/sites/3/2016/01/Financing_change_How_to_mobilize_private-sector_financing_for_sustainable-_infrastructure.pdf (accessed on 3 September 2017).

- Mostafavi, A.; Abraham, D.M.; Sinfield, J.V. Innovation in Infrastructure Project Finance: A Typology for Conceptualization. Int. J. Innov. Sci. 2014, 6, 127–144. [Google Scholar] [CrossRef]

- Kumari, A.; Sharma, A.K. Infrastructure financing and development: A bibliometric review. Int. J. Crit. Infrastruct. Prot. 2017, 16, 49–65. [Google Scholar] [CrossRef]

- Merk, O.; Saussier, S.; Staropoli, C.; Slack, E.; Kim, J. Financing Green Urban Infrastructure; OECD Publishing: Paris, France, 2012. [Google Scholar] [CrossRef]

- González-Ruiz, J.D.; Arboleda, C.A.; Botero, S. Financiación de Proyectos de Infraestructura Sostenible Bajo Asociaciones Público-Privadas: Caso Colombia. Red Iberoamericana de Ingeniería de Proyectos. Available online: https://scielo.conicyt.cl/scielo.php?pid=S0718-28132016000200005&script=sci_arttext (accessed on 26 November 2017).

- Pinz, A.; Roudyani, N.; Thaler, J. Public-private partnerships as instruments to achieve sustainability-related objectives: The state of the art and a research agenda. Public Manag. Rev. 2017, 20, 1–22. [Google Scholar] [CrossRef]

- Pérez-López, G.; Prior, D.; Zafra-Gómez, J.L. Rethinking New Public Management Delivery Forms and Efficiency: Long-Term Effects in Spanish Local Government: Table 1. J. Public Adm. Res. Theory 2015, 25, 1157–1183. [Google Scholar] [CrossRef]

- Teicher, J.; Alam, Q.; van Gramberg, B. Managing trust and relationships in PPPs: Some Australian experiences. Exp. Int. Rev. Adm. Sci. 2006, 72, 85–100. [Google Scholar] [CrossRef]

- Ponomarenko, T.V.; Cherepovitsyn, A.E.; Fedoseev, S.V.; Sidorov, D.E. Organizational-Economic Mechanism of Financing Strategic Investment Projects at the Regional Level in Regions with Poor Infrastructure. Int. J. Appl. Eng. Res. 2016, 11, 9007–9013. [Google Scholar]

- Anwar, B.; Xiao, Z.; Akter, S.; Rehman, R.-U. Sustainable Urbanization and Development Goals Strategy through Public-Private Partnerships in a South-Asian Metropolis. Sustainability 2017, 9, 1940. [Google Scholar] [CrossRef]

- Alonso-Conde, A.B.; Brown, C.; Rojo-Suarez, J. Public private partnerships: Incentives, risk transfer and real options. Rev. Financ. Econ. 2007, 16, 335–349. [Google Scholar] [CrossRef]

- Jin, X.-H.; Zhang, G. Modelling optimal risk allocation in PP projects using artificial neural networks. Int. J. Proj. Manag. 2011, 29, 591–603. [Google Scholar] [CrossRef]

- Zhang, Z.; Durango-Cohen, P. A strategic model of public-private partnerships in transportation: Effect of taxes and cost structure on investment viability. Res. Transp. Econ. 2012, 36, 9–18. [Google Scholar] [CrossRef]

- Carvalho, M.M.; Rabechini, R., Jr. Fundamentos em Gestão de Projetos: Construindo competências para gerenciar projetos: Teoria e Casos, 3rd ed.; Atlas: São Paulo, Spain, 2011; Available online: http://www.grupogen.com.br/fundamentos-gestao-projetos-23393 (accessed on 12 September 2017).

- Kivilä, J.; Martinsuo, M.; Vuorinen, L. Sustainable project management through project control in infrastructure projects. Int. J. Proj. Manag. 2017, 35, 1167–1183. [Google Scholar] [CrossRef]

- Silvius, A.J.G.; Schipper, R.; Nedeski, S. Sustainability in project management: Reality bites 1. PM World J. 2013, 2, 1–14. [Google Scholar]

- Silvius, G. Sustainability as a new school of thought in project management. J. Clean. Prod. 2017, 166, 1479–1493. [Google Scholar] [CrossRef]

- Dellas, E. CSD water partnerships: Privatization, participation and legitimacy. Ecol. Econ. 2011, 70, 1916–1923. [Google Scholar] [CrossRef]

- Schmidt-Traub, G.; Sachs, J.D. Financing Sustainable Development: Implementing the SDGs through Effective Investment Strategies and Partnerships; Sustainable Development Solution Network Working Paper. 2015. Available online: http://Unsdsn. Org/Wp-Content/Uploads/2015/04/150619-SDSN-Financing-Sustainable-Development-Paper-FINAL-02.Pdf (accessed on 5 September 2017).

- Zhou, L.; Keivani, R.; Kurul, E. Sustainability performance measurement framework for PFI projects in the UK. J. Financ. Manag. Prop. Constr. 2013, 18, 232–250. [Google Scholar] [CrossRef]

- Estache, A.; Serebrisky, T.; Wren-Lewis, L. Financing infrastructure in developing countries. Oxf. Rev. Econ. Policy 2015, 31, 279–304. [Google Scholar] [CrossRef] [Green Version]

- Shan, M.; Hwang, B.-G.; Zhu, L. A Global Review of Sustainable Construction Project Financing: Policies, Practices, and Research Efforts. Sustainability 2017, 9, 2347. [Google Scholar] [CrossRef]

- Mowery, D.C.; Nelson, R.R.; Martin, B.R. Technology policy and global warming: Why new policy models are needed (or why putting new wine in old bottles won’t work). Res. Policy 2010, 39, 1011–1023. [Google Scholar] [CrossRef]

- Gatti, S. Project Finance in Theory and Practice: Designing, Structuring, and Financing Private and Public Projects, 3rd ed.; Elsevier: London, UK, 2018. [Google Scholar]

- Pardo-Bosch, F.; Aguado, A. Sustainability as the key to prioritize investments in public infrastructures. Environ. Impact Assess. Rev. 2016, 60, 40–51. [Google Scholar] [CrossRef]

- Baietti, A.; Shlyakhtenko, A.; la Rocca, R.; Patel, U.D. Green Infrastructure Finance: Leading Initiatives and Research; World Bank: Washington, DC, USA, 2012; Available online: https://openknowledge.worldbank.org/handle/10986/13142 (accessed on 4 May 2017).

- Gouldson, A.; Kerr, N.; Millward-Hopkins, J.; Freeman, M.C.; Topi, C.; Sullivan, R. Innovative financing models for low carbon transitions: Exploring the case for revolving funds for domestic energy efficiency programmes. Energy Policy 2015, 86, 739–748. [Google Scholar] [CrossRef] [Green Version]

- González, J. La financiación de la colaboración público-privada: El «Project Finance». Presup. y Gasto Público 2006, 45, 175–185. Available online: http://www.ief.es/documentos/recursos/publicaciones/revistas/presu_gasto_publico/45_Financiacion.pdf (accessed on 5 May 2017).

- Esty, B. Big Deals: Financing Large-Scale Investments; Working Knowledge A Report Resarch; Harvard Business School: Boston, MA, USA, 2000; Volume IV, Available online: http://hbswk.hbs.edu/item/1690.html (accessed on 4 May 2017).

- Kwak, Y.H.; Chih, Y.; Ibbs, C.W. Towards a Comprehensive Understanding of Public Private Partnerships for Infrastructure Development. Calif. Manag. Rev. 2009, 51, 51–78. [Google Scholar] [CrossRef]

- Akintoye, A.; Beck, M. Policy, Finance & Management for Public-Private Partnerships, 1st ed.; Wiley-Blackwell: Oxford, UK, 2009. [Google Scholar]

- Croce, R.; Gatti, S. Financing infrastructure—International trends. OECD J. Financ. Mark. Trends 2014, 2014, 123–138. [Google Scholar] [CrossRef]

- Nijs, L. Mezzanine Financing—Tools, Applications and Total Performance; Wiley Finance: West Sussex, UK, 2014; ISBN 978-1-118-76520-3. [Google Scholar]

- Mascareñas, J. Fusiones, Adquisiciones y Valoración de Empresas, 5st ed.; Ecobook: Madrid, Spain, 2011; ISBN 978-84-96877-45-0. [Google Scholar]

- Fernández-Sánchez, G.; Rodríguez-López, F. A methodology to identify sustainability indicators in construction project management—Application to infrastructure projects in Spain. Ecol. Indic. 2010, 10, 1193–1201. [Google Scholar] [CrossRef]

- Poveda, C.A.; Lipsett, M. A Review of Sustainability Assessment and Sustainability/Environmental Rating Systems and Credit Weighting Tools. J. Sustain. Dev. 2011, 4, 36. [Google Scholar] [CrossRef]

- Rodríguez, F.; Fernández, G. Challenges for Sustainability Assessment by Indicators. Leadersh. Manag. Eng. 2011, 11, 321–325. [Google Scholar] [CrossRef]

- Barbero, J. La Infraestructura en el Desarrollo integral de América Latina. Diagnóstico Estratégico y Propuestas para una Agenda Prioritaria; CAF: Bogotá, Colombia, 2011; Volume 132. [Google Scholar]

- Modigliani, M.; Miller, M. The Cost of Capital, Corporation Finance and The Theory of Investment. Am. Econ. Rev. 1958, 48, 261–297. Available online: https://doi.org/http://www.jstor.org/stable/1809766 (accessed on 3 September 2017).

- Dong, F.; Chiara, N.; Kokkaew, N.; Wu, J. Stochastic Optimization of Capital Structure in Privately Funded Infrastructure Projects. J. Priv. Equity 2011, 15, 36–47. [Google Scholar] [CrossRef]

- Kleimeier, S.; Versteeg, R. Project finance as a driver of economic growth in low-income countries. Rev. Financ. Econ. 2010, 19, 49–59. [Google Scholar] [CrossRef] [Green Version]

- Girardone, C.; Snaith, S. Project finance loan spreads and disaggregated political risk. Appl. Financ. Econ. 2011, 21, 1725–1734. [Google Scholar] [CrossRef]

- Duque, E.A.; González, J.D.; Restrepo, J.C. Developing Sustainable Infrastructure for Small Hydro Power Plants through Clean Development Mechanisms in Colombia. Procedia Eng. 2016, 145, 224–233. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Author/Element | Green Financial Innovation | Creation of a New Market, Product, Process or Service | Processes of Innovation towards the Sustainable Development |

|---|---|---|---|

| [6] | x | x | x |

| [5] | x | x | |

| [37] | x | x | x |

| [38] | x | x | |

| [39] | x | ||

| [17] | x | x | |

| [40] | x | x | |

| [41] | x | x |

| Description | Authors |

|---|---|

| Based on a theoretical example, he demonstrates that using mezzanine debt as a financing source, it is possible to improve ROE. | [9] |

| Emphasize that the consequences of better environmental performance should lead to a better forthcoming financial performance reflected in the ROA and the Operational Cash Flow, as well as in a higher value of the firm measured by Enterprise Value. Also, they demonstrated that good environmental performance reduces regulatory risks. Therefore, this affects directly corporate valuation through a lower discount rate. | [45] |

| Investors may opt for cheaper Capital Expenditures (Capex) in exchange for higher long-term Operating Expenditures (Opex). As a result, the initial higher costs required to implement sustainability practices may negatively affect the short-term Return on Investment (ROI) thereby discouraging decision makers from adopting such methods. | [56] |

| Green benefits derived from sustainable financing are incorporated in the calculation of the WACC. | [57] |

| He provided a theoretical foundation for amending the discount rates currently used for project analysis to account for the social and environmental aspects of business operations and investments. | [58] |

| Barrier | Instrument | Authors |

|---|---|---|

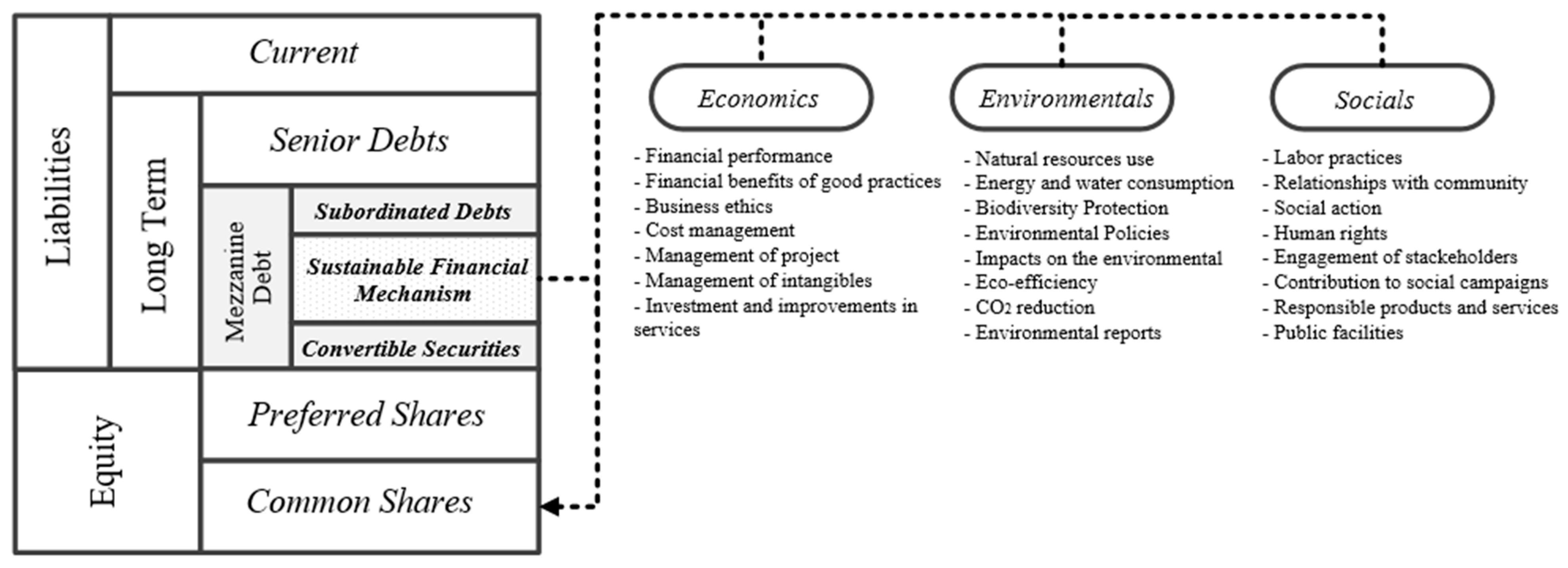

| Associativity | Public-Private Partnerships (PPPs) and Project Finance (PF) | [41,63,64] |

| Investment in Research and Development | Tax credits | [57,65] |

| Institutional weakness | Regulation | [64] |

| Capital market development | Development of financing mechanisms. Expand the base of issuers | [41,62,63,66,67] |

| Funding sources | Private equity funds, Angeles Investors, Banks, PF, Mezzanine, | [41,60,63,68,69,70] |

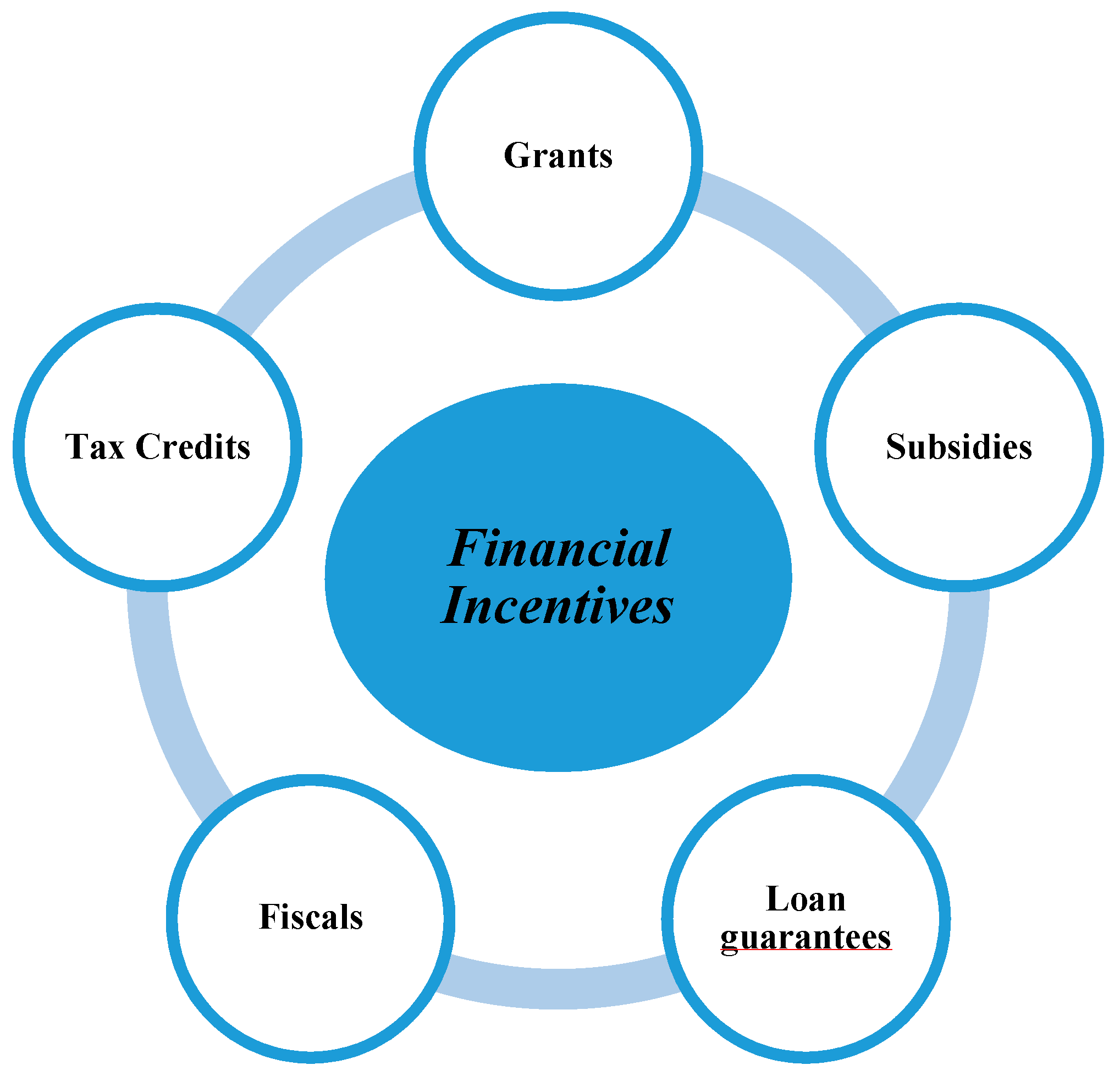

| Early entrant investors | Tax incentives, foreign exchange liquidity facilities, loan guarantees, and subsidies, technical infrastructure and information provision, and PPPs through fiscal tools, such as risk transfers, insurance, and equities | [3,71] |

| Attracting sufficient funds | Governmental guarantees, Loan guarantees | [3,72] |

| Sector | ||||

|---|---|---|---|---|

| Taxes | Transportation | Building | Water/Waste | Energy |

| Fees and charges | Congestion charges High Parking fees Occupancy Toll Lanes | Building permits Property taxes | Tariffs and fees | Electricity user fees |

| Grants | General grants with environmental indicators, specific grants for environmental goods and services, matching grants. | |||

| PPPs | Concessions and Private Finance Initiatives (PFIs), energy performance contracts. | |||

| Land-based income | Development charges/impact fees, tax higher density building rights. | |||

| Loans and bonds | Loans and green bonds. | |||

| Carbon finance | Clean Development Mechanism/Joint Implementation, voluntary carbon offsets. | |||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

González-Ruiz, J.D.; Botero-Botero, S.; Duque-Grisales, E. Financial Eco-Innovation as a Mechanism for Fostering the Development of Sustainable Infrastructure Systems. Sustainability 2018, 10, 4463. https://doi.org/10.3390/su10124463

González-Ruiz JD, Botero-Botero S, Duque-Grisales E. Financial Eco-Innovation as a Mechanism for Fostering the Development of Sustainable Infrastructure Systems. Sustainability. 2018; 10(12):4463. https://doi.org/10.3390/su10124463

Chicago/Turabian StyleGonzález-Ruiz, Juan David, Sergio Botero-Botero, and Eduardo Duque-Grisales. 2018. "Financial Eco-Innovation as a Mechanism for Fostering the Development of Sustainable Infrastructure Systems" Sustainability 10, no. 12: 4463. https://doi.org/10.3390/su10124463

APA StyleGonzález-Ruiz, J. D., Botero-Botero, S., & Duque-Grisales, E. (2018). Financial Eco-Innovation as a Mechanism for Fostering the Development of Sustainable Infrastructure Systems. Sustainability, 10(12), 4463. https://doi.org/10.3390/su10124463